ASML 2Q26 Earnings: The Cycle That Builds the Next Cycle

More machines. More upgrades. A stronger moat..

TL; DR

AI is synchronising Logic and Memory investment. Advanced compute, HBM, networking, and chiplet architectures are increasing both the volume of patterned silicon and the lithography intensity required to produce it.

ASML now operates two production systems. Its factories deliver new machines, while its installed fleet creates immediate capacity through upgrades, service, and software, and generates knowledge that improves future systems.

The thesis now rests on cash and execution. Q2’s guidance and margin reset strengthen the structural case, but ASML must convert its historic ramp into cash, deliver planned capacity, and preserve access to its installed base in China.

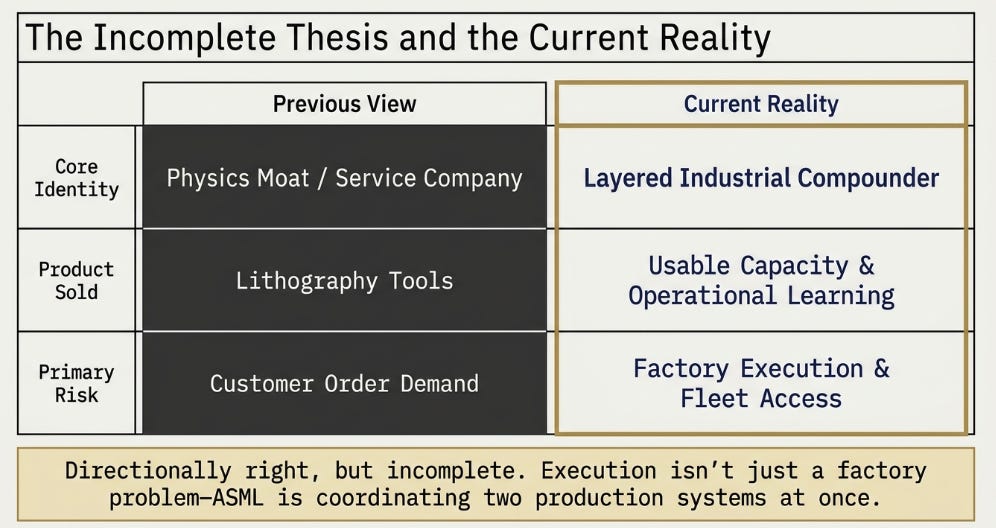

I want to begin with what we got wrong.

Over the past year, our ASML thesis moved from the physics moat to the service company inside the equipment company, to the end of the demand debate. After Q1, we concluded that ASML was no longer merely selling tools; it was selling usable capacity, and the principal risk had shifted from whether customers would order to whether ASML could deliver.

That progression was directionally right. It was also incomplete.

We treated execution mainly as a factory problem: how many systems ASML and its suppliers could build, and how quickly customers could install them. Q2 suggests that ASML is coordinating two production systems at once. The first produces new machines. The second is the fleet already operating inside customer fabs, where service, upgrades, and accumulated field knowledge can create additional capacity before the next machine arrives.

Our earlier work on the re-bundling of silicon explains why both systems are accelerating together. AI has pushed compute, memory bandwidth, power, cooling, and package size beyond the point where they can be optimized independently. The package is becoming the product. The upstream consequence is that Logic and Memory are no longer simply two semiconductor cycles that happen to be strong at the same time; they are different manufacturing requirements created by the same AI system.

The question underneath the quarter is therefore not whether ASML beat estimates. It is whether AI has changed ASML from a company that benefits when chipmakers add capacity into one whose value compounds because customers need more capacity, more lithography per wafer, and more productivity from every system already installed.

The Structural Mechanism

ASML becomes more valuable as semiconductor demand grows because each new generation requires both more patterned silicon and more difficult patterning, while every new system enlarges a proprietary installed base that can be serviced and upgraded for years. The mechanism strengthens because the number of tools, the economic value of each tool, and ASML’s operational knowledge can rise together. It breaks if AI commitments prove temporary, chiplets reduce leading-edge lithography faster than total system complexity increases it, or ASML builds capacity customers cannot absorb—and pay for.

Q2 is the strongest evidence yet that this mechanism exists. It also gives us the first serious test of whether it is real.

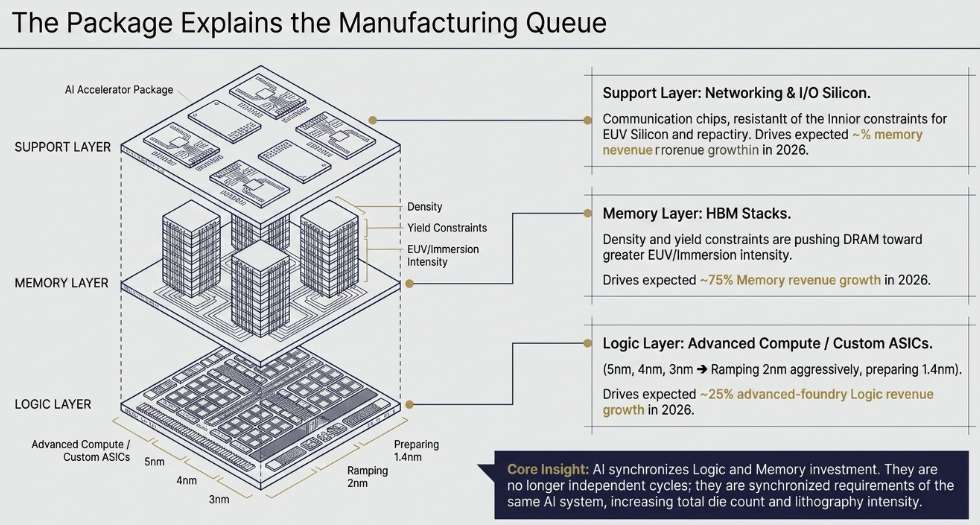

The Package Explains the Queue

“AI demand” is too vague to explain ASML’s results. The more useful observation is that an AI system requires advanced compute and advanced memory to scale together.

On the Logic side, customers are adding capacity at 5nm, 4nm, and 3nm, ramping 2nm as aggressively as possible, and beginning to prepare for 1.4nm. ASML expects advanced-foundry Logic revenue to increase about 25% in 2026. This is not a normal node transition. Accelerators, custom ASICs, CPUs, networking silicon, and supporting devices occupy different nodes, so AI broadens advanced-node demand rather than concentrating it in one process.

The second multiplier is lithography intensity. More advanced processes require tighter overlay, more process control, and generally more critical patterning. ASML therefore benefits from both more wafers and more lithography per wafer.

Memory is the more important change to the old ASML cycle. HBM makes density, power, and yield more important than in conventional commodity memory, pushing advanced DRAM toward greater EUV and immersion use. ASML’s H1 Memory system revenue increased more than 53%, while management expects approximately 75% Memory revenue growth for 2026. Logic system revenue was still down in H1, so the promised Logic acceleration sits largely in the second-half guide rather than reported history.

The re-bundling thesis explains why these demands are connected. An accelerator package increasingly combines leading-edge compute, multiple HBM stacks, logic-rich memory base dies, networking and I/O silicon, and more process-control complexity. ASML sits upstream of all of them. The result is not simply one larger GPU die; it is more patterned silicon across several technologies and node generations.

There is a legitimate counterargument. Chiplets can keep some functions on older nodes and substitute packaging complexity for monolithic scaling. The ASML thesis depends on total die count, advanced-memory content, and manufacturing complexity increasing faster than chiplets reduce leading-edge area.

For now, complementarity is winning. ASML expects EUV, DUV, metrology, Logic, Memory, and installed-base revenue to grow together. The package is not replacing front-end lithography; it is creating more types of silicon that must be patterned, aligned, measured, and made productive.

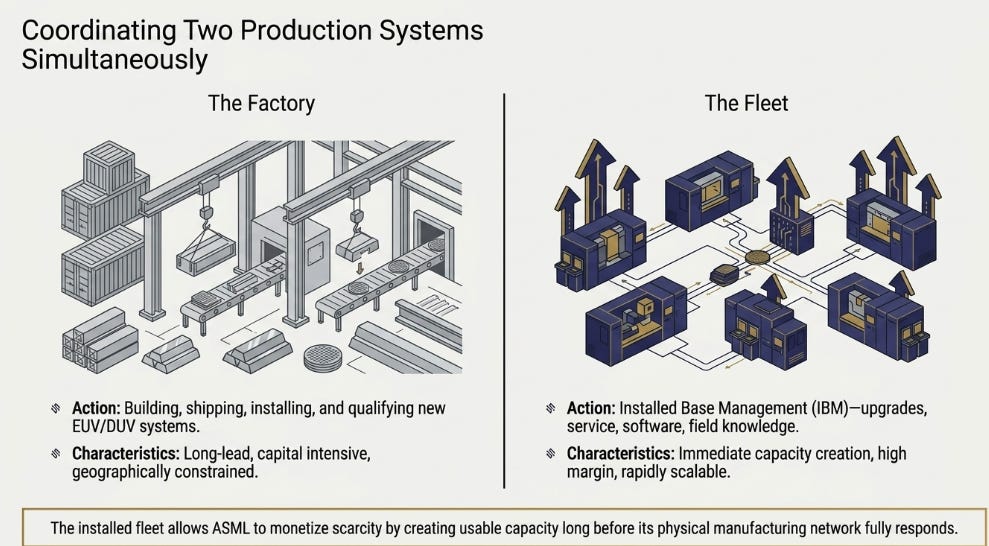

Two Production Systems

ASML’s first production system is its factories, critical suppliers, and field teams that produce and install new lithography tools.

Its second is every ASML machine already operating inside a customer fab.

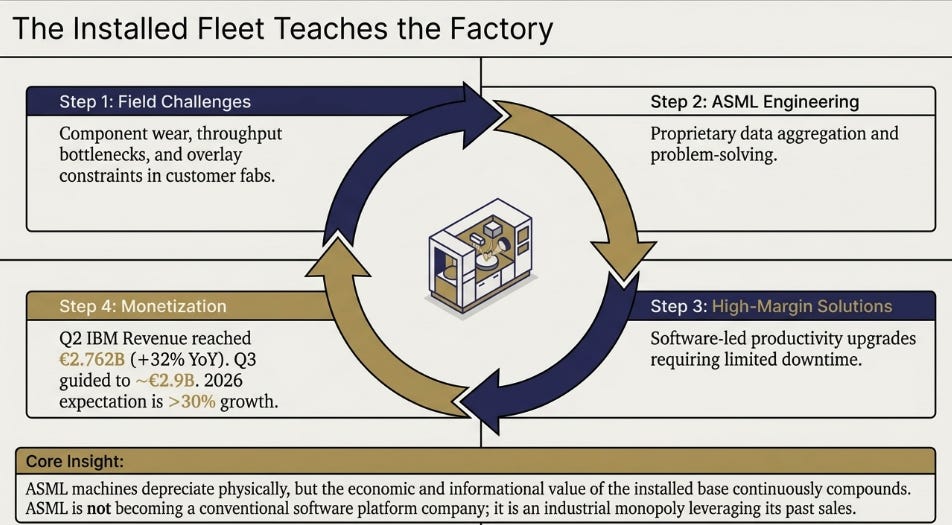

Installed Base Management revenue reached €2.762 billion in Q2, up nearly 32% year over year and roughly €300 million above ASML’s own expectation. Management attributed the upside to productivity enhancements, including software-led upgrades that can raise output with limited downtime. Q3 IBM revenue is expected to be about €2.9 billion, and management expects more than 30% growth in 2026.

A new EUV system is extraordinarily difficult to build, ship, install, and qualify. An upgrade can create usable capacity much sooner. The installed fleet therefore lets ASML monetize scarcity before its physical manufacturing network has fully responded.

The fleet also teaches the factory. Each machine exposes ASML to component wear, availability constraints, overlay challenges, throughput bottlenecks, and customer-specific process problems. The solutions can return as better service, software, hardware options, and next-generation systems. This is an inference rather than a disclosed KPI, but it is the industrial equivalent of a learning loop.

IBM is not pure software. It includes engineers, parts, hardware, and field work, and some upgrade demand will normalize when fabs are less constrained. ASML is not becoming a conventional platform company.

The more accurate conclusion is that ASML is an industrial monopoly whose previous equipment sales enlarge both its future revenue opportunity and its capacity to improve. The machines depreciate physically; the economic and informational value of the installed base to ASML can still increase.

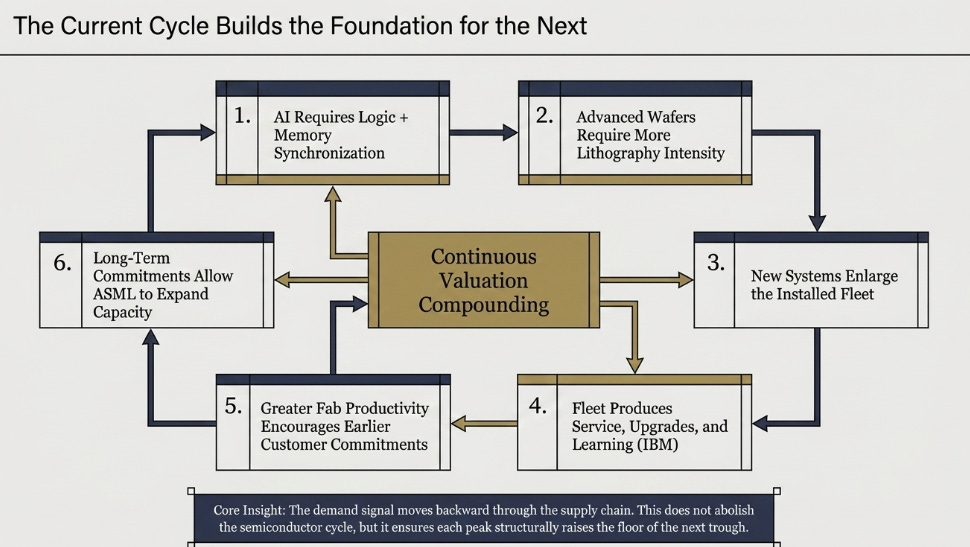

The Cycle That Builds the Next Cycle

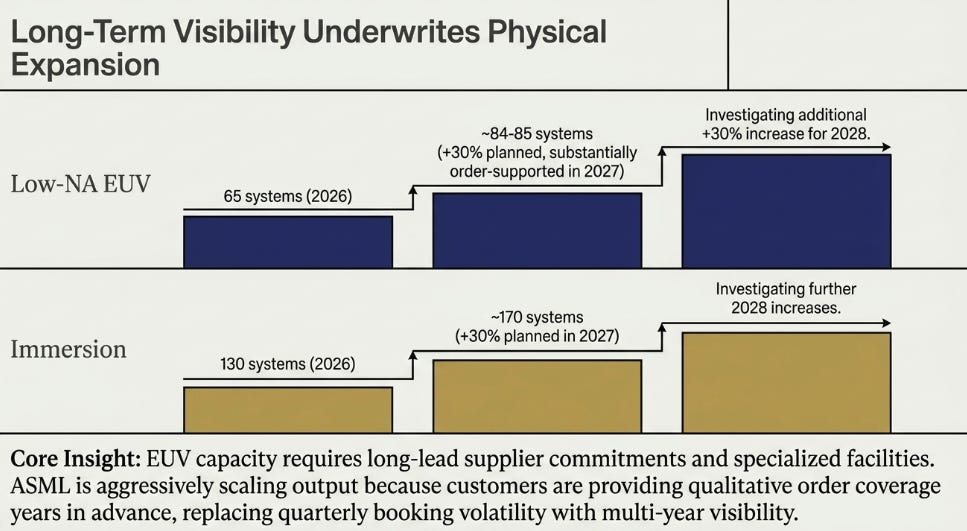

ASML expects to ship about 65 Low-NA EUV systems in 2026. It plans roughly 30% more capacity in 2027, implying around 84–85 systems, and says it is close to receiving all the orders required for that expansion. It has already received a large number of 2028 orders and is investigating another 30% increase.

Immersion follows a similar path: about 130 systems in 2026, roughly 30% more capacity planned for 2027, and another possible increase in 2028.

The 2027 expansion is planned and substantially order-supported; the 2028 increase is still being investigated. Even so, EUV capacity requires long-lead commitments from suppliers, specialized facilities, trained employees, and installation resources. ASML must believe demand will exist when those investments become productive.

Management says its customers have greater confidence because they are receiving longer-term commitments from their own customers. The demand signal is moving backward through the supply chain: AI customers commit to compute, chip designers commit to wafers, manufacturers commit to capacity, and those manufacturers commit to ASML.

The loop is now visible:

More AI systems require more Logic and Memory. More advanced wafers require more lithography. More systems enlarge the installed fleet. The fleet produces service, upgrades, and learning. Greater productivity encourages earlier customer commitments. Those commitments allow ASML to expand capacity again.

This does not abolish the semiconductor cycle. It means the cycle can build the foundation of the next cycle.

ASML no longer reports quarterly bookings because management considered the metric too volatile. Investors are now being asked to replace a hard but noisy number with capacity plans and qualitative order coverage. That may better reflect a multi-year business, but it reduces transparency around concentration, deposits, cancellation rights, and mix. Management credibility is now part of the valuation framework.

What Q2 Changed

The reported numbers are evidence, not the thesis.

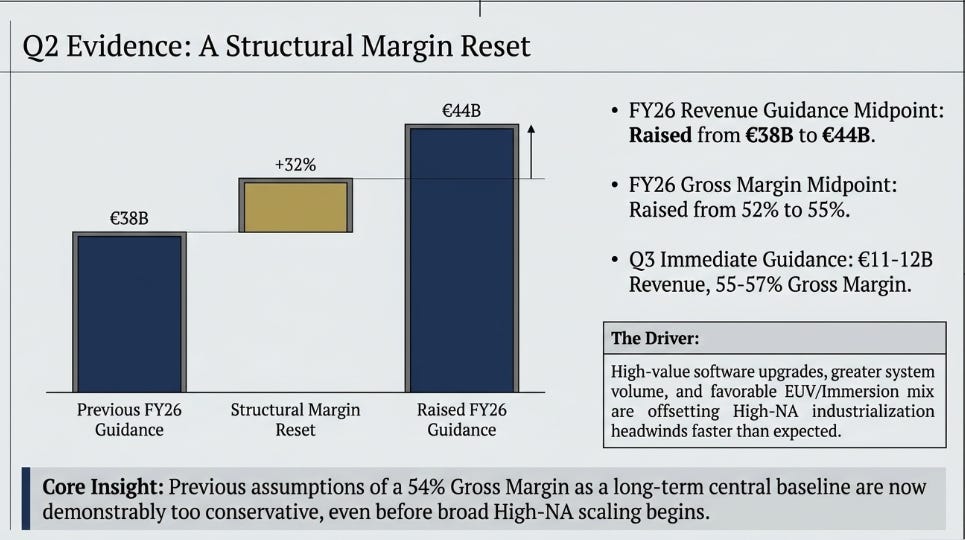

Q2 revenue reached €9.326 billion, IBM reached €2.762 billion, gross margin was 54%, and operating income increased nearly 30% year over year. More consequentially, ASML raised the midpoint of FY2026 revenue guidance from €38 billion to €44 billion and the gross-margin midpoint from 52% to 55%. Q3 is guided to €11–12 billion of revenue and 55–57% gross margin. The €6 billion increase in the annual midpoint reflects a broader change in customer plans and ASML’s ability to respond.

It also forces us to update our margin view. In October 2025, we argued that a realistic 2030 gross margin might be about 54%, rather than the upper-50s outcome embedded in management’s framework. ASML is now guiding to 54–56% in 2026, before broad High-NA scale.

We were wrong about the timing and strength of the margin inflection. We underestimated how quickly high-value upgrades, greater system volume, and favorable EUV and immersion mix could offset High-NA industrialization and geographic headwinds. That does not prove 60% through-cycle margins; it makes 54% look too conservative as a central long-term assumption.

High-NA reached an important milestone with Intel using the technology on selected production layers. That reduces technical risk but does not explain the 2026 raise.

High-NA is the duration of the thesis, not the explanation for the quarter.

The Cash Test

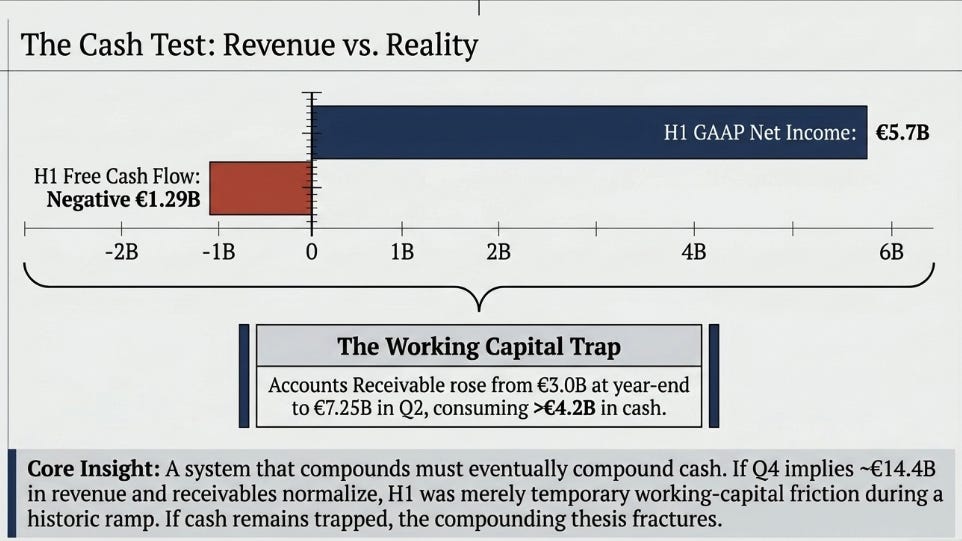

The strongest evidence against the thesis is cash.

ASML generated €5.7 billion of US GAAP net income in H1, but operating cash flow was negative €483 million and free cash flow was approximately negative €1.29 billion. Accounts receivable rose from €3.0 billion at year-end to €7.25 billion at Q2, consuming more than €4.2 billion of cash.

Shipment timing, acceptance, invoicing, and the absence of receivables factoring can explain much of the volatility. They do not make it irrelevant.

A system that compounds should eventually compound cash.

The full-year midpoint implies approximately €14.4 billion of Q4 revenue after H1 and the Q3 midpoint. If receivables normalize and operating cash surges, H1 will look like temporary working-capital pressure during a historic ramp. If revenue accelerates while cash remains trapped, the compounding thesis has a problem stronger guidance cannot solve.

China is the second unresolved issue. Management still expects approximately 20% of 2026 revenue from China on a much larger company base. Restrictions that impair service or upgrades would weaken the installed-base mechanism itself.

What We Think Now

The consensus view is that ASML is the world’s best semiconductor-equipment company, benefiting from an exceptional AI capital-spending cycle and deserving a premium multiple.

That view is not wrong. It is incomplete.

Our prior thesis was that demand risk had become execution risk and that ASML was moving from selling tools to selling usable capacity. The updated view is that execution includes both manufacturing new capacity and extracting immediate capacity—and operational learning—from the installed fleet.

The variant perception is not that ASML has become software or that cyclicality has disappeared. It is that ASML is becoming a layered industrial compounder whose equipment cycle creates its next recurring-revenue and learning cycle.

The most visible catalyst is the Capital Markets Day on June 10, 2027. ASML’s existing 2030 framework of €44–60 billion in revenue is increasingly stale now that it guides to €43–45 billion in 2026. The event is the natural venue for a long-term capacity, IBM, and margin reset.

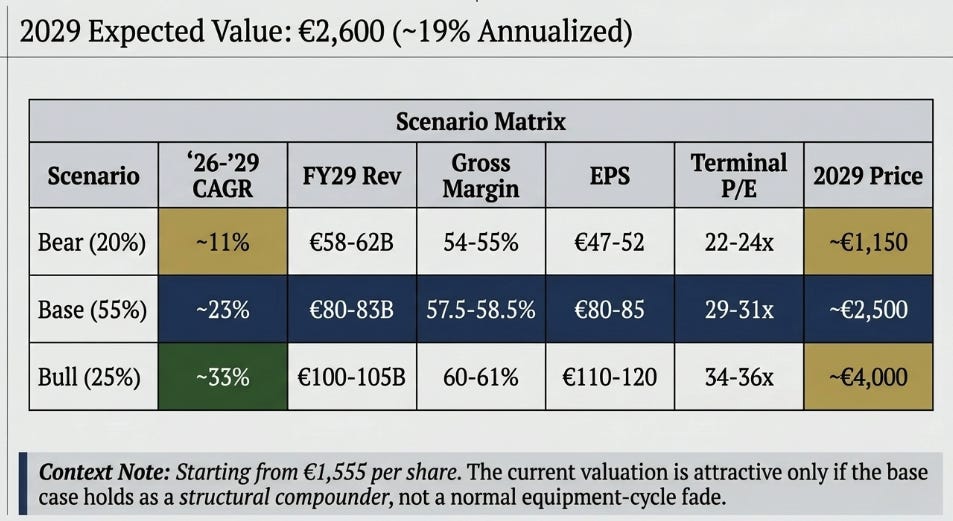

Three Years From Now

The numbers are outputs of the thesis. Starting from €1,555 per share:

Scenario assumptions and probabilities are our estimates, not company guidance.

The bear case requires a genuine break: customer pushouts, a deferred 2028 expansion, weaker HBM investment, material restrictions on servicing China, or persistent cash-conversion problems.

The base case assumes most 2027 capacity is delivered and utilized, a meaningful 2028 expansion proceeds, IBM grows in the mid-to-high teens after the exceptional 2026 step-up, and margins rise through volume and mix. The bull case requires sustained Logic and Memory constraints, both capacity steps, continued IBM monetization, and broader High-NA adoption.

The probabilities produce an indicative expected value of about €2,600, roughly 19% annualized over three years before dividends. The precision matters less than the distribution: the current valuation is attractive only if the base case is structurally different from a normal equipment-cycle fade.

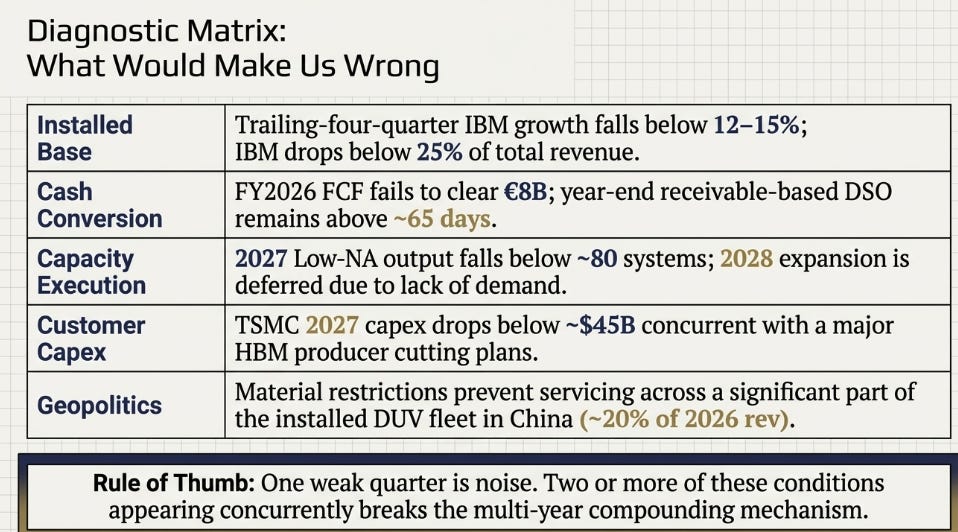

What Would Make Us Wrong

One weak quarter would not disprove a multi-year mechanism. Two or more of these conditions appearing together would.

The Bottleneck Was the Beginning

Our original ASML thesis began with the physics moat. Then the installed base became visible. Then the orders arrived, and the question shifted from demand to delivery.

Q2 connects those observations.

The re-bundling of silicon explains why Logic and Memory are entering the queue together. The installed fleet explains why each new machine creates both future revenue and future learning. Long-term customer commitments explain why ASML can expand production without simply speculating on the next cycle.

ASML sells new capacity through its factories, immediate capacity through its installed fleet, and better future capacity through what both systems teach it.

That does not make ASML immune to the cycle.

It means the cycle can build the next one.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.