CrowdStrike’s 1QFY27 Earnings: The Question Changed

AI made Falcon’s data pipeline matter more.

TL;DR

Four quarters ago, I argued that CrowdStrike was not simply a security software company, but a data infrastructure company operating inside cybersecurity. Now management is making a version of that argument on the earnings call. That should feel like vindication. It does not.

The thesis is stronger than it was at $391, but the opportunity is harder at $659. Q1 made the architecture more credible: AI agents, Mythos-style vulnerability discovery, SIEM, AIDR, Identity, Cloud, and Flex all point in the same direction. But the stock had already rallied on that possibility, and the quarter did not deliver enough ARR proof to justify the move immediately.

CrowdStrike beat consensus, but consensus was not the bar. The company missed the buyside imagination. The question now is no longer whether Falcon is a platform. The question is whether Falcon becomes the control and remediation layer for AI-era security.

The Inversion

To understand CrowdStrike’s Q1, you first need to understand what happened to software before the company reported.

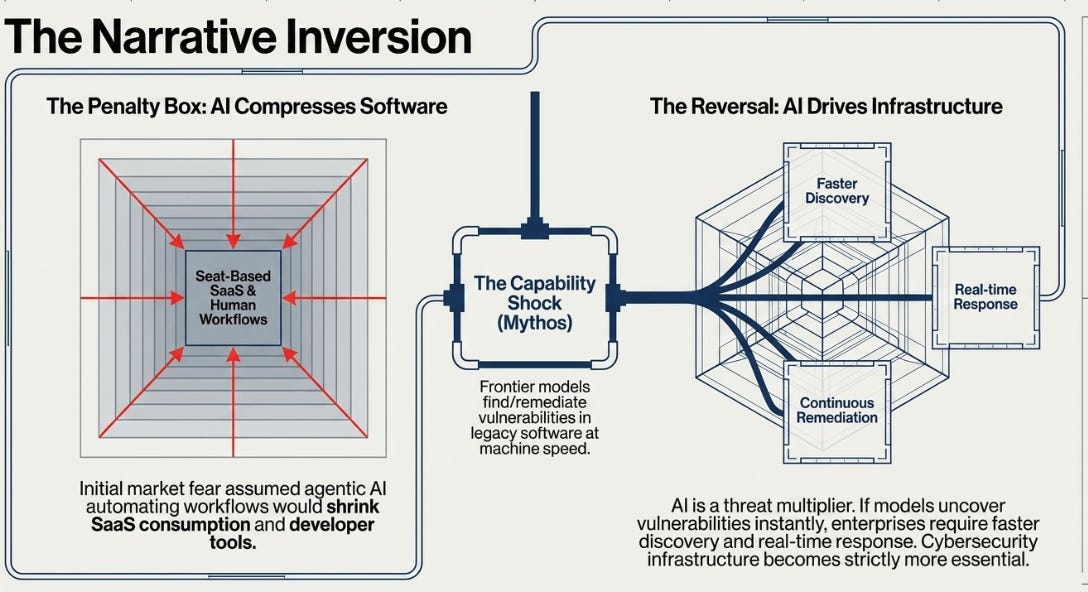

Earlier this year, software and cybersecurity stocks were in a penalty box. Claude Code and other agentic AI products made the threat feel existential: if AI agents can write code, operate tools, and automate workflows at developer speed, what happens to seat-based SaaS consumption? What happens to developer tools, IT management platforms, or even security software if the human workflow becomes less central?

That was the first narrative: AI compresses software.

Then came the inversion. Snowflake helped show one version of the reversal: AI could increase consumption for the right platforms rather than destroy them. If enterprises need more data, governance, compute, and workloads to build AI, then the right infrastructure companies become more important, not less.

Project Glasswing gave cybersecurity its own reversal, but the point needs to be precise. This was not simply “Anthropic needs CrowdStrike and Palo Alto to secure Mythos.” The more important point was that Mythos demonstrated a capability shock: a frontier model could find and help remediate vulnerabilities in complex, old software that had eluded humans. Anthropic’s response was to work with major technology and security partners so critical systems could be hardened before Mythos-like capabilities became broadly available.

That changed the cybersecurity debate. AI was no longer only a possible threat to security vendors. It was also a threat multiplier for the entire software estate. If frontier models can uncover hidden vulnerabilities at machine speed, then the world does not need less cybersecurity. It needs faster discovery, better prioritization, continuous remediation, and real-time response.

CrowdStrike reported after this regime had already turned. The stock had rallied sharply from the March lows because the market moved from fear to belief. Q1 was supposed to confirm that belief. It partly did. That was the problem.

The Bridge

In March, around $391, I argued that CrowdStrike’s base case offered little return unless the market reclassified the company from security software to security data infrastructure. The structural observations were right: Falcon’s telemetry pipeline, SIEM momentum, Flex consumption behavior, and platform consolidation all mattered more than the quarterly optics.

What I underestimated was the possibility of an external catalyst. Mythos was not in the model. It could not have been. But the right lesson is not “models are useless.” The lesson is that when a company owns a genuine control point, the upside scenarios are often larger and arrive faster than a spreadsheet allows.

At $391, the market was still not paying much for the data-pipeline thesis. At $659, it is paying for a meaningful part of it. That is the uncomfortable update. The thesis is stronger. The margin of safety is not.

The Question Changed

The old question was whether Falcon was becoming security data infrastructure. Q4 pushed that answer toward yes. SIEM made the architecture visible. Flex made the economics more repeatable. Customers were not merely buying endpoint protection; they were embedding Falcon into more of the SOC workflow.

Q1 introduced a harder question: does that security data pipeline become the control and remediation layer for AI-discovered software risk?

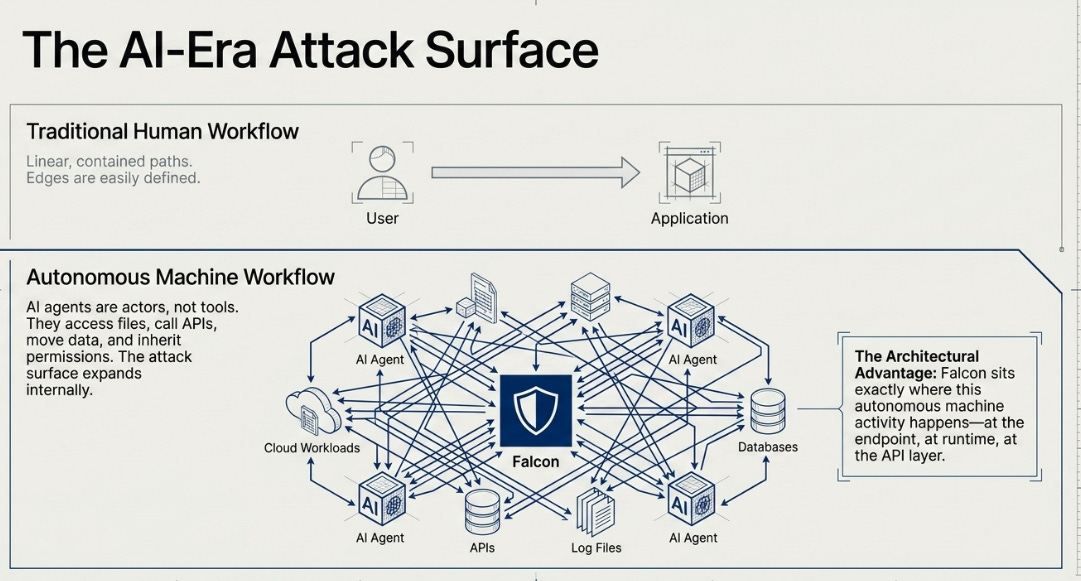

That is the only question that really matters. AI agents are not just tools that help humans work faster. They are becoming actors inside the enterprise. They access files, call APIs, inherit permissions, move data, touch cloud workloads, generate logs, and interact with other systems. At the same time, Mythos-like models can make long-buried vulnerabilities visible. The attack surface is not just expanding at the edge; it is being rediscovered inside the software base enterprises already depend on.

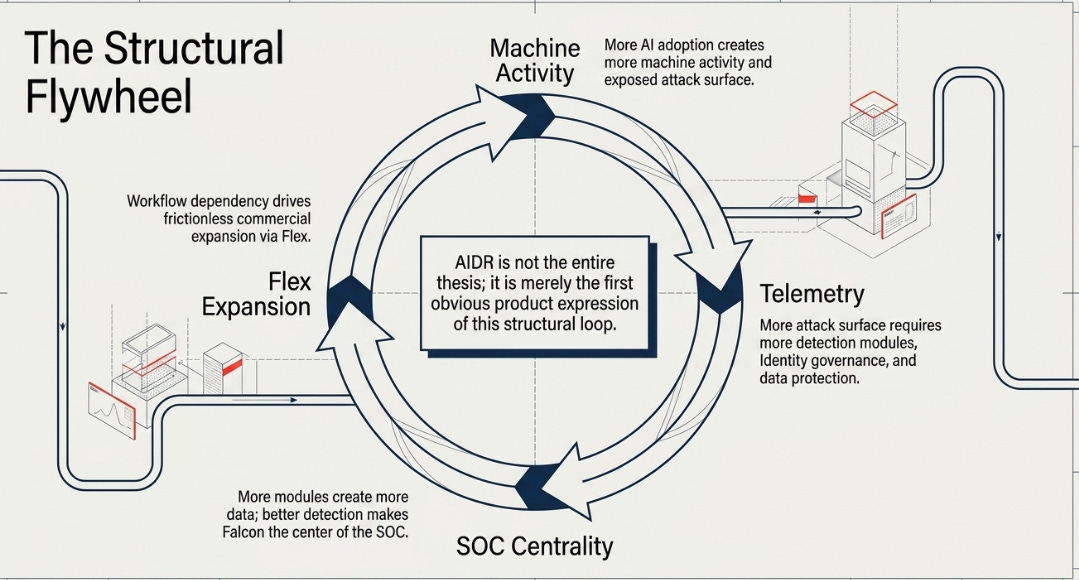

This makes CrowdStrike’s architecture more relevant. Falcon sits where a lot of this activity happens: on the endpoint, at runtime, where processes run, files get accessed, APIs get called, and data moves. The sensor creates telemetry. Telemetry creates insight. Insight creates response. Response creates workflow dependency. Workflow dependency creates expansion.

That loop is now being extended from human workflows to machine workflows.

More AI adoption creates more machine activity. More machine activity creates more attack surface. More AI-discovered vulnerabilities create more remediation urgency. More attack surface requires more telemetry, identity governance, detection, response, and data protection. More Falcon modules create more data. More data improves detection and response. Better detection and response make Falcon more central to the SOC. A more central Falcon creates more expansion through Flex.

That is the structural mechanism. AIDR is not the thesis. AIDR is the first obvious product expression of the thesis.

What the Numbers Actually Say

The quarter supported the architecture thesis. It did not fully prove the acceleration thesis.

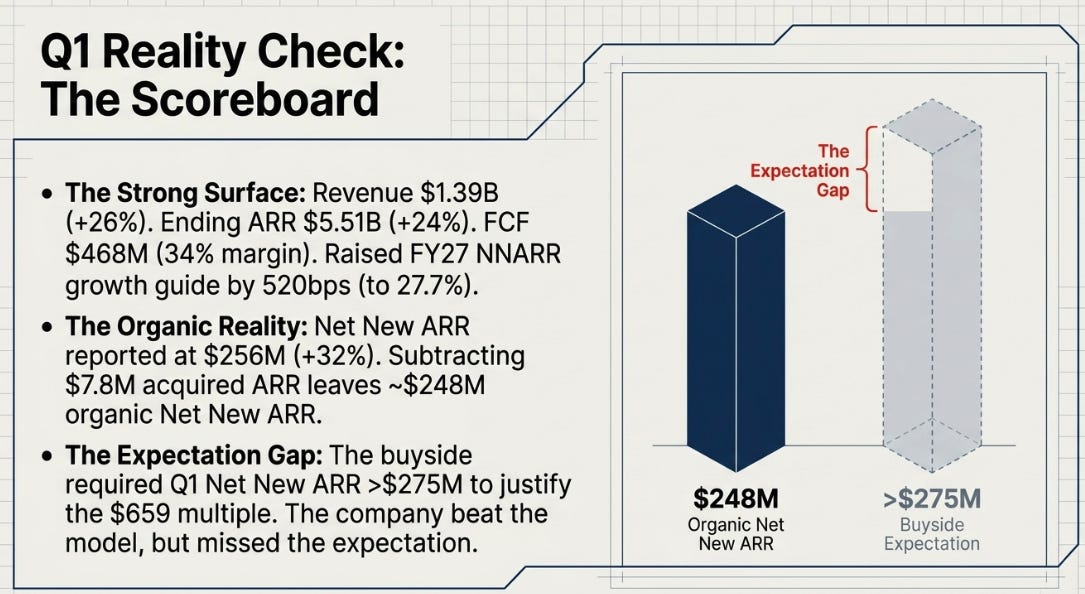

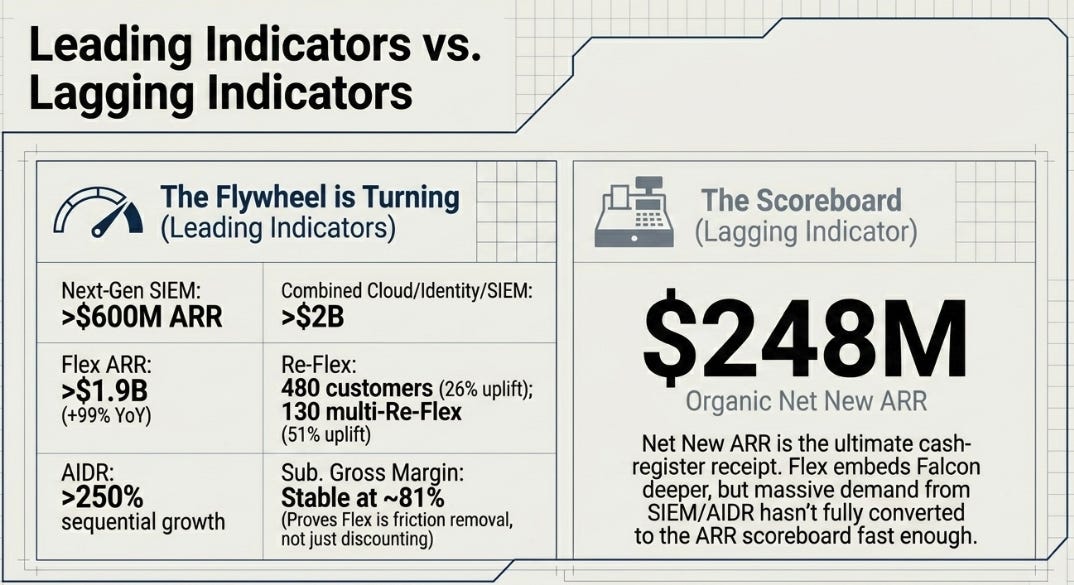

Revenue grew 26% to $1.39 billion. Ending ARR reached $5.51 billion, up 24%. Net new ARR was $256 million, up 32%. Free cash flow was $468 million, or 34% of revenue. Management raised FY27 net new ARR growth guidance by 520 basis points to 27.7% at the midpoint.

Those are strong numbers. They were not enough.

The reason is simple: the stock was not trading against published consensus. The buyside wanted Q1 net new ARR above $275 million. CrowdStrike delivered $256 million. Worse, $7.8 million of net new ARR came from acquired ARR, which means organic net new ARR was roughly $248 million. On that basis, the headline beat was much less impressive. The company beat the model, but it did not beat the expectation embedded in the multiple.

That is why the stock fell. The market did not reject CrowdStrike’s AI-security thesis. The market had already begun to believe it.

The leading indicators were stronger than the lagging indicators. AIDR ending ARR grew more than 250% sequentially, although the base was not disclosed. Next-Gen SIEM exceeded $600 million of ARR. Combined Cloud, Identity, and Next-Gen SIEM crossed $2 billion. Flex ARR surpassed $1.9 billion, growing 99% year over year. Re-Flex customers reached 480, with a 26% average uplift. More than 130 customers have Re-Flexed multiple times, with a 51% uplift versus the original Flex contract. Subscription gross margin held around 81%, which weakens the argument that Flex is just a discounting mechanism.

Those numbers matter because they describe the flywheel before it fully appears in ARR. Flex removes procurement friction. Customers activate modules faster. Operational workflows adapt to Falcon. Re-Flex becomes a larger renewal because the platform has become more embedded. That is the commercial side of the architecture.

But net new ARR is still the scoreboard. It may no longer be the earliest signal in a Flex world, but it is still the cash-register receipt. If Flex, AIDR, SIEM, and Mythos-driven remediation are truly accelerating demand, they must eventually show up in ARR. Q1 said the flywheel is turning. It did not prove it is accelerating fast enough.

The Snowflake Contrast

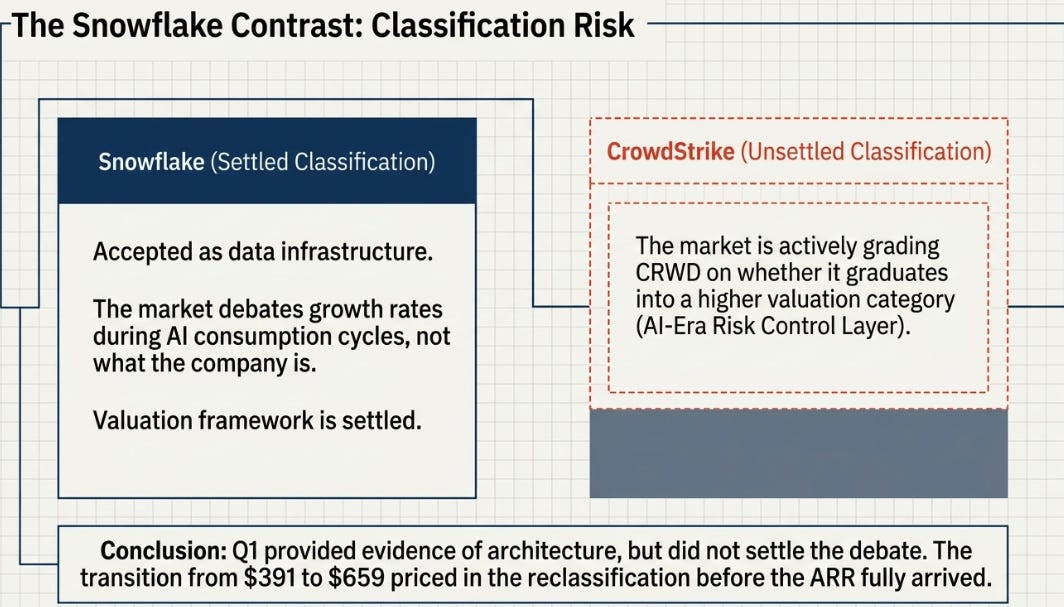

Snowflake matters here not because it is the same business, but because it shows the importance of classification.

Snowflake is already accepted as data infrastructure. The market debates how fast it grows, not what it is. When Snowflake beats and raises in an AI consumption cycle, the stock can work because the valuation framework is settled.

CrowdStrike is different. The market still has to decide what CRWD is. Is it a premium cybersecurity platform? Is it security data infrastructure? Or is it the control and remediation layer for AI-era enterprise risk?

That classification question explains the post-earnings reaction. CrowdStrike is not merely being graded on whether it beat consensus. It is being graded on whether the quarter moves it into a higher valuation category. Q1 gave evidence. It did not settle the debate.

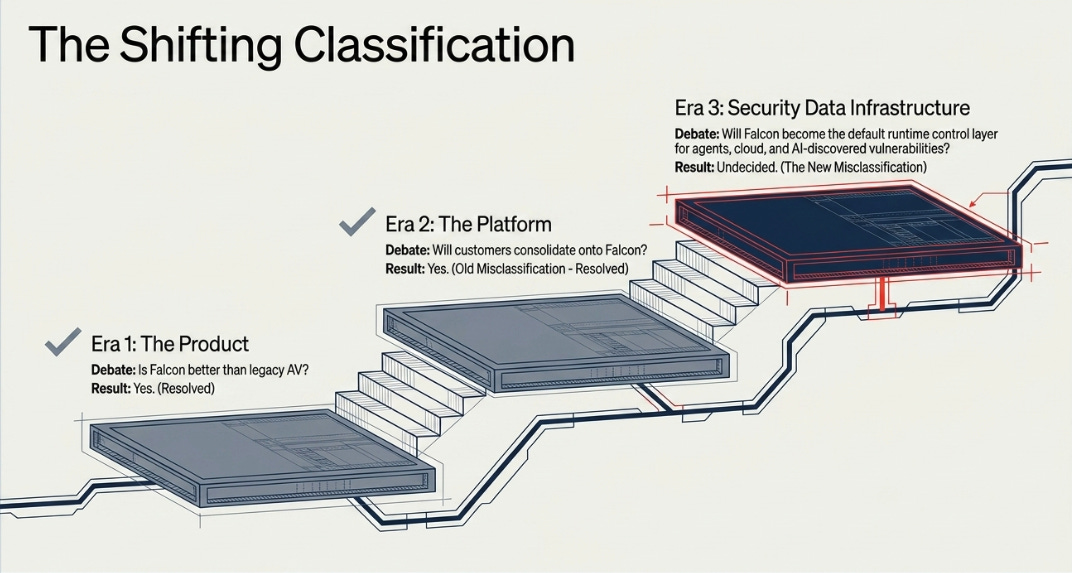

The New Misclassification

The old misclassification was product versus platform. The market viewed CrowdStrike as a security product company when Falcon was becoming security data infrastructure.

The new misclassification is platform versus infrastructure. Consensus now understands that CrowdStrike is a high-quality platform. The question is whether Falcon deserves infrastructure status in the AI era.

If AIDR is simply another module, the stock is expensive. If Falcon becomes the runtime control layer for agents, identities, endpoints, cloud workloads, AI-discovered vulnerabilities, and the AI SOC, the addressable role inside the enterprise expands materially.

This is why I am more confident in the architecture and more cautious on the stock. At $391, the market was not paying for the reclassification. At $659, it is paying for enough of it that the next three years require proof, not just architecture.

Three Futures

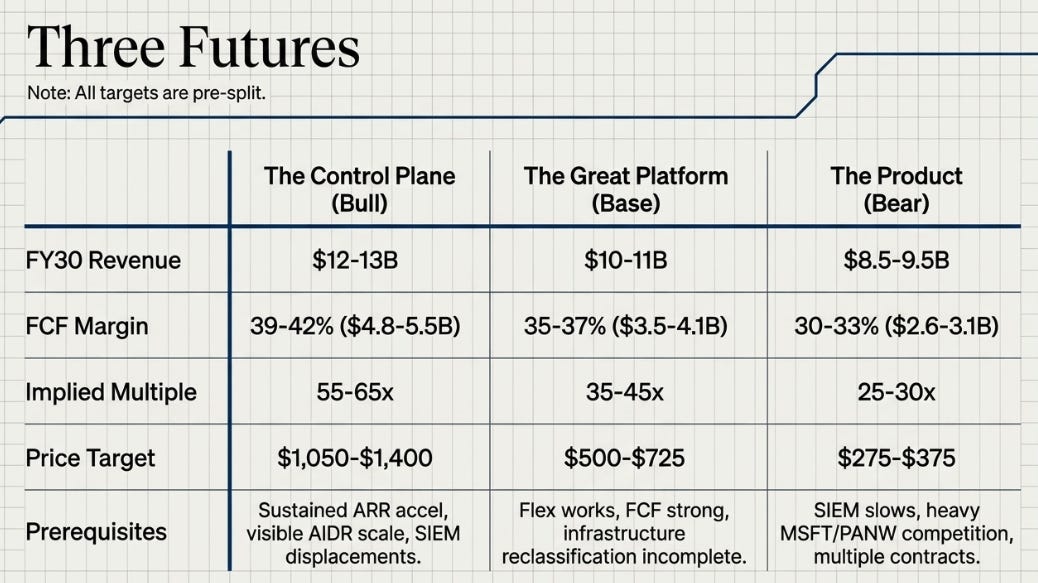

All prices below are pre-split.

In The Control Plane, CrowdStrike becomes the default runtime security and remediation layer for enterprise AI. AIDR scales, SIEM becomes the AI SOC data layer, identity becomes more important because of non-human agents, and Flex converts new security concerns into platform expansion. Revenue grows roughly 23–25% annually through FY30, reaching $12–13 billion. Free cash flow margins reach 39–42%, producing $4.8–5.5 billion of FCF. If the market values that at 55–65x FCF, the stock could be worth roughly $1,050–1,400. This requires sustained ARR acceleration, visible AIDR scale, SIEM displacements, and Flex continuing to compound without margin erosion.

In The Great Security Platform, CrowdStrike remains one of the best cybersecurity companies in the world, but the infrastructure reclassification remains incomplete. Flex works, SIEM grows, AIDR is real but not transformative, and free cash flow remains strong. Revenue grows around 18–20% annually through FY30, reaching $10–11 billion. FCF margins reach 35–37%, producing $3.5–4.1 billion of FCF. At 35–45x FCF, the stock is worth roughly $500–725. This is the uncomfortable middle case: the company remains excellent, but the stock may not work much because excellence was already priced in.

In The Product, Not the Platform, AI-security urgency creates pipeline but not enough ARR conversion. AIDR remains early, SIEM growth slows, Microsoft and Palo Alto compete aggressively, and CrowdStrike remains best-in-class but loses the infrastructure narrative. Revenue grows 14–16% annually, reaching $8.5–9.5 billion. FCF margins settle around 30–33%, producing $2.6–3.1 billion of FCF. At 25–30x FCF, the stock is worth roughly $275–375. The company survives and generates cash. The stock loses because the multiple changes.

What Resolves It

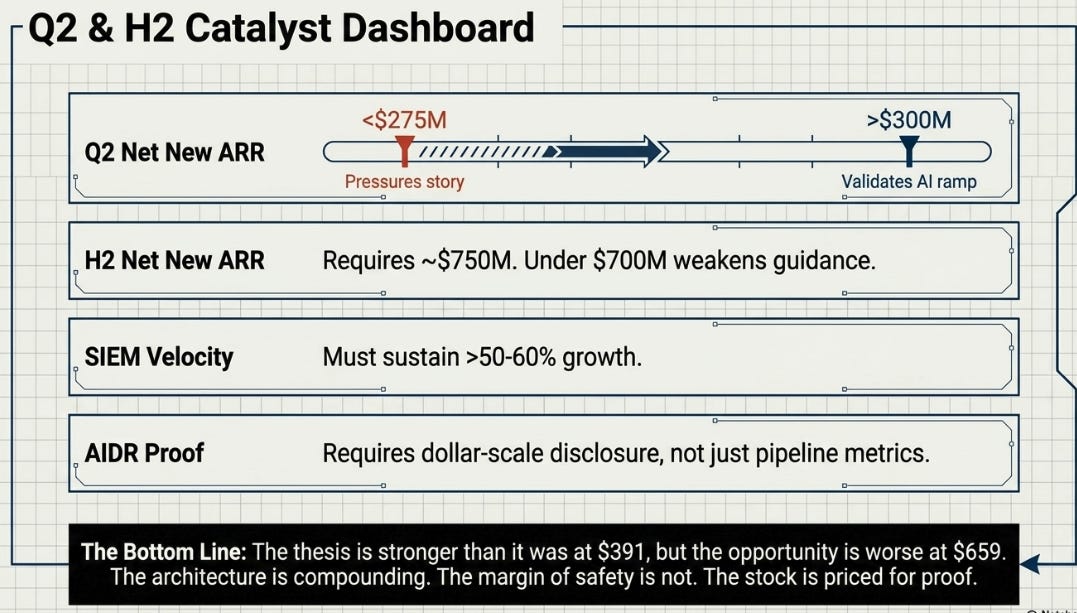

Q2 matters more than Q1.

Net new ARR above $300 million would validate the AI-security ramp. Below $275 million would pressure the FY27 acceleration story. The second half needs roughly $750 million of net new ARR; below $700 million weakens the guide. AIDR needs dollar-scale disclosure, not just growth rates and pipeline. SIEM needs to sustain growth above 50–60%. Re-Flex cadence and uplift need to remain strong. Subscription gross margin should stay near or above 80% while Flex scales. Endpoint momentum must continue if endpoint is truly the AI runtime control point. RPO and billings need to look cleaner next quarter.

At $550–580, I would be more willing to build. At $659, I would hold but not add aggressively. Above $750 without corresponding ARR proof, I would trim. The thesis is intact. The flywheel is compounding. The margin of safety is not.

The Bottom Line

CrowdStrike’s Q1 did not change the thesis. It changed the burden of proof.

The company is no longer trying to prove that it survived the outage. That question has been answered. It is no longer merely trying to prove that Falcon is a platform. That case has strengthened over multiple quarters.

The new question is harder and more valuable: can Falcon become the control and remediation layer for AI-era security?

Q1 made that question worth asking. It did not fully answer it.

This is where I land: the thesis is stronger than it was at $391, but the opportunity is worse. CrowdStrike’s business is proving durability. Its strategy is reaching for infrastructure status. The stock is priced for proof.

Q2 and the second half will decide whether those three statements can coexist.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.