Credo’s 3QFY26 Earnings: Copper, Light, and the Layer in Between

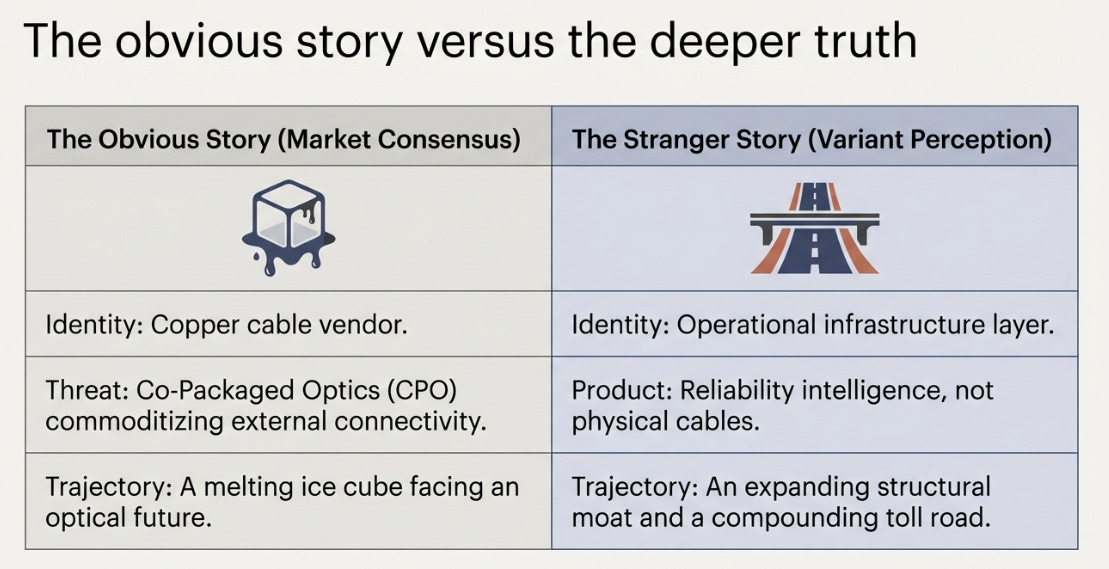

Copper company facing an optical future, or is it mispricing a reliability platform. The gap between the two is the investment debate.

TL;DR

Financial strength is undeniable. 68.6% gross margin and accelerating growth suggest pricing power and embedded value.

The fear has a name: Co-Packaged Optics. The market is discounting a future where external connectivity commoditizes.

This is no longer a copper thesis. It’s a question of whether managed reliability survives architectural transition.

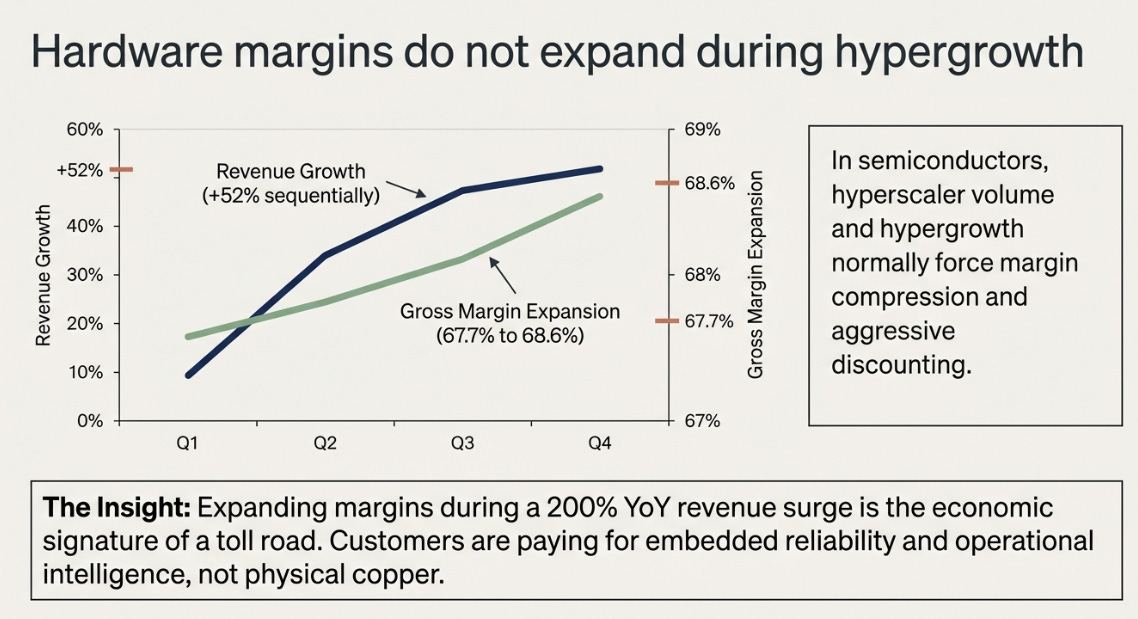

On the evening of March 2nd, Credo Technology reported the strongest quarter in its history. Revenue hit $407 million, up 52% sequentially and more than 200% year, over, year. Non, GAAP gross margins reached 68.6%. Operating margins crossed 49%. Free cash flow nearly quadrupled. Management guided fiscal 2027 to grow more than 50%, above what the Street expected.

The stock fell 12%.

The market is not saying these numbers aren’t worth much. It is saying these numbers don’t mean what you think they mean. It has categorized Credo as a copper connectivity vendor riding an AI capex wave, and it is pricing the inevitable end of that wave. The market may be wrong about the category. But the error is not irrational. It is structural, rooted in a specific fear about where the data center architecture is heading, and whether Credo’s value survives the journey.

What We Argued Before

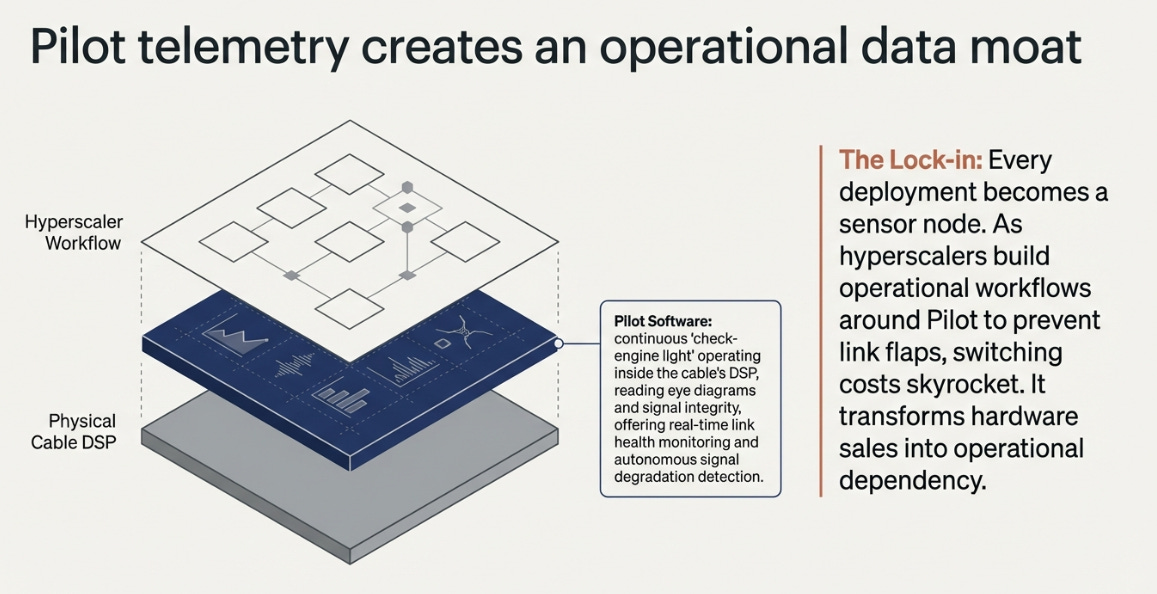

In our previous analysis, we made a specific claim: that Credo was misunderstood. The surface, level story, a company selling Active Electrical Cables into AI data centers, obscured a deeper one. Credo’s margins were too high and too durable for a commodity hardware supplier. Its customer relationships were too sticky. Its product architecture, embedding real, time telemetry into every deployment via the Pilot software platform, suggested the beginnings of operational lock, in, not just a better product.

Our view was that Credo looked like a component vendor on the surface but behaved economically like infrastructure. Q3 didn’t settle that question. But it made the evidence harder to dismiss, and the counter, arguments more urgent.

The Fear

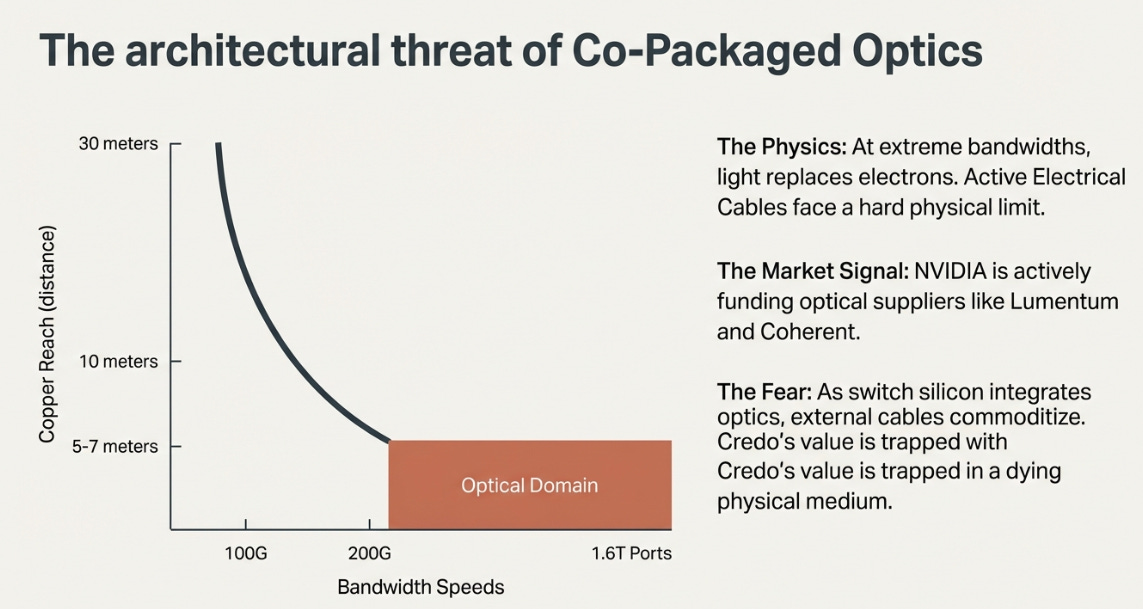

To understand why the stock fell on a great quarter, you have to understand the fear. It has a name: Co-Packaged Optics (CPO).

The physics are real. As AI clusters push toward 1.6 terabit ports and 200 gigabits per lane, the effective reach of copper contracts. Not to irrelevance, Credo’s active cables still handle five to seven meters, covering most intra, rack and many rack, to, rack connections, but the directional pressure is undeniable. At some threshold of bandwidth and distance, light replaces electrons.

NVIDIA knows this. On the same day Credo reported, the market was absorbing NVIDIA’s investments in Lumentum, Coherent, and other optical players. When the company whose GPU architectures define AI infrastructure puts capital behind optical suppliers, it signals architectural intent. Not next quarter. But within the planning horizon that determines valuation multiples.

The market’s logic runs cleanly: NVIDIA integrates optics into switch silicon, external transceivers and cables commoditize, Credo’s AECs become a melting ice cube regardless of current demand, compress the multiple now. This logic is coherent. It is also incomplete, in a way that reveals how markets think about technology transitions and where they tend to get the timing wrong.

What Q3 Actually Showed

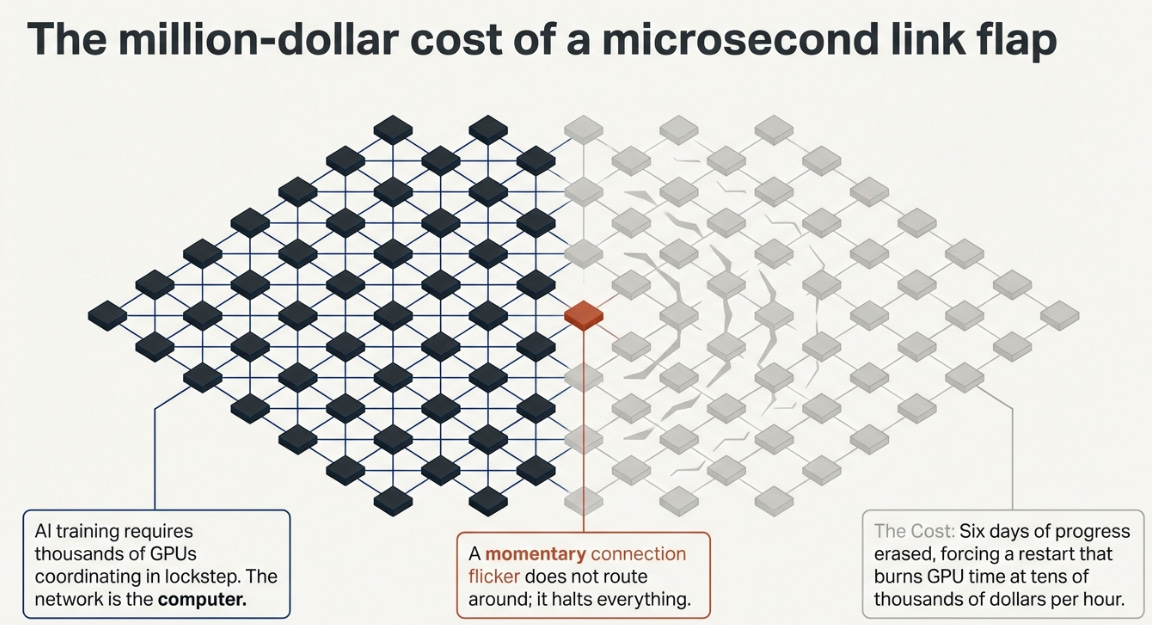

The quarter’s most important development was not the revenue number, which had been pre, announced in February and carried no surprise. It was the six, month pull , forward of ZeroFlap optical transceivers into production, with TensorWave as the first customer and three hyperscalers in qualification.

This reframes the copper, versus, optics debate. Credo is not defending copper against optical disruption. It is attempting to port its reliability architecture across physical media. ZeroFlap transceivers embed the same Pilot telemetry, continuous link health monitoring, autonomous signal degradation detection, switch, level SDK integration, that made AECs the standard for short, reach connectivity. The value proposition was never “copper is superior to light.” It was “managed reliability is superior to commodity reliability, regardless of the medium.”

There is a tension here worth holding. The six, month acceleration is either evidence of product, market fit arriving faster than expected, or evidence that the optical window is closing faster than management originally planned. It is probably both. Customers are pulling ZeroFlap forward because they genuinely need reliable optical at scale. And Credo is willing to ship ahead of schedule because waiting risks ceding the optical transition to incumbents with deeper resources. Strength and urgency are not mutually exclusive, and the distinction matters less than whether the product actually works at hyperscaler scale. That we will learn in the next two quarters.

CEO Bill Brennan was direct about the competitive narrative on the call. He characterized CPO discourse as a “signal to noise ratio issue” and argued that co, packaged optics would remain limited until delivering “bulletproof reliability.” The dismissive tone may have cost him with investors. But the product roadmap told a more considered story: ZeroFlap for pluggable optical, Active LED Cables for mid, reach distances up to 30 meters, and an OmniConnect gearbox targeting near, package optics with MicroLED, designed explicitly to address “the reliability, serviceability, and availability pitfalls of current CPO solutions.”

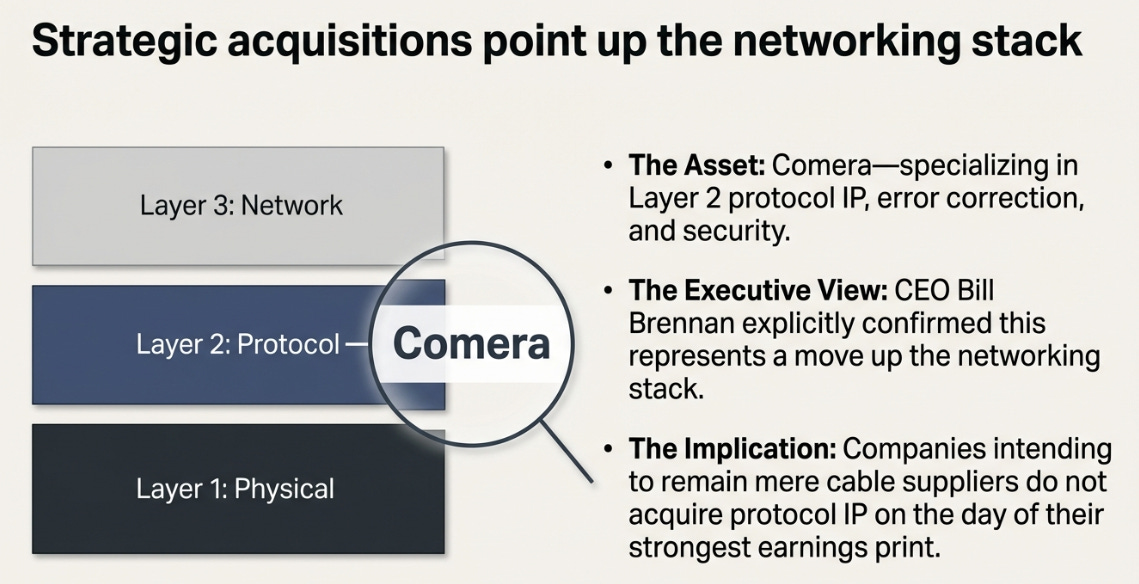

The same quarter saw the quiet acquisition of Comera, a company specializing in Layer 2 protocol IP, error correction, and security. Asked whether this represented a move up the networking stack, Brennan’s answer was simply: “Yes, absolutely.” This does not prove Credo is becoming a platform company. But companies that intend to remain cable suppliers do not typically acquire protocol IP on the day of their strongest earnings print.

The Margin Question

The 68.6% gross margin deserves more scrutiny than the market gave it, in both directions.

The bull case is straightforward: in a quarter where revenue grew 52% sequentially, shipped overwhelmingly to hyperscalers who negotiate aggressively on every line item, margins did not compress. They expanded. By 92 basis points. This is not how commodity hardware behaves during a demand surge. It suggests customers are paying for something embedded in the product, reliability, telemetry, operational intelligence, that goes beyond the physical cable.

Management guided Q4 at 64–66%, roughly 300 basis points below Q3 actuals. The market read this as compression. The historical pattern suggests it is more likely conservative forecasting, management guided Q3 at 64–66% and delivered 68.6%, and the same pattern has repeated for four consecutive quarters.

But there is a version of the bear case that is more interesting than “management is finally right about its own margins.” As Credo’s revenue mix shifts toward optical, ZeroFlap transceivers, eventually ALCs, the blended gross margin may genuinely settle closer to 64–66%. Optical products carry higher component costs, early yield ramp friction, and potentially introductory pricing to win qualifications. If that is what the guide reflects, then 68.6% was not a platform baseline but a copper peak, and the long, term margin is what management has been saying all along: 63–65%. This would not break the thesis, but it would change what the thesis is worth. The difference between a 68% margin business and a 64% margin business, compounded over several years, is meaningful.

The Hardest Question

The debate around Credo has evolved. It is no longer copper versus optics. The more interesting framing is commodity connectivity versus reliability, managed connectivity. Credo is betting that hyperscalers will pay a structural premium for managed reliability, observable, predictable, autonomously maintained link health, across any physical medium.

But there is a harder question underneath this one, and it is the question the thesis ultimately depends on: does reliability remain a separable layer that Credo can own?

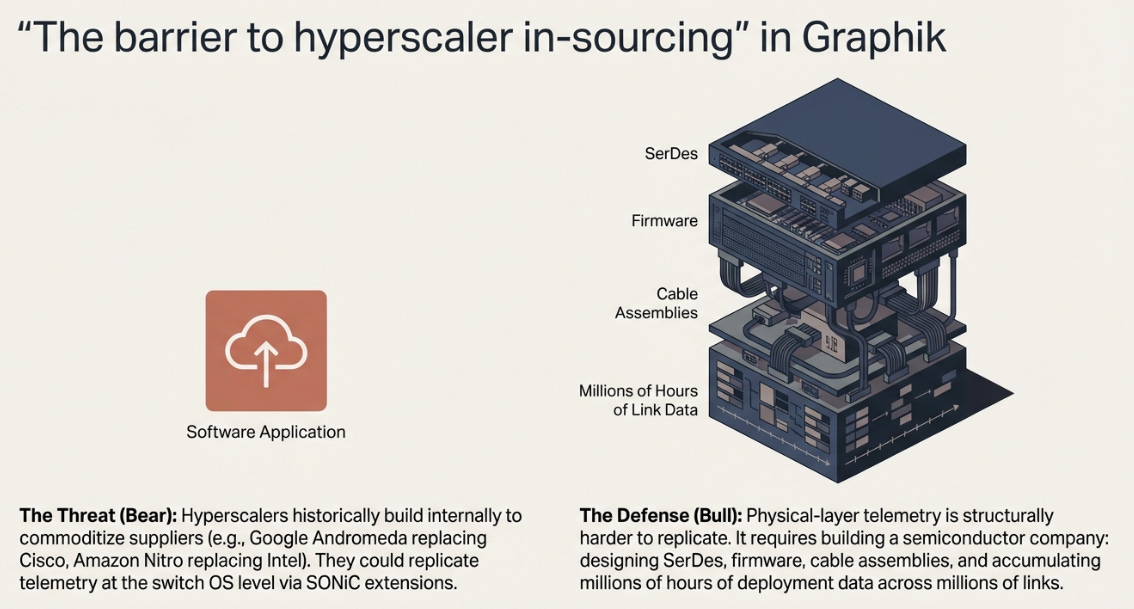

The historical pattern in hyperscaler infrastructure is not encouraging for vendors. Google built Andromeda to replace Cisco. Amazon built Nitro to replace Intel networking. The playbook is consistent: adopt the best external solution, learn from it, then build or commoditize internally. If Pilot’s telemetry value can be replicated at the switch OS level, through SONiC extensions, NVIDIA’s management stack, or a hyperscaler’s own monitoring tools, then Credo’s premium erodes regardless of whether it ships copper or optical.

The counterargument is that physical, layer telemetry is structurally harder to replicate than switch, level software. Pilot operates inside the cable’s DSP, reading eye diagrams, pre, cursor equalization data, and signal integrity measurements that do not exist at the switch level. To build an internal alternative, a hyperscaler would need to design its own SerDes, develop its own firmware, build its own cable assembly and qualification process, and accumulate years of deployment data across millions of links. That is not writing monitoring software. That is building a semiconductor company. The barrier is higher than what Google faced replacing Cisco.

Higher, however, is not insurmountable. And the 68.6% gross margin, while powerful evidence that the reliability premium is being paid today, does not guarantee that the payment continues to be routed through Credo as the architecture evolves. This uncertainty is real. The thesis must be honest about it.

Updating the View

Our prior thesis was that Credo was probably transitioning from hardware to infrastructure. After Q3, we believe it is likely, with a more specific understanding of what “likely” requires.

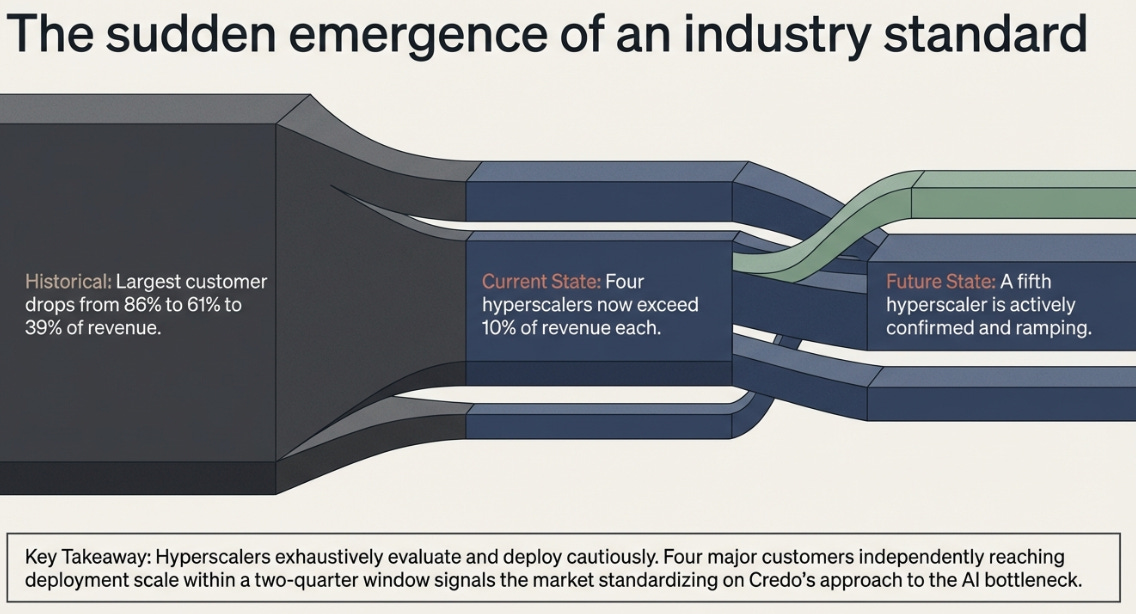

Three of four key debates moved in favor of the bull case. Customer concentration continued improving: the largest customer fell to 39% of revenue, down from 86% a year ago. A fifth hyperscaler was confirmed. ZeroFlap optics are opening an entirely new neocloud customer channel. Growth sustainability was confirmed above expectations, with management guiding fiscal 2027 above 50%. And the optical pivot is no longer theoretical, production units are shipping.

Margin durability remains open. Not because Q3 was weak, but because the product mix is changing and the steady, state margin of a blended copper, optical portfolio is genuinely unknown.

The conceptual upgrade in our thinking: the variant perception on Credo is no longer “AECs will keep winning.” It is that Credo’s reliability advantage may travel further than copper. If ZeroFlap optics gain traction and Pilot telemetry becomes embedded in hyperscaler operational workflows, the total addressable market expands with each architectural transition rather than contracting. If reliability gets commoditized or absorbed into the vertical stack, Credo remains a very good but ultimately cyclical hardware company. That is the distribution of outcomes the stock is pricing, and at 24 times forward earnings with 50% growth, it is pricing closer to the pessimistic end.

Three, Year Framework

The right way to think about Credo is not a single outcome but a range tied to whether its reliability advantage proves portable.

Bull case (35% probability): $350–400. Revenue compounds at 45–50% through fiscal 2029, reaching approximately $4.5 billion. ZeroFlap optics and ALCs become material revenue lines. Gross margins sustain in the mid, to, high 60s as Pilot, embedded products command structural premiums. The market re, rates Credo as infrastructure rather than hardware. This case requires not just execution but sustained AI capex, CPO delays, no macro recession, and, critically, Pilot proving durable against internal hyperscaler alternatives. Many things must go right. The reward if they do is substantial.

Base case (50% probability): $180–210. Revenue compounds at 35–38%, reaching $3–3.5 billion. AECs remain dominant, optics becomes additive but not transformative. Gross margins settle at 64–66%, management’s own target, possibly reflecting an honest blended margin rather than conservatism. Pilot is strategically valuable but never separately monetized. The market values Credo as a premium semiconductor company.

Bear case (15% probability): $70–85. Revenue growth decelerates to 20–22% as AI capex normalizes and CPO timelines compress. Gross margins drift toward 58–62% under hyperscaler pricing pressure. Pilot never achieves visible lock, in. The market treats Credo as a cyclical component supplier. This requires multiple simultaneous failures but cannot be dismissed.

What to Track

Six signposts will determine whether the thesis is evolving correctly.

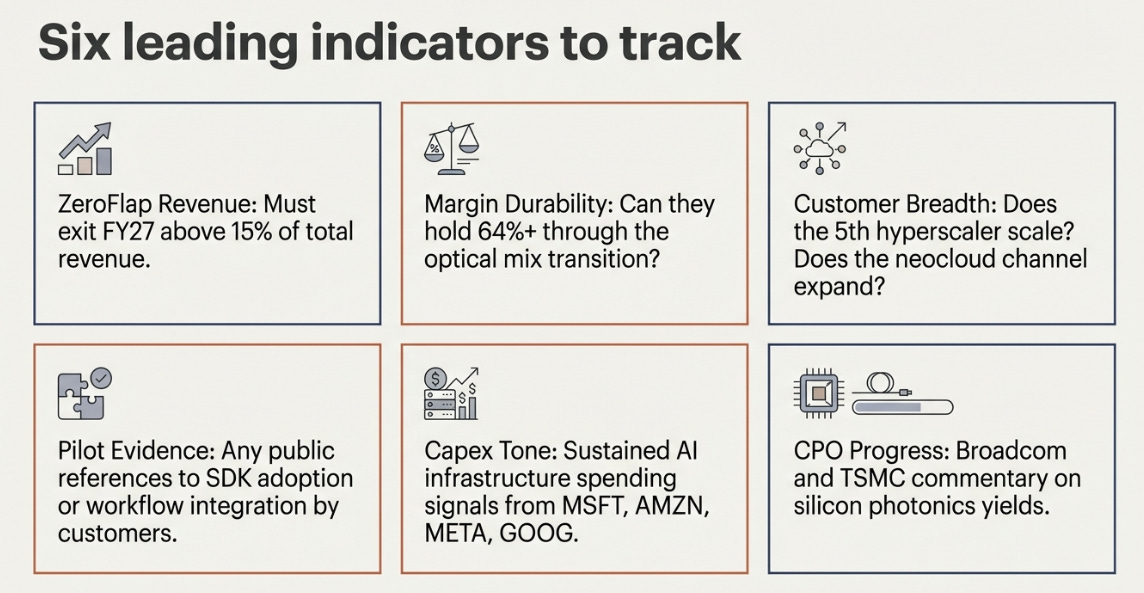

ZeroFlap optical revenue. Optics must become real in the income statement, not just the press release. Exiting fiscal 2027 above 15% of revenue would be meaningful confirmation.

Gross margin through the mix transition. Can Credo sustain 64%+ as optical grows? Another quarter of beating a conservative guide would ease the concern. Falling to guide would suggest the blended margin reality is settling in.

Customer breadth. Does the fifth hyperscaler scale? Does the neocloud channel expand beyond TensorWave?

Pilot evidence. Any concrete disclosure, attach rates, SDK adoption, operational workflow references, would begin to close the separability question.

Hyperscaler capex tone. April and May earnings from Microsoft, Amazon, Meta, and Google will signal whether AI infrastructure spending is sustaining or peaking.

CPO progress. Broadcom and TSMC commentary on silicon photonics yields. Current yields remain below production thresholds, but the gap is narrowing faster than copper bulls expected. Delays extend Credo’s runway. Acceleration compresses it.

Where We Stand

Our view is stronger on the company and more specific about what the thesis requires. Q3 made it harder to argue that Credo is just a well, timed hardware vendor. But it also clarified what still needs proving: not whether Credo can win in copper, that is settled, but whether its reliability advantage remains ownable as the architecture shifts from copper to optical and as hyperscalers do what hyperscalers always do, which is try to commoditize their suppliers.

The stock at $99 already assumes the market’s answer to that question is no. If the answer turns out to be even partially yes, the re, pricing will be significant. The next twelve months will determine which side of that bet is right.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.