Arm 3QFY26 Earnings: The Distributed AI Thesis, The Neutrality Paradox

Distributed AI is rewriting CPU economics, and SoftBank is rewriting Arm.

TL;DR:

Arm is no longer a mobile royalty annuity; data center + CSS are turning it into a platform with materially higher take rates.

SemiAnalysis makes the CPU comeback unavoidable: AI is becoming a distributed system where CPUs are the fabric layer, not the sidecar.

The biggest risk is self-inflicted: designing full CPUs for Meta/Stargate risks collapsing the neutrality premium that makes Arm’s royalty model work.

I’ve been covering Arm, tracking the narrative as it shifted from “overpriced mobile IP licensor” to something considerably more interesting. SemiAnalysis published a major piece yesterday on the datacenter CPU landscape that is directly relevant, and I want to use it alongside Q3 FY26 results to check my own homework.

On to the Update:

A Story That Keeps Rewriting Itself

From the Arm shareholder letter, released February 4:

Arm reported record Q3 FY2026 revenue of $1.24 billion, up 26% year-over-year and ahead of the $1.23 billion consensus estimate. Royalty revenue of $737 million grew 27%, driven by accelerating adoption of Armv9 technology and Compute Subsystems across data center and mobile. License revenue of $505 million, while up 25% year-over-year, missed the $520 million estimate. Non-GAAP earnings per share of $0.43 beat estimates of $0.41. The company guided Q4 revenue to $1.47 billion at the midpoint, above the $1.40 billion consensus, and raised full-year expectations.

I want to be honest: the quarterly results are almost beside the point with Arm right now. The numbers were fine , a clean beat on royalties, a modest licensing miss, guidance that cleared the bar. What makes this company fascinating is that the story has completely rewritten itself every six months since the IPO, and this quarter is the most consequential chapter yet.

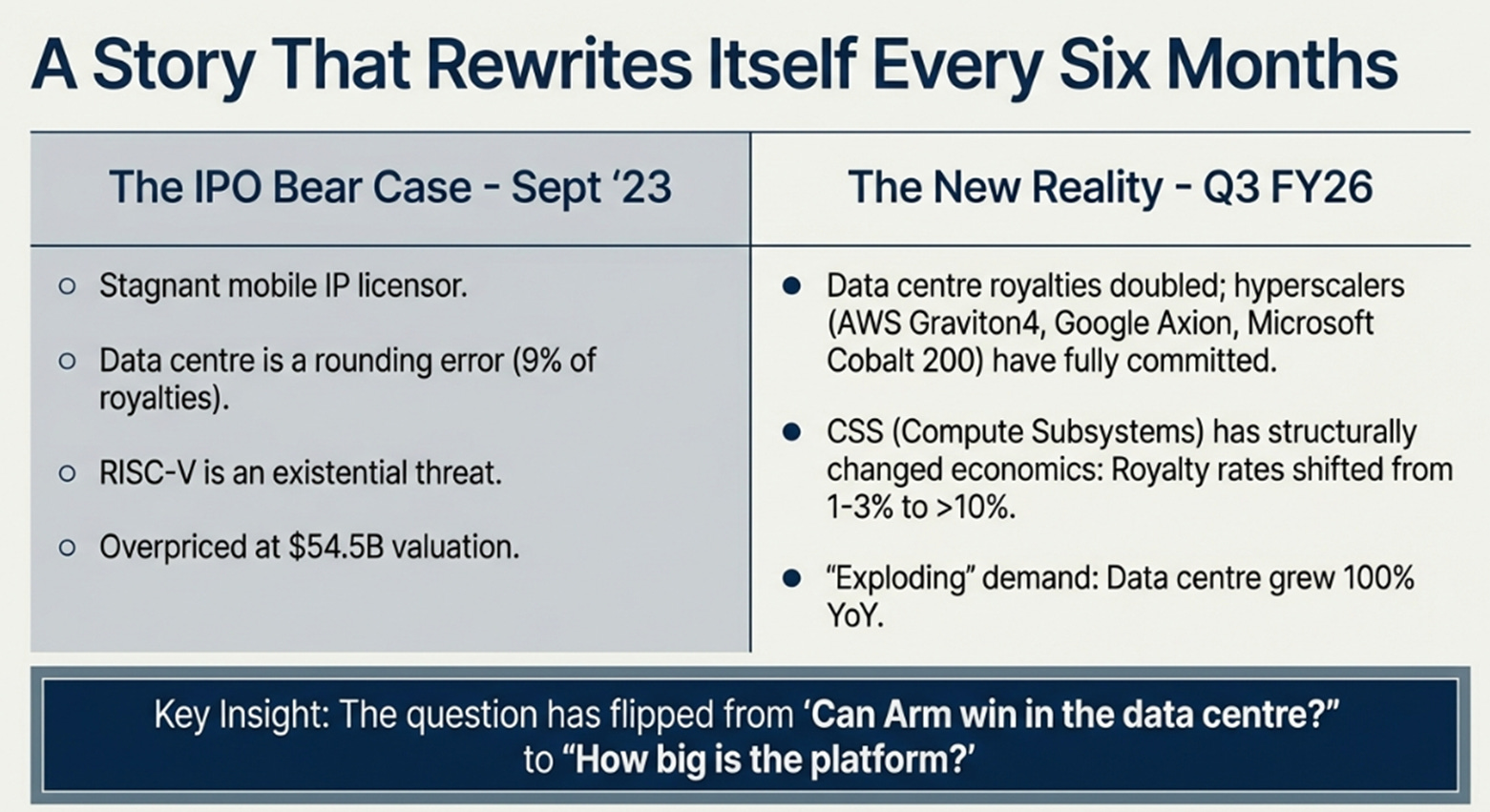

When Arm listed in September 2023 at $54.5 billion, the bear case was simple and pretty compelling. A mobile IP licensor collecting pennies per chip in a stagnant smartphone market. Data center was a rounding error , cloud and networking at 9% of royalties. RISC-V was the existential threat. SoftBank’s 90% stake was pure overhang. The stock went to $160, crashed to $100, and both moves were mostly AI sentiment rather than anything Arm actually did.

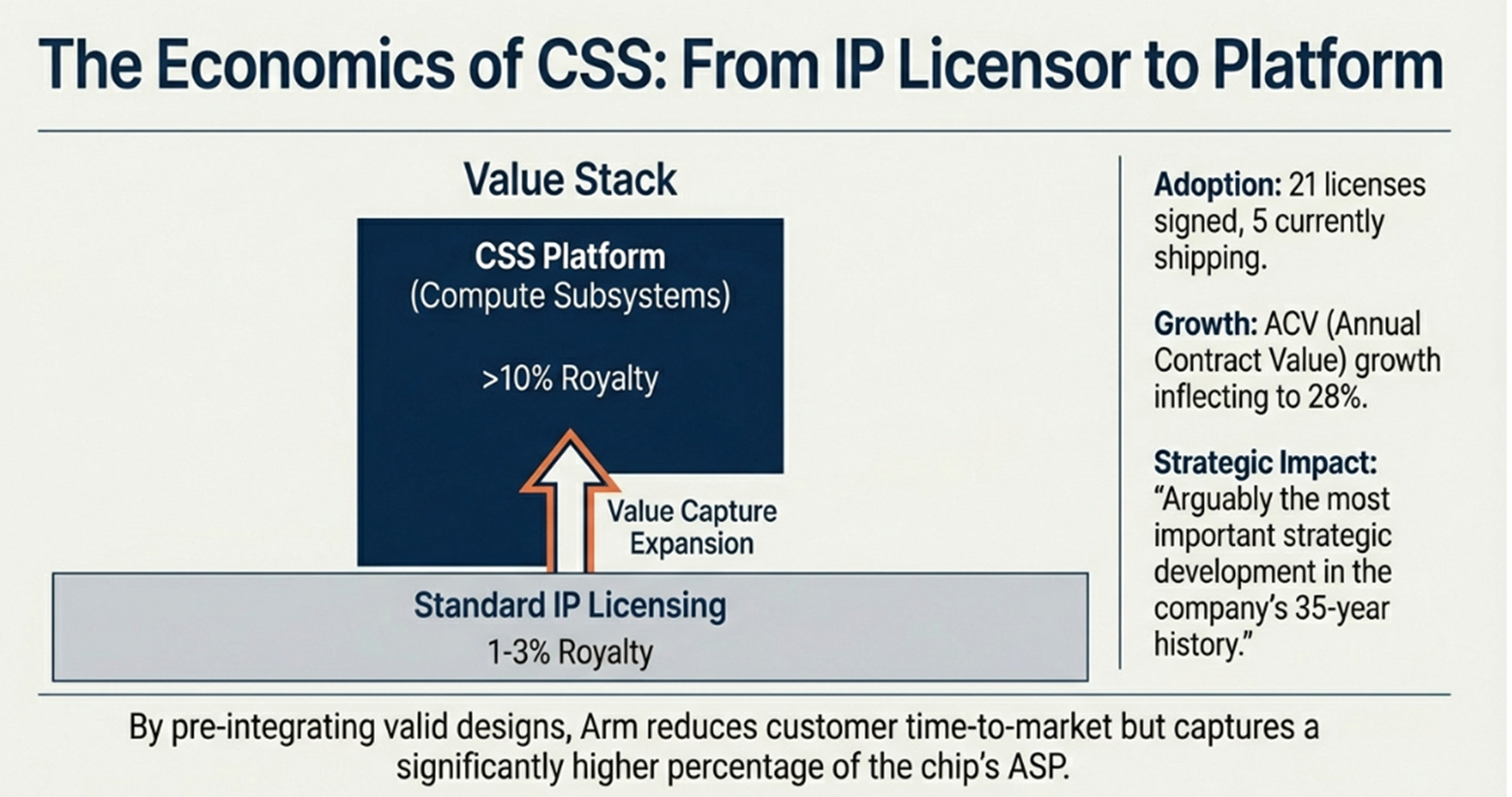

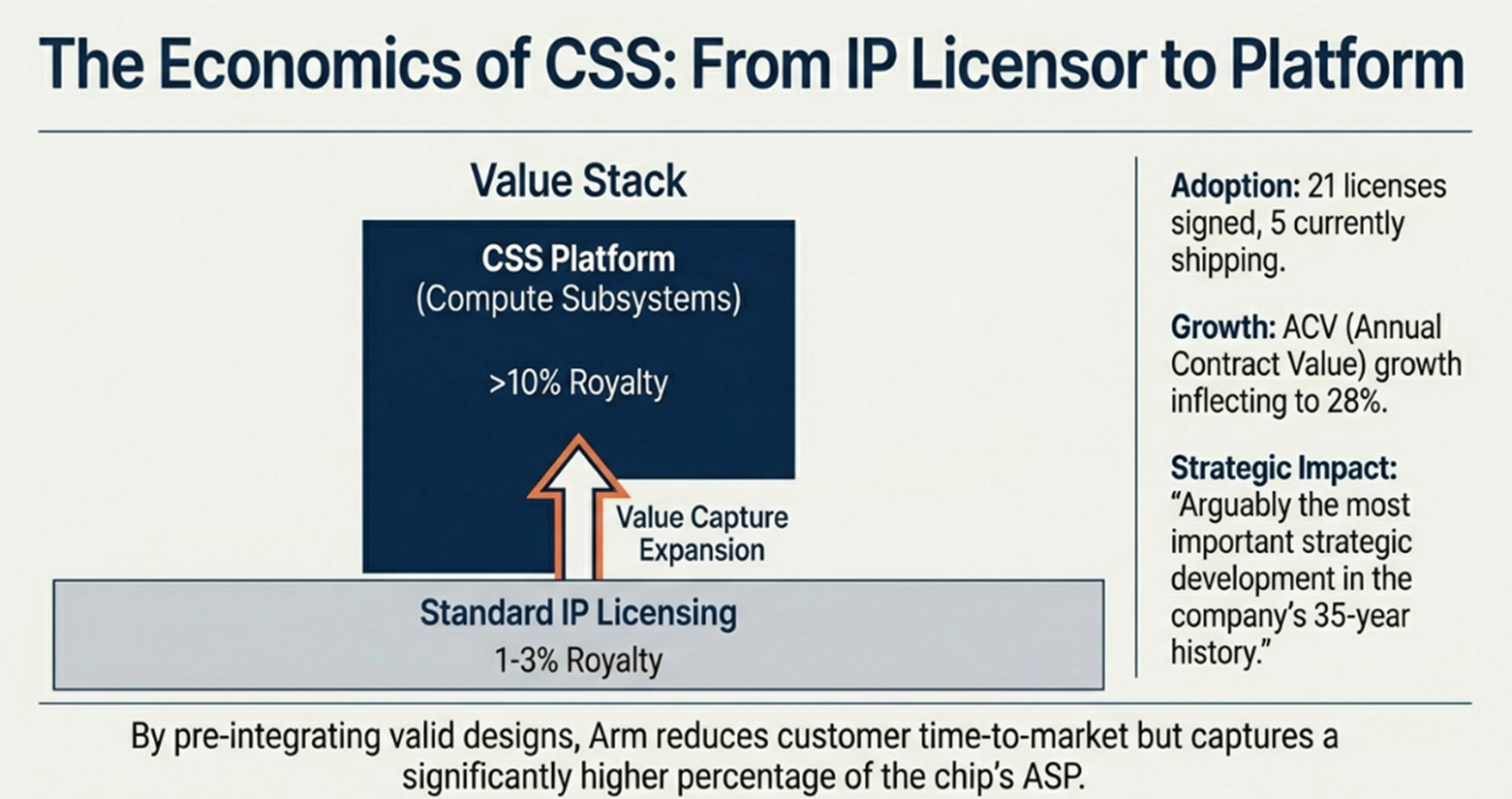

Through FY25, the data center thesis stopped being theoretical. AWS launched Graviton4, Google debuted Axion and migrated 30,000 applications, Microsoft shipped Cobalt 200. Every major hyperscaler committed. The question flipped from “can Arm win?” to “how big?” Then CSS changed the economics entirely , royalty rates went from 1-3% to north of 10% per chip. I called it in our prior analysis “arguably the most important strategic development in the company’s 35-year history.” Twenty-one licenses, five shipping, ACV growth inflecting to 28%. Arm became a platform company.

Which brings us to now. Haas told Bloomberg that data center was “exploding,” up 100% year-over-year. From the earnings call:

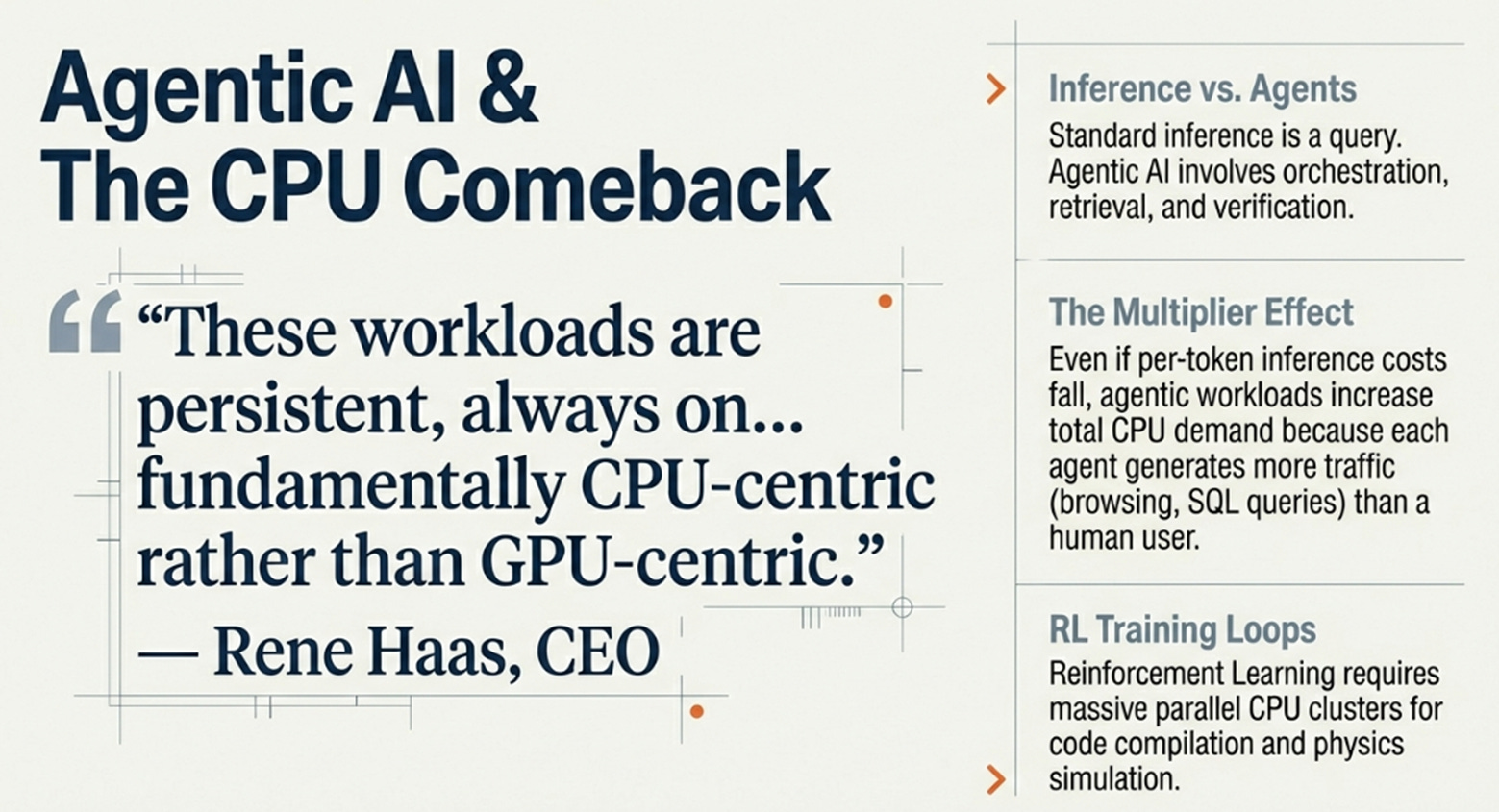

Haas: “The rise of agentic AI is creating enormous new demand for compute. These workloads are persistent, always on, and power constrained , fundamentally CPU-centric rather than GPU-centric. This is a structural expansion of Arm’s addressable market in the data center.”

Child: “Our revenues today come from technology developed years, in some cases decades, ago. The investments we’re making now in CSS, in our compute platforms, in our AI capabilities , these are building the revenue streams of the next decade.”

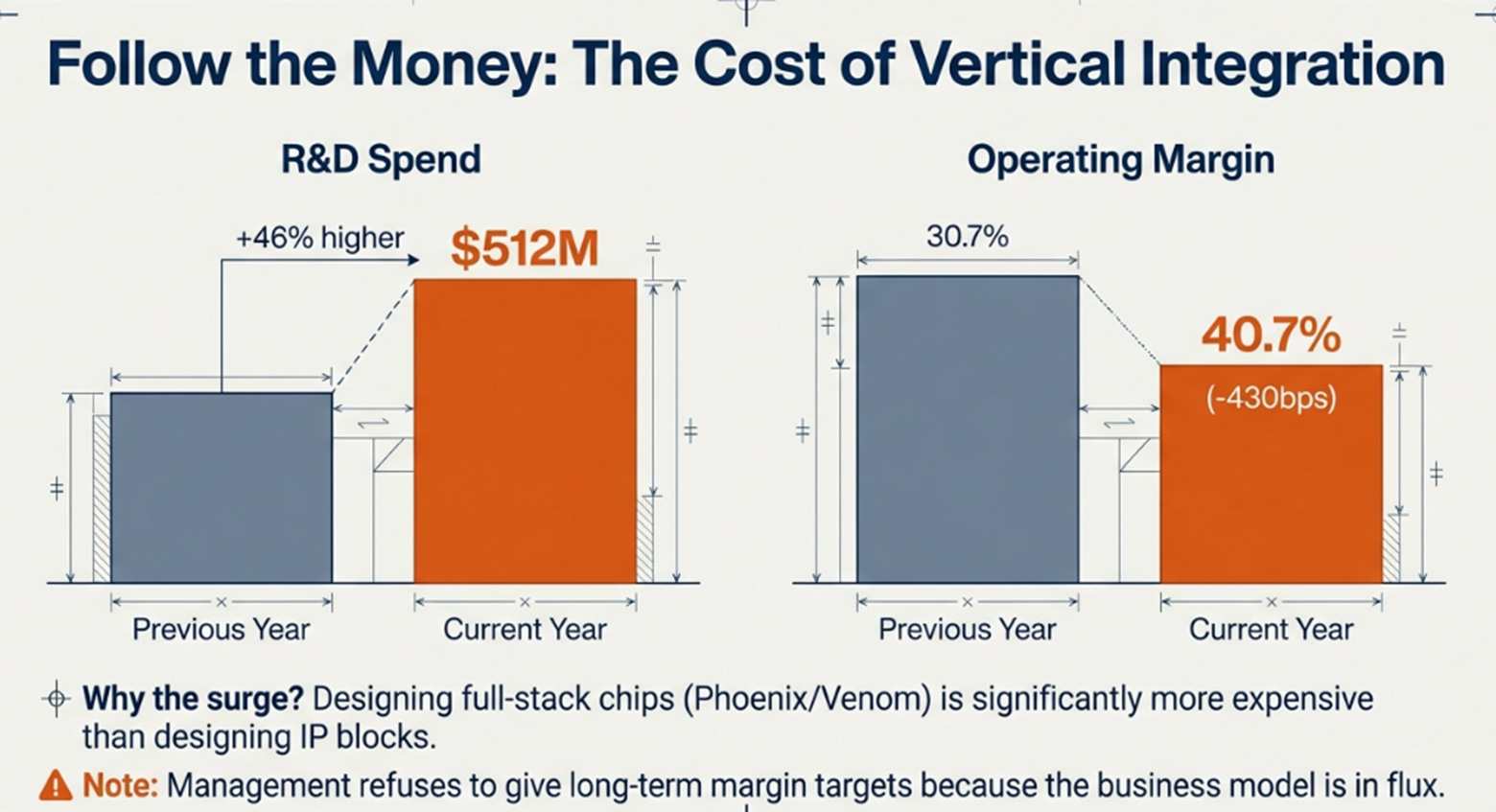

Haas is making two arguments and the market is only hearing one. The first , agentic workloads expand Arm’s TAM , is getting attention. The second, buried in Child’s framing, is more revealing. R&D surged 46% to $512 million. Operating margins compressed 430 basis points to 40.7%. What is all that R&D building? Thanks to SemiAnalysis, we now know: Arm is designing Phoenix, a complete 128-core datacenter

CPU for Meta, and Venom, a 228-core follow-on on TSMC N2 for 2027. This is full-stack chip engineering, not IP block development. Haas’s refusal to provide long-term targets makes more sense , the business model is mid-transformation and he doesn’t want to anchor to margins that reflect neither the old model nor the new one.

What was conspicuously absent: any datacenter royalty rate disclosure, any quantification of Neoverse as a percentage of total royalties (still ~10%, barely changed despite “triple-digit” growth), and any update on RISC-V competition. That last one is interesting , when you’re winning as decisively as Arm claims, you normally don’t mind discussing the competition.

The Bear Case Scorecard

I owe the reader an honest accounting of where the narrative has been right and wrong.

The bears who called Arm a mobile-dependent one-trick pony were wrong, full stop. Data center royalties doubled. Every hyperscaler committed. The RISC-V existential threat hasn’t materialized , not one major hyperscaler has shipped a RISC-V server CPU, and switching costs are higher than ever with Graviton5 at 192 cores and Cobalt 200 at 132.

Licensing lumpiness, however, remains entirely valid. Revenue missed by $15 million this quarter. The Q4 guide implies a step-up to roughly $700-750 million , the largest quarter in company history , and the full-year narrative depends on it.

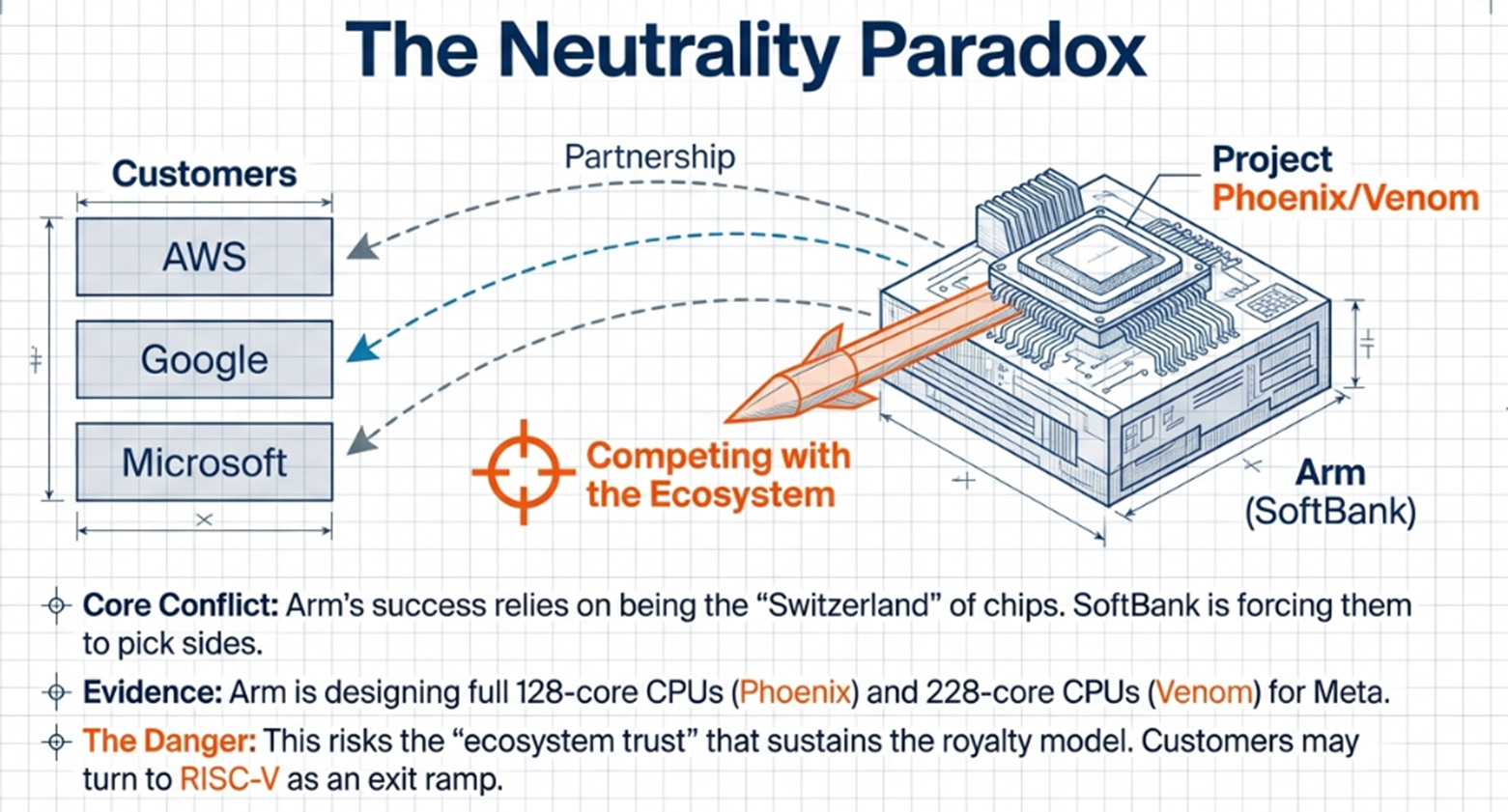

Then there’s SoftBank. I flagged this as the most underappreciated risk in prior analysis, and the concern has transformed rather than resolved. The old worry was share sales. The new worry is what SoftBank is doing with the company itself , acquiring Ampere for $6.5 billion (a company whose biggest customer saw purchases collapse from $48 million to $3 million in two years), directing Arm to design full CPUs for Meta and Stargate, redirecting Ampere’s talent into OpenAI infrastructure. This is no longer an overhang story. It’s a business model risk.

On the opportunity side, management has largely delivered. Armv9 is 25-30% of royalty mix and climbing , up from near-zero three years ago. Roughly half of current royalties still come from products launched over a decade ago, which means the Armv9/CSS revenue stream is in its infancy and compounding. CSS adoption exceeded the pace of traditional licensing. The 50% hyperscaler share target is within reach. And the AI positioning argument , that CPUs become more important in AI infrastructure, not less , has been independently validated in a way that surprised me.

Why CPUs Are Really Back , The Variant Perception

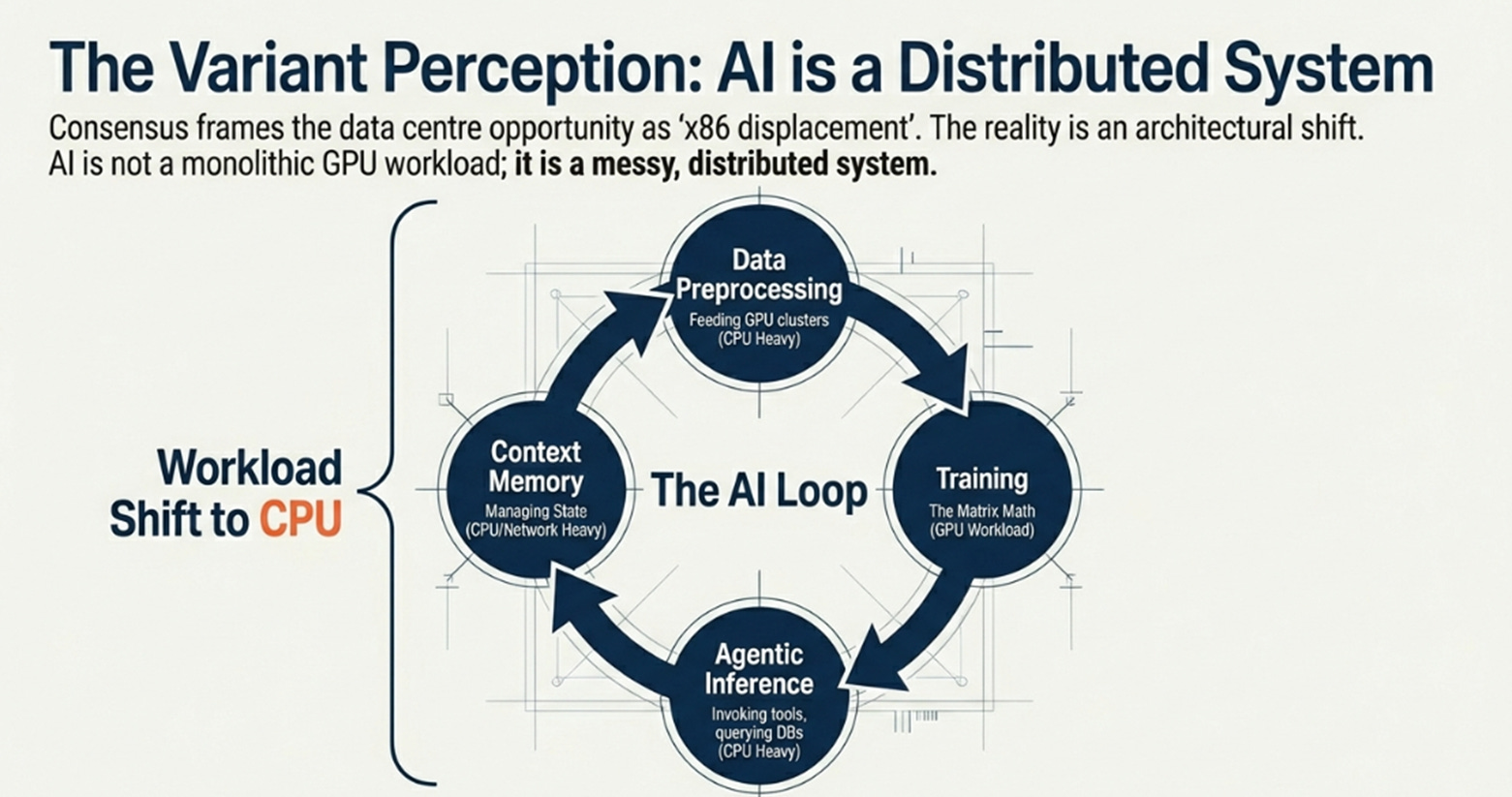

Every interesting investment has a variant perception. With Arm, the consensus frames the data center opportunity as “x86 displacement” , a share-shift story with a calculable ceiling. What the market hasn’t absorbed is something more fundamental, and the SemiAnalysis report published February 9 makes it viscerally clear.

AI is no longer a monolithic GPU workload. It has evolved into a messy, distributed system: RL training loops that require parallel CPU clusters for code compilation, verification, and physics simulation. Agentic inference where models invoke tools, query databases, and browse the internet , each agent generating more CPU-intensive traffic than a human ever could. Data preprocessing pipelines that keep GPU clusters fed. Context memory management that’s spawning entirely new infrastructure categories like NVIDIA’s Bluefield-4, which co-packages a full Grace CPU with a network controller.

This is not a cyclical demand bump. It’s an architectural shift in how AI systems work. Microsoft’s Fairwater datacenter dedicates 48 megawatts of CPU compute to support 295 megawatts of GPUs. Intel is scrambling for wafer capacity and raising Xeon prices. AI labs are competing directly with cloud providers for commodity servers. And here’s the non-obvious part: even if per-token inference cost falls, agentic workloads increase total CPU demand because each agent multiplies the orchestration, retrieval, and verification work that sits on CPUs. Optimization in one part of the system shifts load to another.

The second layer most people are missing is that DRAM has become the real gating function. Memory supply determines who gets CPUs deployed, which favors hyperscalers with procurement leverage , the same hyperscalers paying Arm royalties. And if supply tightness persists, chip ASPs rise, and since Arm charges royalties as a percentage of ASP, scarcity paradoxically increases per-unit royalty dollars. Nobody is modeling this explicitly.

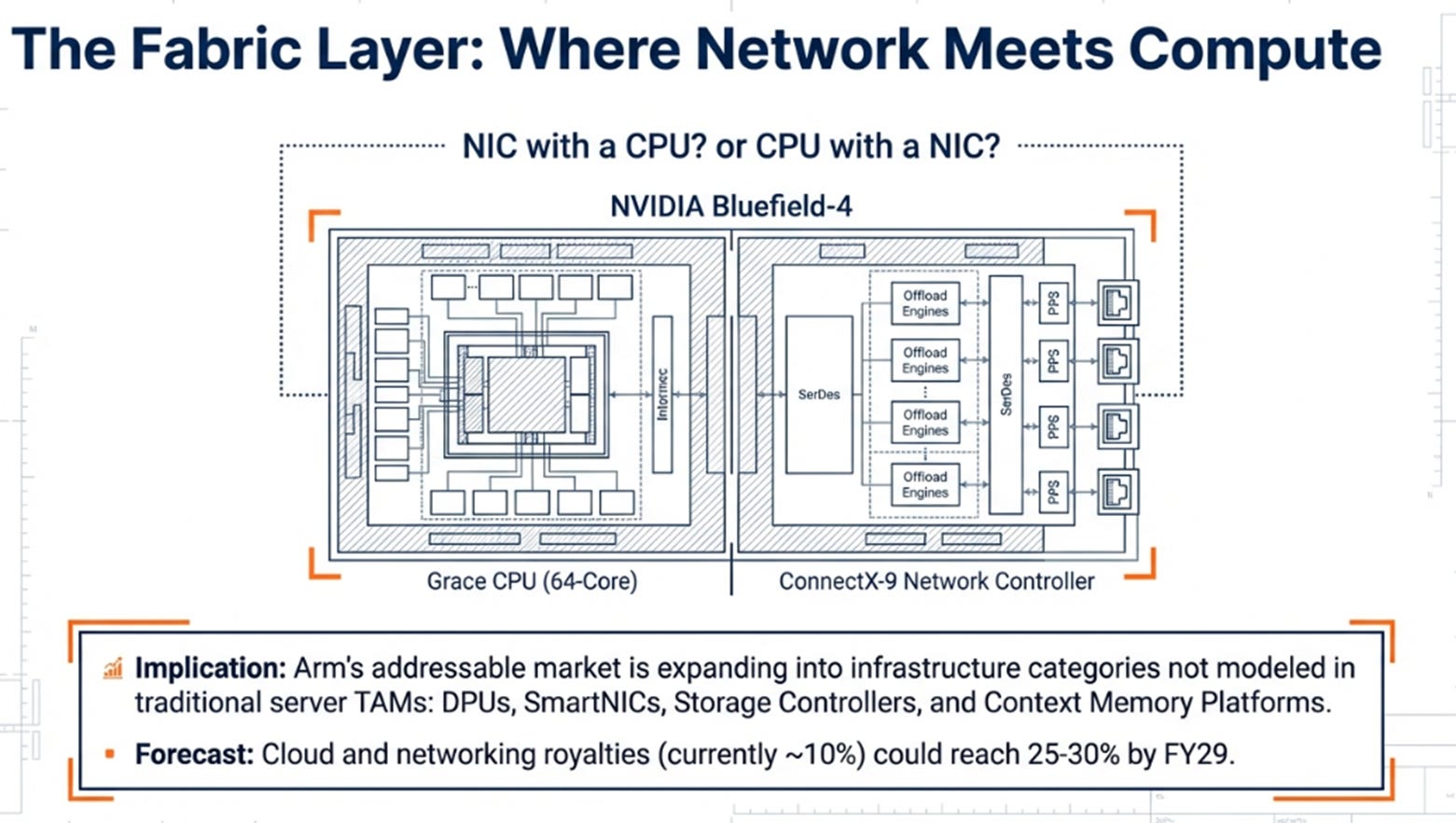

There’s a third layer that barely registers in Arm analysis: CPUs are bleeding into the network fabric itself. NVIDIA’s Bluefield-4 co-packages an entire 64-core Grace CPU with a ConnectX-9 network controller for context memory storage and KV-cache offload. Is that a NIC with a CPU, or a CPU with a NIC? The distinction is becoming meaningless, and it means Arm’s addressable surface area is expanding into infrastructure categories that don’t show up in traditional server CPU TAM models , DPUs, SmartNICs, storage controllers, context memory platforms. Each one pays royalties.

So the variant perception isn’t just “CPU TAM is expanding.” It’s that AI has structurally redefined what CPUs do, from a stagnant support function to a critical fabric layer in distributed AI systems , and Arm collects royalties on roughly half the hyperscaler volume in an expanding, supply-constrained market at improving per-chip economics, across an addressable surface area that keeps widening in non-obvious directions. Cloud and networking is still modeled at ~10% of royalties. I think it reaches 25-30% by FY29, and the dollar amount matters far more than the percentage.

But variant perceptions cut both ways. Phoenix , Arm designing complete CPUs for Meta and Stargate , is being priced as additive revenue. I think there’s a 20-30% probability over three years that it’s subtractive to the ecosystem trust that makes the royalty model work. AWS, Google, and Microsoft can see what’s happening. RISC-V gives them an exit ramp. The demand opportunity is bigger than consensus thinks, and the strategic risk is bigger than consensus thinks. Both tails are fatter than the market is pricing.

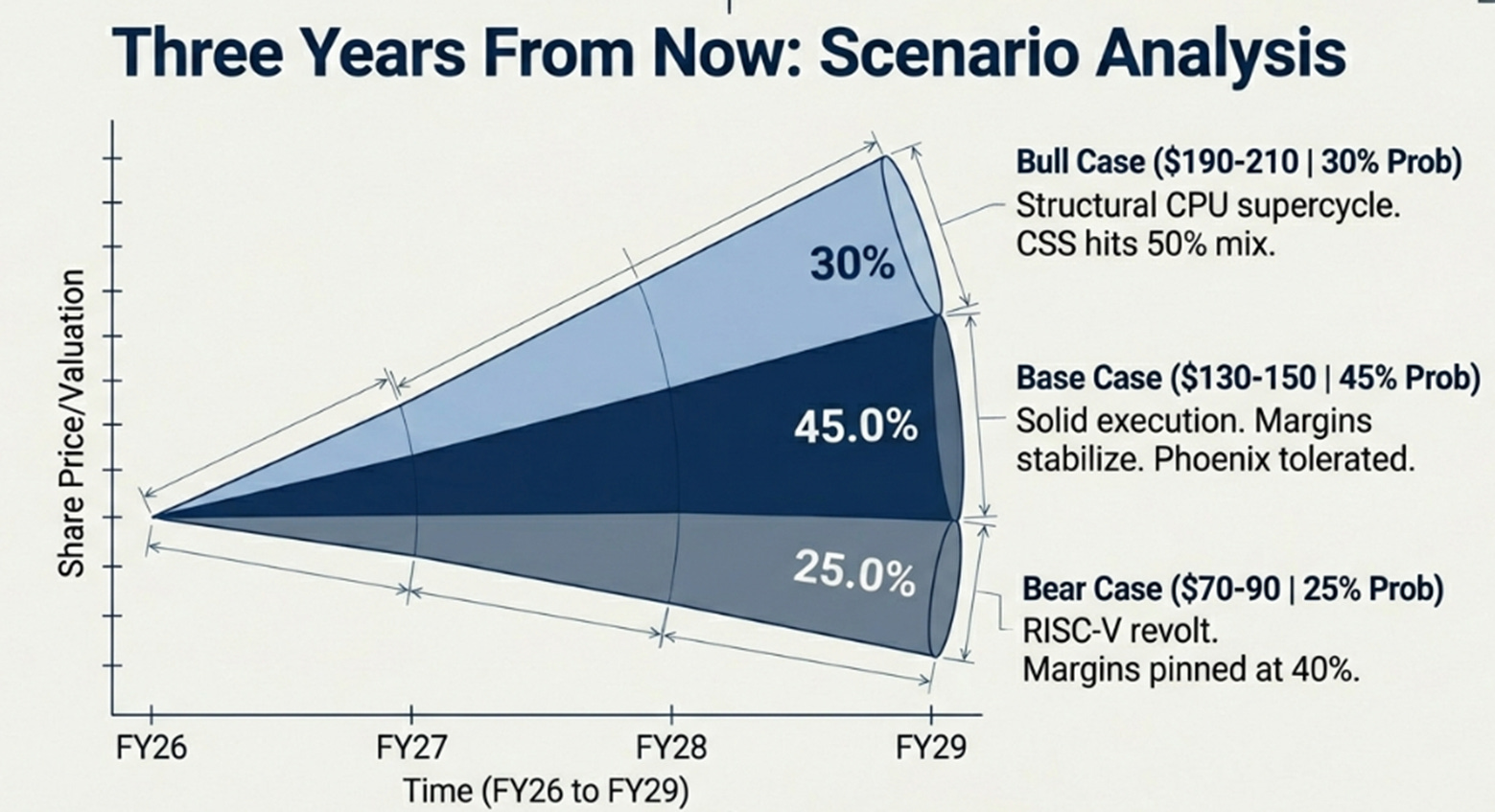

Three Years From Now

The divergence in outcomes is wide enough to put numbers on it. All assume roughly 1.07 billion diluted shares.

Bull , $190-210. Revenue compounds at 22-25% to $9-9.5 billion by FY29. The CPU supercycle proves structural as RL environments grow more complex and agentic inference scales , the CPU-to-GPU power ratio at facilities like Fairwater holds or expands, and every new GPU generation creates derivative CPU demand. CSS penetration reaches 40-50% of royalty mix, pushing blended royalty rates materially higher. Data center and automotive together reach 25-30% of royalties, up from ~10% today. Operating margins recover to 46-48% as revenue scales over the Phoenix/Venom investment base, and chip design revenue , while carrying lower gross margins than pure IP , is more than offset by the ecosystem expansion it enables. FY29 EPS around $4.50-5.00 at 42-45x forward. Key assumption: the distributed AI architecture is permanent, DRAM supply normalizes enough to let server builds proceed at scale, and Phoenix coexists with CSS licensing without eroding trust. Probability: 30%.

Base , $130-150. Revenue compounds at 17-20% to $7.5-8.5 billion. Data center growth decelerates to 30-40% as the RL/agentic demand wave matures and comps harden. CSS licenses reach 35, not 50 , the most willing customers have already signed, and the next wave takes longer to convert. Mobile remains steady; automotive grows but doesn’t inflect into a true third pillar. Margins stabilize at 43-45% , better than today’s 40.7% but below the 50% dream, because Phoenix and Venom are meaningful opex drags generating respectable but not spectacular returns. FY29 EPS $3.50-4.00 at 35-38x as growth slows toward high-teens. This is the “good company, fairly valued” outcome. Key assumption: solid execution, ecosystem tolerates Phoenix without revolt, but the growth rate normalizes. Probability: 45%.

Bear , $70-90. Revenue growth decelerates to 10-14%, reaching only $6.5-7 billion by FY29. Smartphones weaken, DRAM shortages constrain server builds rather than boosting ASPs, and one or two hyperscalers announce strategic RISC-V programs in response to Phoenix , the canary that the neutrality premium is dying. Margins pinned at 40-42% as chip design costs never achieve sufficient scale, while CSS engineering engagement prevents a return to pure-IP margin levels. The “fabric layer” thesis proves premature as DPU adoption stalls and context memory remains niche. FY29 EPS $2.50-3.00 at 28-32x as the market re-rates Arm from “platform compounder” to “good-but-not-great semiconductor company with governance risk.” Key assumption: the supercycle was cyclical not structural, and SoftBank’s vertical integration visibly damages the ecosystem. Probability: 25%.

Expected value: roughly $135-150 versus $111 today. Positive skew, but the bear case involves a structural de-rating that could take years to recover from.

What I’m Tracking

Six items, in order of importance.

Data center royalty growth is the single most important number. If it’s still 70%+ by Q2 FY27, the supercycle thesis is intact. Below 40%, the demand wave was more cyclical than structural.

Operating margin trajectory and the March 24 Investor Day. I need to see a credible path above 43% by mid-FY27 and a framework for how chip design economics coexist with IP licensing margins. If Haas punts on long-term targets again, that’s a yellow flag.

Hyperscaler RISC-V signals. Today this is token investment , $10-20 million annually, mostly research. If any hyperscaler announces a $200 million+ strategic program, the trust premium is eroding. Watch hiring and academic papers, not product launches.

CSS license quality. Are new licenses coming from data center and automotive (high ASP, high royalty dollars) or predominantly mobile? Broad-based expansion validates the platform flywheel. Mobile concentration puts a ceiling on the value-capture story.

Q4 licensing execution. The $700-750 million implied step-up is the largest quarter ever. A miss moves lumpiness from annoyance to thesis risk.

DRAM and CPU supply dynamics. If scarcity persists, higher chip ASPs mechanically increase Arm’s per-unit royalty dollars , a tailwind nobody is modeling. But if DRAM shortages actually prevent server builds, it delays royalty realization entirely. This is a double-edged sword worth watching closely.

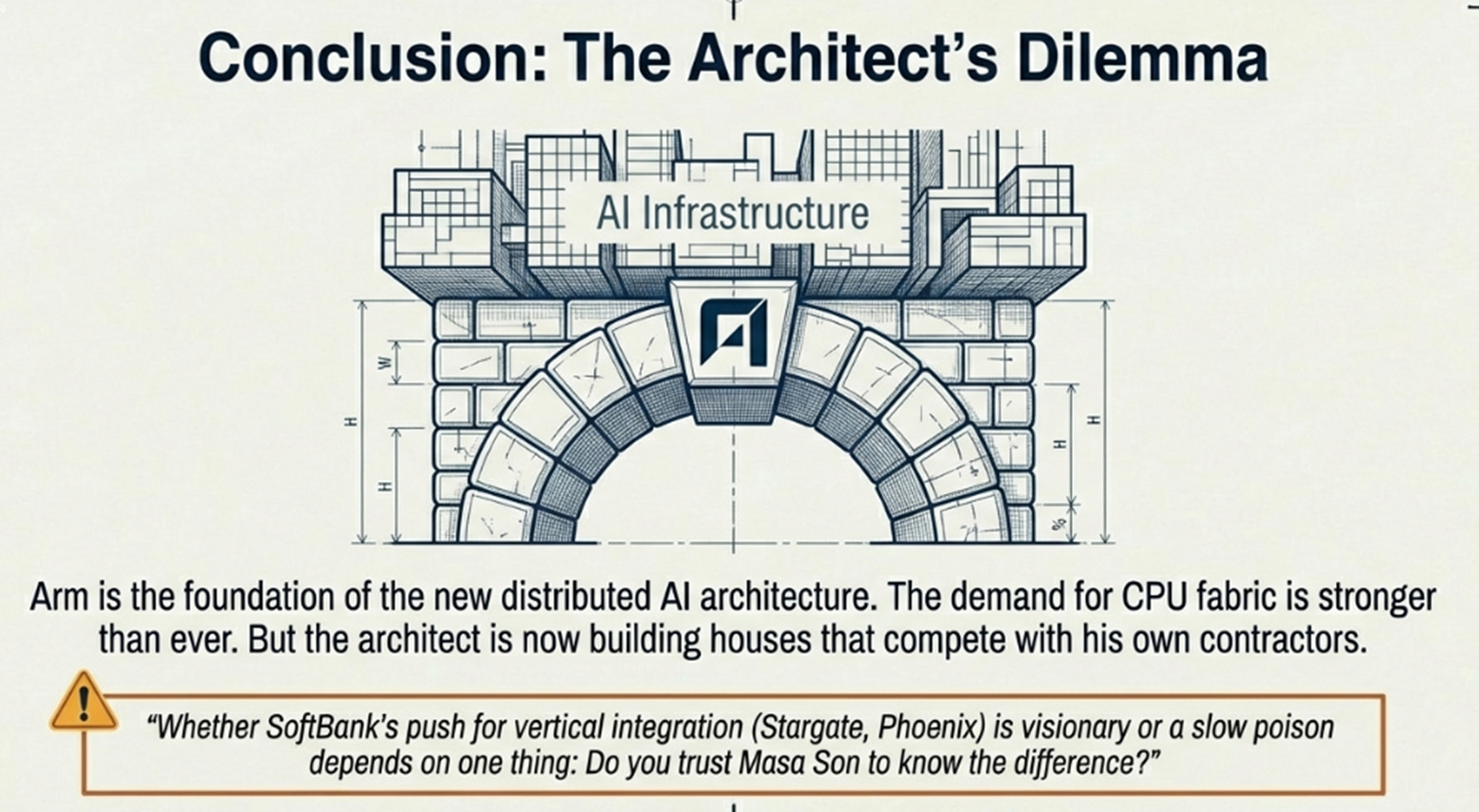

The architecture has never been more central to computing , not just in phones and servers, but in DPUs, network controllers, context memory platforms, and AI training infrastructure that didn’t exist three years ago. Arm sits at the foundation of a distributed AI system that is structurally more CPU-hungry than anything the industry has built before, collecting improving royalties on expanding volume across a widening surface area. That’s the bull case, and the demand evidence has never been stronger.

The architect, however, is starting to build houses that compete with the contractors who depend on the blueprints. SoftBank acquired $6.5 billion worth of failed merchant silicon talent and pointed it at Stargate. Phoenix ships to Meta. Venom targets 228 cores on N2 for 2027. The CSS trust premium , the thing that made Arm’s centrality possible in the first place , is being tested by the same parent company that took it public. Whether that’s visionary vertical integration or a slow poison depends on one thing: do you trust Masa Son to know the difference?

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.