Adyen 1Q26 Earnings: Great Company, Wrong Category

The single-platform thesis is intact. The market is asking whether Adyen can become more than payments.

TL;DR

Adyen’s Q1 did not break the thesis: Unified Commerce, Platforms, and its single-stack architecture still look strong.

The problem is valuation regime change: payments stocks are now being treated like processors, not scarce compounders.

The stock needs a new proof point: visible revenue from fraud, identity, money movement, embedded finance, and Talon.One, not just more processed volume.

We have been positive on Adyen for a long time, and the stock has gone the other way.

That is the place to start. Not with Q1 revenue. Not with processed volume. Not with another elegant explanation of the single platform. The right starting point is more uncomfortable: we have liked the company because the company is genuinely special, but the market has not cared. That means one of three things is true. Either the thesis is wrong, the thesis is early, or the thesis is incomplete.

I think it is incomplete.

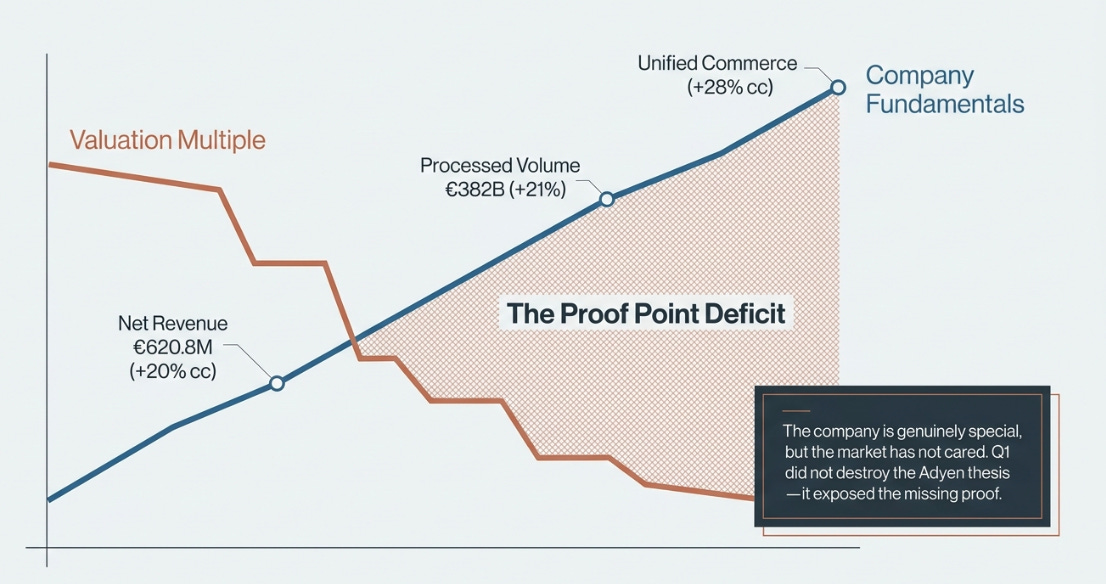

The mistake was not believing in Adyen’s architecture. The single-platform thesis is real. It explains the margins, the reliability, the speed of deployment, the ability to serve large global merchants, and the continued strength in Unified Commerce and Platforms. The mistake was assuming the market would continue to pay for that architecture before it showed up clearly in reported growth, take-rate stability, or capital return.

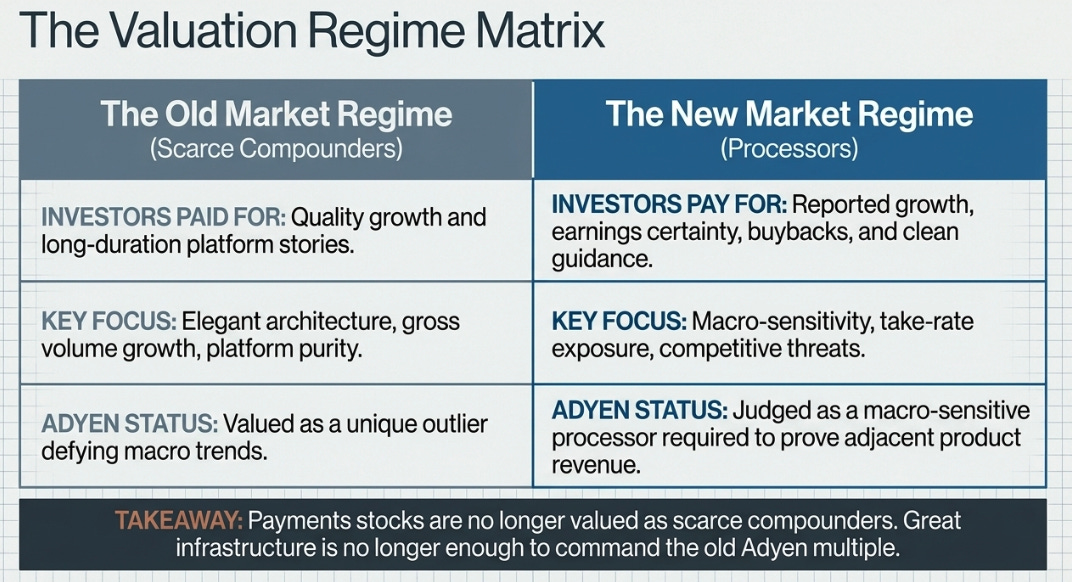

That is the regime change. Payments stocks are no longer being valued as scarce compounders. They are being valued as processors: macro-sensitive, take-rate exposed, competitively threatened, and increasingly required to prove that every adjacent product is real revenue rather than strategic language. In that regime, “great infrastructure” is not enough. Investors want visible proof.

Q1 2026 did not destroy the Adyen thesis. It did expose the missing proof.

The question

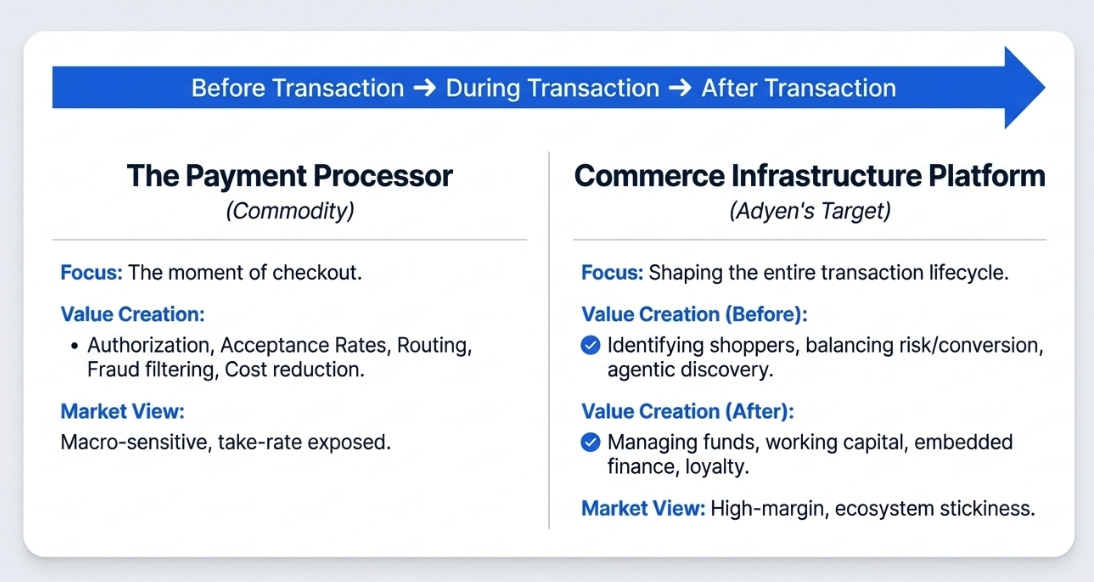

The fundamental question is simple: Adyen built better payment pipes; can it use those pipes to sell more than payments?

If the answer is no, Adyen remains an excellent processor. That is not a bad business. A processor that grows around 20%, earns high margins, and serves the largest merchants in the world is valuable. But in today’s market, it probably does not deserve the old Adyen multiple.

If the answer is yes, the stock is being judged too narrowly. Adyen is not just processing the transaction; it is starting to shape the transaction. It can identify the shopper, judge the risk, influence the offer, process the payment, move the money, and attach financial products around the merchant relationship. That is the difference between a payment processor and a commerce infrastructure platform.

This is exactly the transition management is trying to describe. Ingo Uytdehaage said the value in payments used to sit at authorization, acceptance rates, routing, fraud, cost, but is now moving before and after the payment: before, into decisions about which transactions to allow and how to balance risk and conversion; after, into managing funds across markets, entities, and time.

That is not quarterly noise. That is the new question.

What we missed

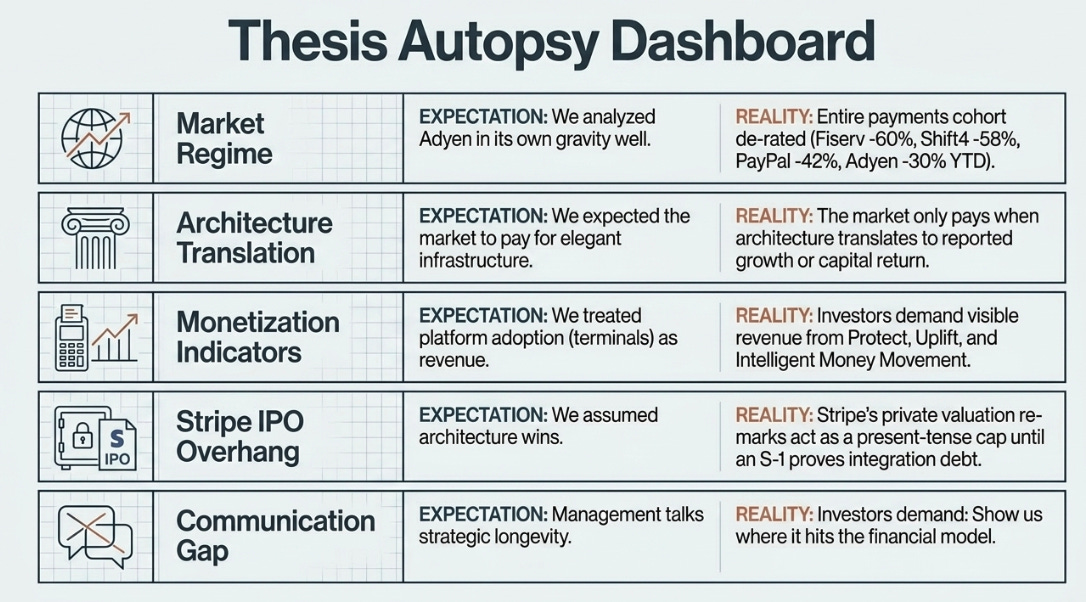

We missed five things.

First, the market regime. In the old regime, investors paid for quality growth and long-duration platform stories. In this regime, they pay for reported growth, earnings certainty, buybacks, and clean guidance. The entire payments cohort de-rated: Fiserv -60%, Shift4 -58%, PayPal -42%. Adyen at -30% YTD is in the middle of the pack, not an outlier. We analyzed Adyen as if it traded in its own gravity well. It doesn’t.

Second, the speed of architecture-to-stock translation. We were right that the single platform is a real advantage. But the market does not pay for architecture in the abstract. It pays when architecture produces higher revenue per transaction, better margins, faster growth, or cash returned to shareholders. Q1 was not enough on that front.

Third, we treated platform indicators as if they were already monetization indicators. They are not. Terminals, platform customers, cross-channel customers, and product adoption are all useful. But the market now wants to know how much revenue comes from Uplift, Protect, Intelligent Money Movement, embedded finance, and eventually Talon.One. Adyen is not giving enough of that yet. This is the deepest version of being wrong: we were measuring the wrong proof points.

Fourth, the Stripe IPO has been a present-tense valuation cap, not a future variable. Every private re-mark of Stripe at a higher valuation re-anchored Adyen’s public multiple lower. The architecture argument cannot win against a comparable that hasn’t reported yet. Until Stripe’s S-1 either reveals integration debt or confirms it has achieved Adyen’s depth without organic discipline, this overhang remains.

Fifth, we underestimated communication risk. Management keeps saying the long-term opportunity is intact. Investors are saying: “Fine, show us where it hits the model.”

That is why the stock has been painful. The company has been executing, but the market has changed what it needs to see.

Q1: good company, not enough stock

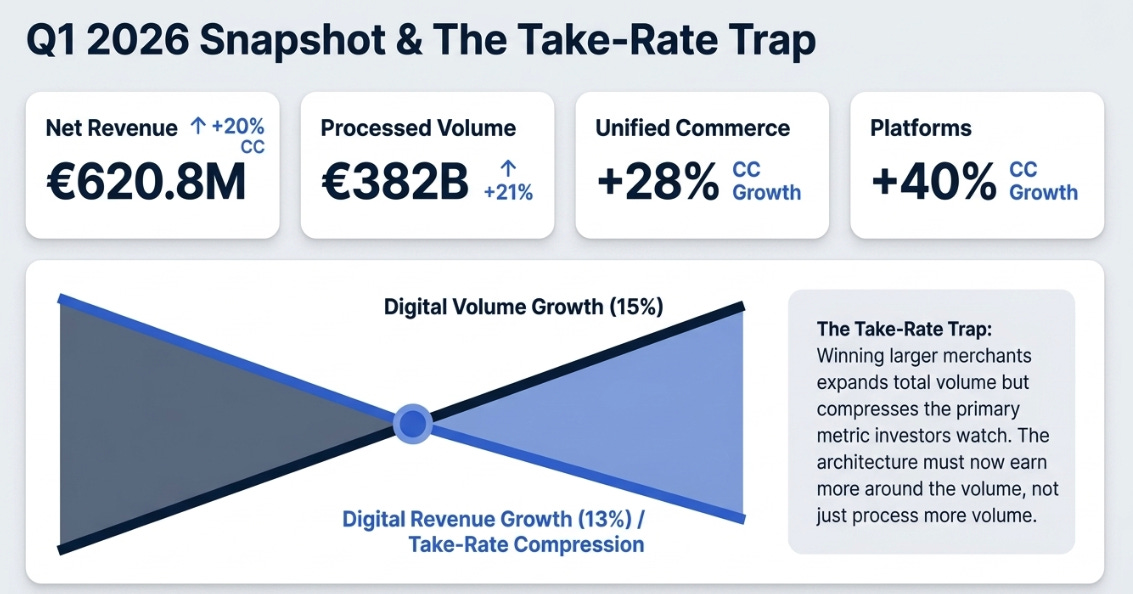

The Q1 numbers were not bad. Net revenue was €620.8 million, up 16% reported and 20% constant currency. Processed volume was €382 billion, up 21%. Unified Commerce grew 28% constant currency, Platforms grew 40% constant currency, and the company reiterated 2026 constant-currency revenue growth guidance of 20–22%.

Those numbers say the business is healthy.

The problem is what the market saw underneath them. Digital revenue grew 13% constant currency, while Digital volume grew 15%. The largest segment still had take-rate pressure. Management said the issue is mix: larger customers are priced lower, and expansion with the biggest customers weighs on take rate.

That explanation is plausible. It is also not fully comforting.

This is the trap. If Adyen wins more volume from the largest merchants, the company may be strengthening its strategic position while weakening the headline metric investors still watch most closely. That is why the old “architecture dividend” thesis now needs an upgrade. The single platform cannot merely process more volume. It has to help Adyen earn more around that volume.

The real purpose of Talon.One

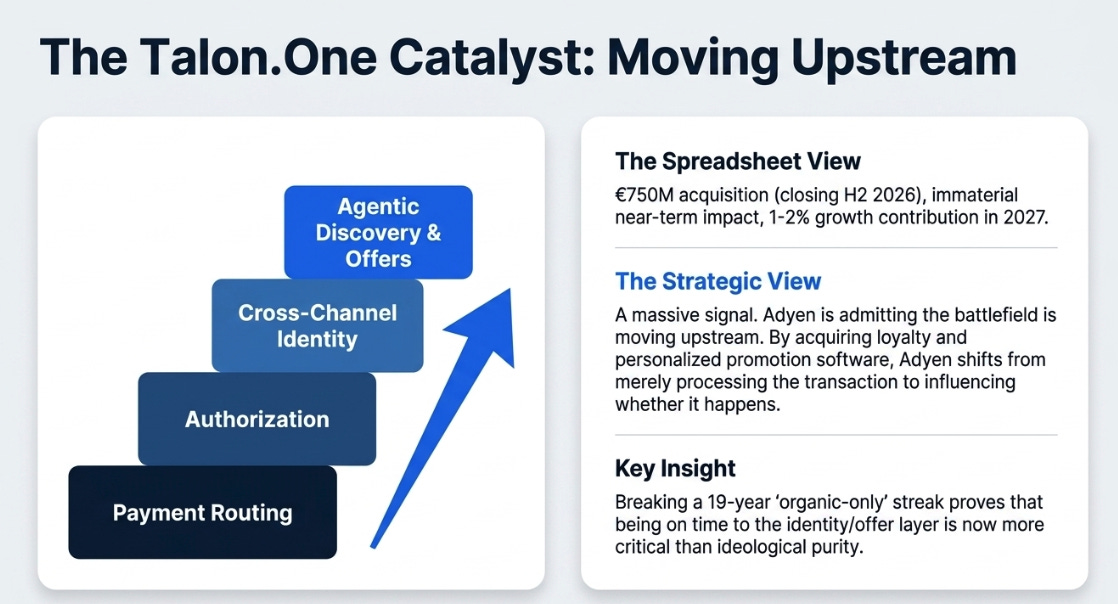

This is why Talon.One matters.

On paper, it is a €750 million acquisition expected to close in the second half of 2026, with no material 2026 impact and 1–2% growth contribution in 2027.

That is the spreadsheet answer. It is not the strategic answer.

The strategic answer is that Talon.One moves Adyen closer to the moment where commerce is actually shaped. A payment processor authorizes a transaction. A better commerce platform influences whether the transaction happens, what offer is shown, what incentive applies, and what the customer is worth over time.

Ethan Tandowsky’s explanation was clear: Adyen can identify shoppers across online and in-store because those transactions run on one stack; Talon.One lets merchants act on that identity with personalized promotions or loyalty decisions in real time.

Talon.One is not just loyalty software. It is Adyen admitting that the battlefield is moving upstream. The company historically built everything itself. That discipline created the platform. But if the next layer of value is being formed now, identity, offers, incentives, pricing, agentic discovery, then being pure is less important than being on time. The deal is small in dollars and enormous in signal. It is also Adyen’s first material acquisition in nineteen years, which opens a capital allocation conversation that has been closed since IPO.

The self-reinforcing mechanism

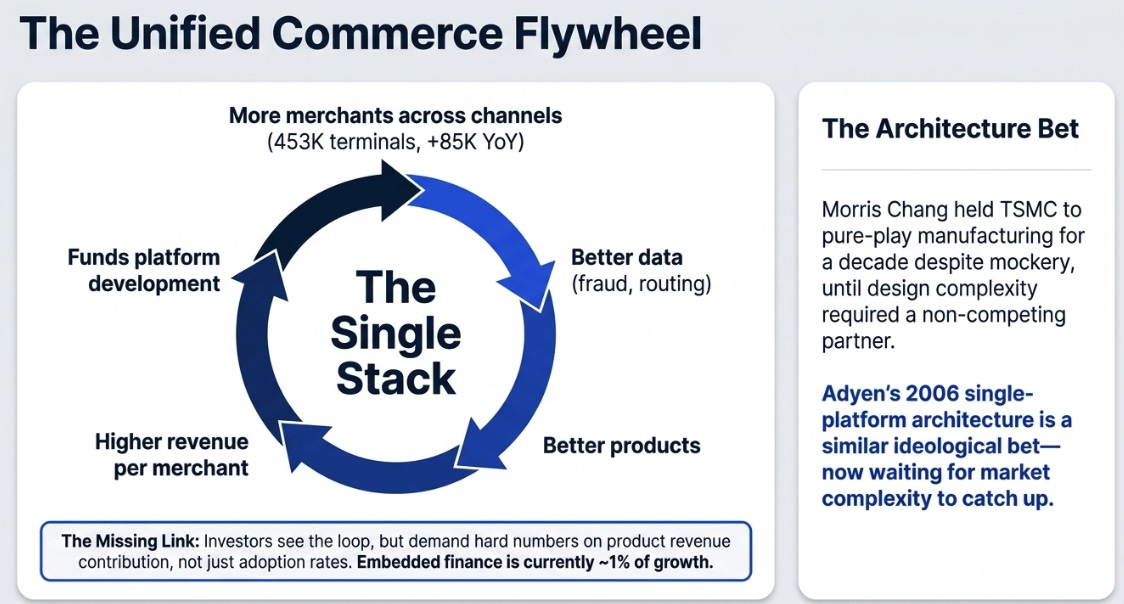

Here is the Adyen bull case in plain English.

More merchants use Adyen across more channels. That gives Adyen more consistent data about transactions, shoppers, fraud, conversion, routing, and settlement. Better data helps Adyen build better products. Better products improve merchant outcomes. Better outcomes allow Adyen to sell more services beyond basic processing. Those services increase revenue per merchant. More revenue funds more product development. The platform gets stronger.

That is the loop.

The loop is visible in some Q1 metrics. Unified Commerce now has 474 customers processing across channels at scale and 453,000 terminals, up 85,000 year over year. Platforms has 34 customers processing more than €1 billion annually, while platform business customers rose to 264,000 from 177,000 last year.

But the loop is not yet proven where investors care most. When analysts asked for hard proof, fraud improvement, authorization uplift, Talon.One conversion impact, product revenue contribution, management answered with direction and adoption, not numbers. Embedded financial products are contributing around the 1% growth level discussed previously. That is still small.

This kind of architecture-led bet has paid off before. Morris Chang refused to design chips when he founded TSMC in 1987. He held the foundry to pure-play manufacturing for a decade and was mocked for ideological purity, until chip design and manufacturing complexity grew faster than integrated competitors could absorb, and the fabless design houses needed a partner who would never compete with them. The architecture choice became the category. The question for Adyen is whether it is the same kind of bet, and whether the world it was designed for has now arrived.

The variant perception

The market’s view is understandable: Adyen is a high-quality processor whose take rate is under pressure, whose reported growth has disappointed before, and whose new product story will take time to prove.

The variant view is not that the market is blind. It is that the market is using the right concern but the wrong endpoint.

Take-rate pressure matters. But the real question is whether take rate remains the best measure of the business. If Adyen only earns basis points on processed volume, the market is right to compress the multiple. If Adyen earns more from fraud, identity, routing, promotions, money movement, issuing, working capital, and embedded finance, then the old metric becomes incomplete.

Adyen does not need investors to stop caring about take rate. It needs to show that take rate is no longer the whole story.

What would actually break the thesis

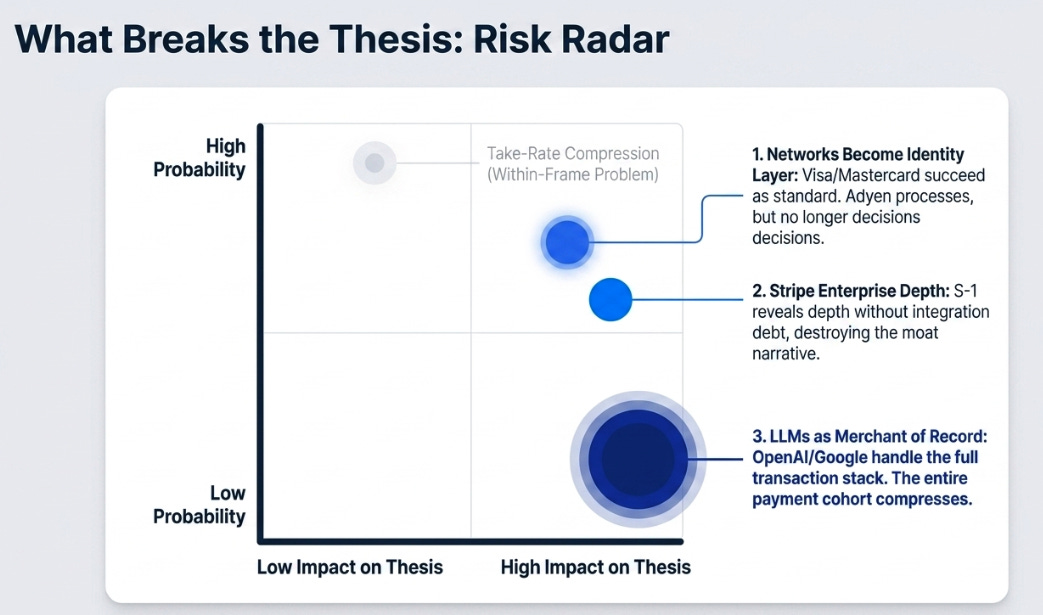

The thesis does not break from take-rate compression in Digital. That is a within-frame problem. It breaks from category-level disintermediation. Three plausible paths.

The networks become the identity layer. If Visa Intelligent Commerce Connect and its Mastercard analog succeed as the cross-merchant identity standard for agentic commerce, Adyen still processes but no longer decisions. The architecture advantage shrinks meaningfully.

Stripe achieves global enterprise depth before Adyen achieves global agentic scale. The IPO is the inflection. If Stripe’s disclosures reveal it has achieved Adyen’s depth without integration debt, the moat narrative is in trouble.

LLM platforms become merchant-of-record. Lowest probability, highest consequence. If OpenAI or Google handle the full transaction stack rather than route to merchants, the entire cohort compresses regardless of architecture.

Q1 produced no evidence on any of these three. The things that could actually break the thesis did not get tested. The take rate did, which is a much narrower thing.

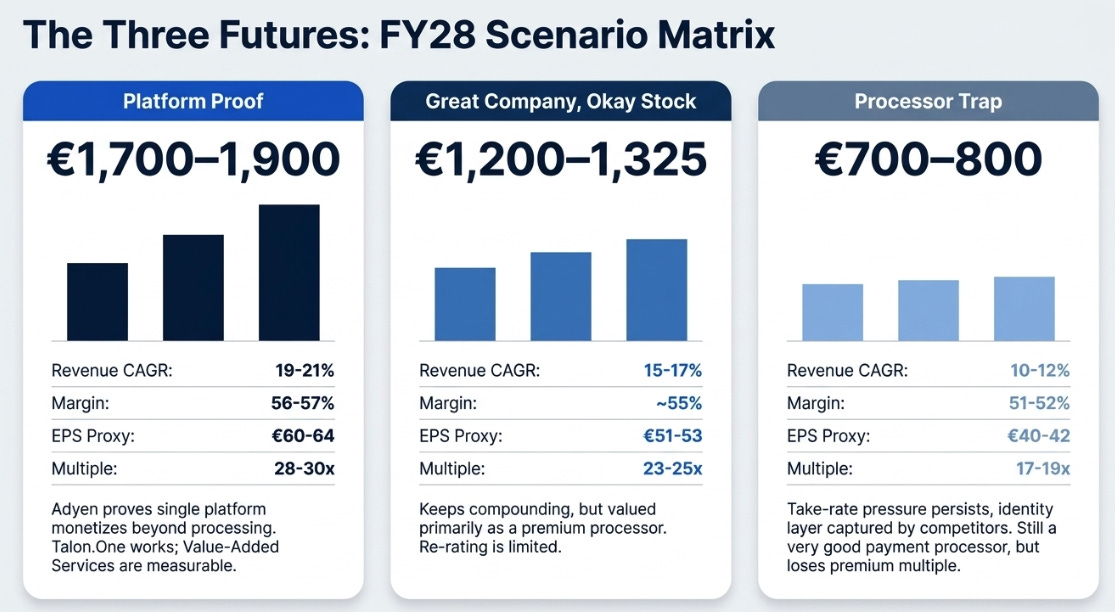

The three futures

Using roughly €950 as a working reference price, the three-year setup depends on whether Adyen proves it can sell more than payments.

The important point is not the precision of the numbers. It is the nature of the failure case.

The bear case is not that Adyen suddenly becomes a bad company. The bear case is that it remains a very good payment processor in a market that no longer pays premium multiples for very good payment processors.

What would change our mind

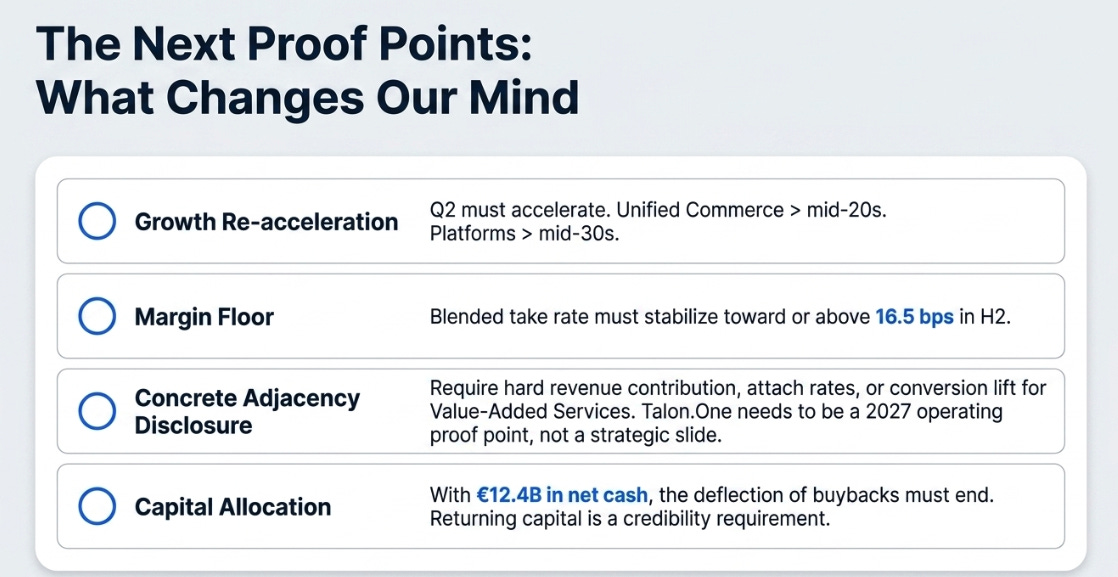

The next proof points are clear. Q2 needs to accelerate, because management said APAC online retail headwinds should ease. Unified Commerce needs to stay above the mid-20s in constant-currency growth. Platforms above the mid-30s. Blended take rate needs to stabilize, ideally back toward or above 16.5 bps in H2.

Management needs to disclose something more concrete on value-added services: revenue contribution, attach rates, conversion lift, fraud improvement, or money-movement monetization. Talon.One needs to become a 2027 operating proof point, not just a strategic slide.

Capital allocation also matters more than before. Talon.One opened the door, it was Adyen’s first material acquisition in nineteen years and broke the organic-only frame the company has held since IPO. With €12.4 billion of net cash, the buyback conversation that has been deflected for years gets harder to deflect. Ethan’s not-quite-no on the Q1 call was warmer than prior versions. In a regime where investors no longer pay blindly for long-duration growth, returning capital becomes part of the credibility discussion.

The conclusion

We were right about the company and wrong about what the market would pay for it.

That is the cleanest way to say it.

Adyen’s single-platform architecture remains special. Q1 did not change that. Unified Commerce and Platforms continue to prove that Adyen is more than a commodity processor. Talon.One is a smart strategic move because it pushes Adyen upstream, closer to the moment where merchants shape demand rather than merely accept payment.

But the stock will not work simply because the architecture is elegant. It will work when that architecture produces visible revenue beyond basic processing.

Adyen built better pipes. Now it must prove those pipes let it sell more than payments. Until then, the company can remain excellent while the stock remains frustrating. Q1 did not settle the debate. It clarified it.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.