Broadcom 2QFY26: The Phase Transition

The quarter disappointed the stock, but strengthened the case for Broadcom as AI’s industrial layer.

TL;DR

Broadcom’s quarter was not weak. It was strong versus reported numbers, but not strong enough versus the buy-side AI bar that had moved ahead of consensus.

The prior thesis still holds: Broadcom is not a normal semiconductor cyclical. AI scale makes its custom silicon, Ethernet networking, SerDes, optics, packaging, supply-chain execution, and VMware cash engine more valuable.

What changes after 2QFY26 is the framing. Broadcom is not the prime contractor for the rack. It is the industrial silicon and networking layer that makes other people’s AI infrastructure deployable, and increasingly financeable.

The Hardest Updates

The hardest earnings updates are not the ones that prove you wrong. Those are easy. The facts change, the thesis breaks, and the only honest response is to move on.

The harder updates are the ones where the thesis was mostly right, but the market caught up, the language became too easy, and the metaphor started doing more work than the evidence could support.

That is where Broadcom is after 2QFY26.

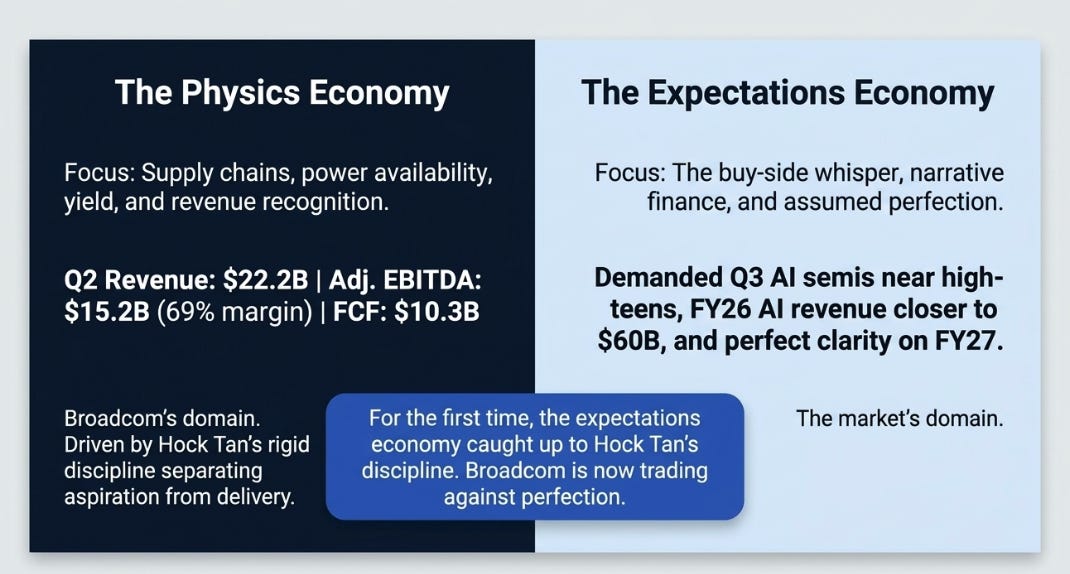

Across our previous Broadcom work, the central idea was that Broadcom lived in the physics economy while much of AI investing lived in the narrative economy. The narrative economy runs on frameworks, partnerships, press releases, optionality, and the emotional value of being adjacent to the next AI model. The physics economy runs on supply-chain allocation, packaging capacity, purchase orders, delivery schedules, power availability, yield, and revenue recognition.

Hock Tan’s great advantage was that he refused to confuse the two. When the market wanted OpenAI’s 10GW framework to become near-term revenue, he clarified that it was not. When investors wanted every AI announcement to sound like contracted backlog, he separated aspiration from delivery. That honesty was punished at first. Then it became credibility.

In December, Broadcom was punished because the market did not appreciate the discipline. In March, Broadcom was rewarded because the market finally did. In June, the same discipline created a different problem: investors had moved from disbelief to expectation.

Broadcom did not stop being the physics economy. The issue is that, for the first time, the expectations economy caught up.

The Twelve-Quarter Contract

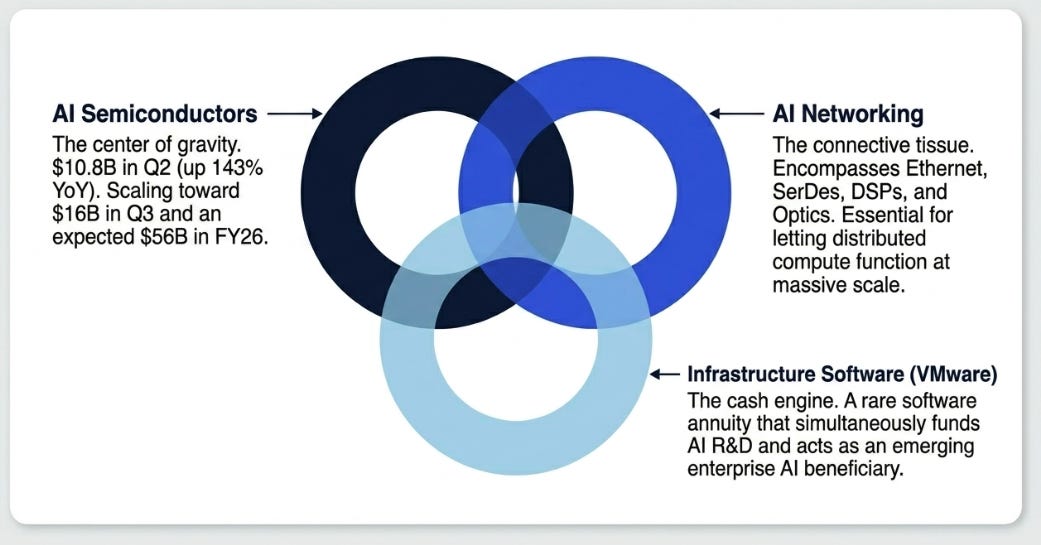

This was a strong quarter by any normal standard. Revenue reached a record $22.2 billion. Adjusted EBITDA was $15.2 billion, or 69% of revenue. Free cash flow was $10.3 billion. AI semiconductor revenue reached $10.8 billion, up 143% year-over-year. Q3 AI semis are guided to $16 billion. FY26 AI semis are expected around $56 billion. FY27 remains above $100 billion.

Those numbers would have seemed absurd two years ago. Yet the stock sold off sharply.

The reason is simple: Broadcom was no longer trading against normal standards. It was trading against the AI whisper. The market wanted Q2 AI semis above the buy-side bogey, Q3 AI semis closer to the high-teens, FY26 AI revenue closer to $60 billion, and a cleaner reason to believe FY27 was not merely above $100 billion but materially above it.

Instead, investors got a good quarter, a good guide, a reiteration of FY27, a messy call, a comment about Google source diversity, and a clarification that Broadcom is not selling racks.

That explains the stock. It does not fully explain the company.

The expectations miss matters because stocks trade on expectations. But the deeper question is whether the structure of AI compute demand is changing in a way that makes Broadcom more valuable over time. This is where the quarter may have revealed more than the market reaction suggested.

From Capex Cycle to Financeable Infrastructure

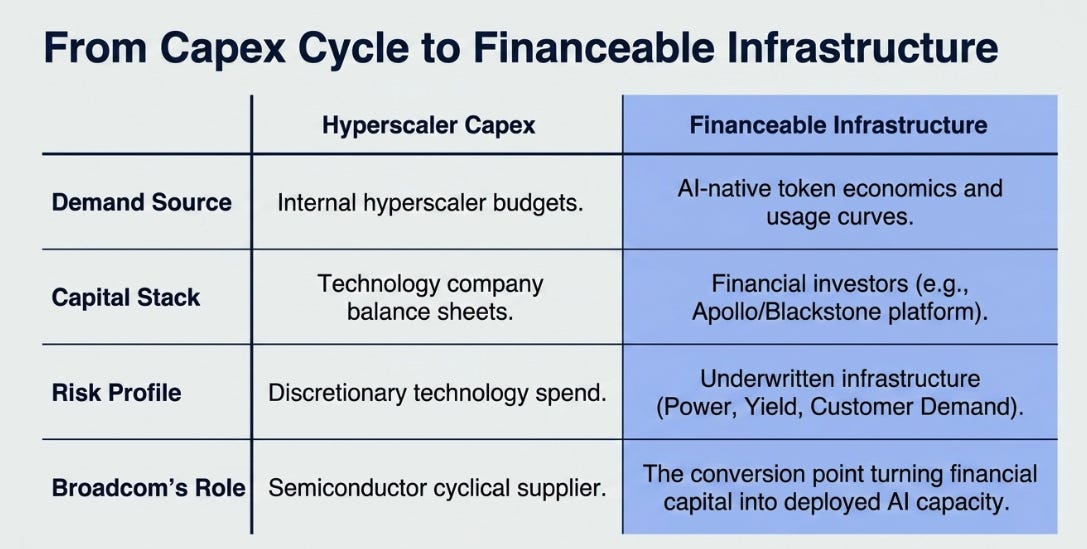

For most of the last three years, AI compute demand has been understood as a hyperscaler capex cycle. Google, Microsoft, Amazon, Meta, and a few others decided how much to spend. Everyone else in the AI supply chain lived beneath that decision. If the hyperscaler CFO got cautious, the order book slowed. If data-center budgets paused, semiconductor revenue paused.

That is what it means to be in a capex cycle: someone else’s budget is your demand function.

The interesting development in Broadcom’s Q2 call was that this model may be changing at the margin. Anthropic, OpenAI, and other frontier labs are not simply internal hyperscaler workloads. They are AI-native demand sources with their own usage curves, token economics, and capacity requirements. They need compute not because a hyperscaler wants to spend, but because users are consuming intelligence and that usage requires infrastructure.

The Apollo and Blackstone AI XPU platform matters because it points to a new capital stack. When financial investors help fund AI compute capacity, they are not merely buying a semiconductor cycle. They are trying to underwrite infrastructure: power, capacity, utilization, customer demand, and yield over time.

That does not make AI compute risk-free. It is still early. Token economics still need to prove themselves. Utilization matters. Power matters. Deployment timing matters. But the conceptual shift is important. AI compute is beginning to look less like discretionary tech capex and more like a financeable infrastructure asset.

Broadcom sits at the conversion point. It is not the owner of the application. It is not the consumer interface. It is not the balance sheet funding every data center. Its role is more specific and, in some ways, more powerful: it helps turn financial capital into deployed AI capacity.

That is a different kind of value than “we design good chips.” It is the value of being the industrial layer that makes the delivery schedule bankable.

What We Got Right

The structural direction was right. Broadcom is not a normal semiconductor cyclical. It is increasingly an AI infrastructure company with three connected engines: AI semiconductors, AI networking, and infrastructure software.

The quarter confirmed that AI semis are not a side business anymore. They are becoming the center of the company. It also confirmed that networking remains essential. Broadcom’s AI stack is not just custom XPUs. It is Ethernet, SerDes, DSPs, optics, PCIe, Tomahawk, Jericho, and the connective tissue that lets distributed compute function at scale.

This is the part of the thesis that remains strongest. AI does not scale like normal compute. Every new gigawatt adds coordination problems: latency, power, packaging yield, optical reach, memory bandwidth, cluster topology, supply timing, and multi-data-center synchronization. At small scale, the chip matters. At massive scale, the system around the chip matters just as much.

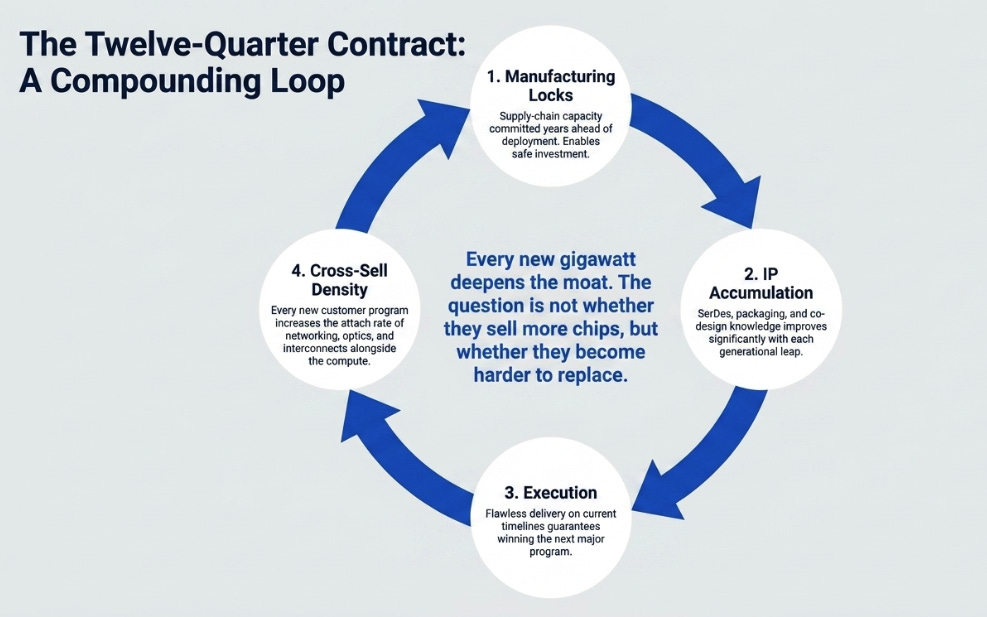

That is Broadcom’s mechanism. Every new customer program deepens three advantages. First, manufacturing locks: supply-chain capacity committed years ahead. Second, IP accumulation: SerDes, packaging, networking, and co-design knowledge that improves with each generation. Third, cross-sell density: networking, optics, and interconnects that travel with the compute.

These advantages reinforce each other. Capacity commitments enable investment. Investment improves execution. Execution wins the next program. The next program increases attach opportunities. That is the compounding loop.

The question is not whether Broadcom can sell more AI chips. The question is whether each new gigawatt makes Broadcom harder to replace.

What We Need to Correct

Honesty also requires updating the parts of the thesis that were too generous.

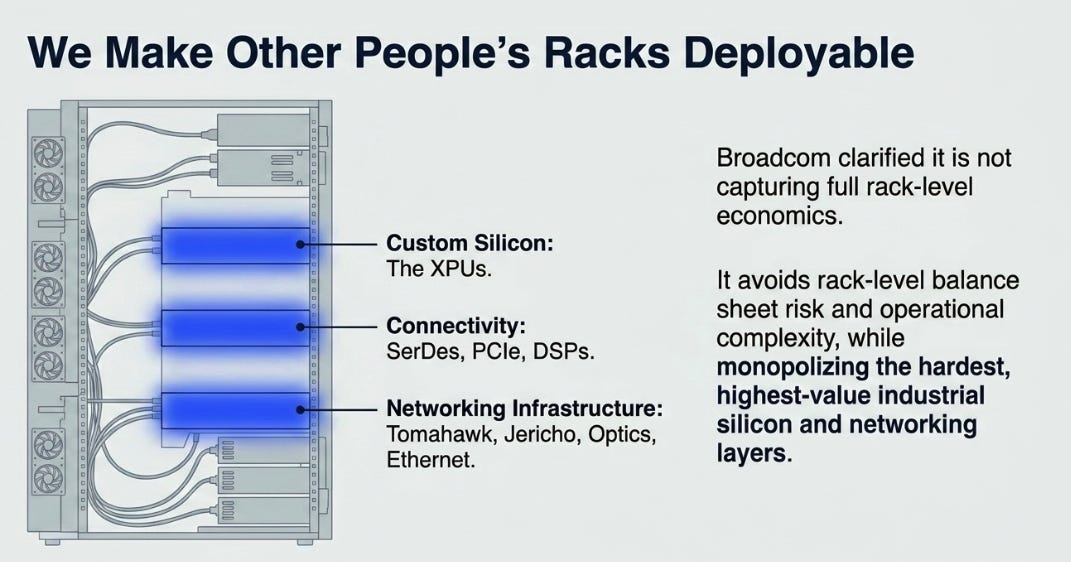

The biggest correction is the prime-contractor metaphor. In our prior work, we leaned into the idea that Broadcom was becoming the AI infrastructure prime contractor, not just selling chips, but increasingly responsible for the system. That captured something real: Broadcom does coordinate critical layers of the AI stack that customers cannot easily assemble alone.

But the metaphor went too far.

This quarter, management clarified that Broadcom is not selling full racks. It is not capturing full rack-level economics. It is in the chip business: chips, connectivity, switching, optics, and networking infrastructure.

That distinction matters. If one assumed Broadcom was capturing full rack economics, the dollars-per-gigawatt model was too generous. If one assumes Broadcom captures the hardest silicon and networking layers inside and across the rack, the thesis remains large, but cleaner.

The right framing is not that Broadcom owns the rack. The right framing is that Broadcom makes other people’s racks deployable.

That may actually be more durable. It avoids rack-level balance sheet risk and operational complexity, while preserving the highest-value silicon and networking layers. Broadcom does not need to own the full system to be essential to the system.

We pushed the metaphor too far. The insight survives, but the model has to be cleaned up.

Google Diversification

The Google comment matters. It is the cleanest new bear hook.

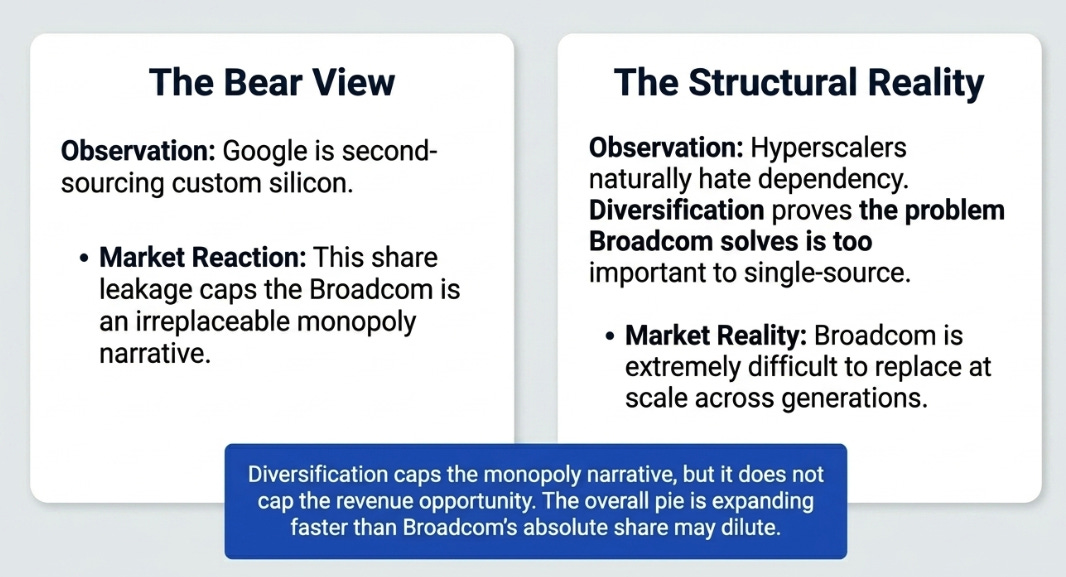

Broadcom’s longest and most important custom silicon relationship is not immune to second sourcing. That should not surprise anyone. Hyperscalers hate dependency. The more important AI infrastructure becomes, the more rational it is for Google to diversify across vendors, internal programs, and alternative SKUs.

This weakens the easy version of the bull case. The easy version said Broadcom was irreplaceable. The more accurate version is that Broadcom is very difficult to replace at scale, across generations, in the most complex parts of the roadmap.

That is still a powerful position. But it is not the same as monopoly.

The nuance is important. Google diversification is not evidence that Broadcom is irrelevant. It is evidence that the problem Broadcom solves has become too important to single-source. The bear case is that Broadcom’s share is capped. The bull case is that the pie is expanding fast enough for Broadcom’s dollars to grow even if share is not absolute.

Diversification caps the monopoly narrative. It does not automatically cap the revenue opportunity.

Networking: Inseparable, Not Bigger

We also need to refine the networking thesis.

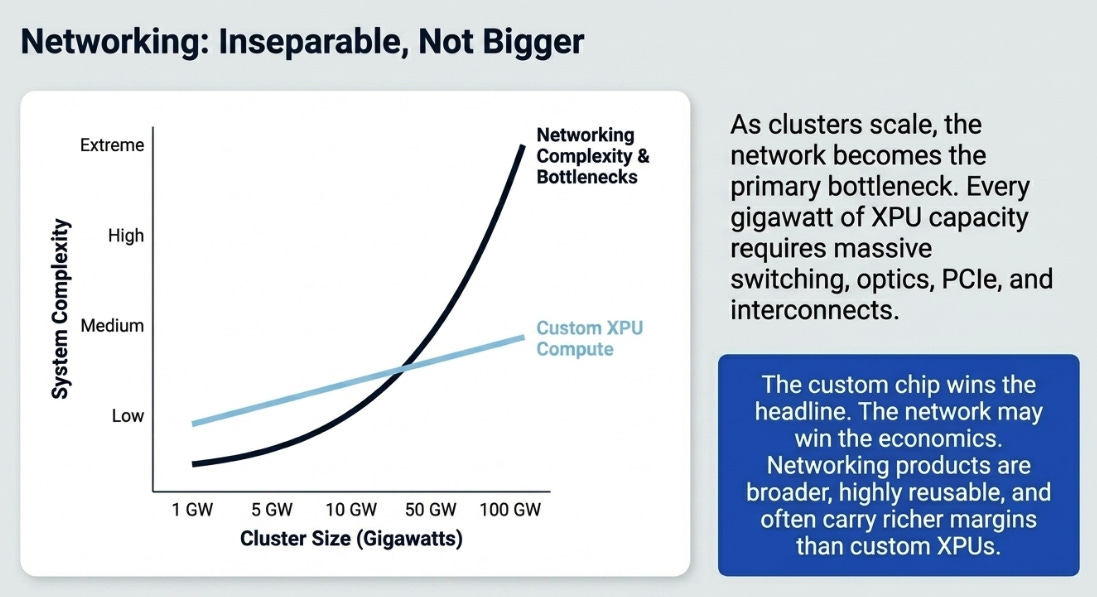

Our prior work was directionally right that AI networking is the hidden asset. The market tends to focus on XPUs because custom accelerators are easier to understand. But as clusters scale, the network becomes the bottleneck. The more distributed the compute, the more valuable the fabric.

The correction is that networking does not need to become larger than compute to be the moat. It only needs to become inseparable from compute.

Every gigawatt of XPU capacity requires switching, optics, SerDes, DSPs, PCIe, and interconnect. Those products are broader, more reusable, and often richer margin than the custom XPU itself. They also make Broadcom less dependent on any single customer’s accelerator architecture.

The custom chip wins the headline. The network may win the economics.

VMware’s Second Act

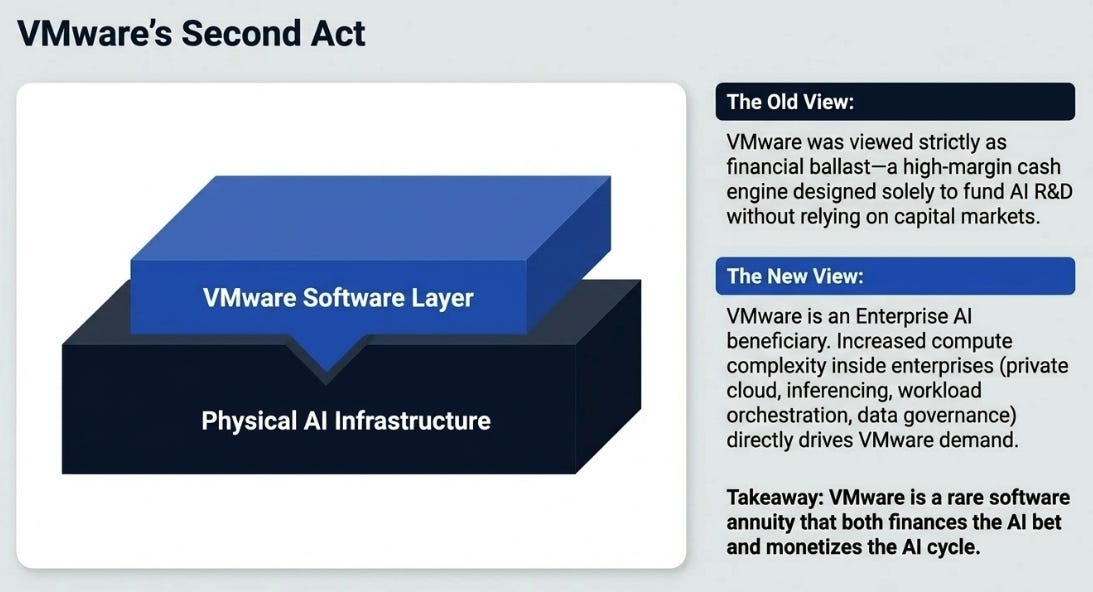

The software business was supposed to be the ballast. It was the high-margin cash engine that let Broadcom fund AI R&D without relying on capital markets or narrative finance.

This quarter suggests something more interesting: VMware may also become an AI beneficiary.

That sounds counterintuitive because VMware is not what investors think of when they think of AI. But enterprise AI is not only frontier model training. It is private cloud, inferencing, data governance, workload orchestration, security, and infrastructure control. AI agents also increase compute complexity inside enterprises. More CPU cores, more heterogeneous workloads, more need to manage private infrastructure, that is not bad for VMware.

This does not make VMware the main growth story. AI semis are still the growth story. But it gives Broadcom something rare: a software annuity that both funds the AI cycle and may participate in it.

VMware was supposed to finance the AI bet. It may now be one of the ways Broadcom monetizes AI.

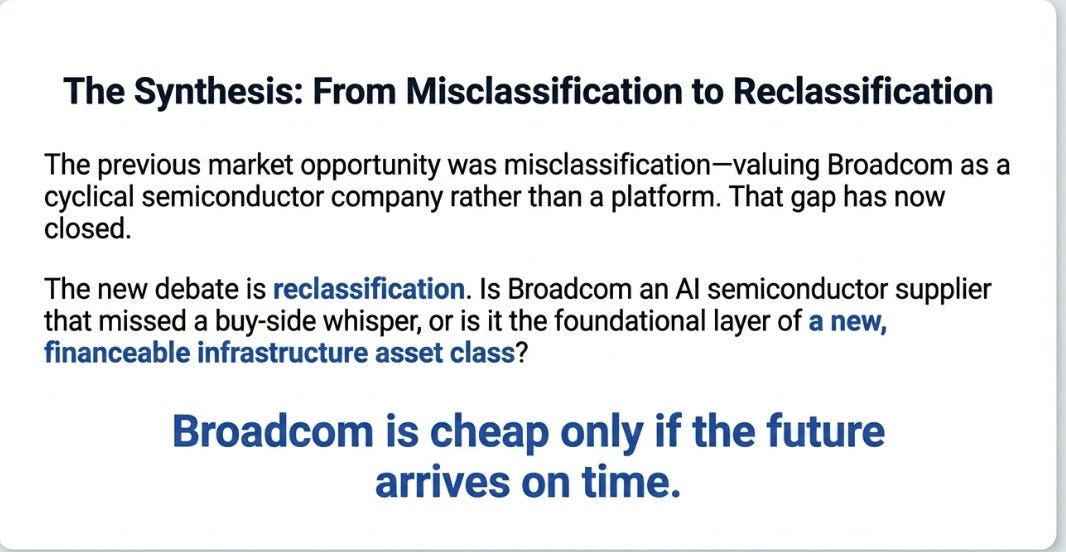

The Stock: Reclassification, Not Just Revision

This is where the investment debate has changed.

Earlier, the opportunity was misclassification. The market valued Broadcom like a cyclical semiconductor company while it was becoming an AI infrastructure platform. That gap has narrowed. The market now understands the story.

The new opportunity, if it exists, is reclassification. Is Broadcom still an AI semiconductor name that missed the buyside bogey? Or is it becoming an AI infrastructure platform whose demand is increasingly tied to financeable compute capacity, not just hyperscaler capex budgets?

That distinction matters for valuation. At roughly $386, Broadcom is not obviously expensive if FY28 and FY29 earnings are real. Bloomberg consensus already implies a dramatic ramp, with revenue moving from roughly $105 billion in FY26 to more than $220 billion by FY28 and adjusted EPS moving from roughly $11.5 to more than $25.

The bear case is not simply that AVGO is expensive. The bear case is that the out-year numbers are too high. Google share may leak. Content per gigawatt may disappoint. Customer deployments may slip. Networking mix may not offset lower-margin XPUs. Operating margin may compress.

The bull case is that FY27 is not the peak; it is the bridge. Meta, OpenAI, Anthropic, Google, and the additional customers scale into FY28 and FY29. Networking remains strategic. VMware contributes more than expected. The Apollo platform repeats. And the market reclassifies Broadcom from semiconductor cyclical to financeable AI infrastructure layer.

Broadcom is cheap only if the future arrives on time.

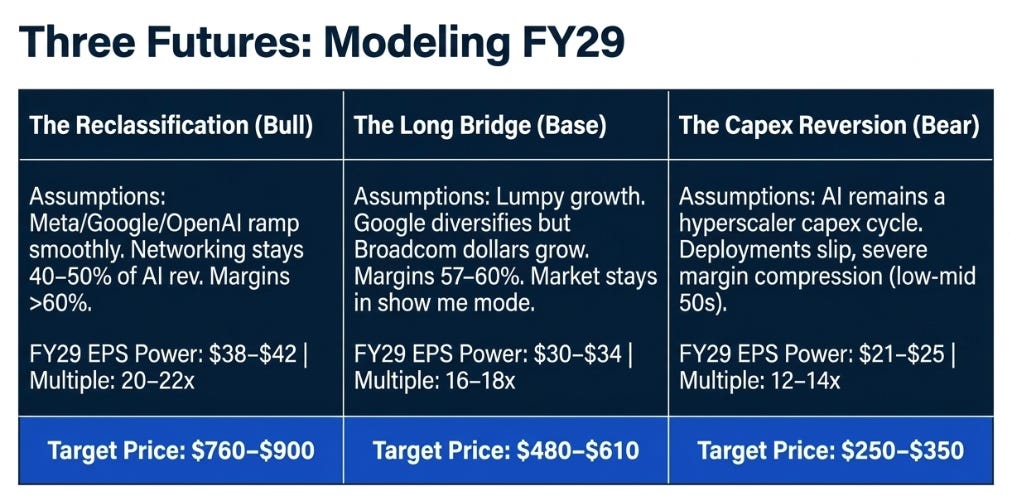

Three Futures

In The Reclassification, Broadcom is no longer treated as an AI semiconductor supplier that happened to catch a powerful cycle. It is re-rated as the industrial layer of financeable AI infrastructure. FY27 AI semis exceed $100 billion comfortably, FY28 and FY29 accelerate as Meta, OpenAI, Anthropic, Google, and the other customers ramp together, networking stays around 40–50% of AI revenue, software grows double digits, and operating margin remains above 60%. That could support FY29 EPS power of $38–42. At 20–22x, the stock could be worth $760–900.

In The Long Bridge, the thesis works, but it takes longer than the market wants. FY27 lands around the $100 billion-plus target, FY28 grows but with lumpiness, Google diversifies but Broadcom dollars still grow, networking remains meaningful, and operating margin settles around 57–60%. Broadcom remains a great company, but the market stays in “show me” mode rather than fully reclassifying the business. That could support FY29 EPS power of $30–34. At 16–18x, the stock could be worth $480–610.

In The Capex Reversion, the market decides that AI compute has not become financeable infrastructure after all. It is still a hyperscaler capex cycle, vulnerable to timing slips, customer concentration, and margin pressure. Customer deployments slip, Google share loss becomes meaningful, content per gigawatt disappoints, networking mix declines, and operating margin compresses toward the low-to-mid 50s. FY29 EPS power may be closer to $21–25. At 12–14x, the stock could be worth $250–350.

The range is wide because the business has become more powerful and more concentrated at the same time. That is usually what happens when a company moves from misunderstood to important.

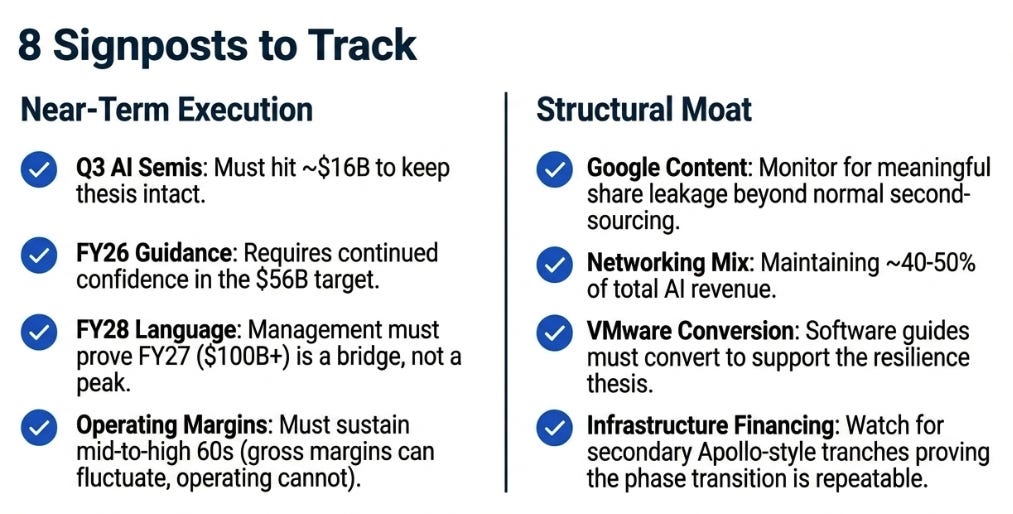

What We Track

The first signpost is Q3 AI semis. Around $16 billion keeps the thesis intact; a miss would raise timing concerns. The second is FY26 AI semis around $56 billion and continued confidence in FY27 above $100 billion. Any softening there would be thesis-level.

The third is FY28 language. The market needs to believe FY27 is a bridge, not a peak. The fourth is Google: normal second sourcing is manageable; meaningful Broadcom content loss is not. The fifth is networking mix. Around 40% of AI revenue is healthy; moving toward 50% would strengthen the margin and moat argument.

The sixth is operating margin. Gross margin can move lower; operating margin needs to remain in the mid-to-high 60s. The seventh is VMware. The Q3 software guide needs to convert because software is now part of the AI resilience thesis. The eighth is infrastructure financing. A second Apollo-style tranche would suggest the phase transition is repeatable, not one-off.

The final signpost is Hock Tan himself. The stock had been awarded a credibility premium because Broadcom was precise for twelve quarters. This quarter dented that premium. Restoring it requires a clean guide, cleaner language, and evidence that the $100 billion FY27 path is not the ceiling but the bridge.

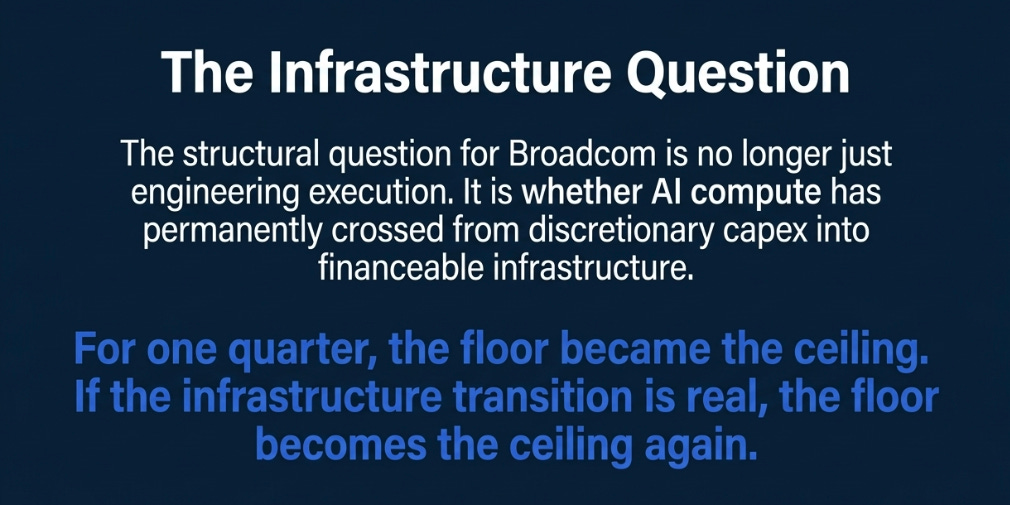

The Phase Transition

Broadcom did not stop being the physics economy. It still operates in delivery schedules, supply chains, engineering execution, and capacity commitments. But the market is no longer treating that as a secret.

The old opportunity was that investors misunderstood what Broadcom was becoming. The new opportunity, if it exists, is that investors may underestimate what happens when AI compute becomes financeable infrastructure.

That is a harder phase. It requires less storytelling and more proof. It also creates a larger prize. Capex cycles are bounded by budgets. Infrastructure markets are bounded by demand, utilization, financing capacity, and return on capital.

Broadcom’s thesis survived the quarter. The expectations premium did not. The next question is whether AI compute has truly crossed from discretionary capex into infrastructure, and whether Broadcom is the industrial layer that makes that transition real.

The floor became the ceiling for one quarter. The structural question is whether it becomes the floor again.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.