ARM’s 4QFY26 Earnings: AI Upside, Platform Risk

Arm’s AGI CPU strategy is not just a response to agentic AI demand. It is Rene Haas’s deliberate trade of neutrality for value capture, and the next three years will decide whether Arm becomes the CPU

TL;DR

Agentic AI makes Arm’s architecture structurally more valuable because CPU orchestration inside fixed power envelopes becomes a binding constraint, and x86 looks increasingly disadvantaged.

But Arm’s AGI CPU strategy breaks the neutrality that made the platform powerful, turning Arm from Switzerland into a potential competitor to its largest licensees.

At $253, the stock prices in too much of the “Platform Owner” outcome, while underweighting the risk that licensees hedge, RISC-V gains traction, and Arm’s platform premium erodes.

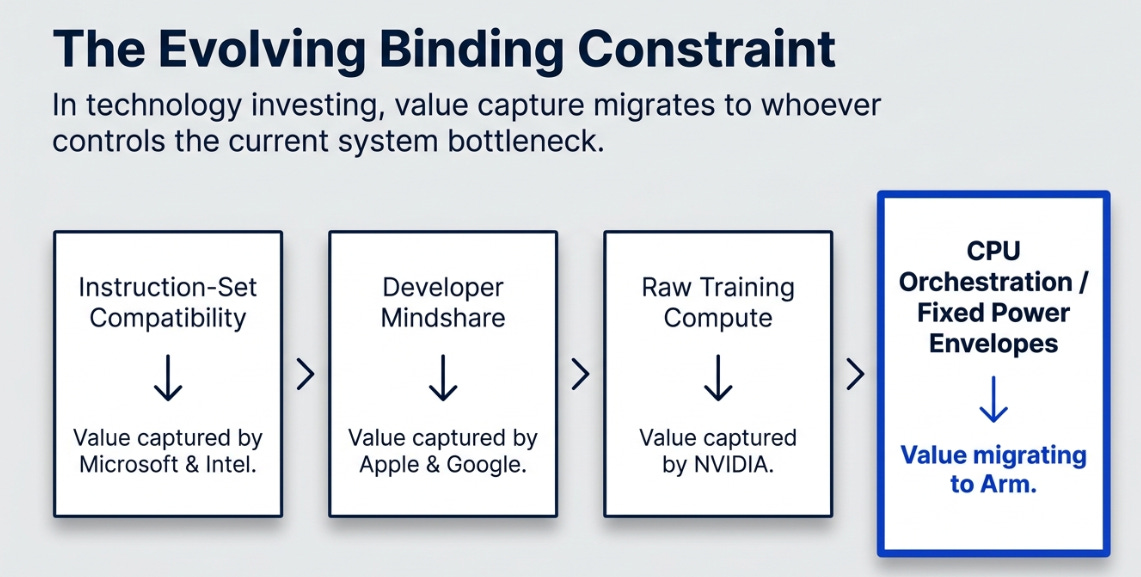

In computing, the question of who captures value is always a question of who controls the binding constraint. When the constraint was instruction-set compatibility, the answer was Microsoft and Intel. When the constraint was developer mindshare, it was Apple and Google. When the constraint became raw training compute, it became NVIDIA. The constraint moves; the value moves with it; and most of the analytical work in technology investing is correctly identifying which constraint is becoming binding next, before the price has finished adjusting.

The standard reading of Arm’s Q4 print is that agentic AI is creating a new constraint, CPU orchestration capacity inside fixed power envelopes, and Arm is the natural beneficiary. Rene Haas told the market that “soon, the data center will be Arm’s largest business.” The AGI CPU pipeline doubled to over $2 billion in six weeks. Data center royalties more than doubled year-over-year for the third consecutive quarter. The narrative writes itself: Arm is riding the second act of the AI infrastructure buildout, and the only remaining question is execution.

I think this reading has the causality backwards. The AGI CPU is not Arm’s response to AI demand. It is Arm’s deliberate trade of platform neutrality for value capture, a wager that the company has spent thirty-five years undermonetizing its position as the default compute architecture, and that the AI moment provides the cover and the commercial vehicle to fix it. The agentic AI workload shift made the trade easier to explain. It did not make the trade. The strategic logic, that Arm could no longer afford to be Switzerland, was building before agentic workloads were a slide-deck phrase, and it would have been built into the next five years of Arm’s roadmap whether AI accelerated or not.

This matters because it changes the question we should be asking. If Arm is a beneficiary of an external trend, the investor question is “how big does AI get and how much of it does Arm capture.” If Arm is a company making a structural choice, the investor question is “can a platform survive its owner becoming a competitor inside it?” Those are different questions, and the answer to the second is less knowable than the analyst community pretends.

When I wrote about Arm in May after the Q4 print, the argument was that the mechanism was real but the price had front-run it. I am updating that view in two directions at once. The mechanism is more structural than I credited; the neutrality cost is also more structural than I credited. Both updates widen the range of plausible outcomes, Arm in three years is more likely to be either substantially more valuable or substantially less valuable than today’s price than the consensus models allow.

The New Bottleneck Is Power, Not Compute

Start with the architectural argument, because everything else depends on it.

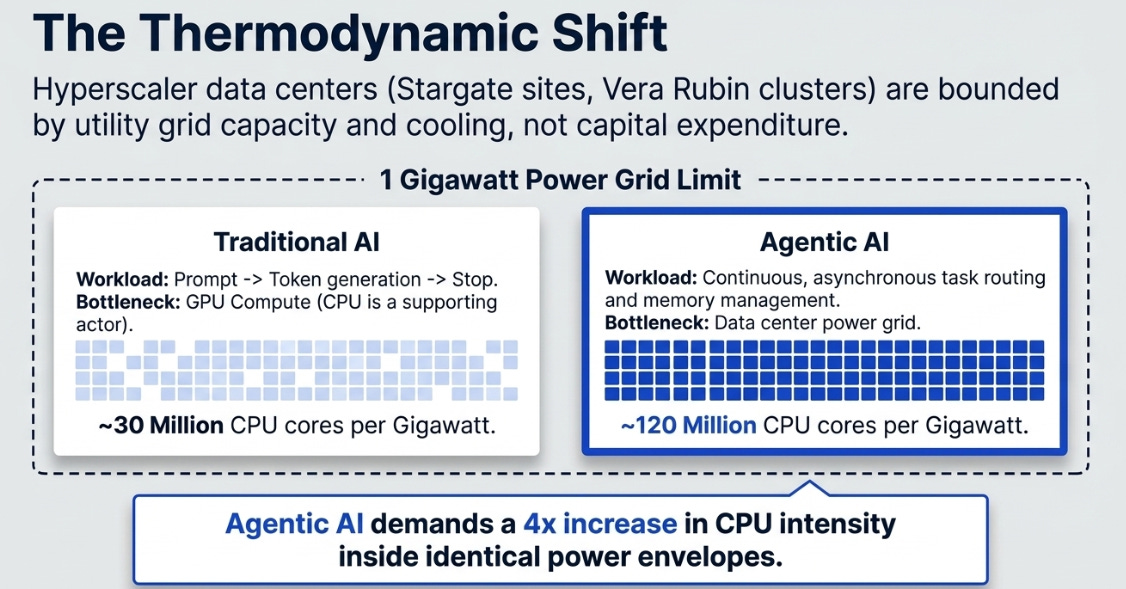

The previous AI cycle ran on raw compute. Larger models, more parameters, more training tokens, more inference. The bottleneck was the GPU, the spoils went to NVIDIA, and the CPU was a necessary but unremarkable supporting actor. In that world, Arm’s performance-per-watt advantage was useful but not central, x86 could absorb the extra power cost because compute density, not power density, was the binding constraint.

Agentic AI changes the shape of the workload. Agents do not generate tokens in response to prompts and stop. They run continuously, asynchronously, executing workflows that schedule tasks, route data, manage memory, enforce security, and feed accelerators on a 24/7 basis. Arm’s slide deck quantifies the implication: traditional AI workloads need roughly thirty million CPU cores per gigawatt; agentic AI needs one hundred and twenty million, four times the CPU intensity inside the same power envelope. The phrase “inside the same power envelope” is doing all the work in that sentence. Hyperscaler data centers are bounded by utility grid capacity and cooling capacity, not by capex. Stargate sites, new AI campuses, the Vera Rubin clusters, all of these are provisioning against power limits that are slow to expand.

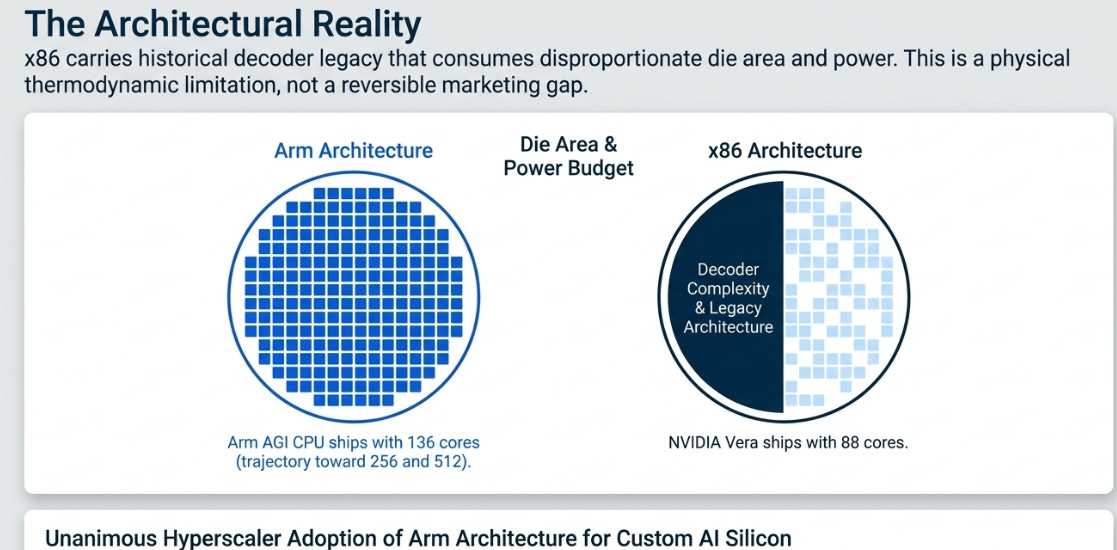

x86 cannot solve this problem. The instruction set carries decoder complexity and historical legacy that consume die area and power per core. At the core counts agentic workloads require, Arm’s AGI CPU ships with 136 cores, NVIDIA’s Vera with 88, the trajectory points toward 256 and 512, x86 simply cannot pack the cores into the available power budget. This is not a marketing claim or a competitive disadvantage that better engineering could close. It is a physical limitation of the architecture. Every hyperscaler with the engineering capacity to choose any architecture has chosen Arm: AWS Graviton,

Google Axion, Microsoft Cobalt, NVIDIA Grace and now Vera. None chose to extend x86. None chose RISC-V for production AI infrastructure. The pattern is unanimous because the constraint is binding and the choice is mathematical.

This reframes the compounding loop in a way that matters. The standard analyst framing is that Arm benefits from a network effect in software optimization, more deployments, more software written for Arm, easier next adoption. That is correct but understates the structural sturdiness. The loop is not running on a market preference that could reverse if a competitor builds a better marketing story. It is running on a thermodynamic constraint that strengthens every time agentic workloads expand. The conservative case for Arm, the IP/CSS business compounding through contracted royalties at a 20% CAGR through FY31, with more than 70% of those royalties already under contract, is therefore not really a forecast. It is a derivative of a physical constraint operating on data center construction.

This is the part of the thesis that is more durable than I credited in May. The mechanism does not weaken at scale. It accelerates.

The Price of No Longer Being Switzerland

Now turn the argument over and look at the other side.

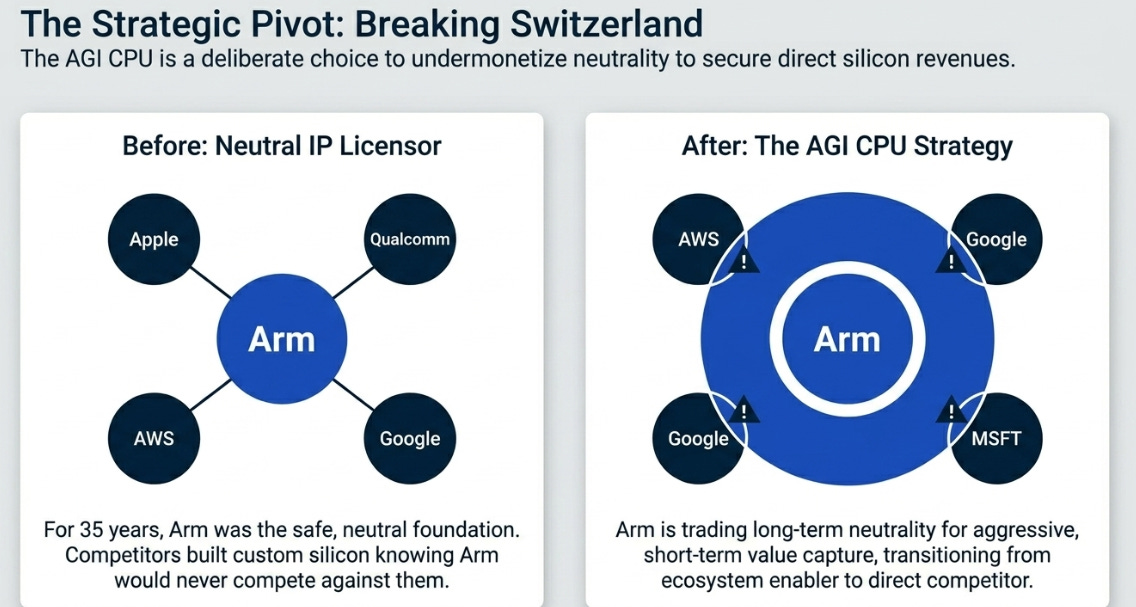

Arm’s value as a platform was never really about the silicon. It was about the neutrality. For thirty-five years, every chip designer in the world, including chip designers competing fiercely with each other, could license Arm’s IP knowing that the company would not turn into a competitor. Apple licensed Arm and built its own silicon. Qualcomm licensed Arm and built its own silicon. AWS, Google, Microsoft, NVIDIA all licensed Arm and built their own silicon. The platform compounded because Arm’s neutrality made it safe for everyone to build on top of it. Arm was Switzerland, and Switzerland’s value comes precisely from refusing to take sides.

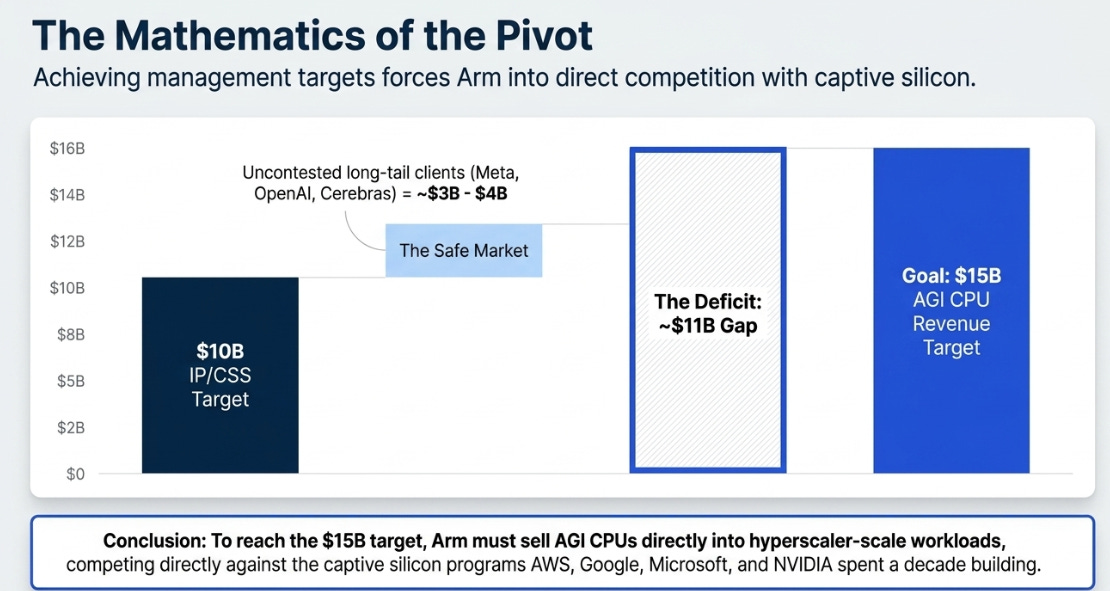

The AGI CPU is a deliberate decision to take a side. Haas chose to break the neutrality on purpose, and the strategic point most analysts miss is that this choice was not forced on him. The standard framing is that Arm is selling silicon only to the long tail of customers who would never have built their own, Meta, OpenAI, Cloudflare, SAP, SK Telecom, Cerebras, and that the move therefore does not threaten the existing licensee relationships. This is true today. It will not be true in five years.

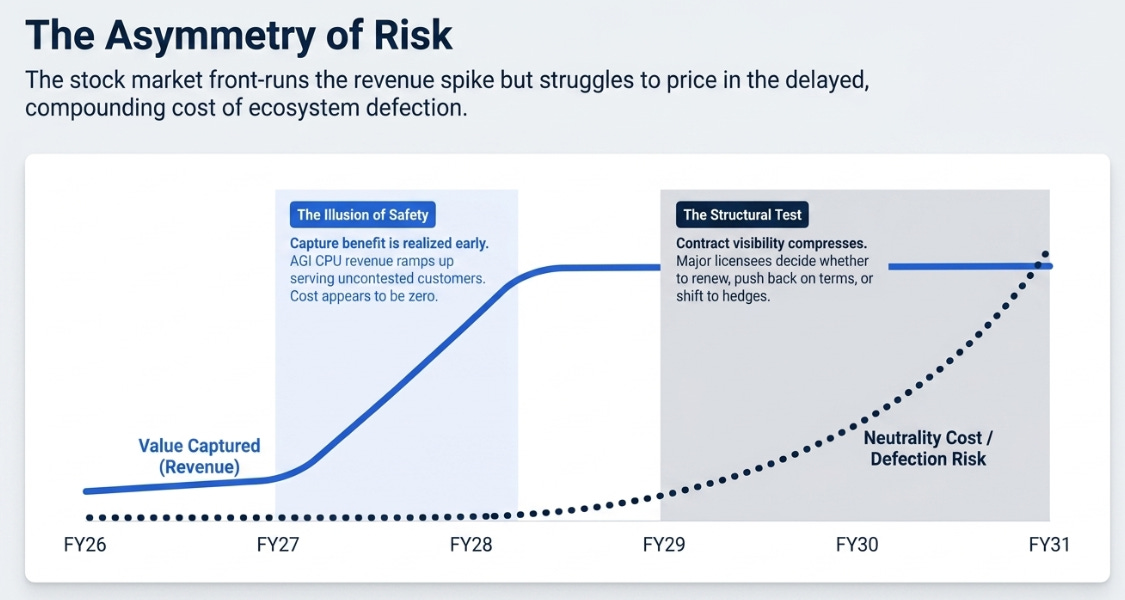

The math forces the issue. Management’s FY31 framework targets fifteen billion dollars in AGI CPU revenue against ten billion in IP/CSS. The long-tail-only customer set, by any honest accounting, is worth perhaps three or four billion at maturity. Getting to fifteen billion requires Arm to sell into hyperscaler-scale workloads, which puts the AGI CPU in direct competition with the captive silicon programs that AWS, Google, Microsoft and NVIDIA have spent the last decade building. The neutrality cost is currently zero because the silicon business is small and serving uncontested customers. By FY29 or FY30, when Arm is meaningfully competing with its largest licensees for the largest data center deployments, the cost compounds.

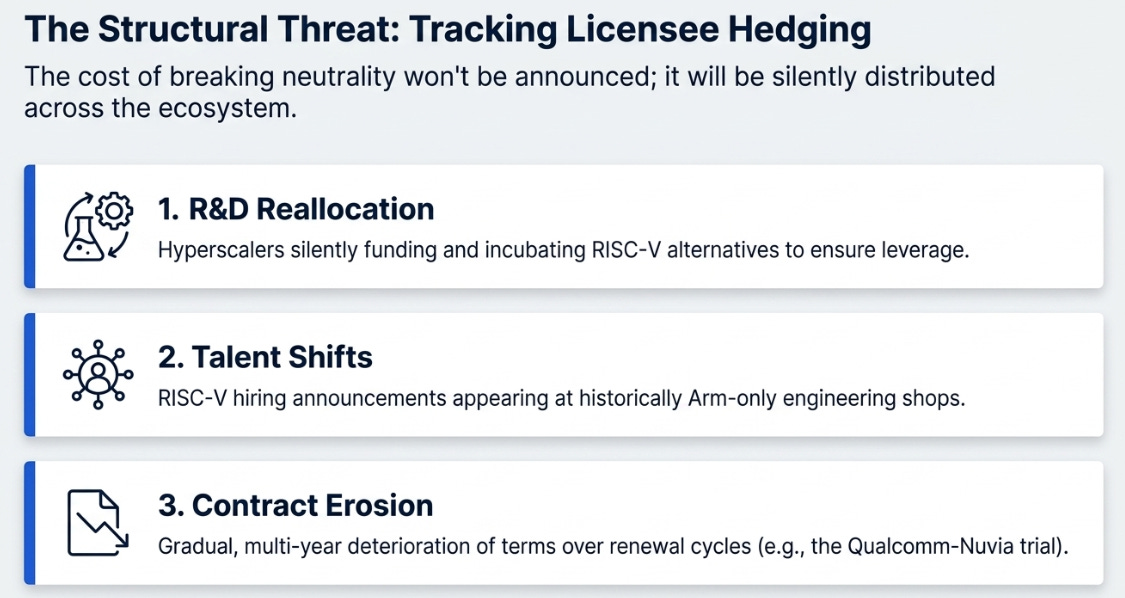

The Qualcomm-Nuvia trial scheduled for late 2026 is the visible test of this dynamic, but it is not the structural one. The structural test is in FY28 and FY29, when the contracted royalty visibility we currently celebrate begins to compress, and licensees decide whether to renew at standard rates, push back on terms, or hedge by funding RISC-V alternatives. If you are a hyperscaler in 2028 watching Arm sell silicon directly to your prospective customers, the right strategic response is to fund a credible alternative, even if you do not immediately deploy it. That is the slow, distributed canary worth watching, and it will not show up in any single quarter’s reported numbers. It will show up in licensee R&D allocations, in conference papers, in RISC-V hiring announcements at companies that previously would not have hired RISC-V engineers, and in the gradual erosion of contract terms over multiple renewal cycles.

The risk is asymmetric in time. The capture benefit is realized first, in the FY27 and FY28 AGI CPU revenue ramp. The neutrality cost is realized later, in the FY29 through FY31 royalty growth that disappoints because licensees have spent the intervening years quietly hedging. Management is making an explicit bet that the platform is sticky enough, the software ecosystem deep enough, the developer base committed enough, that licensees cannot credibly defect even when motivated to. They might be right. They might be partially right. They might be wrong in ways that take three years to become visible. The uncertainty itself is the bargain.

Three Ways the Bargain Can Resolve

The combination of stronger mechanism and realer neutrality cost produces a wider range of outcomes than consensus models allow. Here is how I would frame the three plausible terminal states for Arm in fiscal 2029, three years out from today:

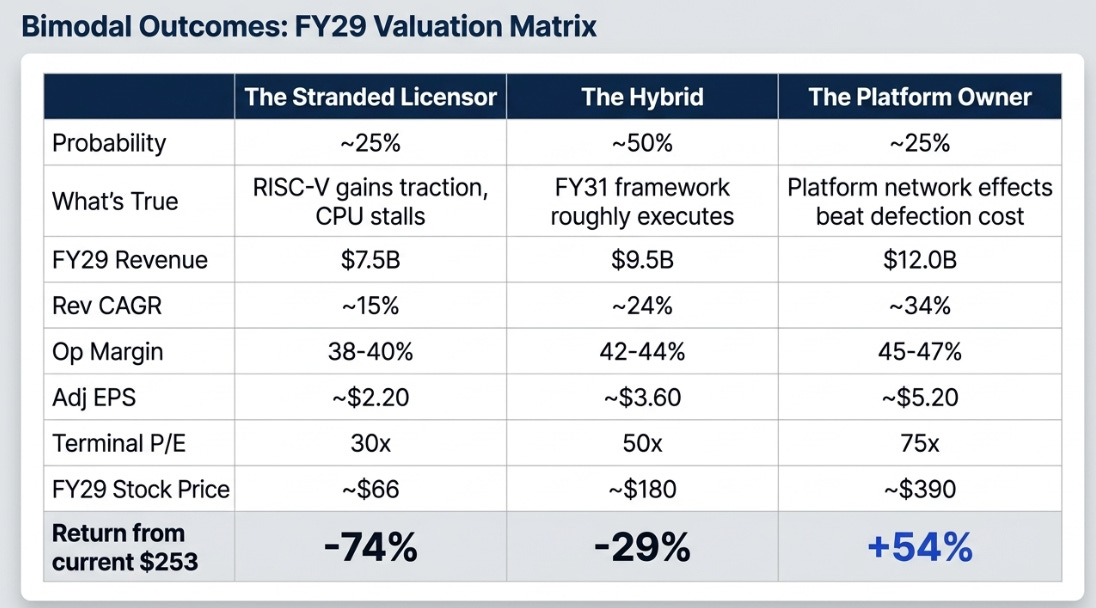

In The Stranded Licensor outcome, Arm reverts to being a high-quality IP business that has lost its platform premium. The contracted royalties hold the floor, this is why the bear case is not catastrophic, but the AGI CPU strategy is judged in retrospect as a self-inflicted wound that compromised the moat in pursuit of incremental revenue that turned out to be smaller than the cost. The historical analog is Imagination Technologies after losing Apple: a structurally diminished company that still earned royalties for years afterward but never recovered platform status. The market re-rates Arm violently downward when the realization sets in, somewhere in late 2027 or 2028, and the stock spends the rest of the decade as a value name rather than a growth one.

In The Hybrid outcome, which I think is the modal case, Arm becomes roughly what management is selling: a twenty-five billion dollar revenue company by FY31 with both an IP/CSS engine and a silicon business, valued at the appropriate blended multiple. The bull thesis of operating leverage doesn’t quite work because the silicon mix shift compresses margins (this is the analytical point that most consensus models miss, at FY31 mix, blended operating margin is roughly 44%, essentially flat with FY26’s 43%). But absolute profit dollars grow enough that EPS compounds attractively. The market eventually re-rates to a hybrid multiple, somewhere between software and semis, and the stock works modestly from a lower starting price than today’s $253. Investors who bought at the current level make low-single-digit annual returns; investors who bought on a 20% pullback make low-teens returns.

In The Platform Owner outcome, Arm becomes the AWS of CPU compute. The thermodynamic constraint proves binding through the entire decade, AGI CPU revenue exceeds the fifteen-billion FY31 target, and the platform survives the capture move because the software ecosystem is genuinely deeper than skeptics credited. The multiple holds at premium because growth stays above 30% and the network effects strengthen with each marginal deployment. The historical analog is NVIDIA’s transition from a graphics chip company to the AI infrastructure platform, once the market recognized the structural shift in 2023, the multiple stayed elevated for years and the stock compounded faster than the underlying earnings.

The probability-weighted price target is approximately two hundred dollars in three years, against today’s two hundred and fifty-three. That is roughly negative seven percent expected annualized return, before considering the time value of capital. The asymmetry cuts both ways, fifty-four percent upside in the Platform Owner case, seventy-four percent downside in the Stranded Licensor case, but the expected value is unattractive at the current price.

The variant perception, then, is not directional. It is about variance. Consensus models assume the FY31 framework executes roughly as stated and apply a tightening multiple as growth normalizes. The reality is more bimodal: Arm in FY29 is meaningfully more likely to be either The Platform Owner or The Stranded Licensor than the smooth-glide-path The Hybrid, because the strategic choice Haas made introduces real path dependency. The three futures are not points on a continuous distribution; they are different companies with different business models and different appropriate multiples.

The Signals That Will Decide the Outcome

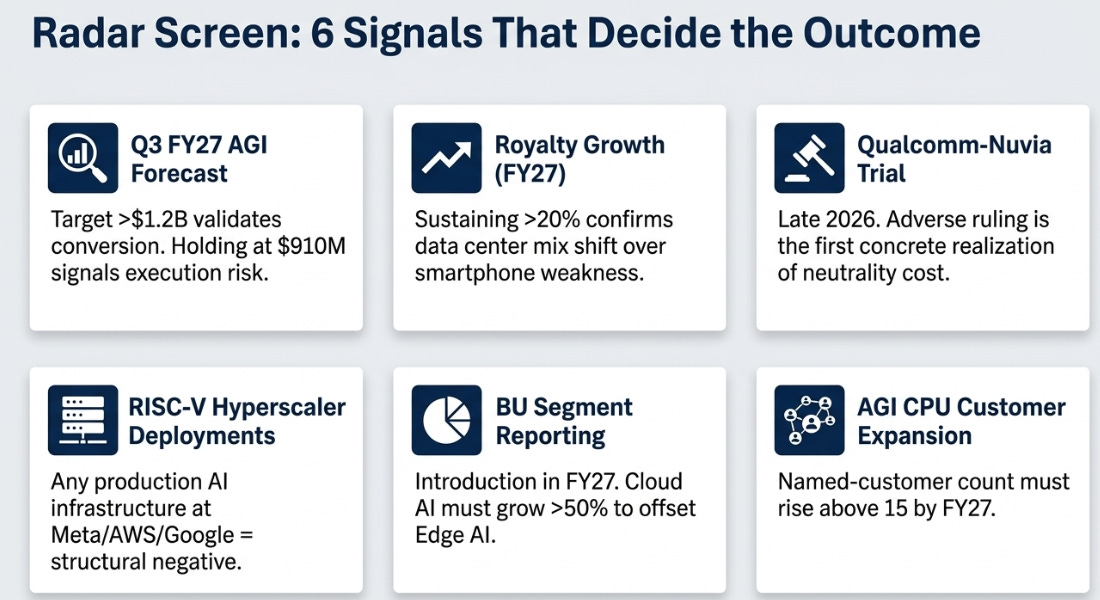

Six observable conditions will distinguish which future is unfolding. The Q3 FY27 update in February 2027 is the first checkpoint: a raise of the AGI CPU revenue forecast above $1.2 billion for FY28 means the supply-constrained framing was real and conversion is happening; a hold at $910 million means demand exceeded execution capability and conversion risk dominates. Royalty growth through FY27 needs to sustain at 20% or above to confirm the data center mix shift; deceleration below 17% means the smartphone weakness is intensifying faster than data center can offset. The Qualcomm-Nuvia trial outcome in late calendar 2026, settlement is neutral, an Arm win is mildly positive, an adverse ruling against Arm is the first concrete realization of the neutrality cost. RISC-V hyperscaler signals: any production deployment of RISC-V infrastructure for AI workloads at Meta, AWS, Google, or Microsoft would be the first structural negative for the moat thesis. The BU segment reporting that I expect Arm to introduce in FY27 will reveal the underlying growth dispersion, Cloud AI growing 50% with Edge AI growing low single digits would confirm the data center transformation. And AGI CPU customer expansion beyond the original eight launch customers, the named-customer count rising above fifteen by FY27 means the addressable market is broader than initially scoped.

The Q4 print showed the mechanism working. The Q1 print will show whether the trajectory is sustainable. Neither will answer the question that matters. The question that determines whether Arm is a four-hundred-dollar stock or a hundred-dollar stock by FY29 is whether the platform survives the strategic choice its owner made when he decided neutrality was undermonetizing the franchise. That question is not knowable from any quarter’s data. It will be answered slowly, through licensee renewal cycles and RISC-V investments and software ecosystem evolution and the long arc of how the AI infrastructure market structures itself. At $253, the price embeds The Platform Owner outcome with little discount for the alternatives. The bargain Haas made may turn out to be brilliant. The price the market is paying assumes it already has.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.