Adobe 2QFY26 Earnings: The Abundance Paradox

We were right that AI would create more content. Q2 showed why turning that content into ARR is harder than we assumed.

TL;DR

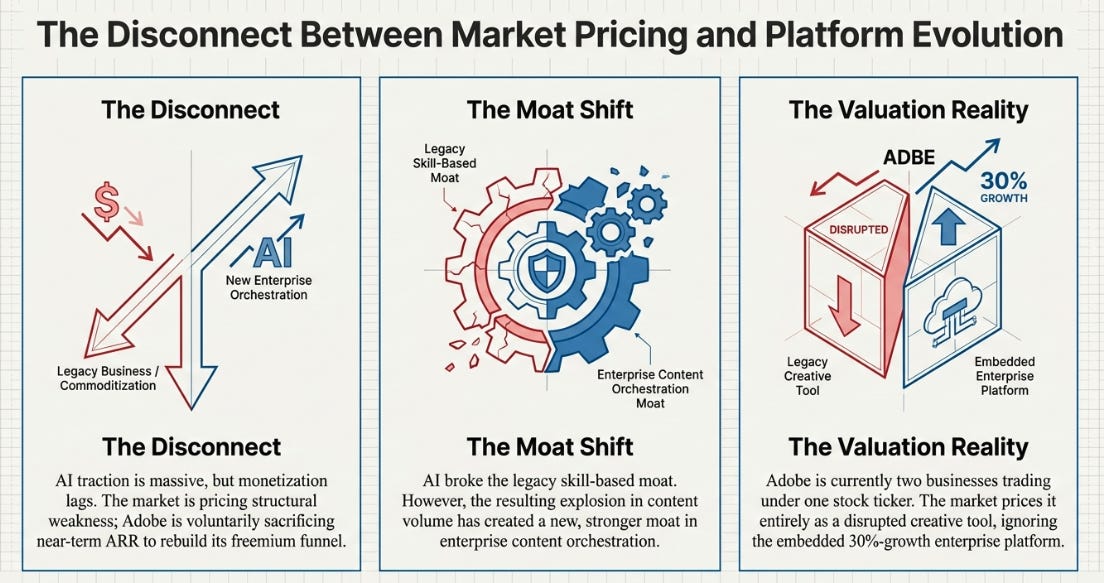

Adobe’s core issue is not lack of AI traction, but weak AI monetization: AI-first ARR, Firefly, GenStudio, enterprise adoption, and freemium usage are all growing strongly, yet organic ARR quality weakened because Adobe is sacrificing near-term paid conversion to rebuild its funnel around freemium.

AI has broken Adobe’s old moat while creating a new possible one: the traditional skill-based Creative Cloud moat is eroding as AI makes creation easier, but the same explosion in content strengthens Adobe’s opportunity in enterprise content operations, governance, workflow orchestration, personalization, and measurement.

The stock depends on whether the enterprise “orchestration loop” becomes visible and measurable: bulls need proof through organic ARR stabilization, freemium conversion data, sustained >20% enterprise CXO growth, margin resilience, and better segment transparency; until then, the market will keep valuing Adobe as a disrupted creative-tools business rather than a high-growth enterprise platform.

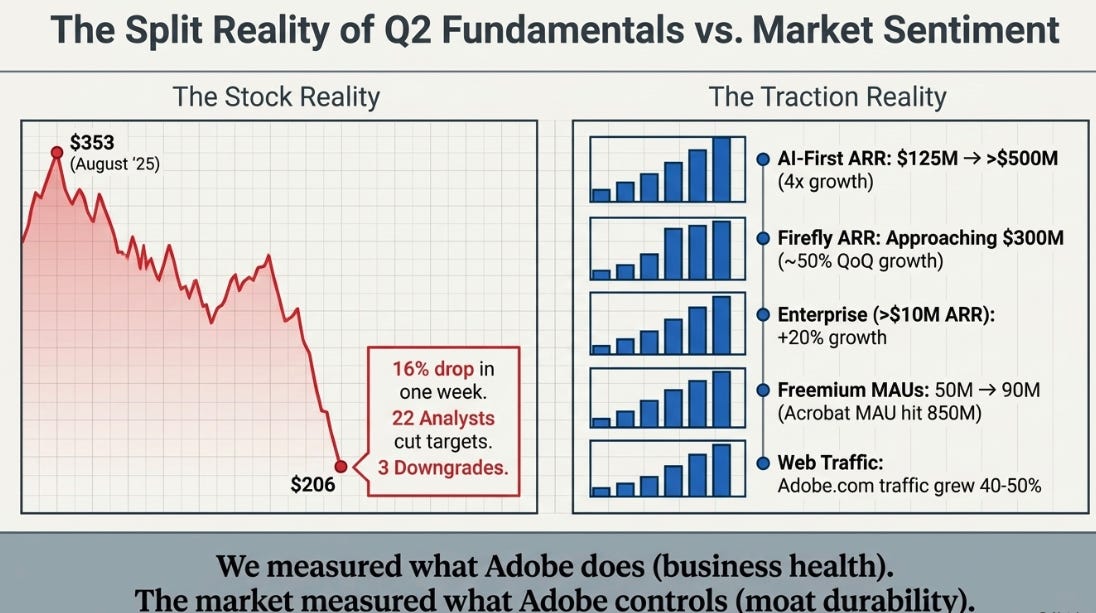

In August 2025 we wrote about Adobe at $353 and laid out three scenarios. Our most probable outcome, Disruption Realized, had a floor of $220. Ten months later, the stock is $206.

Most of the product and enterprise signposts we said to track have improved. AI-first ARR quadrupled from roughly $125 million to over $500 million. GenStudio ARR grew more than 25%. AEP and its native apps grew subscription revenue above 30%. Enterprise customers with more than $10 million in ARR grew over 20%. Firefly ARR is approaching $300 million. Traffic to Adobe.com grew 40-50%. Creative freemium monthly active users nearly doubled. In our September “Pixels to Pipelines” piece, we argued Adobe was becoming enterprise content infrastructure. The enterprise metrics have since exceeded the trajectory we needed to see.

The monetization signpost did not improve. Organic ARR quality weakened. The market’s most important measure, whether Adobe can convert AI traction into durable, direct-to-paid recurring revenue, moved in the wrong direction.

We were right about the fundamentals and wrong about the stock, because we did not anticipate that Adobe would voluntarily sacrifice near-term ARR to rebuild its acquisition funnel, and that the market would read that sacrifice as confirmation of structural weakness rather than evidence of strategic adaptation.

This is not a quarterly miss. It is a framework error. We were measuring what Adobe does. The market was measuring what Adobe controls. Those turned out to be different things. The distinction between the health of a business and the durability of its moat is the entire Adobe story right now, and it may be the most important structural lesson in technology investing: your numbers can improve while your structural power diminishes, and the market will price the power, not the numbers.

The Algorithm That Broke

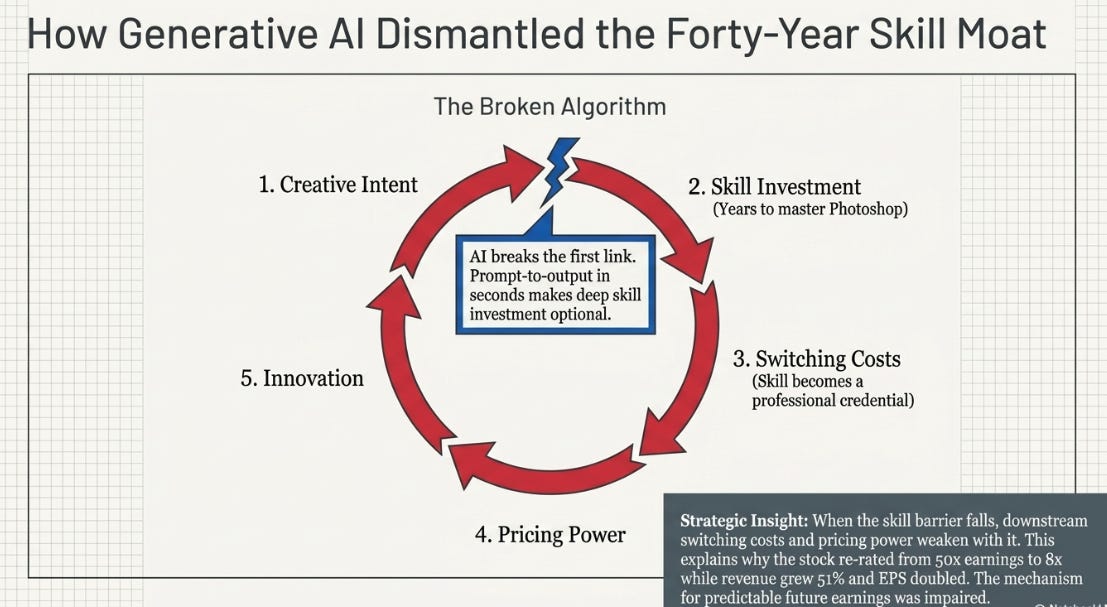

For forty years, Adobe ran one of the most elegant compounding algorithms in software. Creative intent led to skill investment. Skill investment created switching costs, learning Photoshop took years, and those years became a professional credential that made switching irrational. Switching costs created pricing power. Pricing power funded innovation. Innovation rewarded further skill investment. The cycle repeated for decades. It justified a premium multiple because each turn of the wheel made the next turn more certain.

AI broke the first link. When a user can describe what they want in a sentence and receive usable output in seconds, the skill investment that was Adobe’s deepest moat becomes optional. Not worthless, a retoucher finishing a luxury campaign still needs Photoshop’s precision. But optional for a rapidly expanding share of creative tasks. And when the skill barrier falls, everything downstream, the switching costs, the pricing power, the compounding certainty, weakens with it.

This is why the stock re-rated from 50x earnings to 8x while revenue grew 51% and EPS nearly doubled. The market is not saying Adobe’s current earnings are wrong. It is saying the mechanism that made future earnings predictable has been structurally impaired.

Critically, this is not a demand problem. More people want Adobe’s capabilities than at any point in the company’s history. Adobe.com traffic grew 40-50% in Q2. Creative freemium MAU went from 50 million to 90 million. Acrobat MAU hit 850 million. But users are arriving through a different door, intent-based search queries, LLM conversations, task-completion prompts, and that door does not have a cash register at the entrance.

Q2 confirmed this. Management said explicitly that traditional direct-to-paid journeys “may not always fulfill visitor intent,” that Adobe would rebalance traffic toward friction-free freemium experiences, and that this shift would cost near-term ARR. They deferred planned Creative Cloud price increases. They guided FY26 ARR growth to 10.2%, but that target now includes $480 million of acquired Semrush ARR, meaning organic ARR growth was cut roughly 200 basis points versus prior expectations.

The stock fell 16% in a week. Twenty-two analysts cut their price targets. Three downgraded. The market heard what it feared most: Adobe’s old monetization machine no longer maps cleanly onto how customers discover and adopt software in the AI era.

The Abundance Paradox

This is where most analyses stop, at the disruption narrative. But the disruption narrative, while partially correct, misses the structural paradox at the center of Adobe’s situation.

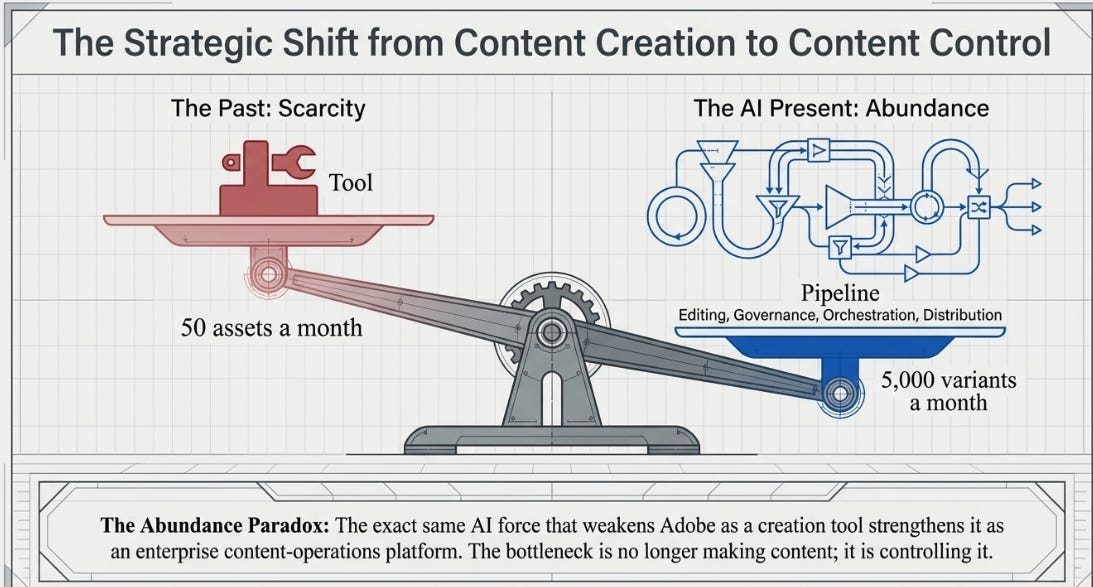

When creative output was scarce, the tool that produced it captured the value. Adobe owned the tool. When creative output becomes abundant, and AI is making it abundant at an extraordinary rate, value migrates away from creation and toward everything that happens after: editing, refinement, brand governance, rights management, workflow orchestration, personalization, distribution, and measurement. A marketing team that once produced fifty assets a month can now generate five thousand variants. The bottleneck is no longer making the content. It is controlling it.

This is the abundance paradox: the same AI force that weakens Adobe as a creation-tool provider strengthens Adobe as a content-operations platform. Both effects are real. Both are accelerating. The question, the only question that matters for the stock, is which one is larger.

Q2 provided evidence for both simultaneously.

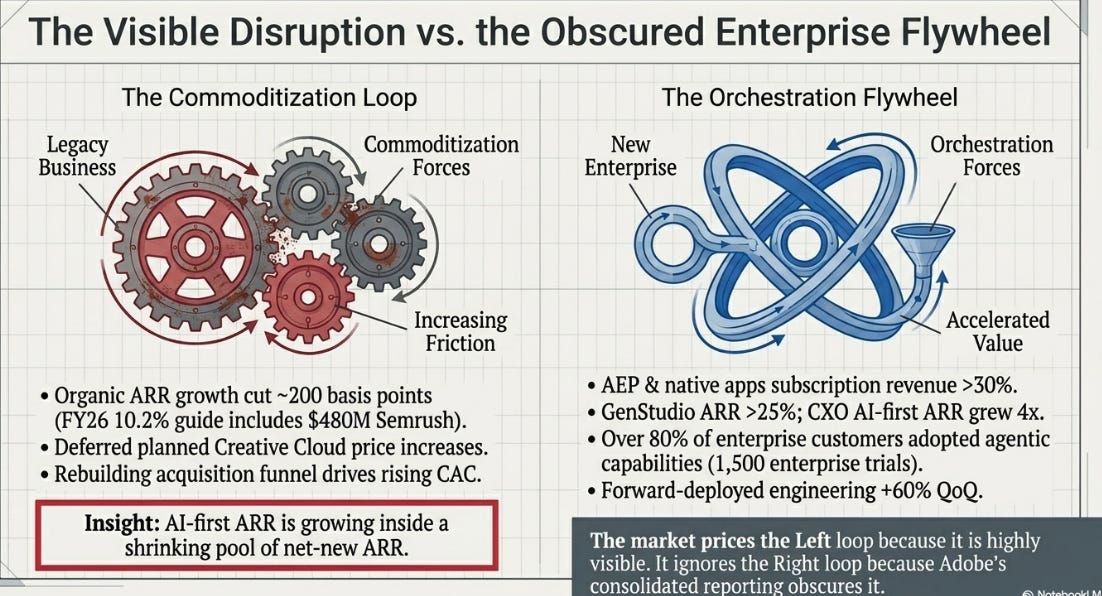

The commoditization loop is visible: management deferred pricing it had planned to take, rebuilt the acquisition funnel around freemium, and acknowledged rising customer acquisition costs. The uncomfortable arithmetic, even allowing for imprecision in how ARR categories are defined, is that AI-first ARR is growing inside a pool of total net-new ARR that is getting smaller, not larger. The new engine is building. It is not yet building fast enough to offset the pressure on the traditional engine. That is the single hardest data point for bulls to dismiss.

The orchestration flywheel is also visible: AEP and native apps grew subscription revenue above 30%. GenStudio ARR grew more than 25%. Customer Experience Orchestration AI-first ARR grew fourfold. Over 80% of enterprise customers adopted agentic capabilities. Fifteen hundred enterprises entered trials for agentic web products. CX Enterprise Coworker reached general availability with 150 enterprises in early adoption. Every major agency holding company standardized on Adobe. Forward-deployed engineering services grew 60% quarter-over-quarter.

The market is pricing the first loop because it is visible and frightening. It is largely ignoring the second because Adobe consolidated its reporting segments into a single unit, at the worst possible time, making it impossible for analysts to value the enterprise platform independently.

Two Businesses, One Stock

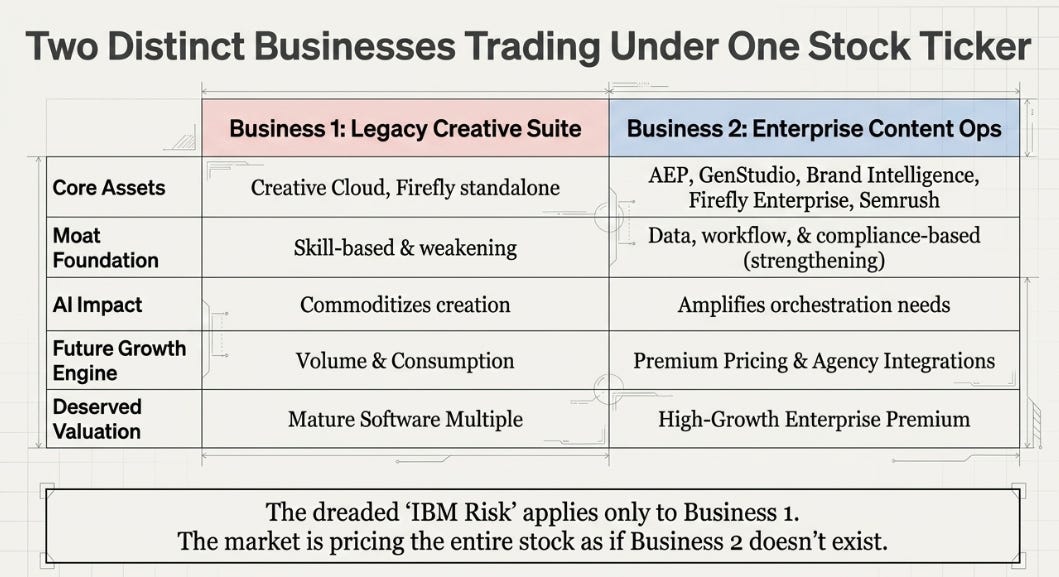

The abundance paradox creates two structurally distinct businesses inside one stock.

The first is creative tools and consumer productivity, Creative Cloud subscriptions, Firefly standalone, Express, Acrobat individual plans, and the freemium funnel. This business is not dying. Revenue grew double digits. Professional users still need precision editing, advanced workflows, and production-grade output. But the moat has weakened. Growth will come from volume and consumption rather than pricing power. It deserves a mature software multiple.

The second is enterprise content operations, AEP, GenStudio, AEM, agentic web products, Brand Intelligence, CX Enterprise, Firefly Enterprise, and Semrush. This business has switching costs that AI cannot erode because they are not skill-based. They are built on customer data, workflow configurations, brand rules, agency integrations, compliance frameworks, and years of accumulated intelligence. Every workflow that runs through the platform makes it harder to leave.

The market is right to worry about the first business. It may be wrong to apply that worry to all of Adobe.

The IBM comparison that haunts Adobe investors applies to the first business but not the second. IBM’s core market was shrinking, fewer mainframe workloads each year. Adobe’s creative market is expanding, more content than ever. And IBM never had a 30%-growth enterprise platform embedded in its financials. The correct frame is not “Adobe becomes IBM.” It is that Adobe contains an IBM-like mature franchise and something resembling a high-growth enterprise platform, and the market is pricing the entire company as if only the former exists.

The Freemium Bet and the Bridge to FY28

The freemium pivot is where the argument gets hardest, because it is simultaneously the right structural response and the most damaging near-term signal.

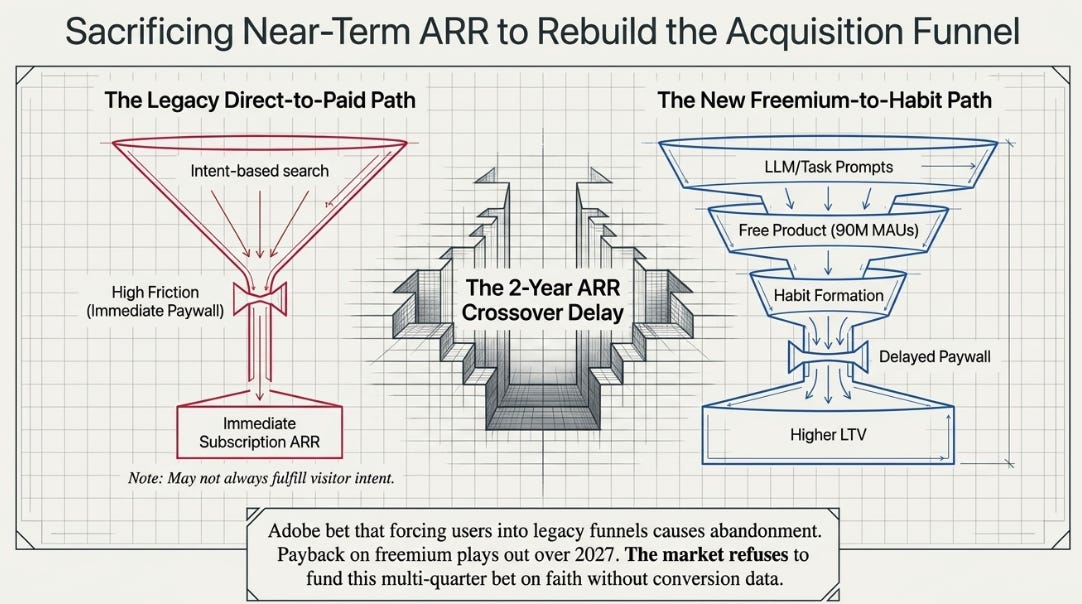

Management’s logic is straightforward. Users arriving through intent-based search want to complete a task, not buy a subscription. Routing them into the product for free, building engagement, and placing paywalls after habit forms should produce higher lifetime value than forcing them into a purchase funnel they will abandon. Early signals support this: freemium-to-paid converts show higher engagement and credit consumption than direct-to-paid cohorts. Firefly ARR grew roughly 50% quarter-over-quarter through apps and credit packs.

But management has disclosed no conversion rate, no LTV/CAC data, and no cohort analysis. They have said the payback “plays out over 2027.” Asking the market to fund a multi-quarter bet on faith, during a CEO and CFO vacancy, inside a hostile sector narrative, with organic ARR decelerating, is an extraordinary ask. The stock price reflects the uncertainty premium of that ask.

The Acrobat Reader analogy management drew is instructive but imperfect. Reader succeeded because PDF had network effects, every shared document created another user. Firefly-generated images are format-agnostic PNGs. The freemium funnel must rely on habit and product quality alone, which is a slower and less certain monetization path.

For the aggregate ARR trajectory to inflect, AI-first ARR needs to add more annually than the traditional book loses. At current trajectories, that crossover is roughly two years away. The market is pricing Adobe for the gap between now and then.

Three Futures

We see three outcomes over the next three years.

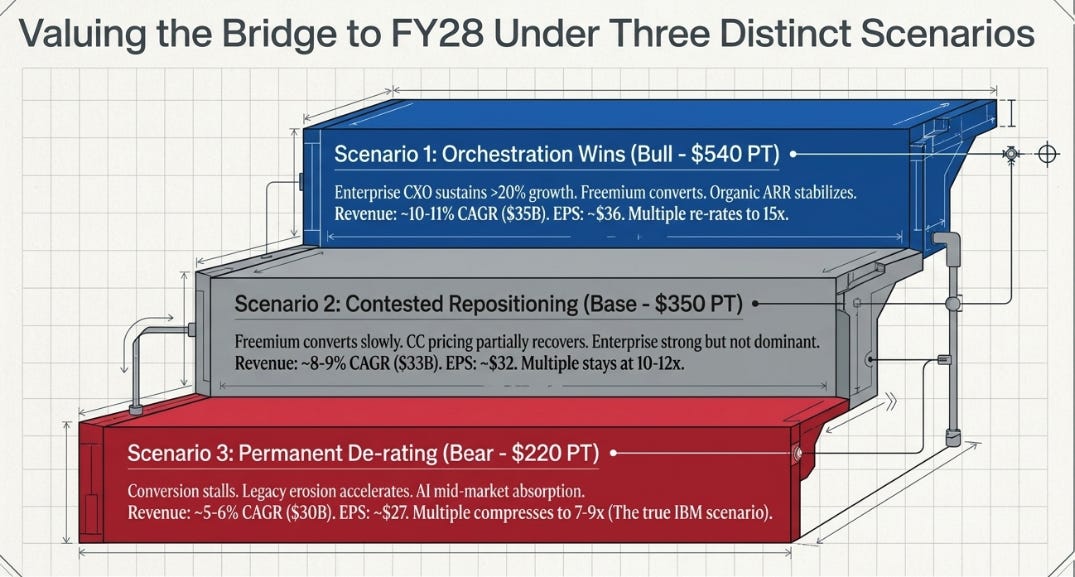

The orchestration loop wins. Freemium conversion works. Enterprise CXO sustains above 20% growth. Organic ARR stabilizes by FY28. A new CEO provides segment transparency, and the market sees the enterprise platform clearly. Revenue compounds at 10-11% through FY29 to roughly $35 billion. Non-GAAP margins hold at 45-46%. EPS reaches approximately $36. The market re-rates to 15x forward earnings as the enterprise platform earns its own premium. Stock price in three years: approximately $540.

Contested repositioning. Freemium converts but slowly. Enterprise remains strong but not dominant enough alone to re-rate the stock. Creative Cloud pricing power partially recovers when line optimizations are reintroduced. Revenue compounds at 8-9% to roughly $33 billion. Margins hold at 43-45%. EPS reaches approximately $32. The multiple stays at 10-12x. Stock price in three years: approximately $350.

Permanent de-rating. Freemium MAU grows but conversion stalls. Traditional Creative Cloud erosion accelerates. AI-native tools absorb the mid-market. Revenue compounds at only 5-6% to roughly $30 billion. Margins drift to 41-43%. EPS reaches approximately $27. The multiple compresses to 7-9x. Stock price in three years: approximately $220. This is not extinction. It is the real IBM risk, a profitable company whose category-defining role has moved elsewhere.

The asymmetry is better than the sentiment suggests, but the catalyst path is long.

What Changes Our Mind

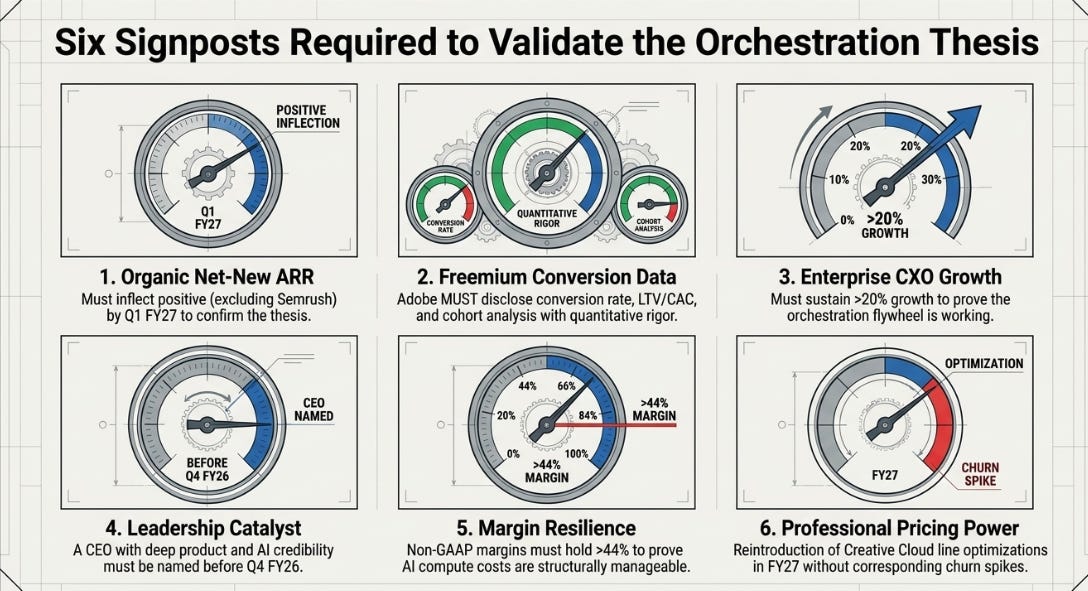

Six signposts will determine which future arrives.

Organic net-new ARR excluding Semrush: inflecting positive by Q1 FY27 confirms the thesis; declining three consecutive quarters impairs it. Freemium conversion disclosure with quantitative rigor: the single most important missing datapoint. Enterprise CXO growth sustaining above 20%: the orchestration flywheel’s proof. A CEO with product and AI credibility named before Q4 FY26: the narrative catalyst. Non-GAAP margins holding above 44%: confirms AI costs are manageable. Creative Cloud line optimizations reintroduced in FY27 without churn stress: evidence that professional pricing power remains intact.

We will revisit the thesis after the CEO appointment and publish a full update with Q3 results.

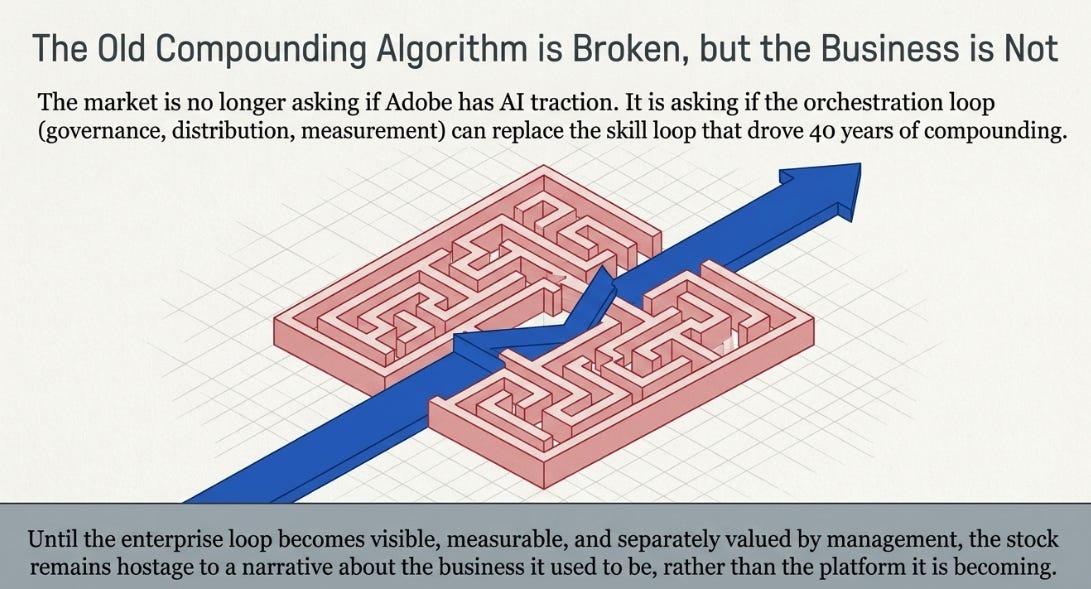

Our prior framework measured the right things and missed the structural shift underneath. Adobe’s business is not broken. Its old compounding algorithm is. The market is no longer asking whether Adobe has AI traction. It is asking whether the orchestration loop, workflow, governance, distribution, measurement, can replace the skill loop that drove forty years of compounding.

That is the only question that matters now. At $206, the market’s answer is a clear no. The enterprise evidence, on balance, suggests the answer is more nuanced than that, but Adobe has not yet given the market the data it needs to see it. Until the orchestration loop becomes visible, measurable, and separately valued, the abundance paradox will remain unresolved, and the stock will remain hostage to a narrative about the business it used to be rather than the platform it is becoming.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.