Alphabet’s 1Q26: Four Markets, One Grid

The grid is no longer the thesis. It is the shared production function.

TL;DR

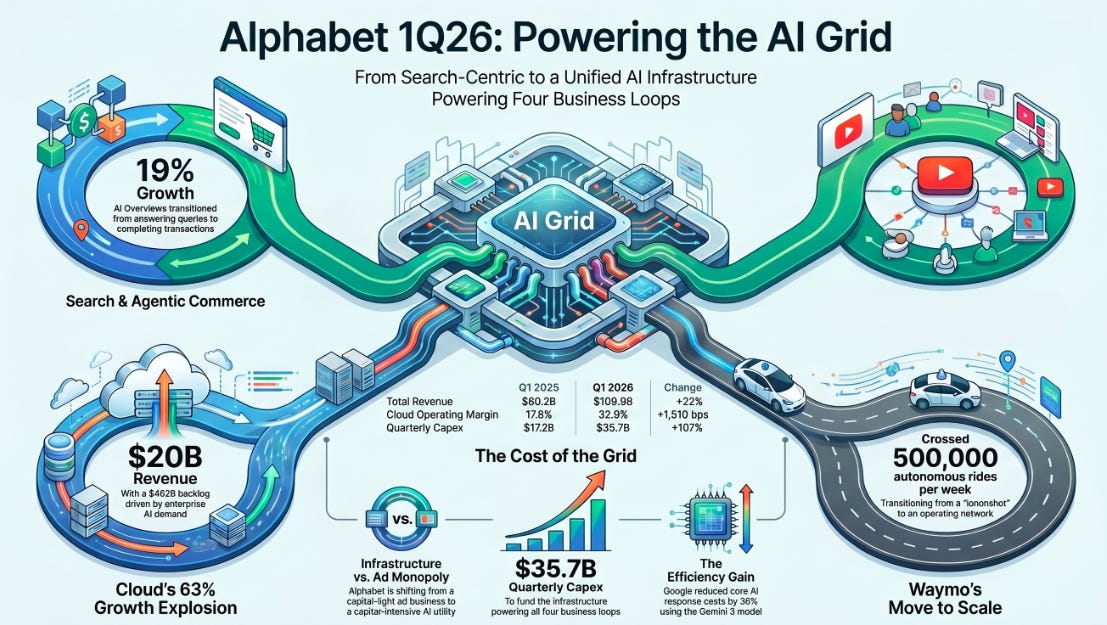

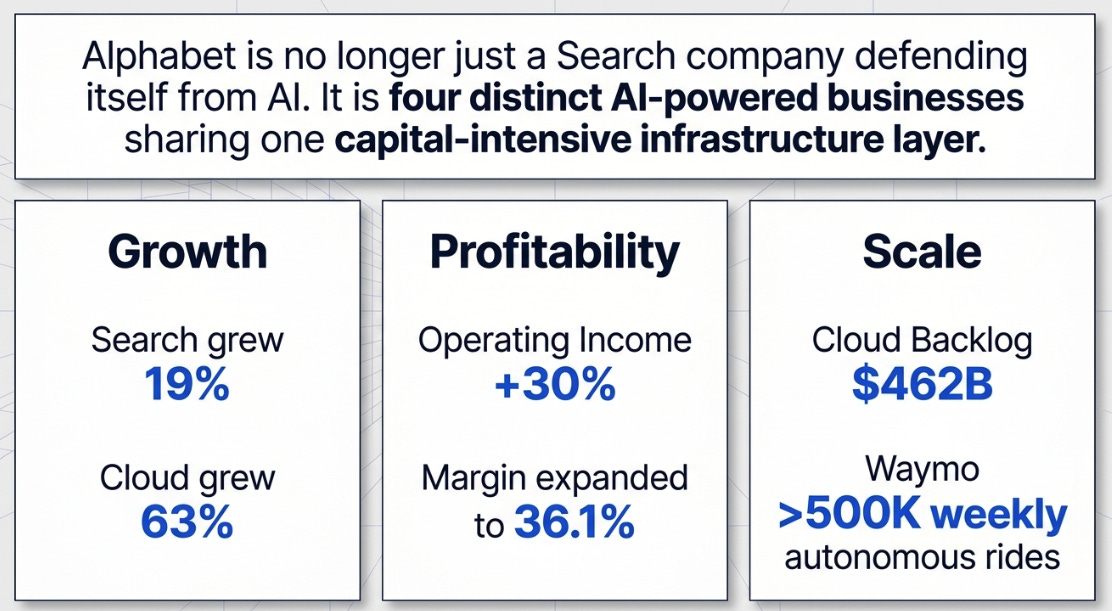

Alphabet is no longer just a Search company defending itself from AI; it is four AI-powered businesses sharing one infrastructure layer. Search compounds intent, Cloud compounds compute demand, YouTube compounds attention, and Waymo compounds autonomous miles.

Q1 2026 showed that the grid is starting to pay off. Search grew 19%, Cloud grew 63% with 32.9% margins and $462B of backlog, YouTube is layering subscriptions on top of living-room scale, and Waymo crossed 500K autonomous rides per week.

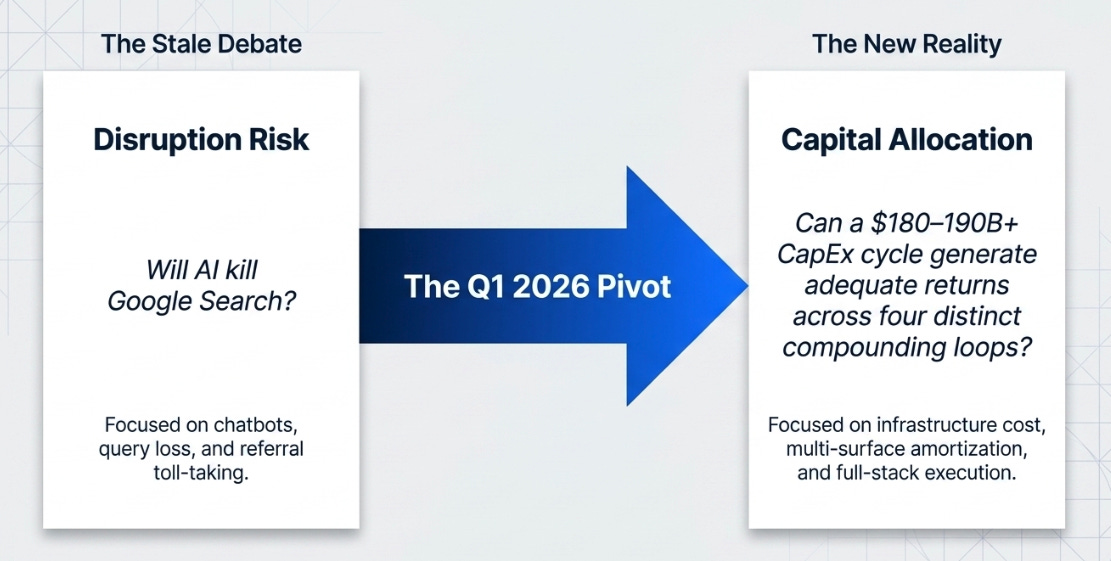

The debate has shifted from disruption risk to capital allocation. The question is no longer whether AI kills Google; it is whether Alphabet’s $180–190B+ capex cycle can generate adequate returns across four separate compounding loops.

Sundar Pichai summarized the quarter neatly: Alphabet’s AI investments and full-stack approach are now “lighting up every part of the business.” The numbers back him up. Revenue grew 22% to $109.9B, Search & Other grew 19%, Google Cloud grew 63%, operating income grew 30%, and operating margin expanded to 36.1%.

Those are excellent numbers. They are not the most interesting thing about the quarter.

For the past year, the right way to understand Alphabet was that it was not trying to win AI by building the best chatbot. It was trying to build the grid: the infrastructure, silicon, models, products, and distribution layer that could make intelligence cheap, ubiquitous, and profitable.

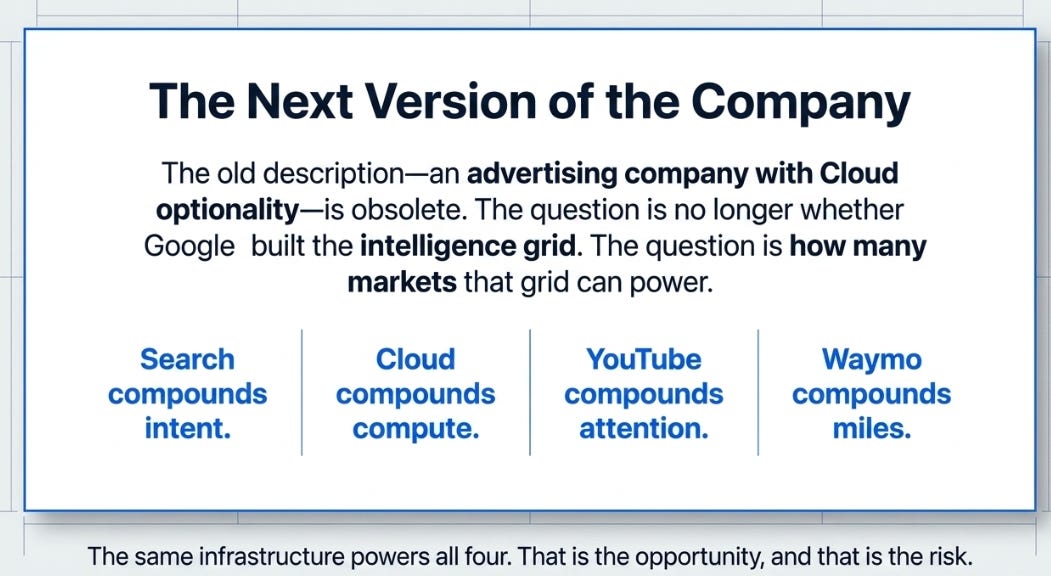

Q1 2026 sharpens that thesis. The grid is not the end state. The grid is the shared production function for four businesses: Search, Google Cloud, YouTube, and Waymo. Each uses the same AI infrastructure. Each compounds differently. Search compounds intent. Cloud compounds compute demand. YouTube compounds attention. Waymo compounds autonomous miles.

That is why Alphabet is harder to analyze than a normal mega-cap. It is not one AI story. It is four AI-powered business-model upgrades funded by one balance sheet.

The question is no longer “Will AI kill Google?” That question looks increasingly stale. The question is:

Can Alphabet turn one massive AI infrastructure investment cycle into four separate compounding loops?

Q1 suggests yes. It also makes the cost impossible to ignore.

The Four Loops

The mistake is to think of Alphabet’s businesses as reporting segments. They are really four markets in which Alphabet is trying to change the unit of competition.

The same stack, TPUs, GPUs, data centers, Gemini models, agents, and developer tools, increasingly powers all four. That is the point.

The Agentic Pivot

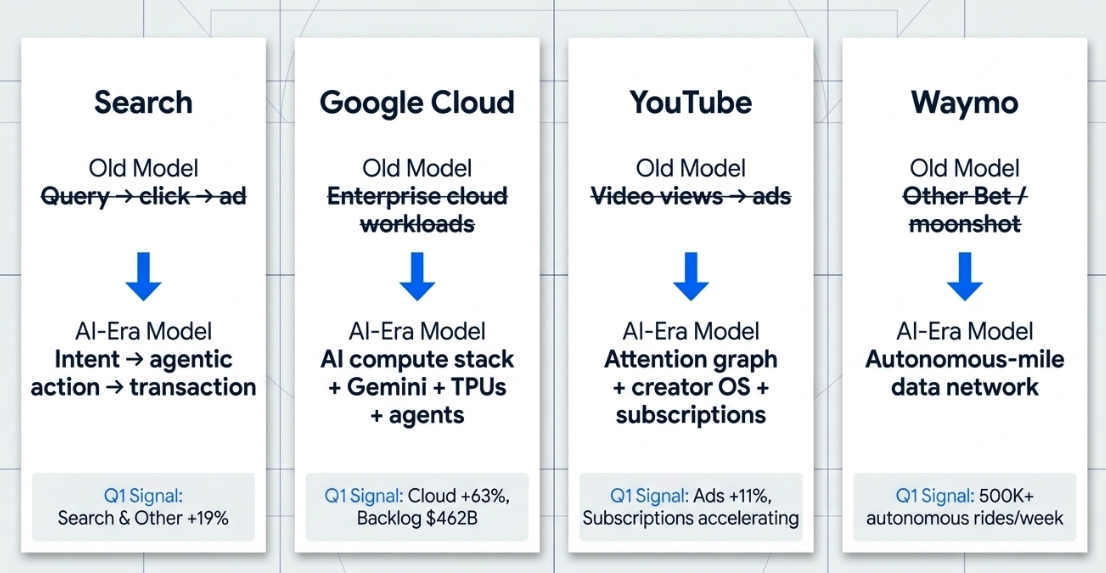

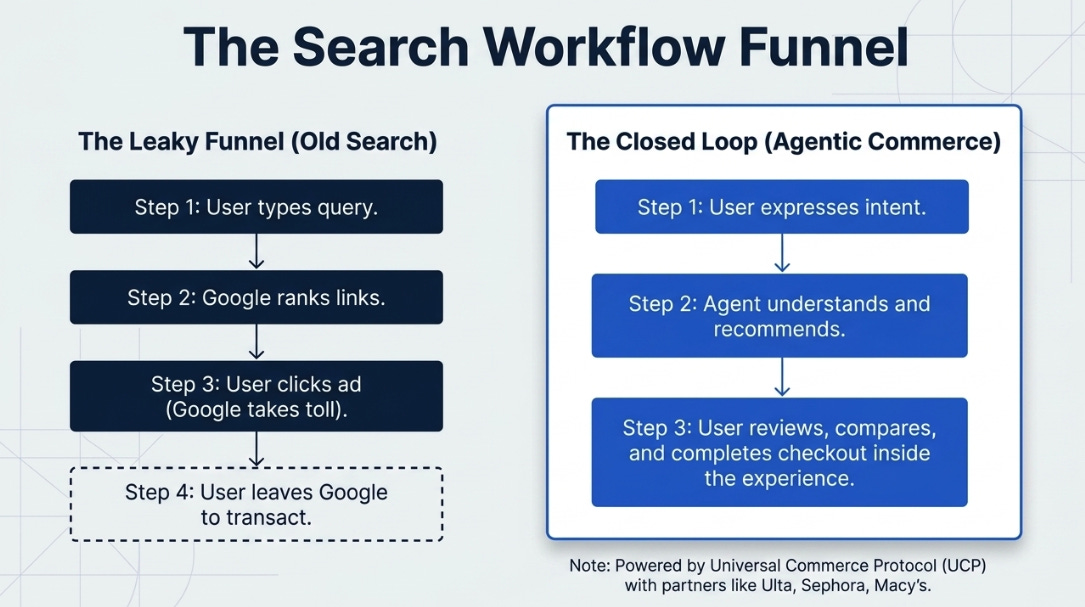

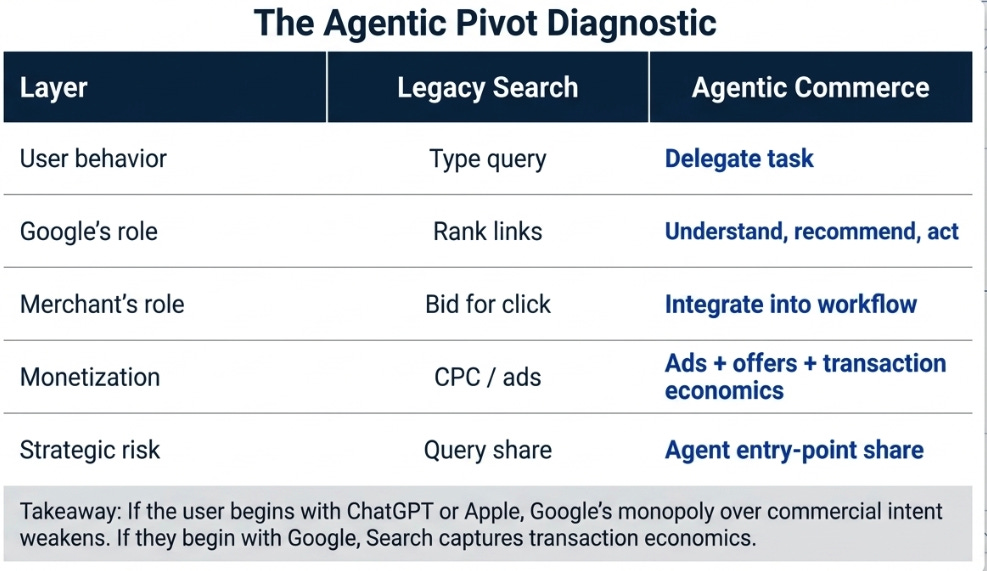

For 25 years, Google’s Search business was simple. A user had intent. Google matched that intent to information and advertising. The user clicked. The transaction happened somewhere else. Google took a toll for the referral.

That was an extraordinary business. It was also why generative AI looked so dangerous. If AI answered the question directly, what happened to the click? If the click disappeared, what happened to the ad? If the ad weakened, what funded the rest of Alphabet?

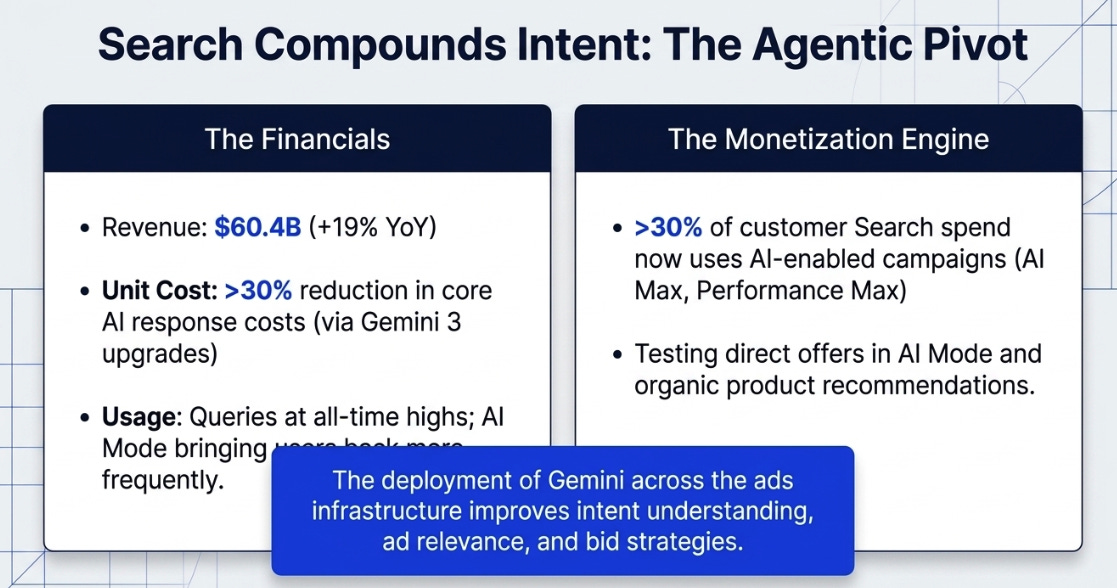

Q1 narrows that bear case. Search & Other grew 19% to $60.4B, and management said AI Mode and AI Overviews are bringing users back to Search more, with queries at all-time highs. Pichai also said Google reduced the cost of core AI responses by more than 30% after upgrading AI Overviews and AI Mode to Gemini 3.

That matters. AI is not merely adding cost to Search; it is expanding usage while Google pushes down unit cost.

But the more important change is the mechanism of monetization. Philipp Schindler said Gemini is being deployed across the ads infrastructure, improving intent understanding, ad relevance, and bid strategies. More than 30% of customer Search spend now uses AI-enabled campaigns such as AI Max or Performance Max. Google is also testing direct offers in AI Mode and new ad formats around organic product recommendations.

Then came the bigger reveal: agentic commerce.

The Universal Commerce Protocol added Amazon, Meta, Microsoft, Salesforce, and Stripe to its technology council, joining Shopify, Etsy, Target, Wayfair, and Google. Partners such as Sephora, Macy’s, and Ulta Beauty are rolling out UCP, and Ulta launched agentic commerce inside AI Mode, Search, and Gemini. Users can review recommendations, compare products, and complete checkout inside the experience.

That is a different business.

To be clear, this is not yet proven. Alphabet has not disclosed GMV, take rate, conversion rate, or transaction revenue from agentic commerce. Google has tried commerce before and failed more than once. The difference this time is that the agent changes the user behavior: the user does not need to leave, the merchant does not need to rebuild the storefront, and the payment rails can sit underneath the assistant.

The old Google monetized intent by sending users elsewhere. The new Google wants to monetize intent by completing the task.

The bear case is no longer simply “AI reduces queries.” Q1 argues against that. The new bear case is that someone else becomes the starting point for agentic commerce.

If the user begins with Google, Search expands from referral layer to transaction interface. If the user begins with ChatGPT, Perplexity, Apple, Amazon, or a vertical agent, Google’s historic monopoly over commercial intent becomes less relevant.

That is the real fight.

The Grid Gets Paid

Cloud is where the grid becomes an external revenue stream.

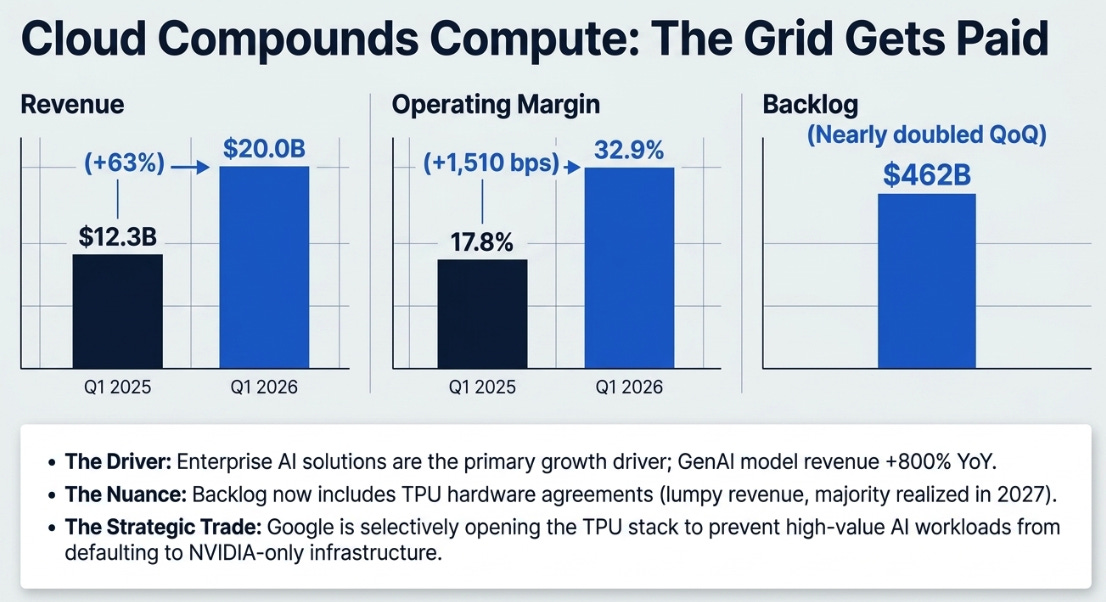

Google Cloud revenue grew 63% to $20.0B. Operating income tripled to $6.6B. Operating margin expanded from 17.8% to 32.9%. Backlog nearly doubled sequentially to $462B.

This is no longer optionality.

Management’s commentary was even stronger than the numbers. Pichai said enterprise AI solutions became Cloud’s primary growth driver for the first time, revenue from products built on Google’s GenAI models grew nearly 800% year-over-year, new customer acquisition doubled, and multiple $1B+ deals were signed.

This is the grid thesis made tangible. Alphabet owns models, silicon, data centers, cloud infrastructure, enterprise applications, agent platforms, and now a security layer through Wiz. That vertical integration is no longer just a technical claim. It is appearing in revenue, margins, and backlog.

The new wrinkle is TPU hardware.

Pichai said Google will begin delivering TPUs to a select group of customers in their own data centers. CFO Anat Ashkenazi later clarified that TPU hardware agreements are included in Cloud backlog, that the majority of backlog is still typical GCP contracts, that just over 50% of backlog should convert into revenue over the next 24 months, and that TPU hardware revenue will be lumpy, with a small percentage recognized later in 2026 and the majority in 2027.

This is not Google “becoming NVIDIA.” It is subtler. Google is selectively opening the TPU stack to prevent the highest-value AI workloads from defaulting to NVIDIA-only infrastructure.

That may be the right trade. It also creates a new disclosure problem.

A dollar of recurring GCP consumption is not the same as a dollar of lumpy TPU hardware revenue. If the backlog is mostly durable GCP and AI services, it deserves a high-quality multiple. If a material portion becomes lower-margin hardware, investors will discount it. Management said the majority is still typical GCP contracts, which is reassuring; the fact that they needed to say it tells you what to watch.

YouTube Is Not an Ad Line Item

YouTube is the business most often underweighted in Alphabet analysis.

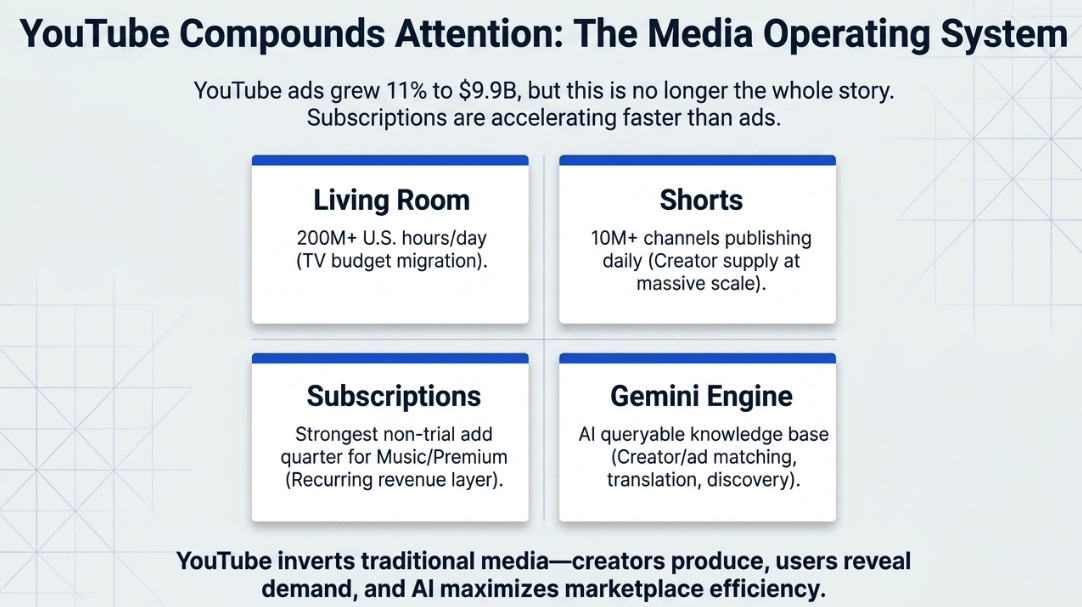

YouTube ads grew 11% to $9.9B. That is solid, but it looks underwhelming next to Search growing 19% and Cloud growing 63%.

The problem is that YouTube ads are no longer the whole story.

Pichai said U.S. viewers watch more than 200M hours of YouTube in the living room daily. More than 10M channels now publish Shorts each day. YouTube Music and Premium had their largest quarterly increase in non-trial subscribers since YouTube Premium launched. Schindler added that YouTube subscriptions revenue continues to grow faster than ads, especially YouTube Music and Premium.

This is not just a video ad platform. It is a media operating system.

Traditional media companies decide what to produce, spend the money upfront, and hope the audience shows up. YouTube inverts the model. Creators produce the content. Users reveal demand. YouTube shares revenue when the content works.

AI makes that more valuable. Gemini can improve creator matching, ad matching, content discovery, translation, summarization, clipping, and eventually video search. YouTube may become the world’s largest AI-queryable video knowledge base.

That is why the disclosure gap matters. If YouTube ads are growing 11%, but YouTube subscriptions are growing faster, then the ad line understates the business. Alphabet should disclose total YouTube revenue, including subscriptions. Until it does, the market will likely continue to undervalue YouTube as a standalone platform.

Search is the intent graph. YouTube is the attention graph. Both become more valuable when AI can understand and act on them.

Waymo Becomes Measurable

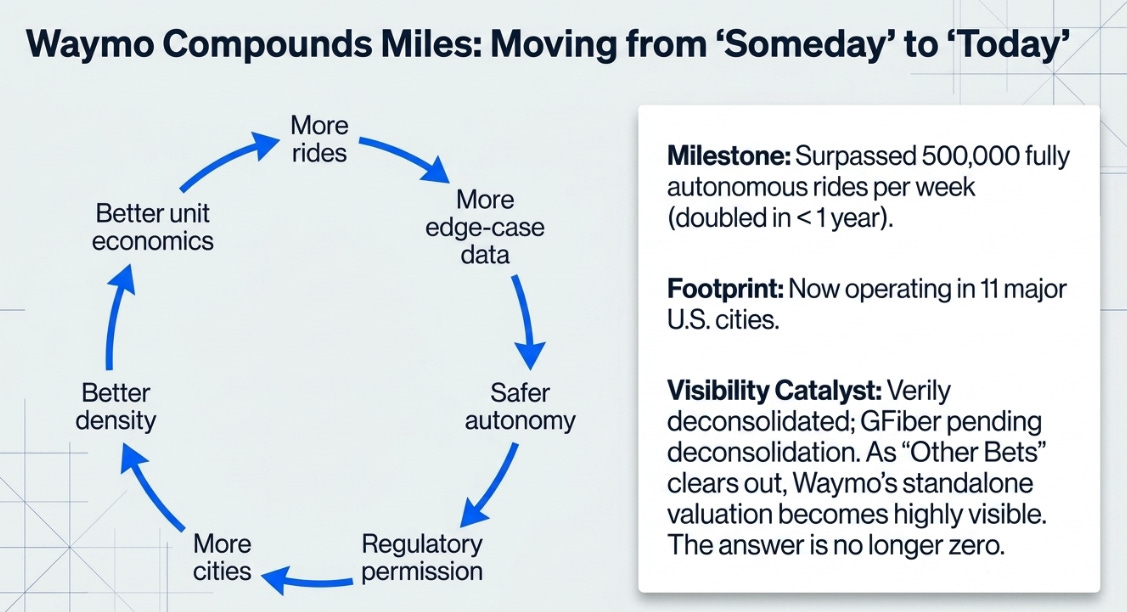

Waymo used to live in the “someday” bucket.

Someday autonomy works. Someday rides scale. Someday the unit economics matter. Someday the valuation shows up.

Q1 moved Waymo closer to today.

Waymo surpassed 500,000 fully autonomous rides per week, doubling in less than a year. It launched in Nashville, added six new cities so far in 2026, and now operates in 11 major U.S. cities.

This is still not a financial story. Other Bets revenue was only $411M, and Other Bets lost $2.1B.

But Waymo is no longer merely a science project. It is an operating network.

The other important disclosure is what Alphabet is doing around Waymo. Verily completed an external capital raise and was deconsolidated. GFiber announced a combination with Astound Broadband and is expected to be deconsolidated when the deal closes. Management said Alphabet will continue allocating significant resources to businesses where it sees meaningful opportunities, such as Waymo.

This matters because Other Bets has historically obscured as much as it revealed. If Verily and GFiber move out of the consolidated segment, Waymo becomes more visible. That does not mean an IPO or tracking stock is imminent. It does mean the market will increasingly have to ask what Waymo is worth.

The answer is not zero anymore.

The Cost of the Grid

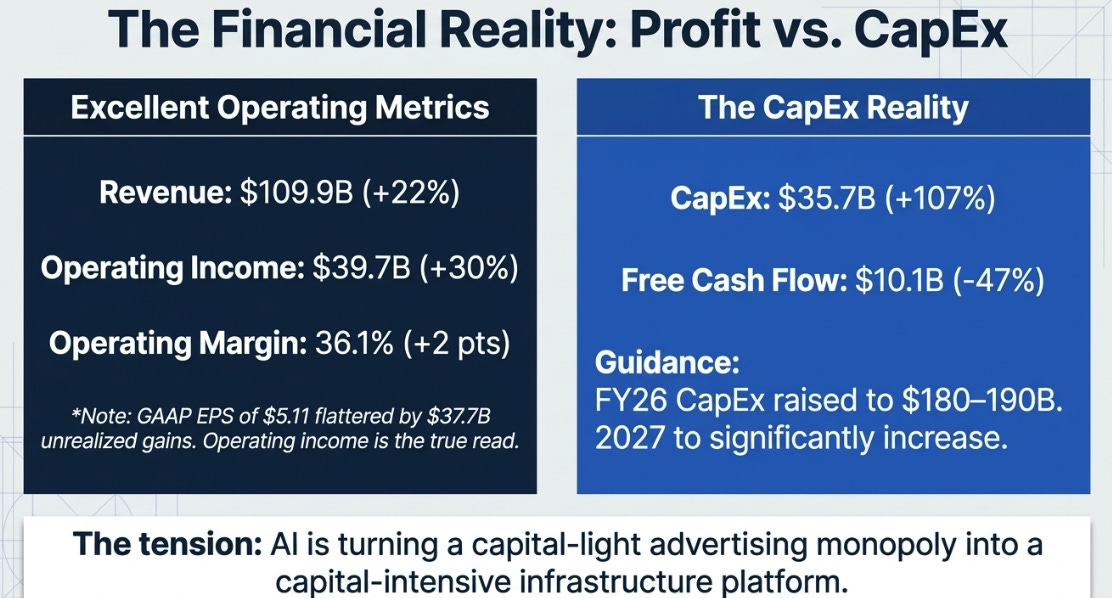

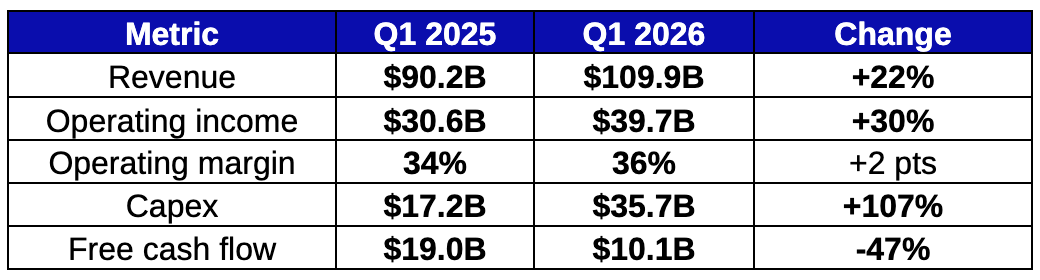

Alphabet’s income statement looked excellent. Revenue grew 22%, operating income grew 30%, and operating margin expanded to 36.1%. But GAAP EPS of $5.11 was flattered by $37.7B of other income, primarily unrealized gains on non-marketable equity securities. The better operating read is revenue and operating income, not EPS.

The cash flow statement is where the cost shows up. Operating cash flow was $45.8B. Capex was $35.7B. Free cash flow was only $10.1B. TTM free cash flow was $64.4B. Alphabet ended the quarter with $126.8B of cash and marketable securities, but long-term debt rose to $77.5B.

Then management raised the stakes. FY26 capex guidance increased to $180–190B, up from $175–185B, and management said 2027 capex will “significantly increase” compared to 2026.

This is not the old Alphabet.

The old Alphabet was a capital-light advertising monopoly. The new Alphabet is still immensely profitable, but it is becoming a capital-intensive AI infrastructure platform.

The bear case is straightforward: AI is turning Alphabet’s high-margin, high-FCF advertising business into a lower-FCF infrastructure utility.

The bull case is more subtle: Alphabet’s capex should not be judged against a single business. The same infrastructure improves Search, monetizes Cloud, enhances YouTube, and trains Waymo.

That is the capital allocation claim embedded in “full stack.” Alphabet is saying it can spend more because it has more surfaces over which to amortize the spend.

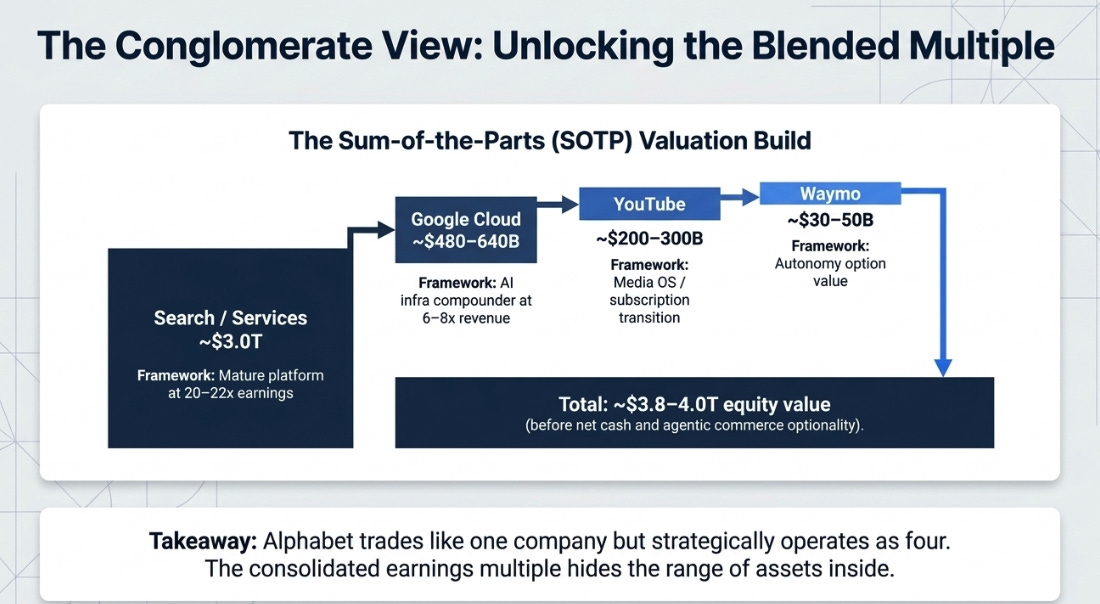

The Conglomerate View

Alphabet trades and reports like one company. Strategically, it increasingly looks like four.

A blended multiple hides businesses at different stages, with different economics and different valuation frameworks:

This is intentionally rough, but useful. A crude SOTP points to $3.8–4.0T of equity value before giving credit for agentic commerce optionality or faster Waymo scaling. Add net cash, and the argument is not that Alphabet is obviously cheap on consolidated earnings; it is that the consolidated multiple obscures the range of assets inside the company.

Search should be valued like a mature but still-growing intent monopoly with agentic commerce upside. Cloud deserves a growth infrastructure framework if it can sustain high growth and high margins. YouTube deserves more than an ad-line multiple if subscriptions and living-room viewing keep scaling. Waymo deserves option value that is no longer theoretical.

The old description, “advertising company with Cloud optionality”, is obsolete.

The Investor Test

The old investor test was simple: does AI kill Search?

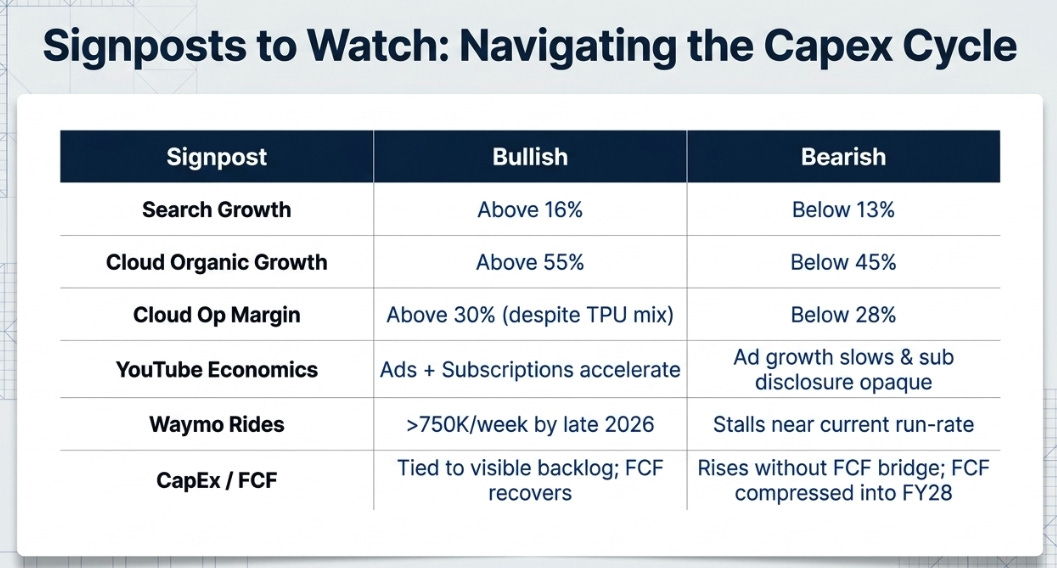

That is no longer sufficient. Search is growing faster with AI. The harder question is whether Alphabet can generate adequate returns across all four loops while capex rises.

The disclosure gaps are equally clear: AI Search monetization, Cloud backlog quality, total YouTube revenue including subscriptions, and Waymo operating metrics.

The more Alphabet becomes four businesses on one grid, the more investors need business-specific metrics.

The New Question

A year ago, the question was whether AI would kill Google.

By late 2025, the question became whether Google had built the intelligence grid. The answer was increasingly yes: AI did not kill Search, Cloud was breaking out, custom silicon mattered, capex was offensive, and Alphabet’s five-layer moat was beginning to compound.

Search compounds intent. Cloud compounds compute demand. YouTube compounds attention. Waymo compounds autonomous miles. The same infrastructure increasingly powers all four.

That is the opportunity. It is also the risk.

Alphabet’s Q1 2026 was not just a strong quarter. It was the quarter that clarified the next version of the company.

The question is no longer whether Google built the grid. The question is how many markets that grid can power.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.