Alibaba 3QFY26 Earnings: From Escrow to Agents

The AI thesis got stronger. The commerce repair got later. And the real question is whether cloud can become important fast enough to fund what commerce no longer can.

TL;DR:

Alibaba is uniquely positioned to turn AI into execution, not just recommendation

But the legacy engine (ads + commissions) is stalling despite strong user growth

The outcome depends on a narrow bridge: cloud scaling into a profit engine before commerce fades

In 2003, Taobao had a problem that had nothing to do with technology. Chinese consumers would not send money to strangers on the internet, and sellers would not ship goods before receiving payment. Every transaction was a standoff. The solution was not a better search algorithm or a wider product catalogue, it was Alipay, which held the buyer’s money in escrow until the package arrived. What made this work was not the software. It was the recognition that in a market where nobody trusted anybody, the company that inserted itself into the middle of the transaction would not merely participate in commerce. It would become the infrastructure that commerce ran on. By 2013, Taobao had 70% of the market. The lesson was not that trust mattered. The lesson was that solving the trust problem made you the market.

What we argued in January

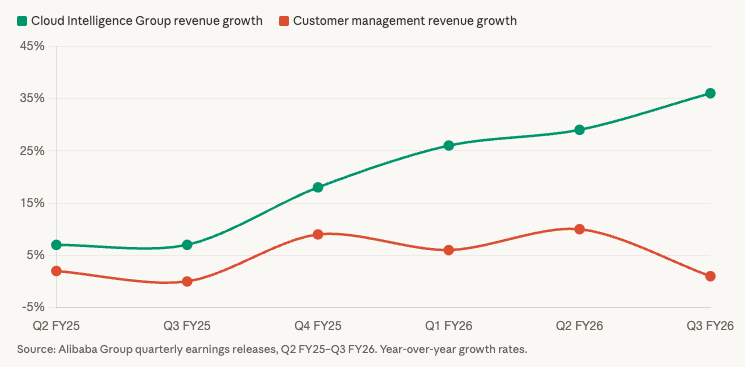

Two months ago, we wrote that Alibaba was facing a second version of that problem, extending trust from human-to-human payments to human-to-software execution. We framed three systems being built simultaneously: a compute spine in cloud infrastructure, a frequency layer in quick commerce, and a monetization engine in advertising and merchant tools. We said everything hinged on whether the bills would get smaller. We were watching three signals: sales and marketing trending toward 23%, customer management revenue holding above 8%, and cloud sustaining above 25% growth. One came in well above expectations. The other two missed.

The quarter that split the story

Alibaba’s December quarter did not settle the debate about the company. It separated it into two debates.

Cloud Intelligence Group revenue grew 36% year-over-year, accelerating for the fourth consecutive quarter. AI-related product revenue posted triple-digit growth for the tenth quarter in a row. Token consumption on the model studio platform grew sixfold in three months. Management announced a new business group called Alibaba Token Hub, set a five-year target of $100 billion in combined cloud and AI external revenue, and disclosed that T-Head, the chip design subsidiary, had shipped 470,000 cumulative AI chips. On the AI and infrastructure side, the momentum is not incremental. It is compounding.

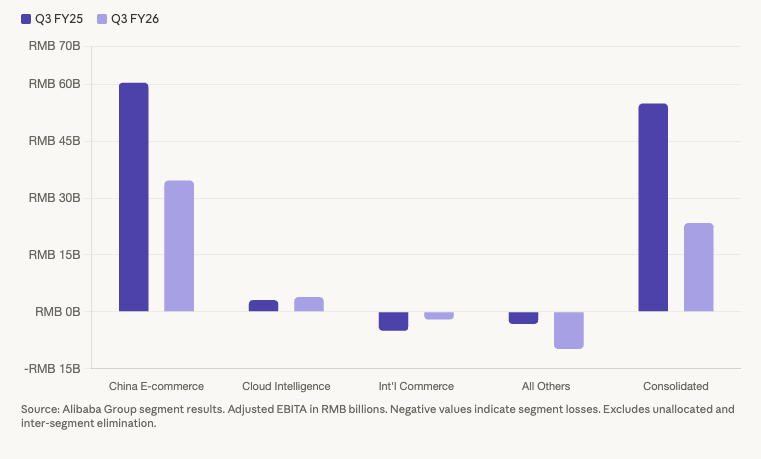

Then there was the other side. Customer management revenue, the advertising and commission income that has historically been the company’s profit engine, grew 1%. Adjusted EBITA fell 57%. Free cash flow was RMB 11.3 billion, down 71% from a year earlier. Sales and marketing remained at 24.9% of revenue. Management dropped the phrase “peak investment” entirely and replaced it with language about “sustained reinvestment” and a “new phase of entrepreneurial reinvention.” The quick commerce business, which grew revenue 56%, was cited as a primary driver of the profit collapse, with profitability now targeted for fiscal year 2029.

Two companies reported under one ticker. The question the rest of this piece tries to answer is which one will define Alibaba three years from now.

Why AI makes Alibaba’s old strengths new again

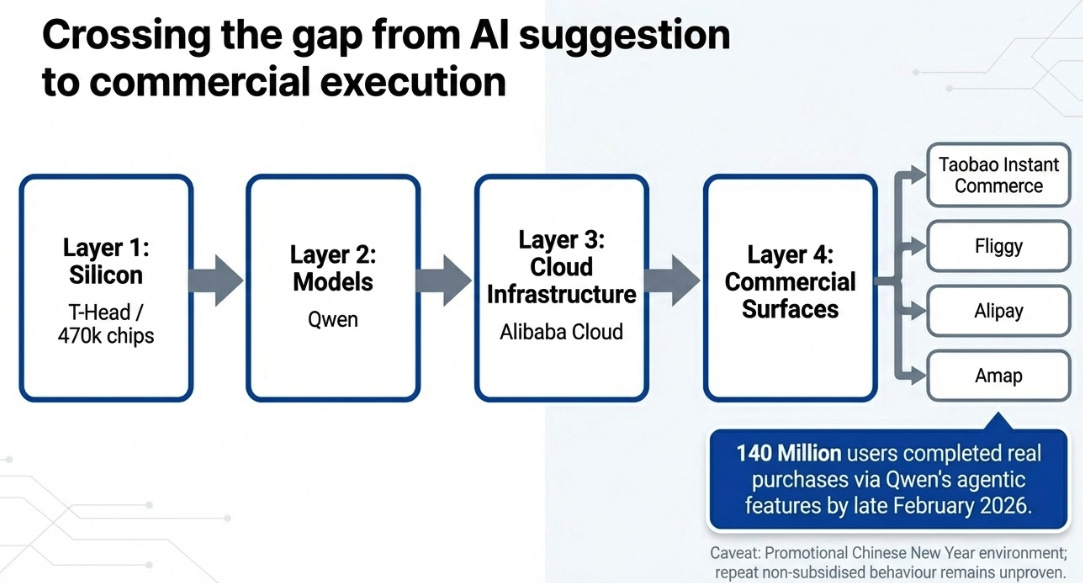

Most AI products today sit beside economic activity. They recommend a restaurant but do not book the table. They compare prices but do not complete the purchase. The gap between suggestion and execution is where most applications stop, because crossing it requires access to payments, identity, logistics, and the commercial surfaces where money changes hands.

Alibaba controls all of those surfaces. When Qwen was upgraded in January 2026, users could order food through Taobao Instant Commerce, book travel through Fliggy, process payments through Alipay, and navigate through Amap, all without leaving the AI interface. By the end of February, roughly 140 million users had completed a real purchase through Qwen’s agentic features.

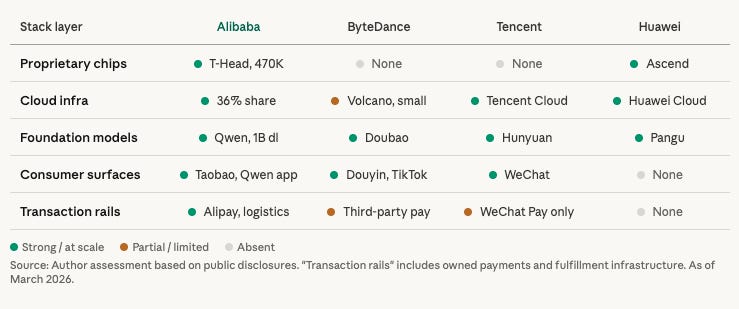

It is worth being specific about who else in China could build this kind of system, because the answer sharpens why Alibaba’s position matters. ByteDance has massive consumer distribution and competitive AI models, but no meaningful external cloud business, Douyin commerce routes payments through third parties rather than owning the rails. Tencent has WeChat, which could become a default agent interface, and a respectable cloud business, but lacks proprietary chips and its commerce surfaces are fragmented across mini-programs rather than integrated. Huawei has chips and cloud but no consumer ecosystem at all. No single competitor currently controls the complete chain from silicon to models to cloud to the endpoints where transactions happen.

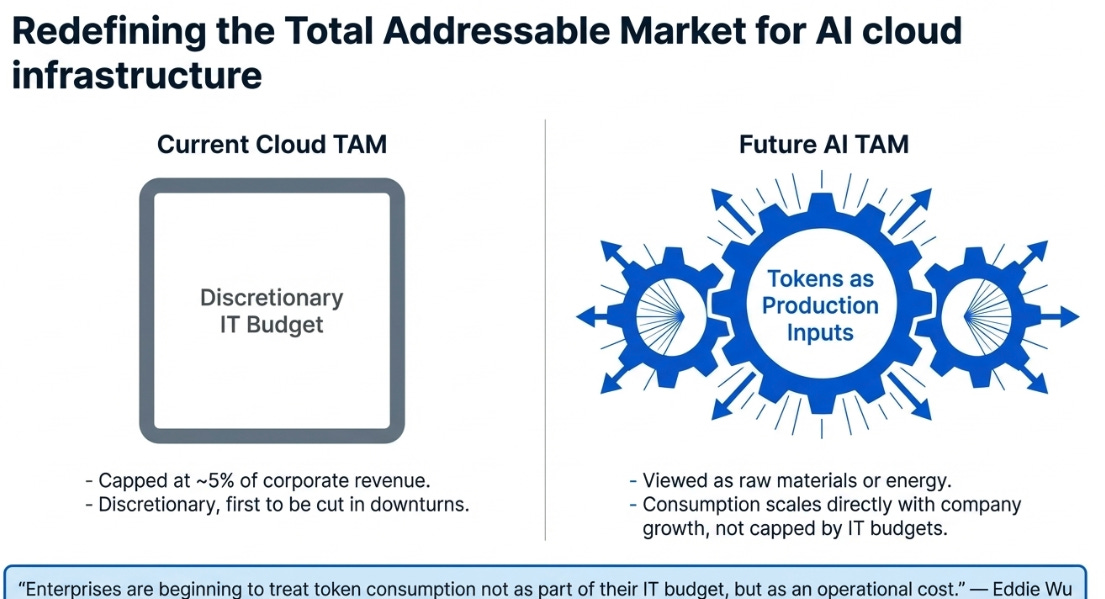

That integration matters because of something CEO Eddie Wu said on the earnings call that deserves more attention than it received. He argued that enterprises are beginning to treat token consumption not as part of their IT budget, but as an operational cost, a production input, like raw materials or energy. If that shift takes hold broadly, the implications for cloud economics are significant. IT budgets have traditionally represented around 5% of corporate revenue. They are discretionary, capped, and among the first expenses cut in a downturn. Production inputs are different. Companies consume more of them as they grow, not less. If AI tokens follow that path, from experimental to operational to simply part of how work gets done, then the addressable market for AI infrastructure is not the current cloud TAM. It is considerably larger.

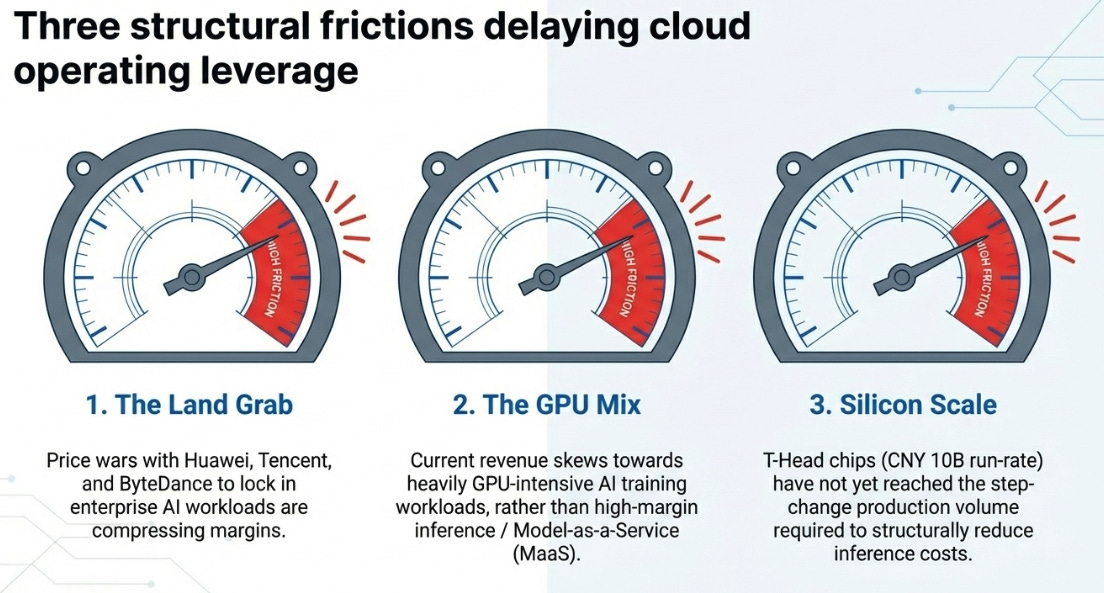

This should raise a natural question: if cloud revenue is growing 36% and the addressable market is expanding, why hasn’t operating leverage appeared? The segment’s adjusted EBITA margin was 9%, essentially flat year-over-year despite accelerating revenue. Three factors explain the gap. First, the China cloud market is in a land-grab phase where Alibaba, Huawei, Tencent, and ByteDance are all competing aggressively on price to lock in enterprise AI workloads, compressing margins even as volumes surge. Second, the current revenue mix skews toward GPU-intensive AI training workloads, which carry lower margins than the inference and model-as-a-service offerings that should eventually dominate. Third, T-Head’s proprietary chips, which could structurally reduce inference costs, have shipped 470,000 units with annual revenue at the CNY 10 billion level, meaningful but not yet at the scale where they materially alter the cloud segment’s cost structure. Management hinted that cost improvements from T-Head may not arrive gradually but as a step-change when production volume reaches a sufficient threshold. That is worth watching closely, but it is a claim about the future, not a feature of the present.

And a note of caution on the Qwen figures. The 140 million transaction number came during a Chinese New Year campaign with significant promotional support, the kind of environment designed to produce impressive launch metrics. What matters more is whether users return to Qwen for purchases in March and April without the promotional nudge. Repeat rate, incremental GMV relative to traditional Taobao flows, and average order value through the AI interface are the metrics that will separate a successful product from a subsidized launch. Those numbers do not exist yet.

The part that got harder

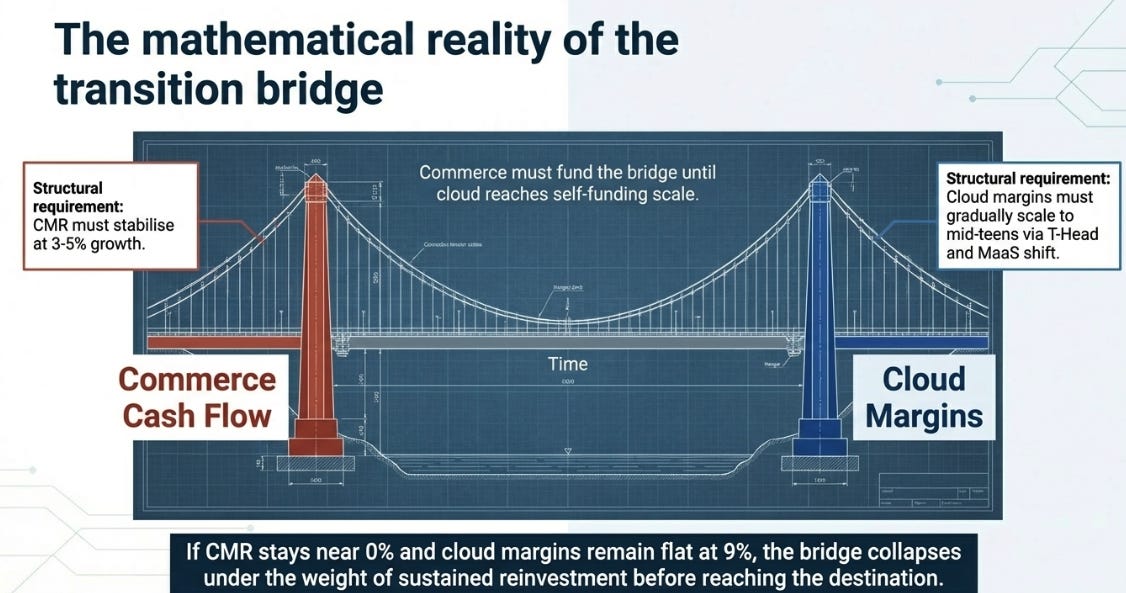

If the previous section described the destination, this section describes the bridge. And the bridge is narrower than we assumed in January.

Start with customer management revenue. Growing 1% sounds like stagnation, but it is actually worse than that in context. Taobao’s monthly active consumers grew by double digits. The 88VIP membership program surpassed 59 million members. Annual active consumers increased by 150 million in calendar 2025. All of those engagement metrics improved, and yet the revenue Alibaba earns from advertising and commissions on those users barely moved. The explanation is compositional: the new users arriving through quick commerce carry structurally lower spending levels and purchase frequency than existing users. Management acknowledged this on the call. The software service fee that had provided a tailwind to CMR in prior quarters is now fully lapped. Management said the March quarter is showing “significant recovery” in both physical goods GMV and CMR trends. That forward guidance is the single most important near-term test of the thesis. But guidance is a claim, not evidence.

Then there is quick commerce itself. Management gave the most specific financial targets yet: over RMB 1 trillion in GMV by fiscal year 2028, positive cash flow at that scale, and profitability in fiscal year 2029. That timeline is more concrete than what we had before, and it is also later than our base case assumed. Quick commerce may well be strategically necessary, if Meituan owns the daily “I need this now” intent and Alibaba does not contest it, the entire ecosystem gradually loses relevance in consumers’ daily routines. But strategic necessity does not make the economics pleasant. The business is still consuming cash, and it will continue to do so for years.

These two problems connect through a specific equation. Alibaba’s transformation depends on commerce cash flow holding long enough for cloud to reach the scale and margin structure where it becomes self-funding. If customer management revenue stabilizes in the 3-5% growth range and cloud margins gradually improve toward the mid-teens as T-Head scales and the revenue mix shifts toward higher-margin model-as-a-service offerings, the math works. Commerce funds the bridge; cloud becomes the destination. If customer management revenue stays near zero growth and cloud margins remain flat, the bridge is too narrow to support the crossing. That rate equation, how fast commerce decays relative to how fast cloud margins improve, is the single most important variable for the stock over the next two years.

What we think now

We are more confident than we were in January that the AI and cloud demand story is real and durable. Qwen’s distribution inside the ecosystem, the cloud acceleration, and the early evidence of agentic transaction execution are stronger signals than we had two months ago, with the caveat that the execution evidence is still early and promotional in nature.

We are less confident that commerce will recover quickly enough to make the transition financially comfortable. The 1% CMR print, the elevated marketing spend, and the pushed-out quick commerce timeline all suggest the funding side of the equation is weaker than we modeled.

Where we differ from the prevailing market view is on what matters more: the level or the direction. The market is looking at a commerce company with 1% CMR growth and a 9% cloud margin and seeing a structurally impaired conglomerate. We are looking at a cloud business that has accelerated from 7% to 36% in four quarters and asking what this company’s earnings mix looks like when cloud is 25% of revenue instead of 15%. If we are wrong, it will be because commerce decayed faster than cloud could compensate, and the March quarter CMR print is the first real test of that.

Three years from now

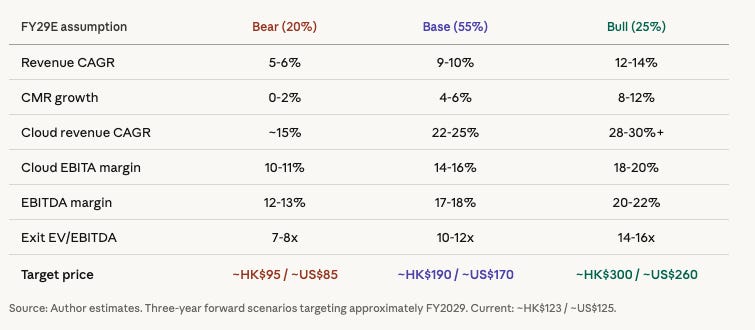

We model three scenarios for roughly fiscal year 2029.

The bear case values the stock at roughly HK$95, or around US$85. Revenue grows 5-6% annually, CMR stagnates near 0-2%, cloud decelerates to the mid-teens, and cloud margins remain around 10-11%. Quick commerce misses the FY29 profitability target. EBITDA margins stay at 12-13%. The market applies 7-8x. We assign this 20% probability.

The base case reaches roughly HK$190, or around US$170. Revenue grows 9-10% annually. CMR recovers to 4-6% as new user cohorts mature and AI-powered merchant tools improve returns. Cloud sustains 22-25% growth with margins expanding to 14-16% as T-Head scales and MaaS becomes a larger share. Quick commerce reaches breakeven by FY28. Sales and marketing normalizes to 20-21%. EBITDA margins recover to 17-18%. The market applies 10-12x. We assign this 55% probability.

The bull case reaches roughly HK$300, or around US$260. Revenue grows 12-14% annually. The token-as-production-input thesis materializes broadly. Cloud sustains 28-30% growth with margins reaching 18-20% as T-Head surpasses one million chips and inference cost advantages compound. CMR re-accelerates to 8-12%. EBITDA margins reach 20-22%. The market applies 14-16x. We assign this 25% probability.

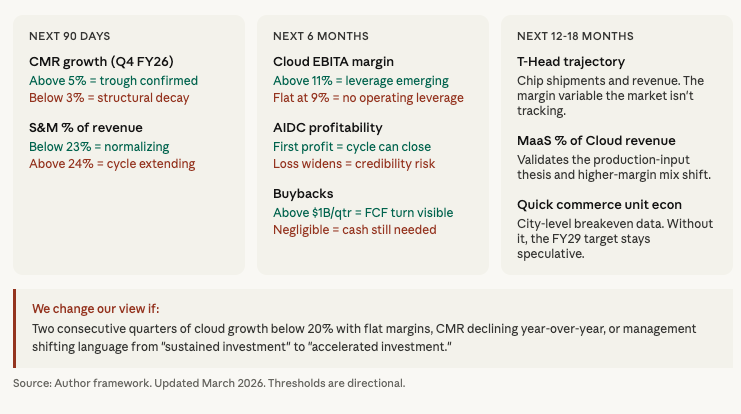

What we are tracking

In the next 90 days, we are watching two things. Customer management revenue growth in the March quarter: above 5% confirms the December trough was seasonal; below 3% suggests the impairment is structural. And sales and marketing as a percentage of revenue: a move below 23% would be the first real signal that spending is normalizing.

Over the next six months, the signposts shift to cloud profitability and capital allocation. Cloud EBITA margin crossing above 11% in any quarter would indicate that operating leverage is beginning to emerge. A return to share buybacks above $1 billion per quarter would signal that management sees the free cash flow turn approaching. And the first profitable quarter from the international commerce segment would demonstrate that Alibaba can actually close an investment cycle.

Over the next twelve to eighteen months, the variables that matter most are the ones the market is not yet tracking. T-Head chip shipments and revenue will determine whether the non-linear margin improvement management hinted at is real. Model-as-a-service as a percentage of cloud revenue will validate or undermine the production-input thesis. And quick commerce unit economics at the city level will provide the first hard evidence of whether the frequency layer can be more than a necessary cost.

We would change our view if we saw two consecutive quarters of cloud growth below 20% with flat margins, customer management revenue declining year-over-year, or management language shifting from “sustained investment” to “accelerated investment”, which would indicate the spending cycle is extending again rather than resolving.

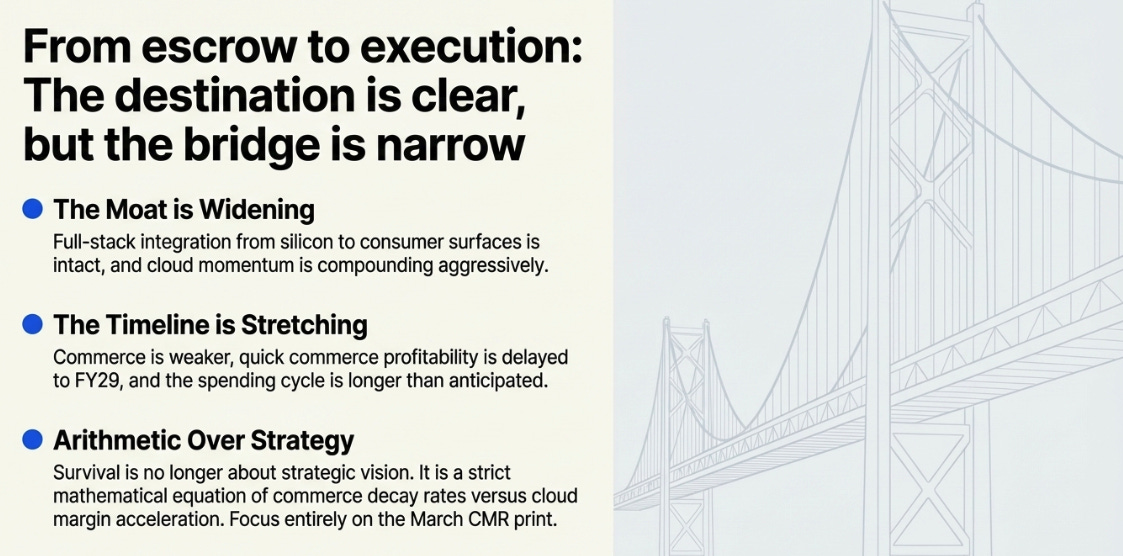

From escrow to execution

In 2003, Alibaba helped strangers trust each other enough to complete a transaction. In 2026, it is trying to help people trust software enough to act on their behalf. That is not a small shift. It changes what the company is, what it is worth, and how it should be evaluated.

After the December quarter, the destination looks more valuable than it did in January. Cloud is compounding. Qwen is executing real transactions at scale, though how durable that behaviour proves without promotional support remains to be seen. The full-stack integration from chips to models to consumer surfaces is, for now, intact and widening. But the bridge from here to there is narrower than we assumed, commerce is weaker, quick commerce is later, and the spending cycle is longer. Whether the bridge holds is not a question of strategy. It is a question of arithmetic, and the next two quarters will provide the numbers that answer it.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.