Constellation Energy 1Q26: From Reservoir to Routing Layer

The reservoir is still the asset. The product is now the date the power arrives.

TL;DR

CEG’s product has evolved: from clean “pressure” to time-to-power, power delivered where and when AI customers need it.

Calpine turns the reservoir into a routing layer: nuclear is the anchor; gas, retail, powered land, and development make it usable.

The key test: can CEG convert its clean-firm optionality into contracted base earnings through PJM, Freestone-like deals, and sustained fleet reliability?

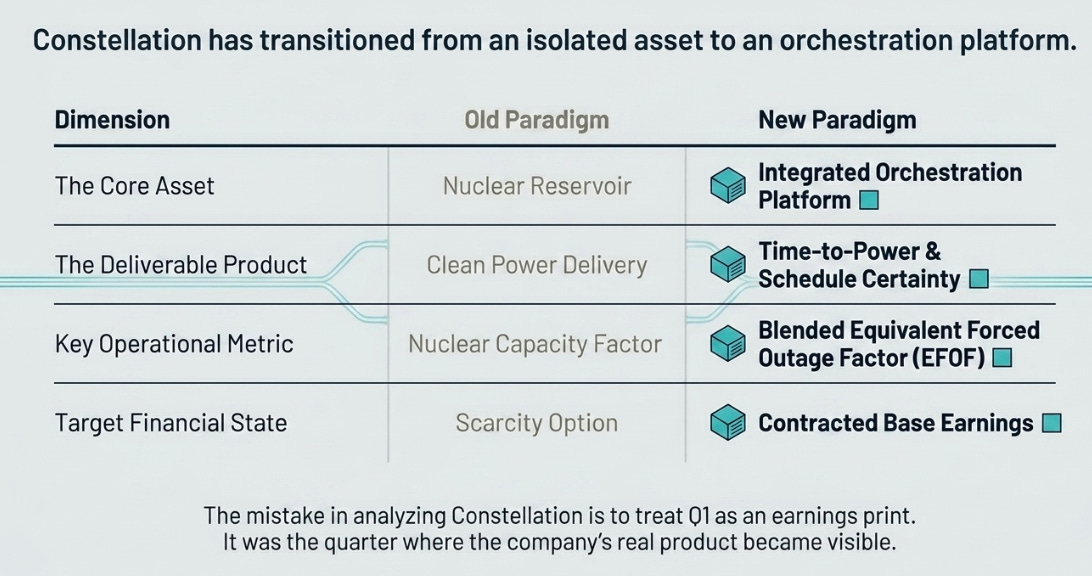

The mistake in analyzing Constellation is to treat Q1 as an earnings print. It was not. It was the quarter where the company’s real product became visible.

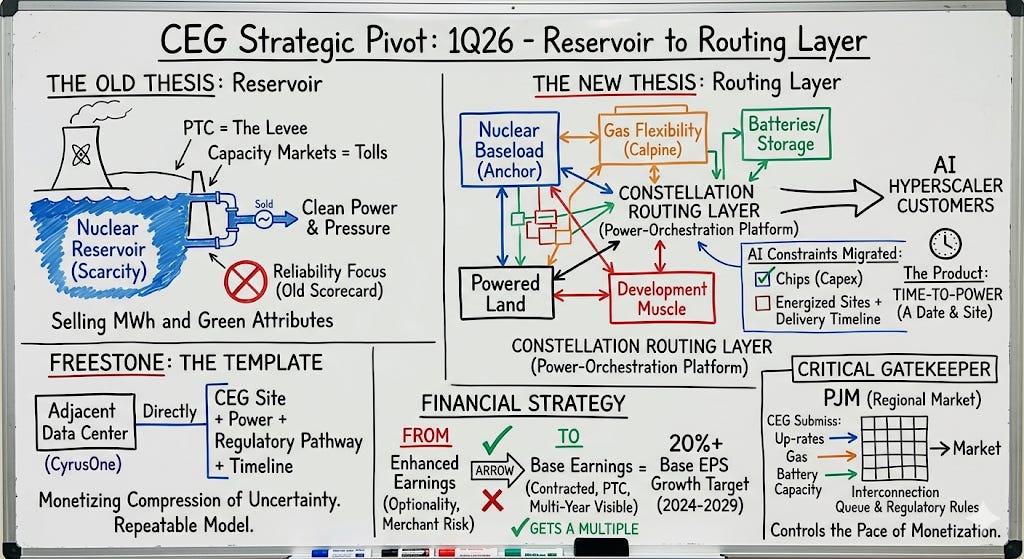

We used to say Constellation sold pressure, not power. That was right. Nuclear plants were the reservoir, contracts were the pipes, the production tax credit was the levee, and capacity markets were the tolls paid for readiness. In a grid increasingly fed by intermittent inflows, the company that could provide steady, carbon-free pressure would become more valuable. That was the core of our original thesis.

Then Calpine forced the next refinement. Constellation was no longer just a reservoir company. It was becoming a power-orchestration platform: nuclear baseload, gas flexibility, batteries, demand response, customer relationships, and structured contracts packaged into solutions that no pure-play generator could easily replicate.

Q1 sharpens the point again. The customer is not simply buying clean power. The customer is not even simply buying firm clean power. The customer is buying a date: power at a specific site, by a specific quarter, with interconnection, reliability, regulatory approval, carbon attributes, and contract structure already solved.

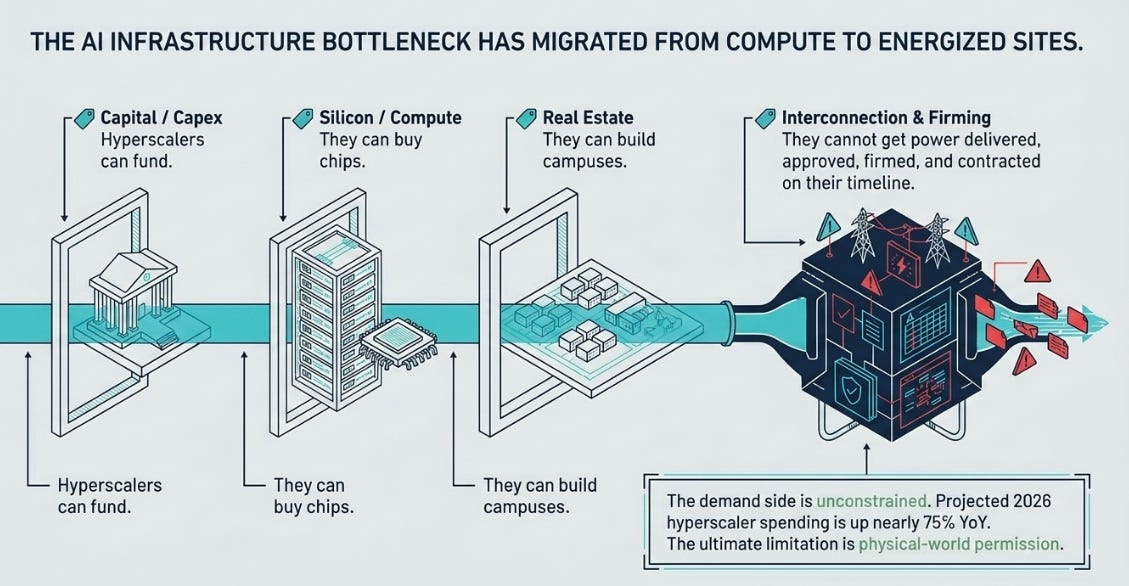

In an AI infrastructure cycle where the bottleneck has moved from chips to energized sites, time-to-power is the product. Constellation is becoming the routing layer that sells it.

The Constraint Has Migrated

Constellation reported $4.49 of GAAP EPS and $2.74 of adjusted operating EPS in Q1, up from $0.38 and $2.14 a year ago. It reaffirmed full-year adjusted operating EPS guidance of $11–$12, commissioned the 105 MW Pastoria Solar Project, brought the 460 MW Pin Oak Creek Energy Center into commercial operation, and received PUCT approval for the Freestone / CyrusOne data-center net-metering application.

Those facts establish that the quarter was fine. They do not explain why the quarter matters.

The reason it matters is that AI infrastructure is now running into a physical-world constraint. Hyperscalers can fund capex. They can buy chips. They can build campuses. What they increasingly cannot do on their preferred timeline is get power delivered, approved, firmed, attributed, and contracted at scale.

That is the key strategic shift. A clean MWh is useful. A firm MWh is more useful. But a clean, firm MWh that arrives when the customer’s construction schedule needs it is a different product altogether. That product requires generation, interconnection, land, permitting, regulatory credibility, retail structuring, and balance sheet capacity. Constellation is assembling all of those pieces.

The reservoir is still the anchor. But the value is now in routing the pressure to the customer’s deadline.

Freestone Shows the Product

The Freestone / CyrusOne agreement should be read as a time-to-power deal, not just a power deal.

Constellation signed a 380 MW agreement to connect and serve a CyrusOne data center adjacent to the Freestone Energy Center, with exclusivity for another 380 MW Phase 2. The PUCT approved the net-metering application, subject to conditions. On the call, management said construction is underway on the substation that will enable power delivery, expected in the fourth quarter.

That is the product in miniature. The customer gets a site, a power source, a regulatory pathway, and a timeline. Constellation gets to monetize not just energy, but compression of uncertainty.

This is why Freestone is more important as a template than as a single project. The premium is not only for the megawatt-hour. It is for taking a multi-year grid-access problem and turning it into something a customer can plan around. That is what AI infrastructure buyers actually need.

The next version of the CEG thesis should therefore be more precise than “AI needs clean power.” AI needs power on time. Constellation’s advantage is that it can increasingly sell the schedule.

Calpine Added the Routing Layer

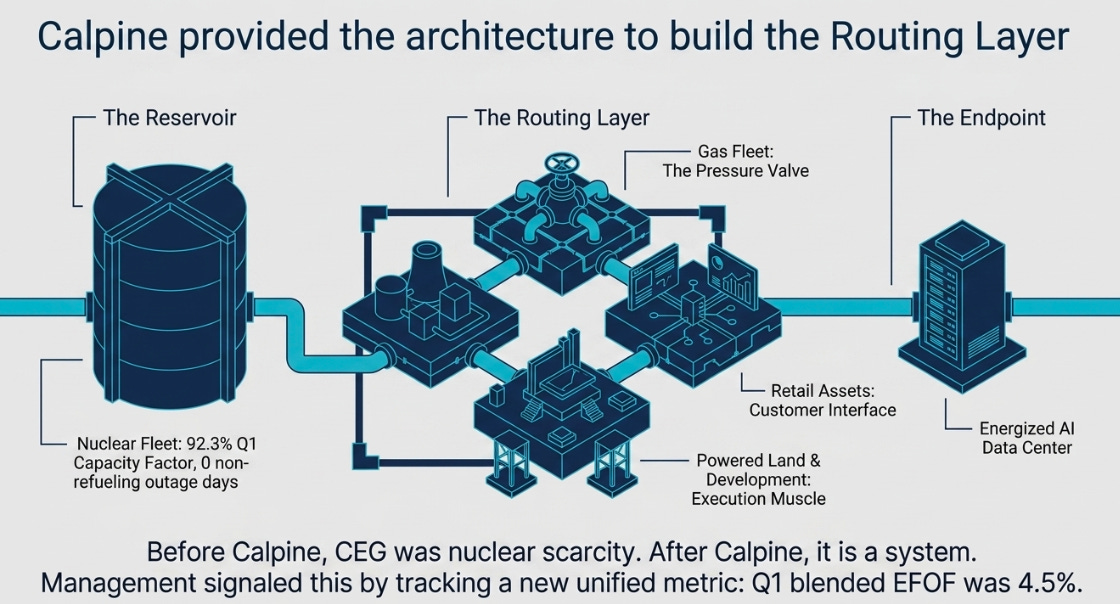

Calpine’s immediate contribution showed up in earnings. Management said higher Q1 earnings were mostly attributable to Calpine, and that full-year guidance includes roughly $2/share of Calpine accretion. But the strategic value of Calpine is not the accretion. It is the architecture.

Before Calpine, Constellation’s story was mostly nuclear scarcity. After Calpine, Constellation can package nuclear baseload with dispatchable gas, geothermal, retail relationships, powered land, development capability, and storage options. Dominguez made that point directly, connecting Calpine’s natural gas, solar, battery storage, and natural-gas data-center capabilities to Constellation’s ability to unlock the value of the combined nuclear and gas fleet.

This is the difference between owning an asset and owning a system. Nuclear is the reservoir. Gas is the pressure valve. Retail is the customer interface. Development is the execution muscle. The balance sheet funds the next pipe. The routing layer is the integration of those parts.

The new operating metrics reinforce the point. Constellation now treats Equivalent Forced Outage Factor as a key metric for the expanded gas, oil, and pumped-storage hydro fleet after Calpine; Q1 EFOF was 4.5%. Nuclear capacity factor was 92.3%, with no non-refueling outage days.

Companies reveal their strategic direction through what they start measuring. The old Constellation was judged primarily on nuclear reliability. The new Constellation wants investors to evaluate clean baseload and dispatchable reliability together. That is what a time-to-power platform requires.

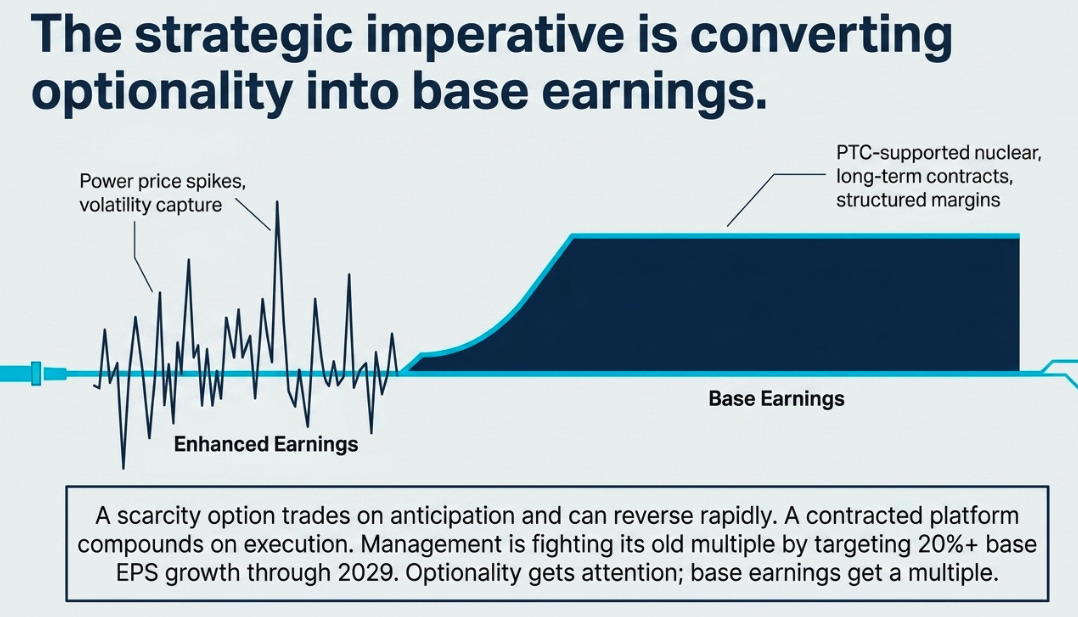

Optionality Gets Attention; Base Earnings Get a Multiple

The most important thing management is doing is not reporting earnings. It is trying to change the valuation category.

That is what the base-versus-enhanced earnings framework is about. Base earnings are the visible components: PTC-supported nuclear, long-term contracts, customer margins, contracted growth, and share repurchases. Enhanced earnings are the variable components: power prices above assumptions, commercial margins above long-term averages, gas utilization, and volatility capture. Management reiterated a long-term outlook of 20%+ base EPS growth through 2029, anchored by visible drivers including the nuclear PTC, long-term contracts, and durable customer margins.

This is management fighting its old multiple.

The 2024 AI-power narrative made Constellation exciting because its uncontracted nuclear fleet looked like a call option on hyperscaler demand. Every available MWh represented a future deal. That narrative can drive a stock up very quickly. It can also reverse when investors ask why the next deal has not arrived.

Management’s new message is better: the option still matters, but the goal is to convert the option into base. A scarcity option trades on anticipation. A contracted platform compounds on execution. Optionality gets attention; base earnings get a multiple.

This is not a retreat from the AI thesis. It is the maturation of it. Constellation is trying to make the AI story investable by moving earnings from “possible” to “contracted.” The route from one to the other is the routing layer.

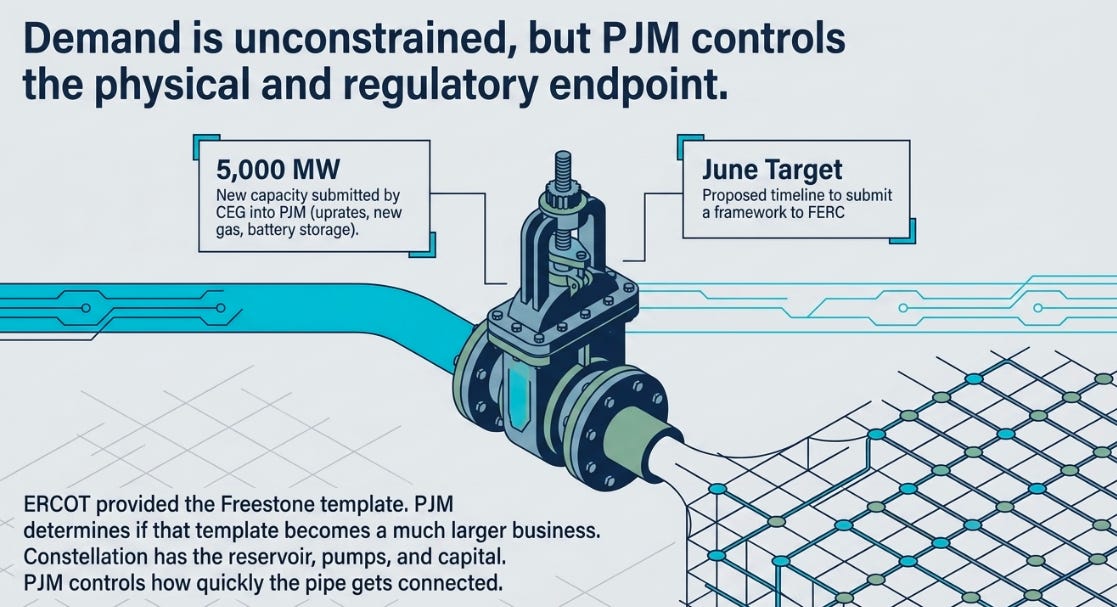

PJM Controls the Endpoint

The demand side is not the problem. Management said demand for additional compute, and therefore additional power, has not slowed; projected 2026 hyperscaler spending is nearly 75% higher than last year and still being revised upward.

The constraint is permission.

Dominguez said PJM has put forward a market-based solution to address incremental capacity needs from large-load growth, with a proposed timeline to submit a framework to FERC in June. He called the timeline “faster than we had hoped.” Constellation has also submitted about 5,000 MW of new capacity resources into PJM’s interconnection queue, including nuclear uprates, new gas generation, and battery storage.

This is the scale version of Freestone. ERCOT showed one template. PJM determines whether the template can become a much larger business.

The customer wants to turn on the tap. Constellation has the reservoir, pumps, customer relationships, and capital. PJM controls how quickly the pipe gets connected.

That is not a reason to dismiss the thesis. It is the thesis. In a regulated physical infrastructure market, the company that can navigate rules, queues, cost allocation, and customer urgency is the company that turns scarcity into cash flow.

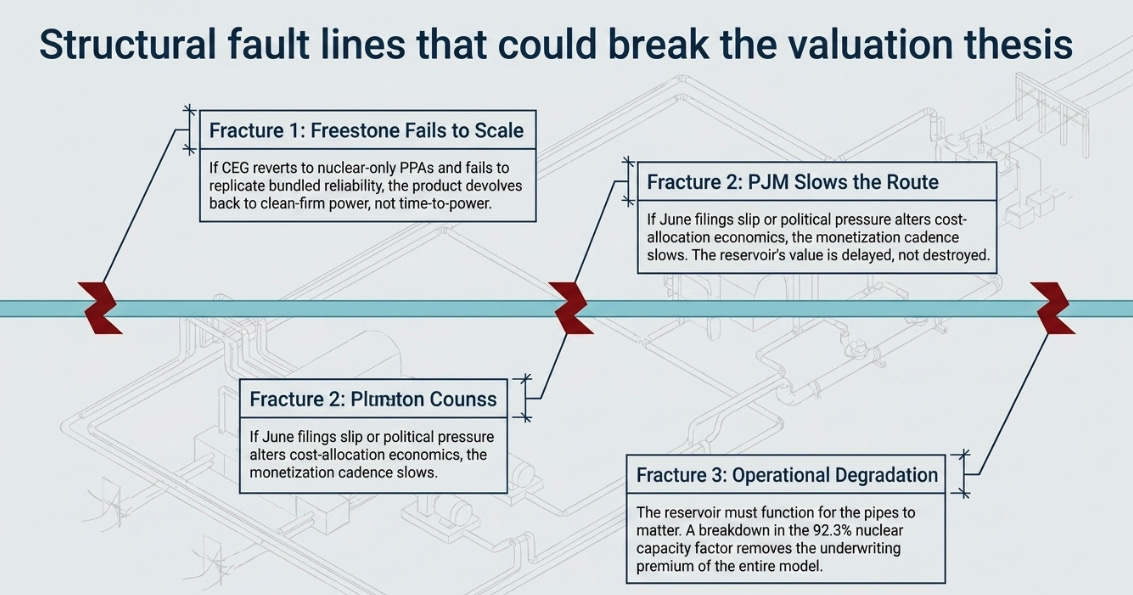

What Can Break the Thesis

There are three ways this can go wrong.

First, Freestone could remain a one-off. If Constellation signs more nuclear-only PPAs but fails to replicate powered-land or bundled reliability transactions, the routing-layer thesis is still directionally right but less valuable than we think. The product would be clean-firm power, not time-to-power.

Second, PJM could slow the route. Customer demand is real, but contracts need rules. If the June filing slips, if bilateral contracting is delayed, or if political pressure changes cost-allocation economics, Constellation’s monetization cadence slows. That would not make the reservoir less valuable. It would delay the moment when reservoir value becomes base earnings.

Third, operational excellence must hold. The reservoir has to work for the pipes to matter. Q1 nuclear capacity factor of 92.3% was acceptable given planned refueling, and there were no non-refueling outage days, but this remains the metric that underwrites the entire premium.

These are real risks, but they are risks to timing and valuation more than to the core structural shift. Power delivery has become the bottleneck. Constellation is one of the few public companies built to solve it.

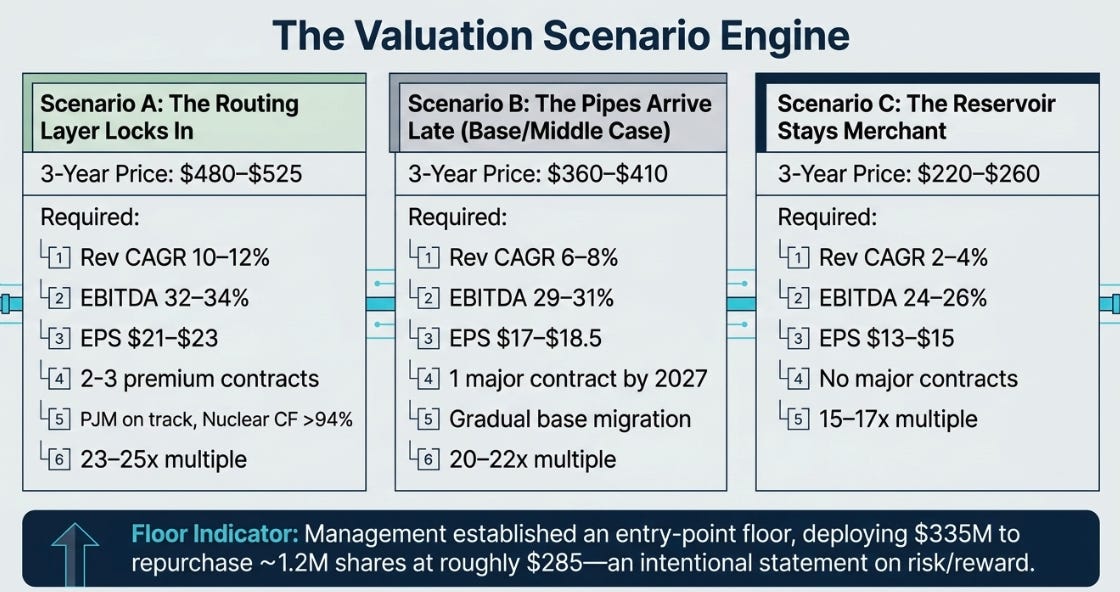

The Math, Subordinated

The valuation debate is not about next quarter’s EPS. It is about whether optionality becomes base earnings.

The middle case is no longer “merchant nuclear with upside.” It is a delayed platform: valuable, compounding, and underappreciated, but not yet fully reflected in estimates.

The entry point matters. Below $285, the risk/reward is supported by management’s own behavior: Constellation repurchased about 1.2 million shares at roughly that price, deploying $335 million, and Dominguez called it an intentional statement that the stock was a compelling use of cash.

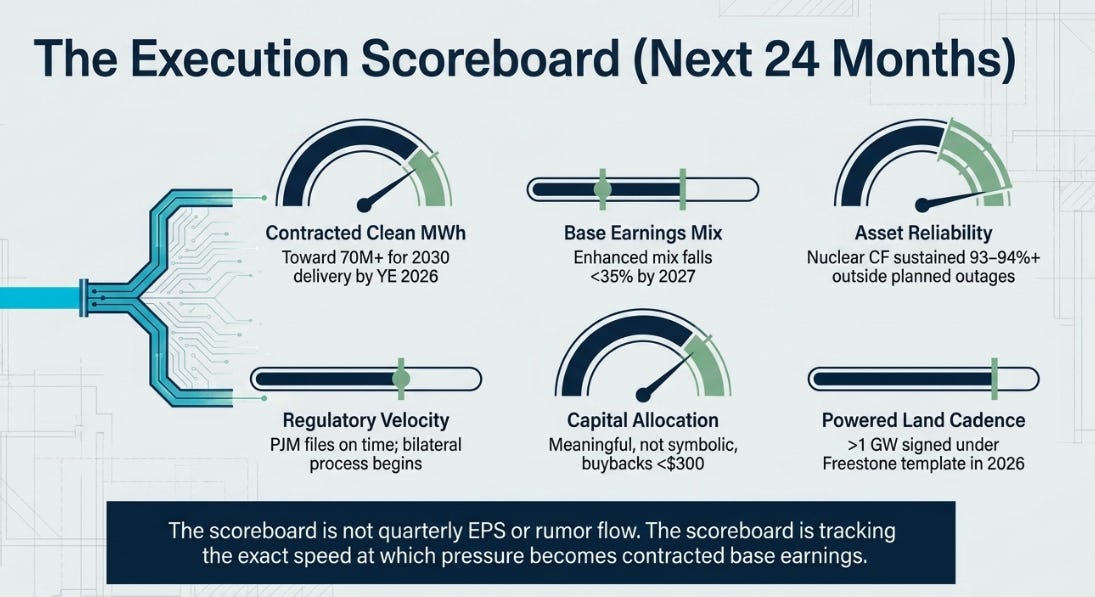

The Scoreboard

The thesis now has six practical markers.

Contracted clean MWh should move toward 70M+ MWh for 2030 delivery by year-end 2026. The enhanced-to-base mix should fall below 35% by 2027. Nuclear capacity factor should sustain 93–94%+ outside planned outage noise. PJM should file on time and allow the bilateral process to begin. Buybacks below $300 should be meaningful, not symbolic. And most importantly, powered-land cadence should accelerate: more than 1 GW signed under the Freestone template in 2026 would confirm that time-to-power is repeatable.

That is the scoreboard. Not quarterly EPS. Not rumor flow. The scoreboard is whether pressure becomes base earnings.

The Bet

The reservoir thesis is intact. Reliable clean power is more valuable than ever. Calpine made the reservoir more flexible. Freestone showed the product. PJM will determine the pace. Free cash flow gives management time: Constellation now expects $8.4 billion of free cash flow before growth across 2026–2027 and $11.5–$13 billion across 2028–2029.

Our view has evolved, but the direction is consistent. In 2025, Constellation sold pressure. In April, it became a power platform. After Q1, the sharper formulation is that Constellation sells the date the pressure arrives.

That is more valuable than power because time is now the constraint. It is also why Constellation’s advantage is widening. The company is not waiting for the AI power market to arrive. It is building the routing layer through which that demand will flow.

The reservoir is full. The pipes are no longer theoretical. The question now is how quickly the customer flow begins.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.