Baidu’s 1Q26 Earnings: The Second Threshold

AI has replaced the story of search. Now it has to replace the economics.

TL;DR

Baidu has crossed the first threshold: AI is no longer a side story. Core AI-powered revenue is now the majority of Baidu General Business, confirming our prior view that Baidu is not defending search so much as rebuilding itself around AI.

The market may be using the wrong scoreboard: Baidu is not the largest Chinese cloud player: Alibaba has scale, Tencent has economics, Huawei has infrastructure, but Baidu may be much more relevant in the narrower AI-native compute layer where its full-stack approach matters.

The second threshold is economics: AI Cloud proves demand, but applications, margins, and free cash flow will decide the multiple. The bull case requires Baidu to turn infrastructure growth into application-layer lock-in, not merely replace high-margin search ads with lower-margin compute revenue.

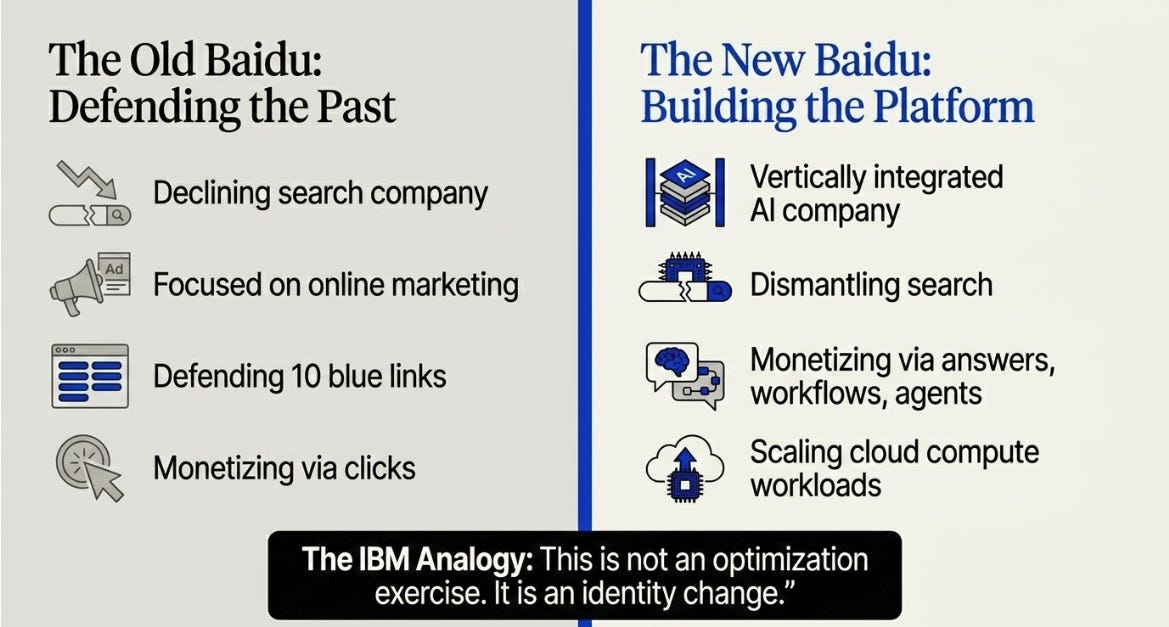

When we wrote “Baidu: The Elephant’s Dance,” the central argument was not that Baidu’s next quarter would be good. It was that the market was using the wrong mental model. Investors were judging Baidu as a declining search company; we argued that Baidu was doing something more deliberate and more dangerous: using search, distribution, data, and cash flow to build a vertically integrated AI company. The IBM analogy mattered because IBM’s transformation under Lou Gerstner was not an optimization exercise. It was an identity change. Baidu, we argued, was attempting the same: not defending search, but dismantling it to build something else.

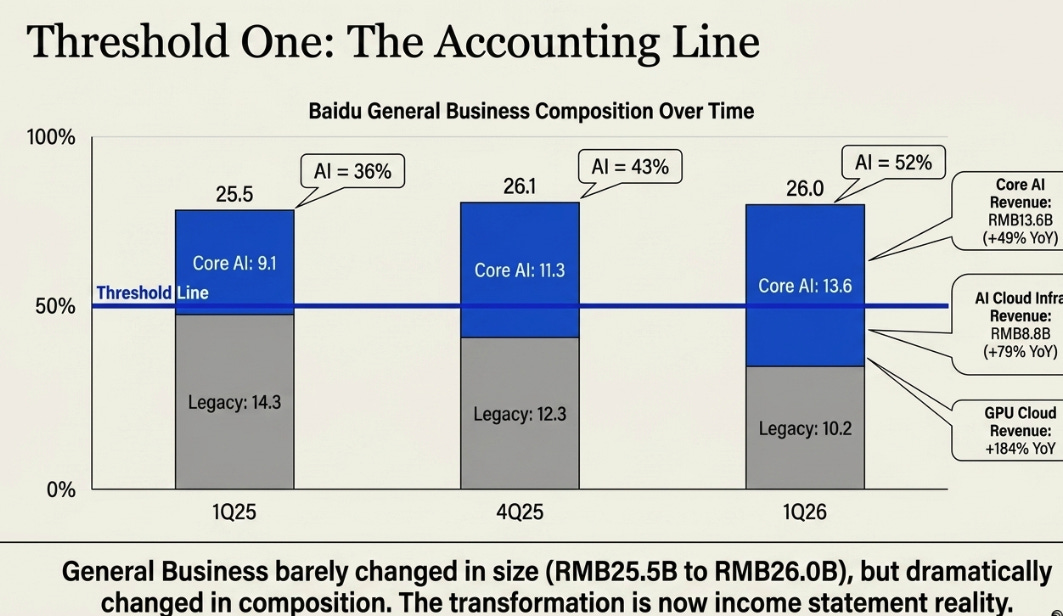

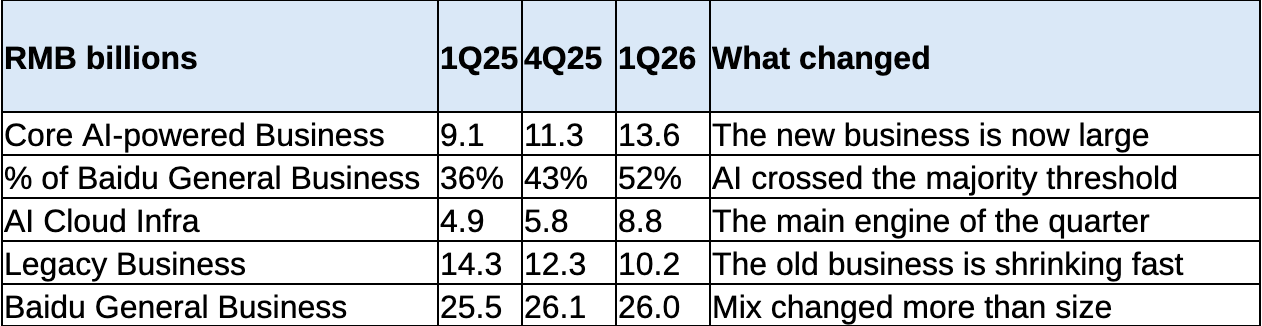

1Q26 is the first quarter where that argument no longer lives only in metaphor. The elephant is not merely dancing in management commentary; it has crossed an accounting line. Baidu’s Core AI-powered Business reached RMB13.6 billion, up 49% year-over-year, and for the first time exceeded half of Baidu General Business revenue. AI Cloud Infra revenue rose 79% year-over-year to RMB8.8 billion, while GPU Cloud revenue grew 184%.

That is not a normal quarterly datapoint. It is the moment when a transformation moves from “management story” to “income statement reality.” But it also makes the debate harder, not easier. Before this quarter, the market could ask whether Baidu’s AI business was real. After this quarter, that question is less interesting. The better question is whether the AI business Baidu is building is economically superior to the search business it is replacing.

That is the second threshold.

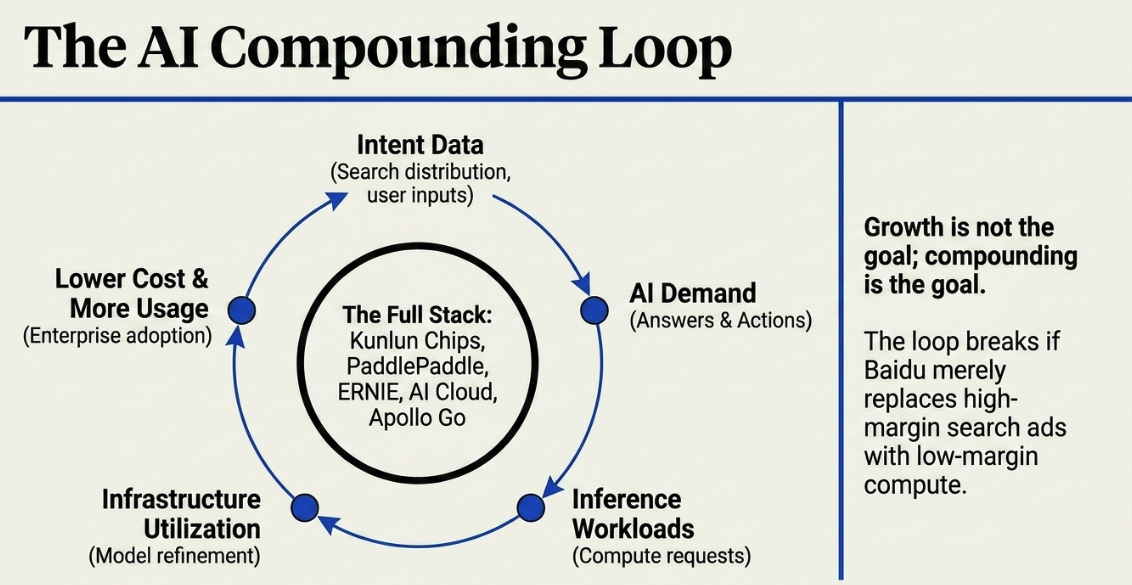

The question is not growth. It is compounding.

The structural mechanism that could make Baidu more valuable is not simply “AI revenue growth.” The mechanism is a loop: intent data creates demand for AI answers and actions; those answers and actions create inference and cloud workloads; those workloads improve infrastructure utilization and model/application performance; lower cost and better performance attract more enterprise and consumer usage; and that usage produces more intent and workload data.

This loop strengthens at scale if Baidu’s stack — Kunlun chips, PaddlePaddle, ERNIE, AI Cloud, search distribution, agents, Wenku, Drive, and Apollo — makes each incremental AI interaction cheaper, faster, and more useful. It breaks if Baidu is merely replacing high-margin search ads with lower-margin compute revenue.

This distinction matters because there are two very different ways to read 1Q26. The first is simple: AI revenue is now big. The second is more important: Baidu may be trying to turn intent into infrastructure, and infrastructure into applications. The former is a revenue story. The latter is a platform story.

The metric is the message.

The most revealing part of Baidu’s release is not the headline revenue beat. It is the metric Baidu wants investors to focus on: Core AI-powered Business. Companies do not introduce new metrics by accident. They do it when old metrics no longer capture the story they want the market to understand — or when old metrics reveal too much pain.

That makes Baidu’s new frame both self-serving and useful. The old Baidu was online marketing plus iQIYI plus optionality. The new Baidu wants to be AI Cloud Infra, AI Applications, AI-native Marketing, and Apollo Go, with legacy search slowly receding into the background.

Source: Baidu 1Q26 results.

This is the quarter’s essential message: Baidu General Business barely changed in size, but it changed dramatically in composition. The company did not beat because the old business recovered. It beat because the new business became large enough to cover more of the old business’s decline.

Crossing 50% does not prove Baidu is an AI winner. It proves Baidu can no longer be analyzed as merely a declining search company.

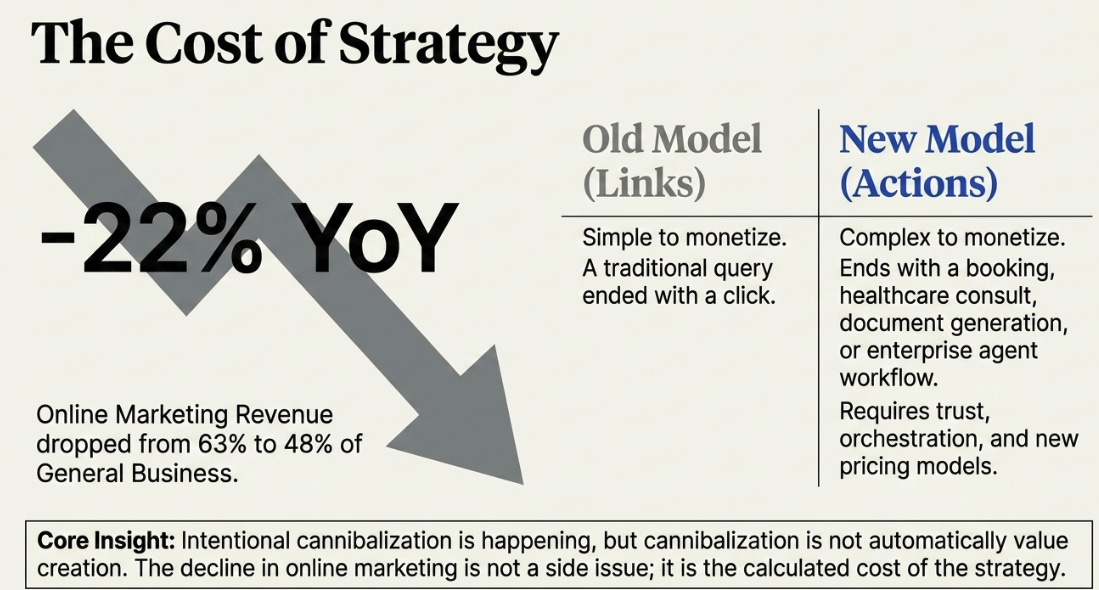

The search business is not being saved.

The prior article argued that Baidu was not trying to preserve search in its old form. 1Q26 supports that view, but it also forces a more disciplined update: intentional cannibalization is not automatically value creation.

Online marketing revenue fell 22% year-over-year in 1Q26 and dropped to 48% of Baidu General Business revenue, down from 63% a year earlier. That decline should not be treated as an unfortunate side issue. It is the cost of the strategy.

The old Baidu monetized intent through links. The new Baidu wants to monetize intent through answers, agents, workflows, cloud workloads, and eventually transactions. A traditional search query ended with a click. An AI search interaction may end with a completed booking, a healthcare consultation, a shopping decision, a document generated in Wenku, a file workflow in Drive, or a business process executed by an enterprise agent.

That is a better strategic ambition than defending ten blue links. But it is also a harder business model to prove. Clicks were simple to monetize. Actions are more valuable, but also more complex: they require trust, orchestration, partner integrations, attribution, and new pricing models.

So yes, the first part of the thesis is working: Baidu is dismantling the old search model. The unresolved question is whether the replacement model captures more value than the one being dismantled.

The wrong scoreboard.

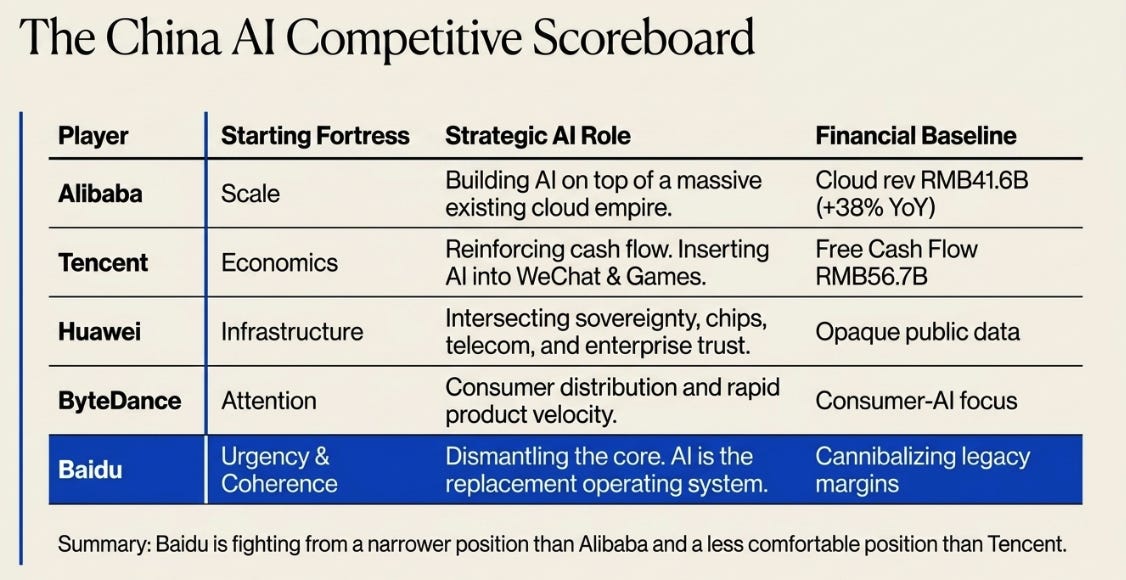

The biggest missing piece in a simple Baidu earnings analysis is the competitive scoreboard. Baidu is not transforming in a vacuum. It is fighting Alibaba, Tencent, Huawei, ByteDance, and others for position in China’s AI stack. The mistake is to treat that as one race.

On the broad cloud scoreboard, Baidu is not the winner. Alibaba has the scale. Its Cloud Intelligence Group generated RMB41.6 billion of revenue in the March quarter, up 38% year-over-year; external cloud revenue rose 40%, and Cloud Intelligence adjusted EBITA rose 57% to RMB3.8 billion. Alibaba is building AI on top of an existing cloud empire. That is a formidable starting point. (Morningstar, Inc.)

Tencent starts from a different fortress. It does not need AI to become a different company; it can insert AI into WeChat, games, advertising, fintech, productivity tools, content, and cloud. Tencent’s 1Q26 revenue was RMB196.5 billion, gross margin was 56.6%, non-IFRS operating profit was RMB75.6 billion, and free cash flow was RMB56.7 billion, even as capex reached RMB31.9 billion. More revealingly, Tencent disclosed non-IFRS operating profit excluding new AI products of RMB84.4 billion, which effectively shows a very profitable core business funding the AI build-out. (Tencent)

Huawei is harder to underwrite because the public numbers are opaque, but strategically it matters because it sits where sovereignty, chips, devices, telecom infrastructure, government relationships, and enterprise trust intersect. ByteDance has the consumer distribution, recommendation engine, and product velocity, but its advantage is more naturally consumer-AI than enterprise infrastructure.

Baidu’s position is narrower than Alibaba’s and less comfortable than Tencent’s. It is not the biggest hyperscaler. It does not have Tencent’s cash-flow fortress. What Baidu has is urgency and coherence: AI is not a feature being added to the business; AI is becoming the replacement operating system for the business.

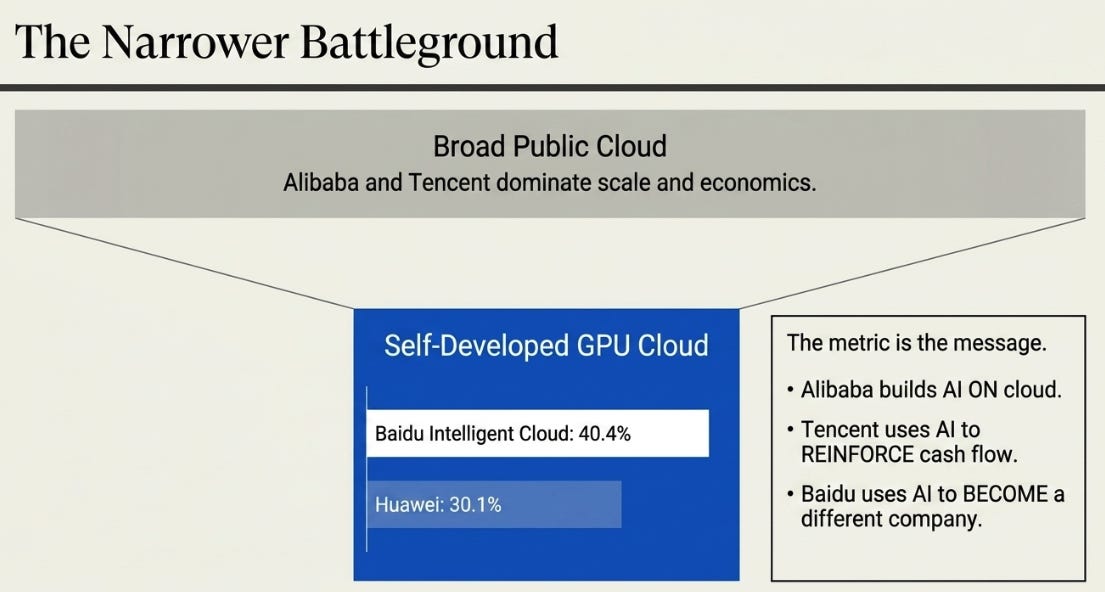

The more interesting scoreboard is therefore not broad cloud. It is AI-native compute. Third-party summaries of Frost & Sullivan’s self-developed GPU cloud market report put Baidu Intelligent Cloud first with 40.4% share, ahead of Huawei at 30.1%. This is a narrower market than overall cloud, and the definition matters: self-developed GPU cloud is not the same thing as all public cloud. But that is precisely the point. Baidu looks small on the old scoreboard and much more relevant on the AI-specific one. (C114Pro)

That distinction reframes the quarter. Alibaba is building AI on top of cloud. Tencent is using AI to reinforce a cash-flow machine. Baidu is using AI to become a different company.

Compute is proof. Applications are control.

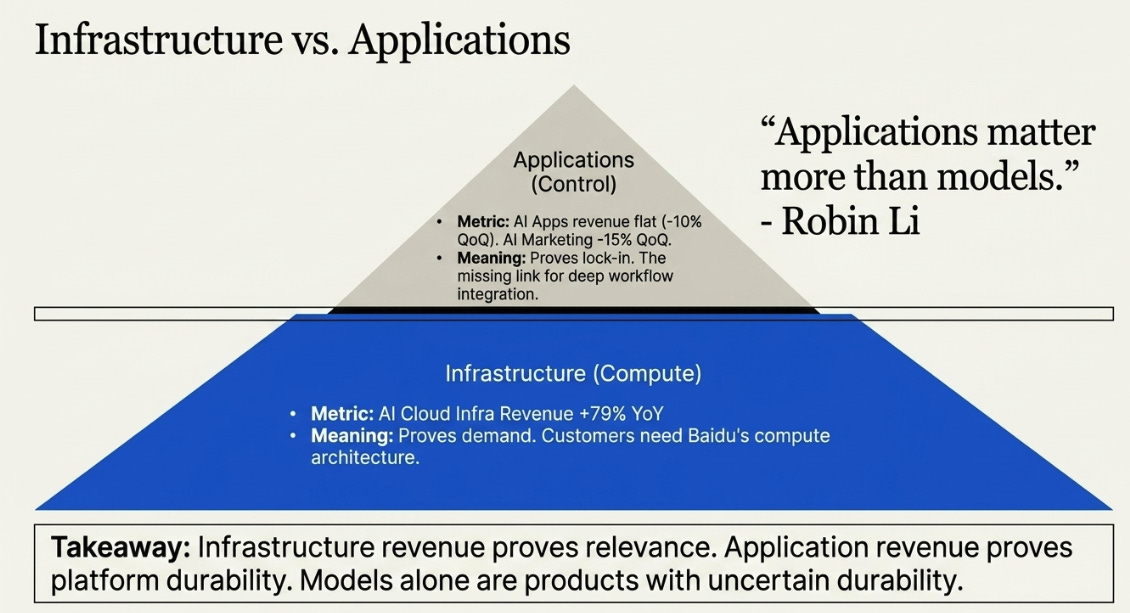

AI Cloud Infra is where Baidu’s full-stack thesis first shows up. Management has been explicit about this. On the 4Q25 call, Baidu described AI accelerator infrastructure as the primary growth driver of AI Cloud, emphasized its full-stack end-to-end architecture, and pointed to heterogeneous computing, unified scheduling, and Kunlun chips as sources of performance and cost efficiency. Robin Li also made the more important strategic point: “applications matter more than models.”

This is the correct answer to the model race. In a world of DeepSeek, Qwen, Doubao, Kimi, and open-source releases, simply having a model is not enough. Models alone are products with uncertain durability. The value is in deployment: how cheaply inference can be served, how reliably enterprise workloads can run, how quickly applications can be built, and how deeply those applications become embedded in customer workflows.

Baidu’s 1Q26 AI Cloud Infra number is therefore significant. It suggests customers are buying the infrastructure. But infrastructure is only the first proof. The final form is applications.

The distinction is crucial. Infrastructure revenue proves customers need Baidu’s compute. Application revenue proves customers are locked into Baidu’s platform.

That is where Baidu has more to prove. AI Applications revenue was RMB2.5 billion, approximately flat year-over-year and down 10% quarter-over-quarter. AI-native Marketing Services grew 36% year-over-year, but fell 15% sequentially. These are not fatal numbers, but they are the missing link in the bull case.

AI Cloud can make Baidu relevant again. AI applications are what can make Baidu valuable again.

The bill comes due.

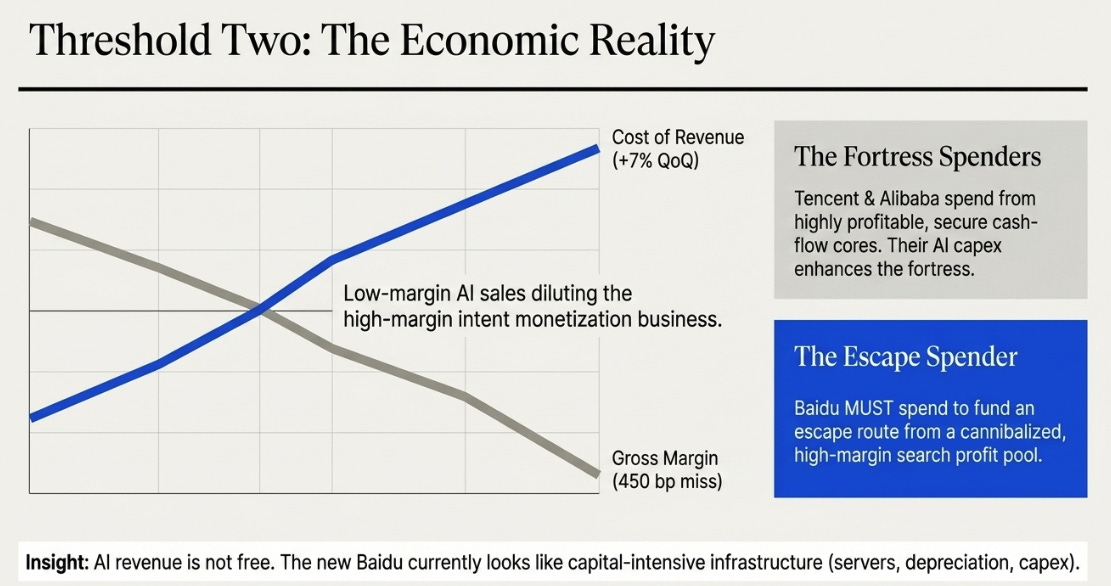

The uncomfortable part of the quarter is that AI revenue is not free. The old Baidu was a high-margin intent monetization business. The new Baidu, at least in its current phase, looks more like infrastructure: servers, chips, depreciation, bandwidth, financing, and capex.

Baidu’s cost of revenue rose 7% quarter-over-quarter, primarily due to costs related to AI Cloud. Operating income recovered sequentially, and operating cash flow was positive at RMB2.7 billion, but the quality debate remains open. Bloomberg Intelligence’s post-result comment was blunt: better-than-expected earnings “masked” a 450 bp gross-margin miss, illustrating the dilutive impact of low-margin AI sales.

This does not invalidate the thesis. It clarifies it.

The absolute capex number matters less than the burden it carries. For Tencent, AI capex enhances the fortress. For Alibaba, it defends cloud scale. For Baidu, it funds the escape route from search. That makes the same kind of spending feel different. Tencent can spend into AI while the core throws off enormous free cash flow. Alibaba can spend because cloud scale is already a strategic pillar. Baidu has to spend because the old profit pool is being cannibalized.

That is the second threshold in financial form. The first debate was whether AI could become material. The second is whether material AI revenue can become high-return AI revenue.

What changed in our view.

1Q26 makes us more confident that the prior strategic diagnosis was right. Baidu is not pretending to be an AI company. The revenue mix has genuinely changed, and AI Cloud Infra is growing fast enough to matter. The market’s old question — “can AI offset search revenue?” — is increasingly stale.

But the quarter also makes us less willing to jump straight to the bull case. The prior article leaned into the elegance of the full-stack thesis: intent, model, framework, chip, infrastructure, application. That architecture still matters. It may matter more after 1Q26. But full-stack integration only creates value if it shows up in margins, cash flow, and application-layer monetization.

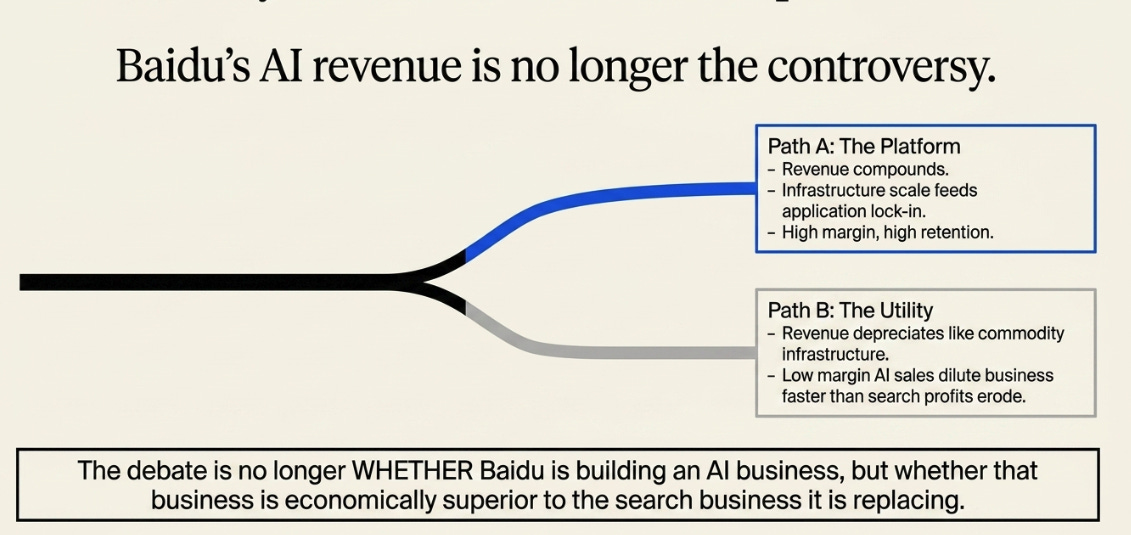

So the updated thesis is this: Baidu has crossed the first threshold. AI is now large enough to redefine the company. The second threshold is harder. AI must become profitable enough to re-rate it.

The variant perception is therefore not “Baidu AI is underappreciated.” That is too simple. The sharper version is: Baidu’s AI revenue is no longer the controversy. The controversy is whether that revenue compounds like a platform or depreciates like infrastructure.

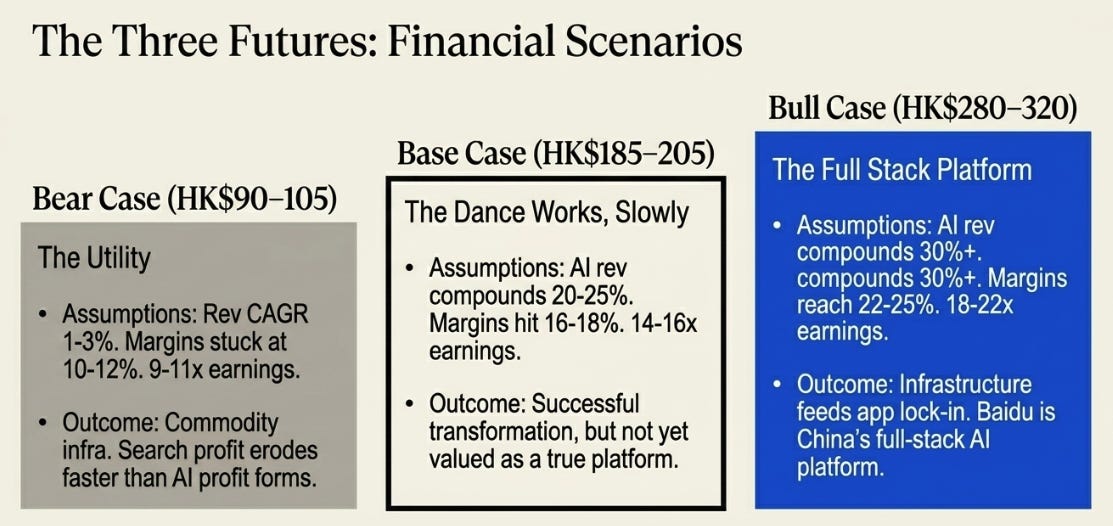

Three futures.

At roughly HK$135–136, the stock still embeds skepticism. That skepticism is not irrational; it is the correct price for an unresolved transformation. The next three years depend less on whether Baidu can grow AI revenue and more on what kind of revenue AI turns out to be.

This keeps the spirit of the prior scenario framework, but raises the bar. The bull case is more visible after 1Q26, but it is not yet earned.

The scoreboard from here.

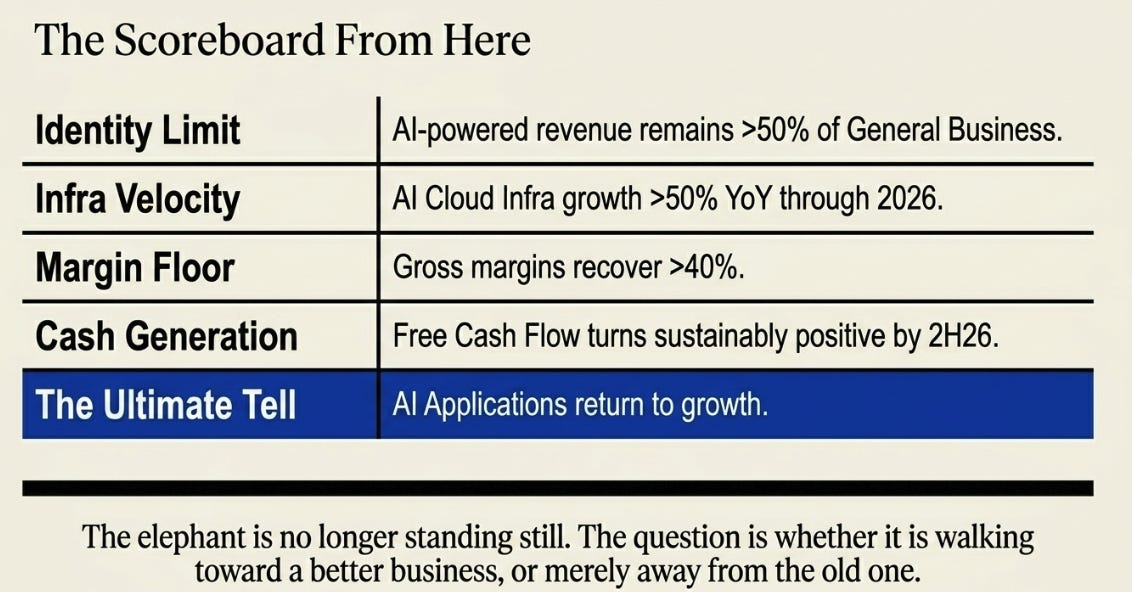

The key markers are not complicated. AI-powered revenue must remain above 50% of Baidu General Business; otherwise the new identity looks premature. AI Cloud Infra needs to remain above 50% year-over-year through 2026 to prove the Q1 step-up was not pull-forward. Gross margin needs to recover above 40%; below 38% keeps the utility bear case alive. Free cash flow needs to turn sustainably positive by 2H26. Online marketing decline needs to narrow to better than -15% year-over-year, or else cannibalization remains ahead of monetization.

Most importantly, AI Applications need to return to growth. That is the real tell. If applications stay flat while AI Cloud grows, Baidu may become a respectable infrastructure vendor. If applications reaccelerate, Baidu may become a platform.

That difference is the investment case.

Baidu has crossed the first threshold: AI is now large enough to replace the story of search. The second threshold is harder: AI must become profitable enough to replace the economics of search. The wrong scoreboard matters because Alibaba has scale, Tencent has economics, Huawei has national infrastructure, and ByteDance has attention. Baidu’s edge is narrower but potentially powerful: the conversion of intent into AI workloads, and eventually into actions.

The elephant is no longer standing still. The question is whether it is walking toward a better business, or merely away from the old one.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.