Applied Materials 2QFY26 : The Complexity Tax Gets a Volume Multiplier

Every signpost cleared. The thesis accelerated. The stock followed. Now the hard question: how much of the next three years is already in the price at $468?

TL;DR:

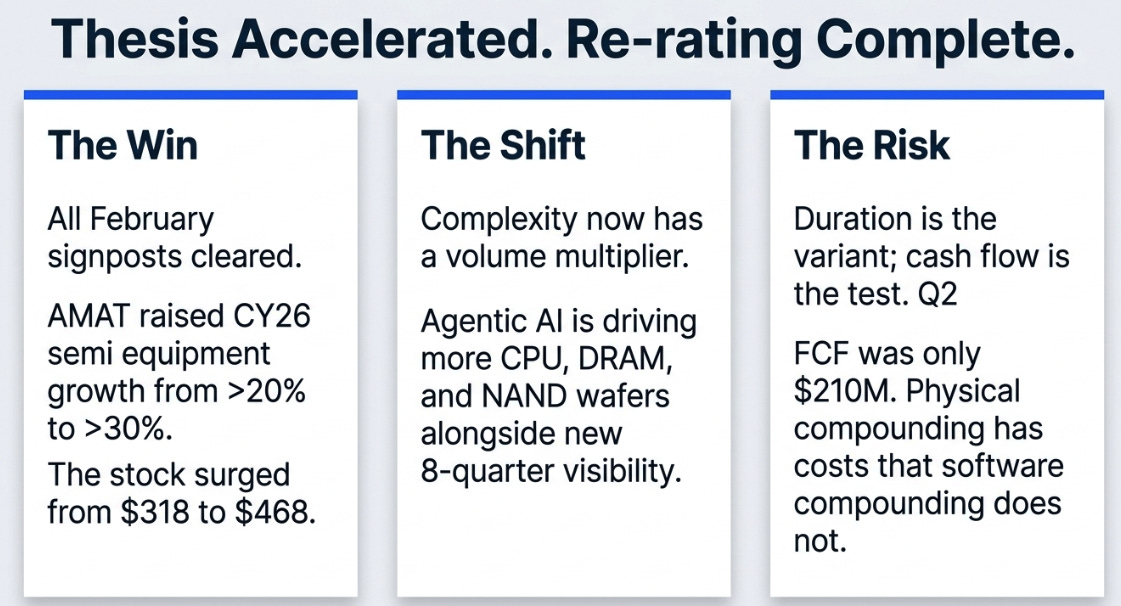

The thesis worked. All four signposts cleared, and AMAT raised CY26 semi equipment growth from >20% to >30%; the debate is now what is priced in at $468.

Complexity now has a volume multiplier. AMAT is not just getting more process steps per wafer from GAA/HBM/packaging; agentic AI may also drive more CPU, DRAM, and NAND wafers.

Duration is the variant; cash flow is the test. The bull case is AMAT becoming a manufacturing-complexity compounder, but Q2 FCF of $210M means Q3 cash conversion has to normalize.

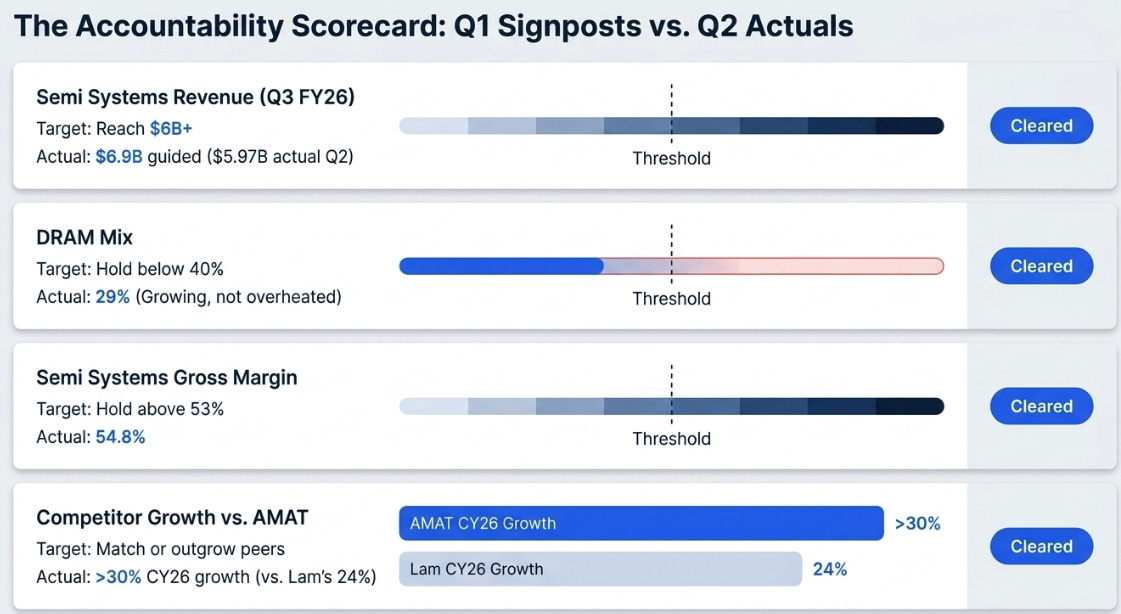

In February, after Applied Materials reported its fiscal Q1, I set four signposts. They were specific, measurable, and designed to test whether the complexity tax thesis, the idea that 3D chip architectures were permanently shifting semiconductor value toward materials engineering, was structural or just another cycle dressed up as a paradigm shift.

Here’s what happened:

All four cleared. I should be pleased, and I am, but I also need to be honest about something. In January, at $318, I wrote that “risk/reward at $362 is balanced, not compelling. Better entry at $300-310.” The stock is now $468. The thesis was completely right. The entry call was too conservative. The stock re-rated and never looked back.

That tension, correct thesis, missed entry, is the honest frame for thinking about what comes next. Because the question is no longer whether the complexity tax is real. It’s whether $468 already pays fair value for it.

Three Things That Weren’t in the Model

I want to resist the temptation to recap the quarter. The numbers were excellent, record revenue of $7.91 billion, record non-GAAP EPS of $2.86, gross margin crossing 50% for the first time in 25 years. You can read those anywhere. What matters is the three things that are genuinely new and weren’t in my framework three months ago.

First, management upgraded CY2026 semiconductor equipment growth from “>20%” to “>30%.” That’s a 50% increase in the growth outlook in 90 days. This was not a routine beat-and-raise. It was a demand acceleration that management itself didn’t see coming, driven by customers finding incremental clean room capacity and placing equipment orders that weren’t in the forecast as recently as February.

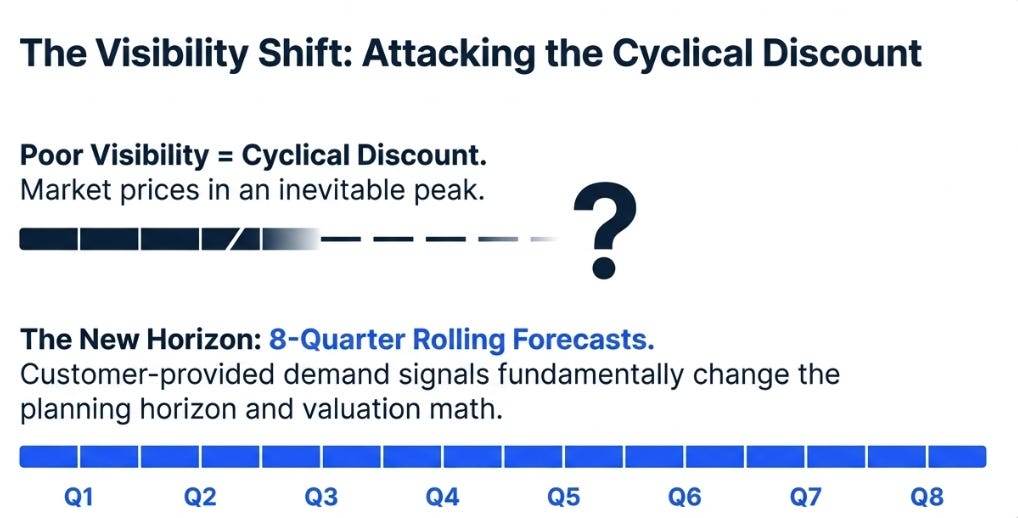

Second, AMAT’s largest customers are now providing rolling eight-quarter demand forecasts. This is, I believe, the single most important disclosure for the re-rating debate. The semi-cap industry has always traded at a cyclical discount because visibility was poor. Two years of customer-provided demand signals directly attacks the foundation of that discount. It doesn’t eliminate cyclicality. But it changes the planning horizon enough to matter for how the business should be valued.

Third, CEO Gary Dickerson introduced agentic AI as an incremental demand driver:

“Agentic AI models do more than respond to queries. They plan, reason, and execute tasks autonomously. They therefore require a computing architecture that is more CPU-intensive while also increasing demand for DRAM and NAND.”

He framed this as additive to existing training and inference workloads. That distinction matters, and it’s the piece that forces me to update my thesis.

Complexity × Volume

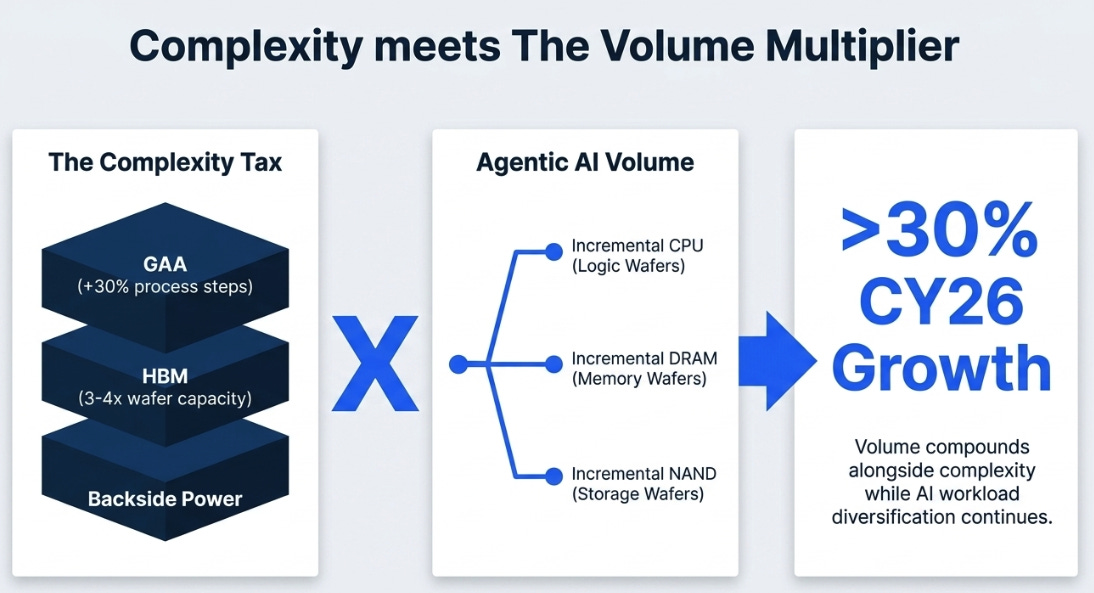

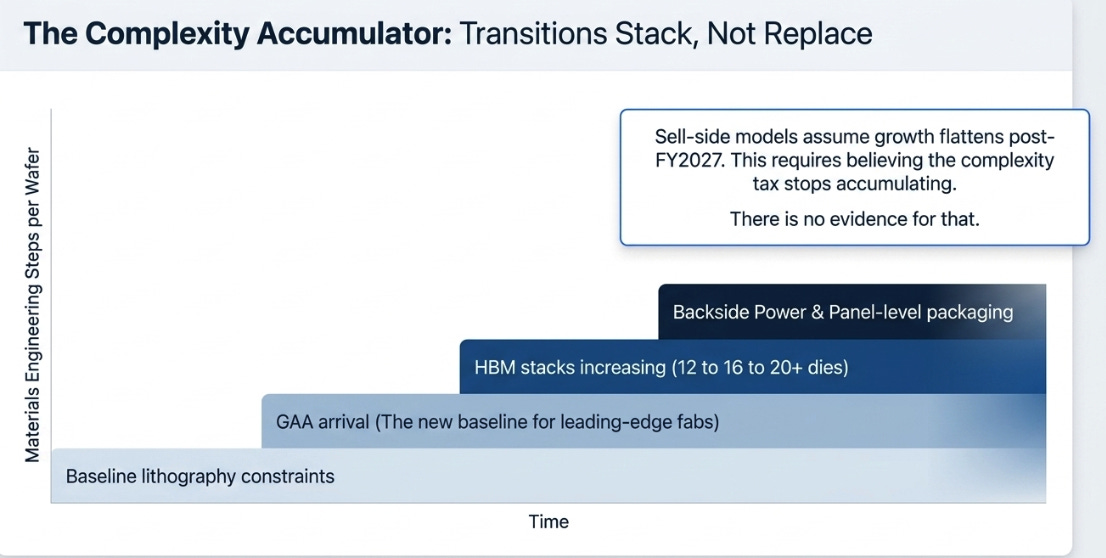

My prior articles framed Applied’s advantage as a complexity tax. GAA transistors add 30% more process steps. HBM requires 3-4x the wafer capacity per bit. Backside power delivery doubles certain equipment categories. Each architecture transition increases the number of materials engineering steps per wafer, and Applied has the broadest portfolio to capture them. The tax doesn’t cycle, it accumulates.

That framework was correct but incomplete. It captured the supply side, more steps per wafer, while treating the demand side, number of wafers, as cyclical. This quarter suggests volume is compounding too.

Agentic AI creates incremental CPU demand (more logic wafer starts), incremental DRAM demand (more memory wafer starts), and incremental NAND demand (more storage wafer starts), all on top of the training and inference workloads the market is already modeling. Dickerson noted that global token generation has tripled in three months. Customers added 10+ fab projects to AMAT’s tracking list in a single quarter, bringing the total above 100.

The updated mechanism is simple: complexity compounds AND volume compounds, at least while AI workload diversification continues. That’s why the >20% to >30% upgrade happened so fast. It’s not that management was being conservative in February, it’s that agentic demand emerged as a material driver faster than anyone anticipated.

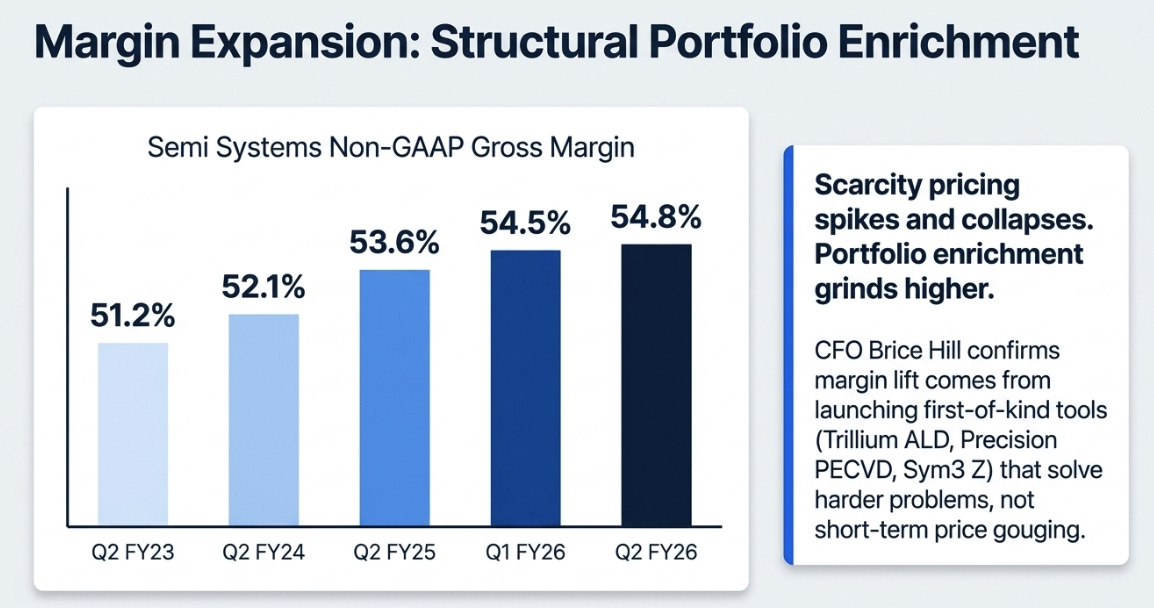

The gross margin data confirms this isn’t just scarcity pricing. When I asked in February whether 54.5% Semi Systems margins were structural or cyclical, the answer was ambiguous. It’s less ambiguous now. CFO Brice Hill was explicit on the call: pricing generally works through two-to-three-year project contracts and moves slowly. The margin lift comes from the portfolio becoming more valuable as AMAT launches tools that solve harder problems, Trillium ALD for GAA gate stacks, Precision PECVD for isolation trenches, Sym3 Z for conductor etch. These are first-of-kind tools with limited competition. Hill guided Q3 gross margin to 50.1%, continued expansion on higher volume.

Four years of steady expansion. Scarcity pricing spikes and collapses. Portfolio enrichment grinds higher. This looks like the latter.

What Consensus Gets Wrong

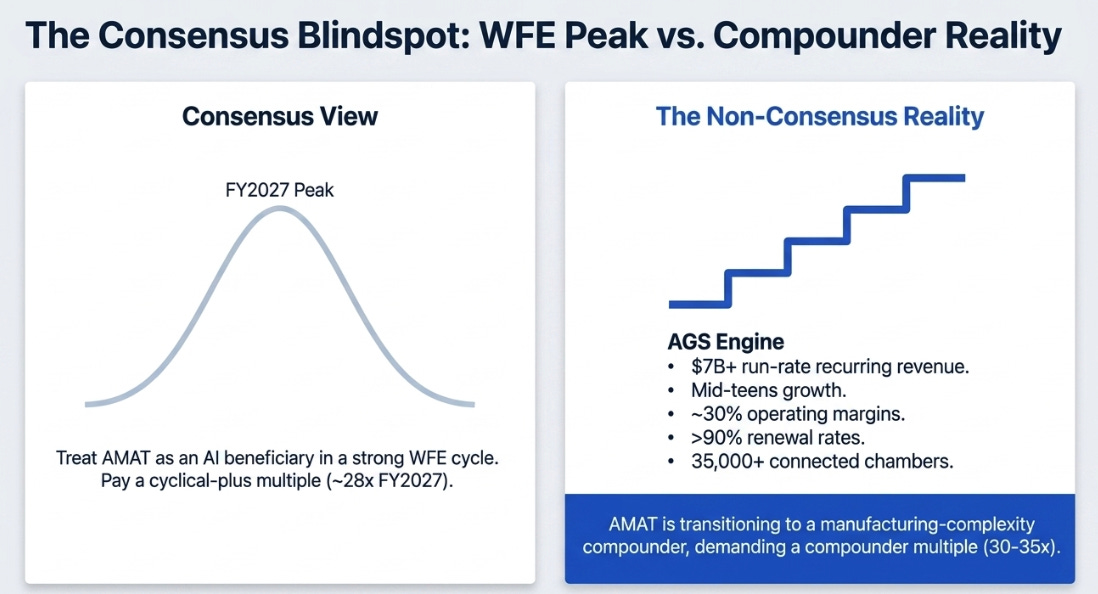

Consensus sees AMAT as a well-positioned AI beneficiary in a strong WFE cycle. Consensus is right on the direction and wrong on two things.

Duration. Sell-side models show growth accelerating through FY2027, then flattening. This is the traditional WFE cycle template applied to a non-traditional demand environment. GAA is not a one-time upgrade; it’s the new baseline for every leading-edge fab going forward. HBM stacks are going from 12 to 16 to 20+ dies. Backside power is arriving. Panel-level packaging is next. These transitions don’t replace each other, they stack. And now agentic AI is adding a volume multiplier on top of the complexity tax. The assumption that growth mean-reverts in FY2028 requires believing the complexity tax stops accumulating. I see no evidence for that.

AGS. Management upgraded AGS growth from “low double digits” to “mid-teens” sustainably, with “potentially higher this year.” AGS revenue hit $1.665B with 29.2% operating margins. Over 35,000 chambers connected to AIx servers. Renewal rates above 90%. This is a $7B+ run-rate recurring business growing mid-teens with near-30% margins, and the market still treats it as a cyclical cushion. I valued it at $80B standalone in January. Nothing this quarter weakened that view; if anything, the growth rate upgrade strengthened it.

The non-consensus call: AMAT is transitioning from cyclical WFE company to manufacturing-complexity compounder. The market is paying a cyclical-plus multiple (~28x FY2027) for what may deserve a compounder multiple (30-35x). The gap closes if growth sustains through FY2028 and cash generation normalizes.

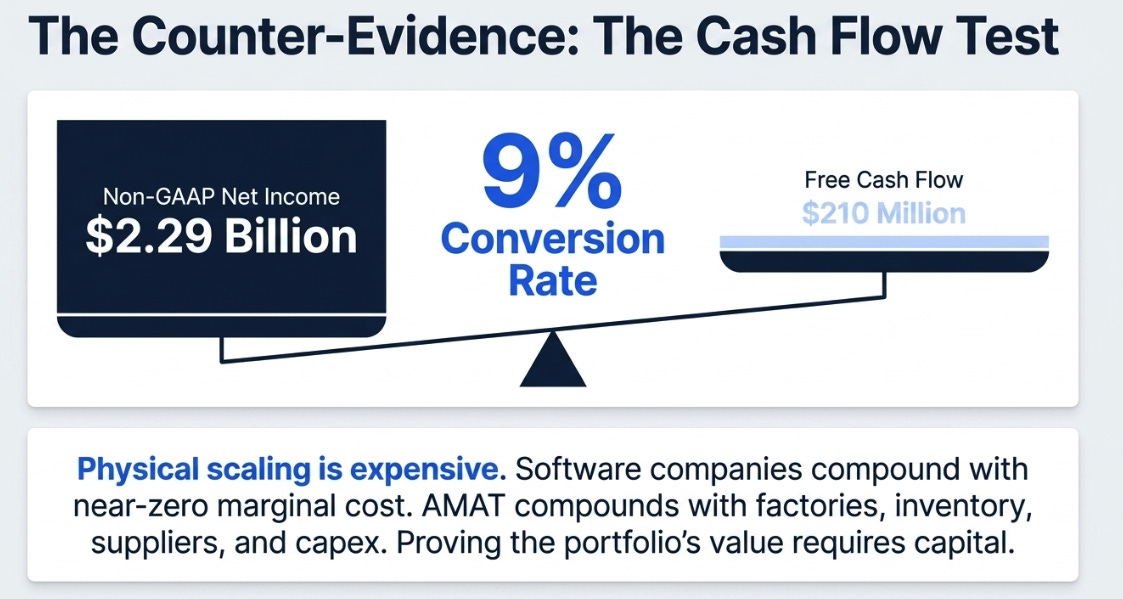

The Cash Flow Question

I should flag the one thing that didn’t look good, because a thesis that ignores counter-evidence isn’t a thesis, it’s a sales pitch.

Free cash flow was $210 million. On $2.29 billion of non-GAAP net income, that’s a 9% conversion rate. The headline is bad. The detail is worse: accounts receivable grew 23% quarter-over-quarter while revenue grew 13%, implying DSOs jumped from roughly 63 to 72 days. Inventory hit $6.3 billion, an all-time high.

Management’s explanation, building capacity and inventory ahead of a >30% growth year, EPIC Center construction, legal and tax payments, is plausible. The 8-quarter customer visibility provides the demand backstop that makes the inventory build rational rather than reckless. But the receivables specifically need watching. If DSOs normalize below 65 days in Q3, it was timing. If they stay above 70, something structural changed in customer payment terms and the quality-of-earnings debate starts in earnest.

Physical scaling is expensive. Software companies compound with near-zero marginal cost. AMAT compounds with factories, inventory, suppliers, and capex. The P&L says the portfolio is becoming more valuable. The cash flow statement says proving that value requires capital. The bull case needs both to be true.

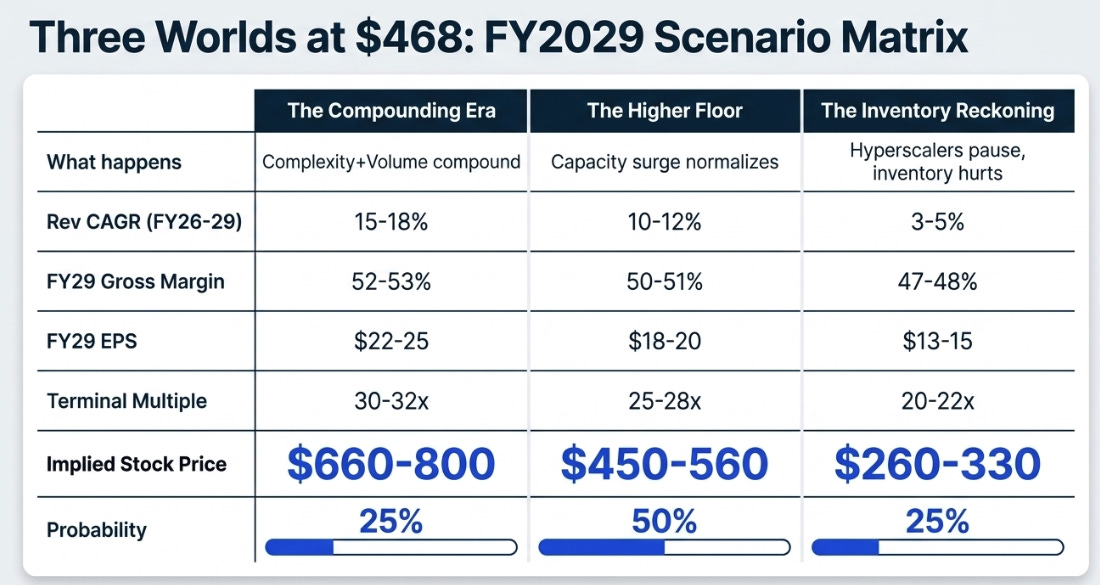

Three Worlds at $468

In January, at $318, I laid out three scenarios through FY2028. “Physics Wins” implied $480 at 30x $16 EPS. The stock is already at $468. Time to recalibrate for a 3-year horizon through FY2029.

Source: Author estimates based on AMAT guidance, management commentary, and historical WFE cycle analysis.

The probability-weighted expected value is roughly $490-530, 5-15% above current price. The asymmetry is modest, which is itself the key insight. At $318, the stock was priced for “The Inventory Reckoning” and you only needed “The Higher Floor” to work. At $468, the stock is priced for “The Higher Floor” and you need “The Compounding Era” to materialize for significant upside.

That’s not bearish. But it’s a fundamentally different risk/reward than six months ago. The thesis has been de-risked by execution, and the stock has re-priced accordingly.

What would shift probabilities: “The Compounding Era” becomes more likely if Q3-Q4 revenues grow linearly (per Hill’s explicit guidance), if the EPIC Center unveiling in October attracts additional partners, and if FY2027 guidance when it comes implies sustained >15% growth. “The Inventory Reckoning” becomes more likely if DSOs stay elevated, DRAM spot pricing falls more than 10% in a quarter, or TSMC cuts FY2027 capex below $50B.

What I’m Watching

Six signposts for the Q3 earnings print in August:

Q3 revenue ≥$9.1B, confirms acceleration beyond the guide midpoint

Semi Systems gross margin ≥54.5%, pricing power intact at higher volume

DSOs back below 65 days, working capital normalizing, not structural

FCF conversion above 35%, earnings quality validated after Q2 weakness

“2027 another strong record year” language maintained, duration signal

CY2026 semi equipment growth held at ≥30%, no downward revision

In January I wrote that the complexity tax doesn’t cycle, it accumulates. In February I set four signposts to test that claim. All four cleared. The thesis has accelerated faster than I expected, and honestly, faster than the stock could have been bought at a comfortable price.

At $468, the market is no longer paying you to identify the shift from lithography to materials engineering. It’s asking you to size the duration. I think the duration is longer than consensus models, complexity compounds, volume is now compounding alongside it, and the visibility mechanism changes the risk profile of the business. But the margin of safety is thinner than it was six months ago, and the cash flow statement is a reminder that physical compounding has costs that software compounding does not.

The complexity tax is real. The question is whether the stock already collects enough of it.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.