Everpure (Pure Storage) 4QFY26 Earnings: The Intelligence Layer Monetizes

Everpure's Q4 proved that controlling how flash is managed is worth more than selling the flash itself.

TL;DR

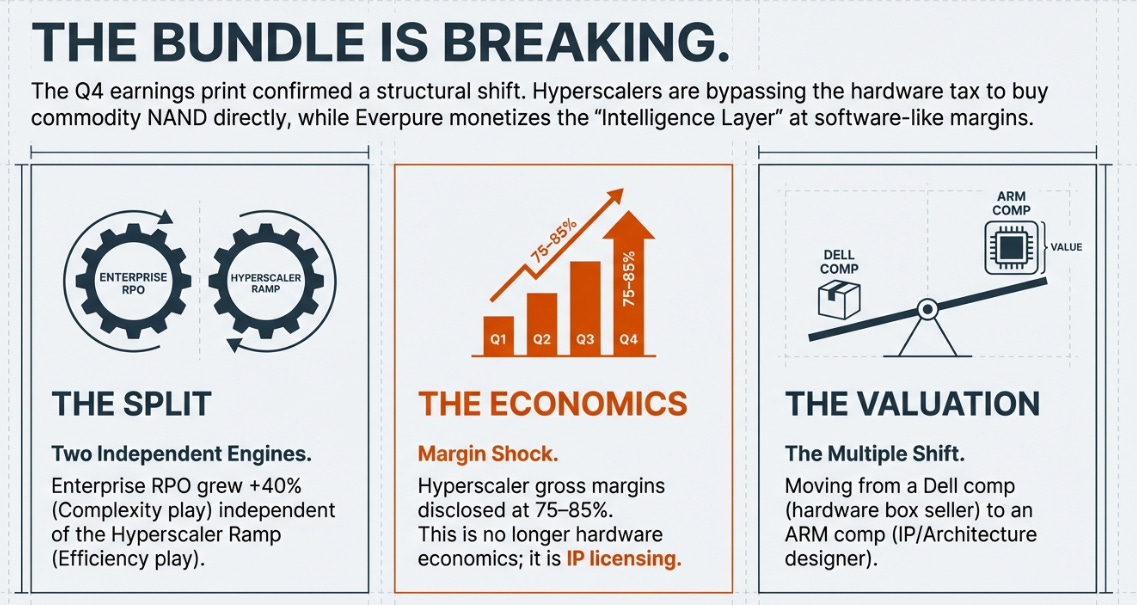

The bundle is breaking. Hyperscalers now buy NAND directly while Everpure monetizes the control layer at 75–85% gross margins.

Two engines, independent. Enterprise RPO +40% (no hyperscaler), while hyperscaler revenue ramps in H2 at structurally higher margins.

The comp set is wrong. If the intelligence layer wins, Everpure starts to look less like Dell and more like ARM.

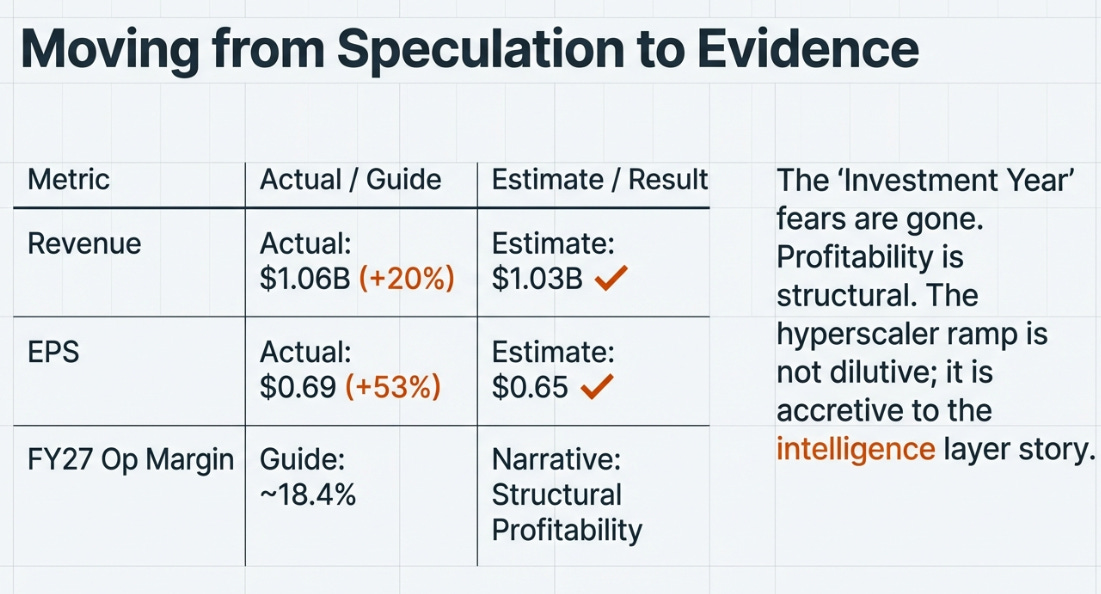

“Pure Storage forecast first-quarter revenue of $990 million to $1.01 billion, estimate $920.8 million. Fourth quarter adjusted EPS 69c vs. 45c y/y, estimate 65c. Revenue $1.06 billion, +20% y/y, estimate $1.03 billion.” , Bloomberg

The Job That Changed

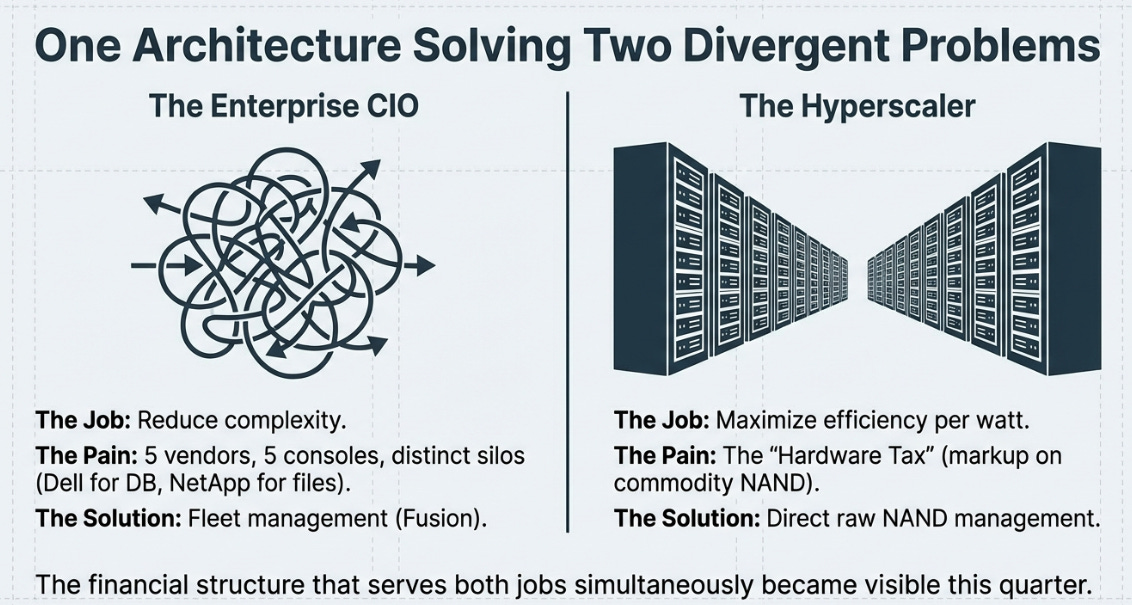

A storage architect at a mid-size bank once described his job to me as: “I spend 80% of my time managing five vendors’ incompatible systems, and 20% actually thinking about data.” Dell for databases. NetApp for file shares. A legacy HPE array nobody wanted to touch. An Isilon cluster for unstructured data. A Pure FlashArray someone piloted for virtualization. Five vendors, five consoles, five upgrade cycles, five sales reps.

His problem wasn’t speed or capacity. It was complexity. Every new workload , an analytics project, an AI proof-of-concept, a compliance archive , meant evaluating which vendor’s box fit, negotiating a purchase, integrating it, training the team. The job he was hiring storage to do wasn’t “store bits fast.” It was: reduce the operational surface area of managing enterprise data so I can focus on what the data is actually for.

That job explains why Everpure’s RPO grew 40% this quarter. But I’m getting ahead of myself.

For a hyperscaler like Meta, the job is fundamentally different. When you’re deploying exabytes to feed thousands of GPUs, the constraints are power, cooling, and floor space. The “tax” embedded in every storage vendor’s product , the markup on commodity NAND, the overhead of SSD controllers translating flash into something legacy software understands , becomes intolerable at that scale. The hyperscaler’s job isn’t “simplify my vendors.” It’s: deliver maximum storage efficiency per watt, and don’t make me pay for your commodity markup.

Two very different jobs. One architecture. And this quarter, for the first time, the financial structure that serves both jobs simultaneously became visible.

The Bundle That’s Splitting

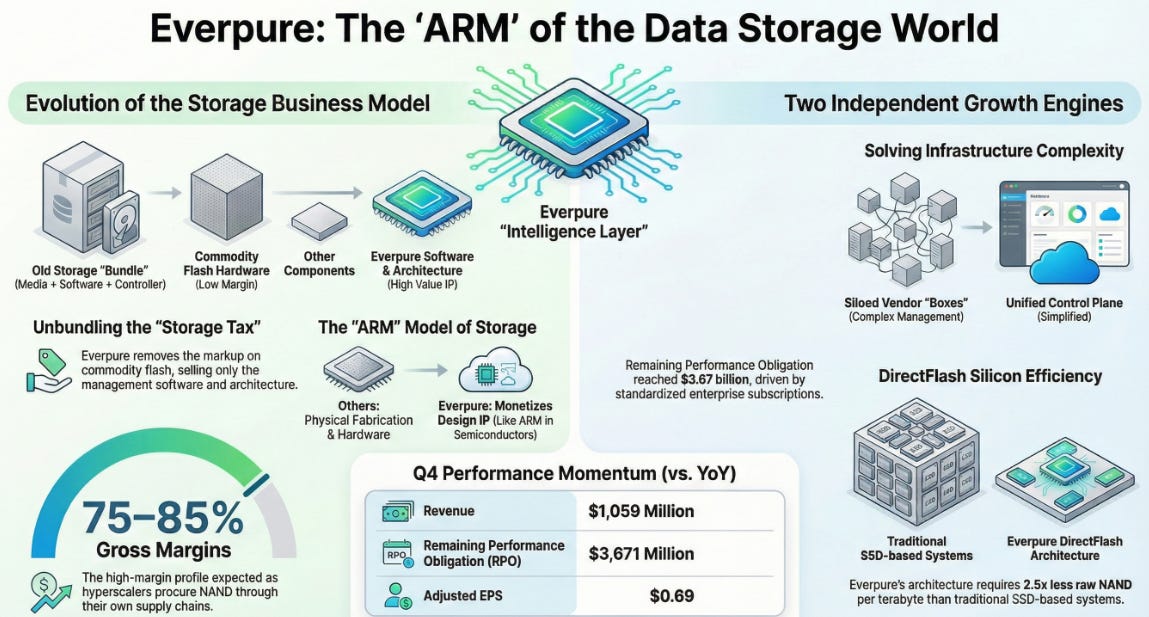

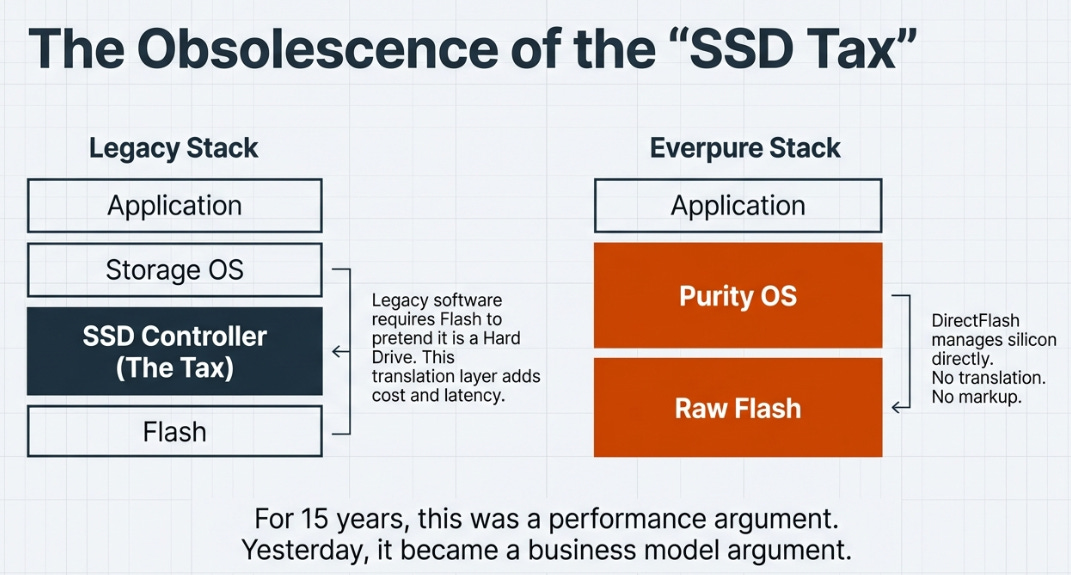

For fifty years, storage was sold as a bundle: media + controller + software, wrapped in a box. This made sense when the media had mechanical constraints , spinning disks needed tightly coupled firmware that understood seek times and rotational latency.

Flash has no mechanical constraints. The reason for the bundle disappeared. But the bundle persisted, because when the industry moved from disks to SSDs, the SSD manufacturers inserted a translation layer , embedded controllers and DRAM caches that made flash pretend to be a disk so legacy storage software could keep working. The entire industry paid a tax for backward compatibility, and nobody questioned it because it worked well enough.

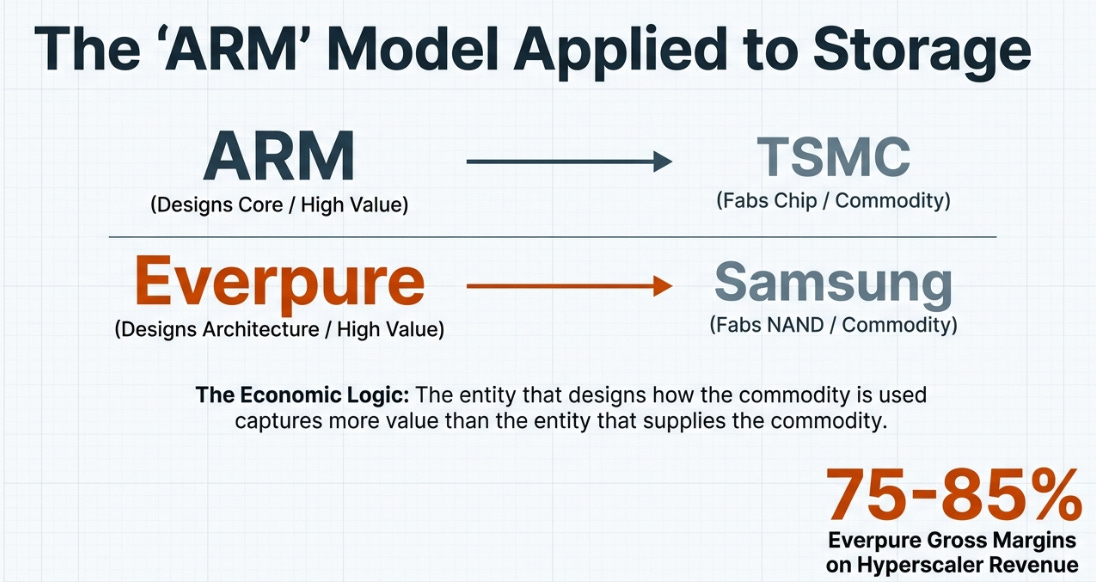

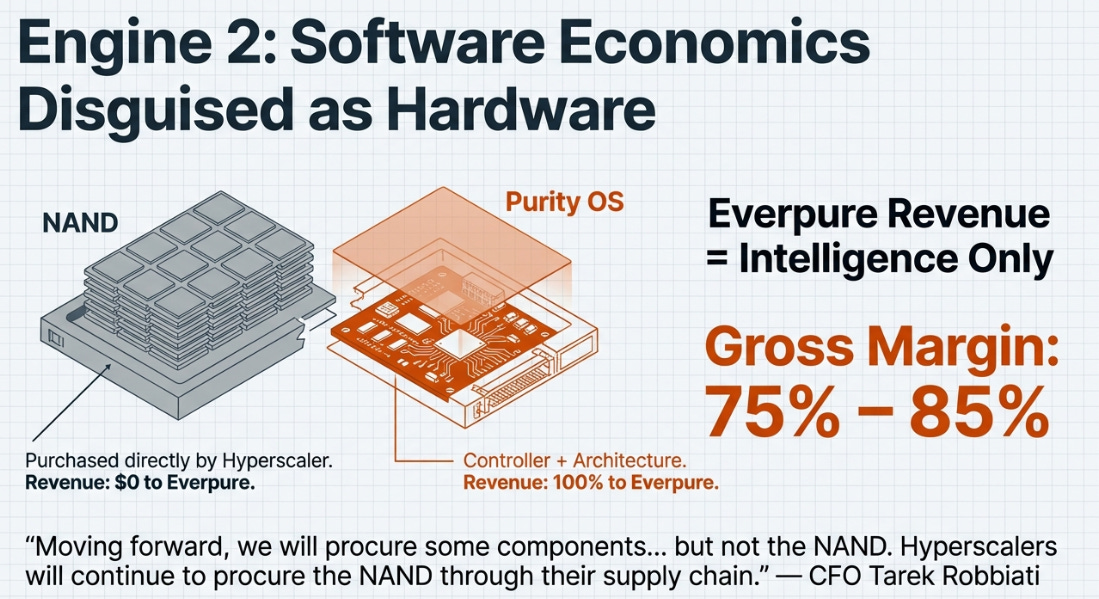

Pure Storage , now Everpure , was founded in 2009 on the bet that “well enough” was a trap. They bought raw NAND wafers directly from the fabs, built their own flash modules (DirectFlash), and wrote an operating system (Purity) that manages flash at the silicon level. No SSD. No translation. No lie.

For fifteen years, this was a performance argument. Yesterday, it became a business model argument. CFO Tarek Robbiati:

“Moving forward, we will procure some of the components that are needed by hyperscalers to build their solution in their environment, but not the NAND. Hyperscalers will continue to procure the NAND through their supply chain. As a result, we expect gross margins of hyperscaler revenues to range between 75%–85%.”

Read that carefully. The hyperscaler buys the commodity (NAND) directly from Samsung or SK hynix. Everpure provides the intelligence layer , the modules, the software, the architecture that makes raw flash perform at exabyte scale. Everpure keeps 75–85% gross margins because what they’re selling isn’t flash. It’s the thing that makes flash work.

This is the same economic separation that made ARM valuable in semiconductors. ARM doesn’t fabricate chips. TSMC does. ARM provides the architecture , the instruction set, the core designs , and captures margin on every chip shipped without touching the silicon. The entity that designs how the commodity is used captures more value than the entity that supplies the commodity.

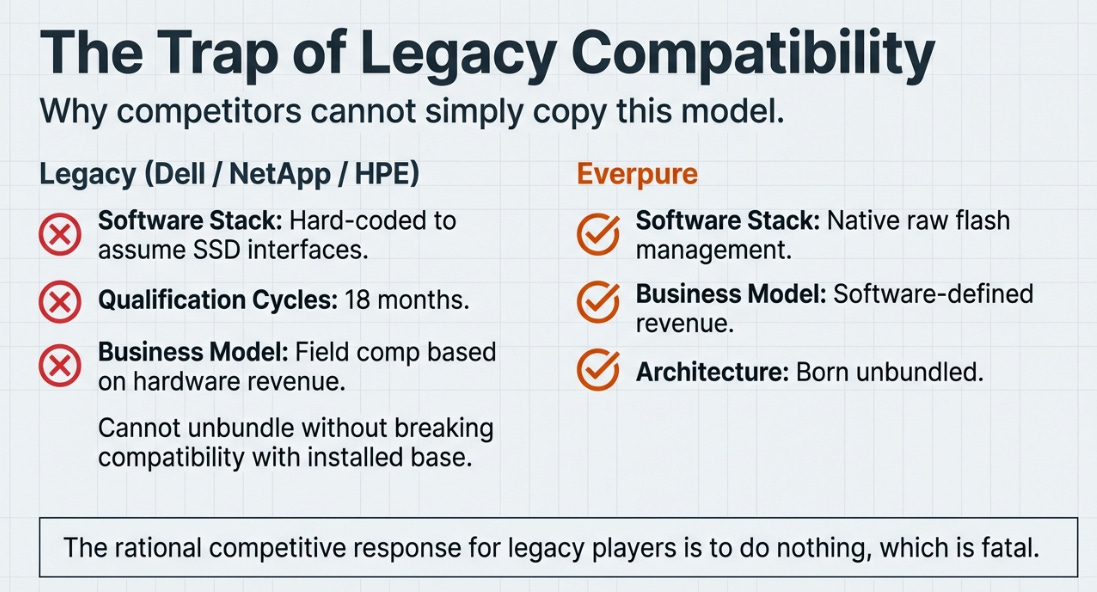

And here’s the part that makes this structural, not anecdotal: Dell, NetApp, and HPE cannot replicate this model. Their storage software assumes it’s talking to an SSD interface. Rewriting it to manage raw NAND would mean rebuilding the stack from scratch and breaking compatibility with billions of dollars of installed base. Their qualification processes take 18 months. Their partner agreements with Samsung and Micron assume finished drives. Their field compensation models are built on SSD-era margin structures. The bundle isn’t a choice for them , it’s an architectural dependency baked into decades of code. The rational competitive response to Pure’s unbundling is to do nothing. Which is exactly what makes it fatal.

Two Independent Engines

I think the most underappreciated aspect of this print is that Everpure is running two growth engines that operate independently , and this quarter proved both are firing.

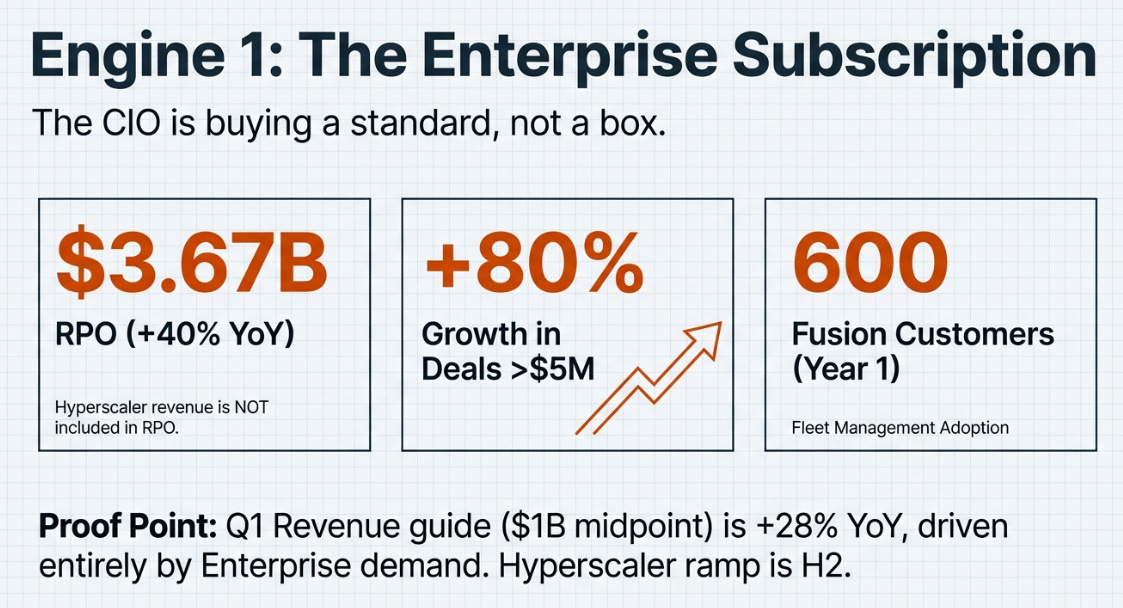

Engine 1: Enterprise franchise. RPO grew 40% to $3.67 billion , an acceleration from 24% last quarter and a sequential increase of $728 million. Robbiati confirmed, in response to a direct question, that hyperscaler revenue is not included in RPO. This is pure enterprise and subscription commitment. Deals over $5 million grew 80% year-over-year. Fortune 500 penetration hit 64%. Fusion , the unified control plane that manages all of a customer’s arrays as one fleet , reached 600 customers in its first year.

This is the CIO from my opening solving his five-vendor problem. He’s not buying boxes for individual workloads anymore. He’s signing multi-year contracts to standardize his entire infrastructure on one operating system. Transactions are competed quarterly. Franchises compound.

Engine 2: Hyperscaler ramp. Management expects hyperscaler revenue to “significantly accelerate” in FY27, concentrated in Q3 and Q4 as it follows data center buildout schedules. Low double-digit exabytes expected , above prior expectations. The standardized commercial model (75–85% GM) wasn’t designed for one customer. It’s a template. CEO Charlie Giancarlo confirmed they’re in “engineering test environments in multiples of the hyperscalers” with “wider interest, broader engagement.” But he was also careful: “until we have another one to announce, we’re still in the fight and not yet at the finish line.”

The Q1 guide is the proof that Engine 1 operates independently. The $1 billion midpoint , 8.6% above the $921 million consensus , comes with no hyperscaler contribution (that’s H2) and minimal pricing benefit (the February 9 price increase doesn’t flow through until Q2 because of 90-day quote windows). Giancarlo was explicit: “Q4 in particular, and Q1 is really all demand-based.” That’s the enterprise franchise engine producing 28% year-over-year growth on its own.

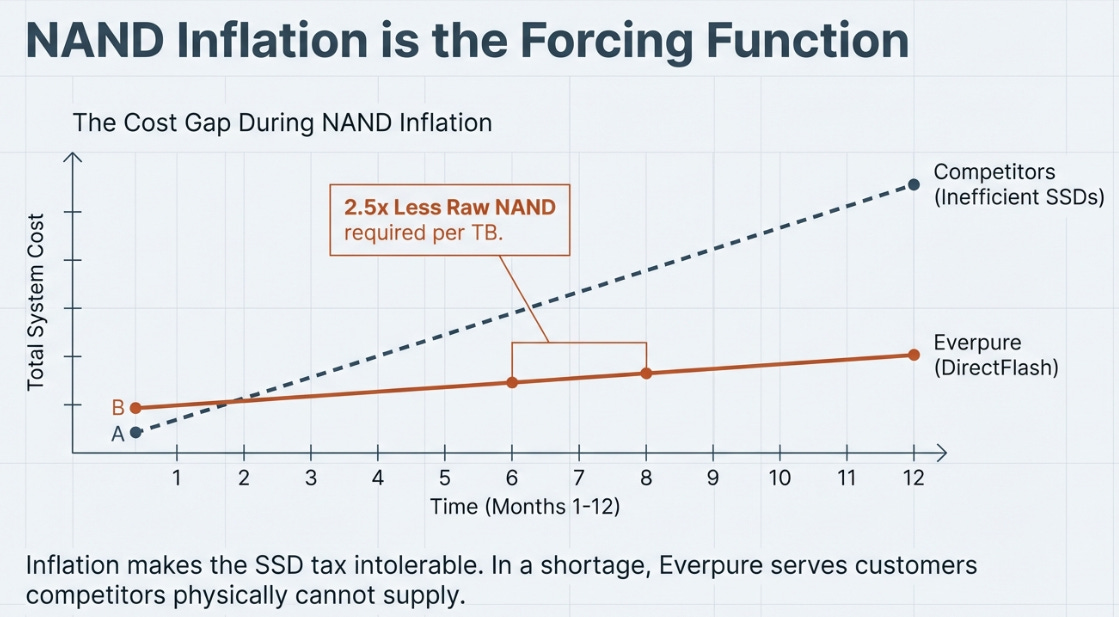

One paragraph on NAND, because it matters but not in the way most analysts think. Components have “more than doubled” in six months. Pure raised prices ~20% , last in the industry, lowest increase. Q1 product margins will trough at the low end of 65–70%. But Pure’s DirectFlash architecture needs roughly 2.5x less raw NAND per usable terabyte than Dell’s SSD-based systems (QLC vs. TLC flash, 10:1 vs. 4:1 data reduction). When NAND doubles in price, the cost gap widens. In a shortage, Pure can serve customers Dell physically cannot supply. NAND inflation isn’t a headwind to manage , it’s the forcing function that makes the SSD tax visible to every buyer, accelerating the very unbundling that favors Pure’s architecture.

Variant Perception

The consensus view: Everpure is a premium storage company recovering from a Q3 communication mishap, managing through NAND headwinds, with an impressive but concentrated hyperscaler relationship.

I think the correct framing is different: the storage value chain is permanently splitting into commodity media and differentiated intelligence, and Everpure is the only scaled company positioned at the intelligence layer. The 75–85% hyperscaler margin structure isn’t a one-off deal with Meta. It’s the template for how flash infrastructure gets monetized at AI scale. The comp set should be migrating from Dell/NetApp toward the likes of ARM or Cadence , companies that monetize design IP while someone else handles the physical layer.

The rebrand to “Everpure” and the 1touch acquisition (data discovery, classification, governance , 1.5% dilutive to FY27 operating income, accretive within 24 months) are scaffolding for this shift. They’re option value on moving further up the stack from infrastructure to data management. Not the thesis today, but reinforcing it.

What the Numbers Now Mean

Going into this print, the central questions about Everpure’s future required guessing. Would the hyperscaler business carry decent margins or wreck the P&L? Would FY27 be the “investment year” that compressed profitability? Was the enterprise business genuinely accelerating or merely steady?

Those were open questions a week ago. They aren’t anymore. The hyperscaler margin structure is 75–85% , disclosed, not modeled. FY27 operating margin is ~18.4% at the midpoint , guided, not hoped for. The enterprise franchise is generating 40% RPO growth and 28% Q1 revenue growth without any hyperscaler or pricing contribution , demonstrated, not projected.

When the key assumptions move from speculation to evidence, two things happen: the range of outcomes narrows, and the time horizon you can model with confidence extends. That matters here. Before this quarter, projecting beyond FY28 required stacking assumptions on assumptions. Now, with the hyperscaler model standardized, the enterprise backlog visible, and the margin structure confirmed, a three-year view becomes reasonable , not because the future is certain, but because the architecture of the business is now legible in a way it wasn’t before.

One thing did get worse: NAND inflation is deeper than anyone anticipated going in. “More than doubled in six months” is a different animal than the 20–30% increases the market expected. That makes the near-term margin trough uglier. But here’s the paradox , the same force that pressures Q1 margins is the force that widens the structural moat for the next three years. The worse NAND gets, the more the SSD tax costs everyone who still pays it.

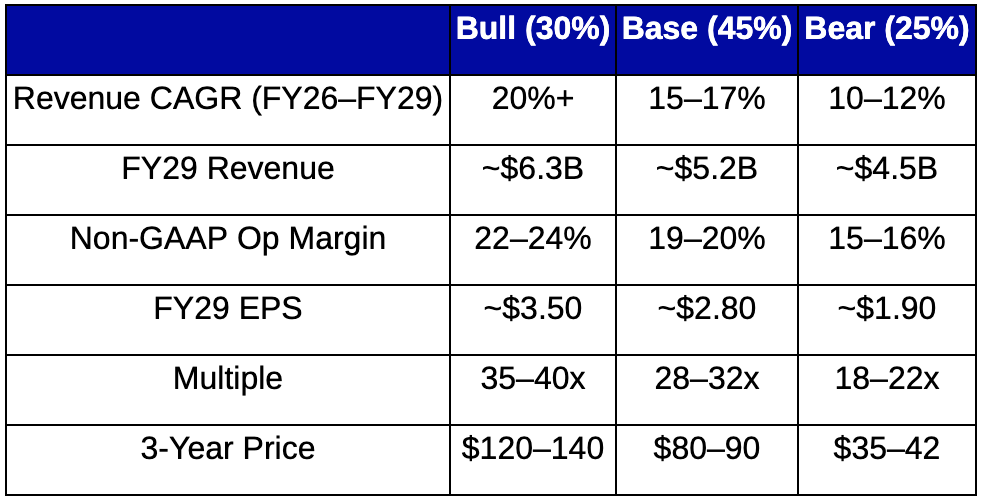

Bull requires the hyperscaler template to replicate , a second name converting, exabyte deployments scaling, and the intelligence layer becoming a larger share of revenue. The E-family accelerates HDD displacement in the enterprise. Operating leverage compounds as incremental hyperscaler dollars at 80% margins flow through at minimal opex. This is the world where the unbundling propagates and Everpure becomes the ARM of storage.

Base assumes Meta scales but remains the primary hyperscaler, enterprise grows mid-teens on franchise consolidation, and margins hold as NAND pricing normalizes. The architecture advantage is real but remains concentrated. Good business. Proves nothing new about the industry structure.

Bear is the thesis breaking on multiple fronts: hyperscaler stalls at one customer, NAND inflation persists beyond the recovery timeline destroying margins, and the enterprise franchise motion slows as macro pressures lengthen sales cycles. The multiple compresses back to hardware comps. This outcome is possible , but it now requires the evidence from this quarter to be wrong, not merely insufficient. Before the print, the bear case was “we don’t know if margins survive the hyperscaler ramp.” After the print, the bear case is “the margins they just disclosed won’t hold.” That’s a harder argument to make.

What to Track

Six items that will tell you which scenario is unfolding:

Q2 product gross margins. Above 68% confirms the pricing recovery and validates management’s timeline. Below 66% means the NAND trough is deeper than guided and the recovery extends.

Q3/Q4 hyperscaler revenue magnitude. If product revenue mix shifts imply $150M+ per quarter from hyperscalers, the ramp is real and the H2 margin snapback follows mechanically.

Second hyperscaler announcement. The single highest-impact catalyst in the model. It converts the story from “concentrated bet” to “industry standard” permanently.

RPO growth sustainability. Above 25% means the enterprise franchise motion is compounding. Below 20% raises questions about whether the contract-duration expansion was a one-quarter phenomenon.

Fusion customer count. The control plane is the moat. 600 in year one needs to become 1,500+ by FY28 to validate the fleet-management thesis.

FY28 guide (next February). If management guides to continued margin expansion, the intelligence-layer thesis is confirmed in the P&L. If margins plateau, it’s still a hardware business with good software attached.

Closing

The storage architect managing five vendors doesn’t need a faster box. He needs a control plane that makes the boxes irrelevant , one operating system, one management console, one subscription that refreshes itself. Everpure built that. Fusion is the product. Evergreen is the business model. And this quarter, for the first time, a hyperscaler paying 75–85% margins for the intelligence layer confirmed that the control plane is worth more than the commodity it manages.

My prediction, which can be proven wrong: within three years, the storage industry will have two tiers. Companies that own the intelligence layer and let customers supply the media. And bundled vendors whose margins compress as AI-scale buyers refuse the SSD tax. The unbundling Everpure demonstrated with hyperscalers will propagate into the enterprise, because the economics are too compelling to stay confined to one customer segment.

For seventy years, the storage industry optimized for a constraint that flash eliminated. Pure built for the world that was coming. Meta validated the bet. And yesterday, the margin structure confirmed what the architecture always implied: the value in storage isn’t the medium. It’s the mind.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.