Booking 1Q26 Earnings: The Stack Beneath the Trip

AI may own travel discovery. Booking is betting the money is in execution. Q1 showed both why that bet matters and why the market is not ready to underwrite it.

TL;DR

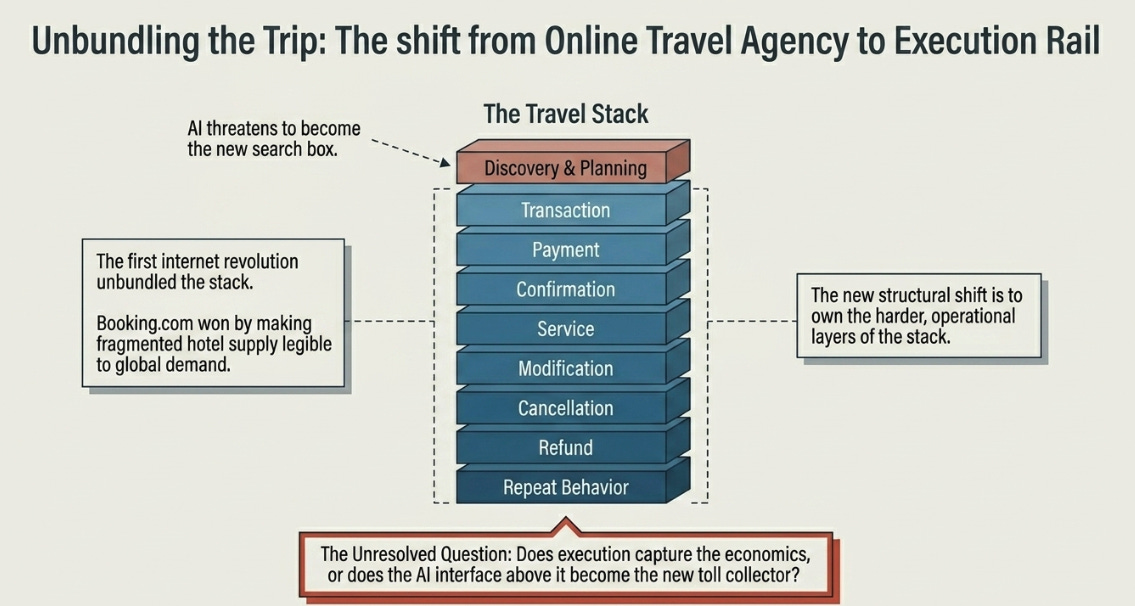

Booking’s real thesis is not about room nights; it is about moving down the travel stack from discovery to execution. The internet made travel searchable; AI may make it conversational. Booking is trying to own the harder layer: payments, settlement, refunds, service, loyalty, fraud, and trip coordination.

Q1 was not interesting because a war hurt travel demand. It was interesting because the Middle East conflict stress-tested the exact layer Booking claims will matter most in an AI world: execution. Reported room-night growth was 6%, but management estimated it would have been about 8% excluding the conflict.

The stock should still be owned, but with a sharper burden of proof. Booking is proving it can execute travel. The unresolved question is whether execution captures the economics, or whether the AI interface above it becomes the new toll collector.

The trip is not the search

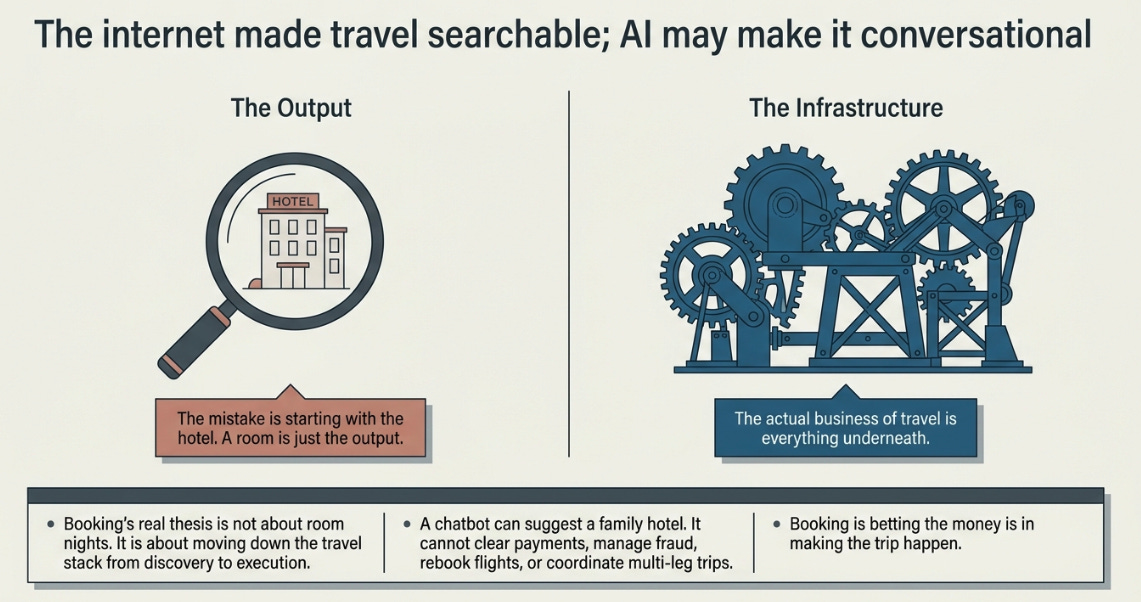

The mistake in analyzing Booking Holdings is to start with the hotel.

A hotel room is the output. The more important question is the stack underneath the trip: discovery, planning, transaction, payment, confirmation, service, modification, cancellation, refund, and repeat behavior. The first internet revolution unbundled that stack. Discovery moved online. Booking.com won because it made fragmented hotel supply legible to global demand.

AI threatens to change the interface again. Asking a model for a family-friendly hotel in Rome under $300 with a pool is simply a better search box. That sounds threatening.

But travel is not only search. The hard part is execution. The room has to exist. The payment has to clear across currencies. Fraud has to be managed. A traveler whose flight is delayed needs service. A multi-leg trip needs coordination. A chatbot can suggest the trip. It cannot, by itself, make the trip happen.

That is Booking’s bet. It is why I have argued across several pieces that the company is moving from online travel agency to transaction rail to execution infrastructure. The thesis still looks right. The stock has not agreed.

The business did not break

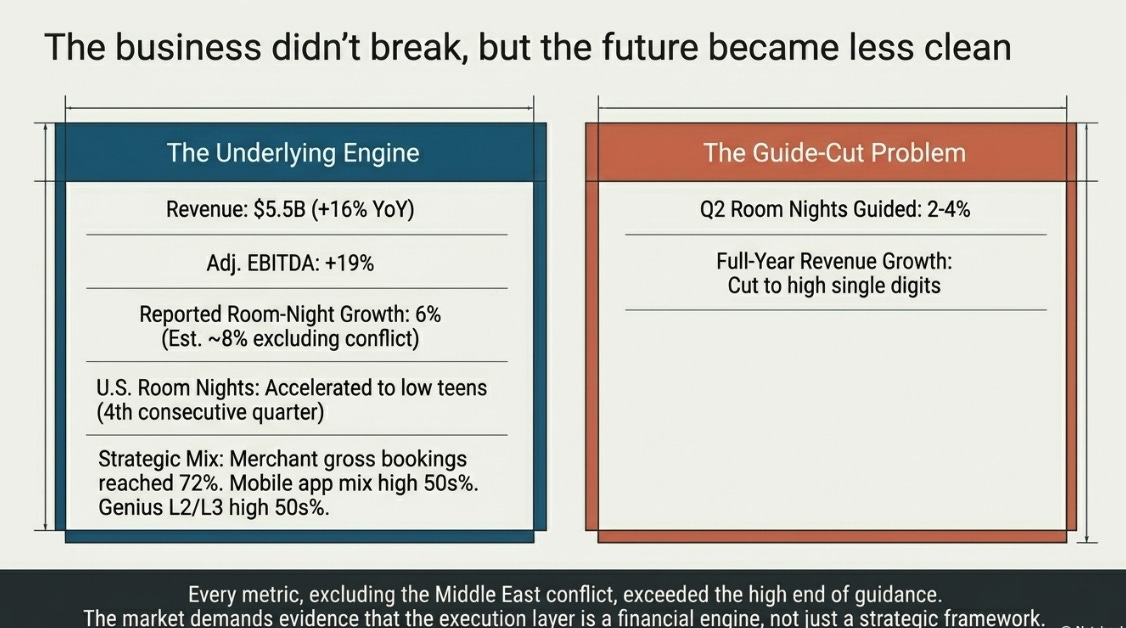

Booking’s Q1 numbers were not the problem. Revenue of $5.5 billion grew 16%. Adjusted EBITDA grew 19%. U.S. room nights accelerated for the fourth consecutive quarter to the low teens. Every metric, excluding the Middle East conflict, exceeded the high end of guidance.

The stock sold off because the future became less clean. Q2 room nights are guided to only 2–4%. Full-year revenue growth was cut to high single digits.

The strategic indicators are not deteriorating. Merchant gross bookings reached 72% of total. Mobile app mix is in the high 50s%. Genius Level 2 and Level 3 members account for a high-50% share of room nights. Connected Trip transactions are a low-double-digit percentage of total transactions.

The loop is visible. It is also not yet financially decisive. The market no longer wants the execution-layer thesis as a strategic framework. It wants evidence that the execution layer is a financial engine.

When the physical world breaks the software story

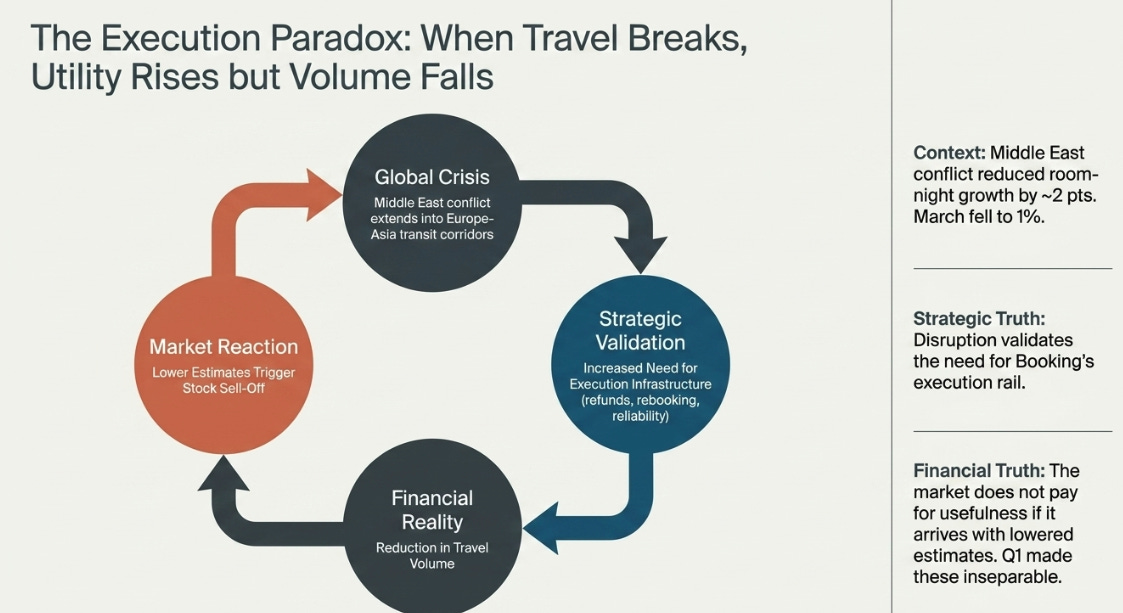

The Middle East conflict reduced room-night growth by about 2 percentage points. March room-night growth was only 1%. The disruption extended beyond the region into Europe-Asia transit corridors.

This is the paradox of the execution thesis. When travel breaks, execution becomes more valuable, customers need refunds, rebooking, and reliability. But when travel breaks, volumes also fall. The market does not pay for usefulness if usefulness arrives with lower estimates.

Strategically, disruption validates the need for execution infrastructure. Financially, disruption still hurts. Both are true. Q1 made them impossible to separate.

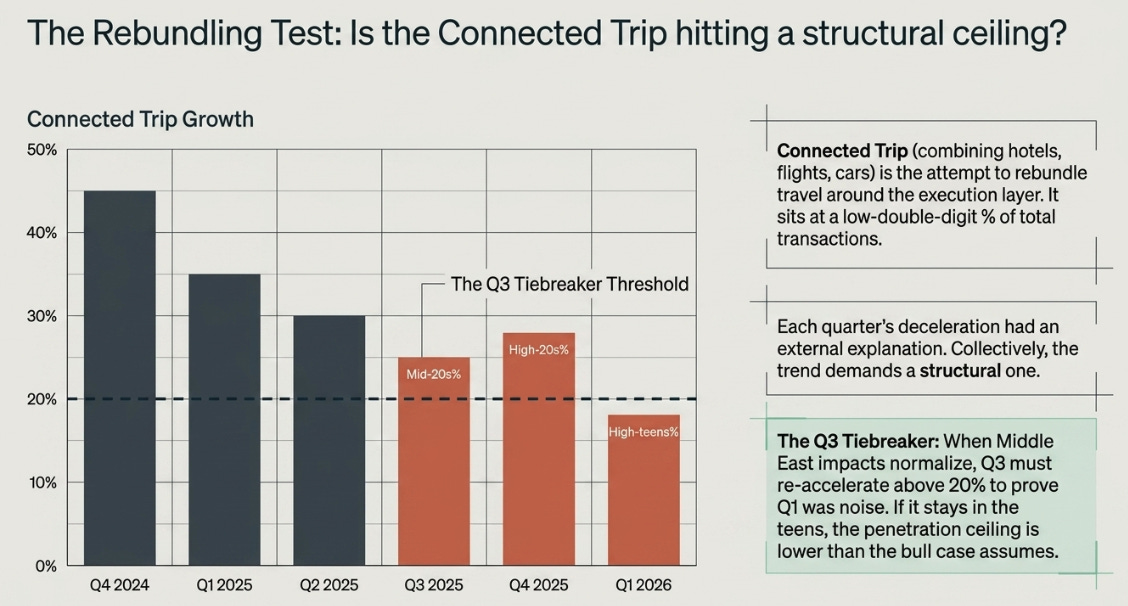

The rebundling test

Connected Trip, multi-vertical bookings combining hotels, flights, cars, and attractions, is Booking’s attempt to rebundle travel around the execution layer. But Q1 raises a subtle question: is a bundled trip more resilient, or more fragile?

The deceleration pattern is now long enough to warrant scrutiny:

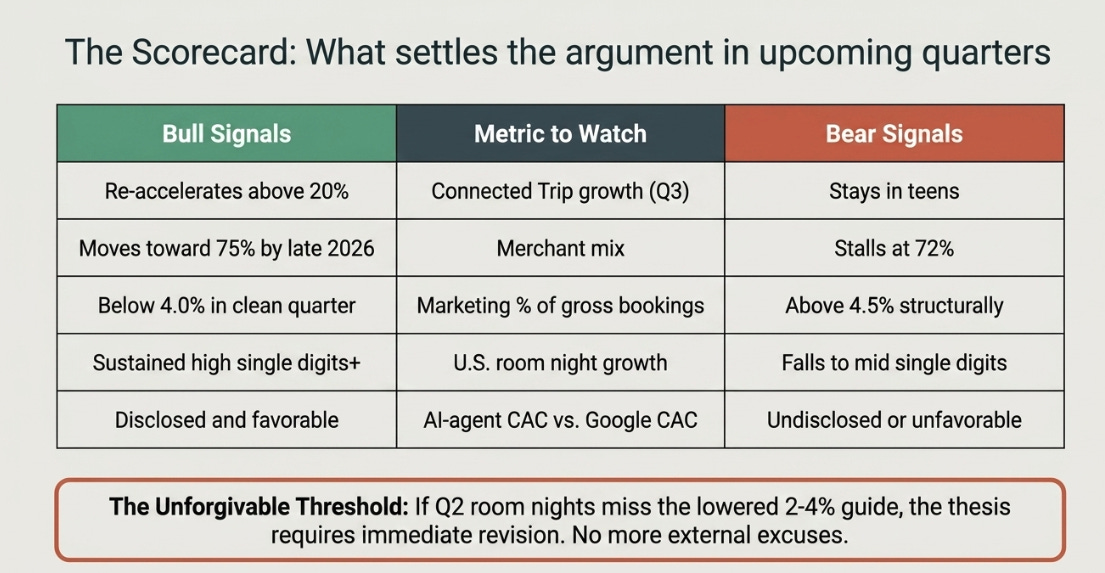

Each quarter’s deceleration had an external explanation. Collectively, the trend needs a structural one. Q3, when the Middle East impact should have normalized, will be the tiebreaker. If growth re-accelerates above 20%, Q1 was noise. If it stays in the teens, the penetration ceiling may be lower than the bull case assumes.

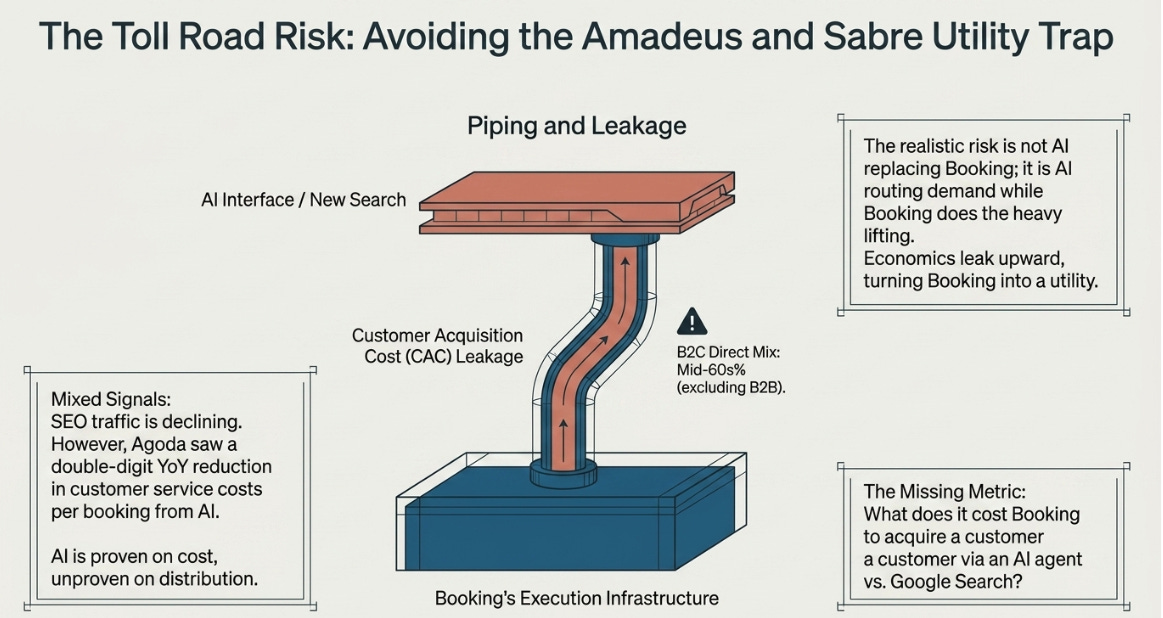

The toll road risk

The biggest long-term risk is not that AI replaces Booking. The more realistic risk is that AI becomes the interface routing demand while Booking remains the execution infrastructure underneath. Booking still matters, but the economics leak upward. Sabre and Amadeus did not disappear. They became utilities valued accordingly.

That is why the missing number matters most: what does it cost Booking to acquire a customer through an AI agent versus Google Search? If AI bookings come at equal or lower CAC, the thesis strengthens. If they cost more, AI becomes another landlord. The company has not disclosed that number.

AI did provide one real proof point: Agoda saw a double-digit year-over-year reduction in customer service costs per booking from AI automation. So the right framing is: AI is already helping on cost. It has not yet proven itself on distribution.

One disclosure nuance also deserves attention. Booking now reports B2C direct mix in the mid-60s%, having changed the definition from total direct mix by excluding B2B room nights. Management acknowledged SEO traffic is declining. If the AI risk is erosion of organic discovery, changes in how direct demand is measured matter.

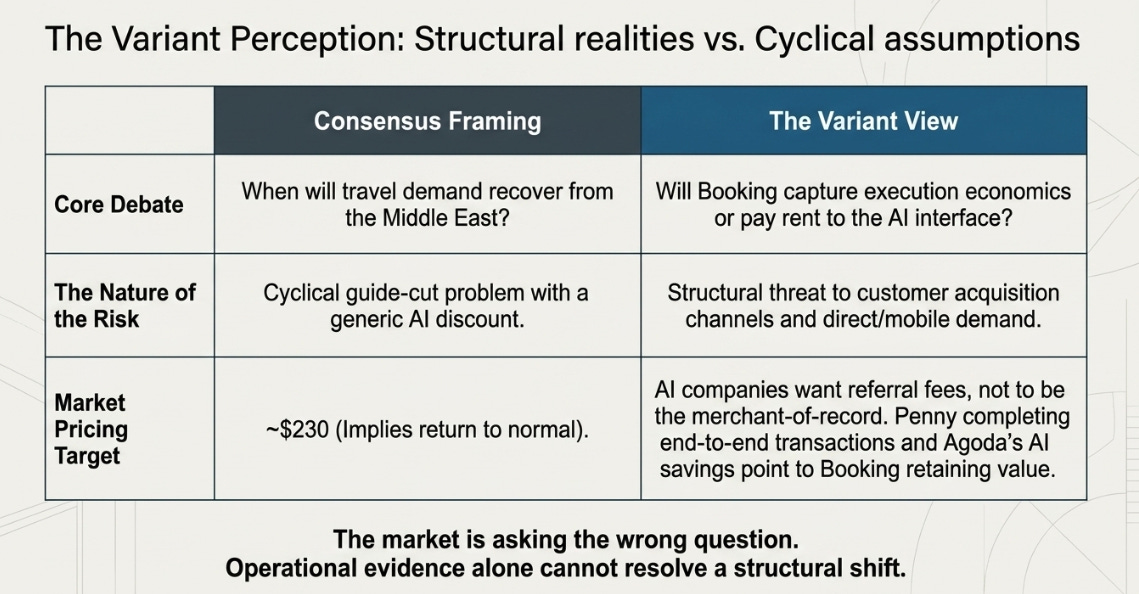

The variant perception

The market sees Booking as a high-quality travel company with a guide-cut problem and an AI disruption discount. Consensus price targets average ~$230, implying recovery once the Middle East normalizes.

That framing is not wrong. It is incomplete.

The variant view is that the market is asking the wrong question. Consensus debates whether travel demand recovers. The more important question is whether Booking’s execution layer, merchant payments, Connected Trip, Genius loyalty, direct/mobile demand, and AI-driven service efficiency, captures its own economics or pays rent to the AI interface above it. That is a structural question, not a cyclical one, and operational evidence alone cannot resolve it.

The bet is that resolution favors Booking because AI companies do not want to be merchant-of-record for global travel. They want to route demand and take a referral fee. Every piece of Q1 evidence, AI companies converging on performance marketing, Penny completing end-to-end transactions, Agoda’s AI cost savings, moves in that direction. But until the AI-agent CAC number is published, the uncertainty discount persists.

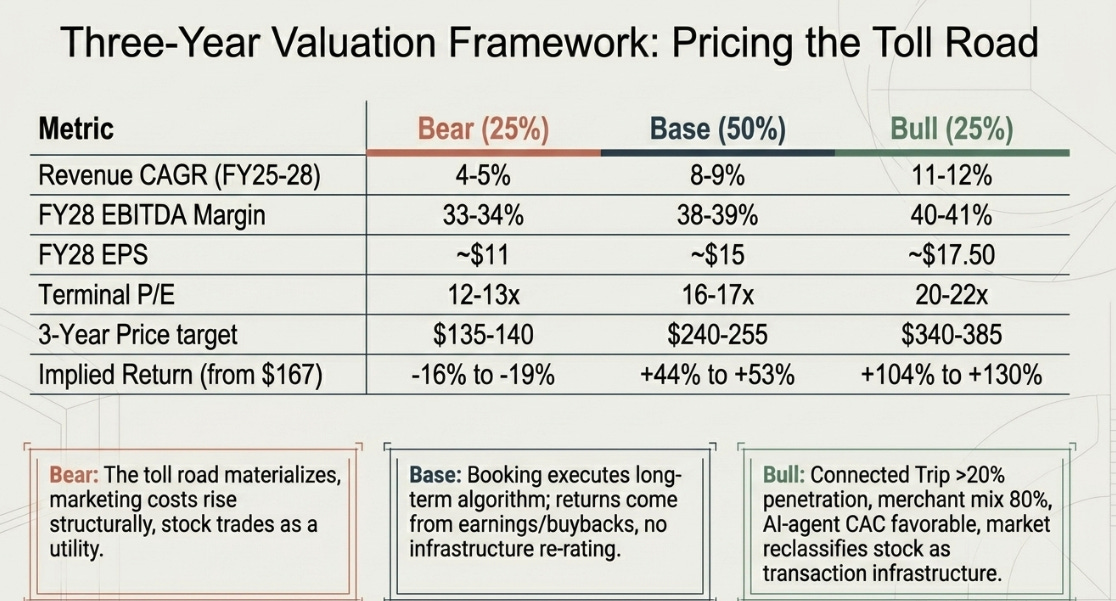

Three-year framework

At $167, the stock prices the toll road. Two of three scenarios pay investors from here.

The bear case assumes the toll road materializes, marketing costs rise structurally, margins compress, the stock trades as a utility. The base case assumes Booking executes at its long-term algorithm without earning an infrastructure multiple, returns come from earnings growth and buybacks, not re-rating. The bull case requires Connected Trip to reach 20-25% penetration, merchant mix to hit 80%, AI-agent CAC to prove favorable, and the market to reclassify the stock from travel to transaction infrastructure.

What settles the argument

I am committing to one threshold I do not want to explain away: if Q2 room nights miss even the lowered 2-4% guide, the thesis needs revision, not another external excuse. I have attributed enough quarterly disappointments to factors outside the company’s control.

Own it, but earn the conviction

At $167, Booking is priced like a travel company with a guide-cut problem, not a platform earning reclassification. That creates opportunity if Q2 is the trough and the strategic metrics keep compounding. I would own it here and add meaningfully at $155-160 if there is no new evidence of thesis deterioration.

The reason to own Booking is not that the market is obviously wrong. It is that the market is asking a hard question the company has not yet answered, and the current price offers enough compensation to wait for the answer.

The evidence says own it. The humility says size it for patience, not certainty.

The catalyst will come when Booking proves not just that it can execute travel, but that it can keep the economics of execution. That proof will not come from AI demos, partnership announcements, or normalized room-night bridges.

It will come from the income statement. It always does.

$BKNG

General Disclaimer: The information presented in this communication reflects the views of the author and does not necessarily represent the views of any other individual or organization. It is provided for informational purposes only and should not be construed as investment advice, a recommendation, an offer to sell, or a solicitation to buy any securities or financial products.

While the information is believed to be obtained from reliable sources, its accuracy, completeness, or timeliness cannot be guaranteed. No representation or warranty, express or implied, is made regarding the fairness or reliability of the information presented. Any opinions or estimates are subject to change without notice.

Past performance is not a reliable indicator of future performance. All investments carry risk, including the potential loss of principal. This communication does not consider the specific investment objectives, financial situation, or particular needs of any individual.

The author and any associated parties disclaim any liability for any direct or consequential loss arising from the use of this material and undertake no obligation to update or revise it.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.