ASML 1Q26 Earnings: The Bottleneck Gets Priced Differently

The old debate was whether AI demand was real. That debate is over. The new one is whether ASML is still a cyclical tool vendor, or an infrastructure utility whose installed base compounds faster than

TL;DR

ASML is no longer just selling lithography tools; it is increasingly monetizing output. Throughput upgrades, software-led performance gains, and service attached to an expanding installed base are turning the physics moat into a recurring earnings engine.

Installed Base Management is now big enough to matter on valuation. A roughly €10B annualized recurring business growing at a strong clip should not be valued like lumpy hardware shipments, and that mismatch is the heart of the re-rating case.

The main risk is now policy, not demand. Non-China demand looks durable, memory and logic customers are still pushing capacity, and the key swing factor is whether export controls interrupt the compounding before the market fully re-prices the business.

“ASML raised its full-year sales forecast as the surge in global artificial intelligence spending fuels semiconductor production and boosts demand for the company’s advanced chipmaking machines. Net sales will be between €36 billion and €40 billion this year.”, - Bloomberg, April 15, 2026

I want to start by retiring a question.

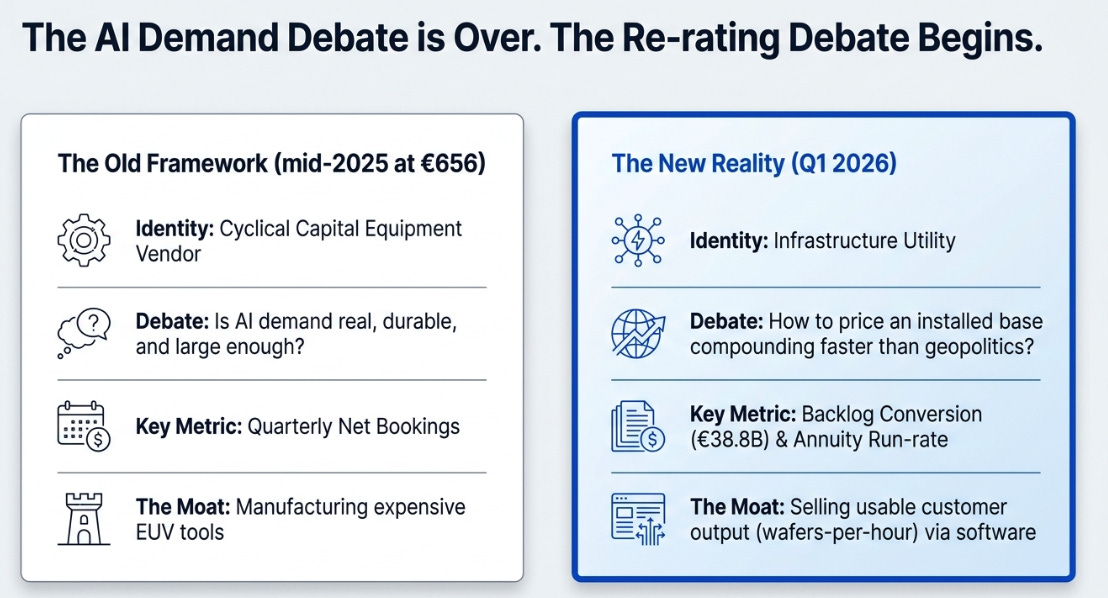

For most of the past eighteen months, the central debate around ASML was some version of: is AI demand real, durable, and large enough to justify the multiple? That was a reasonable question in mid-2025 when the stock was at €656 and the thesis required investors to look past a messy China transition and trust that the backlog was real. It is the wrong question now. Demand is not the hard part. The hard part is whether ASML has crossed a line, from selling tools into selling capacity, and whether the market has any idea what that crossing is worth.

That is what this quarter is about.

The Physics Was Always the Moat, But the Output Is Becoming the Business

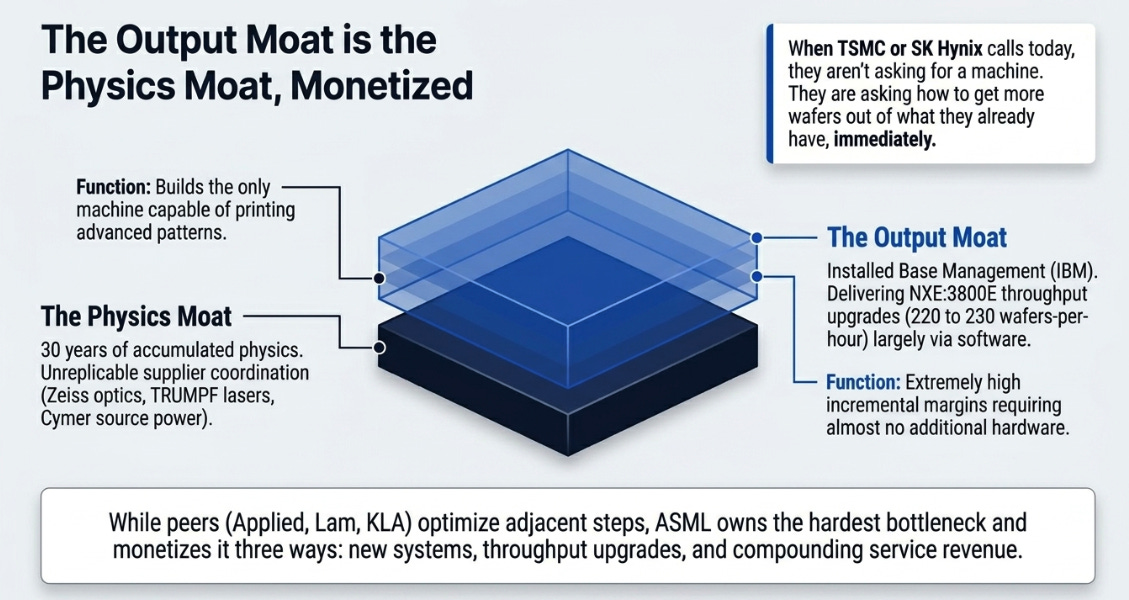

ASML’s competitive position has never been seriously in doubt. EUV is not a product advantage that can be replicated with capital and ambition. It is thirty years of accumulated physics, supplier coordination, and process integration, Zeiss optics, TRUMPF lasers, Cymer source power, and ASML’s own software and metrology, assembled into the only machine that can print the patterns advanced chips require. No competitor is close. That moat is intact and deepening.

But the moat was always the wrong frame for valuation. The right frame is what ASML is increasingly selling inside that moat, and the answer has been changing for six quarters in ways the market has been slow to price.

ASML’s core capability is not making expensive tools. It is converting leading-edge lithography physics into usable customer output. When a TSMC or an SK Hynix calls today, they are not asking whether ASML can sell them a machine. They are asking how to get more wafers out of what they already have, immediately. The NXE:3800E throughput upgrade, 220 to 230 wafers-per-hour, delivered largely via software, is ASML’s answer. It costs very little to deliver. CFO Roger Dassen confirmed on the Q1 call that these software-heavy upgrades carry extremely high incremental margins, often requiring no additional hardware. That is not capital equipment economics. That is infrastructure economics.

The distinction matters when you compare ASML to its equipment peers. Applied Materials, Lam Research, and KLA all matter enormously. They optimize adjacent steps in the process. But ASML owns the hardest bottleneck, the step where light becomes pattern and pattern becomes transistor, and it is monetizing that bottleneck three ways simultaneously: new system sales, throughput upgrades on systems already in the field, and compounding service revenue on a growing installed base. No competitor can upgrade an ASML tool. The output moat is the physics moat, monetized.

The Service Company That Stopped Hiding

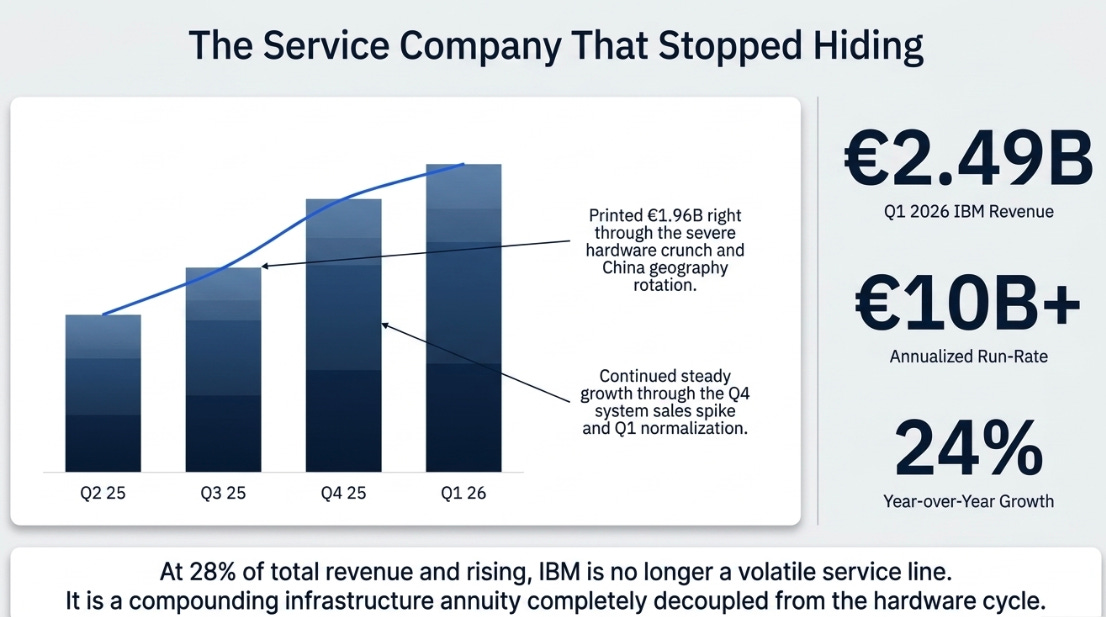

In October 2025, I called IBM the service company hidden in plain sight. By Q1 2026, it has stopped hiding.

The number that matters most in that table is not what IBM did in Q1. It is what IBM did in Q3 2025, the quarter where hardware pressures were most acute, system mix was weakest, and the stock fell sharply on fears the cycle was cracking. IBM printed €1.96 billion anyway. It grew through China geography rotation. It grew through EUV mix shifts. It grew through the Q4 system sales spike and the Q1 normalization that followed. That is not a volatile service line. That is an infrastructure annuity.

At €2.49 billion in Q1, a €10 billion annualized run rate growing 24% year-over-year, IBM is no longer a line item. It is a business. And to understand how badly ASML wants the market to look at that table, look at what they took away.

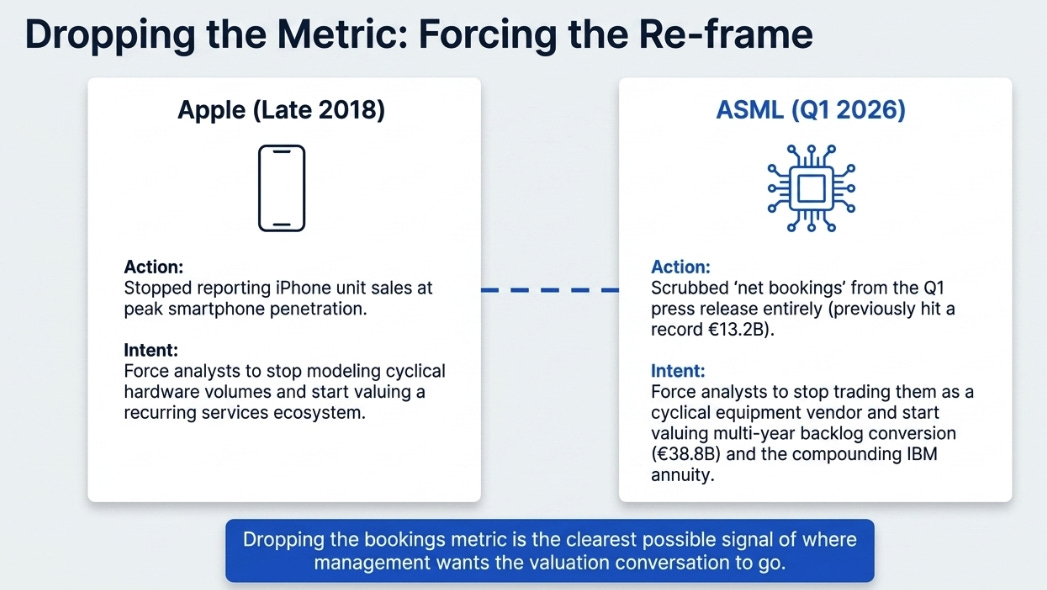

For years, the defining metric of any ASML earnings cycle was net bookings, the forward order intake that told investors whether the cycle was accelerating or peaking. Last quarter it hit a record €13.2 billion, nearly double consensus. This quarter, it has been scrubbed from the press release entirely. No table. No line item. A single sentence: “order intake continues to be very strong.”

This is Apple in late 2018, when the company stopped reporting iPhone unit sales at the exact moment peak smartphone penetration had been reached. Apple knew the unit cycle had plateaued and wanted analysts to stop modeling hardware volumes and start valuing a services ecosystem. ASML is executing the same reframe. They have €38.8 billion in backlog. They do not need quarterly bookings to prove demand exists. What they need is for the market to stop trading them as a cyclical equipment vendor and start valuing a company with multi-year backlog conversion and a compounding installed-base annuity. Dropping the metric is the clearest possible signal of where they want the conversation to go.

The re-rating thesis follows directly from the size. IBM is being valued at the same cyclical multiple as system sales. A €10 billion recurring revenue business growing 20%+ with extremely high incremental margins and zero competitive pressure deserves a different multiple than lumpy EUV shipments. The re-rating is structural rather than sentiment-driven, it happens when IBM becomes large enough that analysts are forced to model it separately. At 28% of revenue and rising, that threshold is close. The 2027 Capital Markets Day, where ASML will likely update its 2030 targets upward, is the most probable catalyst. But the re-rating arrives regardless of when, because the math eventually requires it.

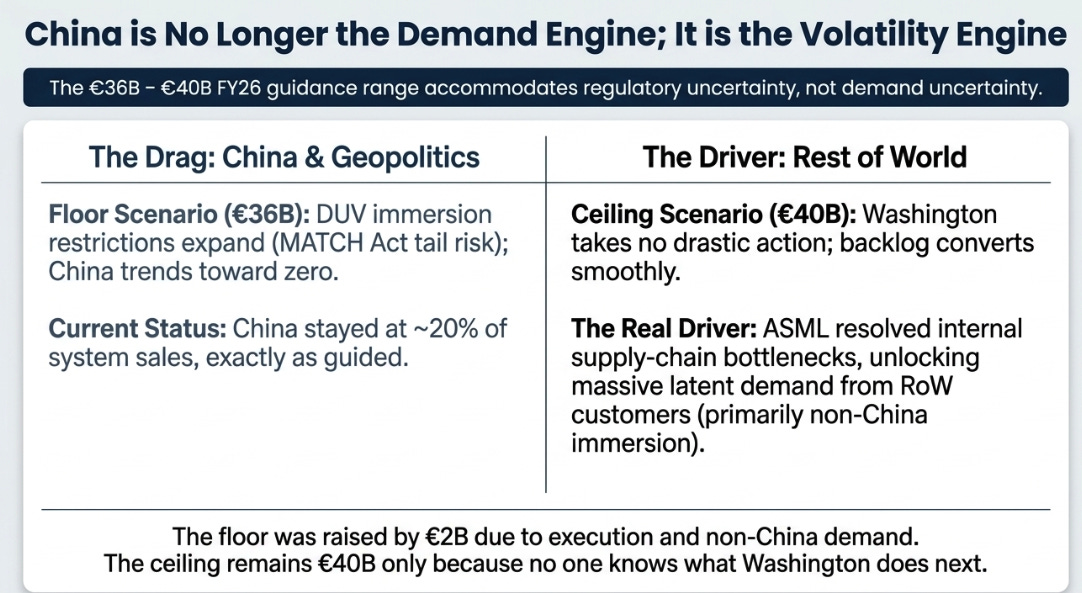

China Is No Longer the Demand Engine, It Is the Volatility Engine

The single most important sentence in the Q1 press release was not in the headline. It was in CEO Christophe Fouquet’s operational guidance paragraph: “We expect that the bandwidth in our 2026 guidance accommodates potential outcomes of ongoing discussions around export controls.”

That sentence has never appeared in an ASML press release before. It is not legal boilerplate, it is in the paragraph where Fouquet explains the revenue numbers, not in the forward-looking statements appendix. Management is telling investors, in the most direct language available, that the €4 billion guidance range is not demand uncertainty. It is China regulatory scenario uncertainty. Strip out the MATCH Act tail risk and ASML’s real 2026 guide is the upper half of the range. The floor of €36 billion, roughly flat with FY25, is the scenario where DUV immersion restrictions expand materially and China trends toward zero. The raise of the floor by €2 billion reflects growing confidence in non-China demand. The ceiling staying at €40 billion reflects the fact that nobody knows what Washington does next.

The Q1 transcript clarified the mechanism precisely. When Wells Fargo asked what drove the higher 2026 guide, Dassen said the uplift was “primarily non-China” immersion, ASML had solved a supply-chain constraint in its own manufacturing, unlocking demand from ROW customers that was already there. China stayed at approximately 20% of system sales, exactly as guided. The raise came from ASML fixing its own bottleneck, not from any improvement in the geopolitical environment. That is a more bullish read than “demand improved.” It means latent demand was waiting, and ASML unlocked it through execution.

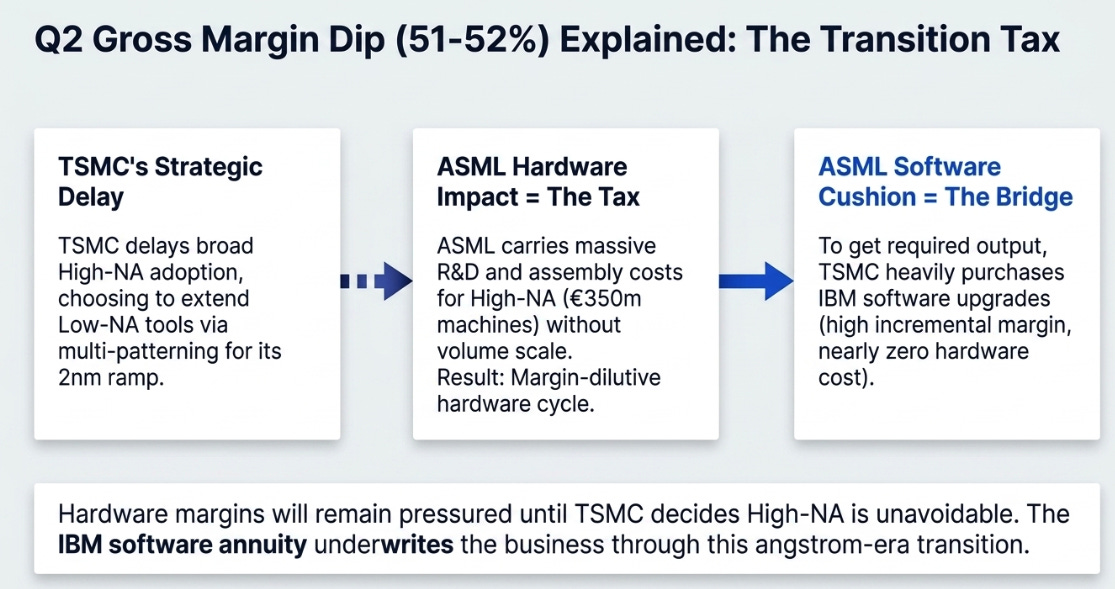

This transition is not without friction. If IBM is booming at extremely high margins, why did ASML guide Q2 gross margins down to 51-52%? The answer is that the hardware side of the business is currently absorbing a transition tax. High-NA EUV tools, €350 million machines required for angstrom-era chips, are margin-dilutive at current volumes. TSMC, ASML’s most important customer, is deliberately delaying broad High-NA adoption by extending its existing Low-NA tools through multi-patterning. TSMC is powerful enough to make that choice, and it is powerful enough to make ASML carry the R&D and assembly costs of the transition without granting the volume scale that would make it profitable. The hardware margin is compressing precisely because the most important customer in the world has decided not to move yet. That makes the IBM software floor not just an attractive business, it makes it an economic necessity during the transition.

That is the China and margin update together: the business is increasingly underwritten by South Korean HBM customers, TSMC’s 2nm ramp, and the IBM annuity compounding independently of geography. But the stock will continue to carry a policy discount as long as Washington can meaningfully widen the gap between backlog and recognized revenue, and the hardware margin will remain under pressure until TSMC decides High-NA is unavoidable.

The Debate That Actually Matters Is 2027

The quarter worth analyzing right now is not Q1 FY26. It is 2027, and Q1 is evidence about 2027, not an end in itself.

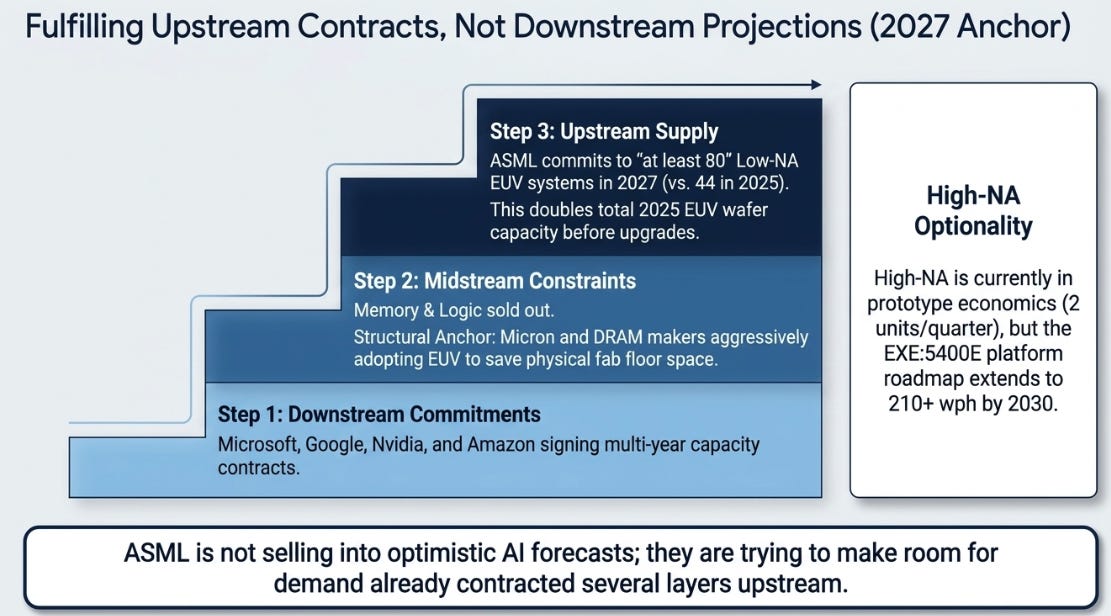

On the call, Fouquet committed to producing at least 80 Low-NA EUV systems in 2027, against 44 shipped in 2025. Dassen then pointed out that 80 systems at 230 wafers-per-hour represents more than double the total EUV wafer capacity ASML delivered in 2025, before counting installed-base upgrades. When asked whether 80 tools meets 2027 demand, Fouquet would not say yes. “At least 80” is a negotiation in progress. That is as close as management will come to telling you demand is still rising and they are still trying to make room.

The customer behavior confirms what the language suggests. Memory customers are sold out for the rest of the year and expect supply limitations to persist beyond 2026. Logic customers are expanding across multiple advanced nodes simultaneously. Both groups are responding not to optimistic forecasts but to committed purchase orders from their own downstream customers, Microsoft, Google, Nvidia, Amazon signing multi-year contracts that require the capacity. ASML is not selling into demand projections. It is fulfilling demand that is already contracted several layers upstream.

DRAM is driving more of this than the market has priced. Fouquet was explicit on the call that DRAM customers are adopting EUV not just for performance but for fab space efficiency, EUV reduces multi-patterning steps and frees floor space, which is a binding constraint when you are building fabs as fast as physically possible. Micron was named explicitly as making this shift for exactly this reason. Every major DRAM maker is now committed to accelerating EUV layer adoption. That is the memory thesis from the Q4 2025 analysis, DRAM flipped from cycle amplifier to structural anchor, playing out faster than modeled.

High-NA remains optionality. Approximately two units in each of Q4 2025 and Q1 2026 are prototype economics. But the roadmap shown at SPIE in February extends through the EXE:5400E platform at 210+ wafers-per-hour around 2030, and the EXE:5600 High Productivity platform beyond that. TSMC will eventually need it. The question for the second half of the year is whether any signal emerges on TSMC’s timeline, which would move the scenario probabilities materially.

What the Market Sees and What Is Actually There

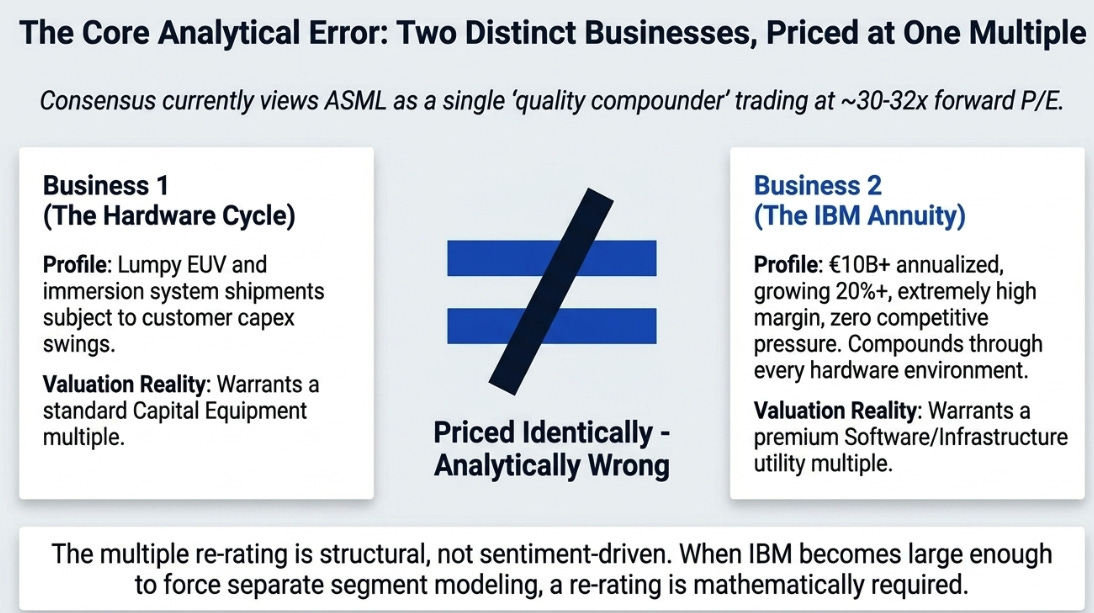

Consensus sees a quality compounder executing well on the AI trade, fairly valued at 30-32x forward earnings, with China as a managed headwind and the guidance raise as confirmation that execution is on track.

The better frame: two businesses, one multiple. The hardware cycle, EUV and immersion system sales, is priced at a capital equipment multiple. The IBM infrastructure annuity, €10 billion annualized, growing 20%+, extremely high incremental margins on software upgrades, zero competitive pressure by definition, is priced identically. That is analytically wrong. A monopoly infrastructure annuity that compounds through every hardware environment is not the same business as lumpy system shipments that swing with customer capex cycles.

The specific catalyst that forces the correction is the 2027 Capital Markets Day. If ASML introduces formal IBM segment disclosure or separate margin guidance, which the business now justifies by size, every sell-side model gets rebuilt on the same day. The stock moves on the model rebuild. That is a structural event, not a sentiment shift. It arrives because the math requires it.

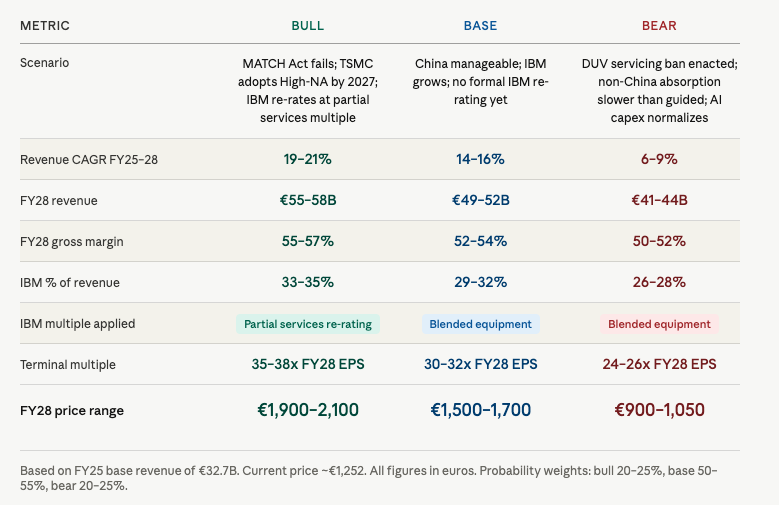

Three Years Out: What This Is Worth Under Different Futures

The critical distinction in the bull case is that the IBM re-rating does as much work as revenue growth. Most bull cases on ASML are simply higher revenue assumptions on the same multiple. The IBM multiple uplift is separate and additive, it happens when IBM segment reporting forces a model rebuild independent of what the hardware cycle is doing. In the bear case, IBM cushions the downside but cannot absorb a €5-6 billion China revenue shock plus lost servicing revenue simultaneously. In the base case, ASML earns its multiple through earnings growth, not a disaster, not a re-rating, a business that rewards patient ownership at current prices.

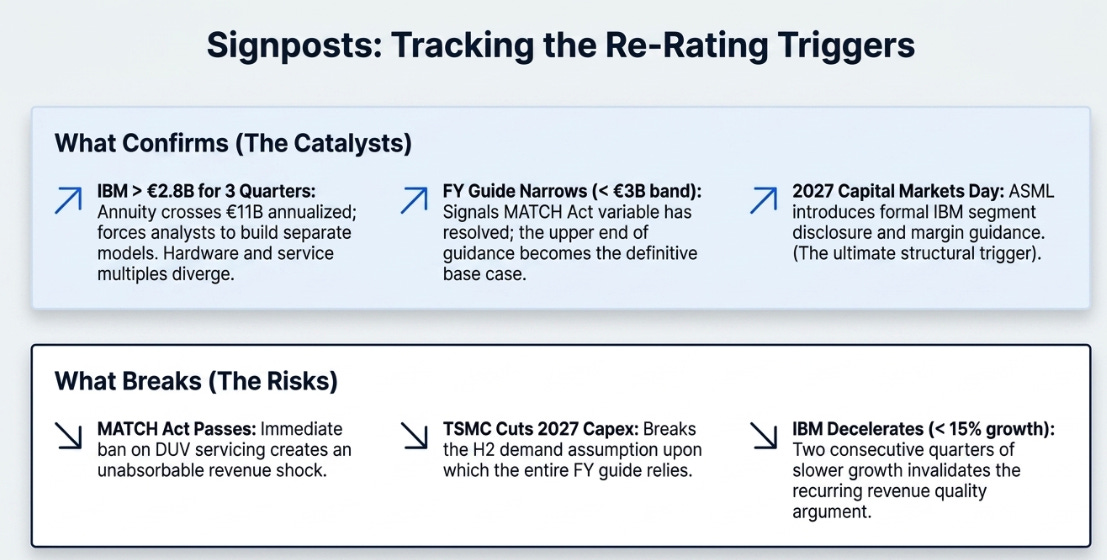

What Confirms This and What Breaks It

Three signals that actually move the thesis, not a checklist, but the specific thresholds worth tracking:

IBM above €2.8 billion for three consecutive quarters. At that level the annualized business exceeds €11 billion. Analysts build separate models. The multiple on IBM diverges from the multiple on hardware. The re-rating begins not because sentiment shifted but because the numbers demand a different framework.

FY guidance range narrows to €3 billion or less. That is management telling you the MATCH Act variable has resolved enough to commit to a tighter band. The floor and ceiling converging is the clearest available signal that geopolitical drag is easing and the upper end of the revenue range is becoming the base case.

2027 Capital Markets Day introduces IBM segment disclosure. This is the structural trigger. When ASML formally reports IBM with its own margin guidance, every model in the market gets rebuilt on the same day. That is a one-time re-rating event independent of whatever the hardware cycle is doing in that quarter.

What breaks it is equally specific. MATCH Act passes with a DUV servicing ban, that is a simultaneous revenue shock and IBM China loss that no near-term compounding absorbs. TSMC cuts 2027 capex materially, that breaks the H2 demand assumption the entire FY guide is built on. IBM decelerates below 15% growth for two consecutive quarters, that invalidates the recurring revenue quality argument that justifies the premium multiple on the whole business.

What We Thought, and What We Think Now

When this series began in July 2025 at €656, the argument was that the market was applying equipment-cycle multiples to a monopoly physics layer with a growing service annuity. IBM was the tell, a €6 billion recurring revenue stream at high margins, priced as a rounding error by analysts focused on quarterly system shipments.

That view was right. What has changed is the scale of the confirmation and the specificity of the remaining risk.

IBM is no longer a hidden flywheel. It is a €10 billion business large enough to require its own valuation treatment, growing through every hardware environment thrown at it. The demand debate ended. The transition trap never sprung. The non-China absorption is working. The DRAM structural anchor is real. And management has now made its strategic intent explicit by dropping the bookings metric, the old measure of cyclical hardware demand, and replacing it with qualitative language about a business they want valued on backlog conversion and recurring monetization.

What remains unresolved is one variable: whether geopolitics can interrupt the compounding before IBM, upgrades, and non-China demand make the old cyclical framework permanently obsolete.

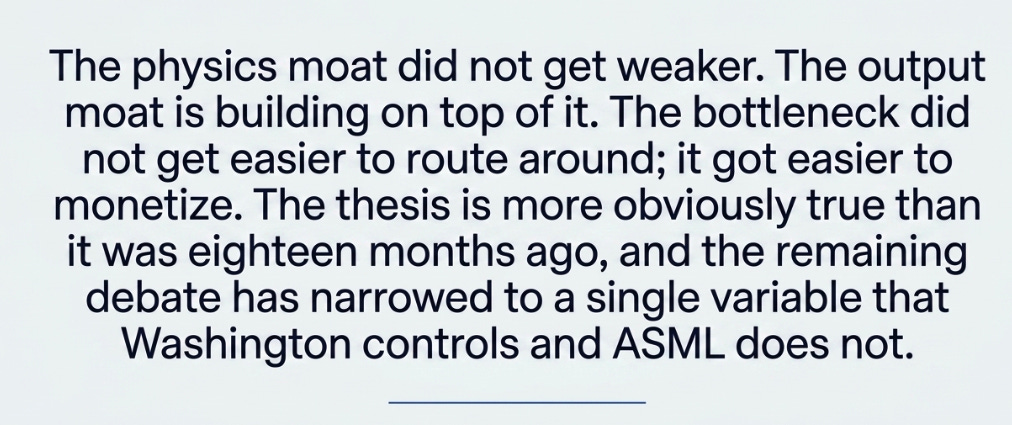

The physics moat did not get weaker. The output moat is building on top of it. The bottleneck did not get easier to route around, it got easier to monetize. That is the update. Not a change of view, but a sharpening of it: the thesis is more obviously true than it was eighteen months ago, the evidence is more concrete, and the remaining debate has narrowed to a single variable that Washington controls and ASML does not.

That is a better position than it sounds. The compounding is winning. The question for the second half of the year is by how much.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.