Doordash 1Q26 Earnings: The Two Businesses Inside

Q1 wasn’t about the revenue miss. It was about whether grocery can turn DoorDash from a logistics company into a retail media platform.

TL;DR:

DoorDash’s 10%+ post-earnings rally suggests investors are no longer scoring the company mainly on revenue or take rate, but on GOV growth, order scale, EBITDA, and evidence that CPG advertising is beginning to work.

The core debate is whether grocery can reach break-even at scale; if it can, fulfillment becomes the cost of admission to a much higher-margin advertising business.

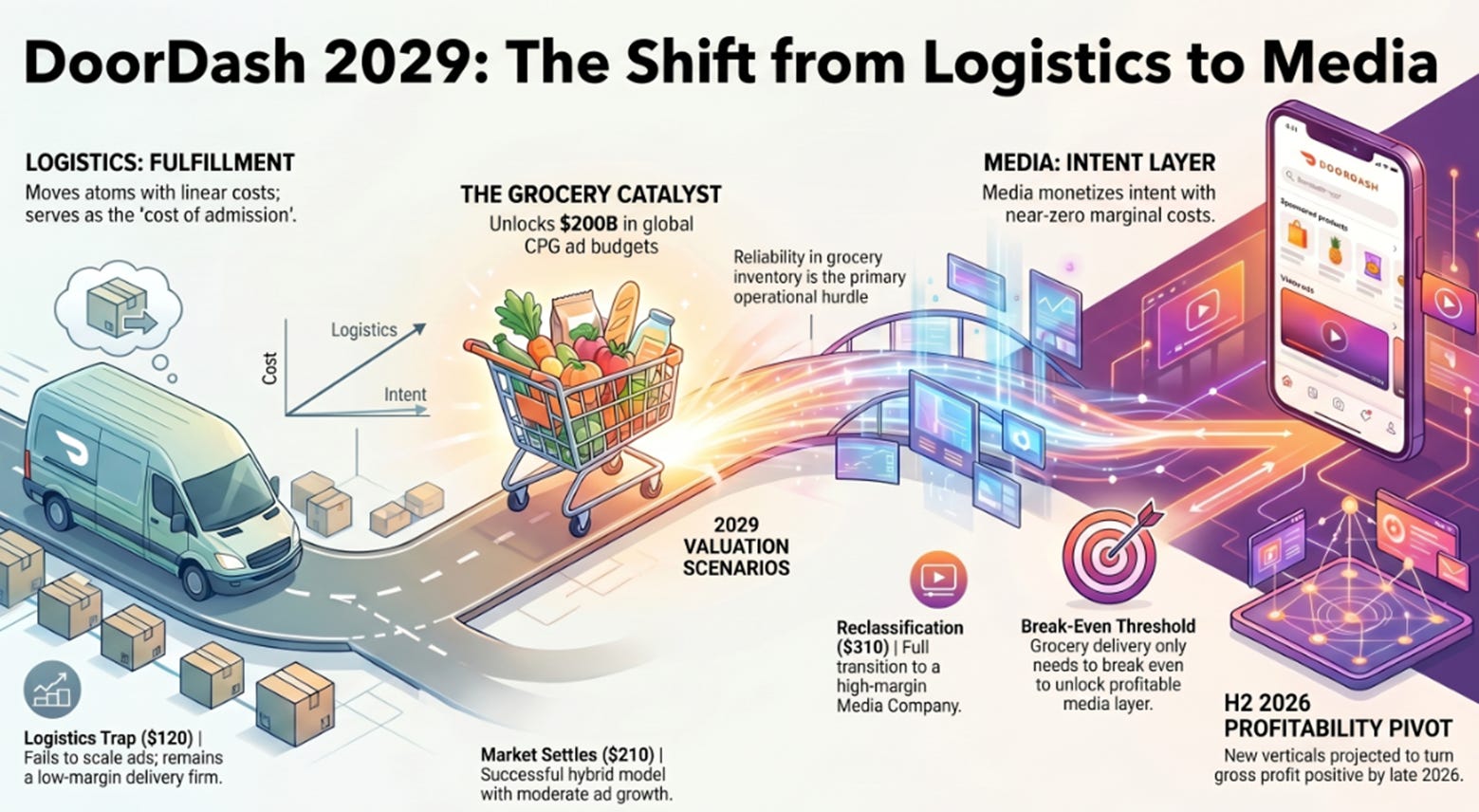

By 2029, DoorDash is either reclassified as a media company with logistics attached, or remains a well-run delivery business priced too richly for its underlying economics.

A number can be true and still lie.

DoorDash reported first-quarter revenue of $4.04 billion, up 33% YoY. The number missed expectations. Net Revenue Margin fell to 12.8%, the lowest in five quarters. Free cash flow was $420 million, down from $494 million a year earlier. Adjusted EBITDA as a percentage of GOV fell to 2.4%, down from 2.6% in both the year-ago quarter and the sequential quarter.

Then the stock went up 10%+.

A stock does not rise sharply after missing revenue unless investors have decided revenue is no longer the number that matters most. The market chose a different set of facts: 933 million orders, $31.6 billion of GOV up 37%, adjusted EBITDA of $754 million, and a Q2 GOV guide of $32.4–33.4 billion against a Street estimate of $32.2 billion. Buried in the Q&A, Tony Xu offered the sentence that almost nobody flagged as the most important thing said all afternoon: DoorDash had, in his words, “cracked the code on CPG advertisers.” Almost no analyst follow-up. No mention in the press release. No quantification.

The market was not saying the quarter was perfect. It was saying the old scoreboard was incomplete. This piece is about what the new scoreboard is actually measuring, and what it implies for where DoorDash is worth in 2029.

In prior pieces we argued that DoorDash was running the Zomato playbook, not the Meituan one; that the Digital Shelf, grocery-enabled CPG advertising, was the single variable determining whether DoorDash was a $150 stock or a $300 stock; and that the Tudor reliability framework explained both the moat and the threat. Q1 didn’t change that thesis. It advanced it.

Two Layers, Two Economies

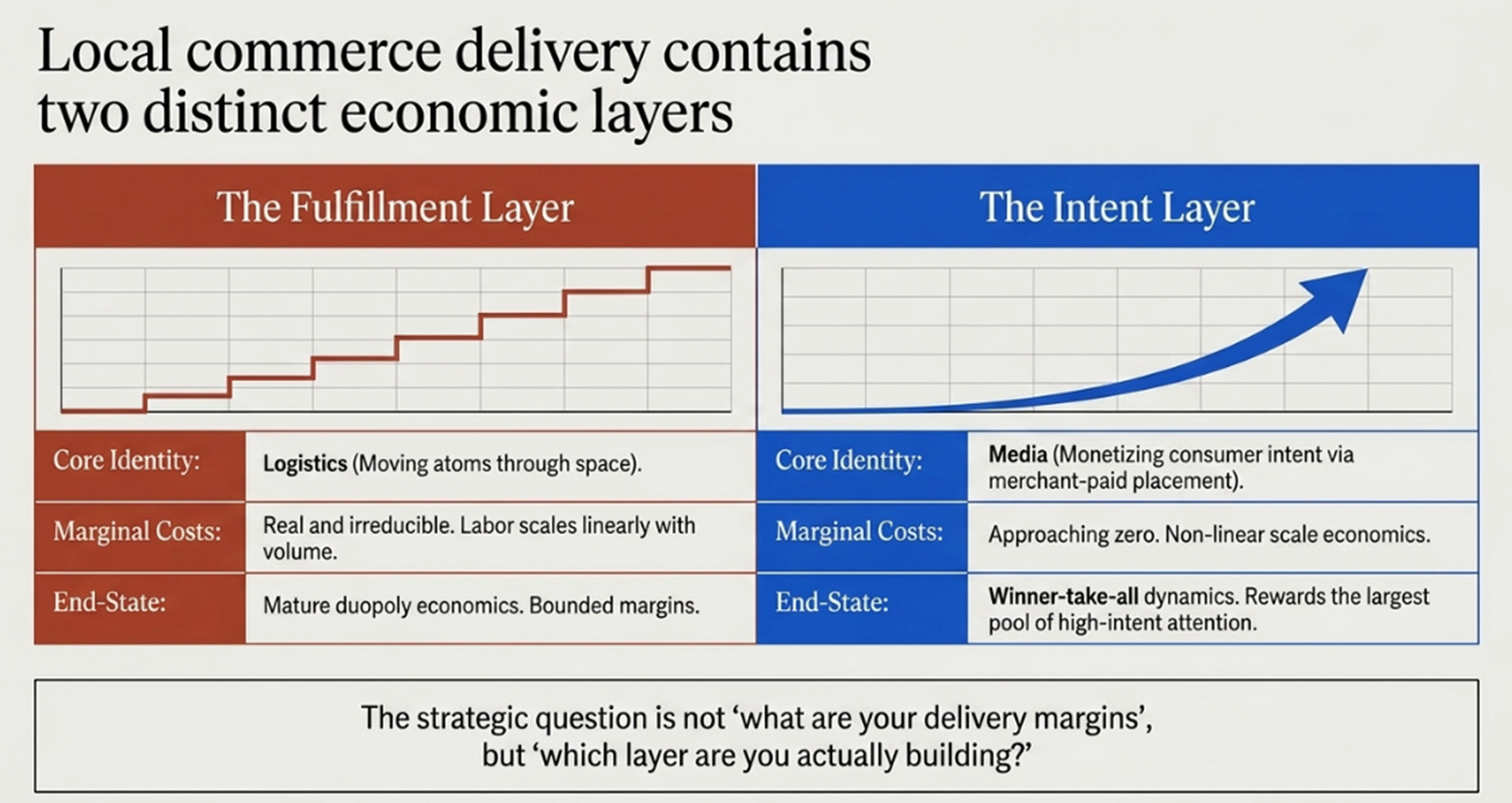

Local commerce delivery contains two distinct economic layers that are routinely conflated. Distinguishing them is the analytical move that makes everything else clear.

The fulfillment layer, moving items from merchants to consumers, is logistics. Marginal costs are real and irreducible. Labor scales linearly with volume. Margins are bounded by the physics of moving atoms through space. The end-state of mature fulfillment markets is duopoly economics, not winner-take-all.

The intent layer, capturing what consumers want before they transact and monetizing that intent through merchant-paid placement, is media. Marginal costs approach zero. Scale economics are non-linear. The structure rewards whoever owns the largest pool of high-intent consumer attention in a given category.

These two layers have different cost curves, different competitive dynamics, and should command different multiples. The strategic question for any local commerce company is not “what are your delivery margins” but “which layer are you actually building, and how far along are you?”

Why Restaurants Capped the First Business, and Why Grocery Doesn’t

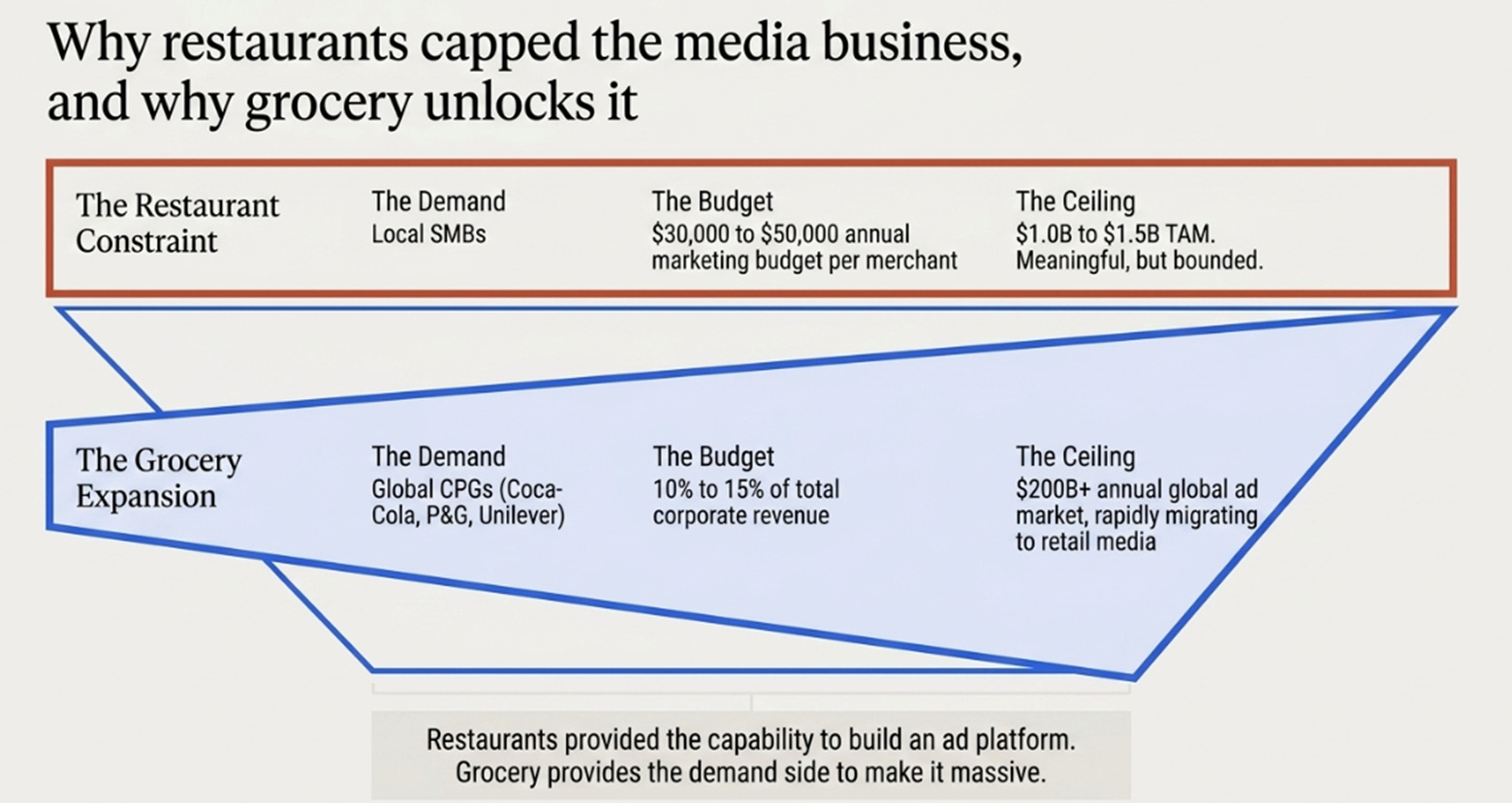

DoorDash spent its first decade dominating restaurant fulfillment. What’s been less examined is why restaurants, despite enormous order volume and rich intent data, couldn’t anchor a transformative media business.

The restaurant advertising market is structurally small. A typical independent restaurant operates with $30,000 to $50,000 of annual marketing budget. Across DoorDash’s merchant base, the addressable advertising opportunity caps at $1 to $1.5 billion. Meaningful, but not transformative. The deeper problem is the demand side: the advertisers paying restaurants to be visible are local SMBs, not large branded buyers running national campaigns. Restaurants gave DoorDash the capability to build a media business but not the demand side to make it large.

Grocery changes the demand side on every dimension that matters. Coca-Cola, Procter & Gamble, Unilever, Kraft Heinz spend 10 to 15 percent of revenue on marketing. Global CPG advertising exceeds $200 billion annually and is migrating toward retail media, where attribution to a purchase is direct rather than inferred. The catalog is different, SKUs map to brands with ad budgets attached. The intent signal is different, grocery purchases are routine, predictable, high-frequency.

The reference case is Amazon. Amazon retail runs at thin margins; Amazon advertising now generates over $50 billion annually at near-pure profit. Retail is the cost of admission to operate the media business at the necessary scale.

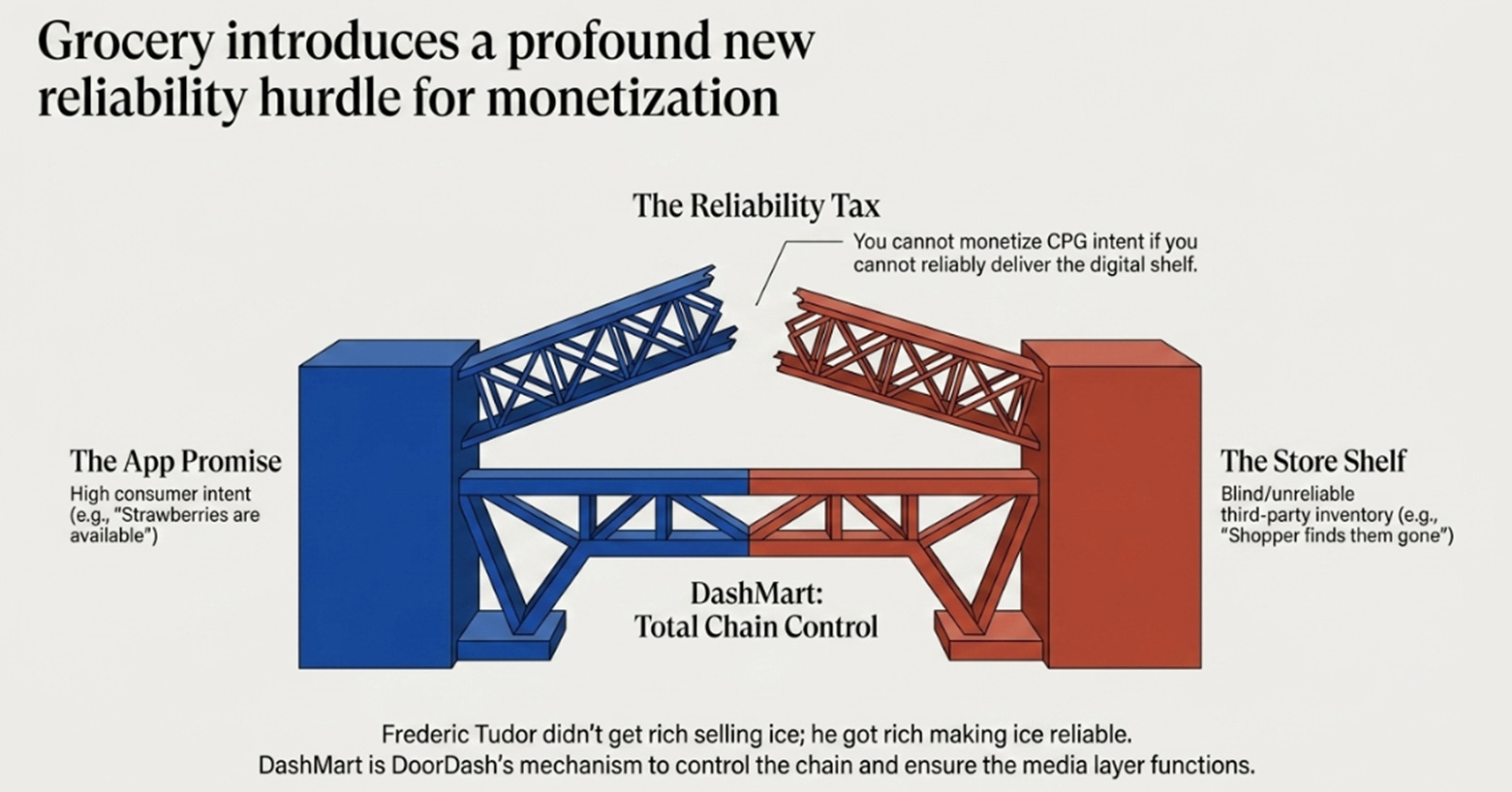

But grocery introduces a problem restaurants didn’t have. Restaurants make the order after it arrives; grocery promises a shelf the platform can’t see accurately. The app says strawberries are available; the shopper arrives to find them gone. This is the Tudor problem, Frederic Tudor didn’t get rich because he sold ice; he got rich because he made ice reliable, and reliability required controlling the entire chain. DoorDash cannot monetize grocery intent if it cannot reliably deliver what was promised on the digital shelf. DashMart is the response. Whether DoorDash can solve grocery reliability at marketplace scale is the operational question that determines whether the second business unlocks.

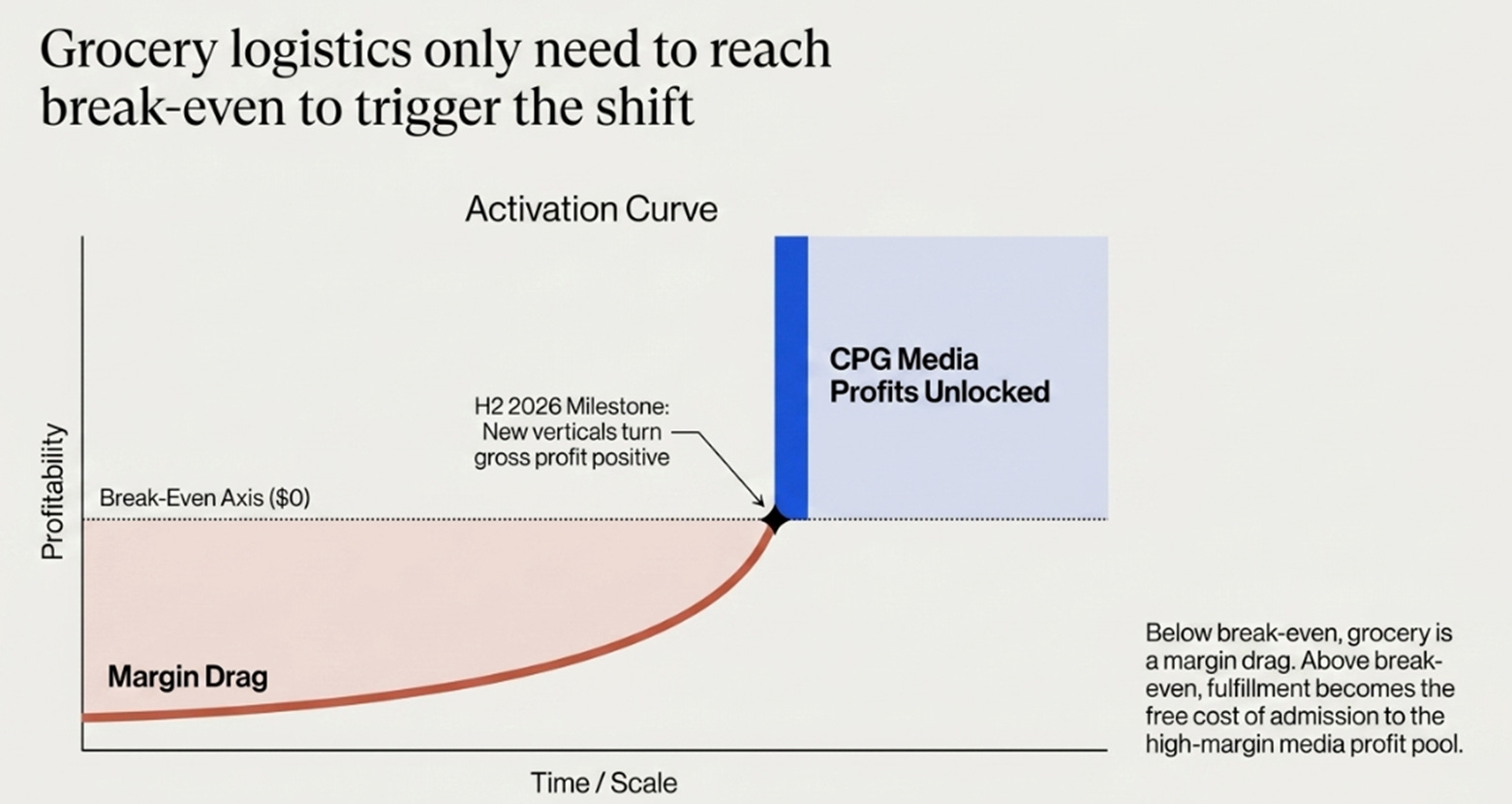

The Break-Even Threshold

Here is the structural claim that defines the entire investment debate: grocery delivery doesn’t need to be profitable. It needs to break even at scale.

Once grocery delivery is unit-economic neutral, every additional order is a free option on the larger advertising business. The fulfillment layer becomes the cost of admission; the media layer becomes the unlocked profit pool. Below break-even, grocery is a margin drag and the media business doesn’t unlock. Above break-even, grocery becomes the substrate, the advertiser pool grows, the data improves, and the company gets revalued.

The competitive race in local commerce is not about who delivers groceries most efficiently. It’s about who reaches grocery break-even first, with sufficient consumer scale to attract CPG advertising at meaningful volume.

Q1 advanced this variable materially. Management disclosed for the first time that new verticals are expected to turn gross profit positive in the second half of 2026. The CPG advertising comment in Q&A was the qualitative companion. Together they form the most consequential disclosure on the call. They are also why the market repriced.

What We Got Right, What We Underweighted

We argued the Digital Shelf was the only variable that mattered for terminal valuation. Q1 confirmed this, the market reacted not to revenue or NRM but to evidence the second business was advancing. We argued the Tudor frame would explain both moat and constraint; the blind storefront problem remains DoorDash’s central operational challenge, and DashMart’s role as a reliability solution is now visible. We argued organic growth at DoorDash’s scale was more durable than the saturation thesis implied. U.S. restaurant GOV growth above the 16-quarter average at 67% market share validates this.

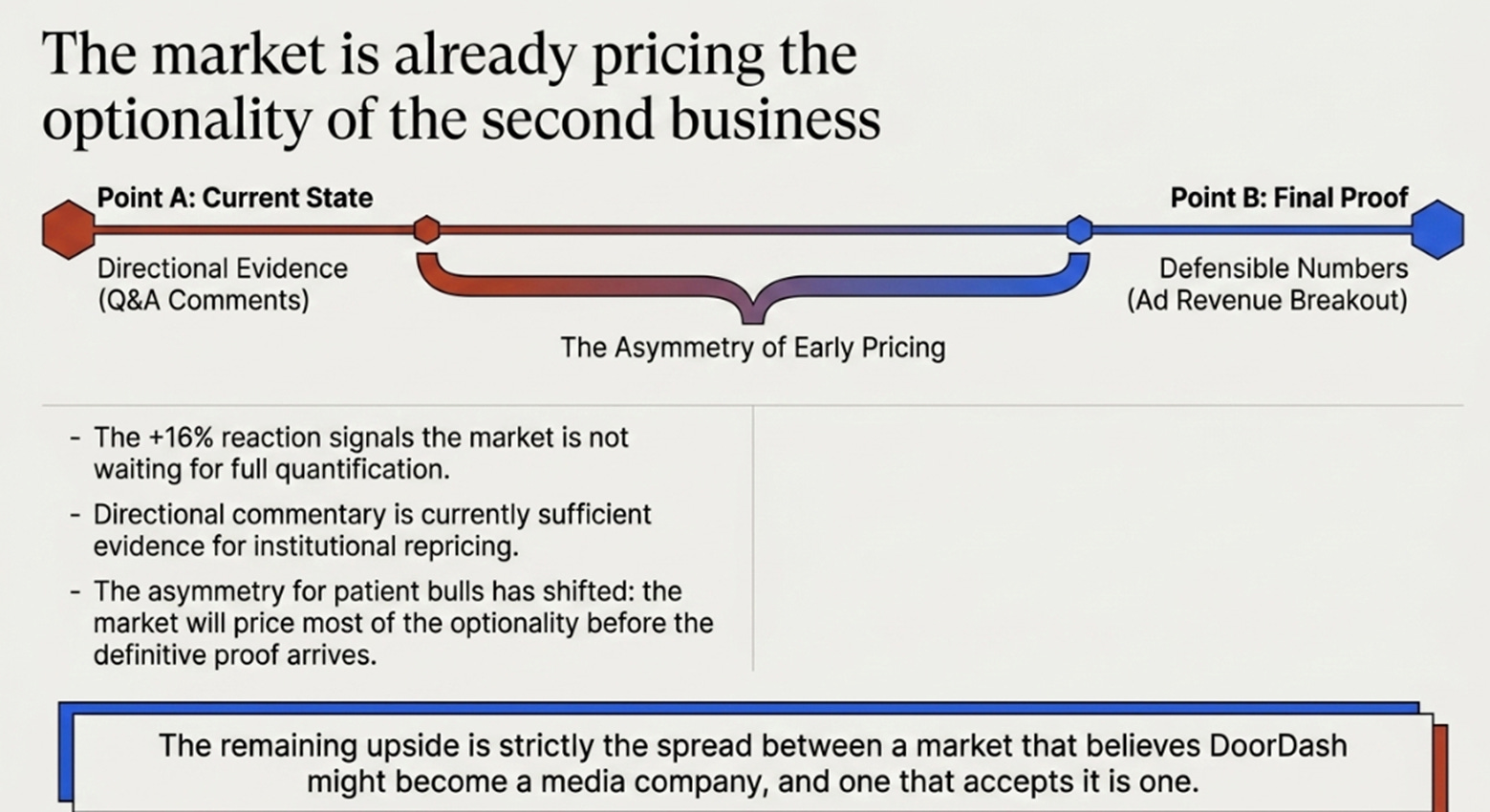

What we underweighted was the speed at which the market would shift scoreboards. Our base case treated Q1 as a modestly positive print where investors began testing whether the framework had changed. Instead, the +16% reaction signals investors are already pricing the optionality of the second business, not waiting for confirmation, not requiring quantification, accepting directional commentary as sufficient evidence to begin repricing. That is a meaningful signal about how this market reads the company.

The implication is uncomfortable for the patient bull. The asymmetry is no longer “wait for proof, then add.” The market will price most of the optionality before the proof arrives. What’s left for the patient investor is the gap between optionality pricing and full reclassification pricing, the spread between a market that believes DoorDash might become a media company and a market that has accepted DoorDash is one. That spread closes only when advertising disclosure becomes specific enough to defend in numbers rather than words. Until then, the stock will trade on incremental directional evidence, with each quarter’s tone potentially worth more than each quarter’s numbers. This is unfamiliar terrain for investors trained to wait for fundamentals.

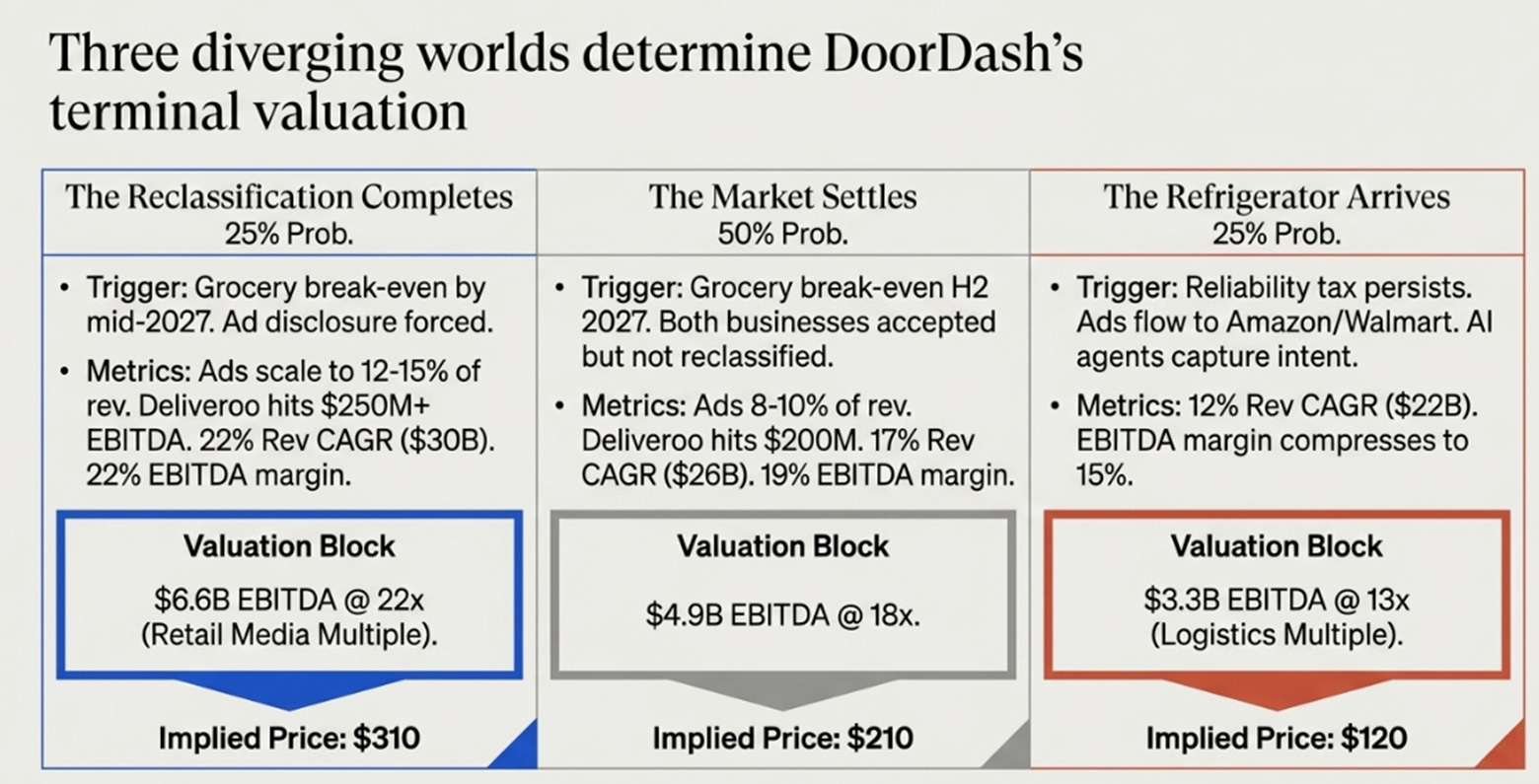

Three Worlds, 2029

The consensus model treats DoorDash as a logistics business with an advertising option. The variant perception is that this is the wrong terminal frame. By 2029, DoorDash is either a media company with a logistics cost of goods sold or a well-run logistics business priced as something it isn’t. The middle outcomes are unstable.

The Reclassification Completes (25%). Grocery reaches break-even by mid-2027. Advertising scales to 12-15% of revenue by 2029, growing 30%+ annually. Deliveroo delivers $250M+ EBITDA by 2027. CPG advertiser concentration becomes large enough that DoorDash discloses it publicly. Revenue CAGR 2025-2029 of 22%, reaching $30B by 2029. EBITDA margin expanding to 22%. 2029 EBITDA of $6.6B at 22x, DoorDash gets repriced as retail media. Implied price: $310.

The Market Settles (50%). Grocery reaches break-even by H2 2027. Advertising reaches 8-10% of revenue by 2029. Deliveroo hits the $200M target. New verticals reach contribution breakeven but don’t drive structural margin expansion. Revenue CAGR of 17%, reaching $26B. EBITDA margin at 19%. 2029 EBITDA of $4.9B at 18x, the market accepts both businesses but doesn’t fully reclassify. Implied price: $210.

The Refrigerator Arrives (25%). Grocery doesn’t reach break-even at marketplace scale; the reliability tax persists. CPG advertising flows to first-party retailers (Walmart, Amazon, Instacart) rather than third-party delivery platforms. AI agents emerge as the primary surface for local commerce intent, capturing the value DoorDash hoped to monetize. Revenue CAGR of 12%, reaching $22B. EBITDA margin compresses to 15%. 2029 EBITDA of $3.3B at 13x, logistics multiple. Implied price: $120.

Probability-weighted price: ≈$215. The asymmetry sits almost entirely in the multiple, not the operating numbers. The 2029 EBITDA range across the three scenarios is $3.3B to $6.6B, a 2x spread. The multiple range is 13x to 22x, a 1.7x spread. But the price range is $120 to $310, a 2.6x spread, because the multiple and EBITDA compound rather than offset. What this means is that the scenarios diverge primarily on what kind of company the market decides DoorDash is, not what kind of company it operationally becomes. The fundamental question over the next three years is not “how fast does DoorDash grow” but “what does the market decide it has been growing into.” At ~$200, the stock prices roughly the base case with modest weight to reclassification.

What to Watch

Five signposts will determine which world materializes. Advertising disclosure is the most important, the moment DoorDash breaks out advertising as a percentage of revenue is the moment the second business is real enough to defend in numbers rather than words. New verticals gross profit positive in H2 2026 must be confirmed in Q3 commentary; deferral materially weakens the thesis. NRM stabilization at 12.5-13.0% while EBITDA/GOV improves means lower take rates are buying something; below 12.5% with no offsetting margin expansion means structural pricing pressure. Deliveroo hitting the $200M FY EBITDA target shifts the international narrative; missing reopens the capital allocation debate. AI agent positioning, whether DoorDash announces proprietary agentic features at scale, and whether any major LLM platform announces direct delivery integration that bypasses DASH, answers the refrigerator question.

The Question That Matters

The Q1 print didn’t answer the structural question. It advanced the timeline on which the answer becomes knowable. By 2029, DoorDash is either operating two businesses on top of each other or one business priced as if it were two. There is no comfortable middle outcome. The market has begun pricing the optionality of the second business; full revaluation requires the disclosure and execution that hasn’t happened yet.

The ice houses are still useful. The question over the next three years is which of these worlds we’re actually in.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.