GE Vernova Q1 2026: The Window and the Annuity

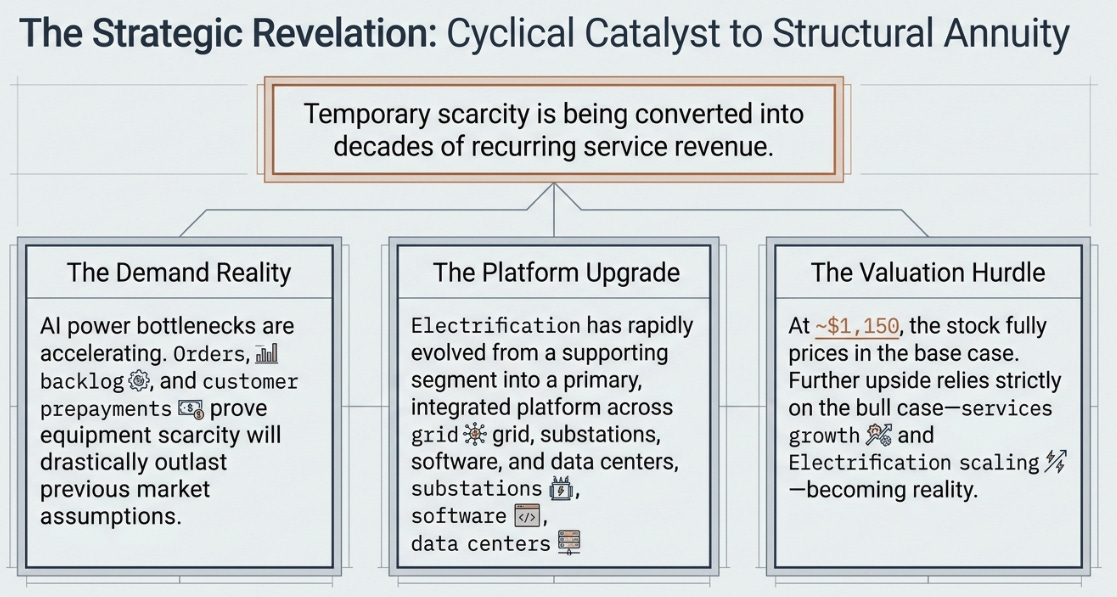

Q1 confirmed the AI power bottleneck thesis, but the bigger story is how temporary scarcity is being converted into decades of recurring service revenue.

TL;DR

GE Vernova’s Q1 showed that demand is still accelerating, not normalizing: orders, backlog, pricing, and customer prepayments all point to power equipment scarcity lasting longer than the market previously assumed.

The biggest upgrade to the thesis is Electrification: what looked like a supporting segment is increasingly becoming a platform business across grid equipment, substations, software, and data center power infrastructure.

The stock now reflects much of the base case: business quality has improved, but at around $1,150, upside depends on the bull case becoming the new base case, especially through services growth, Electrification scaling, and continued execution.

The Queue Got Longer

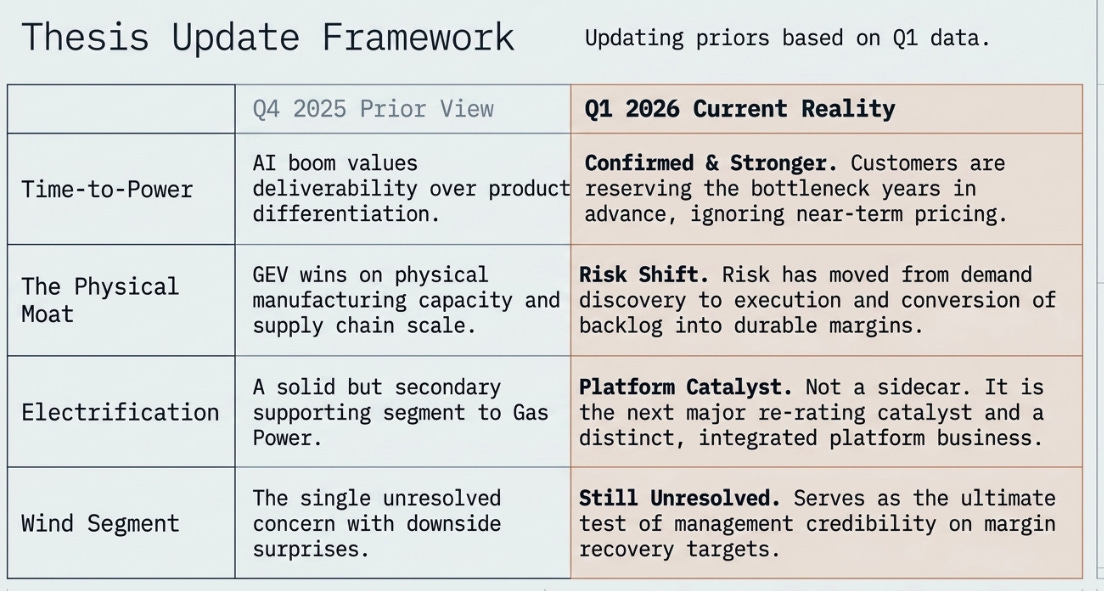

Three months ago, after GE Vernova’s fourth-quarter results, our view was simple: the AI boom runs on turbines, and GEV wins because it sells scarce capacity in a market where time-to-power matters more than price.

That was true, but incomplete.

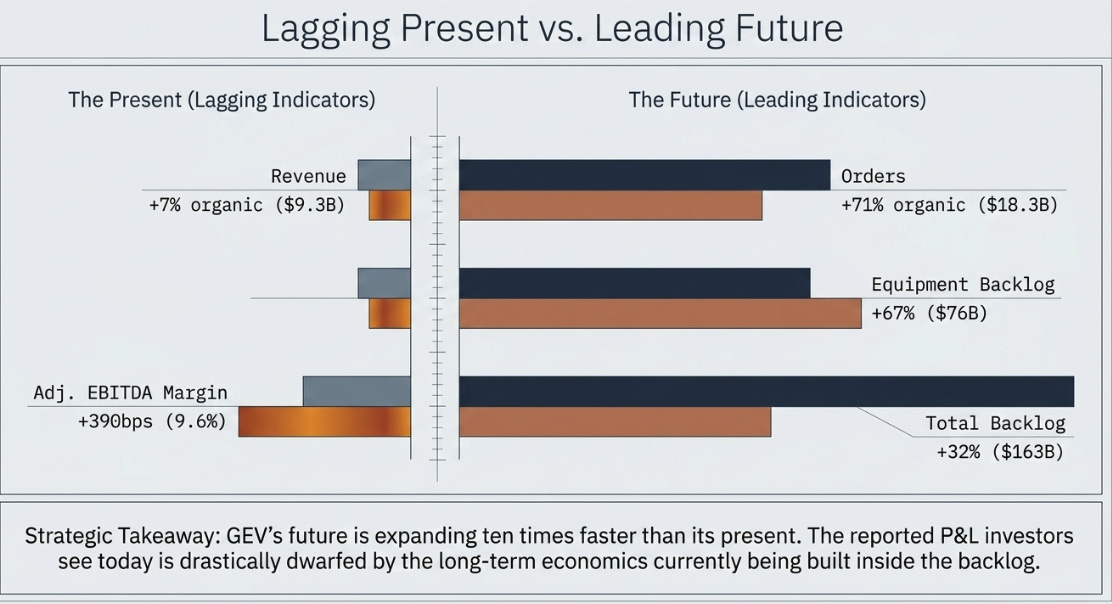

The first-quarter numbers were extraordinary. Orders of $18.3 billion, up 71% organically. Revenue of $9.3 billion, up 16%. Adjusted EBITDA of $896 million. Free cash flow of $4.8 billion, more than all of 2025. Backlog of $163 billion. Management raised guidance for revenue, EBITDA margin, and free cash flow. The stock moved from $780 to above $1,150.

But the quarter revealed something beyond a strong print. The scarcity loop we described is real and confirmed. What we underweighted is what it is producing: a permanent installed base, turbines, transformers, substations, grid systems, whose service revenue will compound for decades after the scarcity itself fades.

The loop is temporary. The assets it creates are not. That is what this piece is about.

What We Thought Then. What Changed Now.

After the fourth quarter, our view was built on four pillars. First, that AI changed the value of time-to-power, making deliverability more important than product differentiation. Second, that GEV’s advantage was its physical position: manufacturing capacity, installed base, and supply chain relationships that could not be replicated on any relevant timeline. Third, that Electrification was a solid supporting segment but secondary to the Gas Power scarcity story. Fourth, that Wind was the one unresolved concern, the segment that had surprised to the downside three times in twelve months.

After the first quarter, two of those pillars hold and two require updating.

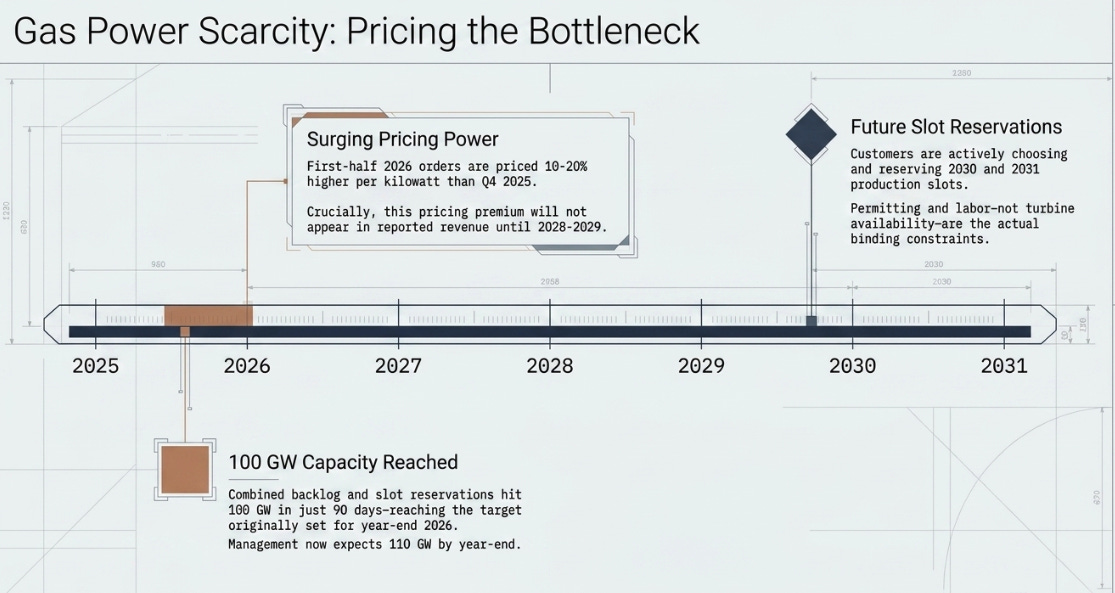

The demand and deliverability thesis is confirmed and stronger. Gas Power backlog and slot reservations grew from 83 GW to 100 GW in ninety days, hitting a target management had set for year-end 2026. Pricing on new orders is running 10-20% above Q4 2025 levels. Customers are reserving 2030 and 2031 production slots. The scarcity loop is tightening, not loosening.

But the strategic hierarchy was wrong. Electrification is not the sidecar. It may be the next re-rating catalyst. And the risk has shifted: three months ago the question was is demand real? Now the question is can GEV convert this backlog into durable margins, free cash flow, and a services annuity that outlasts the cycle?

Q1 did not eliminate risk. It changed the risk from demand discovery to execution and conversion.

Revenue Is the Present. Orders Are the Future.

The most important analytical frame for GE Vernova is not the income statement. It is the gap between what the company is booking and what it is shipping.

Orders grew 71%. Revenue grew 7%. GEV’s future is expanding ten times faster than its present, and that future is being booked at meaningfully better economics.

Gas Power tells the story most clearly. Combined backlog and slot reservation agreements reached 100 GW, with management now expecting at least 110 GW by year-end. Strazik disclosed that some customers are choosing 2030 delivery over 2029 because permitting, labor, and fuel supply, not turbine availability, are the binding constraints. Customers are reserving the one bottleneck they can reserve years in advance.

Pricing confirms the dynamic. First-half 2026 orders are expected to be priced 10-20 points higher than Q4 2025 on a dollar-per-kilowatt basis. That pricing will not appear in revenue until 2028-2029. And in April alone, GEV booked more power equipment orders in value than all of Q1.

The P&L investors can see today is a lagging indicator. The business being built inside the backlog is larger, faster-growing, and higher-margin than reported results suggest.

Electrification Is No Longer the Sidecar

This is where my view changed most.

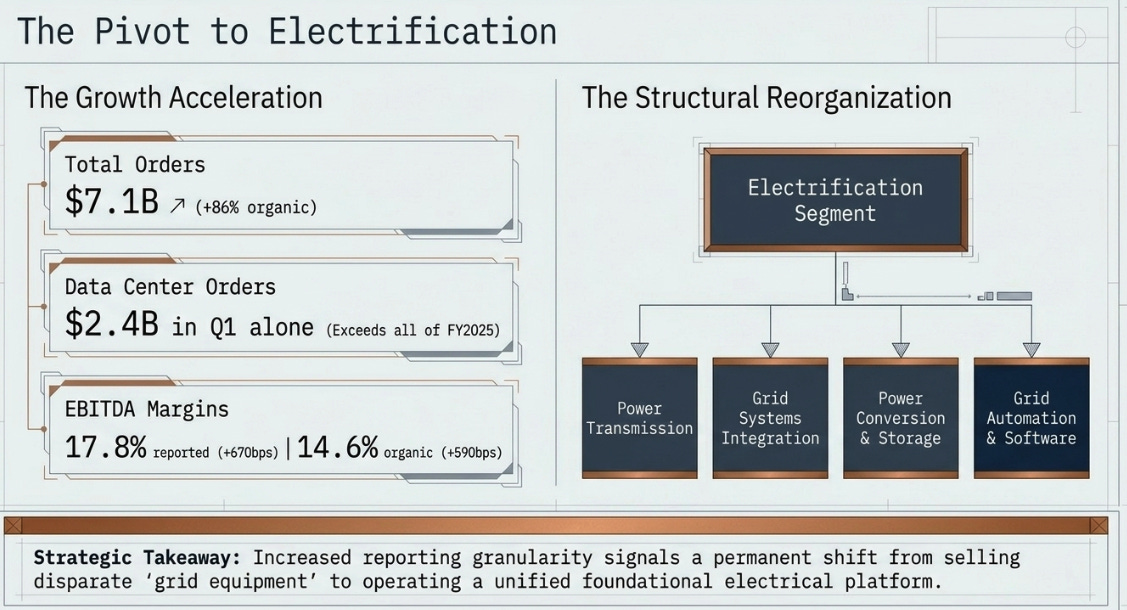

Electrification booked $2.4 billion of data center equipment orders in Q1, more than all of 2025. Strazik repeated this point in both his prepared remarks and Q&A. When a CEO repeats a data point, he is telling you the market is under-modeling something.

Management reorganized the segment into four distinct business units, Power Transmission, Grid Systems Integration, Power Conversion & Storage, and Grid Automation & Software, with separate revenue disclosure for each. Companies add reporting granularity when they want investors to see a business differently. This is management saying: Electrification is not “grid equipment.” It is a platform for the electrical system.

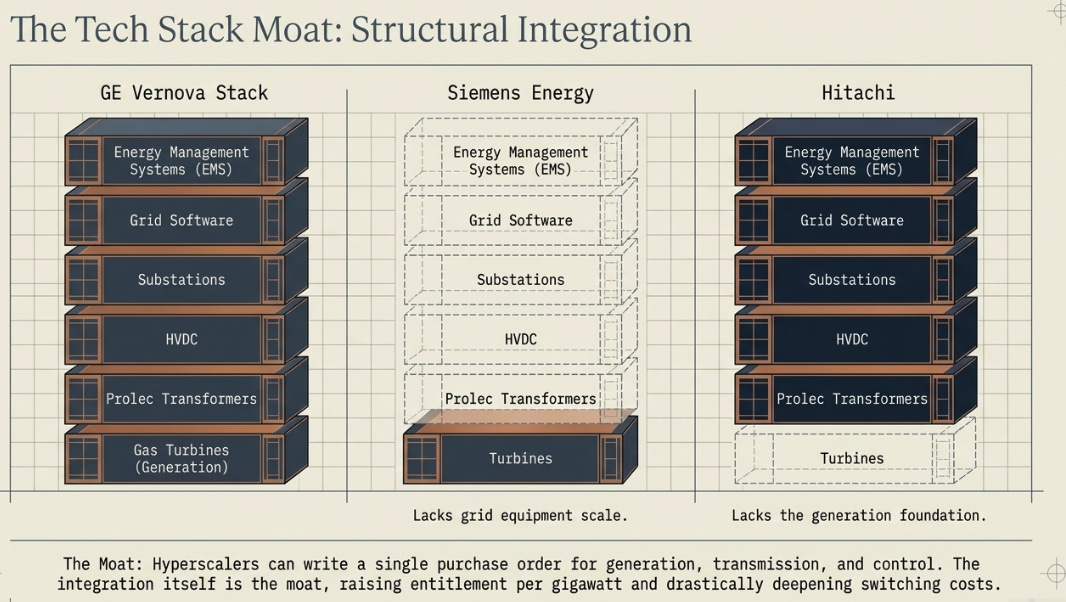

The first Energy Management System order, software integrating gas power, substation equipment, and data center load management, was small in dollars. Strazik called it “a small part of this large order.” He then spent several minutes explaining why it was strategically significant, describing a product roadmap: EMS today, stability blocks later this year, solid-state transformers in 2027. Each addition raises GEV’s entitlement per gigawatt and deepens switching costs.

This is the competitive point that matters. No Western competitor can offer an integrated stack spanning gas turbines, transformers (Prolec), HVDC, substations, grid software, and energy management. Siemens Energy has turbines but not grid equipment scale. Hitachi has grid equipment but not the generation side. When a hyperscaler can write one purchase order for generation, transmission, and control, the integration itself becomes the moat.

Gas Power explains the current narrative. Electrification determines the next valuation leg.

Customer-Funded Scarcity

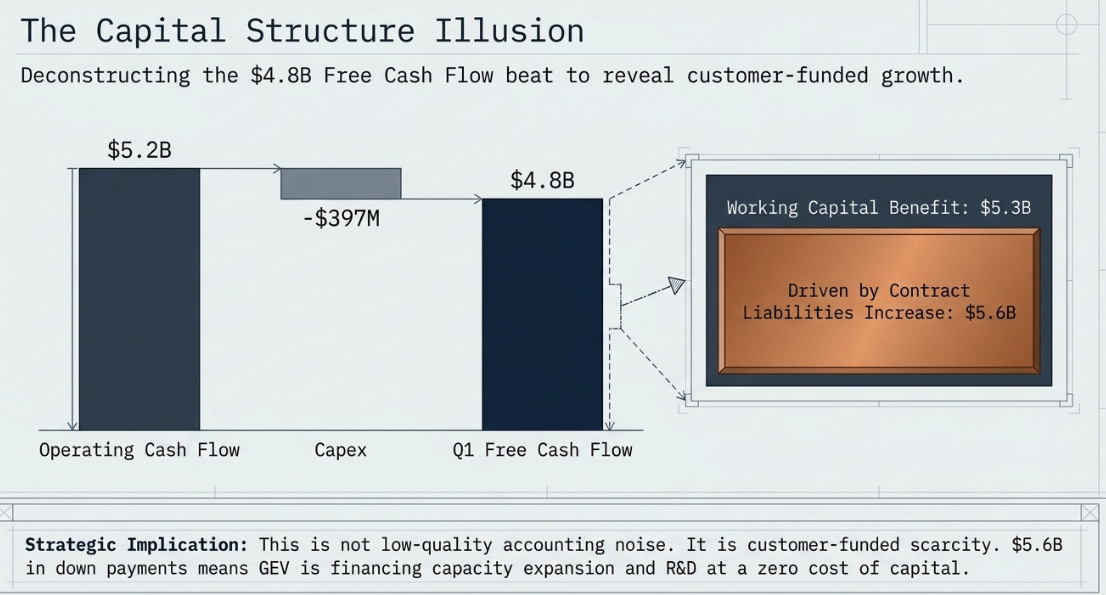

The $4.8 billion of Q1 free cash flow deserves careful interpretation. It should not be annualized. It should not be dismissed.

The $5.6 billion in contract liabilities, customer down payments on orders and slot reservations, drove the quarter. That is not low-quality accounting noise. It is commercial evidence of scarcity. Customers are financing GE Vernova because they need access to its future output.

The full-year guide tells the story. Management raised FCF guidance from $5.0-5.5 billion to $6.5-7.5 billion, a $1.5-2.0 billion raise. Revenue guidance moved only $500 million. EBITDA margin moved 100 basis points. The FCF move was the metric where management’s own model was most wrong, because they underestimated how powerfully the scarcity loop converts into cash.

The structural insight: GEV is increasingly a pre-funded business. Customer advances finance capacity expansion, R&D, and share repurchases at zero cost of capital. Growth is substantially self-financing. That is a capital structure advantage disguised as a working capital event.

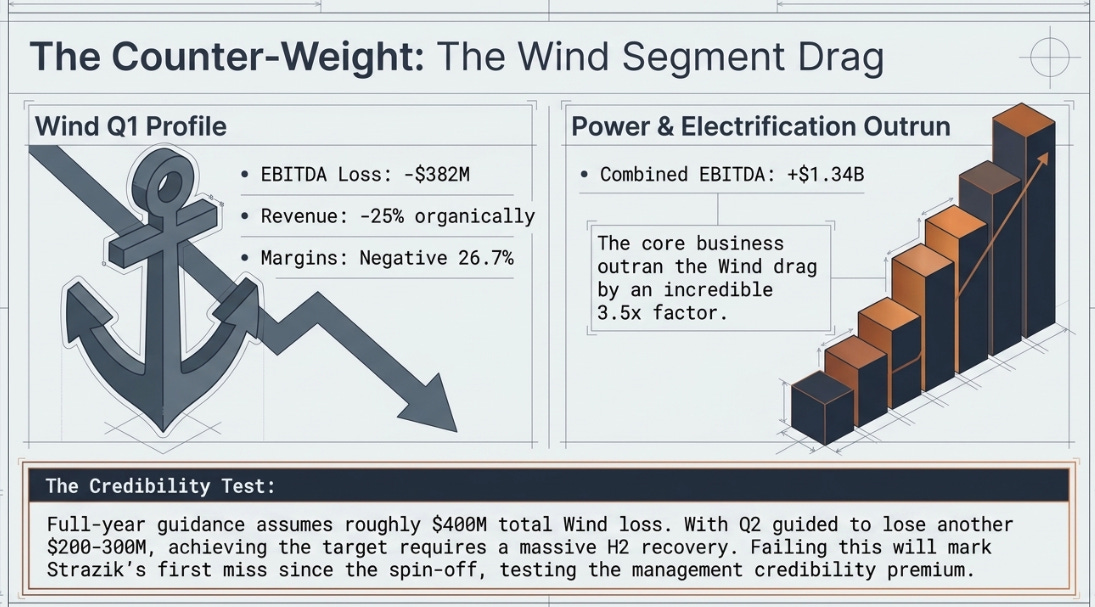

Wind Still Refuses to Disappear

Wind lost $382 million of EBITDA in Q1. Revenue fell 25% organically. Margin was negative 26.7%. Full-year guidance remains approximately $400 million of losses, which requires a meaningful H2 recovery given Q2 is guided to lose another $200-300 million.

Wind no longer defines GE Vernova, Power and Electrification generated $1.34 billion of combined EBITDA against Wind’s loss, outrunning the drag by 3.5x. But Wind still tests management credibility. If the second half does not improve as guided, it will be Strazik’s first miss since the spin-off. And credibility is what supports the guidance premium the market assigns to this management team.

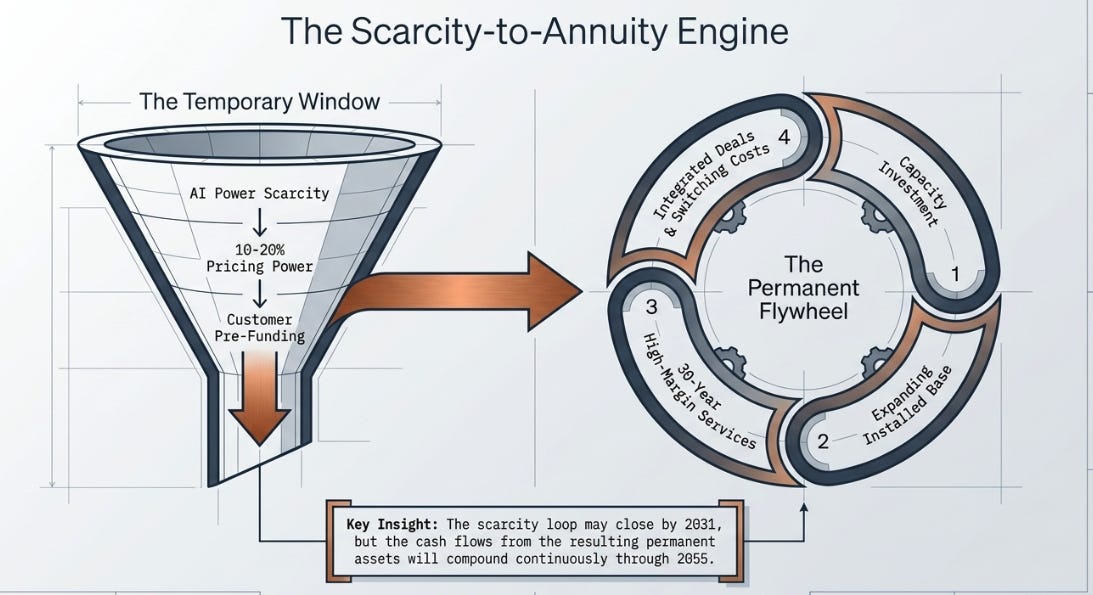

The Temporary Moat and the Permanent Asset

Here is the insight that was missing from my previous analysis.

The scarcity window is real but temporary. Siemens will eventually expand gas turbine capacity. Transformer supply will eventually loosen. Pricing power will moderate. I estimated the loop has through 2030, maybe 2031, left to run. That is probably still right.

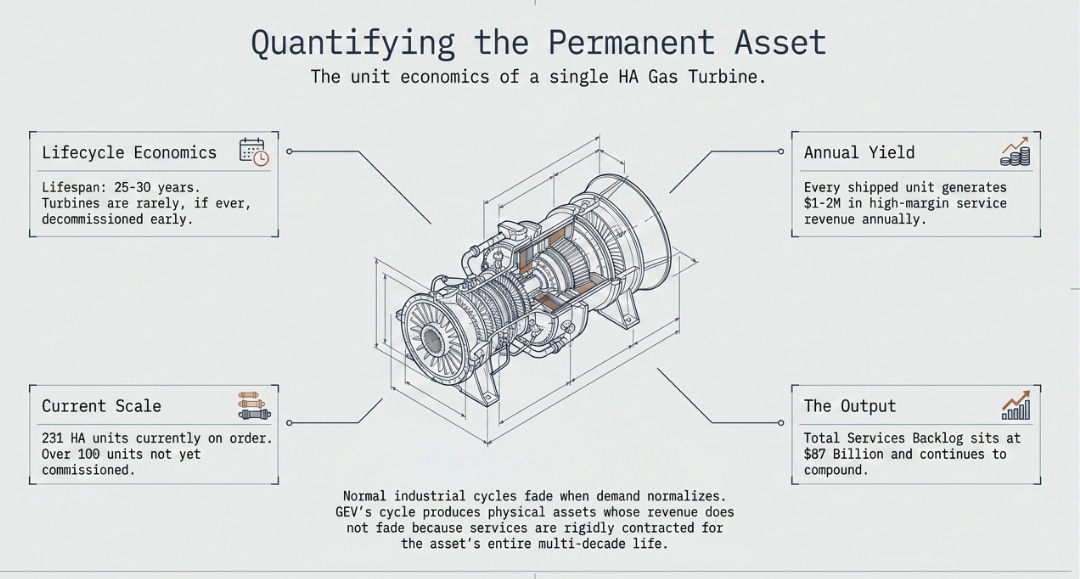

But every turbine shipped during the scarcity window creates a permanent asset. A gas turbine operates for 25-30 years. GE Vernova services it for the entire life, predictive maintenance, parts, upgrades, outage management. Each HA turbine generates roughly $1-2 million annually in high-margin service revenue. GEV has 231 HA units on order with over 100 not yet commissioned. The services backlog is $87 billion and growing.

The moat may close by 2031. The cash flows from turbines shipped while it was open will compound through 2055. The installed base never shrinks, you do not decommission a gas turbine after five years. It runs for three decades, and GEV services it the entire time.

The compounding mechanism is worth stating explicitly:

Scarcity → pricing power → customer pre-funding → capacity investment → larger installed base → recurring services → deeper customer relationships → more integrated deals → higher switching costs.

Each turn of this loop builds something permanent. That is what distinguishes it from a normal industrial cycle, where strong demand creates strong revenue that fades when demand normalizes. Here, strong demand creates an installed base whose revenue does not fade, because services are contracted for the life of the asset.

This reframes the investment question. The market treats the scarcity premium as cyclical upside: strong demand, strong pricing, eventual mean-reversion. The time asymmetry suggests something different: each year the scarcity persists, GEV is building a permanently larger recurring revenue base. The window is temporary. The annuity it produces is not.

The question is not “how long does scarcity last?” It is “how large can GEV grow its installed base before the window closes?”

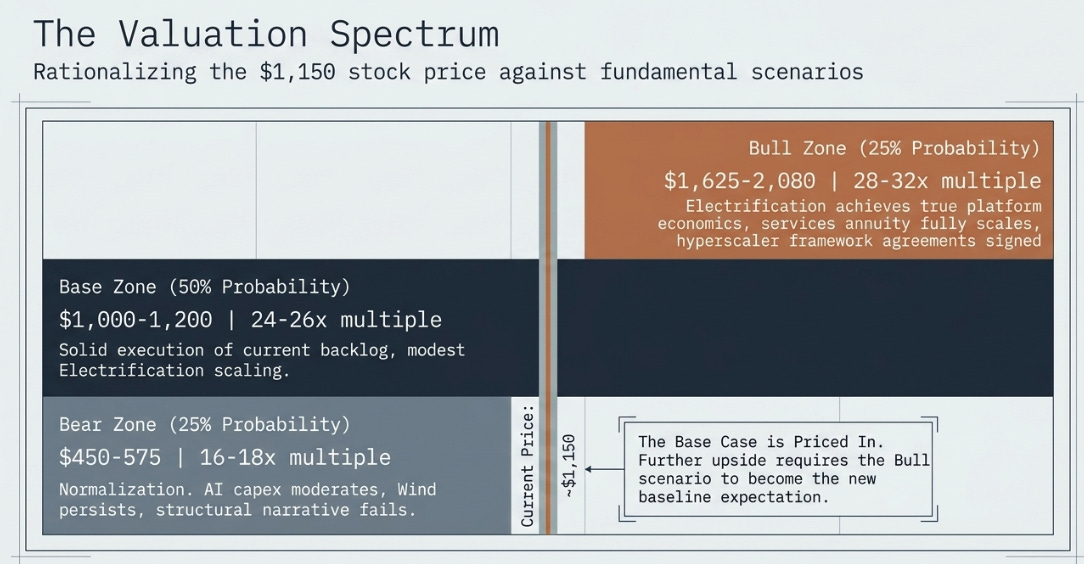

What $1,150 Requires You to Believe

The stock has moved from $780 to $1,150 in three months. The view must update accordingly.

The bear case is not a disaster. It is a normalization, AI capex moderates, pricing flattens, Wind persists, the market remembers that power equipment has historically been cyclical. The multiple compresses because the “structural” narrative loses conviction.

The base case is solid execution of the current backlog with modest Electrification scaling and the services flywheel beginning to appear in reported numbers. The stock does roughly nothing from here because the market has already priced most of this.

The bull case requires Electrification to achieve platform economics, the services annuity to become visible in analyst models, and management to exceed its own targets (which Strazik has done consistently). Framework agreements with hyperscalers would be the most obvious catalyst.

Probability-weighted, the expected value is roughly $1,100-1,250, approximately where the stock trades today. That means GEV is no longer mispriced on the base case. The upside depends on the bull case becoming the base case. Q1 moved the evidence in that direction, but the market moved the price at least as far.

At $780, the market was still arguing about whether the thesis was real. At $1,150, the market is paying for the thesis. That is a different kind of ownership.

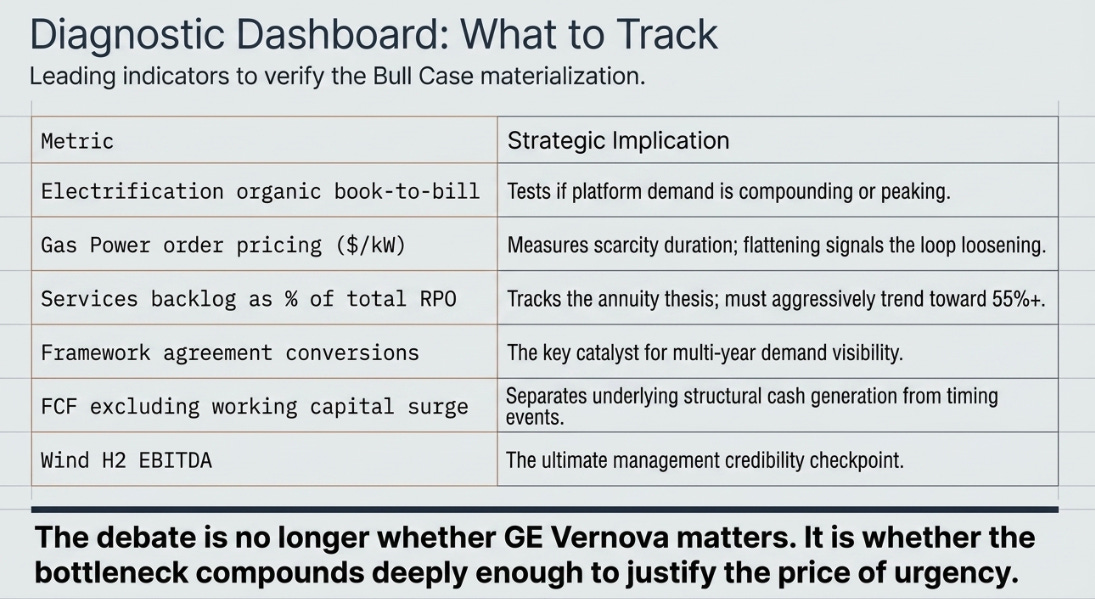

What We Will Track

The thesis strengthens if Electrification grows faster than Power while services backlog compounds. It weakens if orders stay high but margins plateau, that would signal scarcity without conversion, which is a cycle, not a franchise.

The Price of Urgency

GE Vernova’s first act as a public company was proving that the leftover from the GE breakup owned the assets the AI economy suddenly needed. The second act is harder: proving that scarcity can become a durable business model rather than a spectacular cycle.

Our view has changed, but not in the simplistic direction of “more bullish because the stock went up.” We are more convinced that GEV’s business quality is improving, through Electrification’s platform trajectory, through customer-funded capacity expansion, through the services annuity building inside the backlog. We are also more aware that the stock now prices in a large part of that improvement.

The debate is no longer whether GE Vernova matters. It is whether the bottleneck lasts long enough, and compounds deeply enough, to justify the price of urgency..

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.