Adyen's 4Q25: The Price of Being Right

Record margins. Record take rates. Record enterprise wins. And a 22% single-day decline that exposes the gap between building a great platform and owning a great stock.

TL;DR:

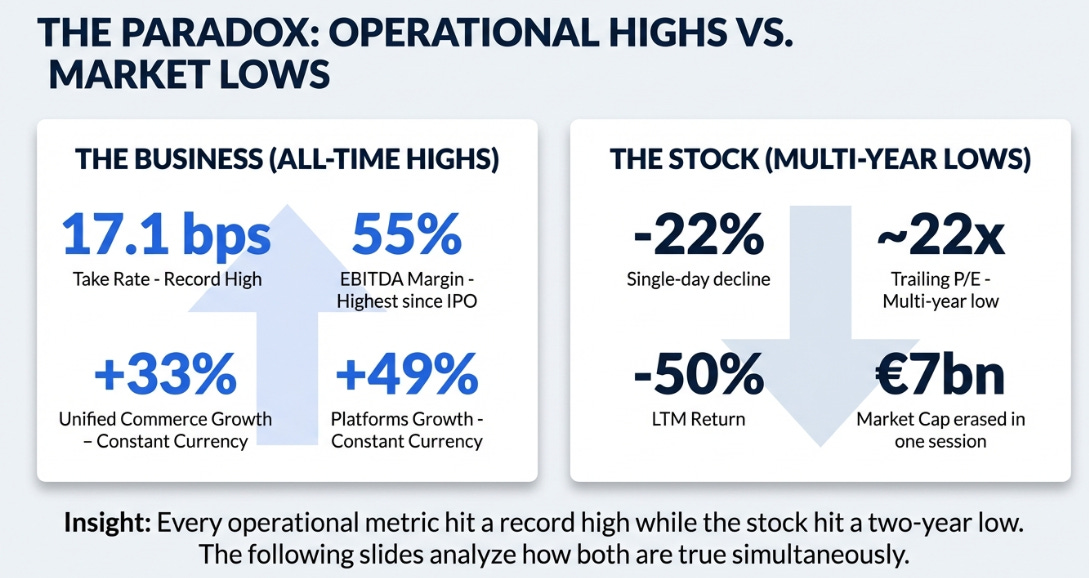

The paradox: Every operational KPI hit an all-time high. The stock hit a two-year low. Both are true simultaneously.

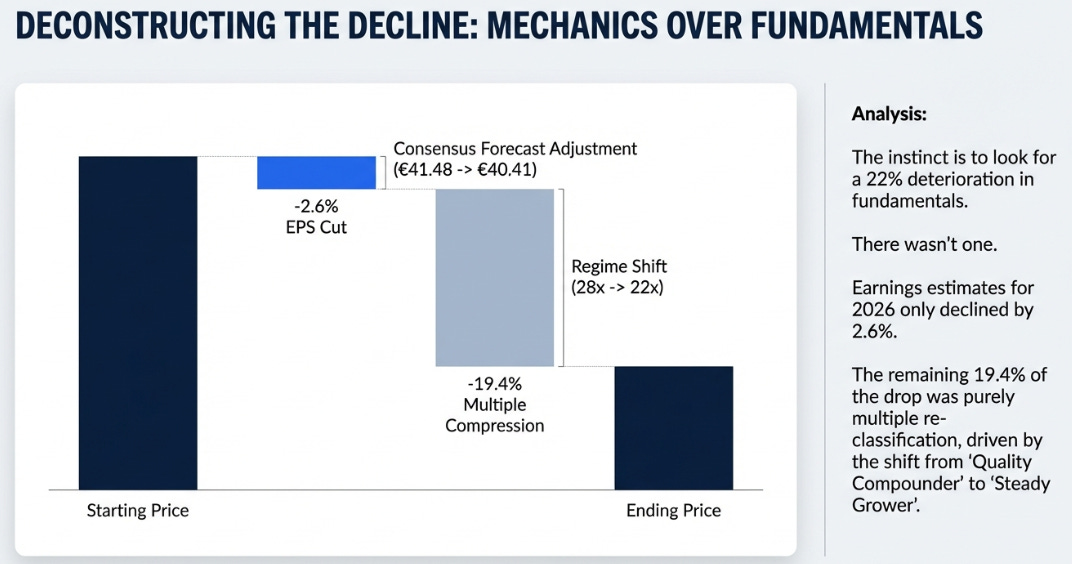

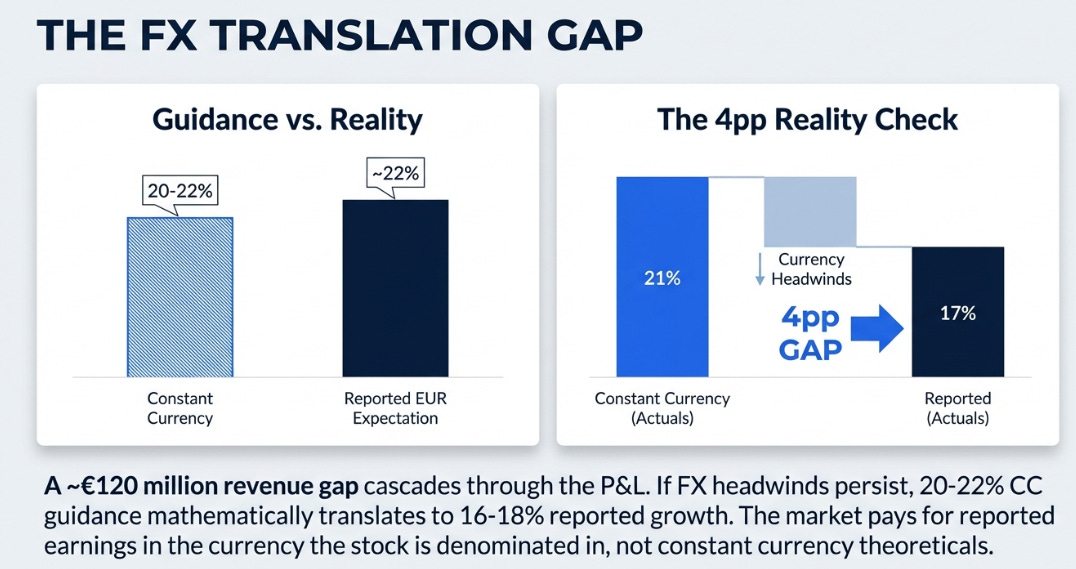

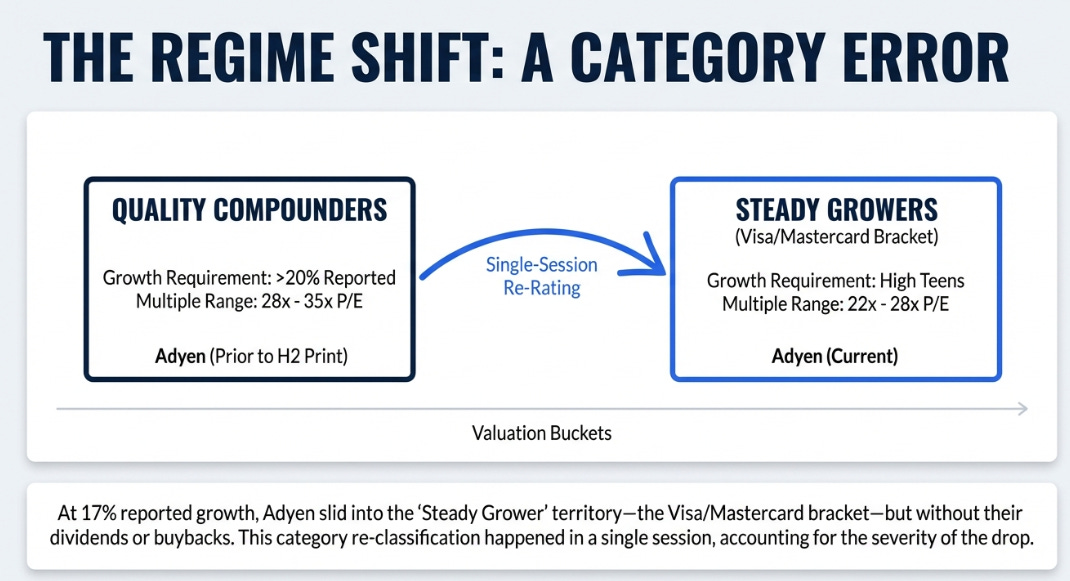

The mechanism: Consensus EPS was cut 2.6%. The stock fell 22%. The other 19 points was a multiple re-classification from “quality compounder” (28x) to “steady grower” (22x), driven by a 4pp FX gap that translates 20-22% CC guidance into 16-18% reported EUR growth.

What comes next: The estimate revision cycle hasn’t started, FY26 EPS needs to fall another ~10%. Q1 will be the weakest quarter. The higher-probability entry is after revisions settle, likely at €800-850.

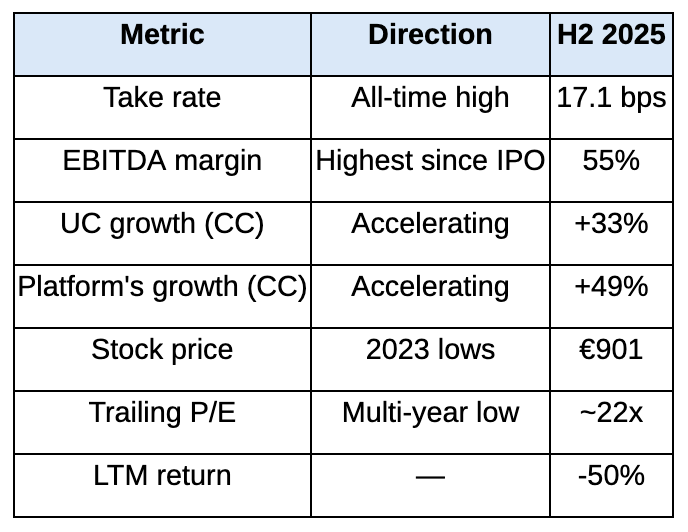

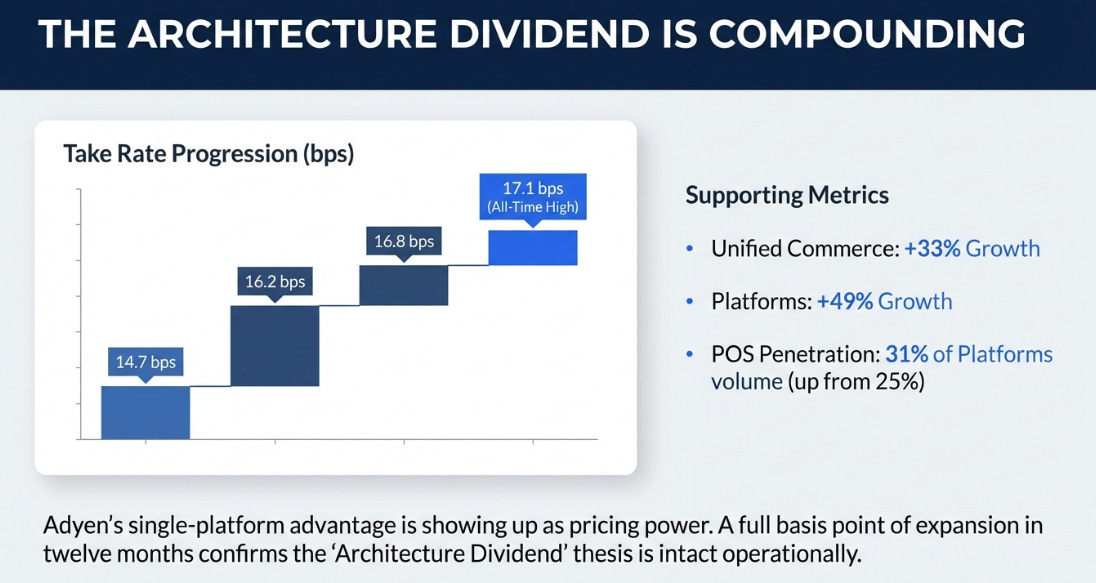

I’ve been writing about Adyen’s “architecture dividend” for a while. The thesis was straightforward: by building a single, unified platform from scratch, Adyen created a compounding data advantage that would show up as pricing power, margin expansion, and enterprise dominance. H2 2025 was the most emphatic validation yet. EBITDA margins hit 55%, the highest in Adyen’s history. The take rate reached 17.1 basis points, a new all-time high. Unified Commerce revenue grew 33% constant currency. Platforms grew 49%. Issuing volumes grew eightfold.

And the stock fell 22% in a single session, erasing €7 billion in market capitalisation.

Every operational metric is at an all-time high. Every market metric is at a multi-year low. This piece is about how both can be true simultaneously, what I got wrong, and what it means going forward.

How 2.6% Became 22%

The instinct when a stock drops 22% is to look for a 22% deterioration in fundamentals. There wasn’t one. Consensus earnings estimates for 2026 moved from €41.48 to €40.41, a decline of 2.6%. The other 19.4 points came from three forces compounding simultaneously.

The first was the FX translation gap. Adyen guided to 20-22% net revenue growth on a constant currency basis. Consensus had modelled ~22% in reported euros. In H2 2025, constant currency growth was 21% while reported growth was 17%, a four-point gap driven by dollar weakness. If that persists, 20-22% CC translates to 16-18% reported. That’s a ~€120 million revenue gap cascading through every line below it.

Even after the selloff, Bloomberg consensus for FY26 revenue sits at €2,888 million, still implying ~22% reported growth. Analysts haven’t re-modelled for FX. When they do, EPS consensus will migrate toward ~€36.50. That’s another 10% of cuts ahead. The revision cycle hasn’t started; it’s been announced.

The second was the margin pause. The street expected margin expansion toward 55%. Instead, management guided “broadly in line with 2025” (~53%) as they plan to hire 550-650 people. Probably the right long-term call. But when you remove the next leg of the earnings growth story from a stock at 28x, the stock stops trading at 28x.

The third, which did 90% of the damage, was multiple re-classification. Markets assign multiples in categories, not on a smooth spectrum. At 22% reported growth, Adyen was a “quality compounder” at 28-35x. At 17% reported, it slides into “steady grower” territory at 22-28x, the Visa/Mastercard bracket, except without their dividends or buybacks. The market reclassified the stock in a single session. A category re-classification is not a valuation adjustment. It is a regime shift. And regime shifts are violent.

The Architecture Dividend, Still Compounding

I won’t re-litigate the full platform thesis. Three data points from H2 advance it.

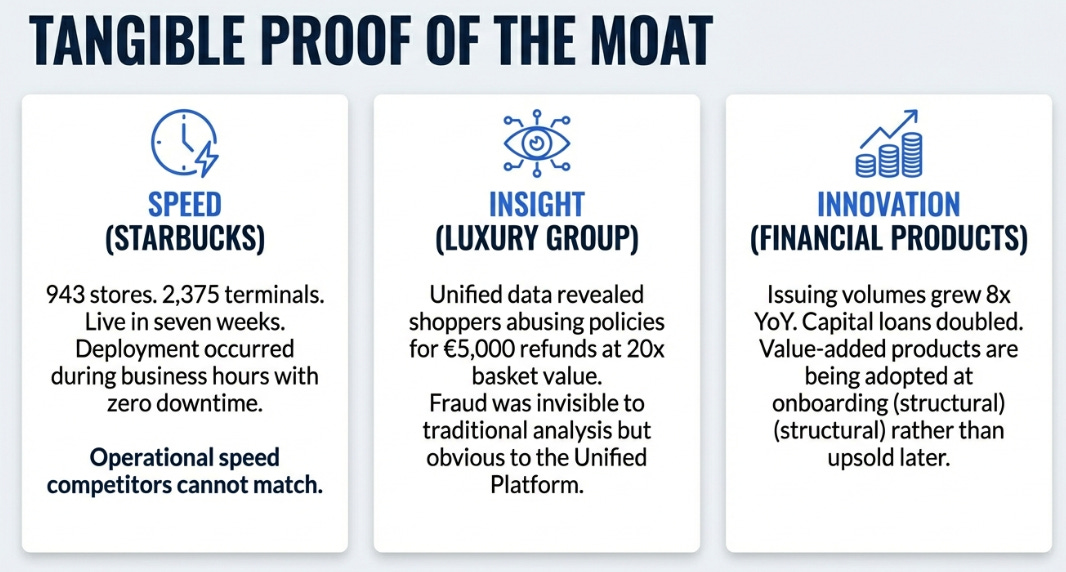

The take rate progression, 14.7 to 16.2 to 16.8 to 17.1 basis points over four periods, is a full basis point of expansion in twelve months. The mechanism: POS hit 31% of Platforms volume (up from 25%), terminals reached 456,000, and a new product called “Personalize” delivered 6% conversion improvements alongside 3% cost reductions in pilots. One luxury group discovered shoppers receiving up to €5,000 in refunds at twenty times their basket value, policy abuse invisible through traditional analysis. Uytdehaage confirmed on the call that two-thirds of new enterprise merchants activate Uplift from day one. When value-added products are adopted at onboarding rather than sold as upsells years later, the expansion is structural.

Deployment speed proves the moat tangibly. Starbucks: 943 stores, 2,375 terminals, live in seven weeks, during business hours. LVMH expanded across its Maisons. Lufthansa unified payments across booking, onboard, and airports. Uber launched kiosks at LaGuardia. These aren’t logos, they’re proof of operational speed competitors cannot match on acquisition-built platforms.

Financial products are inflecting. Issuing grew 8x YoY. Capital loans doubled. CashOut hit a hundreds-of-millions run rate while still in pilot. Adyen is collaborating with OpenAI, Google, Visa, and Mastercard on agentic commerce standards, optionality in zero sell-side models.

None of this prevented a 22% selloff. The architecture dividend compounds in the product. It does not automatically compound in the stock price.

What I Got Wrong

I underestimated three things.

First, the violence of multiple re-classification. I modelled 8-15% downside. The actual was 22%. I knew 17% reported growth would compress the multiple, I didn’t appreciate the market would snap from one category to another in a single session rather than gradually adjusting.

Second, the FX compounding effect. I identified the gap before the print but treated it as a known headwind rather than the dominant narrative. The four-point drag determined whether Adyen’s growth started with a “2” or a “1”, the boundary between two entirely different multiple brackets.

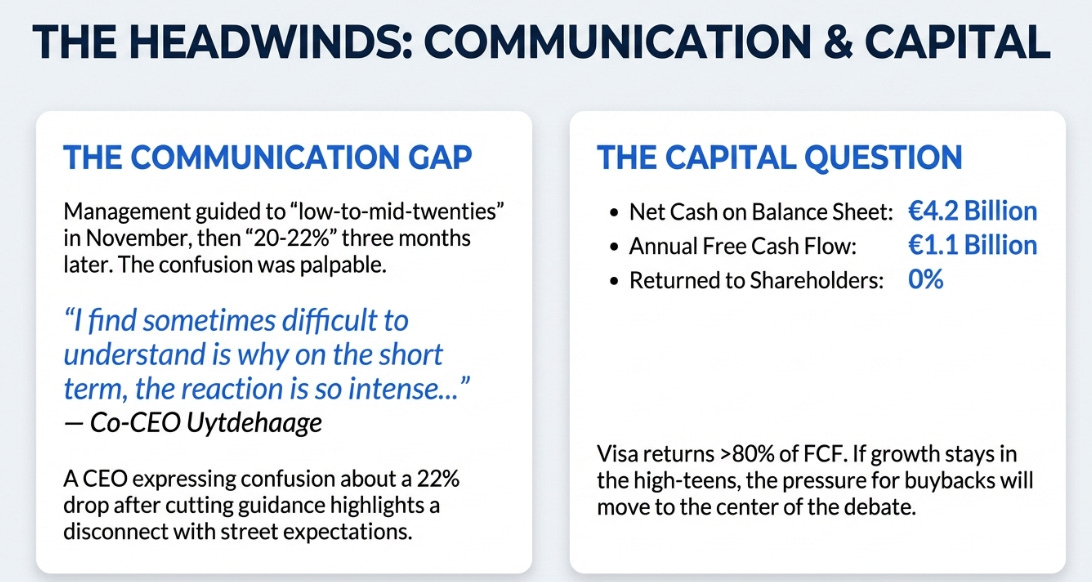

Third, management’s communication. In November, the Investor Day set expectations at “low-to-mid-twenties.” Three months later: 20-22%. UBS’s Justin Forsythe asked on the call: why didn’t you guide to low twenties in October for conservatism? Tandowsky’s answer, November was a “transitionary period” to the new annual framework, is technically correct but unsatisfying.

More telling was Co-CEO Uytdehaage’s closing remark:

“I find sometimes difficult to understand is why on the short term, the reaction is so intense, because the long-term perspective for us does not change.”

A CEO expressing confusion about why his stock fell 22% after cutting guidance is the problem. Five analysts asked variations of the same question. When the entire Q&A is consumed by a single topic, the communication has failed. Bernstein’s Harshita Rawat captured the frustration precisely: “We wish Adyen would get in the habit of under-promising and over-delivering on numbers.”

The sell-side fared no better. Thirty-one Buy ratings. Consensus target €1,617. Stock at €901. Every analyst delivered -43% LTM returns while maintaining Buy. Those targets will converge toward €1,100-1,200 as models are re-built, but until then, the “consensus” is fiction.

One question nobody is asking yet: capital allocation. Adyen sits on ~€4.2 billion net cash, generates €1.1 billion in annual free cash flow, and returns zero to shareholders. At 25% growth, reinvest everything. At 17% reported, investors ask why. Visa returns over 80% of FCF and trades at a higher multiple growing slower. On the call, Tandowsky offered a subtle shift: “We’re certainly not dogmatic here. We constantly assess what’s the right decision.” Different language from prior categorical rejections. If growth stays in the high-teens, this question moves to the centre of the debate.

The Three-Year View

Here is where I must check my own framework. Most of the analysis produced in the last twenty-four hours, mine included, has been valuing Adyen on FY26, the trough year. FX headwinds peak in Q1. Margins are deliberately held flat. The 2025 cohort is still ramping. But stocks don’t trade on the current year forever. By mid-2026, the market prices FY27. By early 2027, FY28. And when you extend the lens, the arithmetic changes considerably.

The architecture dividend I’ve been tracking for three years doesn’t pause because the stock fell 22%. Take rate expansion, margin leverage, financial products inflection, enterprise deepening, these compound whether the stock is at €900 or €1,500. The question is what that compounding looks like on the income statement over the next three years, and what the market should pay for it at the terminal point.

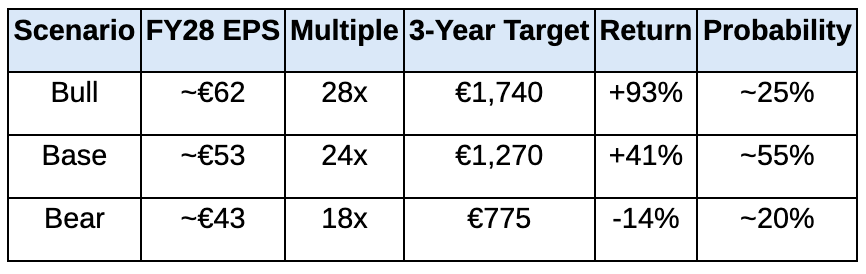

I model three scenarios, each built on explicit assumptions that can be tracked quarter by quarter.

The bull case requires FX normalisation, management beating the conservative guide, and a capital return programme signalling maturity. Revenue grows at 18-19% reported as the dollar stabilises, margin expansion resumes to 57% by FY28 as investment-phase hiring yields operating leverage, and financial products contribute meaningfully. That path produces roughly €62 in FY28 EPS. At 28x, justified if reported growth re-enters the low-twenties and margins reach 57%, which is “quality compounder” territory, the stock reaches approximately €1,740, a 93% return from today.

The base case assumes management delivers on guidance without exceeding it. FX remains a mild headwind. Reported growth settles at 15-16%. Margins expand gradually to 55.5% on schedule. No capital return. No new product inflection surprises. That produces roughly €53 in FY28 EPS. At 24x, a fair multiple for a 15% grower with best-in-class margins and FCF conversion, the stock reaches approximately €1,270, a 41% return. This is the most probable outcome.

The bear case requires macro deterioration, persistent FX headwinds, and evidence the platform thesis is plateauing, take rate stalling, merchants pushing back on premium pricing, Stripe or Checkout.com winning UC deals that previously went to Adyen. Reported growth decelerates to 10-12%. Margins barely expand. That produces roughly €43 in FY28 EPS. At 18x, legacy processor territory alongside FIS and Fiserv, the stock reaches approximately €775, a 14% decline. Nothing in the H2 2025 operational data supports this outcome.

But these are not numbers to take on faith. They are assumptions to be tested. The take rate must hold above 16.5 bps to confirm structural pricing power. Margin expansion needs to show up in H1 2027, if EBITDA margin reaches 54%+ with continued hiring, operating leverage is intact. Financial products need to reach a scale where Adyen discloses their revenue contribution, even directionally. And management must beat the 20-22% CC guide for FY26 to repair the credibility damage. If they miss the low end, the trust deficit widens materially.

On competitive dynamics, there is nothing to fix, yet. Zero evidence of losses in H2 2025. The signal to watch is whether Adyen continues landing complex multi-country, multi-channel UC deployments that competitors struggle to execute. If a major enterprise merchant defects, it’s a red flag. If the pipeline continues producing Starbucks and Lufthansa-calibre wins, the moat is deepening exactly as the thesis predicts.

The near-term path is still messy. Tandowsky noted on the call that Q1 growth will be lower than Q2, peak USD headwind plus APAC retailer lapping. The first data point investors see will be the ugliest quarter of the year. Patience is required.

The Price of Being Right

The architecture dividend is real. Every metric confirms it. Take rates compound. Margins expand. The platform deepens. Dynamic Identification is the moat widening in real time. Starbucks in seven weeks is the moat made tangible.

But the market does not pay you for being right about architecture. It pays you for reported earnings growth in the currency your stock is denominated in. At €901, you are buying the highest-quality payments infrastructure in the world at the lowest multiple since 2023, and at sub-21x the FY27 earnings this business will very likely produce. The three-year arithmetic favours the patient buyer. I believe the stock will recover. I also believed operational excellence would prevent a 22% selloff, and it didn’t. Humility is part of the job.

Boring? Perhaps.

The future of global commerce? Still, absolutely.

Cheap enough to buy? Getting closer.

But the market demands patience, and patience, it turns out, has a price too.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.