Alibaba 4QFY26 Earnings: The Bills Changed Shape

AI demand is real. The returns are not.

TL;DR

Alibaba’s Q4 validated the strategy but not the economics. Cloud external revenue grew 40%, AI revenue is now meaningful, and Qwen/MaaS monetization is becoming measurable, but adjusted net income was effectively zero, FCF was deeply negative, and Cloud margins remain around 9%.

The key debate is no longer whether Alibaba can grow AI/cloud revenue. It can. The real question is whether Alibaba can earn platform returns on that revenue, or whether China AI cloud becomes essential infrastructure with utility-like economics.

Our view is downgraded but not broken. The “Second Trust” thesis still survives: Qwen could become a trusted transaction layer across Taobao, Alipay, Amap, DingTalk, and Alibaba Cloud. But until Cloud margins expand, All Other losses narrow, and FCF turns, Alibaba is not China’s AWS; it is a very important company still trying to prove that importance belongs to shareholders.

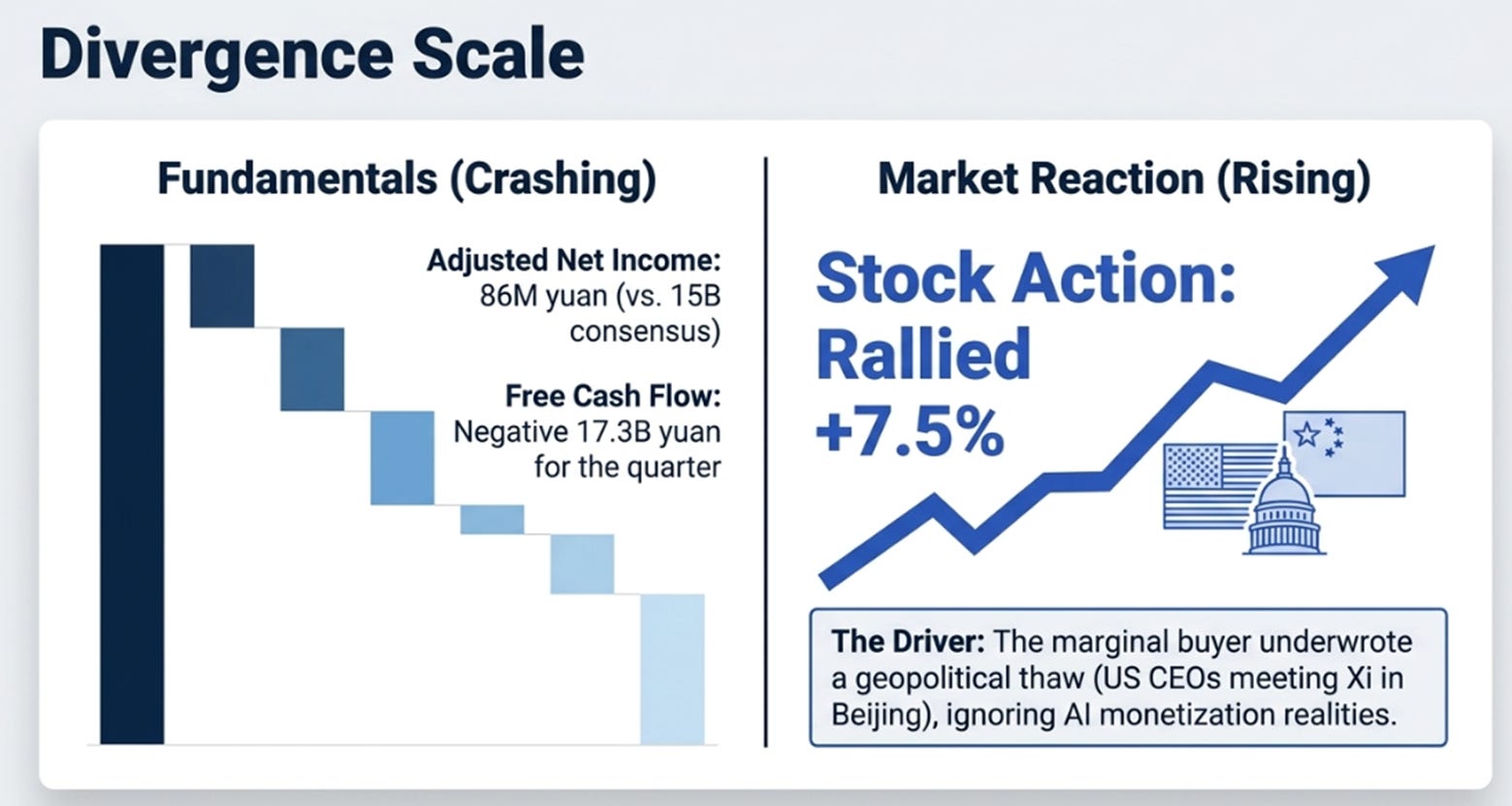

Alibaba’s Q4 FY2026 was the kind of quarter that makes a stock screen useless.

Revenue missed. Adjusted EBITDA missed badly. Adjusted net income was 86 million yuan, effectively zero, against consensus of 15 billion. Free cash flow was negative 17.3 billion yuan, bringing the full year to negative 46 billion. On any conventional earnings framework, the stock should have gone down and stayed down.

It went up 7.5%.

The rally was not purely about earnings. It coincided with reports that Jensen Huang and other US CEOs were joining Trump for meetings with Xi in Beijing, a broader China AI and détente trade that lifted the KraneShares China Internet ETF alongside Alibaba. The marginal buyer on May 13 may have been underwriting geopolitical thaw, not AI monetization milestones. That distinction matters for how durable the move is.

But the deeper question is not whether Alibaba had a good quarter. It did not. The question is whether the quarter made Alibaba’s long-term architecture more believable.

Our answer: yes, on demand, no on economics.

What We Said

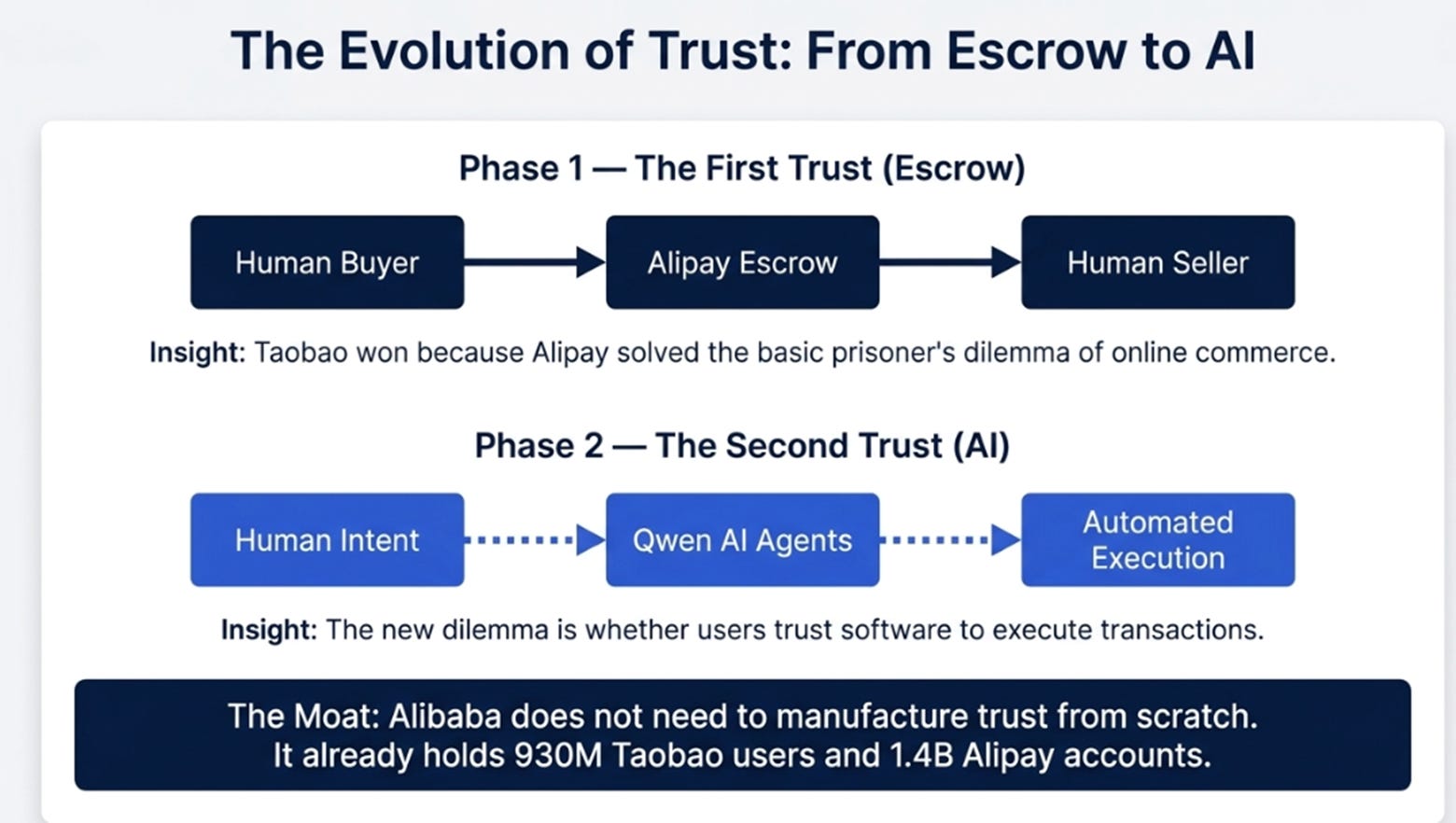

Our prior Alibaba thesis had a simple starting point: Alibaba’s original superpower was trust infrastructure. Taobao did not win merely because it was a better website. It won because Alipay solved the prisoner’s dilemma between buyers and sellers. The “Second Trust” thesis argued that AI creates a new version of that problem, will users trust software to execute transactions, not just suggest them?, and that Alibaba, with 930 million Taobao users and 1.4 billion Alipay accounts, does not need to manufacture that trust from scratch.

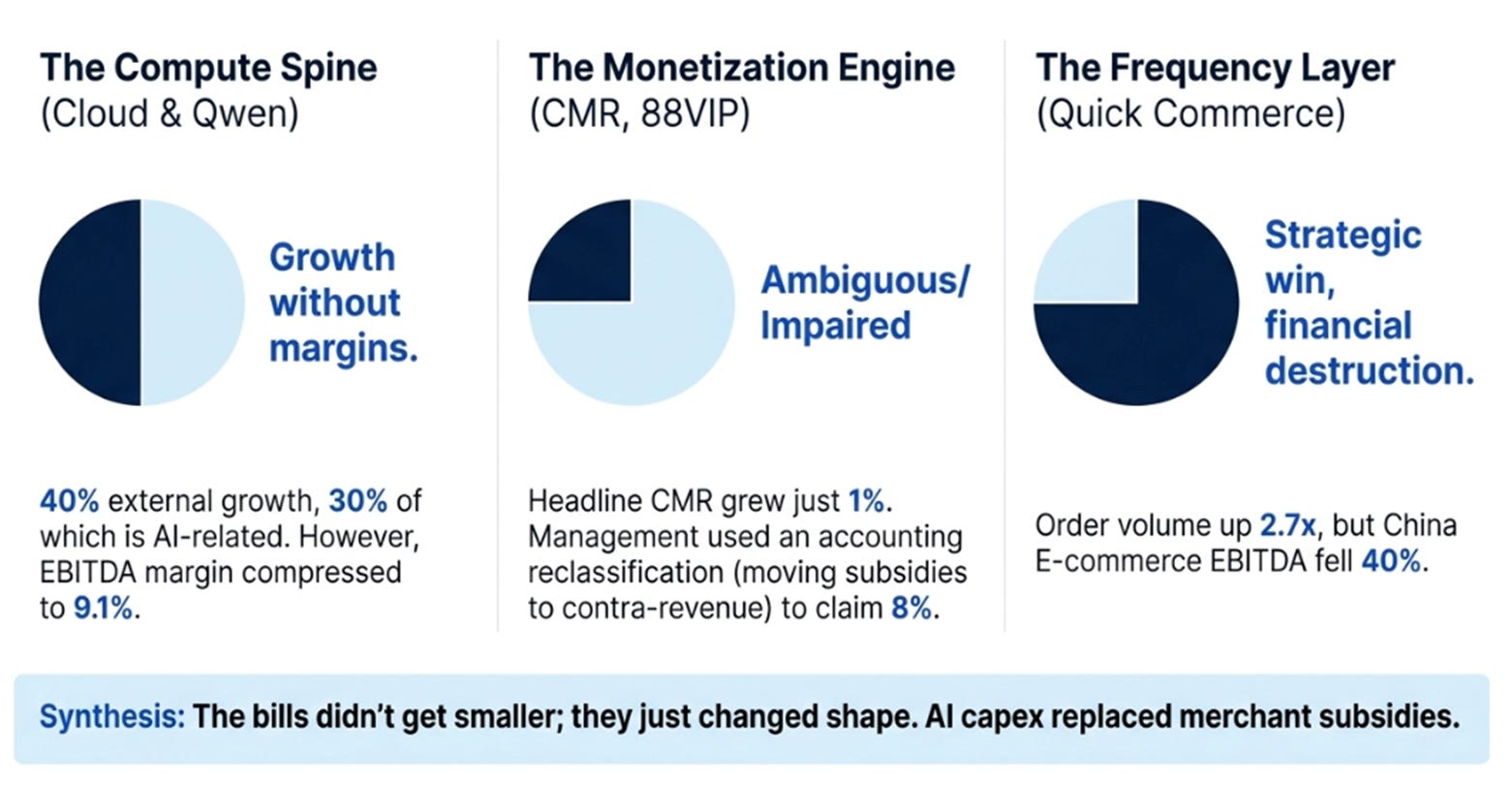

The investment case rested on three systems. The Compute Spine was Alibaba Cloud and Qwen: the infrastructure layer for China’s AI adoption. The Frequency Layer was quick commerce: expensive, but necessary to defend daily habit against Meituan. The Monetization Engine was CMR, Quanzhantui, 88VIP, and the software service fee: the mechanism by which user activity turned into platform revenue.

We said the thesis came down to one question: would the next few bills get smaller?

Q4 answered in the least satisfying way possible. The systems are more real than before. The bills are not smaller. They changed shape, AI capex replaced merchant subsidies, model development replaced user acquisition, but the total burden stayed the same.

Here is the scorecard:

The Compute Spine exceeded expectations. We set the bar at 25% cloud growth. Got 40% external growth. AI-related product revenue posted triple-digit growth for the eleventh consecutive quarter, now representing 30% of external cloud revenue. Management gave specific forward targets: MaaS ARR above 10 billion yuan in the June quarter, 30 billion yuan by year-end. The demand side validated more strongly than our bull case assumed.

But Cloud EBITDA margin compressed to 9.1%. We specified “stable or improving margins” as part of the criteria. We got the growth without the margins.

The Monetization Engine produced an ambiguous result. We set CMR growth above 8% as the structural validation threshold. Reported CMR grew 1%. Management then introduced an accounting reclassification, moving merchant subsidies from S&M expense to contra-revenue, and claimed 8% adjusted growth. When the company needs an accounting change to hit your validation number in the same quarter the headline metric decelerates to 1%, the appropriate response is not to accept the adjusted figure at face value. The Monetization Engine may be intact. It may be impaired. The fact that we cannot tell is itself a downgrade.

The Frequency Layer delivered exactly what we expected: strategic validation and financial destruction simultaneously. Quick commerce revenue surged 57%. Order volume was 2.7x. China E-Commerce EBITDA fell 40%. Management committed to positive unit economics by end of FY2027, the first specific timeline. Whether they hit it is the next test.

Free cash flow and buybacks confirmed our November warning. FCF was negative 46 billion yuan for the year. Buybacks did not resume. The $1.05/ADS dividend signals maintenance, not confidence. “Peak investment” was management narrative, not financial reality.

The strongest sentence I can write about Q4 is this: the strategic thesis validated; the economic thesis did not.

The Metric Alibaba Wants You to See

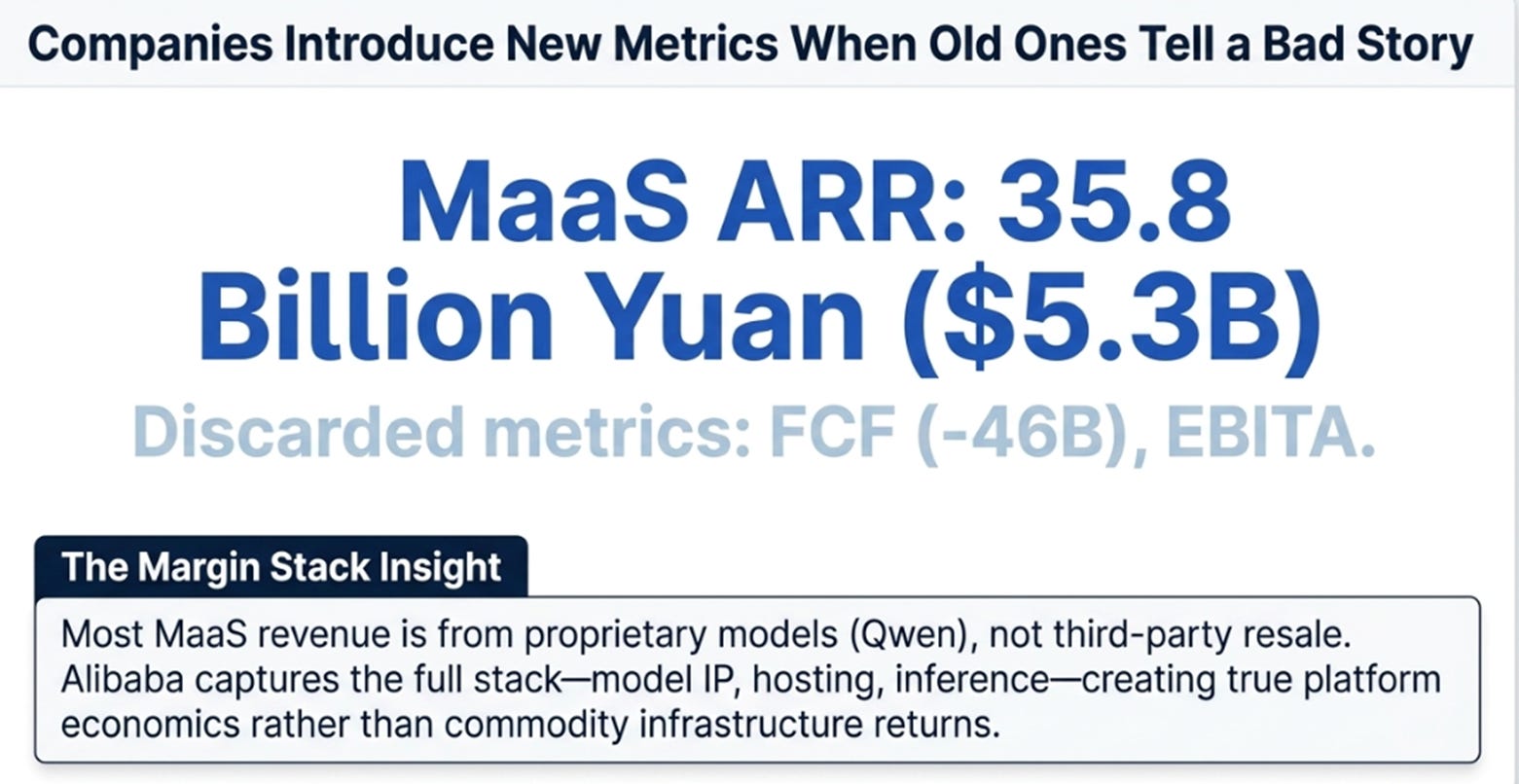

The most important disclosure was not the headline miss. It was the introduction of AI annualized recurring revenue as a primary metric.

Management disclosed quarterly AI revenue of 9 billion yuan, an ARR of roughly 35.8 billion yuan ($5.3 billion), and specific forward targets for MaaS monetization. Companies introduce new metrics when old ones tell a bad story. The old metrics, EBITA, net income, free cash flow, are catastrophic. The new metric is spectacular. That is not inherently dishonest. Amazon introduced the AWS disclosure the same way. But it should trigger analytical caution, not relief.

The critical detail most coverage missed: most MaaS revenue comes from Alibaba’s own proprietary models, Qwen, T-MOR, voice and video generation, not third-party resale. That means Alibaba captures the full margin stack: model IP, hosting, inference. Customers building on Qwen-specific APIs face real switching costs. If that pattern holds for multiple quarters, it changes what Cloud is worth, because it is platform economics rather than commodity infrastructure.

The Bloomberg screen still showed an overwhelmingly bullish analyst stack, 47 buys, 3 holds, and 1 sell, for a company that just printed near-zero adjusted net income. That is not proof the analysts are wrong. But it is a reason to haircut consensus estimates, which embed a near-quintuple in EBITDA over the next twelve months.

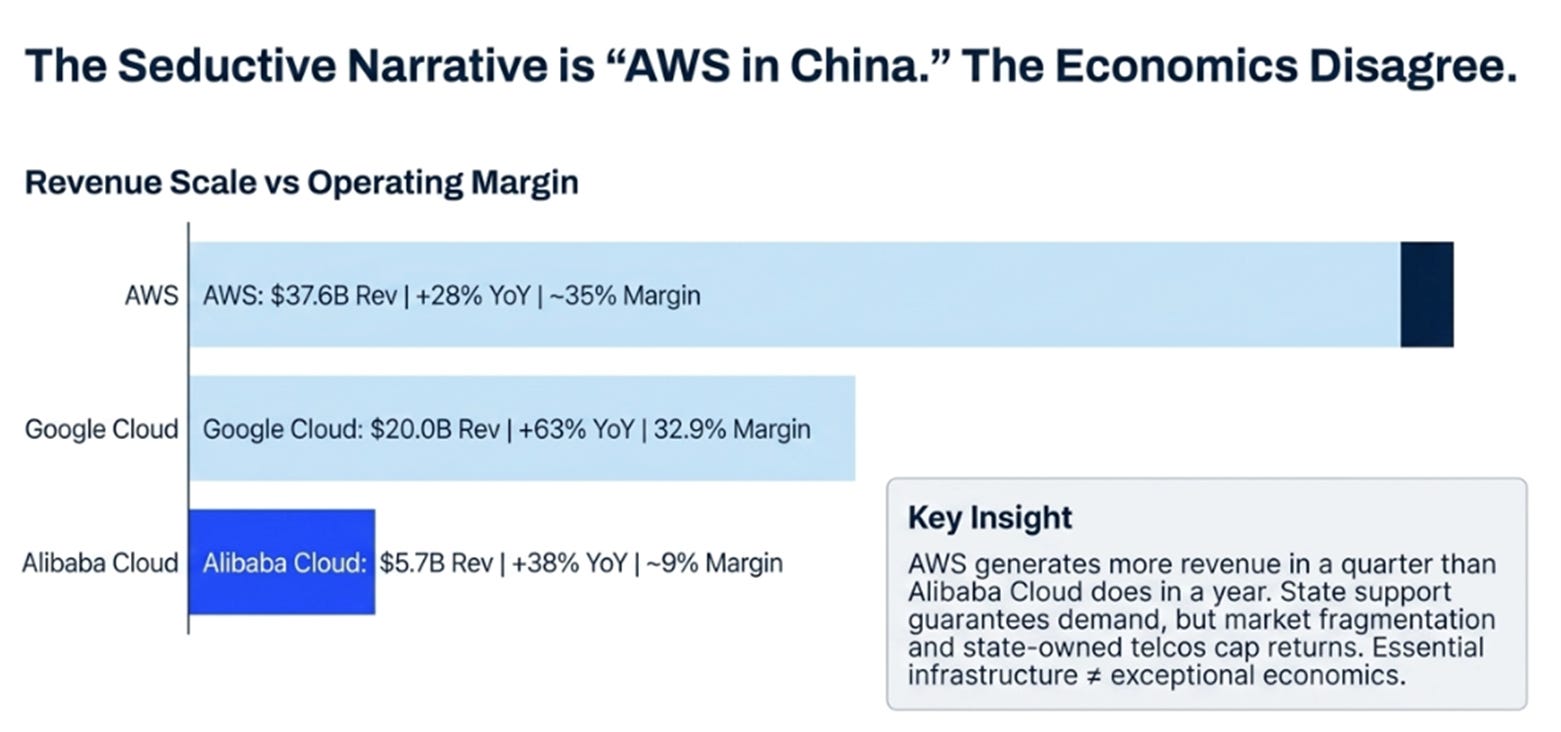

The Comparison That Reframes the Question

The biggest change to our view is not about Alibaba’s technology. It is about the returns investors should expect from that technology.

The seductive narrative is “AWS in China.” China skipped enterprise cloud adoption; AI forces that migration; Alibaba owns the leading domestic cloud; the stock re-rates. There is truth in that story. But the economics tell a different one.

Google Cloud is growing faster than Alibaba Cloud at 3.5x the revenue with margins nearly four times higher. AWS generates more quarterly revenue than Alibaba Cloud generates in a year. The entire Chinese cloud market is smaller than AWS alone.

The structural explanation is market fragmentation: seven-plus competitors for a market one-seventh the size of the US, with state-owned telcos pricing below cost. Server deployment costs have doubled year-over-year despite T-Head chip production. Google Cloud went from operating losses to 33% margins in roughly three years. Alibaba Cloud has been operating for fifteen years at sub-10% EBITDA margins.

This leads to the variant perception that I think matters most:

The market is debating whether Alibaba can grow AI/cloud revenue. The better question is whether Alibaba can earn platform returns on that revenue.

State support can guarantee demand, but it can also cap returns. If AI cloud is treated as national infrastructure, Alibaba may be allowed, even encouraged, to grow. But the same political economy that protects the market may also prevent Alibaba from extracting Western hyperscaler economics from it. In that world, Alibaba becomes essential without becoming exceptional.

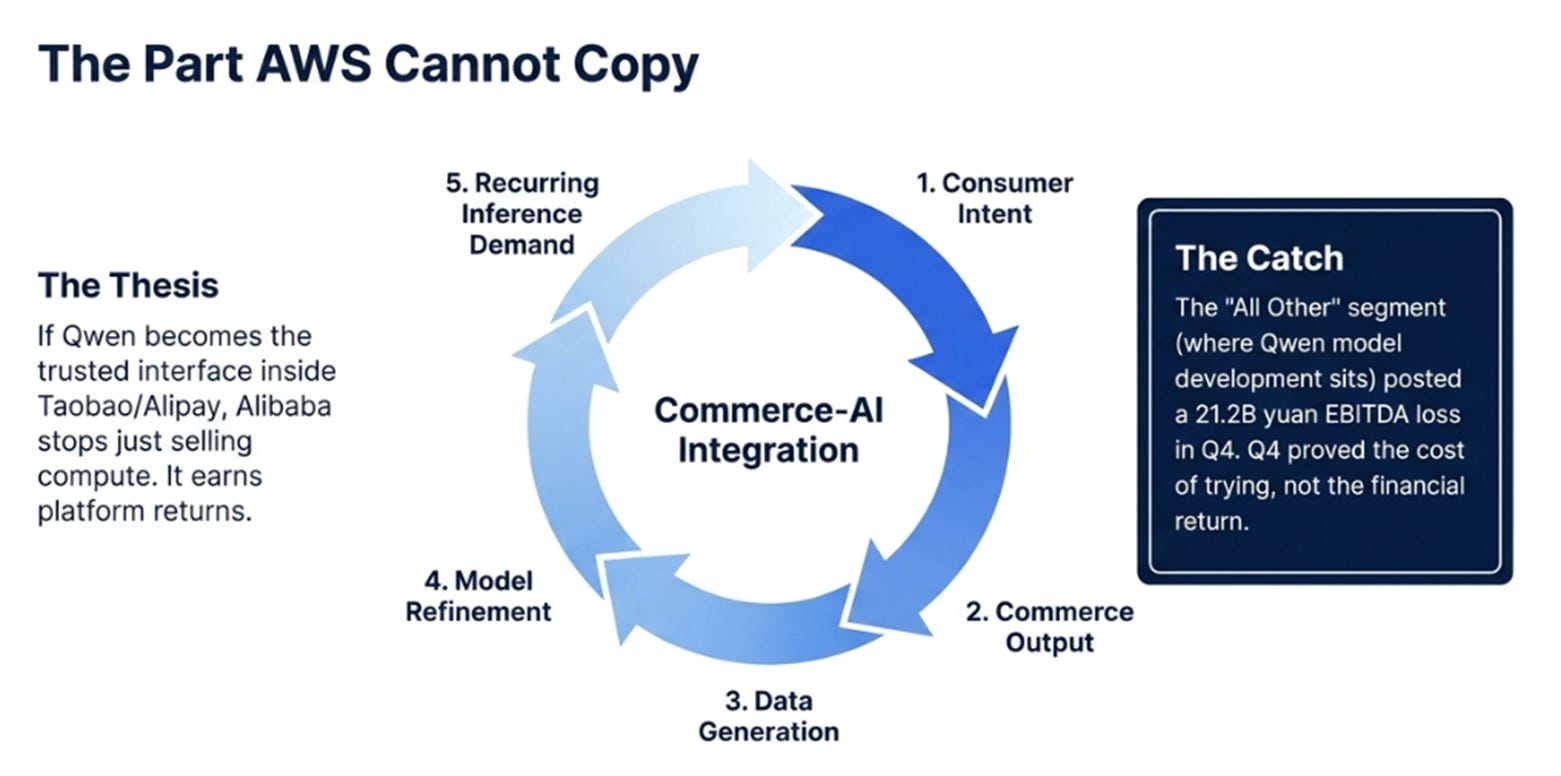

The Part AWS Cannot Copy

The only credible counter to the margin comparison is not better cloud infrastructure. It is the commerce integration that no Western hyperscaler can replicate.

AWS has better cloud economics. Google Cloud has better margin momentum. Microsoft has better enterprise distribution. Alibaba’s advantage is the possibility that Qwen becomes a trusted transaction interface inside Taobao, Alipay, Amap, DingTalk, and the merchant stack. If that happens, Alibaba is not merely selling compute. It is converting consumer intent into commerce, commerce into data, data into models, and models into recurring inference demand that runs on Alibaba Cloud.

That is the Second Trust thesis: trust scaled through AI agents that can decide, recommend, execute, and transact. It is also the only version of the bull case where Alibaba earns something better than utility-grade returns on its cloud investment.

Q4 did not prove it. Q4 only proved the cost of trying. The “All Other” segment, where Qwen model development and consumer AI sit, posted a 21.2 billion yuan EBITDA loss in a single quarter. The commerce-AI integration may work. But the financial evidence for it showing up in CMR or conversion rates is not yet visible.

Three Futures

Scenarios are useful only if they describe what the company becomes.

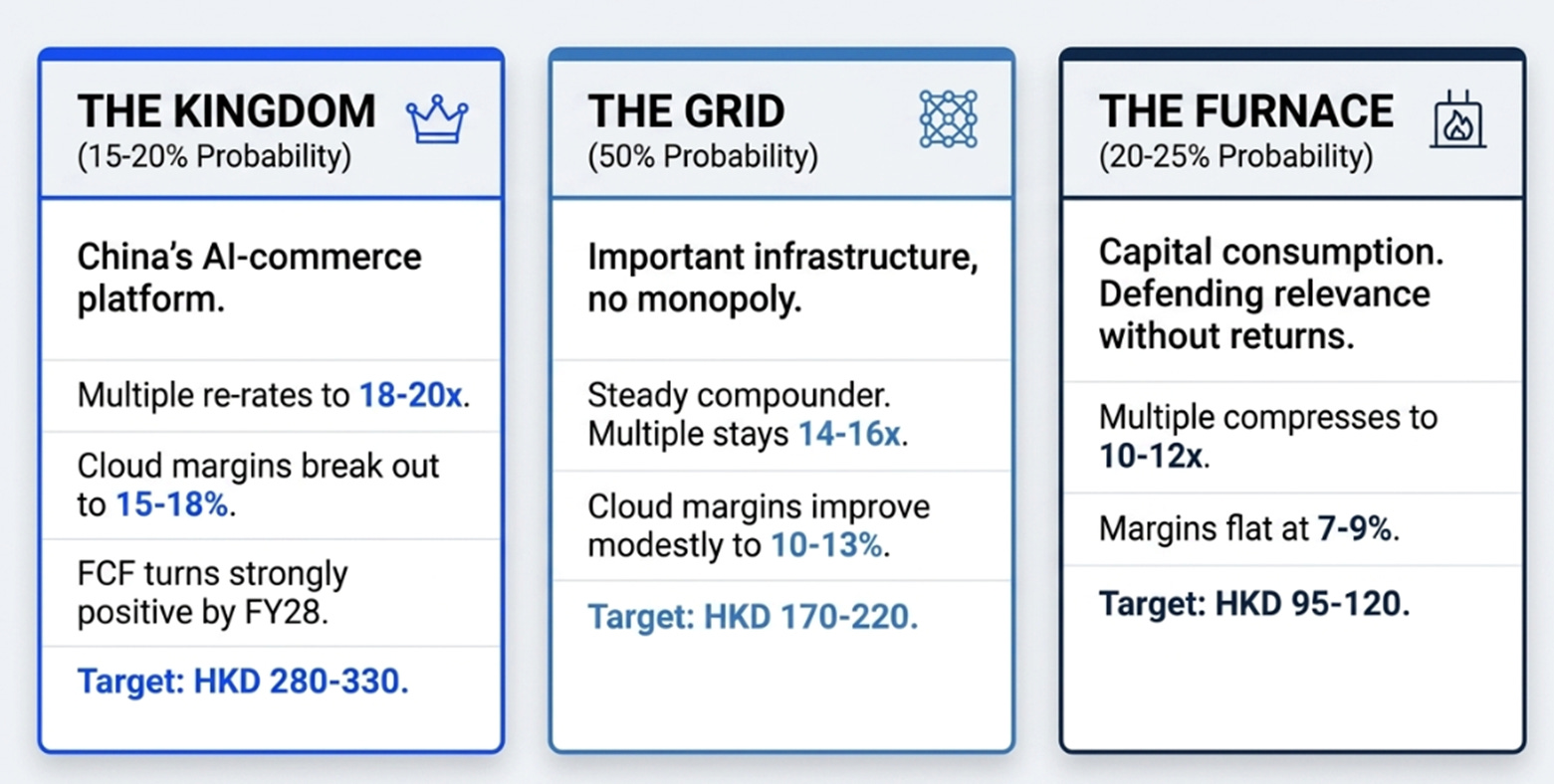

The Kingdom (15-20% probability → HKD 280-330)

Alibaba becomes China’s AI-commerce platform. Qwen becomes a transaction interface. Cloud growth sustains above 30%. AI becomes a majority of external cloud revenue. MaaS mix lifts Cloud margins toward 15-18%. Quick commerce breaks even. CMR grows 10%+ as AI tools improve merchant ROI. Revenue compounds at 12-14% through FY2029 with group net margins reaching 14-16%. FCF turns strongly positive by FY2028. Multiple re-rates to 18-20x.

This requires Chinese cloud margins to break their fifteen-year pattern AND the commerce-AI loop to produce measurable economic uplift. Possible but demanding.

The Grid (50% probability → HKD 170-220)

Alibaba becomes important infrastructure but not a platform monopoly. Cloud grows 20-25%. Margins improve modestly to 10-13%, better than today, but nowhere near Western levels. Quick commerce stops bleeding but never becomes a profit engine. CMR grows mid-to-high single digits. Revenue compounds at 8-10%. Net margins reach 11-13%. FCF turns positive but below prior expectations. Multiple stays at 14-16x.

This is what management is actually describing when Wu says ROI will be “extremely clear in 3-to-5 years.” Not a re-rating story. A steady compounder where returns come from earnings growth, not multiple expansion.

The Furnace (20-25% probability → HKD 95-120)

Alibaba keeps burning capital to defend relevance. Cloud grows but capex grows with it. Quick commerce remains a permanent tax. Qwen investment sits in All Other without visible payback. CMR slows. Revenue grows 4-6%. Margins stay flat at 7-9%. FCF remains weak. Multiple compresses to 10-12x.

This is not collapse. It is capital consumption, strategic importance without shareholder returns. Railroads were essential. Utilities are essential. Essential infrastructure does not automatically mean good equity.

A separate 10-15% probability covers geopolitical disruption, delisting, severe chip sanctions, Taiwan escalation, where fundamentals become irrelevant. We do not model it, but we size positions to survive it.

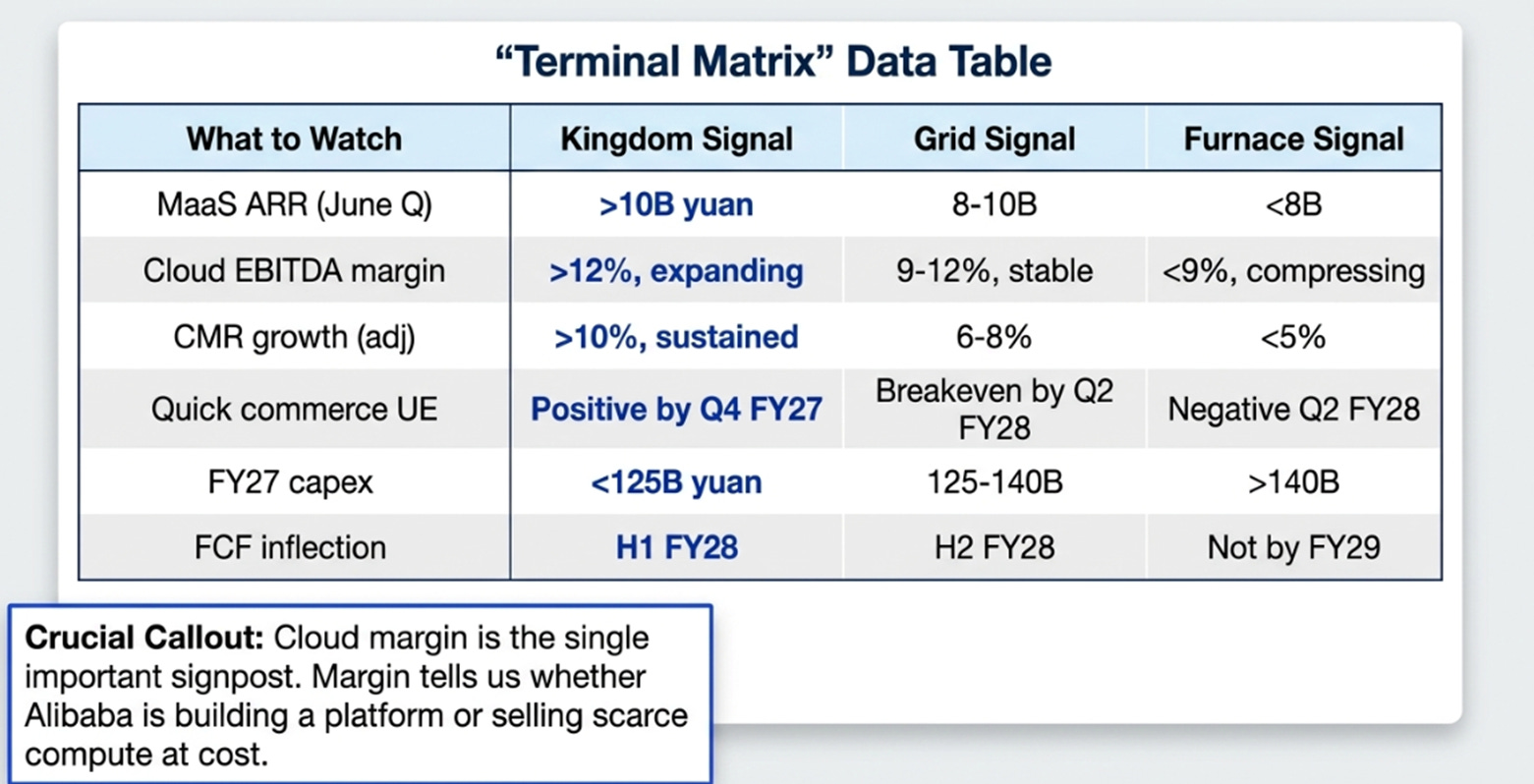

The Dashboard

The single most important signpost is Cloud margin. AI revenue growth will be easy to celebrate. Margin will tell us whether Alibaba is building a platform or selling scarce compute at cost.

The Bottom Line

Alibaba’s first trust machine was escrow. It made strangers comfortable transacting online, and that was enough to build one of China’s most important companies. The second trust machine is AI, Qwen deciding, recommending, executing, transacting across the largest consumer platform in China. If it works, Alibaba is not just a cloud infrastructure provider. It is the transaction and compute layer for China’s AI economy.

Q4 made that possibility more believable. It also made the cost impossible to ignore.

The old Alibaba compounded because trust scaled almost for free. The new Alibaba is trying to compound trust through data centers, chips, delivery riders, models, and AI agents. That can still work. But it is no longer enough to say the architecture is elegant.

Until Cloud margins expand, All Other losses narrow, and free cash flow turns, Alibaba is not China’s AWS. It is a very important company still trying to prove that importance belongs to shareholders. Fifteen years of margin data say the proof will not come. One quarter’s AI ARR disclosure says maybe it will.

I know which one I want to believe. I am waiting for the data to tell me which one is true.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.