ABF: The Material Beneath the Model

How Ajinomoto’s obscure film became the standard layer inside advanced packaging, and why AI is turning a forgotten materials business into infrastructure.

TL;DR

ABF (Ajinomoto Build-up Film), is not “just packaging material”; it is the insulating layer that makes high-end organic substrates possible, and AI is driving far more ABF per chip through larger packages, more layers, and harsher yield economics.

The industry is structurally split: Ajinomoto sits upstream in a capital-light near-monopoly, while substrate makers operate a capital-heavy, qualification-bound oligopoly where only a few players can really serve AI-grade demand.

The market still mostly sees Ajinomoto as a food company, but the economics increasingly look like semiconductor infrastructure, and that mismatch is the heart of the thesis.

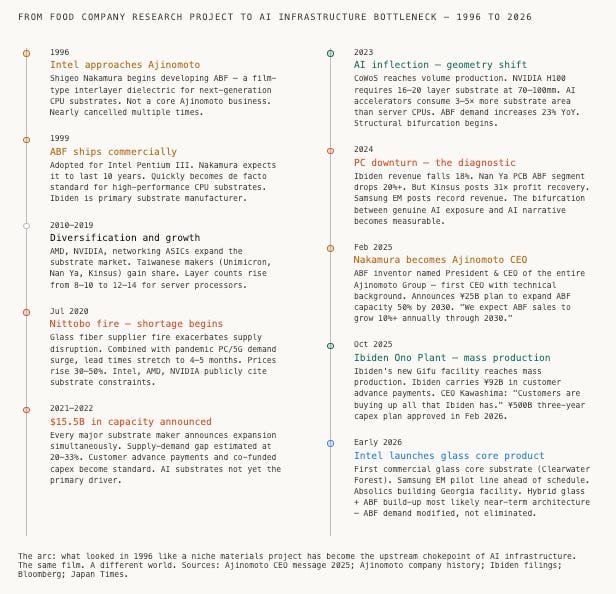

In 1996, a young researcher at Ajinomoto, the Japanese company that invented MSG, dominates global soy sauce markets, and sells seasoning packets in 130 countries, was handed an unusual assignment. Intel needed a better insulating film for its next-generation CPU substrates. The materials it was using were inconsistent, difficult to process uniformly, and insufficient for the routing density the Pentium III would require. What Intel needed was a thermosetting film that could be laminated uniformly onto circuit panels, survive laser drilling at microscopic scales, support copper plating in semi-additive processes, and do all of this reliably across millions of packages.

The researcher was Shigeo Nakamura. He had joined Ajinomoto’s Central Research Laboratory four years earlier, drawn to fermentation chemistry and materials science, working in what the company then described as an “emerging business segment.” Electronic materials was not Ajinomoto’s core business. It was not obvious it ever would be.

“In 1996, we started development of Ajinomoto Build-up Film,” Nakamura wrote in his CEO message for 2025. “Along the way, we faced many crises of survival, as it was not a core business, but I devoted myself to research and development due to the tenacity of my superiors and a pride-based sense of urgency making me unwilling to let the research end so unceremoniously.”

The film shipped commercially in 1999 for the Pentium III. When it was adopted, Nakamura assumed it might stay in production for ten years. It has now been over twenty, and ABF is still going strong.

Nobody outside the packaging industry noticed at the time. No analyst note captured the significance. A food company had quietly become the upstream supplier to the entire high-performance computing industry, and it had done so not through acquisition or grand strategy, but through one researcher who refused to let an obscure materials project die.

On February 3, 2025, Ajinomoto named Nakamura as President and CEO of the entire Ajinomoto Group, noting that he had “led the launch and growth of the Electronic Material business centering on Ajinomoto Build-up Film.” He became, as his official biography records, the Ajinomoto Group’s first CEO with a technical background.

That promotion is the tell. When the inventor of your most strategically important product becomes group CEO, not of the electronics subsidiary, not of the materials division, but of the whole company, the organization is communicating something about where its center of gravity is moving. But to understand why it matters specifically now, in 2026, you have to start not with Ajinomoto but with what AI has done to the substrate underneath every chip it powers, and why that shift is forcing a rerating of an entire supply chain that most investors still price as a commodity cyclical.

The Package Became the Problem

The standard frame for the semiconductor supply chain puts the interesting action on the die. Transistors scale. TSMC builds them smaller. Performance improves. The chip ships. Packaging is plumbing, necessary, unglamorous, and strategically peripheral.

That frame was largely correct through the PC era. It is wrong now and understanding why is the key to understanding everything that follows.

For fifty years, Moore’s Law delivered performance by shrinking transistors. That scaling has slowed, not stopped, but slowed enough that the industry has had to find performance elsewhere. The answer, increasingly, is the package itself. AI systems gain performance today not primarily by making the die smaller, but by integrating more compute dies together on one package, stacking high-bandwidth memory directly beside them, and connecting everything through increasingly sophisticated interconnect structures. The package, in other words, has moved from plumbing to compute infrastructure. It is now part of the scaling curve.

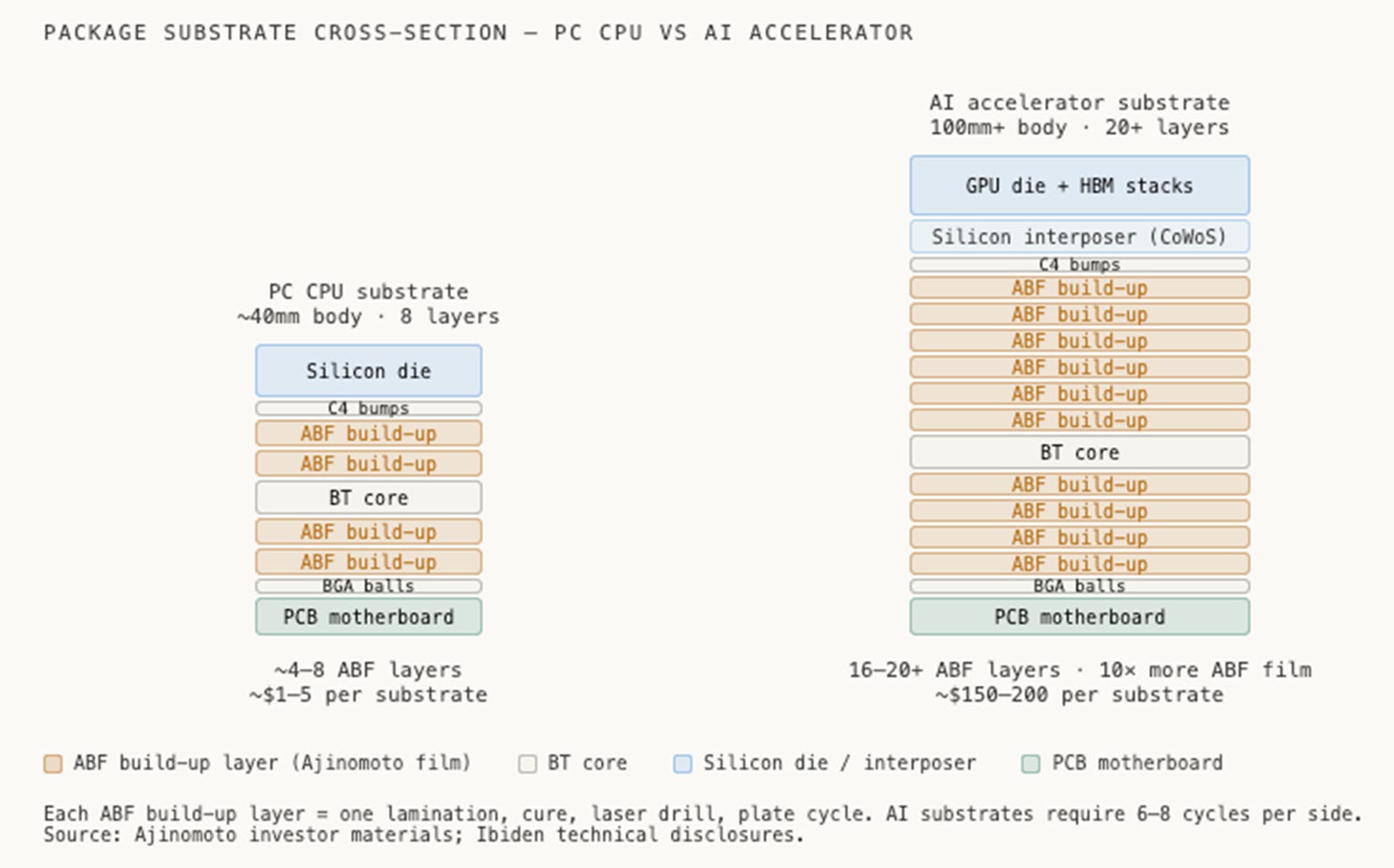

This shift has a specific material consequence. Every routing layer inside a high-performance substrate, every insulating layer that separates copper traces, allows laser-drilled microvias to connect one layer to the next, and maintains electrical integrity at multi-gigahertz frequencies, is built from ABF. The film is laminated, cured, drilled, and plated, then the cycle repeats for every additional layer the package requires. A substrate for a PC CPU might go through that cycle six times. A substrate for a current-generation AI accelerator goes through it eighteen times or more.

That difference is not incremental. It represents a completely different business.

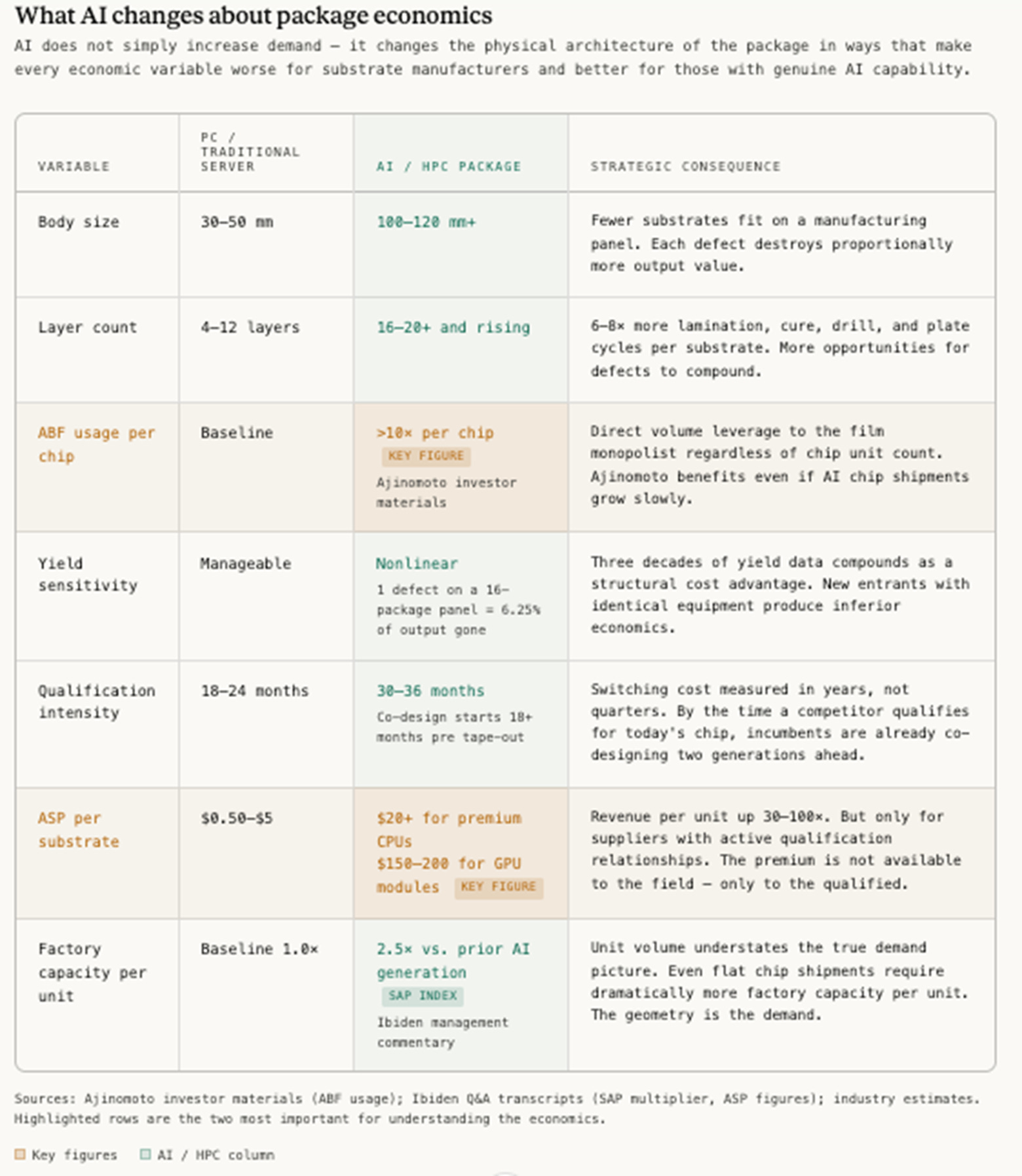

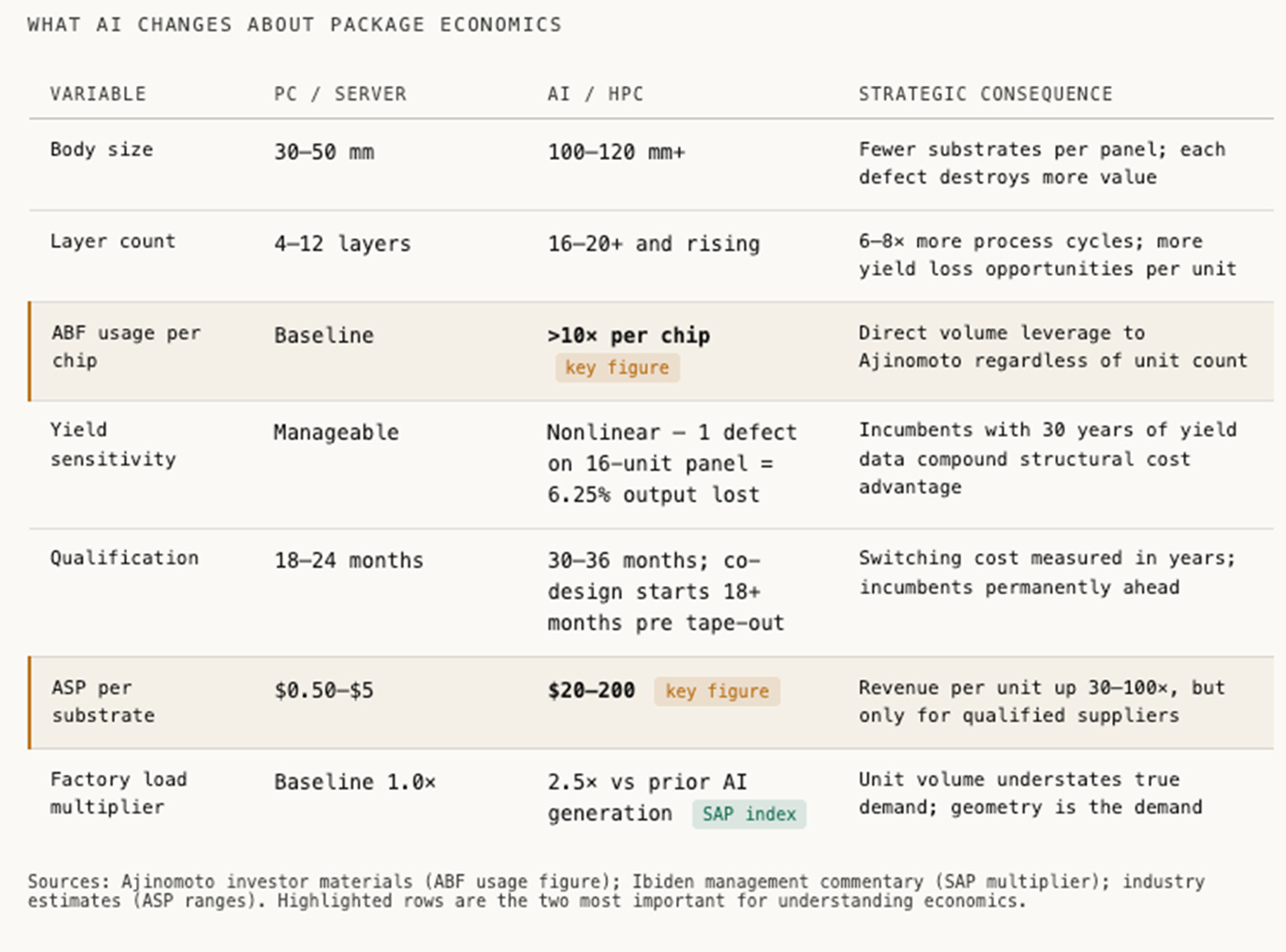

What AI Changes About Package Economics

Unimicron chairman Tzyy-Jang Tseng has noted that substrate areas for CoWoS technology have grown more than ten times. That statement is worth sitting with. The substrate under an AI accelerator is not a bigger version of a PC substrate. It is a categorically different product, more layers, larger body, tighter tolerances, harsher yield economics, that happens to use the same insulating film and similar equipment. A company that makes six-layer PC substrates is not in the same business as a company making twenty-layer AI substrates. They share an industry name. They do not share an economics.

This is where the market has been making its central error. The ABF substrate industry is not a single market that AI has made better for everyone. It is two markets, advanced AI substrates with pricing power and structural scarcity, and commodity PC substrates with overcapacity and margin pressure, that share branding and some equipment but have diverged completely in economics. Understanding which tier each company actually operates in is the only thing that matters for understanding who benefits from the structural shift and who doesn’t.

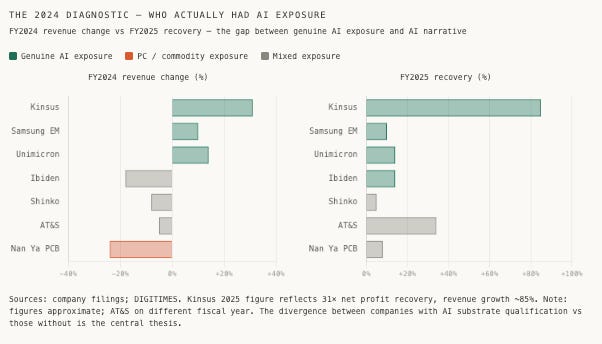

The 2024 semiconductor downturn was the clearest diagnostic event in recent sector history, and most analysis drew the wrong conclusion from it. When Ibiden’s revenue fell eighteen percent and Nan Ya PCB’s ABF segment dropped more than twenty percent, the conventional read was that AI substrate demand was softer than expected. The better read is almost the opposite: the companies with genuine AI substrate exposure held; the companies with AI narratives, still largely PC businesses with AI stories bolted on, were exposed by PC overcapacity hitting their core business. Kinsus, which had concentrated its advanced lines on AI clients, achieved a thirty-one times profit recovery in 2025. Samsung Electro-Mechanics posted record annual revenue of KRW 11.3 trillion. AI-powered applications reshaped the electronics manufacturing landscape in 2024, with Unimicron and Kinsus posting double-digit revenue growth, while Nan Ya PCB struggled. The bifurcation was not a temporary anomaly. It is the permanent structure of the industry.

Monopoly Chemistry, Oligopoly Manufacturing

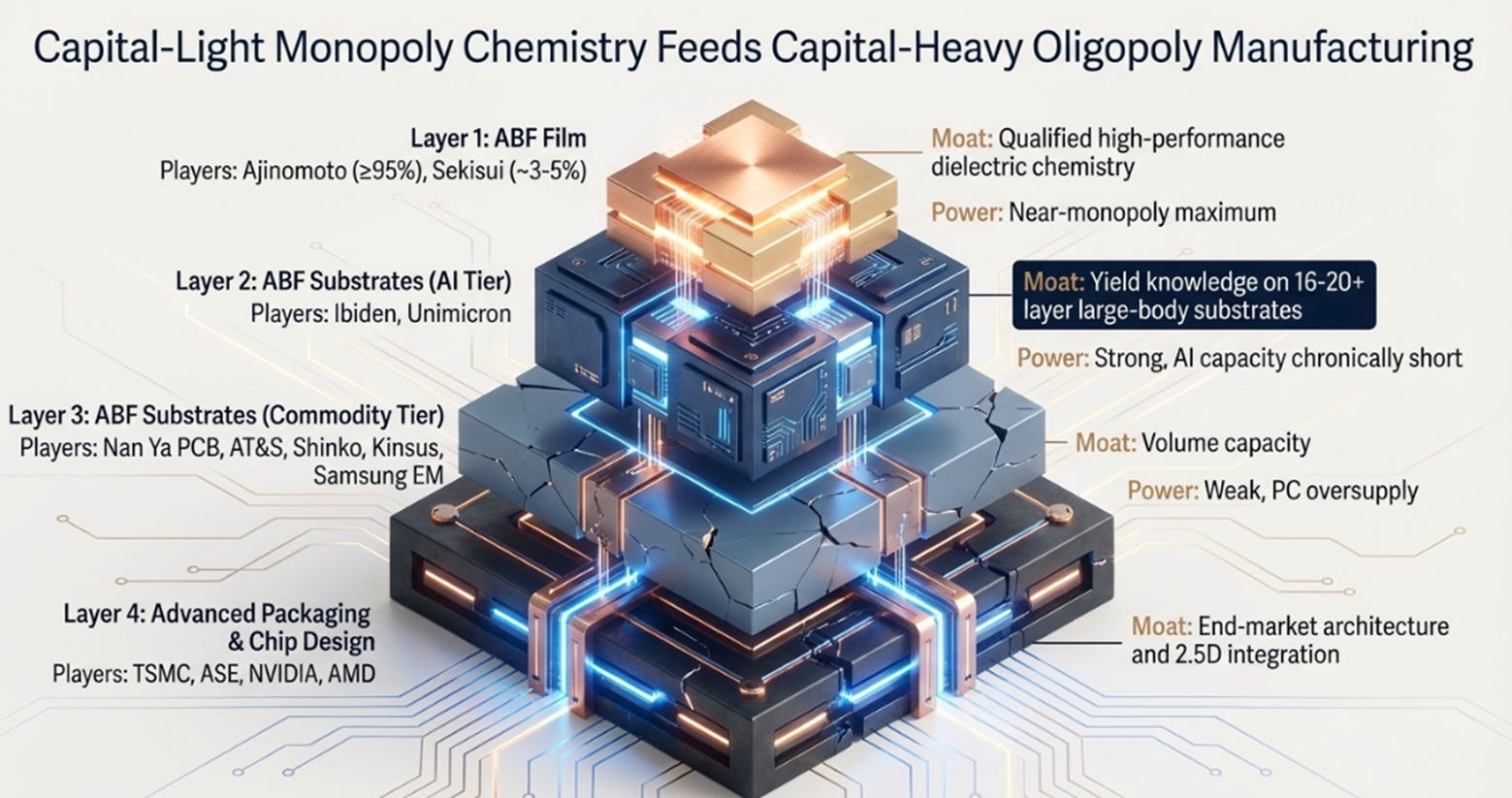

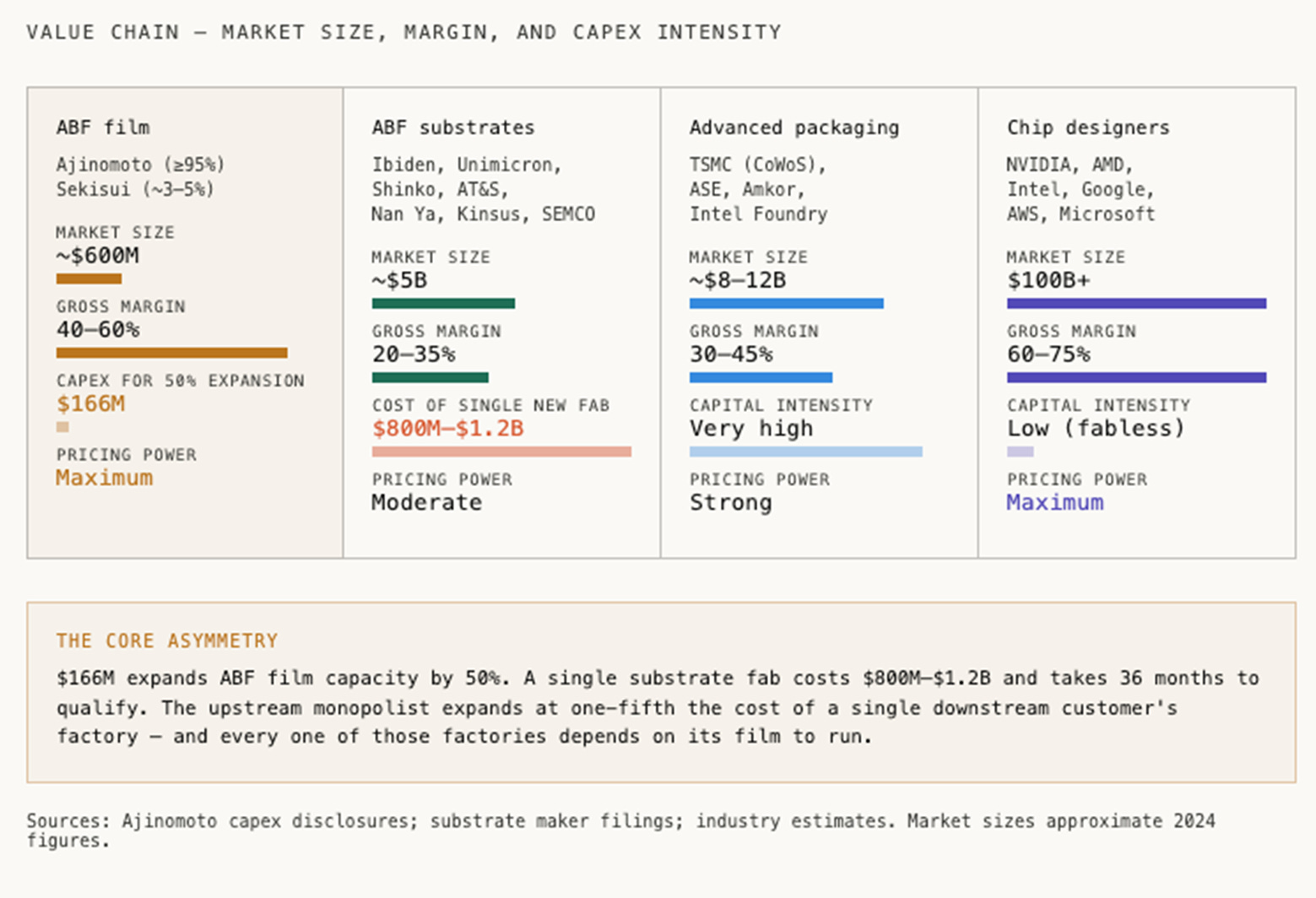

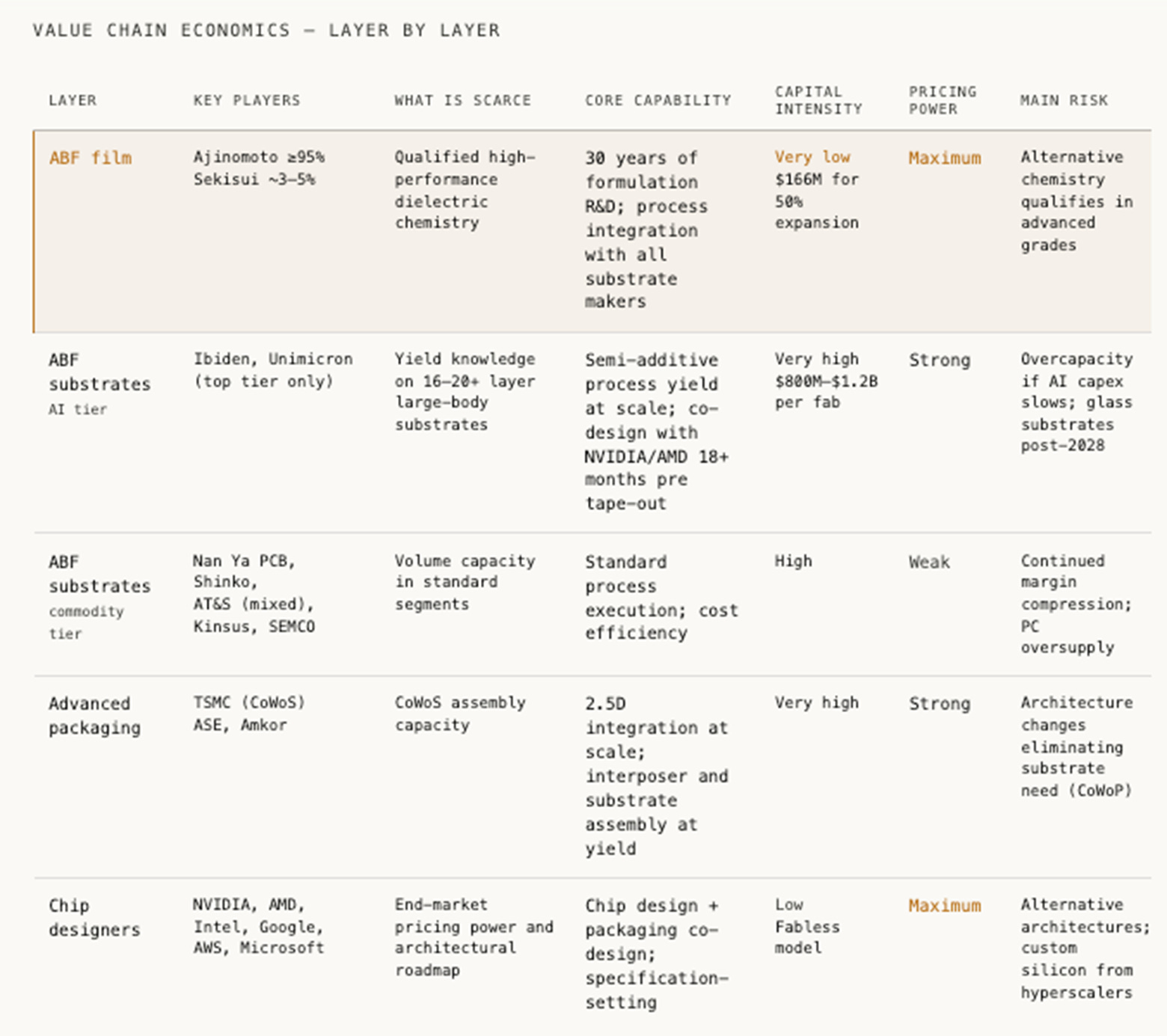

Before you can understand the substrate makers, you have to separate two things the industry routinely conflates: ABF film and ABF substrates. They have different competitive structures, different capital requirements, and completely different economic outcomes. Conflating them is how most coverage of this sector goes wrong from the first paragraph.

ABF film is Ajinomoto’s product. It is a thermosetting composite, epoxy resin, hardener, silica filler, delivered in rolls to substrate manufacturers worldwide. Ajinomoto’s market share in high-performance CPU and GPU substrate grades: above ninety-five percent. Sekisui Chemical, its nearest competitor, holds a few percent in lower-end applications and has not credibly challenged Ajinomoto’s advanced grade position in over two decades of trying.

“We expect sales of electronics materials, mainly ABF, to grow at an annual rate of more than 10% through 2030,” Nakamura told Nikkei Asia. “We will invest the same amount or more by 2030 as demand increases.” The investment required to achieve this: a ¥25 billion, approximately $166 million, plan to grow ABF production capacity by fifty percent by 2030.

ABF substrates are a completely different business. Seven manufacturers convert Ajinomoto’s film into the finished packages that sit under every AI chip. Their capital requirements: $800 million to $1.2 billion per new fab. Their qualification timeline: thirty to thirty-six months before a single revenue-generating substrate ships. Their gross margins: decent when utilization is high and product mix skews AI, brutal when it doesn’t.

The asymmetry in this table is the industry in miniature. $166 million buys a fifty percent expansion in the film that every downstream business depends on. $800 million to $1.2 billion buys a single substrate fab that still needs three years to qualify before shipping revenue. The film monopolist expands at one-fifth the cost of a single downstream factory, and every one of those factories depends on its film allocation to run.

This is the structure: capital-light monopoly chemistry feeding capital-heavy oligopoly manufacturing. Ajinomoto is not a supplier in the conventional sense. It controls the standard layer on which the rest of the industry runs, and it does so with pricing power, minimal competitive pressure, and capital requirements that barely register against the businesses downstream. As of today, no U.S. entity manufactures ABF or has secured licensing rights, making the United States entirely import-dependent on a material essential for advanced semiconductors. That is not a supply chain vulnerability that announced itself loudly. It accumulated quietly, one qualified substrate generation at a time, while everyone was watching the chip companies.

Qualification, Not Capacity, Is the Real Moat

The lazy frame for the ABF substrate supply situation is: everyone is expanding, so the shortage should ease. More than $15.5 billion in substrate capacity was announced industry-wide in 2021 and 2022. Ibiden committed ¥500 billion, roughly $3.3 billion, over three years. Unimicron raised its 2026 annual capex to a record NT$34 billion. AT&S has invested more than €2.5 billion across three continents.

The better frame: announced capacity and real supply are completely different things, separated by thirty-six months and a yield learning curve that no amount of money can compress.

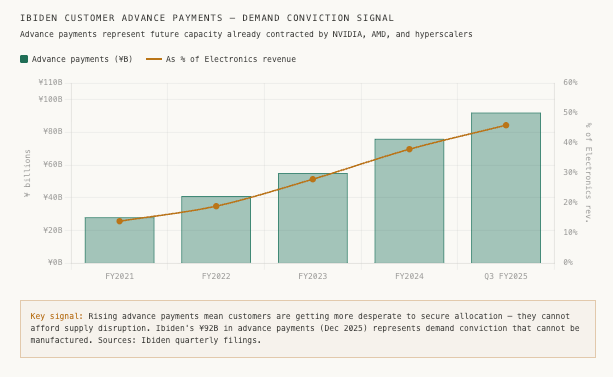

Bloomberg reported that Ibiden CEO Koji Kawashima said sales of the company’s AI-use substrates are “robust with customers buying up all that Ibiden has,” with demand likely to last at least through the following year. “Our customers have concerns,” Kawashima told reporters. “We’re already being asked about our next investment and the next capacity expansion.”

That language, customers asking about the investment after next, reveals the fundamental structure of competition in this industry. The qualification cycle is so long that customers who want substrate supply in 2028 are negotiating factory commitments in 2025. The production timeline and the demand timeline are separated by years, and the sophisticated customer knows it. This is precisely why Ibiden carries ¥92 billion in customer advance payments, not as a balance sheet metric but as a demand conviction signal. When NVIDIA pre-pays for substrate capacity years before the substrate ships, it has calculated that supply disruption is worse than paying above-market prices today.

Toyo Securities analyst Hideki Yasuda stated the competitive reality plainly after assessing the field: “Nvidia’s AI chips need sophisticated substrates, and Ibiden is the only one that can mass produce them at a good production yield.”

Not the largest. Not the most capital-invested. The only one that can mass produce at good yield. Yield is the moat, and yield is accumulated over decades of production runs, refined through failure analysis, embedded in proprietary chemical recipes, plating parameters, and laser settings that are not disclosed and cannot be transferred. A competitor with identical equipment and unlimited capital still needs years to match the yield curve of an incumbent with thirty years of process history on the specific substrate type in question.

The customer co-investment structure makes this explicit. Intel, AMD, and NVIDIA have collectively subsidized approximately fifty percent of expansion capex at their top substrate suppliers. This is not generosity. It is a revealed preference about irreplaceability. When a company with NVIDIA’s pricing power decides the correct move is to pre-fund a substrate manufacturer’s factory, they have revealed that a financially weak or supply-constrained substrate maker is worse for them than overpaying for guaranteed allocation today.

This also explains why more announced capex does not automatically tighten the supply picture for everyone. AT&S has invested over €2.5 billion in substrate capacity. That investment is real. But AT&S’s ability to capture AI substrate economics is constrained by AMD customer concentration above seventy-seven percent of Americas revenue, €1.3 billion in net debt, a sub-twenty percent equity ratio, and three top executives replaced within twelve months during a critical ramp period. Capital deployed is not the same as qualification achieved. The distance between those two things is where most analysis of this sector goes wrong.

A Market That Does Not Lift All Boats

The seven substrate makers are not in the same business, and AI has made them less equal over time, not more. The bifurcation is not a temporary divergence that supply normalization will correct. It is the permanent structure of the industry, driven by yield economics and qualification depth that compound with every generation.

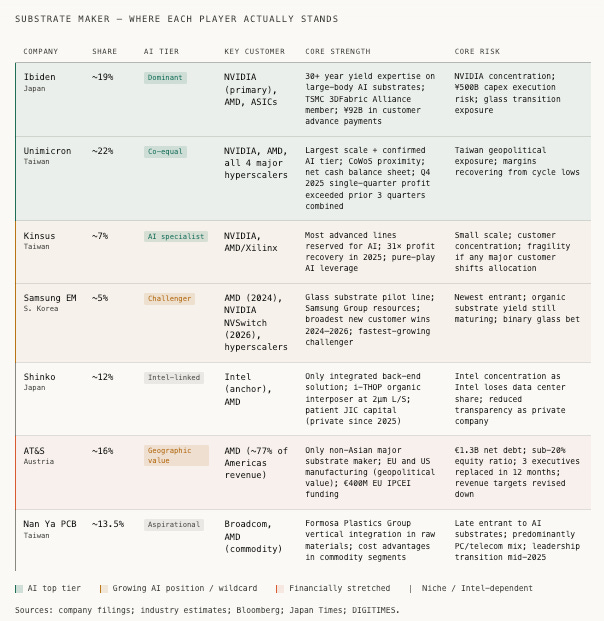

Where Each Player Actually Stands

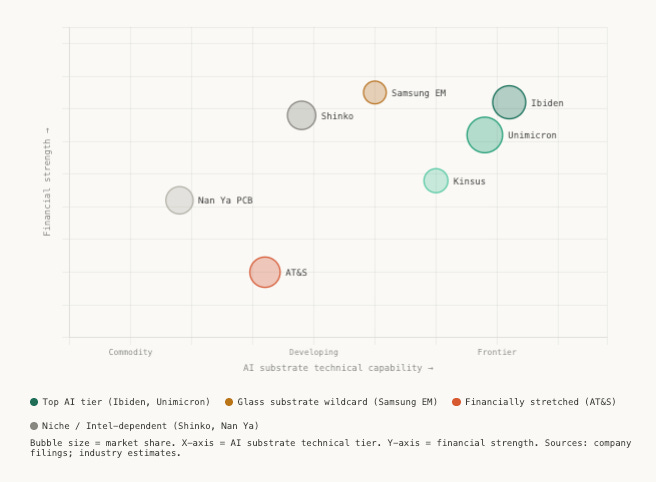

Ibiden and Unimicron form the genuine top tier, and the gap between them and the rest is wider than market share numbers suggest. Industry observers describe the two as operating in a “quiet duopoly” in one of the most strategically critical segments of the semiconductor supply chain, as the only suppliers capable of manufacturing the most advanced ABF substrates that AI accelerators require. Every other substrate maker is competing for secondary position, commodity volume, or a specific niche that may or may not grow.

Kinsus deserves more attention than its seven percent market share implies. It is the purest AI-leverage play in the group, not because it is the most technically capable, but because it has concentrated its most advanced production lines almost entirely on AI clients. The thirty-one times profit recovery in 2025 is the clearest financial expression of what happens when a substrate maker successfully makes the move from PC exposure to AI exposure. The risk is the mirror image of the opportunity: that level of concentration creates fragility if any major customer shifts allocation.

Samsung Electro-Mechanics is the highest-variance name. It is the newest entrant in high-performance server substrates, mass production started only in October 2022, yet it has secured supply relationships with AMD, NVIDIA’s NVSwitch product line, and multiple hyperscalers within eighteen months. Samsung Electro-Mechanics has accelerated its glass substrate timeline, moving equipment procurement and installation to September and launching a pilot production line a full quarter ahead of schedule, with expectations of producing glass substrates for high-end applications in 2026. If glass cores reach meaningful volume after 2027 and Samsung is the only substrate maker with production-ready glass capability at scale, the thirty years of organic substrate yield expertise that Ibiden has accumulated becomes less relevant than its absence of glass substrate expertise. That is a binary outcome, either Samsung leapfrogs the field or it has split its resources between two substrate technologies while incumbents concentrated entirely on one.

AT&S is where the geopolitical diversification narrative and the financial reality are most in tension. The company is genuinely the only non-Asian major substrate maker. That is strategically valuable for Western chip companies with supply chain concerns. But strategic value and investment value are not the same thing when the balance sheet carrying that value has €1.3 billion in net debt, revenue targets that have been revised materially downward, and customer concentration in a single client navigating a difficult market. The bull case requires AMD to win in AI accelerators at scale. That remains an open question.

What Could Actually Break This Structure

Three things could disrupt the current dynamics. Only one is imminent.

The most-discussed threat is glass core substrates. Glass offers real advantages: near-zero coefficient of thermal expansion matching silicon, elimination of warpage in packages exceeding 100mm, and theoretical interconnect density improvements of up to ten times. Intel launched the first commercial glass core product in early 2026. Samsung Electro-Mechanics is aiming for mass production as early as 2026, potentially challenging Intel’s first-mover advantage, while TSMC is integrating glass into its CoWoS ecosystem through a new variant called CoPoS.

The sobering counterpoint: glass substrates currently cost two to three times organic equivalents, manufacturing yields remain at seventy-five to eighty-five percent versus organic substrates’ ninety to ninety-five percent, and brittleness requires specialized handling automation that the industry is still developing. Mass production readiness is unproven. The most likely near-term outcome is a hybrid architecture, glass core with ABF build-up layers, which benefits Ajinomoto: glass cores don’t compete with ABF build-up layers, they add a new substrate component while ABF remains the build-up dielectric. The company most vulnerable to full glass displacement is Ibiden, whose moat is entirely built on organic substrate yield expertise. The company best positioned to benefit is Samsung Electro-Mechanics, for precisely the opposite reason.

The geopolitical risk is less discussed but more immediately material. Eighty percent of Japanese container traffic transits the Taiwan Strait, while China is rapidly investing in alternatives to reduce its dependence on Ajinomoto’s product. Over forty-five percent of substrate production sits in Taiwan. The CHIPS Act investments, Ibiden’s Arizona fab, AT&S’s Texas facility, are real, but meaningful US capacity is 2028 at the earliest. Until then, the supply chain’s geographic concentration is essentially unchanged.

The demand risk that matters most in the near term is a hyperscaler capex pause. AI infrastructure spending is discretionary in a way that smartphone components are not. The advance payment structure is the best available leading indicator of demand conviction, and it is currently rising. But it has risen for only two years, through a period of extraordinary AI investment enthusiasm. The AI infrastructure buildout has not yet been tested through a full economic cycle.

The Category Error Nobody Has Named Yet

Here are the numbers the market has not yet fully processed.

Ajinomoto’s total annual revenue is approximately ten billion dollars. ABF film revenue is approximately $570 million, five to six percent of total group revenue. The functional materials segment containing ABF generates an estimated twenty percent of total group profit. Nakamura has set a target for electronics materials sales to grow at more than ten percent annually through 2030, with $166 million of capex buying a fifty percent capacity increase, at a time when a single substrate fab costs five to eight times that amount.

Five to six percent of revenue. Twenty percent of profit. One-fifth the capex cost of a single downstream customer’s factory. No credible challenger. Growing at double digits. Trading at food company multiples.

This is the same category error the market made with AWS inside Amazon’s retail reporting for years. The evidence was in the financials. The frame, Amazon is a retailer, was so established that the strategic significance of the cloud business was invisible to most investors until it became undeniable. Ajinomoto is a food company that controls the upstream material standard for advanced semiconductor packaging. Its most economically significant operation is a specialty chemicals monopoly generating near-monopoly margins on the insulating film inside every AI chip on earth. It is covered primarily by consumer staples analysts who model it on seasonings, frozen foods, and pharmaceutical ingredients.

The gap between those two descriptions is where the mispricing lives. And it is not unique to Ajinomoto. The broader substrate sector is being rerated from cyclical industrial to structural infrastructure, but not equally, and not all seven companies participate in that rerating. The market is beginning to recognize that Ibiden and Unimicron are not commodity manufacturers riding an AI demand wave. They are qualified infrastructure providers for a compute stack that has no near-term alternative. The qualification timeline, the advance payments, the co-design relationships, these are not just operational details. They are the mechanism by which what looks like a cyclical business is actually a structural one.

Unimicron’s single-quarter profit in Q4 2025 surpassed the combined total of the previous three quarters, that inflection is what a structural rerating looks like when it begins to show up in the financials.

Back to 1996

In 1999, when ABF first shipped commercially, Nakamura assumed it might stay in production for a decade. Twenty-six years later, every AI accelerator that powers the largest models in the world, every NVIDIA GPU, every AMD MI300X, every custom silicon chip that Google and Amazon and Microsoft run their most demanding workloads on, sits on a substrate built from his film.

“We expect sales of electronics materials, mainly ABF, to grow at an annual rate of more than 10% through 2030,” Nakamura said after taking the CEO role. “We will invest the same amount or more by 2030 as demand increases.”

He did not say: we will invest dramatically more. He said: the same amount or more. The monopolist at the top of the stack does not need to spend like the manufacturers below it. It needs only to expand its capacity modestly and let the geometry of AI packaging, more layers, larger bodies, ten times the film per chip, do the rest.

The question the market is slowly beginning to ask is whether the ABF substrate companies are commodity cyclicals or structural infrastructure. The answer, for the top tier, is the latter, and the evidence is in the advance payments, the qualification depth, and the co-design relationships that make switching suppliers a multi-year project rather than a procurement decision. Ibiden and Unimicron are not riding the AI wave. They are part of the physical architecture that the wave requires.

The harder question, the one the market has not yet asked, is what Ajinomoto actually is. The financials say semiconductor infrastructure. The valuation says food company. That gap closes eventually.

Thesis confirmation: Customer advance payments at Ibiden and Unimicron continue rising through 2026–2027 as the Gama Plant ramps, confirming AI demand conviction beyond the current cycle. Semiconductor analysts initiate standalone coverage of Ajinomoto’s functional materials business. Ajinomoto introduces separate segment reporting for electronics materials, signaling management is preparing to surface a valuation that the current conglomerate structure obscures.

Thesis break: Sekisui Chemical or a Chinese challenger successfully qualifies for high-performance ABF grades at a tier-one substrate maker by 2027, the first credible crack in a monopoly that has held for twenty-six years. Or hyperscaler AI capex guidance turns negative in consecutive quarters, unwinding the advance payment structures that currently underwrite ¥500 billion in expansion commitments across the industry.

In 1996, Nakamura was told to build something that probably wouldn’t last. He built it anyway. What he built, though neither he nor Intel fully understood it at the time, was the upstream standard for the physical infrastructure of modern compute. The food company running that standard won’t stay hidden forever.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.