Booking 4Q25: The Toll Road

I will commoditize travel discovery. The durable economics belong to whoever owns execution: payments, liability, and settlement.

TL;DR:

AI will crush the interface layer (search + metasearch), but travel’s real moat is the execution layer: merchant-of-record complexity, fraud, refunds, FX, compliance, and 24/7 service.

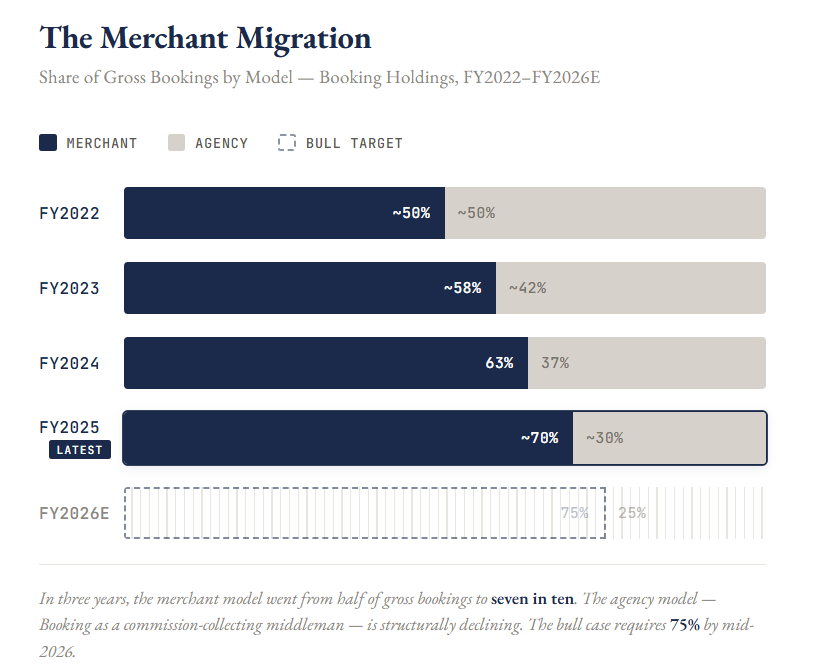

Q4 confirmed Booking is becoming travel’s transaction infrastructure: merchant mix hit ~70% (up from 50% two years ago) while agency revenue declined.

The key risk isn’t disruption, it’s toll extraction: if AI agents become demand routers, Booking may stay essential but pay a new “Google tax” to the dominant interface.

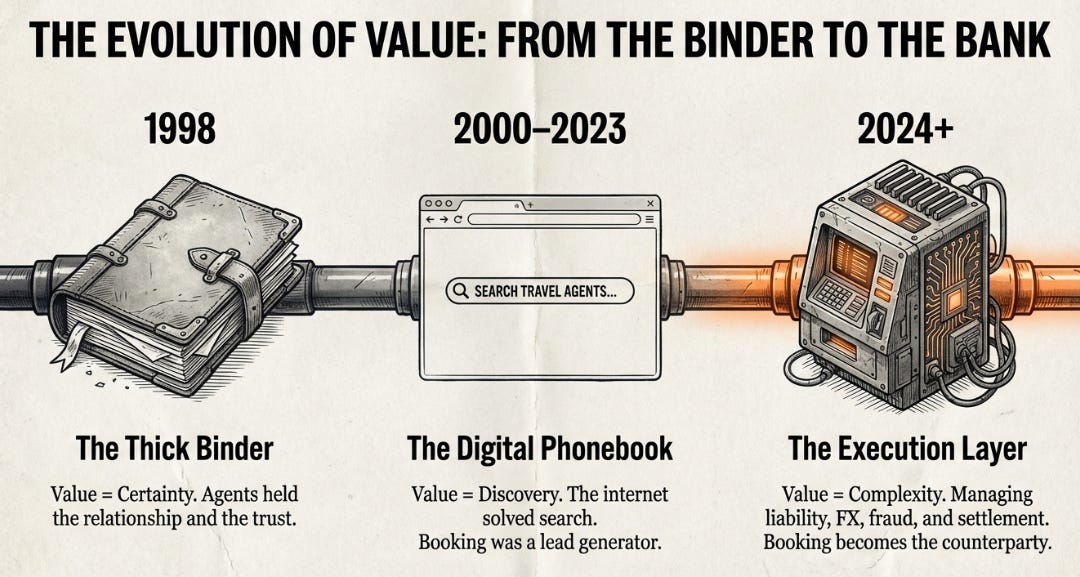

The Thick Binder

In 1998, if you wanted to book a small hotel on the Amalfi Coast, you called a travel agent. Not because they had better taste in hotels, you could flip through a Fodor’s guide yourself, but because they had a binder. The binder contained phone numbers, fax protocols, deposit policies, cancellation terms, and, critically, a relationship with someone at the property who would actually honor the reservation when you showed up. The agent’s value wasn’t discovery. It was certainty: the confidence that your money would reach the right place, in the right currency, and that a room would be waiting.

The internet solved the discovery problem. It digitized the binder. Booking.com made it possible to find that Amalfi hotel from your desk, read reviews, and compare prices in seconds. But for two decades, the execution problem, the certainty problem, remained surprisingly intact. You found the hotel online, but you often paid at the front desk. The OTA was a lead generator that took a commission for the introduction. Booking was a digital phone book with better typography.

That era is ending. And the way it’s ending tells you almost everything you need to know about why the market’s current panic over AI disruption is mispricing one of the most important structural shifts in online travel.

What the Quarter Revealed

Booking reported Q4 on February 18th. Room nights grew 9%, accelerating for the fourth consecutive quarter. Revenue grew 16%. Adjusted EBITDA grew 19%. For the full year, margins expanded nearly 200 basis points and adjusted EPS grew 22% to $228.

But the number that matters is this one: merchant gross bookings reached $130 billion, approximately 70% of total volume, up from 63% a year ago and 50% two years ago. Agency revenue declined nearly 7%.

Booking is no longer introducing you to the hotel and collecting a finder’s fee. On 70% of its transactions, it’s the counterparty. It collects your money, holds it, settles with the supplier in their local currency, handles chargebacks, manages fraud, and bears the liability if something goes wrong.

I’ve been writing about this merchant transition for over a year. Each quarter has validated the thesis and the trajectory has compounded: merchant mix from 59% to 70%, Connected Trip from high-single-digit to low-double-digit penetration, agency revenue declining, and, new this quarter, absolute customer service costs falling despite 10% volume growth, the first time a GenAI efficiency claim has shown up unambiguously in a major P&L line item.

The one thing Q4 did not validate is whether Booking becomes the preferred execution endpoint for AI agents. CEO Glenn Fogel made a forceful argument for why LLMs won’t go downstream into merchant-of-record complexity. But no AI-agent booking volume was disclosed. The partnerships with OpenAI, Google, Microsoft, and Amazon are real but pre-revenue. The argument is compelling. The evidence remains circumstantial.

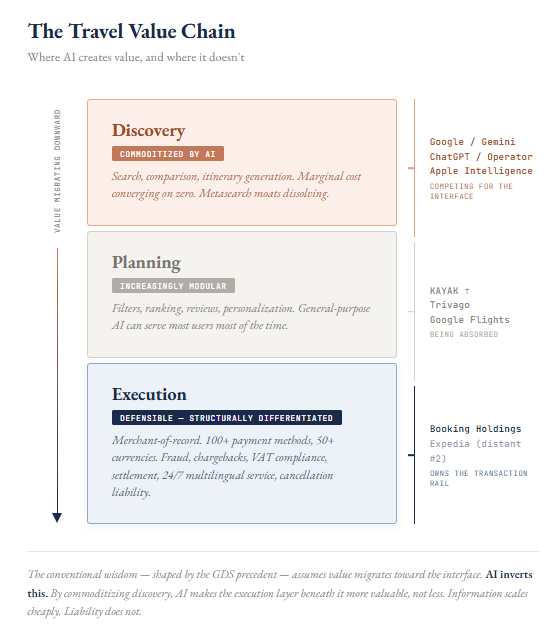

Information Scales Cheaply. Liability Does Not.

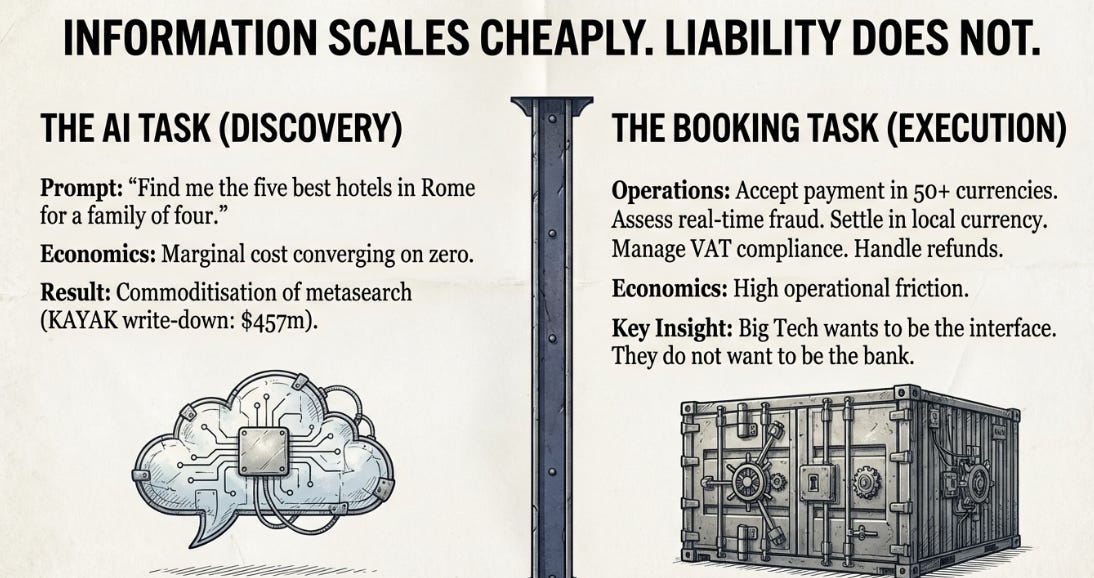

AI is very good at discovery: “Find me the five best hotels in Rome for a family of four in June under $300 a night with a pool.” An LLM can do this better than any search box ever built. The marginal cost of producing a customized travel itinerary is converging on zero.

This is genuinely bad news for metasearch, which is why Booking wrote down KAYAK for $457 million. The discovery layer is being commoditized.

But discovery is only the beginning of a travel transaction. Consider what happens after you choose the hotel. The platform must accept payment across 100-plus methods in 50-plus currencies. Assess fraud in real time. Hold the funds. Confirm with the property. Settle in the supplier’s local currency. Handle VAT compliance. Manage cancellations across different refund policies depending on rate type, jurisdiction, and timing. Provide service in the traveler’s language at any hour.

This is not an information problem. It’s an operations problem layered with financial liability and regulatory complexity. Information scales cheaply; liability does not.

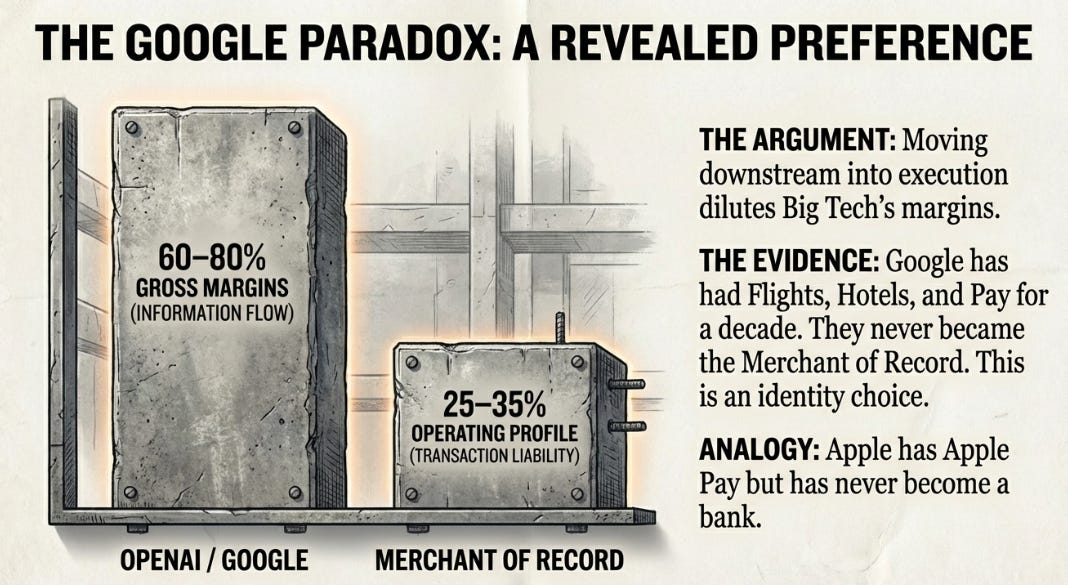

The question for every major AI company isn’t “can it do this?” It’s “does it want to?” OpenAI’s gross margins run 60–80%. Becoming the merchant-of-record for fragmented global travel would compress those toward 25–35%. These companies want to be the interface. They do not want to be the bank.

The Toll Road

If AI won’t disintermediate Booking, why is the stock down 24%?

Because there’s a subtler threat. The GDS didn’t die. Sabre still generates $3 billion in revenue. Amadeus is a $30 billion company. They’re alive, just valued as utilities. The interface layer captured routing power. The infrastructure layer’s economics compressed. What happened wasn’t replacement. It was toll extraction.

In a world where AI agents become the primary travel intent router, the booking still flows through Booking’s merchant rails, but now Booking pays a referral fee to the AI platform. Same game, new landlord. Today, Booking pays Google roughly $8.2 billion a year in marketing, a search tax for demand routing. If AI agents replace search, the tax migrates rather than disappears.

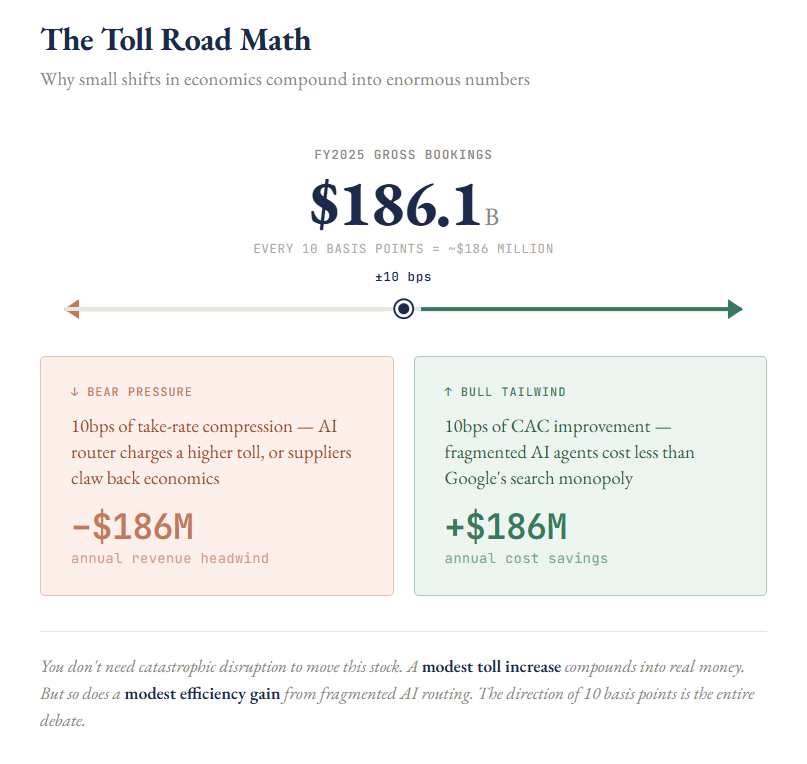

With $186 billion in annual gross bookings, every 10 basis points matters enormously. A 10bps shift in marketing cost represents roughly $186 million. A 10bps compression in Booking’s “take rate”, the share of each booking dollar it keeps as revenue, represents another $186 million. You don’t need catastrophic disruption. A modest toll increase compounds into real money.

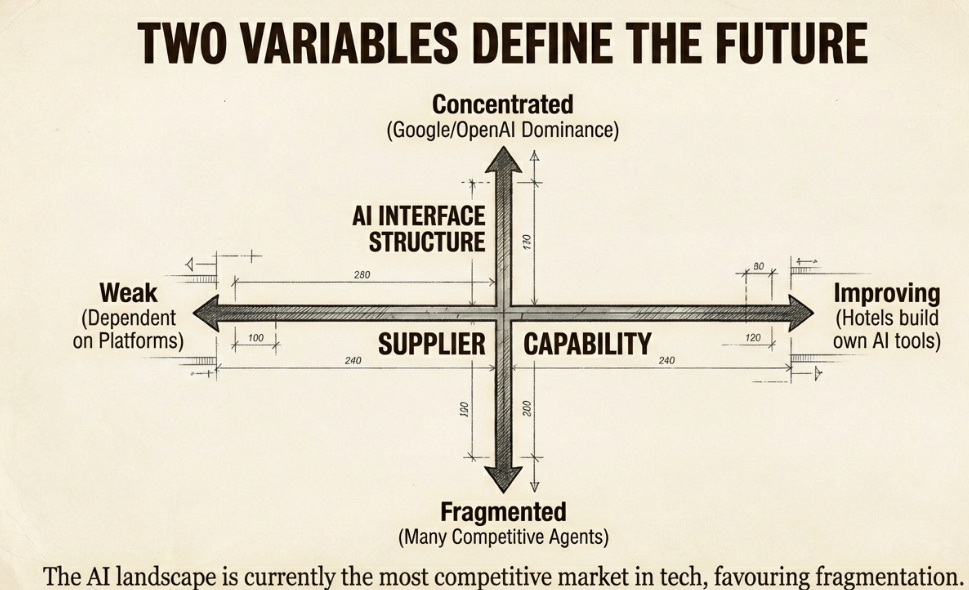

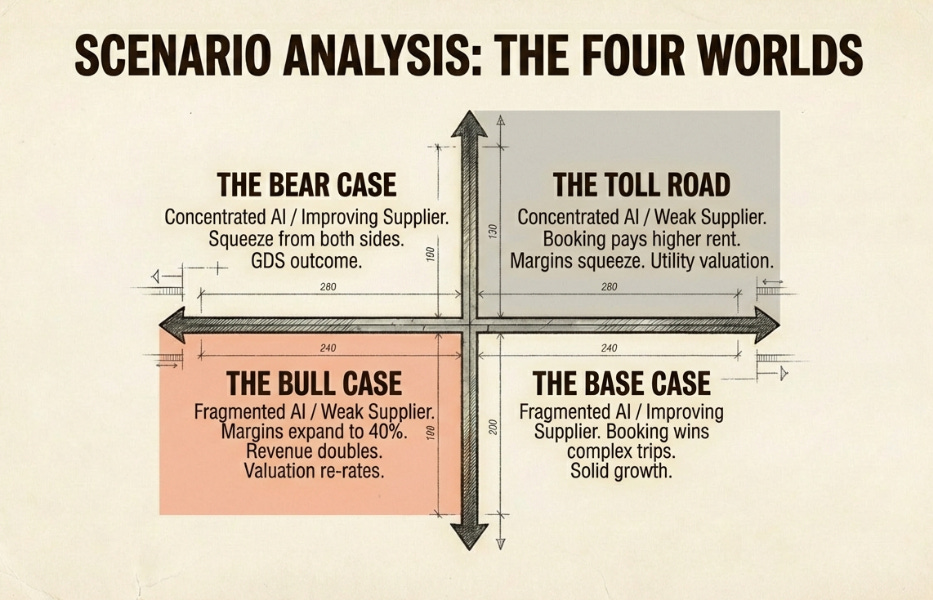

Two Variables, Four Worlds

The AI risk reduces to two variables.

First: does the AI interface concentrate (Google dominates routing) or fragment (many competing agents)? Second: does supplier-direct booking improve (hotels build competent AI-powered direct channels) or stay weak (independent properties remain dependent on platforms)?

Fragmented interface, weak supplier-direct is the bull case. Multiple agents compete for Booking’s API. No single router has monopoly pricing power. AI becomes additive demand at competitive acquisition cost. You’d see it as merchant mix climbing past 75%, marketing costs flat or declining, margins expanding.

Fragmented interface, improving supplier-direct is the base case. Booking wins for complex trips but faces modest pressure as some suppliers build competent direct channels. You’d see room nights growing but revenue-to-bookings ratio drifting down. The business stays strong but the upside gets capped.

Concentrated interface, weak supplier-direct is the toll road. Booking remains essential but pays higher rent to the dominant router. You’d see marketing spend trending up structurally, management talking about “opportunistically leaning in” more frequently, code for “we must pay the gatekeeper.” Margins squeeze from above.

Concentrated interface, improving supplier-direct is the bear case. Booking gets compressed from both sides. Take-rate compression becomes visible. Merchant mix stalls. The GDS outcome.

The stock, at roughly 16 times forward earnings, is pricing the toll road or worse. I think we’re heading for the first or second world. The evidence supports this, and so does the market structure.

The AI interface landscape is the most competitive market in technology. Google, OpenAI, Apple, Microsoft, Amazon, Meta, and vertical specialists are all building agent platforms. A fragmented ecosystem, where Booking is an API partner for all of them, could actually reduce acquisition costs relative to the current Google monopoly on search-driven travel demand.

And Google specifically, the only player with the assets to potentially concentrate the interface, has had Google Pay, Google Flights, and Google Hotels for over a decade without ever going downstream into transaction execution. This isn’t an oversight; it’s a revealed preference. Google’s organizational DNA is built around monetizing information at 55–60% margins. Becoming the merchant-of-record for global travel would mean building a 25–35% margin operations business inside a company whose identity rejects exactly that kind of work. It’s the same reason Apple has Apple Pay but has never become a bank. Google could do this. Google almost certainly won’t.

The Rebundling

There’s a deeper structural story that explains why the execution layer is getting more valuable, not less.

Travel was unbundled by the internet, flights on one site, hotels on another, cars on a third. This was efficient for simple trips but imposed all coordination on the consumer. If your flight is delayed, the hotel doesn’t know.

Connected Trip is the rebundle. Not cross-selling, an integrated experience where the platform manages interdependencies between components. Booking’s “Autonomous Rebooking” detects a disruption and rebooks across multiple components without human intervention.

This pattern, unbundling followed by rebundling around a new integration point, is one of the most reliable dynamics in technology. Music was unbundled by iTunes into individual songs, then rebundled by Spotify into a subscription that added playlists and podcasts, because coordinating your own library across platforms cost more than a single subscription. Office productivity was unbundled by Google Docs and Slack and Zoom, then rebundled by Microsoft into Teams-plus-365, because managing seven collaboration tools was worse than one integrated suite. In each case, the rebundler won by owning the integration layer.

Travel is following the same arc. And the integration point is the merchant-of-record infrastructure. You can’t coordinate cancellation policies across four verticals as a commission-collecting middleman. You can’t fund Genius loyalty discounts through float income and payment spreads if you don’t process the payment. The merchant model at 70% is what makes rebundling viable, and rebundling is what makes the execution layer defensible.

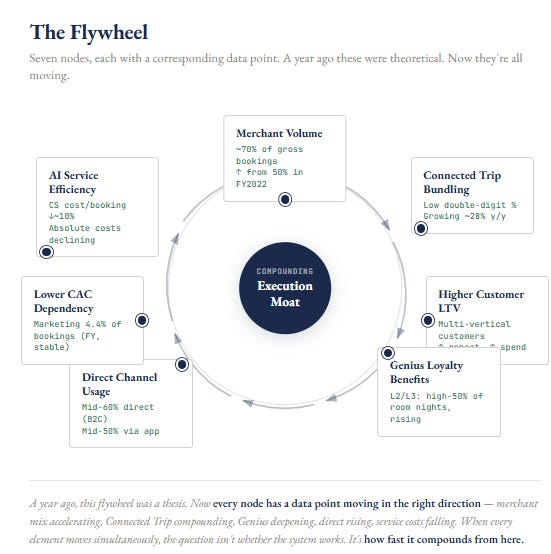

The flywheel is now visible in the data: merchant volume enables Connected Trip bundling, which increases lifetime value, which funds Genius benefits, which drives direct channel usage (now mid-60% of consumer bookings, app at mid-50% of room nights), which reduces dependence on external demand sources, while transaction data trains AI service models that reduce cost per booking. A year ago, these loops were theoretical. Now each has a corresponding data point moving in the right direction, merchant mix from 50% to 70% in two years, Connected Trip growing nearly 30%, Genius top-tier members in the high-50% of room nights, and service costs declining in absolute terms for the first time.

The Thesis, Updated

Previously: Booking is becoming a fintech company disguised as a travel platform.

Now: Booking is the transaction infrastructure that both humans and AI agents need to execute travel. The market is pricing it as if that infrastructure is at risk of replacement. The evidence says it’s becoming more essential.

What the Stock Is Worth in Three Years

In my Q3 piece, I laid out a bull case of $12,000–$15,000 when the stock was around $5,200. Two things have changed: the stock fell 24%, improving the entry point dramatically, and my framework now explicitly accounts for the toll road risk rather than treating it as a tail event.

The bull case, fragmented AI, weak supplier-direct, has revenue compounding in the low-teens, margins expanding toward 40%, and the market re-rating Booking as transaction infrastructure rather than cyclical travel. Roughly a double from here: $8,000–$10,000 by 2028. Lower than my Q3 target because I now give the toll road 25–30% probability rather than dismissing it.

The base case, fragmented AI, improving supplier-direct, has revenue growing in line with management’s algorithm, margins holding as efficiency offsets competitive spend. Stock: $5,500–$6,500. A solid return. The Q3 adjustment: I hadn’t priced in supplier-direct improvement capping the upside even in a fragmented AI world.

The bear case, Google dominates routing, has marketing costs rising structurally, margins compressing, and a utility-like multiple. Stock: $3,400–$4,300. Essentially flat. This is the scenario already priced in.

The asymmetry: the bear case delivers a flat return, the base case delivers 30–50% upside, and the bull case delivers a double. Two of three scenarios pay you, and the one that doesn’t is already in the stock.

A Prediction

Structural analysis without a falsifiable claim is storytelling.

Over the next two to three quarters, merchant mix will move toward 75%, Connected Trip penetration will reach the mid-teens, and marketing as a percentage of gross bookings will hold near 4.4%. If that happens, the router tax fear is overstated and the 24% drawdown was narrative ahead of evidence. If marketing cost rises above 5% while revenue growth lags gross bookings growth, the toll road is real and the multiple compression is justified.

The metrics that will tell the story, in order of importance:

Merchant mix is the tiebreaker. It was 50% two years ago, 63% a year ago, 70% now. In my Q3 piece, I set 75% as the Q4 bull target, it came in at 70% for the full year, likely 72–73% in Q4 specifically. Progressing but not there yet. If it stalls at 70–71%, the supply-side lock-in story has a crack. If it pushes toward 75% by mid-2026, the thesis is not just intact, it’s accelerating.

The most important new metric, one I didn’t even flag in Q3, which was a gap in the framework, is the cost of acquiring a customer through an AI agent versus Google Search. That single number resolves the entire debate. If AI-sourced bookings arrive at lower CAC, the first world is playing out. If higher, the toll road is confirmed. Every quarter of silence extends the uncertainty discount.

Beyond those two: Connected Trip needs to reach mid-teens penetration to prove the rebundling thesis at scale. Marketing as a percentage of gross bookings held at 4.4% for the year, management framed the Q4 uptick to 4.5% as deliberate investment, but the distinction only holds if it doesn’t keep rising. Customer service cost per booking fell roughly 10% via GenAI this year; that margin buffer needs to persist because it’s the hedge against a potential toll increase. And the $700 million reinvestment in 2026 needs to generate the promised $400 million in incremental revenue, if it doesn’t, management’s capital allocation discipline comes into question.

Each metric maps to the four worlds. In the first, they all move right simultaneously. In the fourth, they all deteriorate. The most likely outcome is mixed signals, and merchant mix is the tiebreaker.

The answer won’t come from AI demos or partnership announcements. It will come from the income statement.

It always does.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.