Amazon 1Q26: The Foundry Answers Back

The Engine Room is still funding the AI buildout. Q1 showed the Foundry has real demand. Now Amazon has to prove the returns.

TL;DR

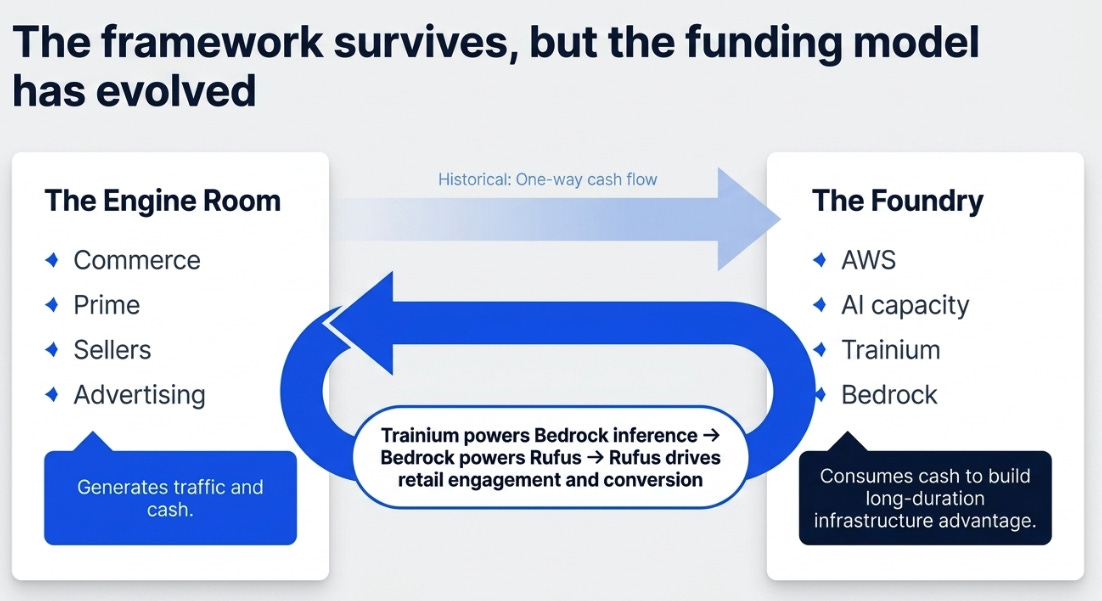

Our prior view was that Amazon had become an Engine Room funding a Foundry. Retail, Prime, sellers, and advertising generated the cash; AWS, AI infrastructure, and custom silicon consumed it to build long-duration advantage. Q4 sharpened the point: the Foundry was the organizing principle of Amazon’s capital allocation.

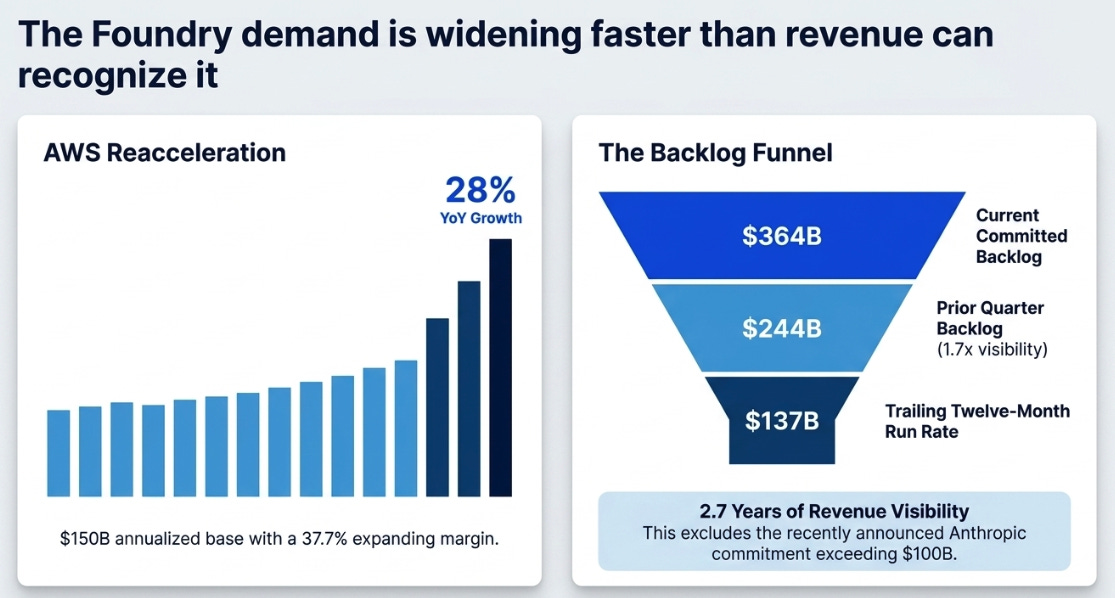

Q1 was the first real answer to the $200B capex question. AWS grew 28%, its fastest in 15 quarters, on a $150B annualized base. Amazon’s chips business crossed a $20B revenue run-rate. Trainium commitments reached $225B. AWS backlog surged to $364B, 2.7 times trailing revenue, up from 1.7 times last quarter, and that figure excludes the recently announced Anthropic commitment exceeding $100B.

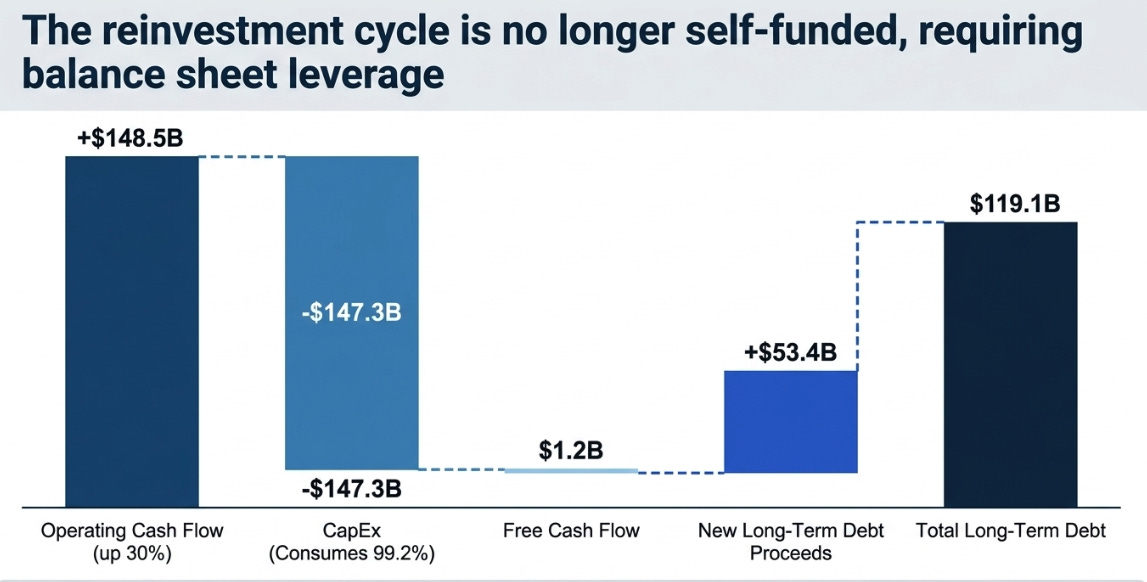

The thesis is stronger on demand, more conditional on returns. Operating cash flow rose to $148.5B on a trailing basis. Free cash flow fell to $1.2B as capex consumed nearly all of it, and Amazon raised $53B in new long-term debt. The Foundry is not a fantasy. It still has to become a cash-flow machine.

The Framework Survived. The Funding Model Changed.

Our framework across Q3 and Q4 was that Amazon is an Engine Room (commerce, Prime, sellers, advertising, generating traffic and cash) and a Foundry (AWS, AI capacity, Trainium, Bedrock, consuming cash to build infrastructure advantage). Q3 showed the Engine Room had the power to fund the Foundry. Q4 raised the stakes: $200B in capex, free cash flow likely turning negative, the Foundry becoming the company’s capital allocation priority.

Q1 updates, but does not replace, that framework. The Engine Room and Foundry are still distinct. But the relationship is no longer one-way. The Foundry is beginning to improve the Engine Room, Trainium powers Bedrock inference, Bedrock powers Rufus, Rufus drives engagement and conversion. That is not yet the same as saying Amazon has one fully fused AI grid. It is too early for that. But it means the Q4 question, can Amazon afford the Foundry?, is now incomplete.

The better question is: can the Foundry generate enough demand, cost advantage, and product leverage to justify the cash it is consuming?

Q1 starts to answer yes.

The Foundry Is No Longer a Promise

AWS grew 28% year-over-year to $37.6B, the fastest growth rate in 15 quarters. AWS operating margin was 37.7%, expanding while growth accelerated, a combination that is exceptionally rare at this scale. This matters because the bearish version of the $200B capex story was that Amazon might be building capacity before demand existed. Q1 argues strongly against that.

The backlog is the strongest single data point. AWS committed backlog surged to $364B, up 49% sequentially from $244B. At the current $137B trailing twelve-month run rate, that is 2.7 years of revenue visibility. Nine months ago, it was 1.7 years. The demand pipeline is not merely holding; it is widening faster than revenue can recognize it.

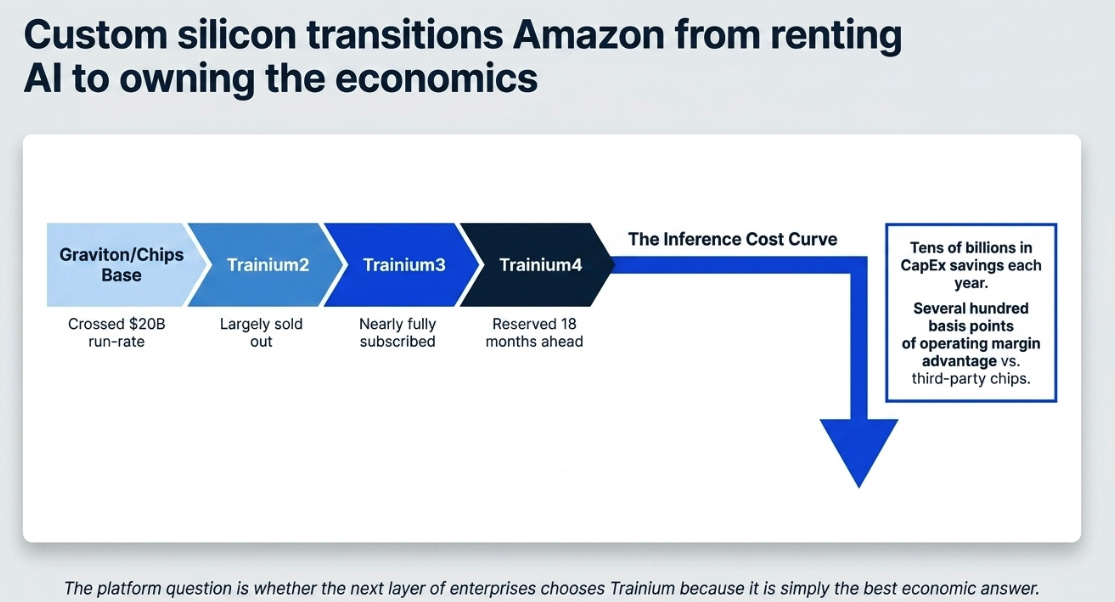

The more important disclosure was custom silicon. Amazon’s chips business, Graviton, Trainium, Nitro, crossed a $20B revenue run-rate, growing triple digits. Jassy went further: measured like an external chip vendor, the run-rate would be closer to $50B. Trainium commitments exceed $225B. Trainium2 is largely sold out. Trainium3 is nearly fully subscribed. Much of Trainium4, still 18 months from broad availability, has already been reserved.

That is the real narrative shift. Amazon is not renting GPUs and calling it an AI strategy. It is trying to own the inference cost curve. Jassy quantified this for the first time: Trainium saves Amazon “tens of billions of dollars of CapEx each year” and provides “several hundred basis points of operating margin advantage” versus third-party chips. If that advantage is real and durable, AWS becomes more than a cloud platform participating in the AI boom. It becomes one of the few companies that can shape the economics of the boom.

The asterisk is that Trainium still has to broaden. OpenAI, Anthropic, Meta, and Uber are powerful names. But the platform question is not whether enormous customers will reserve capacity. It is whether the next layer of enterprises chooses Trainium because it is simply the best economic answer, not because Amazon invested in them.

The Engine Room Is Still Throwing Off Heat

It would be a mistake to turn Q1 into only an AWS note.

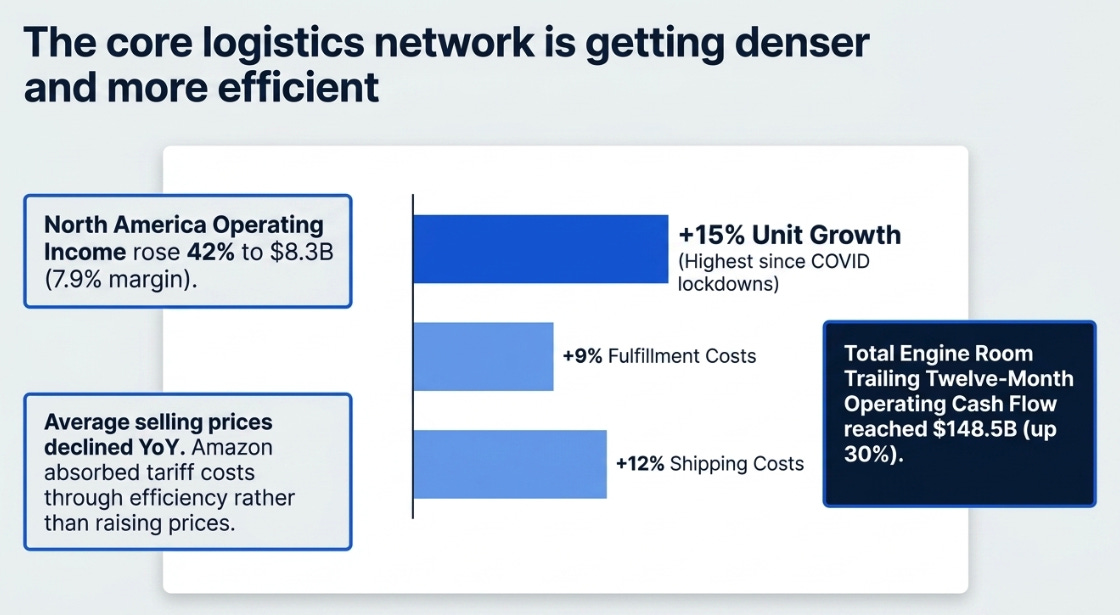

Unit growth reached 15%, the highest since COVID lockdowns. North America operating income rose 42% to $8.3B at a 7.9% margin. The cost spread confirmed structural operating leverage: units grew 15%, fulfillment costs grew 9%, shipping costs grew 12%. The logistics network is getting denser and more efficient at the same time volume is accelerating.

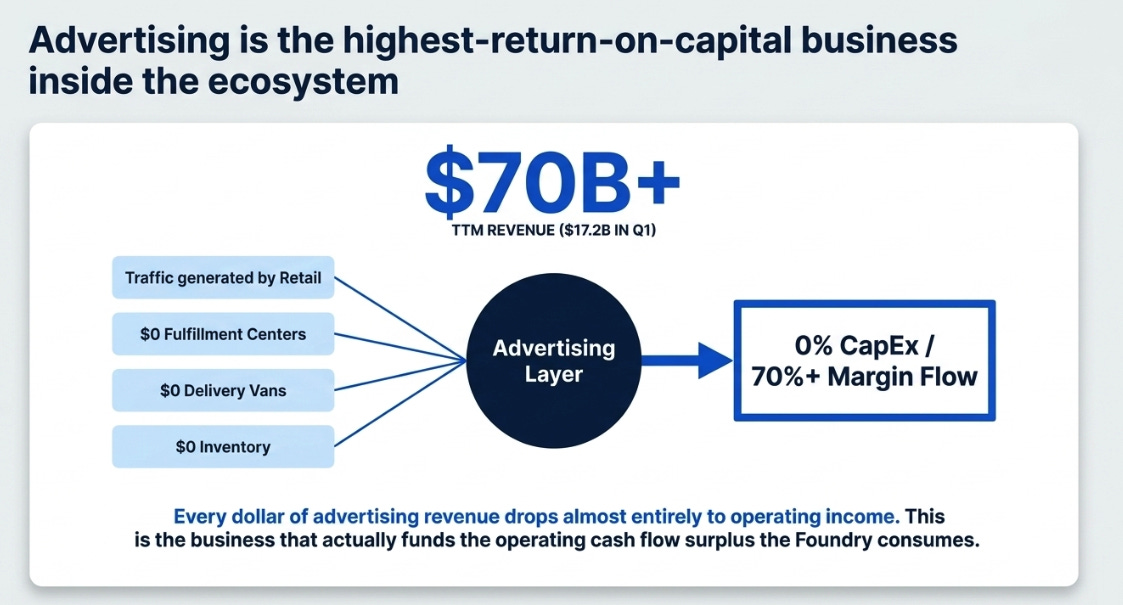

Advertising deserves its own recognition. At $17.2B in Q1 and over $70B on a trailing basis, advertising is the single highest-return-on-capital business inside Amazon. It requires no fulfillment centers, no delivery vans, no inventory. It operates at estimated 70%+ margins, layered on traffic the retail business already generates. Every dollar of advertising revenue drops almost entirely to operating income. This is the business that, more than AWS, more than Prime, actually funds the operating cash flow surplus the Foundry consumes.

The tariff bear case, which dominated pre-earnings sentiment, was a non-event in Q1. Average selling prices declined year-over-year. Amazon absorbed costs through efficiency rather than raising prices and still expanded margins. Jassy did not mention tariffs in prepared remarks. The silence is itself a data point.

Together, the Engine Room produced $148.5B in trailing twelve-month operating cash flow, up 30%. The funding mechanism is not a theory. It is accelerating at the exact moment the Foundry needs it most.

The Balance Sheet Enters the Story

The income statement was excellent. Revenue grew 17% to $181.5B. Operating income rose to $23.9B, above the guide high-end by $2.4B. Operating margin hit a record 13.1%. Reported EPS of $2.78 was inflated by a $16.8B pre-tax gain from Anthropic investments; the operating performance, not the bottom line, is the cleaner signal.

The cash-flow statement was more uncomfortable. Operating cash flow rose 30% to $148.5B on a trailing basis. Free cash flow fell to $1.2B. Capex consumed 99.2% of all cash the business generated.

Then the balance sheet. Long-term debt rose from $65.6B at year-end to $119.1B, with $53.4B of new long-term debt proceeds in Q1. This received zero discussion on the earnings call.

That does not break the thesis. Interest coverage is 29.8 times. The cash balance grew to $101.8B. But it refines the thesis.

Our earlier version was: the Engine Room funds the Foundry. The more accurate version after Q1: the Engine Room funds most of the Foundry; the balance sheet is funding the rest. At $200B of annual capex on ~$150B of operating cash flow, Amazon needs approximately $50B per year in external financing. This is no longer a self-funded reinvestment cycle. It is a reinvestment cycle with leverage.

The Market Is Still Using the Wrong Capex Frame

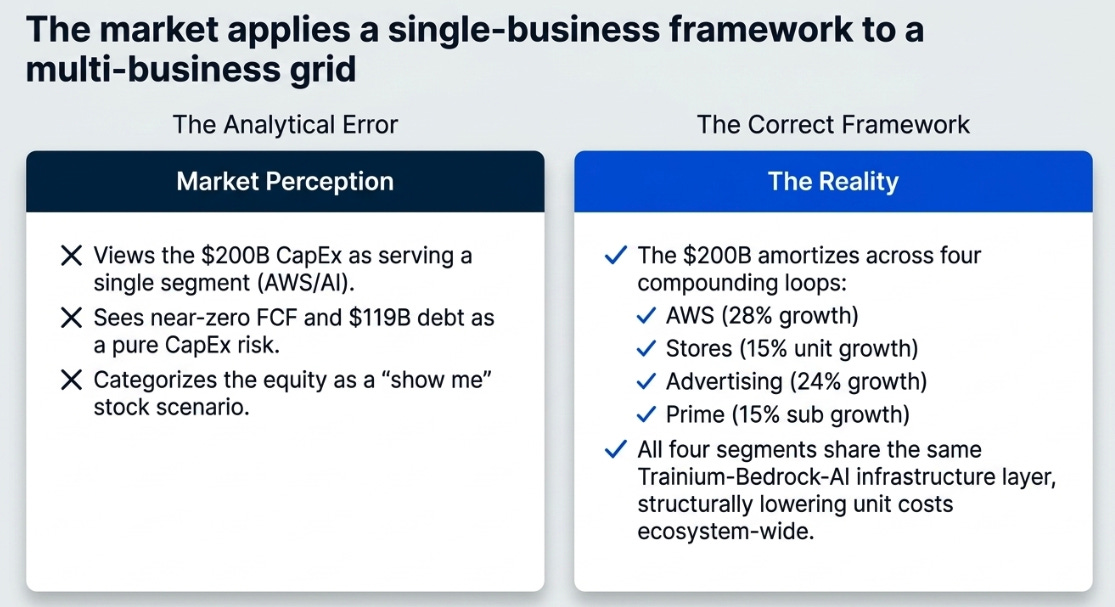

Here is what the market sees: a company spending $200B per year with near-zero free cash flow and $119B in debt. A capex risk. A “show me” stock.

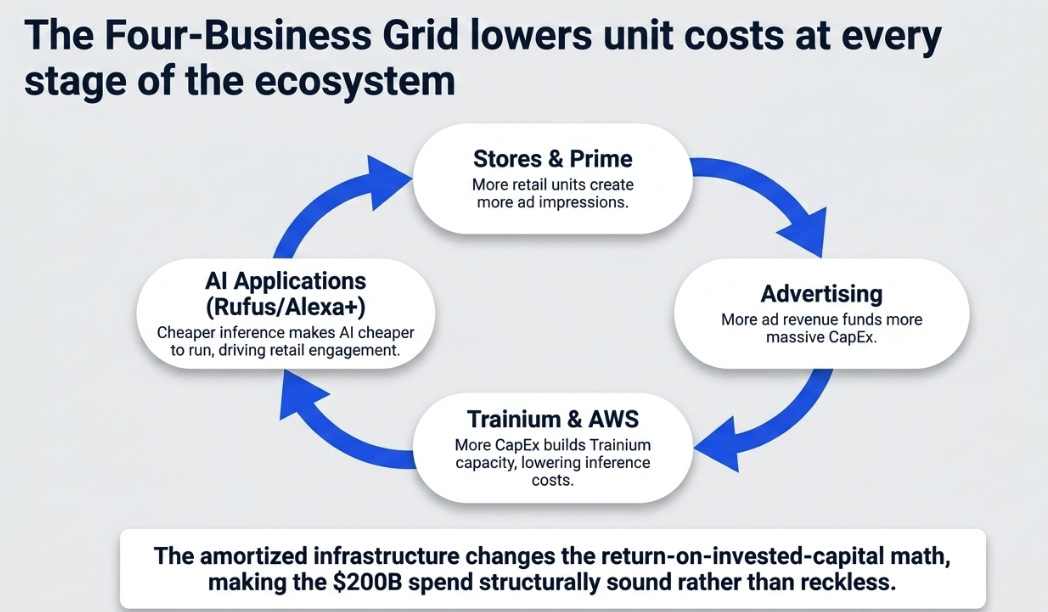

Here is what the market is underweighting: the $200B in capex is not serving one business. It is serving four, AWS (28% growth), Stores (15% unit growth), Advertising ($70B+, 24% growth), and Prime (15% subscription growth), all of which use the same Trainium-Bedrock-AI infrastructure layer. Each business’s growth reduces the others’ unit costs: more retail units create more ad impressions, more ad revenue funds more capex, more capex builds more Trainium capacity, more Trainium capacity lowers inference cost, lower inference cost makes Rufus and Alexa+ and Health AI cheaper to run, and cheaper AI applications drive more retail engagement.

The market applies a single-business capex framework to a four-business grid. That is the analytical error. The correct framework amortizes the infrastructure across all four loops, which changes the return-on-invested-capital math. It does not make the capex cheap. It makes it less reckless than it appears on a single-segment basis.

What would make this wrong: a third-party shopping agent captures the consumer entry point, severing the Stores-to-Advertising loop. AWS growth decelerates below 22%, suggesting Q1 was a cyclical peak. Tariffs compress retail margins enough to weaken the Engine Room’s cash generation. Debt exceeds $150B without a clear FCF inflection timeline. Any of those would impair the grid’s economics. All of them simultaneously would break the thesis.

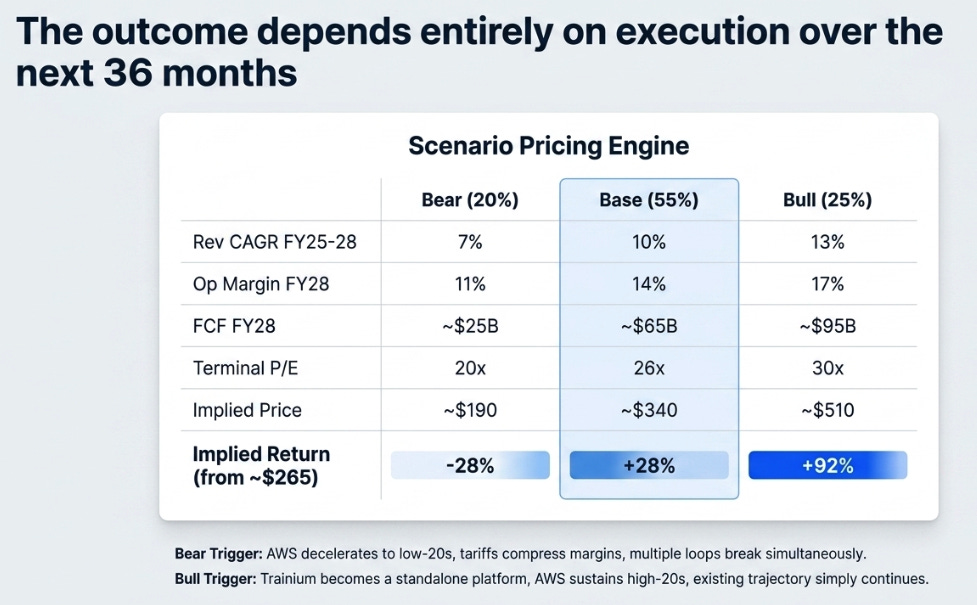

The Price of the Grid

The range is wide because the outcome genuinely depends on execution over the next two to three years, not on information available today.

The bear case requires AWS to decelerate to low-20s, tariffs to compress margins, advertising to slow to mid-teens, and the FCF trough to extend into 2028. The base case requires AWS at 25%+ through 2027, advertising above 20%, margins expanding as the depreciation window closes, and FCF inflecting to $60B+ by 2028. The bull case requires Trainium to become a platform, AWS to sustain high-20s growth longer than expected, and the market to re-rate as four compounding loops become visible in the financial statements.

The skew matters: the bear case requires multiple loops to break simultaneously; the bull case requires the existing trajectory to continue.

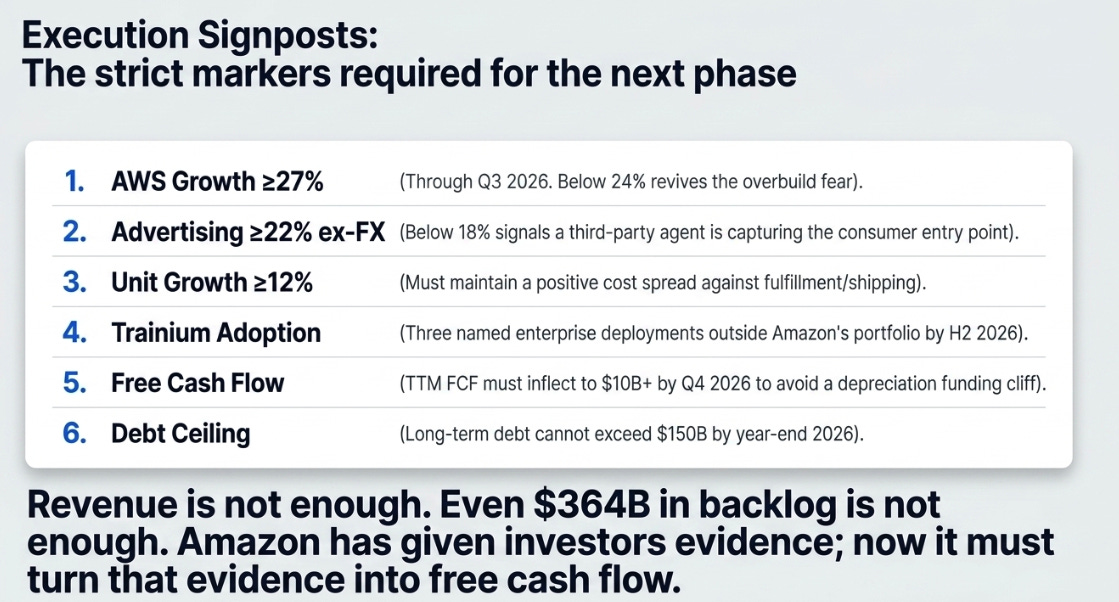

The New Proof Points

The Q4 signposts have largely been met. The next phase requires stricter markers.

AWS growth ≥27% through Q3 2026. Below 24%, the overbuild question returns.

Advertising ≥22% ex-FX. This is the Engine Room’s highest-margin turbine. Below 18% signals the agentic entry point is shifting.

Unit growth ≥12% with the cost spread remaining positive, units must grow faster than fulfillment and shipping costs.

Three named Trainium enterprise deployments outside Amazon’s investment portfolio by H2 2026.

TTM FCF inflects to $10B+ by Q4 2026. Near zero into 2027 means the depreciation window becomes a funding problem.

Long-term debt does not exceed $150B by year-end 2026. Above that, the conversation shifts from investment cycle to structural leverage.

Evidence Is Not Yet Cash

Q4 was when Amazon asked investors for patience. Q1 was when it gave them evidence.

The Foundry has numbers behind it: AWS reacceleration, Trainium commitments, Bedrock momentum, custom silicon at scale, and demand arriving before capacity. The Engine Room still has power: units, ads, fulfillment leverage, Prime, and segment profits all improved.

But the proof that matters most is still ahead. Revenue is not enough. Operating income is not enough. Even $364B in backlog is not enough.

The proof is cash.

Amazon is no longer asking investors to believe in the Foundry on faith. Q1 gave them evidence. Now the company has to turn that evidence into free cash flow.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.