Applied Materials 1QFY26 Earnings: The Complexity Dividend

Semiconductor value is shifting from lithography to materials engineering, and AMAT may be the primary beneficiary.

TL;DR

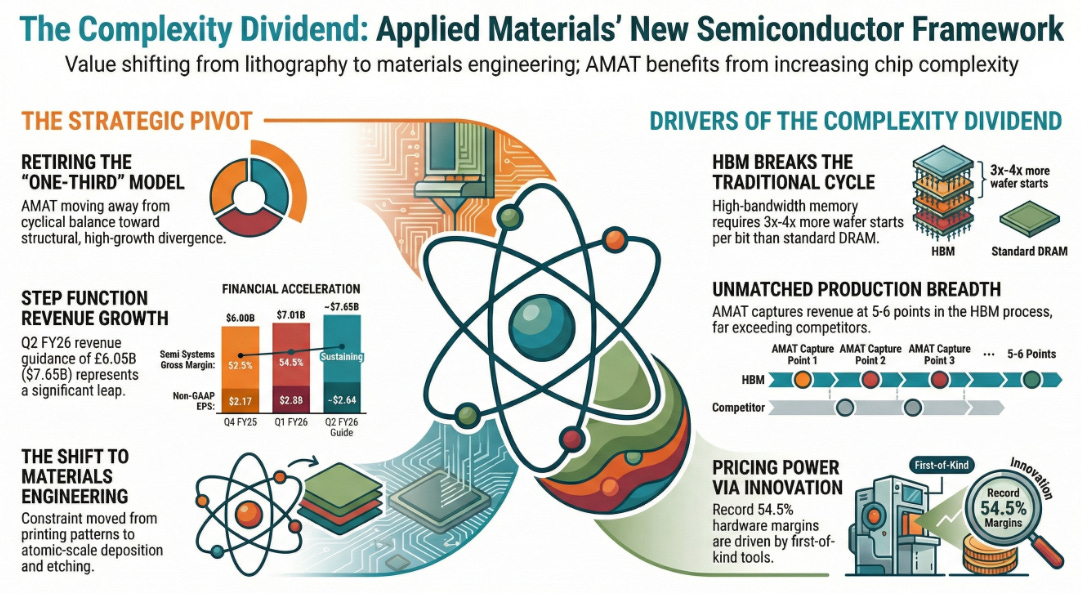

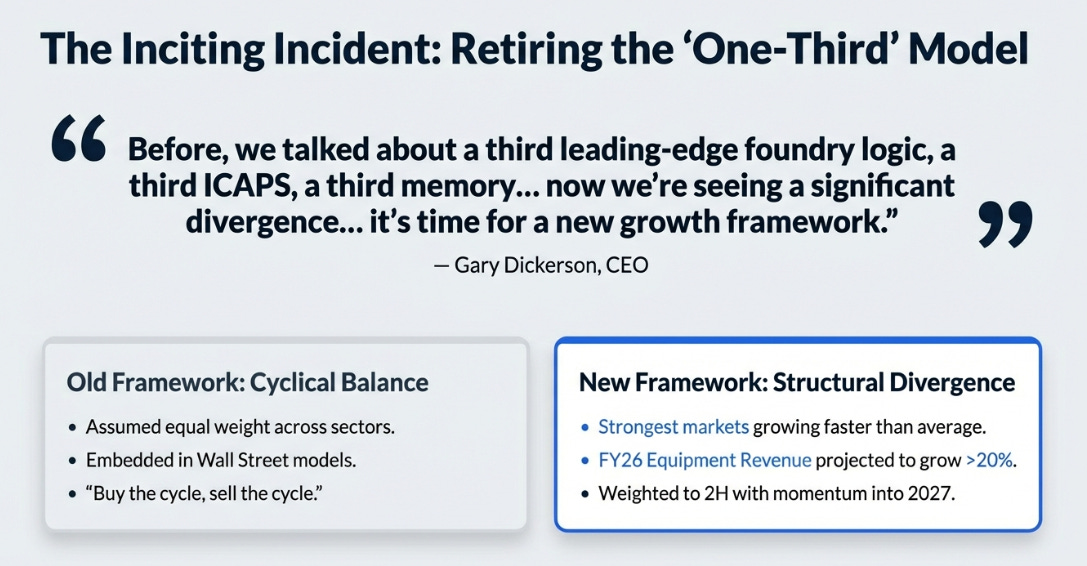

A framework shift, not just a beat. Q2 guidance crushed expectations (+$620M revenue, +15% EPS vs. Street), and CEO Gary Dickerson formally retired the “one-third foundry / one-third memory / one-third ICAPS” model, signaling structural divergence, not cyclical balance.

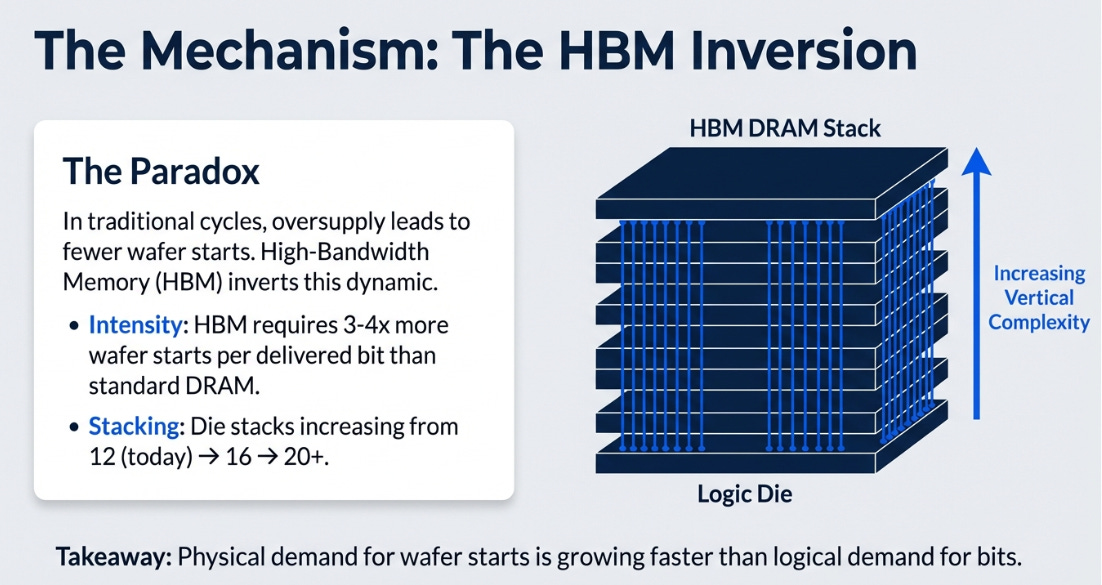

HBM changes the memory playbook. High-bandwidth memory requires 3-4x more wafer starts per bit and increasingly complex packaging. Even if bit demand moderates, process intensity per bit keeps rising, structurally increasing equipment demand where AMAT has unmatched breadth.

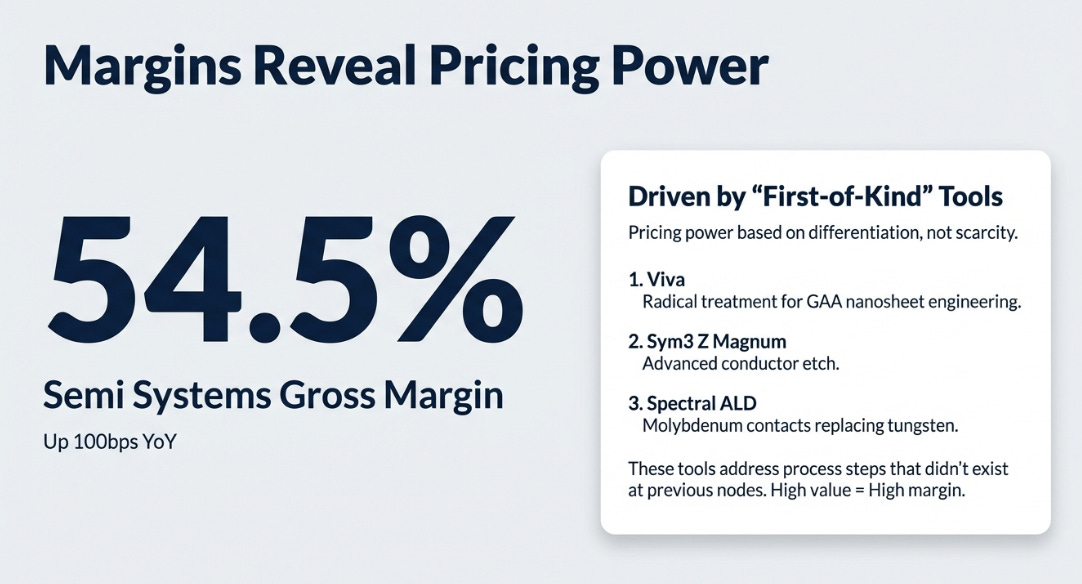

Margins reveal pricing power. Semi Systems gross margin hit 54.5%, extraordinary for hardware. First-of-kind tools (GAA, molybdenum contacts, advanced packaging, e-beam) suggest differentiation-driven pricing, not scarcity-driven uplift. The key question: structural inflection or another cycle peak?

The Complexity Dividend

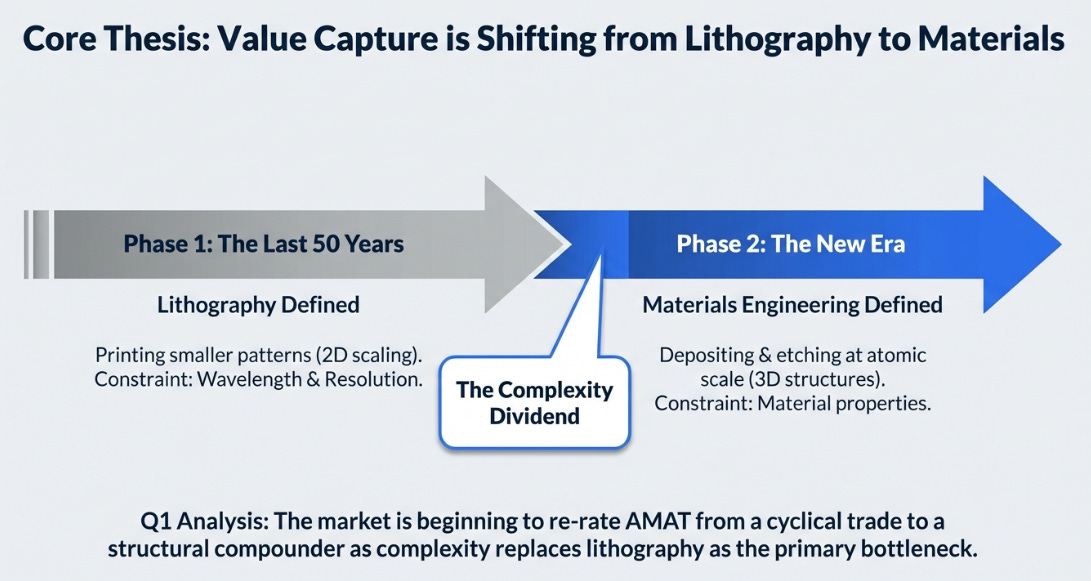

For fifty years, semiconductor progress was defined by lithography, printing smaller patterns. That era is over. The binding constraint now is materials engineering: depositing, etching, and treating new materials at atomic scale. On February 12, Applied Materials reported a quarter that suggests the market is finally beginning to price this shift in.

From Bloomberg:

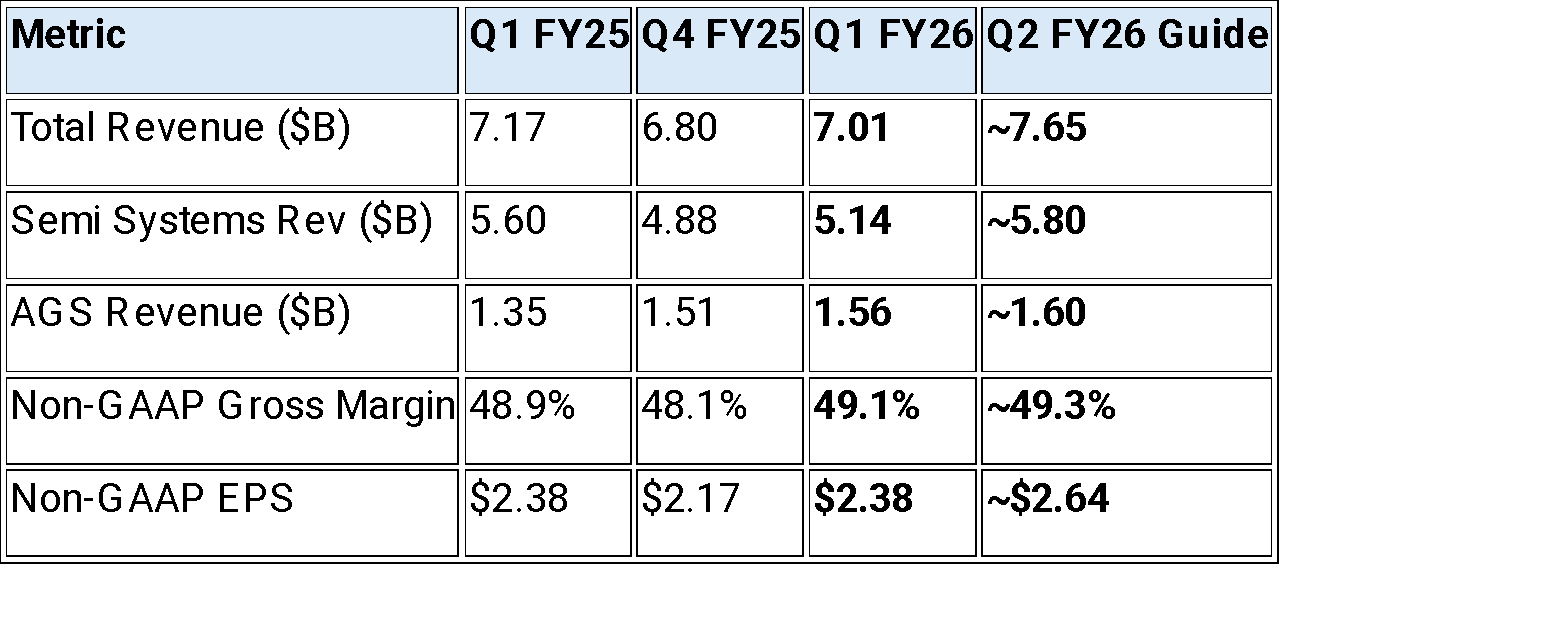

Applied Materials Inc. surged 10% in late trading after delivering a surprisingly upbeat sales forecast, signaling that demand for artificial intelligence and memory semiconductors is fueling equipment purchases. The company expects revenue of approximately $7.65 billion in the fiscal second quarter. Analysts had estimated $7.03 billion.

The Q1 results themselves were fine, revenue down 2% year-over-year, EPS flat, a clean beat on a low bar. The stock didn’t move 10% on Q1. It moved on what came next: Q2 guidance of $7.65B and $2.64 EPS, crushing the Street by $620M and 15% respectively. And then CEO Gary Dickerson said this:

“Before, we talked about a third leading-edge foundry logic, a third ICAPS, a third memory... now we’re seeing a significant divergence in the end market growth rates, and I think it’s time for a new growth framework.”

CEOs do not publicly retire their own industry frameworks by accident. The one-third/one-third/one-third model is embedded in every sell-side model on Wall Street for semi equipment companies.

Dickerson was making a deliberate choice: stop valuing us as a broad-based WFE company. The markets where we’re strongest are growing far faster than the markets where we’re average, and your models don’t capture that. The full-year call: semiconductor equipment revenue growing more than 20% in calendar 2026, weighted to the second half, with momentum carrying into 2027.

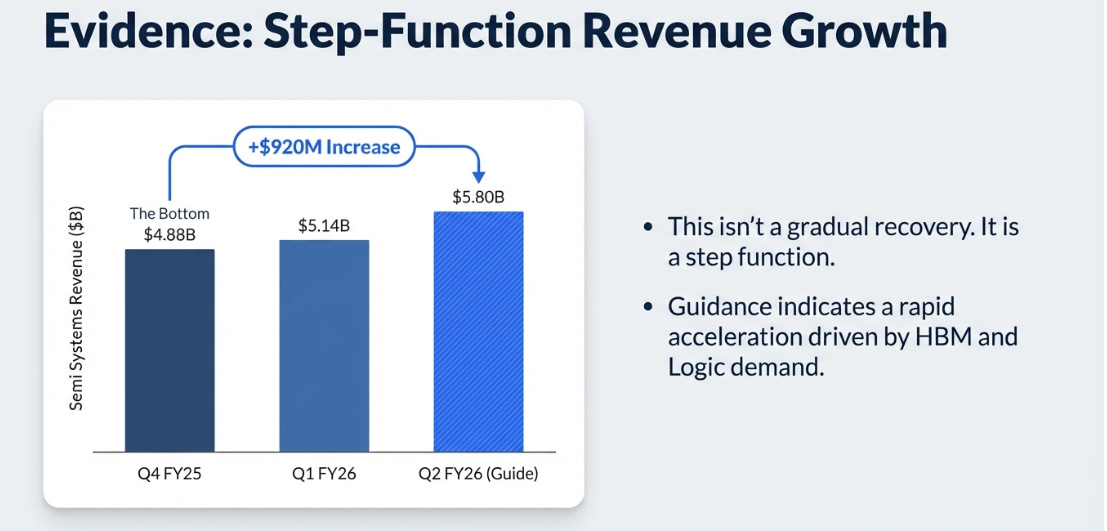

Semi Systems bottomed at $4.88B in Q4 and is guided to $5.80B in Q2, a $920M increase in two quarters. This isn’t a gradual recovery. It’s a step function.

The DRAM Metamorphosis

The structural argument for why Dickerson’s “new framework” is more than marketing lives in one line of the segment breakdown:

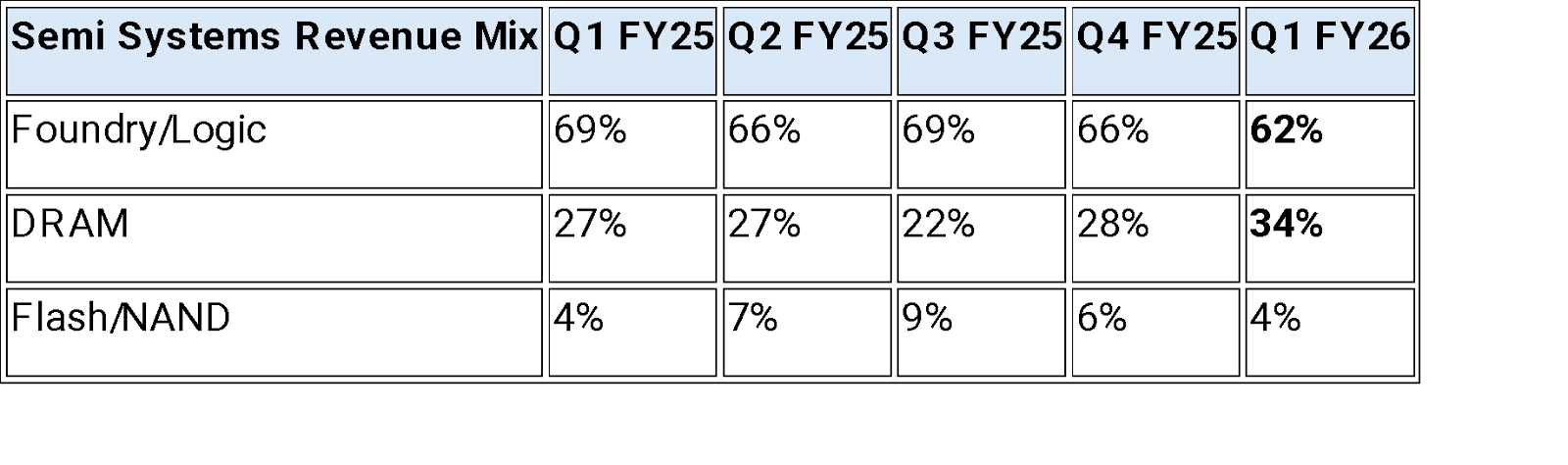

DRAM hit a record 34% of Semi Systems revenue. The immediate reaction is to pattern-match this to previous memory cycles: DRAM spending surges, oversupply follows, capex gets slashed. That pattern has held for thirty years. But HBM breaks the mechanism, and Dickerson explained exactly why:

“HBM DRAM has larger die sizes and requires 3x-4x more wafer starts per delivered bit than standard DRAM. In addition, the number of dies in the HBM stacks is increasing from 12 today to 16, and then 20 or more in the future.”

In a traditional memory cycle, oversupply means fewer wafer starts. HBM inverts this: the physical demand for wafer starts grows much faster than the logical demand for bits, because each bit requires 3-4x more silicon and increasingly complex packaging. Each additional die in the stack requires deposition and etch steps at both the wafer and packaging level. Even if bit demand moderates, wafer start demand, which is what drives equipment sales, can continue growing. The complexity per bit is compounding, not flattening.

What makes this specifically an Applied Materials story, rather than a generic semi-cap tailwind, is the breadth of their exposure to the HBM production flow. Lam Research is strong in etch. Tokyo Electron is strong in deposition and coater/developers. But HBM fabrication and packaging touches deposition, etch, CMP (chemical mechanical planarization), thermal processing, e-beam inspection, and advanced packaging, and AMAT has leading or dominant positions across all of them. They capture revenue at five or six points in the HBM production process where a competitor might capture one or two. It’s the difference between owning a tollbooth on the highway and owning every tollbooth on a six-lane bridge. That breadth is why AMAT can credibly claim #1 in DRAM process equipment, #1 in HBM DRAM, and #1 in HBM packaging simultaneously, and why the DRAM mix shift accrues disproportionately to them.

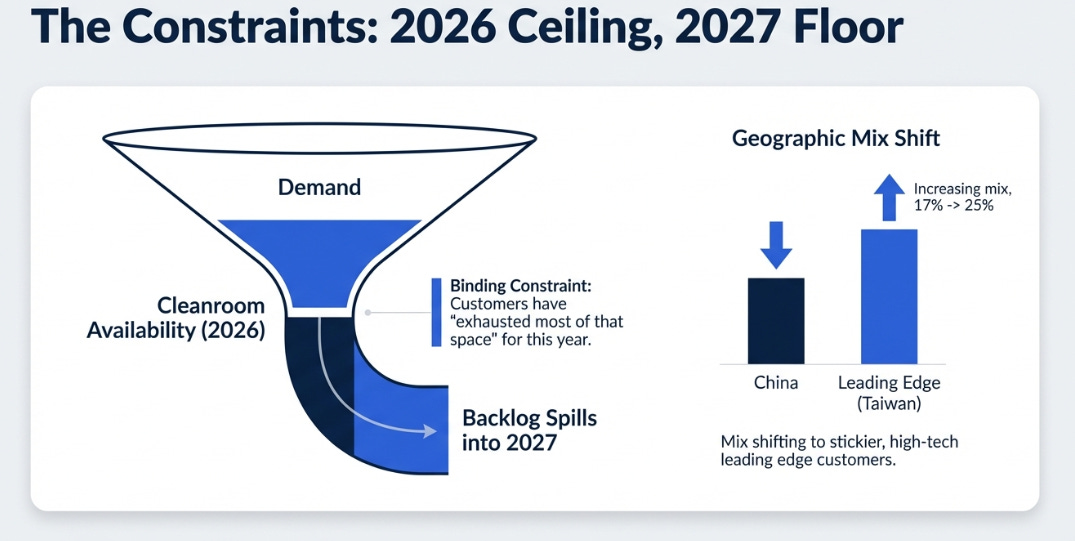

The geographic data supports this. Taiwan surged from 17% to 25% of total revenue year-over-year, almost certainly TSMC ramping leading-edge logic and advanced packaging for AI accelerators. The growth is coming from the most advanced fabs in the world, not commodity capacity.

And here’s what makes this a multi-year story rather than a one-quarter trade: cleanroom availability is the binding constraint on 2026 growth.

CFO Brice Hill said customers have “exhausted most of that space” for this year. This caps the upside, but it also means demand exceeds supply, creating a backlog that extends into 2027 as new fabs come online. Hill confirmed he sees “a number of factories in DRAM and leading logic scheduled to come online next year.” The constraint is both the ceiling on 2026 and the floor under 2027.

54.5%

This quarter was the first time Applied disclosed segment-level gross margins under its new reporting structure. Companies introduce new metrics when the numbers make them look good, and this number does: Semi Systems non-GAAP gross margin of 54.5%, up 100 basis points year-over-year. For a company selling physical hardware into a competitive market with capable rivals, this is extraordinary.

There’s a revealing tension in how the two top executives discussed it.

Dickerson: “I have very high confidence that we’ll be able to sustain that margin growth going forward.” Hill, in the very next exchange: “The progress will be, I’ll say, very slow through the course of the year.”

The subtext of Hill’s caution is specific: as China (higher-margin, smaller customers) shrinks as a share of revenue while large leading-edge buyers (TSMC, Samsung, Micron) grow, the customer mix works against margin expansion. But I think the structural direction is up, for one reason: the products driving the expansion aren’t iterations, they’re first-of-kind. The Viva radical treatment for GAA nanosheet engineering, the Sym3 Z Magnum for conductor etch, the Spectral ALD for molybdenum contacts replacing tungsten. These address process steps that didn’t exist at previous nodes. When you’re the only qualified vendor for a critical new step, customer size matters less than customer need. This is the lesson Intel learned painfully at 10nm, the materials are the constraint, and whoever solves them has pricing power.

The flywheel: higher margins fund more R&D, which produces more first-to-market tools, which sustain higher margins. Applied expects its e-beam revenue alone to double to over $1 billion in CY2026. When a specific product line is doubling to a billion-dollar run rate in a category that creates lock-in for the rest of the equipment portfolio, the margin story has legs beyond this cycle.

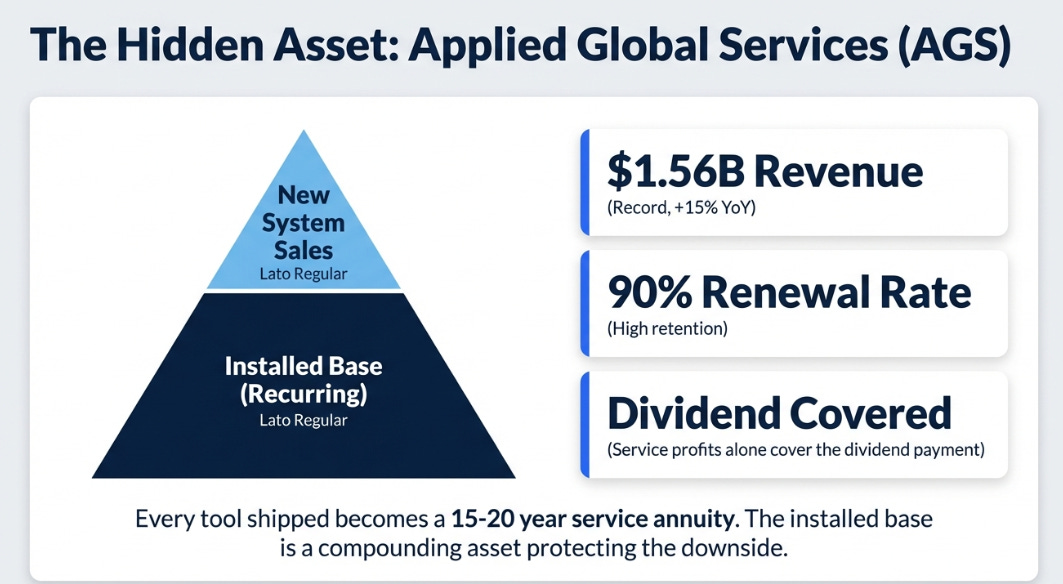

One more detail worth noting: Applied Global Services hit record revenue of $1.56B, up 15% year-over-year, with two-thirds under contract and 90% renewal rates. Hill disclosed that AGS cash profitability now covers the entire dividend. Every tool AMAT ships during this upcycle becomes a 15-20 year service annuity. The installed base is a compounding asset that the market consistently undervalues.

What the Stock Implies

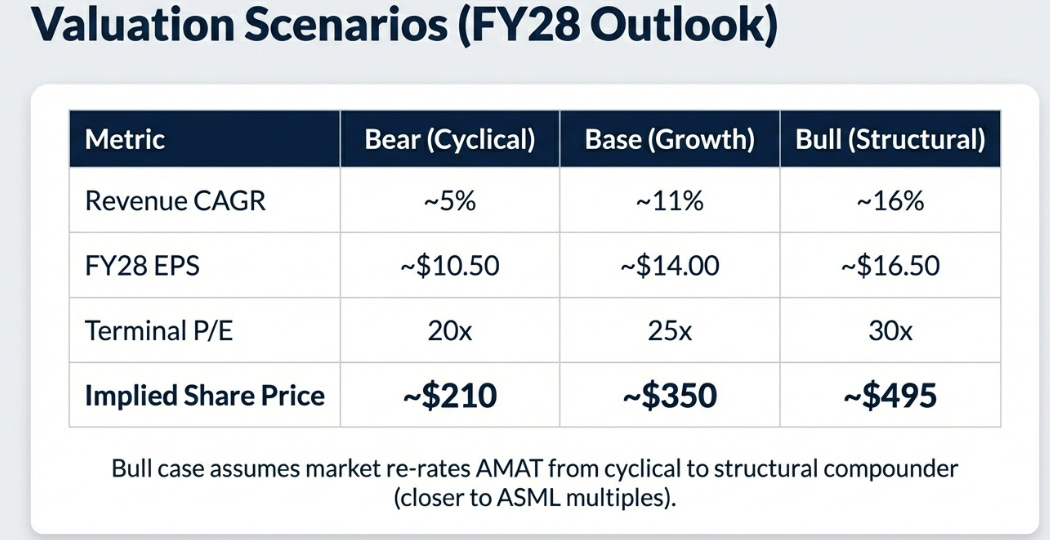

At ~$362, here’s what you need to believe, and the assumptions behind each scenario:

The bull case requires WFE to grow mid-teens in both CY26 and CY27, with AMAT outgrowing the market by 3-5 points on GAA and HBM content gains. Gross margins breach 50% as value-based pricing takes hold and the high-margin product mix (e-beam, advanced packaging tools) becomes a larger share. The market re-rates AMAT from cyclical (25x) to structural compounder (30x), closer to where ASML trades. This is the scenario where Dickerson’s “new framework” comment looks prescient.

The base case says the >20% CY26 growth materializes but CY27 decelerates to low-teens as HBM investment normalizes. Margins hold near current levels, pricing gains offset by the China mix headwind. The stock trades sideways: EPS growth offset by multiple compression from the current ~33x to a more normal 25x. You own a very good company at a fair price.

The bear case is the historical pattern reasserting itself. HBM demand peaks in CY27, memory capex gets cut, WFE contracts. AMAT’s revenue stalls or declines. The stock de-rates to 20x on lower earnings, the classic semi equipment “buy the cycle, sell the cycle” outcome that has played out every single time for the past three decades.

The risk/reward at $362 is balanced, not compelling. Better entry at $300-310. At current prices, a hold.

Four signposts

Semi Systems growth in Q3 FY26 (May earnings). The >20% CY26 call requires acceleration to $6B+. Flat or below $5.8B breaks the narrative.

DRAM mix trajectory. Healthy at 30-35% while total Semi Systems grows. Dangerous above 40% (concentration) or a sharp drop (demand cliff).

Equipment gross margins through the ramp. Must hold above 53%. Below 52% means pricing power was scarcity, not differentiation.

Competitor growth rates. If Lam and TEL are also guiding >20%, it’s a rising tide. If AMAT is materially outgrowing peers, the share gain thesis is confirmed. The distinction determines the multiple.

The question this quarter poses is simple. Is the shift from lithography to materials engineering a permanent change in where value accrues in the semiconductor supply chain, or is it a cyclical peak dressed up as a structural shift? The >20% growth call, the 54.5% equipment margins, the record DRAM quarter, the multi-year cleanroom backlog, the CEO retiring his own framework on a public call: these are not the hallmarks of a company riding a cycle. They’re the hallmarks of a company that believes its moment has arrived.

The base rate for “this time is different” in cyclical industries is not encouraging. Every memory upcycle has produced a compelling structural narrative, and every one has eventually reverted. If you’d bought semi equipment stocks every time a CEO said the cycle was becoming secular, you’d have a mixed record at best. That history demands respect.

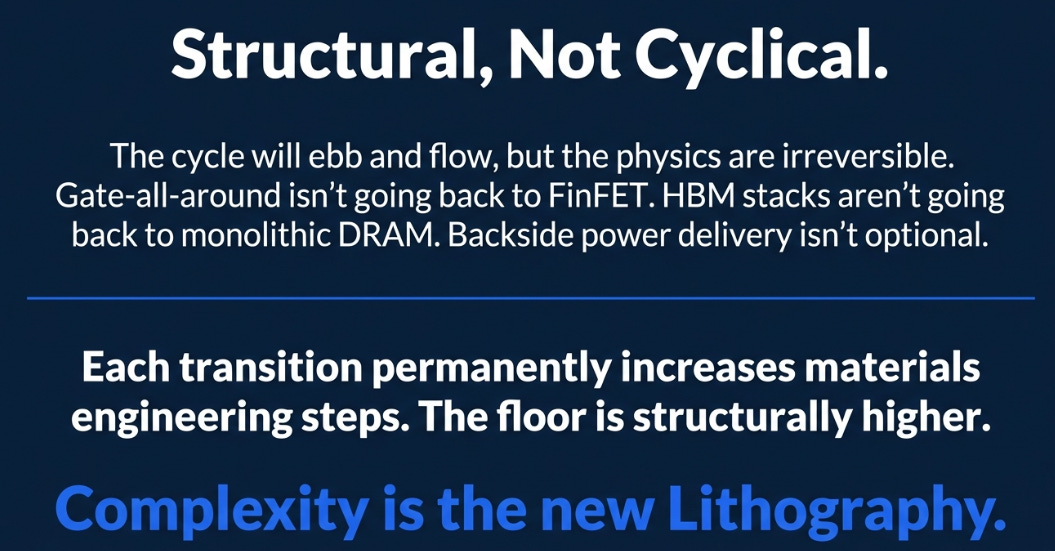

But I keep coming back to the physics. Gate-all-around transistors are not going back to FinFETs. HBM stacks are not going back to monolithic DRAM. Backside power delivery is not optional. Each of these transitions permanently increases the number of materials engineering steps per chip, and Applied Materials has the broadest portfolio to address them. The cycle will ebb and flow, it always does. But the level to which it ebbs is structurally higher than it was five years ago, and will be structurally higher still five years from now.

That’s the complexity dividend. Whether the market has fully priced it in at 33x earnings is a separate question. But the thesis itself, that complexity is the new lithography, and Applied Materials is the new bottleneck, is the most coherent strategic argument I’ve heard from a semi equipment company in years.

I think Dickerson is right. I’m watching the signposts.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.