DoorDash Q4 2025: The Meituan Referendum and the Digital Shelf

The market is pricing Meituan’s destination, but DoorDash is climbing Zomato’s mountain, and one margin variable is worth $100B.

TL;DR:

Q4 confirmed DoorDash’s franchise strength (orders +32%, GOV +39%, cohorts still accelerating), even as margins compressed and guidance missed.

The market’s Meituan framing is consensus, but DoorDash’s true comp is Zomato/Blinkit: same stage, same playbook, harder environment.

If grocery hits breakeven, CPG ads become the margin engine; if not, the stock is structurally capped.

The Hard Choice, Twice

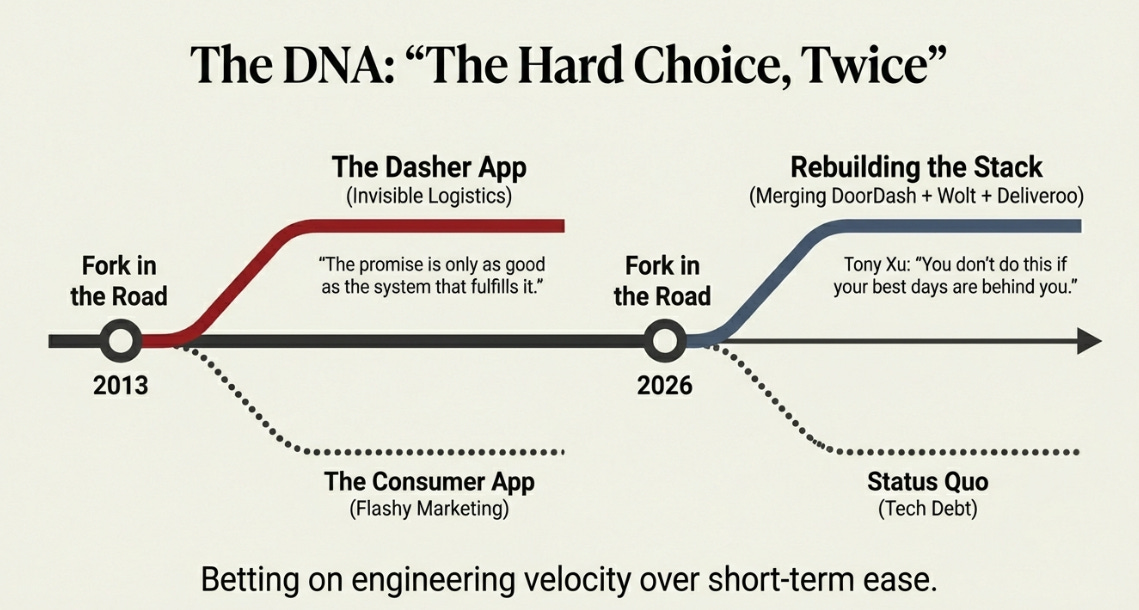

In 2013, DoorDash’s founders faced a decision that would define the company’s DNA. They could build the consumer app first, the visible, marketable product, or the Dasher app first, the invisible coordination layer that determined whether a burrito arrived hot. They chose the Dasher app. The logic was simple and unglamorous: in the physical world, the promise is only as good as the system that fulfills it. Software is necessary but insufficient. What matters is whether someone shows up at your door with the right order, at the right temperature, at the right time.

Thirteen years later, Tony Xu is making the same choice again. DoorDash currently operates three separate technology stacks, DoorDash, Wolt, and Deliveroo, meaning every feature is built three times, data teams work on incompatible systems, and engineering velocity is structurally impaired. Xu called the rebuild a “massive and expensive undertaking” in the Q4 shareholder letter. He also said you don’t do it if your best days are behind you.

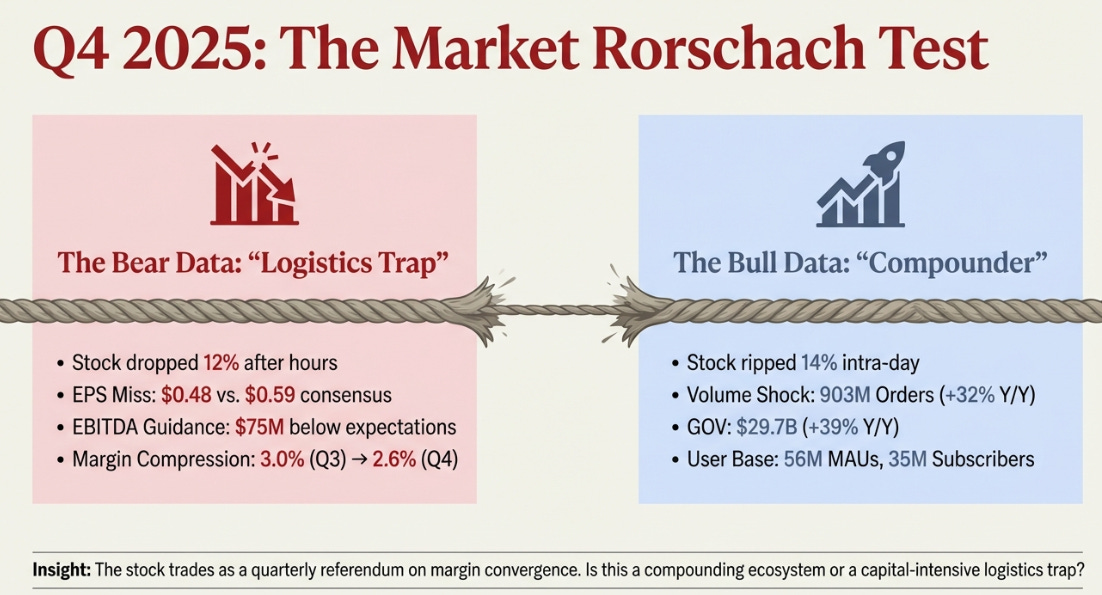

The market’s reaction to Q4 2025 was the Rorschach test you’d expect. The stock dropped 12% after hours on an EPS miss ($0.48 vs. $0.59 consensus) and Q1 EBITDA guidance that landed $75 million below the Street. Then it ripped 14% higher as investors digested 903 million orders (+32% Y/Y), $29.7 billion in GOV (+39%), 56 million MAUs, 35 million subscribers, and Q1 GOV guidance above expectations.

Same data. Two stories. And every sophisticated investor now understands why: the stock trades as a quarterly referendum on whether DoorDash is converging toward Meituan’s economics or trapped in delivery logistics. That framing is consensus. It’s not edge.

The edge is in two places. First: recognizing that DoorDash isn’t tracking toward Meituan at all. It’s tracking toward Zomato, a materially different comparison with materially different implications. Second: identifying the specific mechanism that could break through the margin ceiling the delivery business imposes. That mechanism isn’t hotel bookings or travel or entertainment. It’s the Digital Shelf.

The Wrong Comparison

The market uses Meituan as the destination. This is a mistake.

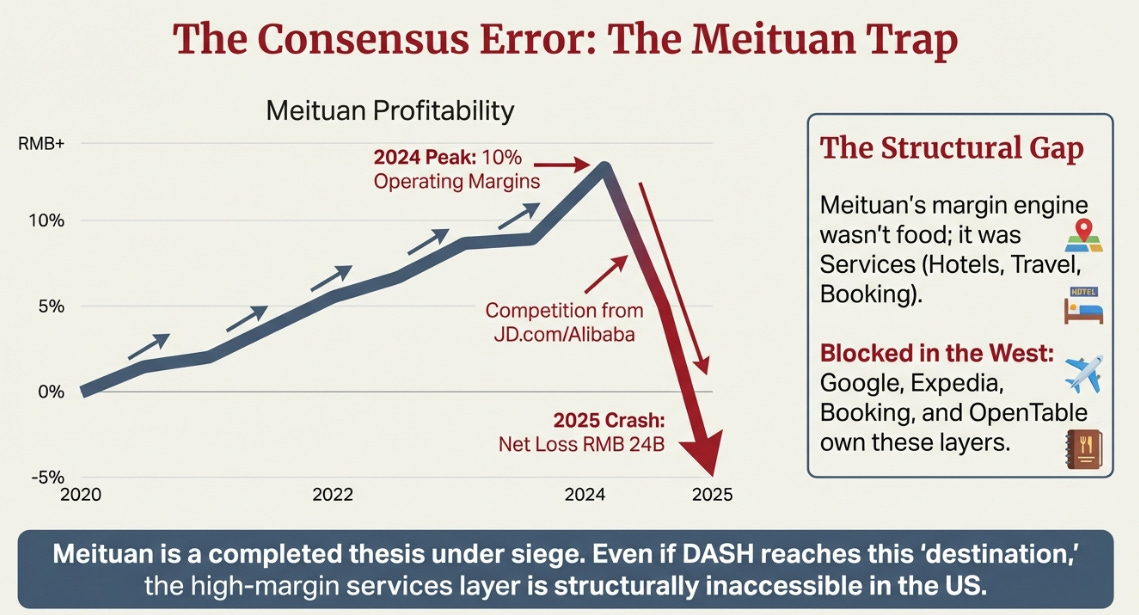

Meituan is the completed version of the local commerce thesis, and it’s under siege. Sixty percent food delivery share. A hundred and fifty million daily orders. Thirty thousand quick commerce warehouses. Seven hundred and seventy million transacting users. Fourteen and a half million merchants. In 2024, Meituan earned RMB 36 billion in profit on roughly 10% operating margins. That is the proven ceiling for this model in the most favorable operating environment on earth: low labor costs, fragmented grocery retail, established super-app consumer behavior, and a regulatory regime that until recently was permissive.

Then 2025 happened. JD.com and Alibaba launched massive incursions into food delivery and instant retail. Meituan was forced to match their subsidies. The expected result for 2025: a net loss of RMB 24 billion. A sixty-billion-yuan profit swing. The destination everyone uses to value DoorDash just demonstrated that even at full maturity, with maximum scale, a well-funded competitor can temporarily destroy the entire earnings base.

Nobody building the DoorDash narrative prices this in.

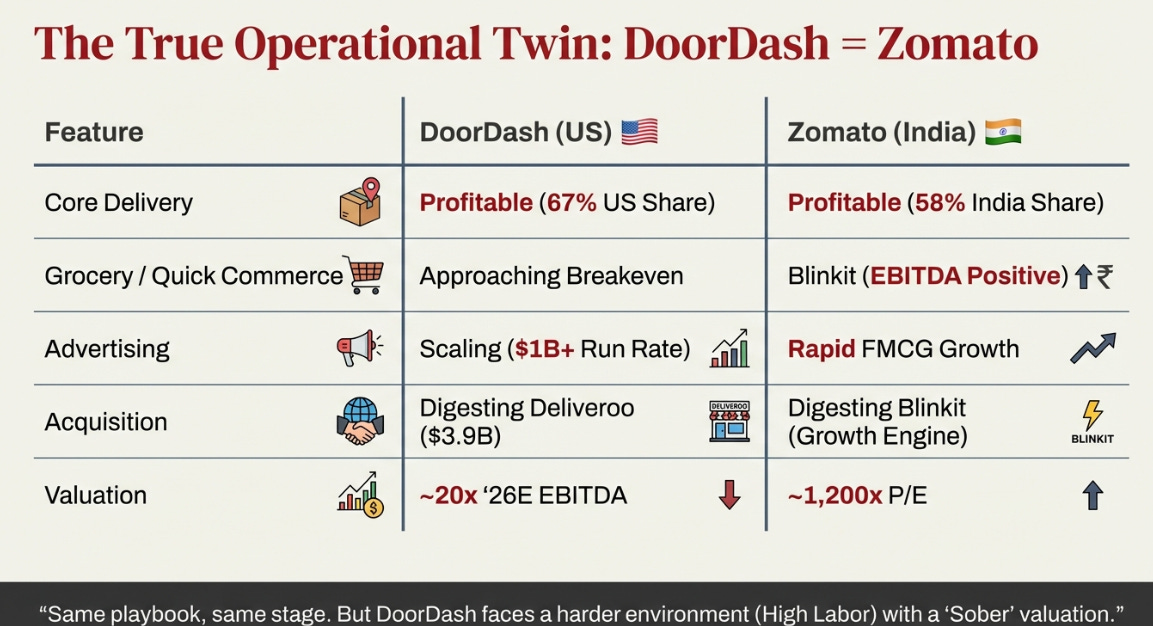

DoorDash’s actual operational twin isn’t Meituan. It’s Zomato, now called Eternal.

Both companies are at base camp. Core delivery profitable. Growth vertical just reaching EBITDA breakeven. Advertising scaling as the high-margin overlay. Major acquisition being digested. Spending through an investment cycle the market punishes. Neither is halfway up the mountain.

But there is a critical structural difference between the two climbs, and between both of them and Meituan.

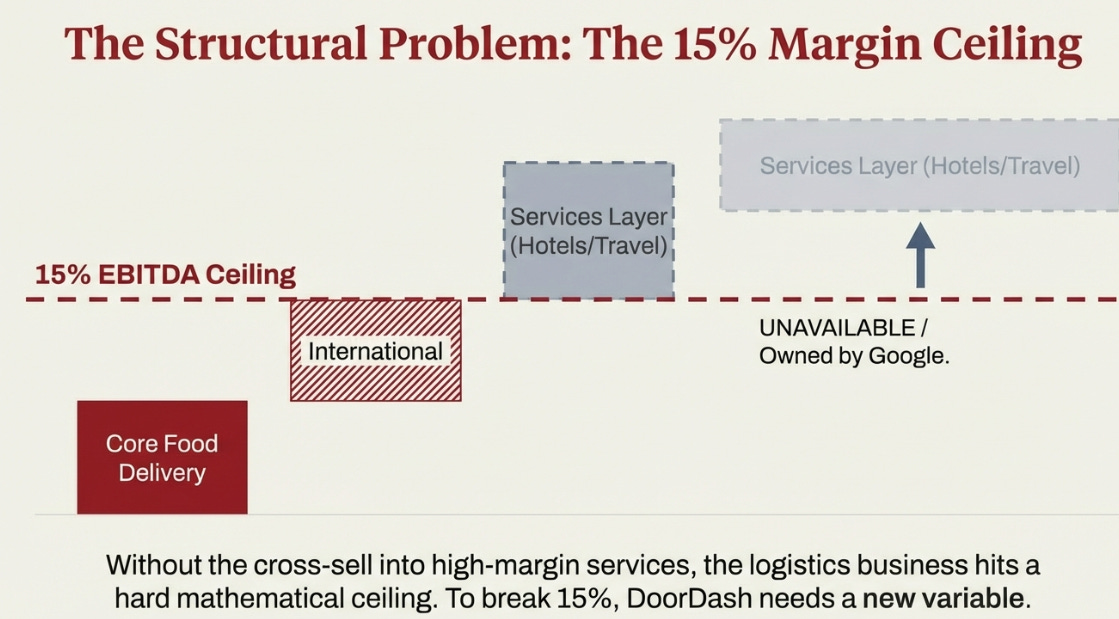

Meituan’s margin engine was never food delivery alone. It was the high-margin services layer, hotel bookings, movie tickets, in-store deals, travel, cross-sold to its massive delivery user base. That business operates on fundamentally different economics than moving food. DoorDash is structurally locked out of this in the West. Booking, Expedia, Google Maps, and OpenTable own those relationships and aren’t ceding them. Zomato’s District segment is trying but remains tiny.

If the services path to high margins is closed, where does the margin unlock come from?

The Digital Shelf

Here is the specific, testable thesis that determines whether DoorDash is worth $100 billion or $300 billion.

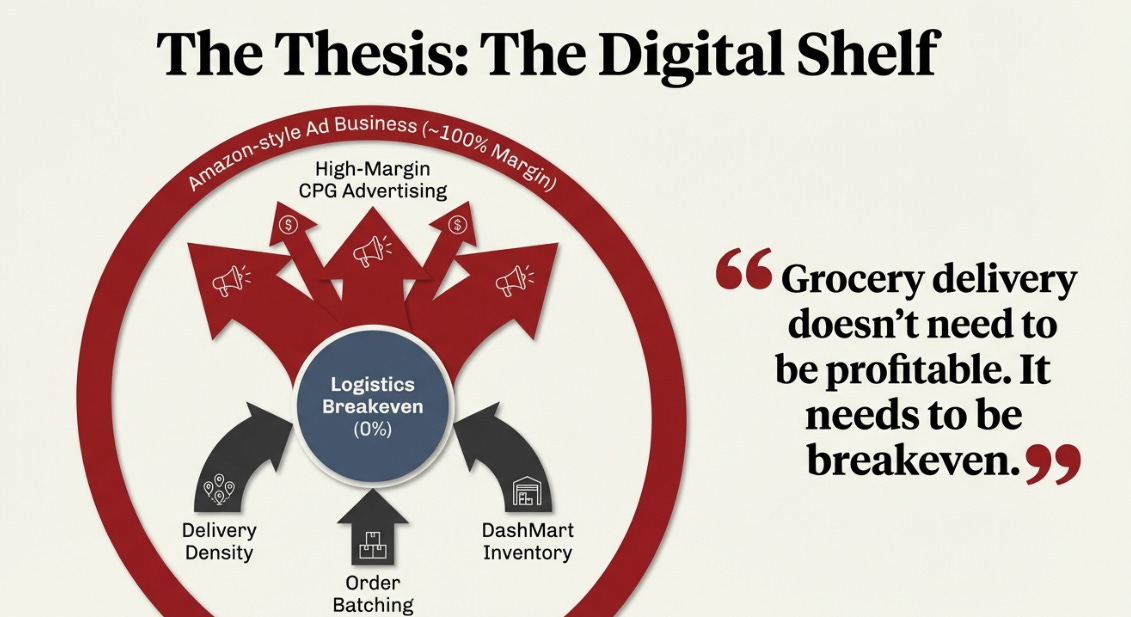

Grocery delivery doesn’t need to be profitable. It needs to break even.

If DoorDash can drive grocery unit economics to roughly zero, through delivery density, order batching, and DashMart inventory control, it unlocks a revenue stream with fundamentally different economics: CPG advertising.

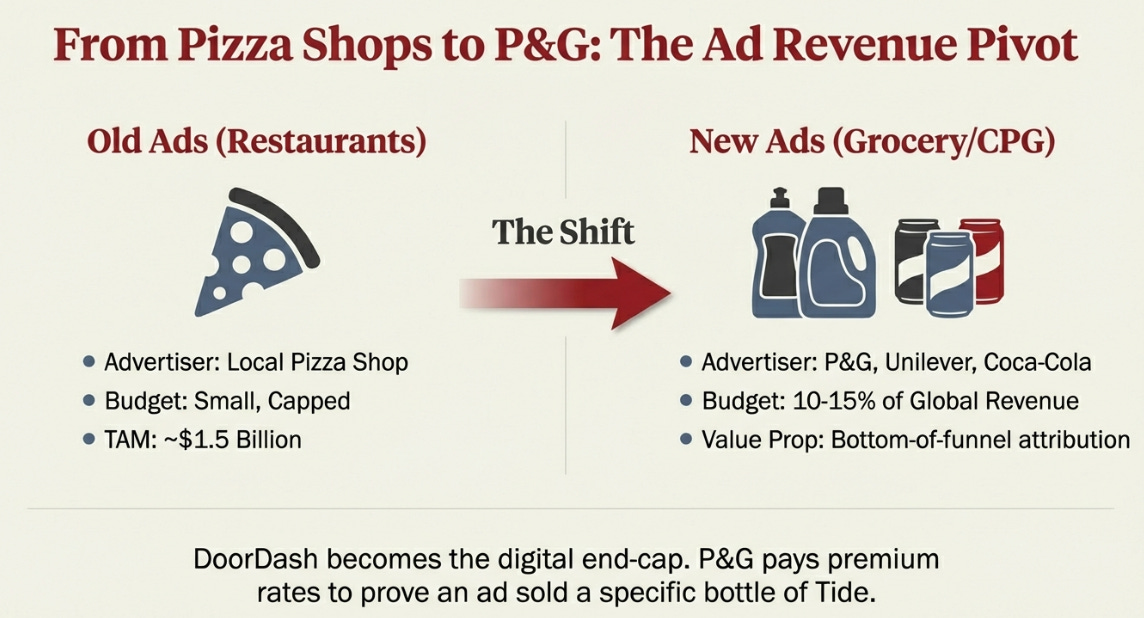

In the restaurant business, DoorDash sells ads to local pizza shops with small marketing budgets. The total addressable market is real but capped, perhaps $1 to $1.5 billion. In grocery, the advertisers are Coca-Cola, Procter & Gamble, and Unilever. These companies spend 10 to 15 percent of revenue on marketing and are desperate for bottom-of-funnel attribution, the ability to show that an ad dollar led directly to a purchase. DoorDash becomes the digital end-cap. Even if the economics of delivering the Tide detergent are breakeven, charging P&G for prominent placement in search results is nearly pure margin. This is how Amazon built a $50 billion advertising business on top of a retail operation with razor-thin product margins.

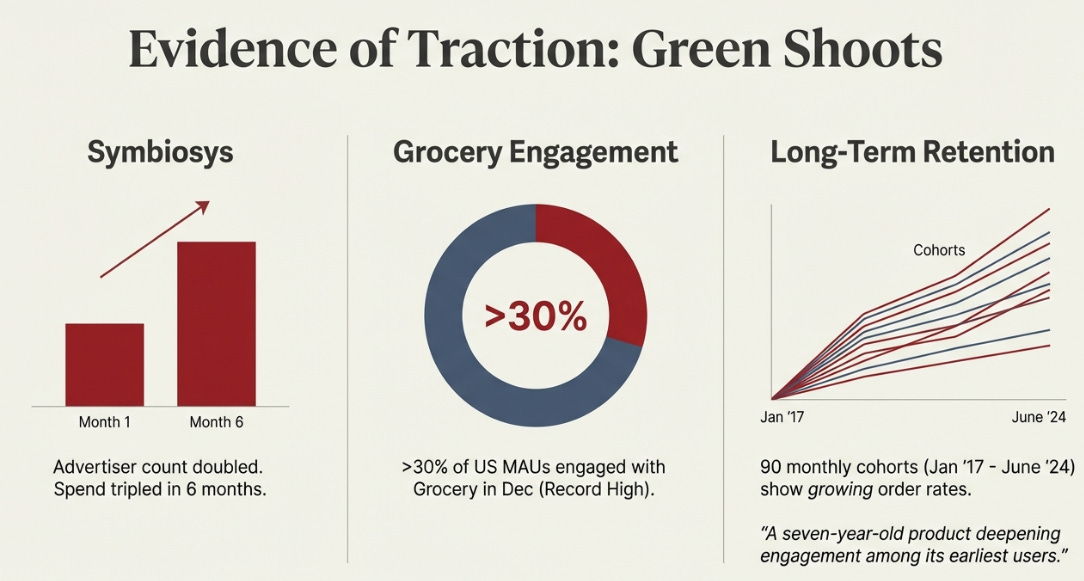

Q4 provided real evidence this is more than theoretical. Symbiosys, DoorDash’s advertising product, doubled its advertiser count and tripled spend in six months. Smart Campaigns, an AI-powered tool that lets merchants run ROI-positive ad campaigns with minimal effort, was described as one of the fastest-growing products in the company. Over 30 percent of U.S. MAUs engaged with grocery in December, a record. The demand side of the equation is working.

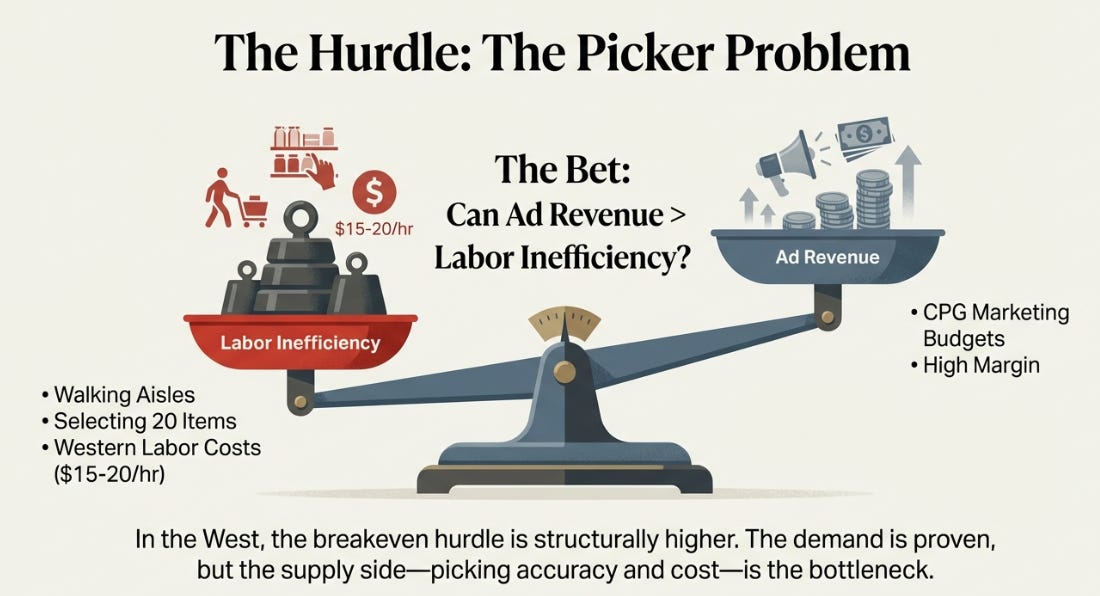

The supply side is harder. This is the Picker Problem. Unlike a restaurant order, where a chef cooks and a Dasher grabs a bag, a grocery order requires someone to walk aisles and select twenty items while maintaining quality and accuracy. That labor cost either falls on the Dasher (tripling delivery economics) or the grocer (raising fees). DashMart solves this by owning inventory and controlling the pick, but it makes DoorDash asset-heavy, exactly the path Zomato took with Blinkit. And in Western markets with $15 to $20-plus hourly labor costs, the breakeven hurdle is structurally higher than in India or China. The demand for grocery delivery is proven. The reliability, substitution rates, pick accuracy, on-time performance, is the bottleneck.

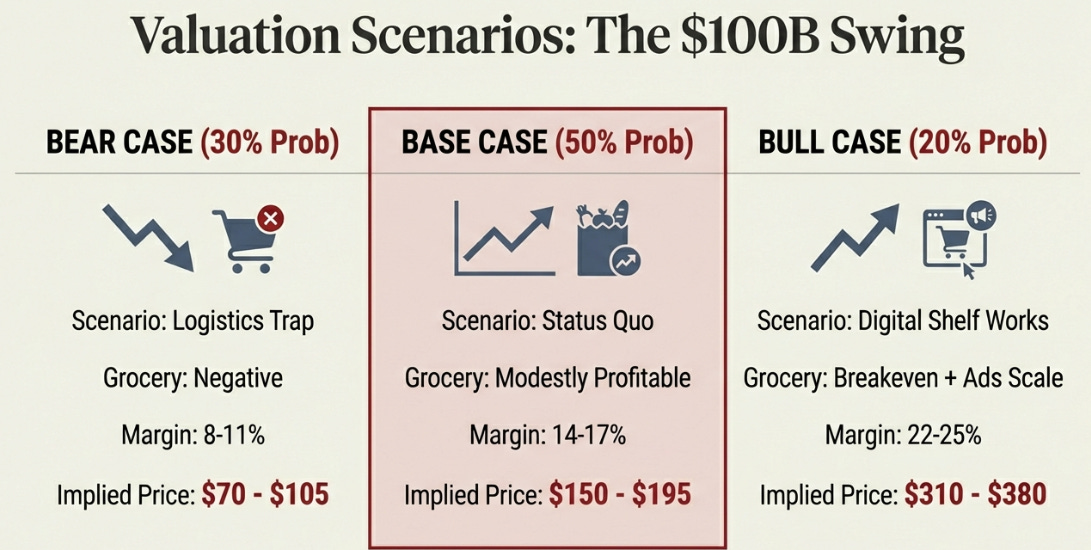

The bet, stated plainly: high-margin ad revenue exceeds high-cost labor inefficiency. That equation is the entire bull case. If it works, DoorDash’s margin ceiling breaks open from 12–15% toward 20-plus percent. If it doesn’t, the ceiling holds and the stock is a $150–175 name permanently.

What Shifted

I should be honest about what Q4 changed.

The pre-earnings thesis, with DASH at roughly $220, was bearish-leaning. DoorDash was priced for Meituan economics in a structurally harder operating environment. Grocery faced margin challenges the market underestimated. Advertising was approaching a restaurant-TAM ceiling. International carried impairment risk. The base case target was $175. The stock fell to $173, apparently vindicating the view.

The margin concern was validated. EBITDA as a percentage of GOV declined from 3.0% in Q3 to 2.6% in Q4. The Q1 EBITDA guide missed by $75 million at the midpoint. The $5 billion buyback authorization remains completely unused, twelve months and a 23% stock decline later, zero shares repurchased. Stock-based compensation of $1.05 billion means GAAP profitability is essentially funded by dilution. On valuation and near-term margins, the bearish lean was correct.

What the thesis underestimated was the franchise momentum, and this matters.

The cohort data is the single most important disclosure in the entire earnings release and it appeared in the operational commentary, not the financials. Every mature restaurant cohort, ninety monthly cohorts spanning January 2017 through June 2024, showed continued strong growth in order rates. Not plateauing. Not stabilizing. Growing. A seven-year-old product deepening engagement among its earliest users. That almost never happens at this scale.

Deliveroo outperformed. It is growing faster under DoorDash ownership at the same profit contribution, the opposite of the digestion-risk thesis. Grocery engagement at 30% of MAUs arrived faster than modeled. And the advertising trajectory, particularly the CPG pivot through Symbiosys and Smart Campaigns, suggests the Digital Shelf is closer than the prior thesis assumed.

The bear case has not been invalidated. It has been narrowed. The margin ceiling concern is structural and intact. But the probability that DoorDash reaches the grocery breakeven threshold needed to unlock CPG advertising has increased. And the compounding duration, how long the growth flywheel spins before maturation, appears longer than the market’s three-year modeling window captures.

Where We Stand

The variant perception is not about what DoorDash is. Everyone is arguing that question, delivery company or local commerce ecosystem. The variant is about a specific number: the steady-state margin ceiling.

Consensus models 24–25% EBITDA margins by 2028. That requires Meituan-like economics in a structurally harder environment. Meituan itself only achieved 10% operating margins at full maturity before the subsidy war destroyed them. Even Zomato, in a more favorable market, targets just 5–6% EBITDA on Blinkit’s net order value at maturity and runs sub-1% consolidated margins after years of scaling. A defensible DoorDash steady-state without the Digital Shelf is 12–15%. With it, if grocery breaks even and CPG advertising scales, 18–22% is achievable.

That single variable, the margin ceiling, swings equity value by roughly $100 billion between the bull and bear cases.

The market is making two offsetting errors. It is too optimistic about how high margins go, because it models the Meituan destination in a Western environment that structurally cannot replicate it. It is too pessimistic about how long the compounding lasts, because cohort data, cross-category adoption, and subscriber economics suggest the growth runway extends well beyond the typical three-year DCF window. These errors roughly cancel at $173. The stock is fairly valued for the wrong reasons.

This creates asymmetric positioning depending on time horizon. A twelve-month trader faces margin disappointment as the primary near-term risk. A three-to-five-year holder is buying compounding duration the market refuses to underwrite.

Three Paths to 2029

Expected value across scenarios: roughly $175–200. At $173, the stock prices the base case, not the bull that the narrative machine promotes, not the bear that quarterly margin misses provoke.

One observation worth making: Zomato at $30 billion is priced somewhere between its own bull and super-bull case for essentially the same stage of the same journey in an easier environment. If you believe both companies are running the same playbook, DoorDash’s pricing is the sober one.

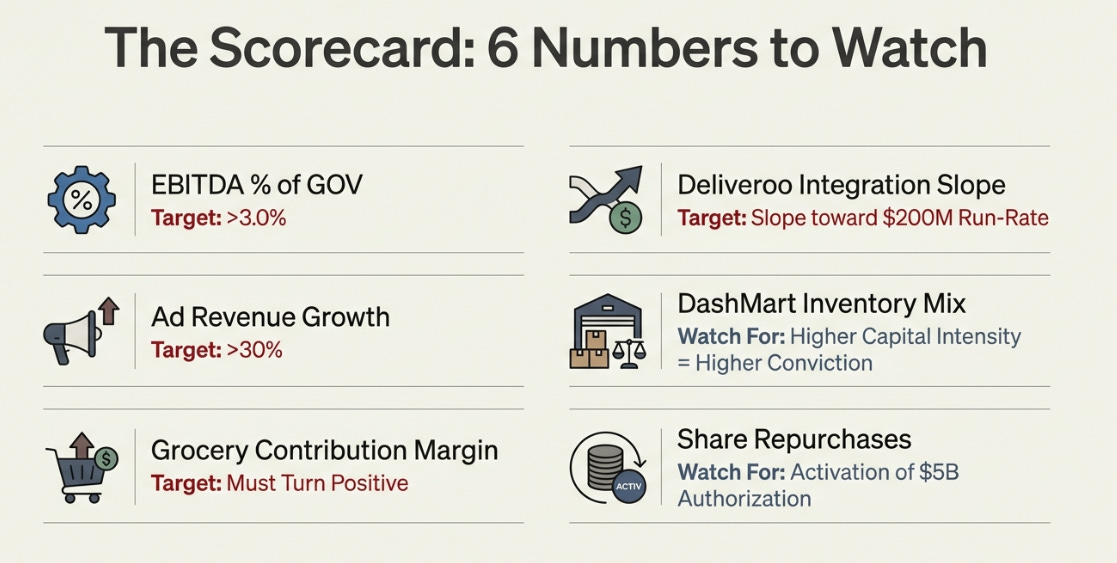

The Scorecard

Six numbers that will resolve this debate over the next four quarters. No interpretation needed, the thresholds speak for themselves.

EBITDA as % of GOV. Above 3.0% sustained signals base-to-bull. Below 2.5% signals bear.

Advertising revenue as % of total revenue. Disclosed and growing above 30% annually is the bull case materializing. Decelerating below 20% means the Digital Shelf isn’t valuable enough.

Grocery contribution margin, the actual number. Positive and expanding validates the base case. Still described in qualitative terms by the end of 2026 is a bear signal. Management has avoided quantifying this. Demand specificity.

Deliveroo quarterly EBITDA. The $200 million annual target requires roughly $55–70 million per quarter in H2 2026. Track the slope of the ramp, not the endpoint.

DashMart and owned-inventory mix. Aggressive expansion means DoorDash is committing to the Zomato model, higher conviction on the Digital Shelf thesis, but lower returns on invested capital. Watch capital intensity alongside growth.

Share repurchase activity. Any activation of the $5 billion authorization signals management conviction that the equity is undervalued. Continued inaction, now twelve months and counting, signals they either don’t believe the stock is cheap or prefer reinvestment over returns. Either answer is informative.

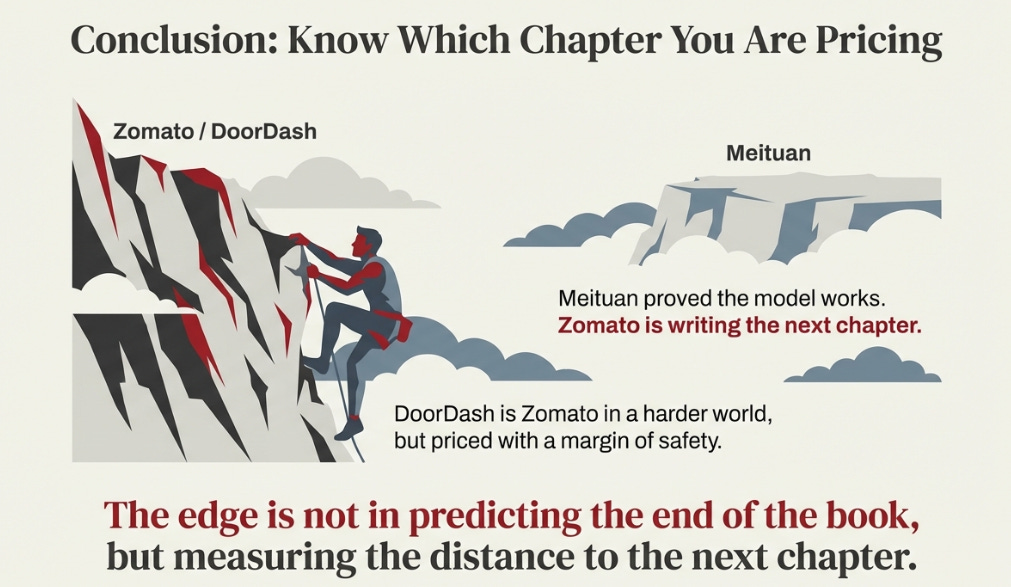

Which Chapter You’re Pricing

DoorDash, Zomato, and Meituan are all running the same playbook. Meituan proved it works at enormous scale, and then proved it can break in a single year when well-funded competitors decide to attack. Zomato is one chapter ahead of DoorDash and priced as though every remaining chapter writes itself. DoorDash is the most reasonably valued of the three, operating in the most difficult environment.

The earlier thesis said overvalued at $220. The updated thesis says fairly valued at $173, with the Digital Shelf as the single variable that creates asymmetry in both directions. If grocery breaks even and CPG advertising scales, the margin ceiling breaks open and the stock is worth north of $300. If the logistics costs prove irreducible, the ceiling holds and this is a $150 name with limited upside from here.

The market is voting on resemblance to Meituan. The edge is in measuring distance, and right now, that distance looks a lot more like Zomato’s present than Meituan’s past. Knowing which chapter you’re paying for is worth more than knowing how the book ends.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.