Bloom Energy: What All the World Desires to Have

AI made power scarcity urgent. Bloom has the right machine, but the stock depends on whether related-party revenue becomes clean customer proof.

TL;DR

Bloom is not an AI pivot; it is a 25-year-old edge-power thesis finally meeting the right customer problem. AI data centers do not merely need cheaper electricity: they need power in months, not years, and Bloom’s onsite, modular fuel-cell architecture is unusually well matched to that job.

The business inflection is real, but the revenue pipe is messy. Q1 2026 revenue grew 130% YoY and guidance was raised sharply, yet roughly half of Q1 revenue and nearly three-quarters of Q4 2025 revenue came from related-party structures, making conversion quality the key analytical issue.

The stock now needs the Boulton Ending. Demand is visible; the next proof is operating megawatts, cleaner non-related-party customer wins, service margins holding, cash conversion improving, and Fremont scaling toward 5 GW without quality or margin breaks.

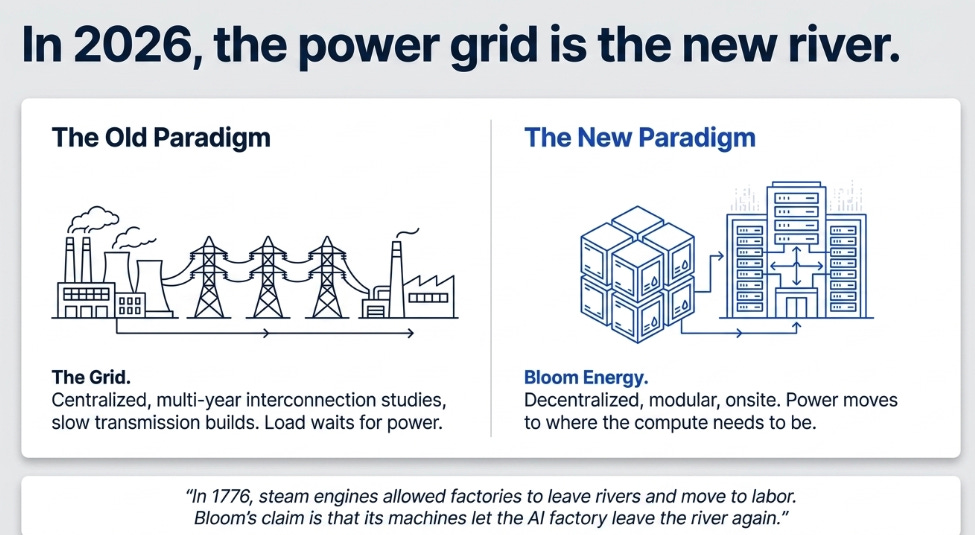

In March 1776, James Boswell visited the Soho Manufactory outside Birmingham. His host was Matthew Boulton, the manufacturer who had entered partnership with James Watt. Boulton’s introduction became one of the cleanest sentences in industrial history: “I sell here, Sir, what all the world desires to have, POWER.”

The quote is famous; the business arrangement was more interesting. Boulton and Watt did not simply sell engines. They charged customers based on the coal their engine saved versus the older Newcomen machine. The price was not anchored to the cost of iron, labor, or assembly. It was anchored to the value of avoided waste.

The second detail matters even more. Watt’s engine was not originally built for factories. It was built to pump water out of mines. The factory use case arrived later, once manufacturers realized that steam could free production from the tyranny of falling water. A mill no longer needed to sit by a river. It could sit near workers, suppliers, and customers. Power moved to where production wanted to be.

That is the useful frame for Bloom Energy. The company is not interesting because it makes fuel cells. It is interesting because AI data centers are discovering that the grid has become the river. And Bloom’s claim is that its machines let the factory leave the river again.

The Rocket Scientist’s Long Wait

Bloom’s founder, KR Sridhar, likes to trace the company’s origin to Mars. That story can sound theatrical, but it is analytically useful. Mars has no grid, no repair crew, no local utility, and no tolerance for failure. A machine designed for that environment begins with different assumptions from a machine designed for ordinary interconnection.

In a 2026 founder interview, Sridhar said his 2001 Kleiner Perkins pitch deck already showed a Bloom box powering a data center, using waste heat for cooling, and connected to nothing else. That is the founder’s cleanest version of the story: the AI data-center use case was there from the beginning; the market simply took twenty-five years to arrive.

The less clean version is just as important. Bloom did not spend those twenty-five years marching in a straight line. It spent them surviving. The company began as Ion America, became Bloom Energy in 2006, came out of stealth with enormous fanfare, and then endured the usual hard-tech middle: high costs, complicated financing, persistent losses, service issues, customer concentration, and the constant question of whether a technically impressive machine could become a financially attractive business.

Sridhar’s Andy Grove story captures the company’s scar tissue. The first few Bloom boxes, hand-built by engineers, worked. The next batches, built from written instructions, failed badly in the field. Grove told Sridhar to stop studying binders and start talking to the people on the factory floor. The lesson was not “manufacturing matters,” a cliché; it was that manufacturing knowledge lives in repeated practice, tacit skill, and feedback from failure.

That matters because Bloom’s edge, if it has one, is not just ceramic chemistry. It is twenty years of learning how to make the chemistry in volume, keep it running, monitor it remotely, service it, finance it, and convince conservative customers that it will not fail.

The Wilderness, Honestly Told

Founder stories become dangerous when they erase the detours. Bloom had many.

In 2021 and 2022, the story was broad: hydrogen, electrolyzers, biogas, marine, carbon capture, Korea, resilience, sustainability, and cost predictability. The South Korean relationship with SK ecoplant was central. Hydrogen was described as a major future market. Marine looked like a possible new vertical. The company had a long list of ways the same core technology might matter.

Some of those stories faded. Marine largely disappeared from the earnings-call narrative. Electrolyzers remained strategically interesting but not central to near-term revenue. Korea remained important, but policy changes and amended purchase timing made it less of a straight-line growth engine. Service economics, for years a drag on margins, had to be repaired.

The company’s historical accounting scar also belongs here. Bloom’s 2019 filing disclosed that prior financials should no longer be relied upon because certain Managed Services revenue had been recognized upfront when it should have been recognized over the contract duration. The correction reduced cumulative revenue through September 2019 by $192.1 million and revealed a material weakness in internal control over financial reporting.

That does not make today’s story invalid. It makes one thing clear: Bloom’s financial plumbing has never been simple. Any investment case that skips that fact is incomplete.

The New River

The old grid was built for a different demand curve. Large power plants, transmission lines, local distribution, interconnection studies, regulated returns, rate cases, and multi-year construction schedules made sense in a world where electricity demand grew slowly and predictably.

AI is a different customer. A large AI data center is a factory whose input is electricity and whose output is compute. The customer does not want an academic answer to the question of whether the grid can eventually serve the load. The customer wants to know whether power will be available before the revenue opportunity moves on.

This is what changed for Bloom. The old question was: “Can Bloom produce a cleaner or more resilient electron at an acceptable cost?” The new question is: “Can Bloom bring power online before the grid, turbines, permitting, and interconnection queues can?”

Bloom’s Q1 2026 results showed why the change matters. Revenue was $751.1 million, up 130.4% year over year, driven by product revenue growth of 208.4%. Gross margin was 30.0% on a GAAP basis and 31.5% on a non-GAAP basis. Operating income was $72.2 million on a GAAP basis and $129.7 million on a non-GAAP basis. Cash flow from operations was $73.6 million.

The company then raised full-year 2026 guidance to $3.4–$3.8 billion of revenue, roughly 34% non-GAAP gross margin, $600–$750 million of non-GAAP operating income, and $1.85–$2.25 of non-GAAP EPS.

This is not just a narrative inflection anymore. It is hitting the P&L.

The Machine for This Age

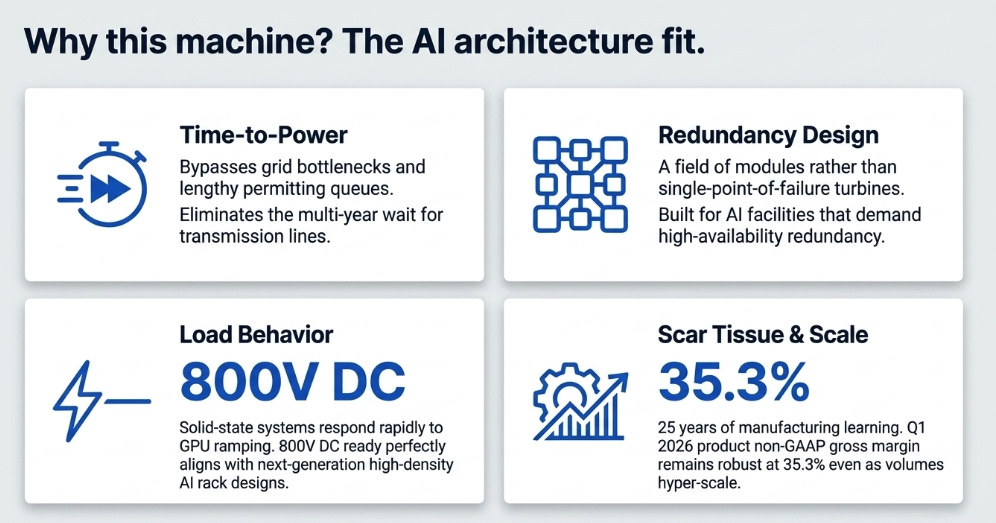

Grant that the demand is real: why this machine?

The answer starts with time. Bloom’s systems are modular, can be placed onsite, and do not require the same years-long route as new transmission or conventional power equipment. They use fuel, mostly natural gas today, and convert it into electricity through an electrochemical process rather than combustion. That gives Bloom a local-emissions, water-use, noise, and siting argument versus many combustion-based alternatives.

The second answer is reliability design. Bloom’s systems are built from many smaller power modules. That matters because an AI data center is also built from redundancy. A single turbine is a large point of failure; a field of modules can be maintained in pieces. That does not eliminate all risk, but it aligns with how data centers already think.

The third answer is load behavior. AI loads are not always smooth. GPU demand can ramp and pulse. Bloom argues that its solid-state systems can respond faster than rotating machinery and can support newer data-center electrical designs. In Q4 2025, management said every Bloom server shipped from that point would be 800V DC ready, framing the machine as better aligned with high-density AI rack design.

The fourth answer is learning. Product margin remains robust even as volume grows. In Q1 2026, product revenue was $653.3 million, product non-GAAP gross margin was 35.3%, and service non-GAAP gross margin improved to 18.0% from 4.8% a year earlier.

That is the financial fingerprint investors should care about: not just growth, but growth without immediate margin collapse.

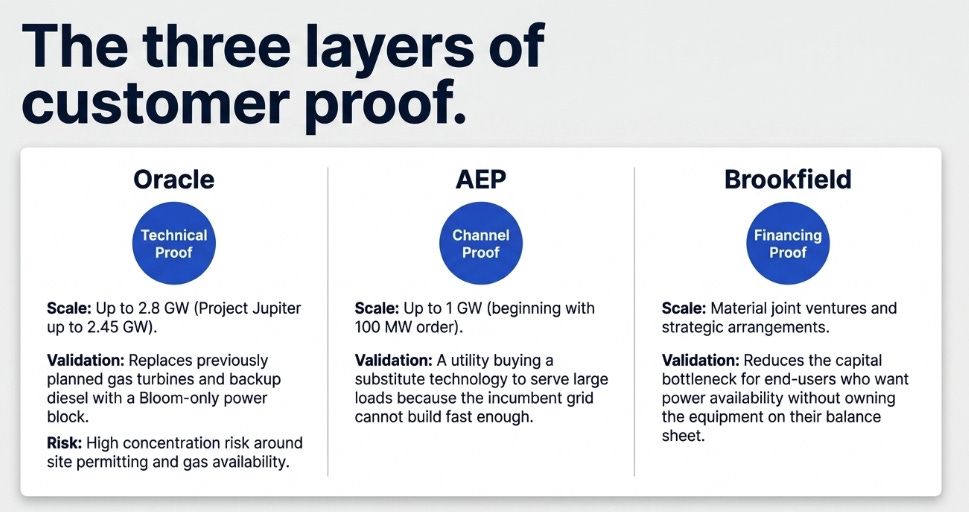

Oracle, AEP, Brookfield: Three Kinds of Proof

The proof now comes in three layers.

Oracle is technical proof. The expanded Oracle agreement covers up to 2.8 GW, with Project Jupiter accounting for up to 2.45 GW of Bloom-only power. The Q1 2026 call described Project Jupiter as replacing previously planned gas turbines and backup diesel generators with a Bloom-only power block.

That is a huge validation. It is also concentration risk. If one campus represents most of the headline Oracle ceiling, then permitting, gas availability, site construction, and customer schedule at that location matter enormously.

AEP is channel proof. Bloom’s 2025 10-K says AEP is expected to procure up to 1 GW of Bloom solid oxide fuel cells under a strategic supply agreement, beginning with an initial 100 MW order, and that Bloom began working with AEP in 2025 as both channel and financing partner.

This matters because a utility buying Bloom to serve large loads is structurally different from an enterprise customer buying Bloom to bypass the utility. The incumbent is hiring the substitute because it cannot serve the new load fast enough.

Brookfield is financing proof. The Brookfield arrangement matters not because it is revenue, it is not, but because it can reduce the capital bottleneck for customers that want power availability without owning the equipment themselves. Bloom’s filings show this relationship is already material. The strategic value is real. So is the accounting complexity.

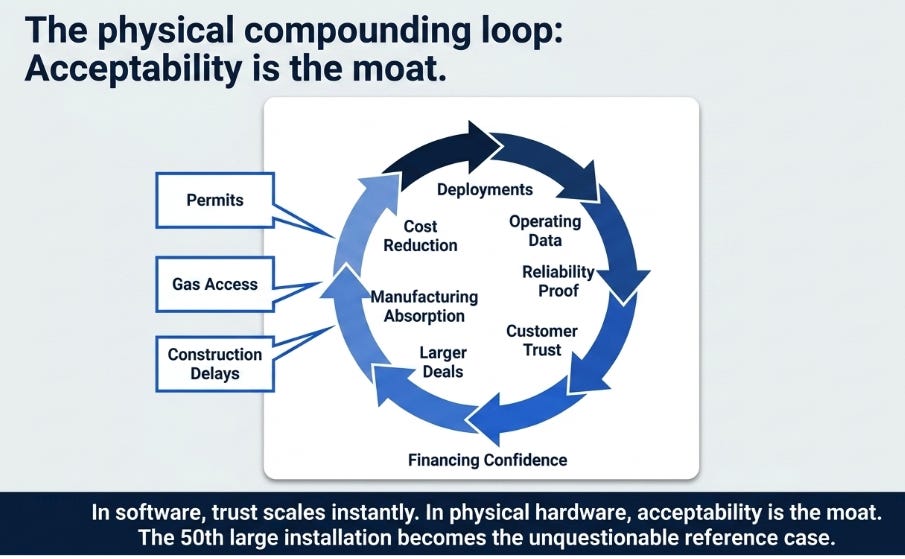

The Loop That Could Matter

The self-reinforcing mechanism is straightforward:

This is slower and more fragile than software. It requires equipment, permits, gas access, construction, service, and cash collection. But in physical markets, trust compounds. The first large installation is hard. The fifth is easier. The fiftieth is a reference case.

Service is part of this loop. The installed base becomes valuable only if service stays profitable as the fleet grows and ages. Bloom has made progress. Q1 service revenue was $61.9 million, service GAAP gross margin was 13.3%, and service non-GAAP gross margin was 18.0%.

But this is not a software-like royalty. It is a maintenance obligation. It includes field labor, replacement modules, repair and overhaul, performance guarantees, and fleet degradation risk. The service book becomes an asset only if reliability improves faster than the fleet ages.

That is why the next phase is not about demand alone. It is about whether the operating proof compounds faster than the physical complexity.

The Pipe Matters

This is where the Bloom story becomes more interesting than the usual AI-power stock pitch.

The demand is real. The reported growth is real. But the path from end demand to reported revenue is not simple.

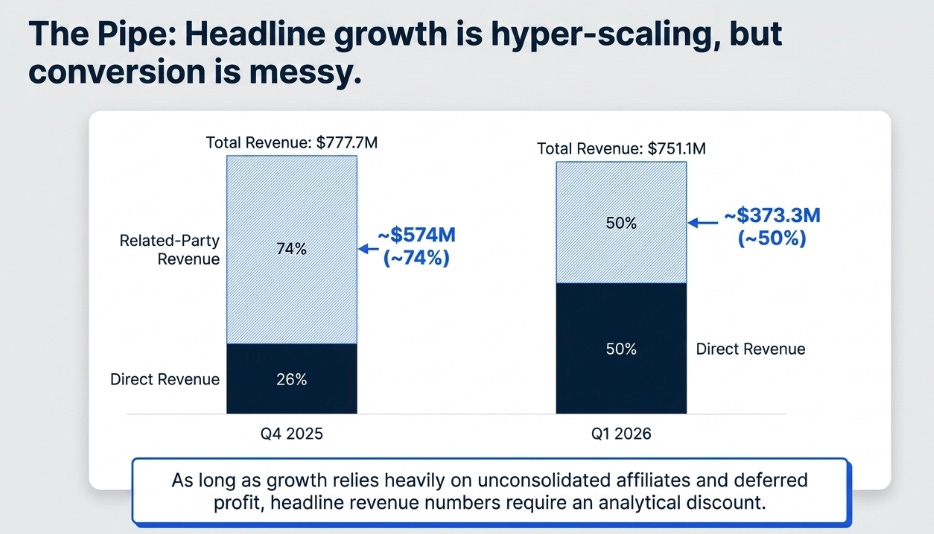

In Q1 2026, Bloom reported $373.3 million of related-party revenue on $751.1 million of total revenue. In Q4 2025, related-party revenue was $574.2 million on $777.7 million of total revenue. That means roughly half of Q1 revenue and nearly three-quarters of Q4 revenue flowed through related-party structures.

That is not a footnote. It is one of the central analytical facts in the story.

The balance sheet adds nuance. Related-party accounts receivable fell from $151.9 million at year-end 2025 to $0.6 million at March 31, 2026, which is a positive collection signal. But related-party contract assets rose from $3.0 million to $74.1 million, and the company disclosed related-party investments in Brookfield joint ventures and deferred profit from transactions with those unconsolidated affiliates.

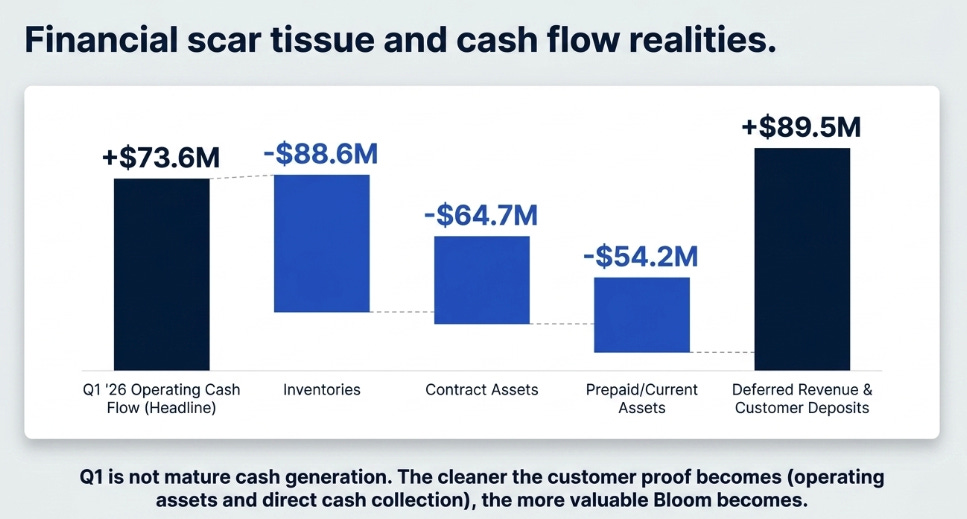

The cash-flow statement also shows why investors should avoid treating Q1 as mature cash generation. Operating cash flow was positive at $73.6 million, but inventories consumed $88.6 million, contract assets consumed $64.7 million, prepaid and other current assets consumed $54.2 million, while deferred revenue and customer deposits added $89.5 million.

Again, none of this means the demand is fake. It means the customer proof needs to get cleaner over time.

The right sentence is simple:

The cleaner the customer proof becomes, the more valuable Bloom becomes.

If growth increasingly comes through direct or clearly attributable end-customer demand, with operating assets and cash collection, the market will have more reason to pay a premium. If growth remains dominated by related-party vehicles, unconsolidated affiliates, deferred profit, warrants, and working-capital movements, investors should discount the headline numbers.

What the Market Still Misses

The obvious view is that Bloom is now an AI power winner. That view is no longer contrarian. The stock has already moved from disbelief to expectation.

What the market may still underappreciate is that Bloom’s best asset is not any single order. It is the possibility that a few successful large deployments turn the machine from unusual to acceptable. In conservative physical markets, acceptability is the moat. Once customers, utilities, financiers, and local regulators believe a system works, the next sale becomes easier.

The second underappreciated point is that AI changes the metric. Bloom is not competing only on the cost of electricity. It is competing on the value of time. A delayed AI facility does not merely pay more for power; it may lose customers, compute revenue, and strategic position.

The third underappreciated point is the DC angle. If AI racks increasingly standardize around high-voltage DC designs, Bloom’s 800V DC readiness could matter more than traditional comparisons against turbines or engines imply.

But there is also a less pleasant truth the market may be underestimating: related-party revenue is not the same thing as clean end-user adoption. Brookfield may be an accelerant, but the more Brookfield-related entities become the buyer of record, the more investors need to separate financing proof from customer proof.

The business is more real than old skeptics believed. The stock is more demanding than new believers admit.

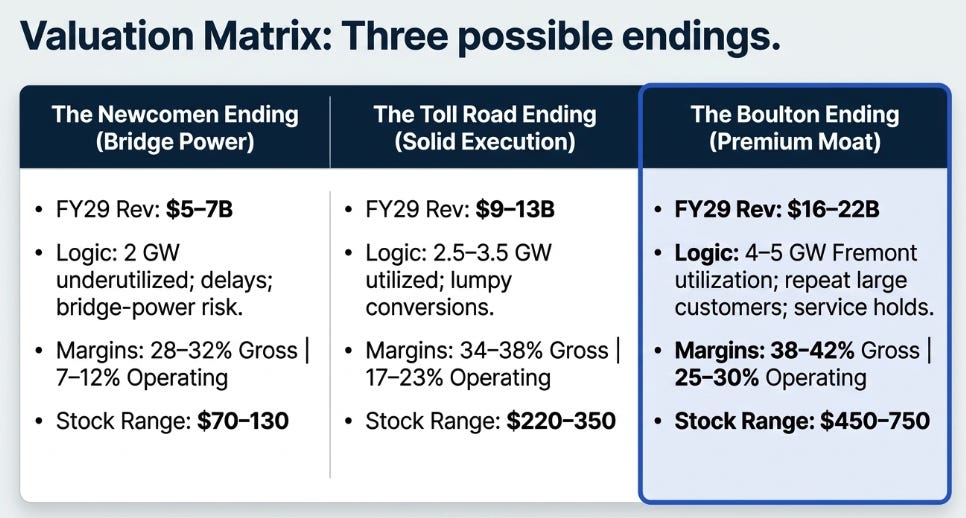

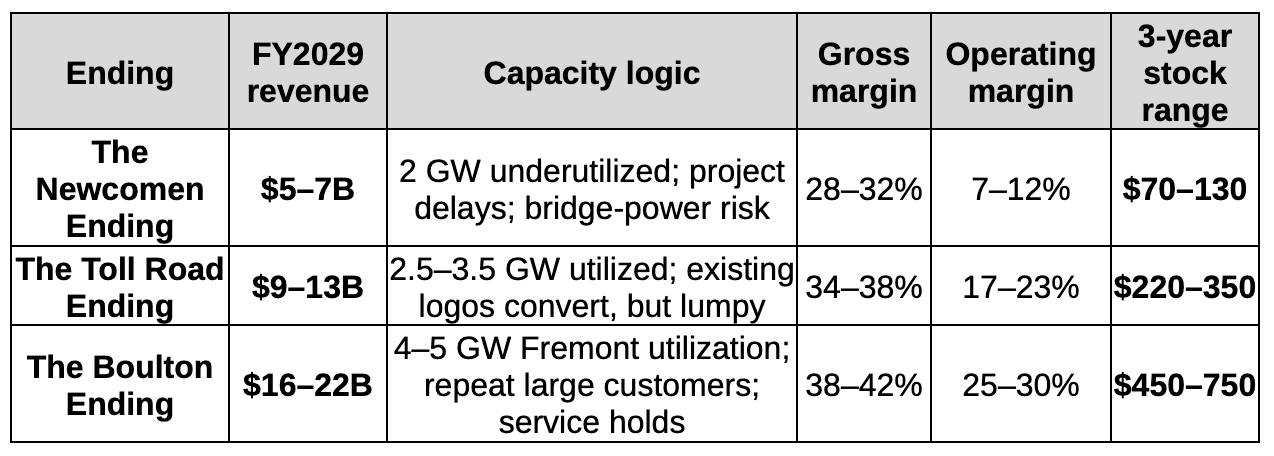

Three Possible Endings

The scenarios should be anchored to capacity, not only demand. Management said on the Q3 2025 call that doubling capacity to 2 GW by December 2026 would support about four times 2025 revenue. Since 2025 revenue was about $2.0 billion, that implies roughly $8 billion of blended revenue support at 2 GW.

The 2025 10-K also says the Fremont facility can accommodate up to approximately 5 GW of annual production capacity, with each additional 1 GW requiring roughly six to nine months and $100–150 million of capex.

That makes the scenario table more disciplined:

The Newcomen Ending is not failure. It is repricing. Bloom grows, but customers use it as bridge power, related-party revenue remains elevated, margins disappoint, and the market values the company more like energy equipment than scarce AI power capacity.

The Toll Road Ending is solid execution. Bloom converts the current logos, margins improve, service remains profitable, and Fremont scales beyond 2 GW. But growth is lumpy, customer concentration remains visible, and the multiple settles lower as the story becomes more industrial.

The Boulton Ending is the premium case. Bloom fills much of Fremont’s 5 GW potential, wins more large customers without material equity sweeteners, service margins remain high, and related-party revenue falls as a percentage of total. In that world, Bloom is not merely selling machines. It is charging for time saved.

A supercharged version above $25 billion of revenue probably requires either a second major manufacturing footprint or unusually high revenue per GW. That should not be the main case. It is the option.

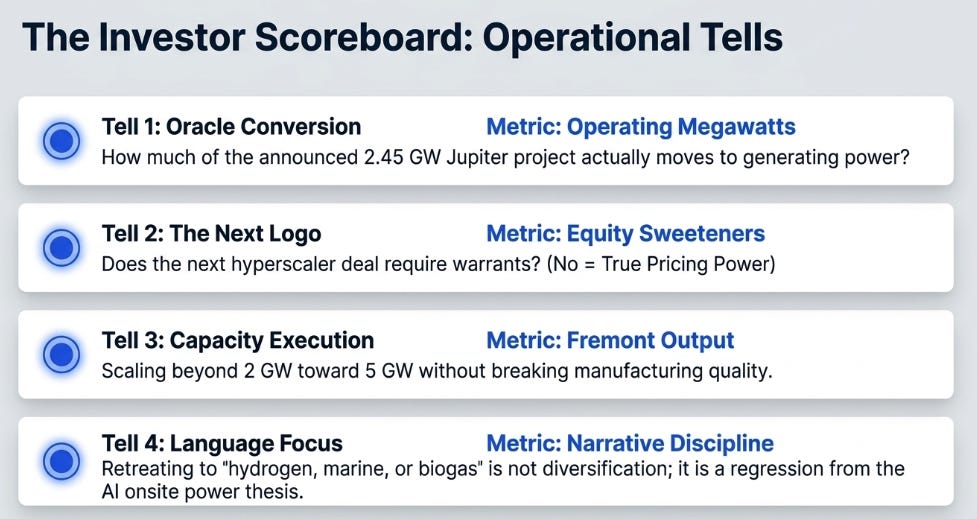

The Scoreboard

The thesis is trackable. Use the same funnel for every large project:

Revenue announced is not revenue earned. Revenue earned is not necessarily cash. Cash is not necessarily clean if it is pulled forward by deposits, payables, or related-party structures.

The first tell is Oracle/Jupiter conversion: how much of the 2.45 GW moves from announcement to operating megawatts.

The second tell is the next large customer. If the next hyperscaler-scale deal comes without a warrant or equity sweetener, Bloom has more pricing power than skeptics think. If equity incentives become normal, early validation is being partly purchased.

The third tell is related-party revenue share. Q1 2026 was roughly half related-party. That number should fall over time if the customer proof is broadening.

The fourth tell is contract assets and deferred profit. If these grow faster than revenue, the quality question gets louder.

The fifth tell is product margin. It needs to stay in the mid-30s or better as AI projects grow.

The sixth tell is service margin. High-teens to 20% is supportive. A decline would suggest the installed base is becoming more obligation than asset.

The seventh tell is installation margin. Q1 2026 installation non-GAAP margin was negative 29.4%. If large AI projects increase installation complexity, this line matters more than the headline narrative suggests.

The eighth tell is capacity. The story requires 2 GW, then 3 GW, then 5 GW, not just as nameplate capacity, but as real output with acceptable quality.

The ninth tell is language. If management retreats from focused language about onsite power and time-to-power back into a broad catalogue of hydrogen, marine, biogas, carbon capture, and every possible application, that is not diversification. It is regression.

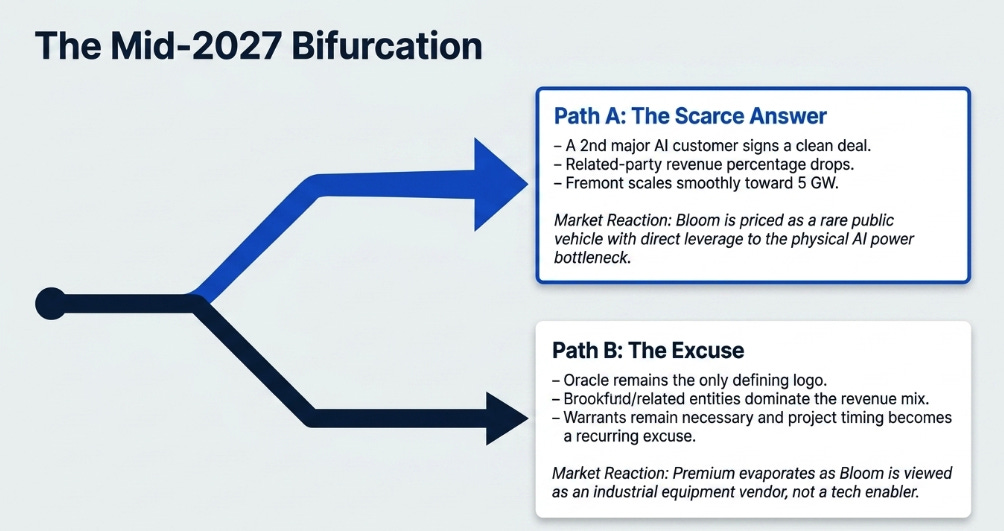

The Prediction

By mid-2027, Bloom will likely be in one of two places.

In the first, a second major AI customer has signed a large, clean, multi-site deal; related-party revenue has fallen as a percentage of total; Fremont expansion is visibly progressing toward 5 GW; service margins remain high-teens or better; and cash conversion improves. In that world, the market continues treating Bloom as one of the few public companies with direct leverage to the physical bottleneck in AI.

In the second, Oracle remains the defining logo, Brookfield-related sales stay a large share of revenue, customer warrants or financing structures remain necessary, and project timing becomes the recurring excuse. In that world, Bloom may still be a good company, but the stock will stop being valued like the scarce answer to a scarce problem.

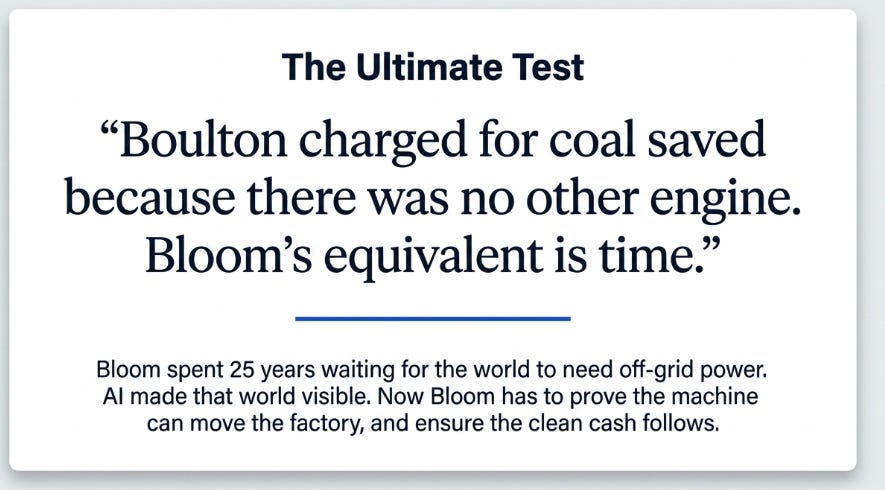

Boulton charged for coal saved because there was no other engine. Bloom’s equivalent is time. The company will deserve its premium only when it can charge for the time it saves without giving too much of that value back through warrants, financing structures, margin concessions, or accounting complexity.

Bloom spent twenty-five years waiting for the world to need power where the grid was not ready. AI has made that world visible. Now Bloom has to prove that the machine can move the factory, and that the cash follows.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.