Credo 4QFY26 Earnings: The Proof Moved to Light

Stronger company, less forgiving stock, and why gross margin is now the only number that matters

TL;DR:

Q4 strengthened the company but made the stock less forgiving: Credo proved it is more than an AI cable supplier, with FY26 revenue more than tripling, Q4 revenue up 157%, gross margin at 68.3%, and FY27 revenue guided above 80% growth but the market now understands the reliability-layer thesis, so the stock needs proof, not discovery.

The key debate has moved from copper to optics: AECs already validated Credo’s reliability advantage in AI clusters; the new question is whether that advantage can travel into optical DSPs, silicon photonics PICs, and ZeroFlap Optics, where management expects more than $600M of FY27 revenue.

Gross margin is now the referendum on the whole thesis: high-60s margins would suggest Credo is selling an ownable system-level reliability layer; mid-60s would make it a premium component leader; low-60s would imply optics, modularity, or customer bargaining power is diluting the moat.

There is a particular discomfort in watching the market agree with you.

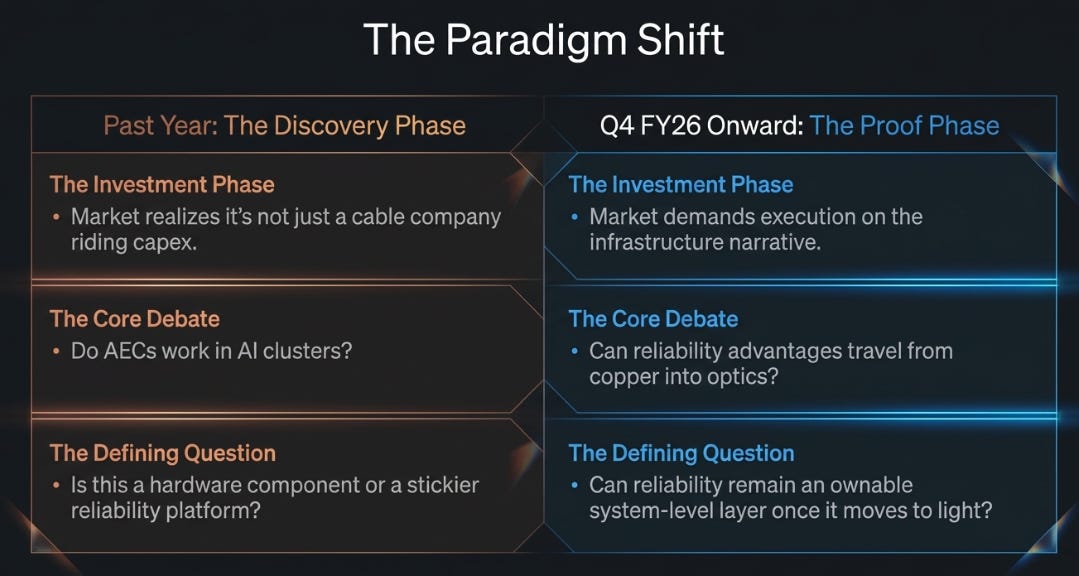

For the past year, our Credo argument has taken different forms, but the underlying claim has been the same: the market was miscategorizing Credo as a cable company riding an AI capex wave, when the more interesting possibility was that it was building something closer to infrastructure, a reliability layer, sold through hardware, that hyperscalers were beginning to standardize on.

Each quarter made that argument harder to dismiss. The margins were too high. The customer adoption was too broad. The language around telemetry, diagnostics, and ZeroFlap was too deliberate. The company looked like a component vendor but behaved economically like something stickier.

Q4 FY26 was the quarter where the market stopped ignoring that possibility.

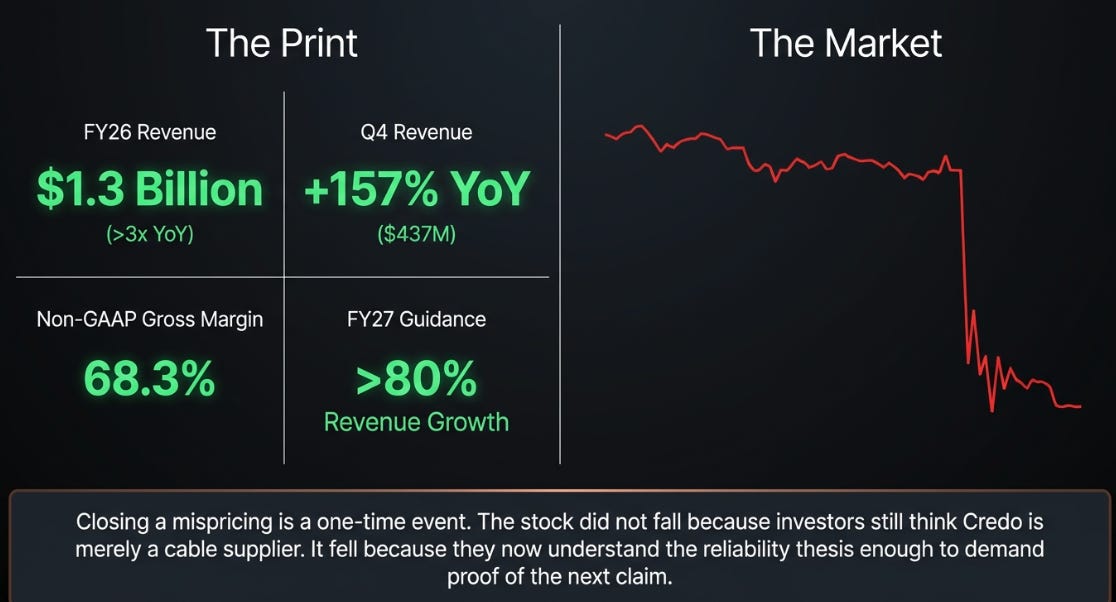

Credo reported revenue of $437 million, up 157% year over year. Full-year revenue more than tripled to $1.3 billion. Non-GAAP gross margin was 68.3%. Management guided fiscal 2027 revenue growth above 80%. And the stock fell.

That sounds contradictory. It is not. The first few times Credo fell on good numbers; the opportunity was that the market misunderstood the company. This time is different. The stock did not fall because investors still thought Credo was merely a cable supplier. It fell because they now understand enough of the reliability thesis to demand proof of the next claim.

Closing a mispricing is a one-time event. We have spent much of it.

What Q4 Actually Settled

The question coming into this quarter was not whether AECs work. That is settled. Credo’s active electrical cables became the wedge because AI clusters do not merely need bandwidth; they need stable links that help preserve GPU utilization and reduce cluster instability.

The harder question, which we framed last quarter, was whether that reliability advantage could travel from copper into optics. Copper has a real role at short distances, but the architecture is moving. Higher bandwidth, 1.6T ports, 200G lanes, scale-up networks, and eventually CPO or NPO all point toward more optical content. If Credo’s advantage was copper-specific, the thesis had an expiration date.

Q4 moved that debate forward. Management now expects more than $600 million of FY27 revenue from the optical portfolio, with optical DSPs, silicon photonics PICs, and ZeroFlap Optics each contributing more than $100 million. That is no longer a side project. It is the plan of record.

But we should be precise. Commercial portability is now in the model. Economic portability is still the test.

Customers appear willing to adopt Credo’s optical portfolio. That does not yet prove that optical carries the same margin structure, workflow lock-in, or platform value as AECs. The question has changed from “can reliability travel?” to “can reliability remain ownable once it arrives?”

That is the new fundamental question.

Integration Wins This Round

I think the answer, for now, is yes.

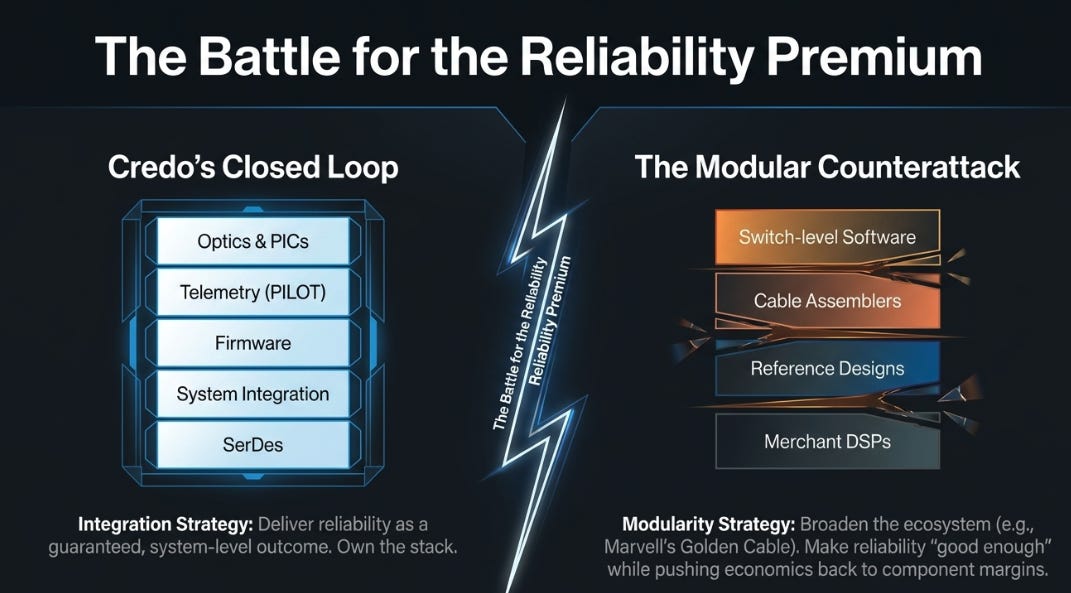

Credo’s strategy is integration. Own the SerDes. Own the system. Own the firmware. Own the telemetry. Own more of the optical stack. Deliver reliability as a system-level outcome, not a component specification.

The modular counterattack is equally clear. Merchant DSPs, reference designs, partner ecosystems, cable assemblers, and switch-level software all exist to make reliability good enough while pushing economics back toward component margins. Marvell’s Golden Cable initiative is the cleanest expression of that strategy: broaden the AEC ecosystem, provide validated architectures and firmware, and let partners scale around merchant silicon.

This is not just Credo versus Marvell. It is integration versus modularity.

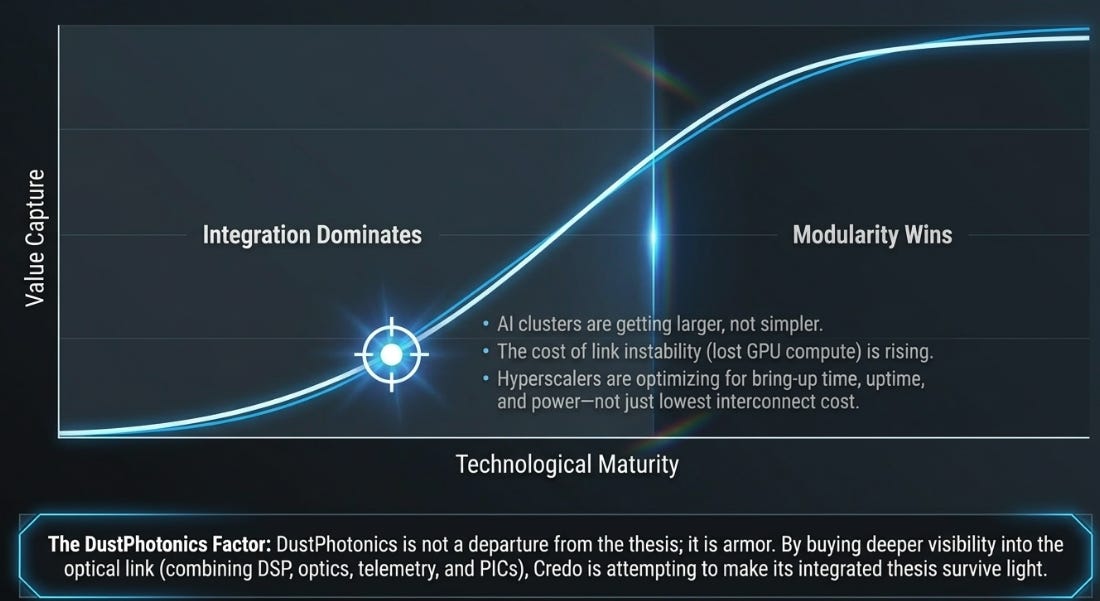

The history of technology says modularity eventually wins when the problem becomes understood well enough to standardize. That is the Cisco cautionary tale. Integrated systems dominate when performance is not good enough; modular ecosystems attack once the interfaces settle.

The question is where AI-network reliability sits on that curve. I think it is still early. Clusters are getting larger, not simpler. The cost of link instability is rising, not falling. Customers are still optimizing for bring-up time, uptime, power efficiency, and utilization, not merely lowest-cost interconnect.

That is the kind of environment where integration should win.

DustPhotonics fits this view. Credo did not simply buy optical revenue. It bought deeper visibility into the optical link. If silicon photonics PICs let Credo combine DSP, optics, telemetry, diagnostics, and system-level optimization more tightly, then DustPhotonics is not a departure from the original thesis. It is the attempt to make the original thesis survive light.

That does not mean Credo wins forever. Integrated advantage is often strongest just before the modular wave begins to matter. The view is narrower: Credo wins this round, because AI-network reliability is not yet good enough to modularize. The day it becomes good enough, the thesis changes.

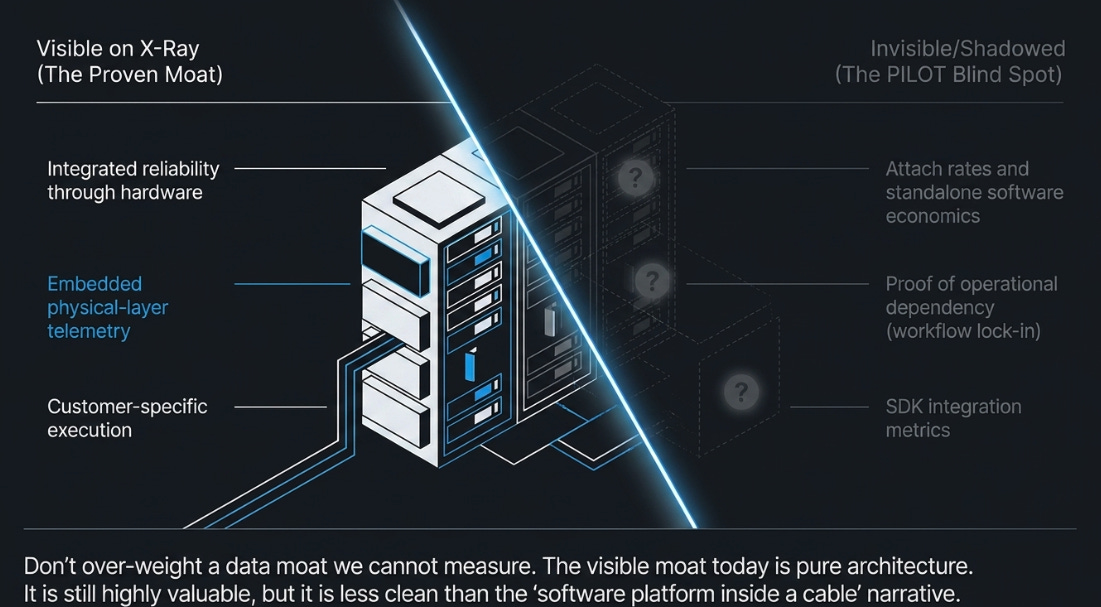

The Metric We Still Cannot See

There is one place where we need to be more disciplined than before: PILOT.

Our earlier argument leaned on PILOT as a possible data flywheel. Every deployment could become a sensor. Every link could generate failure-mode information. Every customer workflow built around Credo’s telemetry could make switching harder.

The logic still makes sense. But the disclosure has not caught up. Management continues to talk about telemetry, diagnostics, monitoring, SDK integration, and autonomous mitigation. What it does not provide is attach rate, pricing, separate software economics, customer workflow evidence, or proof that PILOT has become an operational dependency.

That absence matters.

It does not break the thesis. Physical-layer telemetry embedded in the product is still harder to replicate than dashboard software sitting above the network. But we should not put too much weight on a data moat we cannot measure. The visible moat today is not standalone software. It is architecture: integrated reliability delivered through hardware, firmware, optics, telemetry, and customer-specific execution.

That is still valuable. It is just less clean than the “software-like platform inside a cable” version of the story.

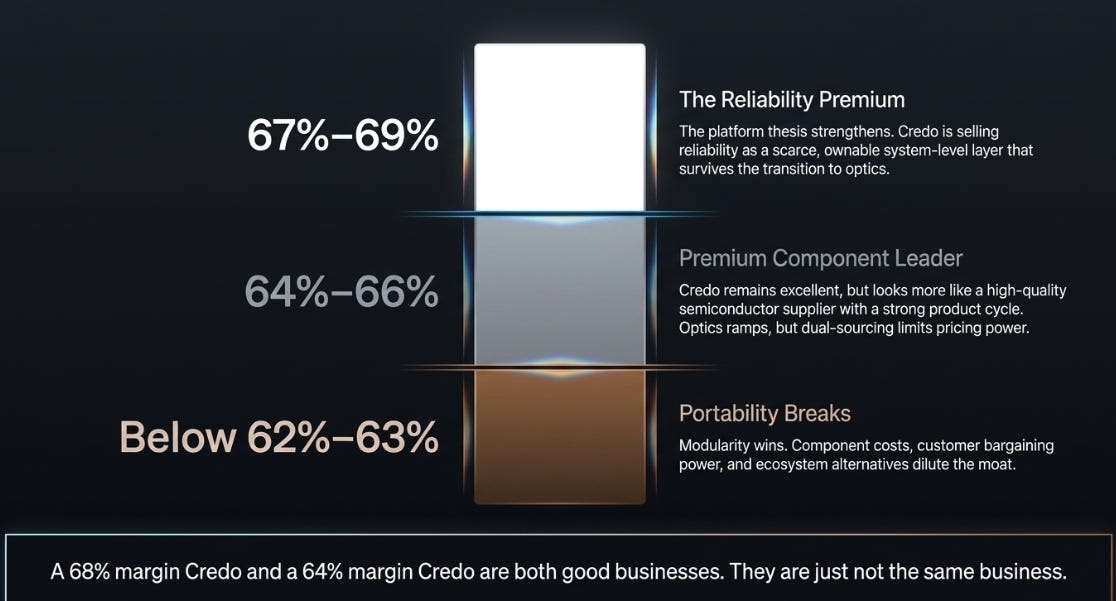

Gross Margin Is the Referendum

This is why gross margin is the most important number now.

Not because gross margin is an accounting line. Because it is where integration versus modularity becomes visible.

If Credo is truly selling reliability as a scarce system-level outcome, then high margins should survive the optical transition. If optics is merely a larger but more competitive market, margins should drift lower as component costs, customer bargaining power, dual sourcing, and modular ecosystems show up.

The framework is simple:

A 68% gross-margin Credo and a 64% gross-margin Credo can both be good businesses. They are not the same business. The first suggests an ownable reliability layer. The second suggests a high-quality semiconductor supplier with a strong product cycle.

That difference matters because the stock is no longer cheap on misunderstanding.

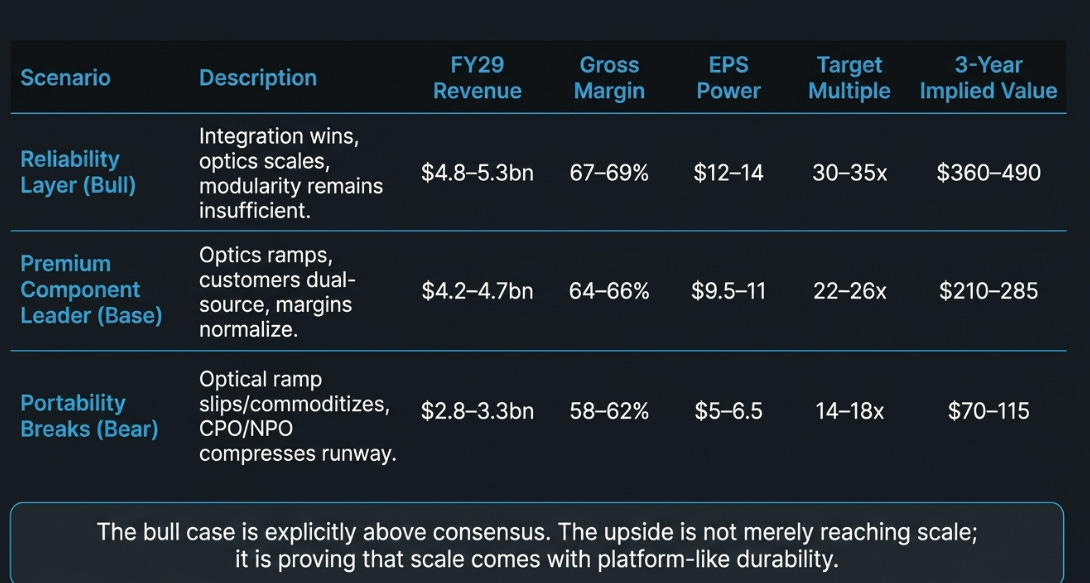

Three Futures

The three-year outcome is less about forecasting every quarter than deciding which architecture wins.

The bull case is now explicitly above consensus. That is important. The Street already models a large FY29 business. The upside is not merely that revenue reaches scale; it is that scale comes with high-60s margins and platform-like durability.

The base case is also not bad. A company doing more than $4 billion of revenue with mid-60s gross margins would still be exceptional. It just would not deserve the same multiple as a reliability control point.

The bear case is where the discipline comes in. If the optical ramp slips or arrives with lower margins, the downside is not just an estimate cut. It is a category reset.

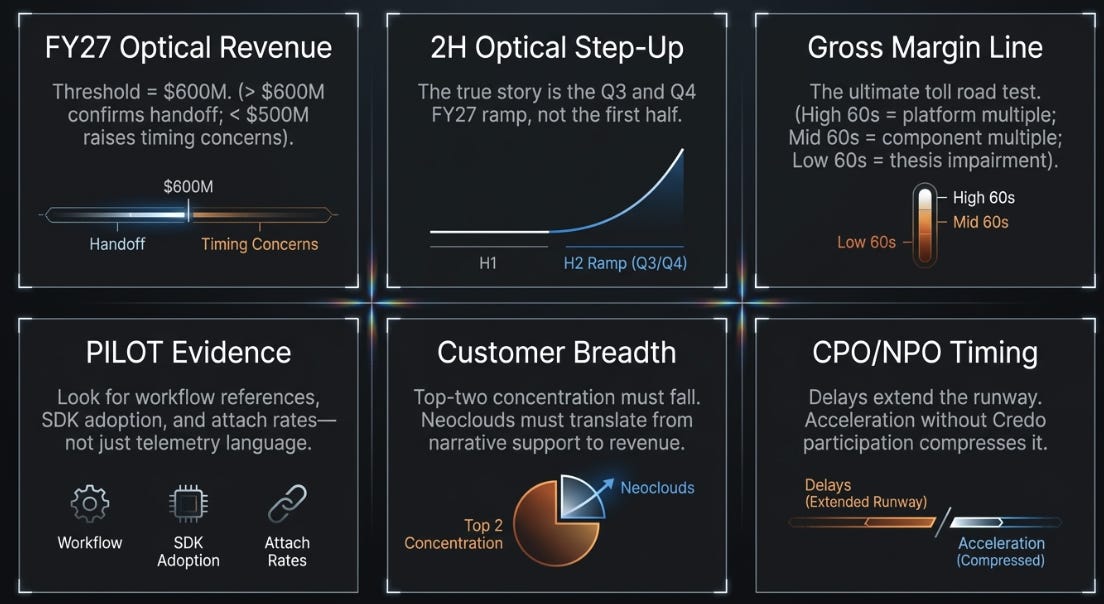

What We Track

The signposts are now clear.

First, FY27 optical revenue. Above $600 million confirms the handoff; below $500 million raises timing concerns.

Second, the Q3 and Q4 FY27 step-up. The first half is not the story. The second-half optical ramp is.

Third, gross margin. High-60s supports the platform case. Mid-60s lowers the multiple. Low-60s impairs the thesis.

Fourth, PILOT evidence. We need more than language: attach rates, customer workflow references, SDK adoption, or proof of operational dependency.

Fifth, customer breadth. Top-two concentration must keep falling, and neoclouds need to become more than narrative support.

Sixth, CPO/NPO timing. Delays extend Credo’s runway. Acceleration without Credo participation compresses it.

Where We Stand

Our view on Credo the company is stronger. Q4 makes the reliability thesis more concrete, not less. The company is no longer merely an AEC winner. It is attempting to extend managed reliability across copper, optical, and eventually near-package connectivity.

Our view on the stock is more disciplined. Credo is no longer deeply misunderstood. The market has begun to understand the story, and that means investors are no longer being paid simply to be early. They are being asked to be right.

That is the uncomfortable but healthy update.

We were early in asking the right question. Q4 gives us more confidence that the question matters. But the answer is still ahead.

Credo has moved the proof from copper to light. Now the margin line will tell us whether the toll road followed.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.