Constellation Energy’s 4Q25 Earnings: Second Act

Our original view was that Constellation sold pressure, not just power. Our updated view is that it is becoming something more valuable: a platform that packages clean power, reliability, flexibility,

TL;DR

We were right about the reservoir, but early on the pipes. Constellation’s nuclear fleet, PTC support, and rising capacity prices have all validated the original thesis that reliable clean power is becoming more valuable, but co-location turned out to be a slower and more regulated monetization path than we expected.

The real update is strategic, not quarterly. Calpine changes Constellation from a seller of clean power into a broader power orchestration platform: nuclear, gas, batteries, demand response, and commercial relationships can now be packaged into customer-specific solutions.

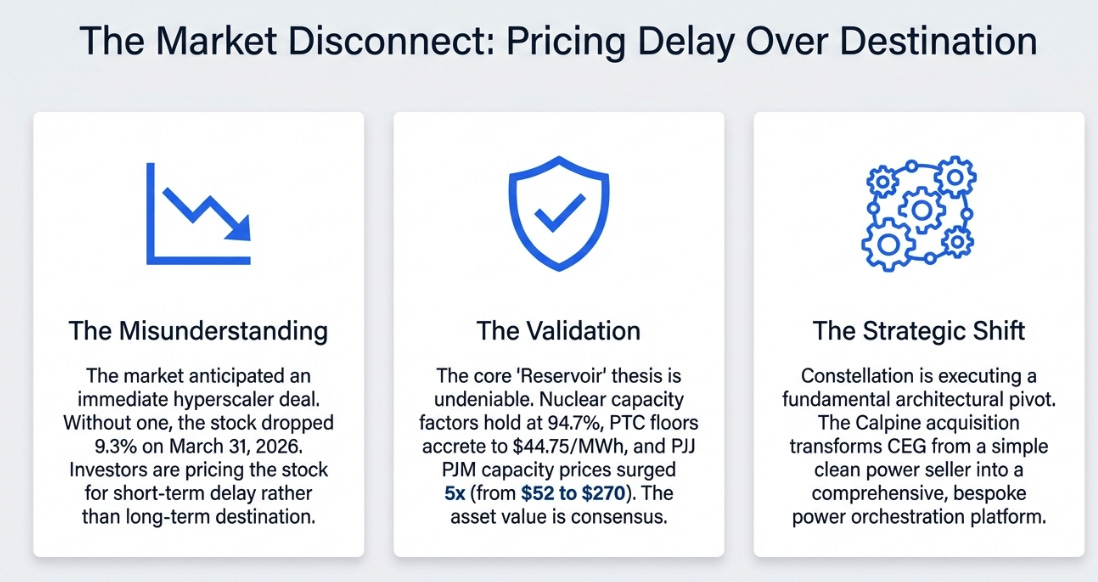

The stock is being priced for delay, not destination. The market sold the name because there was no new hyperscaler deal and 2026 guidance only met the long-term framework, but the bigger story is that Constellation’s earnings flywheel and contracting inventory are stronger than before.

“I recognize that the last time we spoke, I indicated that we expected to be done with an important transaction by this call, but we’re not ready to announce anything today.”

That was CEO Joe Dominguez on March 31, 2026, the same day Constellation Energy introduced a 20% base earnings growth commitment through 2029, authorized $5 billion in share repurchases, and laid out the most structurally sound long-term financial framework in the power sector. The stock fell 9.3%.

The market wanted a hyperscaler deal. It got a platform thesis. In the language of our previous analysis, the reservoir is fuller than we expected. The plumbing turned out to need permits nobody anticipated. The question that matters, the only question, really, is which of those two facts determines what the company is worth.

What We Got Right, What We Got Wrong

In August 2025, we published “The Reservoir Company,” arguing that Constellation wasn’t in the business of selling electricity. It was selling pressure, reliable, schedulable, carbon-free power available every hour of every day. Nuclear plants were the reservoir, long-term contracts the pipes, the production tax credit the levee that prevents the water level from falling, and PJM capacity revenues the toll paid for readiness.

That framework proved more right than we expected. Nuclear capacity factor held at 94.7%, four points above the industry average, for the second consecutive year. The PTC floor continued to accrete with inflation, reaching roughly $44.75 per megawatt-hour. PJM capacity prices in the Eastern Mid-Atlantic zone surged from $52 to $270 per megawatt-day, a fivefold increase that validates the “toll” mechanism we described. Long-term contracted clean output for 2030 delivery tripled, from 12 million to 48 million megawatt-hours. The thesis that reliable pressure would command an increasing premium is now consensus.

Where we were wrong was about the pipes. We framed behind-the-meter co-location, physically wiring a data center to a nuclear plant, as the primary monetization path. It turned out that FERC’s rejection of the Talen interconnection agreement, followed by PJM’s unworkable compliance proposal and the executive order that forced hyperscalers to renegotiate contract terms, created a regulatory thicket that made direct co-location impractical at scale. We also didn’t anticipate that the Calpine acquisition would close with DOJ-mandated divestitures of highly efficient gas plants, creating near-term earnings noise that obscured the deal’s strategic value.

Our thesis was directionally correct but the timeline was too aggressive. The value is still there, arguably more of it now. But the path to realization runs through regulatory resolution and management execution, not just asset scarcity.

The Grid as an API

The strategic development that matters most since our last writing is not any single deal or number. It’s the transformation of what Constellation actually sells.

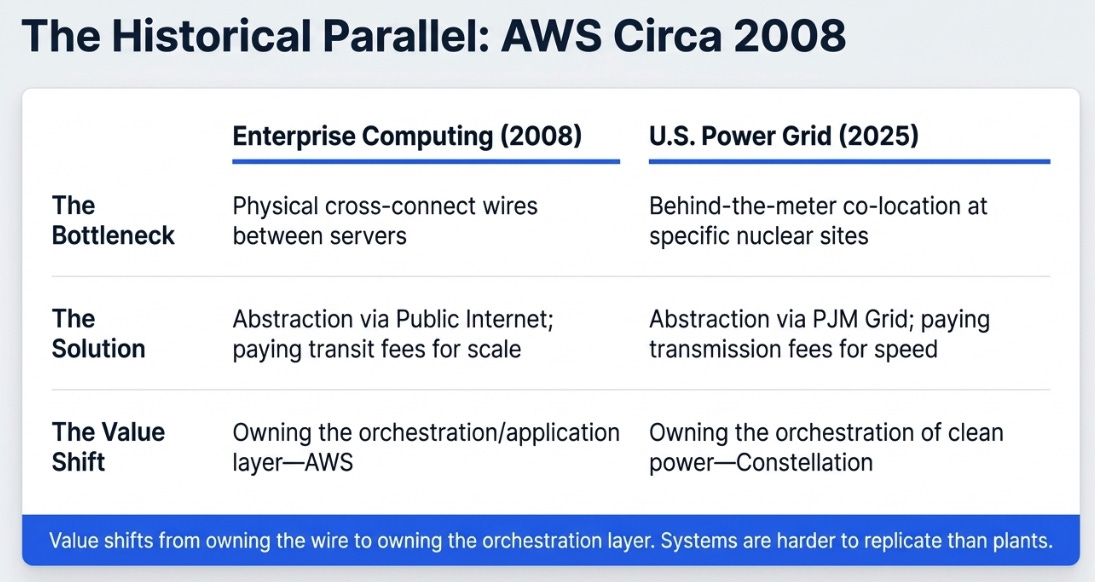

Consider an analogy from enterprise computing. In the early days, companies that needed secure, high-speed connectivity would build physical cross-connects, direct wires between their servers and their partners. It was fast, it was private, and it completely bypassed public network costs. It also couldn’t scale. Every new connection required bespoke infrastructure and manual routing.

The industry solved this by abstracting the network. Instead of physical cross-connects, companies used the public internet as a platform, paying modest transit fees in exchange for infinite speed, flexibility, and reach. The value shifted from owning the wire to owning the application that ran on it.

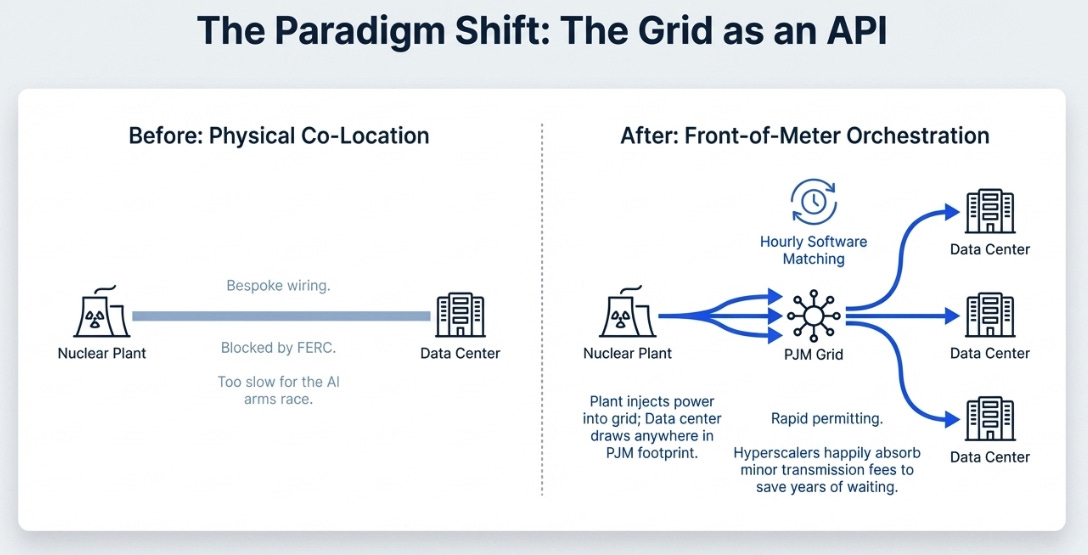

The U.S. power grid is undergoing exactly this transition, and Constellation is the company best positioned to exploit it.

Faced with a regulatory blockade on behind-the-meter co-location, Constellation is pivoting to front-of-the-meter deals that use the existing PJM transmission grid as the interconnection layer. The mechanics are straightforward: Constellation injects clean, firm power into the grid from its 180-million-megawatt-hour nuclear fleet. The hyperscaler builds its data center wherever zoning is friendly and permitting is fast, anywhere in the PJM footprint, and draws that power down. Hourly matching software verifies the clean energy delivery.

This is not a retreat from the data center thesis. It’s an architectural upgrade. Constellation can now execute deals anywhere in the grid without waiting for bespoke FERC rulings on each site. The hyperscaler pays modest transmission fees, a cost they’ll absorb willingly because their bottleneck is time, not electricity prices. In the AI arms race, waiting three years for co-location approval is far more expensive than paying grid charges.

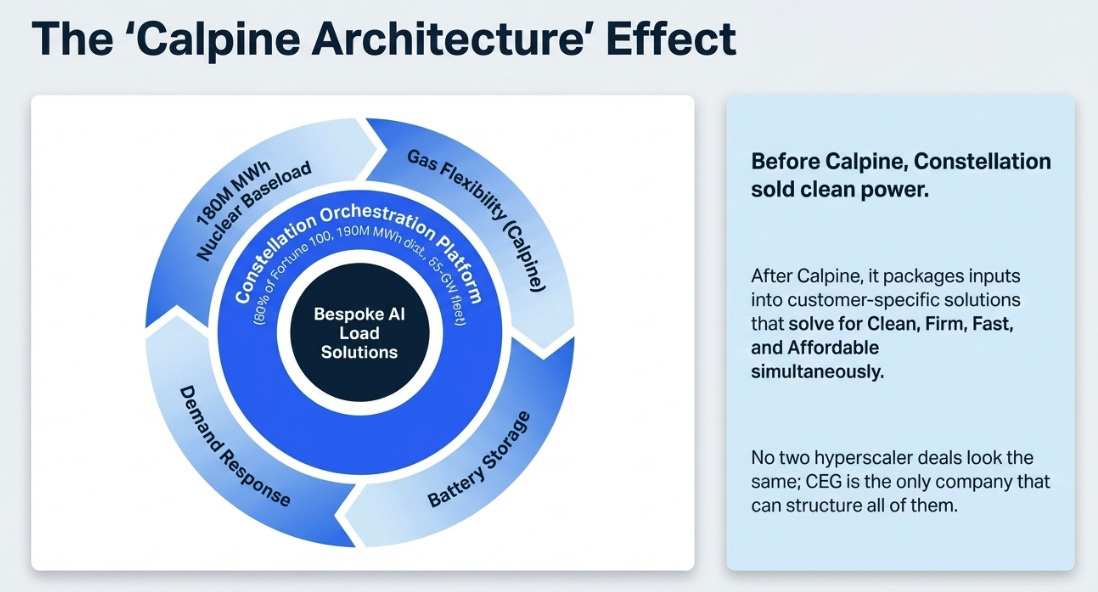

And this is why Calpine changes the company’s architecture, not just its income statement. Before Calpine, Constellation sold clean power. After Calpine, it sells orchestration, the ability to package nuclear baseload, gas flexibility, battery storage, demand response, and structured contracts into a single customer solution that solves for clean, firm, fast, and affordable simultaneously. Dominguez described this on the call: some customers want nuclear paired with batteries and demand response; others will pay for backstop capacity from PJM and buy energy and attributes directly; still others will use AI-enabled load shifting to curtail during peak hours. The point is that no two deals look the same, and Constellation is the only company that can structure all of them.

The historical parallel is Amazon Web Services circa 2008. Early cloud computing was a single product, virtual machines. AWS became dominant when it realized the real business was not selling compute, but selling a platform of services that made compute, storage, networking, and deployment work together. Once Amazon made that shift, no competitor could replicate the full stack.

Constellation is making an analogous move. The 190 million megawatt-hours of commercial distribution, the relationships with 80% of the Fortune 100, the 55-gigawatt fleet spanning nuclear, gas, geothermal, and renewables, the investment-grade balance sheet, these are not isolated assets. They are a system. And systems are harder to replicate than plants.

The Metric That Tells the Real Story

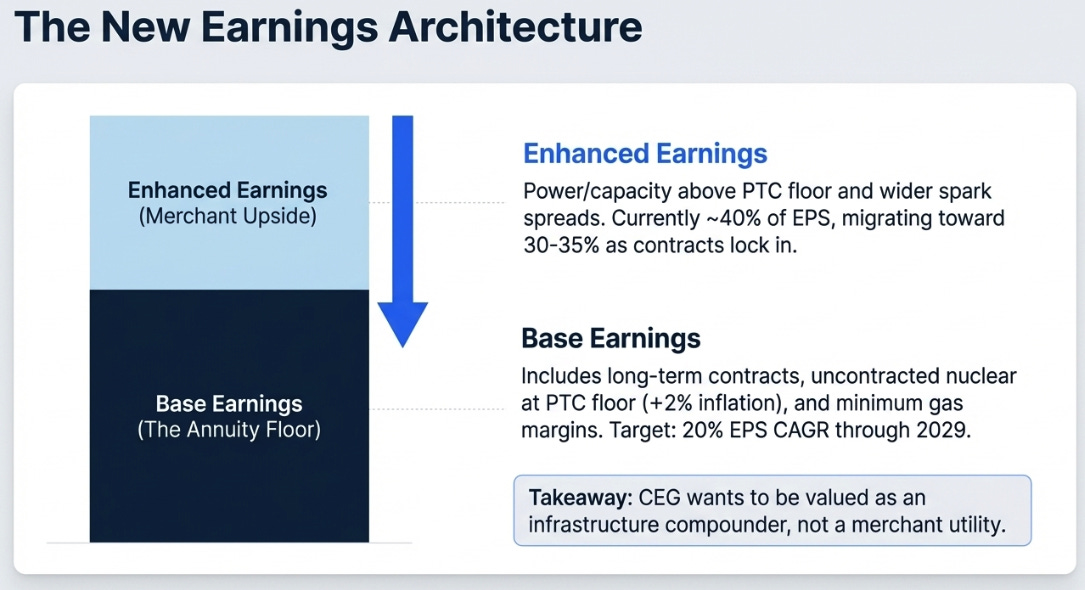

The most important thing Constellation reported was not 2025 adjusted operating earnings of $9.39 per share, or 2026 guidance of $11 to $12. It was the formalization of a new earnings architecture.

Management now wants the company understood through two lenses: base earnings and enhanced earnings. Base EPS includes long-term contracted generation, uncontracted nuclear priced at the PTC floor with 2% inflation, minimum expected gas fleet margins, and commercial margins based on a ten-year weighted average. Enhanced earnings are everything above that, power and capacity prices exceeding the PTC floor, wider spark spreads, stronger commercial optimization.

This distinction matters because it reveals what management is actually arguing. Companies introduce new metrics when they want the market to see a different business. The old Constellation was a strong merchant-contract hybrid. The new Constellation wants to be valued as a contracted platform with a durable earnings floor and a large inventory of unmonetized optionality. Management is making a re-rating argument without quite calling it one.

The argument has a lot of truth in it. The 20% base EPS CAGR through 2029 deliberately excludes every discretionary lever, the $5 billion buyback, all unannounced contracts, any inflation above 2%, and any gas fleet utilization improvement. CFO Shane Smith confirmed that free cash flow in 2028 and 2029 simply earns interest income in the projections. Management built a framework designed to be beaten, using the same playbook that has produced four consecutive years of guidance outperformance.

But here is where intellectual honesty matters. Enhanced earnings are still roughly 40% of 2026 EPS. That means the company is not yet the pure infrastructure annuity the new framework implies. It is moving in that direction, enhanced earnings should decline to 30–35% of the total over time as more contracts move into the base, but the migration is not complete. The opportunity for investors lies in whether that migration happens faster than the market expects. The risk lies in whether it stalls.

The Number That Nobody Noticed

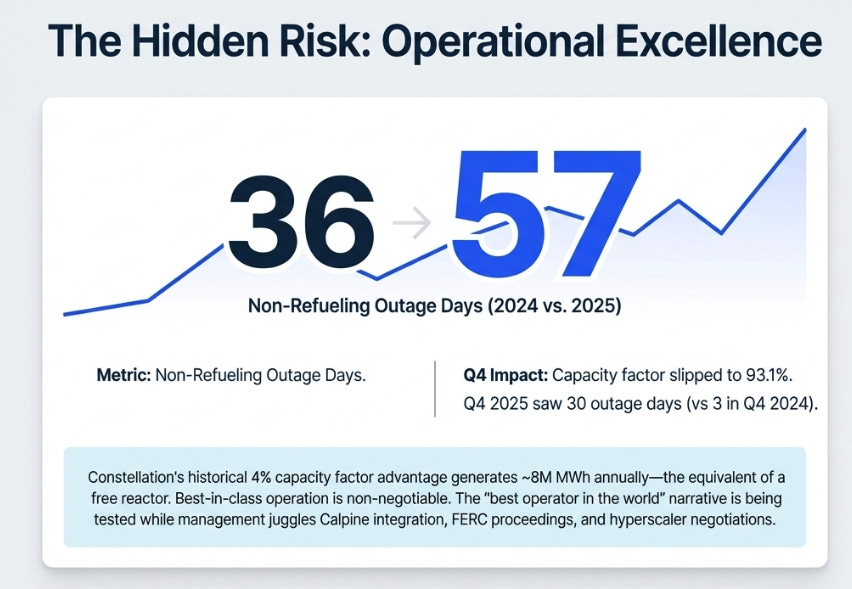

Buried in the statistics section of the Q4 earnings release is a data point that deserves more attention than it received.

In Q4 2025, Constellation’s nuclear fleet experienced 30 non-refueling outage days, compared to 3 in Q4 2024. Full-year non-refueling outage days rose from 36 to 57. The quarterly capacity factor slipped to 93.1%.

For any other company, this would be a footnote. For Constellation, it is the most important operational metric in the business. The entire thesis depends on the nuclear fleet running at best-in-class levels. Management has argued for years that their four-percentage-point capacity factor advantage over the industry translates into roughly 8 million additional megawatt-hours annually, effectively an extra reactor, generated for free by operational excellence.

One lumpy quarter doesn’t break a thesis. But the trend, 36 outage days in 2024, 57 in 2025, warrants monitoring, especially as management simultaneously integrates a $26.6 billion acquisition, restarts a shuttered nuclear plant, navigates FERC proceedings, and negotiates hyperscaler contracts. The “best operator in the world” narrative gets tested when every plate is spinning at once.

What the Reservoir Is Worth

Narrative without numbers is just storytelling. Here is what we think Constellation is worth under three realities, using a three-year horizon.

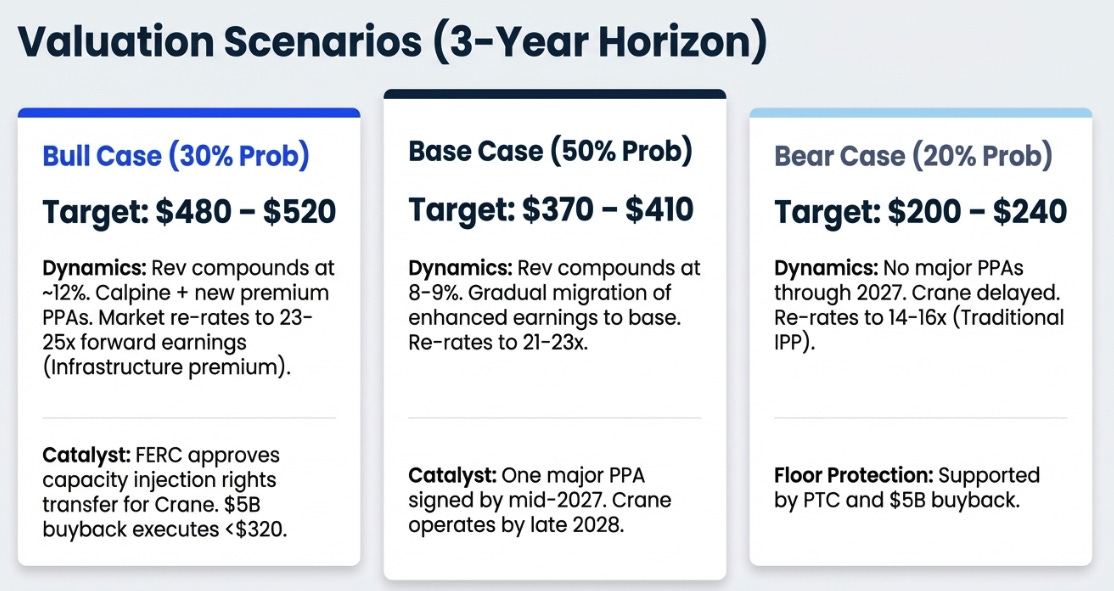

Bull case, $480 to $520 (30% probability)

Revenue compounds at roughly 12% as full Calpine contribution layers onto two or three new premium PPAs and an on-schedule Crane restart. Adjusted operating EPS reaches approximately $21 by 2028 as EBITDA margins expand past 32%, driven by base earnings dominance, rising gas utilization, and PTC inflation adjustments at 3%+. The market re-rates the stock to 23–25 times forward earnings, recognizing Constellation as an infrastructure compounder rather than a utility. The FERC approval of capacity injection rights transfer for Crane pulls forward the restart timeline. The $5 billion buyback executes at prices below $320, mechanically adding 450–500 basis points to EPS growth beyond the stated CAGR. This scenario requires regulatory resolution, hyperscaler deal execution, and sustained fleet reliability above 94%.

Base case, $370 to $410 (50% probability)

Revenue compounds at 8–9% on Calpine consolidation, modest new contracting, and organic growth. EPS reaches $17–18 by 2028 as margins expand to 29–31% and enhanced earnings gradually migrate into the base. The market values the stock at 21–23 times forward earnings, a premium to utilities but not yet full infrastructure-compounder pricing. One new major PPA is signed by mid-2027. Crane begins operations by late 2028. PJM capacity prices moderate but stay well above historical averages. This is roughly where Bloomberg consensus sits today, and it implies a 12–15% annualized return from current levels including dividends.

Bear case, $200 to $240 (20% probability)

No new major PPAs materialize through 2027. Enhanced earnings normalize faster than new contracts replace them. Gas fleet utilization disappoints. Crane is formally delayed past 2029. Nuclear fleet capacity factor slips below 93% on a sustained basis as management attention is divided across too many priorities. The market re-rates to 14–16 times forward earnings, traditional IPP territory, on EPS of roughly $14–15 in 2028. The PTC floor and buyback authorization provide mechanical support, preventing a collapse below $200, but the premium multiple evaporates.

Probability-weighted three-year target: approximately $380. At $279 today, that implies roughly 36% total return over three years including dividends, attractive, but the entry point matters. Below $260, the math becomes compelling across all scenarios. Below $240, the PTC floor and buyback create a hard bid.

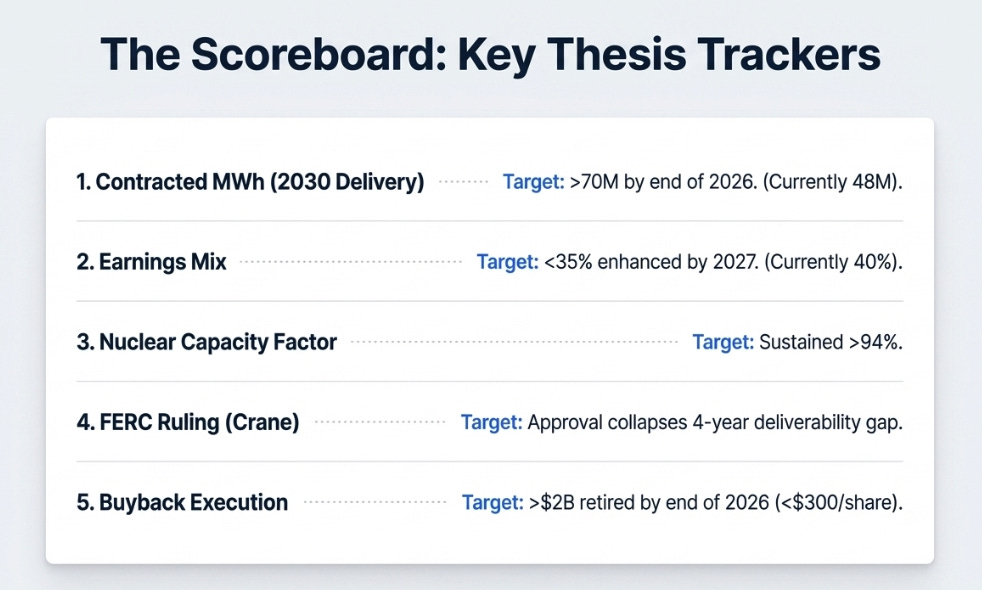

The Scoreboard

The temptation with a company this complex is to track everything. The discipline is to track only what actually determines whether the thesis is working.

First, contracted megawatt-hours for 2030 delivery. Currently 48 million, up from 12 million a year ago. Above 70 million by year-end 2026 means the contracting engine is converting scarcity into base earnings. Below 55 million means the regulatory friction is winning.

Second, the enhanced-to-base earnings mix. Currently 40% enhanced. Below 35% by 2027 means the infrastructure compounder thesis is real and the multiple should expand. Still above 40% means the market is right to withhold the premium.

Third, nuclear fleet capacity factor. Sustained above 94% means the crown jewel is intact despite integration demands. Two consecutive quarters below 92% means management has a resource allocation problem that directly impairs the earnings trajectory.

Fourth, the FERC ruling on the Eddystone-to-Crane capacity injection rights transfer. This is the single highest-impact near-term catalyst that almost nobody is discussing. Approval collapses the four-year gap between Crane’s physical readiness in 2027 and PJM’s 2031 full deliverability timeline. Denial preserves the most visible bear case on the stock.

Fifth, buyback execution. More than $2 billion retired by year-end 2026 at prices below $300 means management is backing conviction with capital. Token execution at higher prices means signaling, not commitment.

That is the scoreboard. Not the next quarter’s earnings per share. Not the next rumor about a hyperscaler deal. The scoreboard.

The Bet

Last August, we argued that owning the reservoir beats chasing the weather. That thesis is stronger today, not weaker. The reservoir is larger, Calpine added the pumping stations. The levees are higher, PTC inflation adjustments are accreting mechanically. The tolls are more lucrative, capacity prices are five times their prior-year level. And the demand for pressure has never been greater, as artificial intelligence workloads collide with a grid that wasn’t built to serve them.

What changed is that the market learned something we should have emphasized more: reservoirs are only valuable if the pipes reach the customers. Constellation is building those pipes, through front-of-meter deals, regulatory filings, AI-enabled flexibility partnerships, and the broadest commercial platform in the power sector. But building pipes in a regulated industry takes longer than filling reservoirs in a scarce one.

The variant perception is this: the market sees a nuclear utility that missed its guidance and failed to announce a deal. The correct framing is a power orchestration platform whose monetization set just widened, whose base earnings are growing at 20% with every optional lever excluded, and whose stock is being sold by momentum investors who bought the AI narrative and left when it didn’t arrive on their schedule. The market is pricing the delay. It should be pricing the destination.

We’d accumulate below $280 and add aggressively below $260. The reservoir is full. The pipes are coming. Patience is the trade.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.

Interesting article, thanks. Valuation appears fair, but peers like TLN and VST offer better growth prospects and exposure to rising electricity prices. I would also have a look at 280$