Ibiden 4QFY25 Earnings: When Difficulty Starts to Pay

FY2025 earnings tested whether substrate complexity compounds into economics. The answer arrived in a profit bridge.

TL;DR

The original question was whether difficulty would become economic power or just higher capital intensity. This quarter moved the answer toward economic power: Electronics margins expanded 500bp in two years, and the FY2026 profit upgrade was driven 14:1 by ASP/product mix over volume.

Ibiden’s real asset is qualified complexity, not capacity. AI packages are getting larger, denser, more multilayered, and harder to yield. That concentrates volume at the few suppliers that can qualify each new generation, and Ibiden is beginning to get paid for it.

The thesis has advanced, but the next proof is returns. Customer advances, Ono utilization, Gama ramp, and ROIC will determine whether Ibiden becomes structural AI infrastructure or simply an important supplier doing harder work for similar economics.

In April, I wrote that the core question about Ibiden was not whether AI substrates were getting harder. They obviously were. The question was whether that difficulty would compound into Ibiden’s economics, better margins, deeper customer lock-in, a widening yield gap, or merely force the company to spend ever more capital to stay relevant.

I framed three scenarios. I identified the customer advance payment balance as the leading indicator. I said that if advances kept rising, the market had underestimated what Ibiden was becoming, and if they stalled, the old cyclical classification was right.

On May 11, Ibiden reported results that moved the answer, not definitively, but clearly enough that the burden of proof has shifted.

The 14:1 Ratio

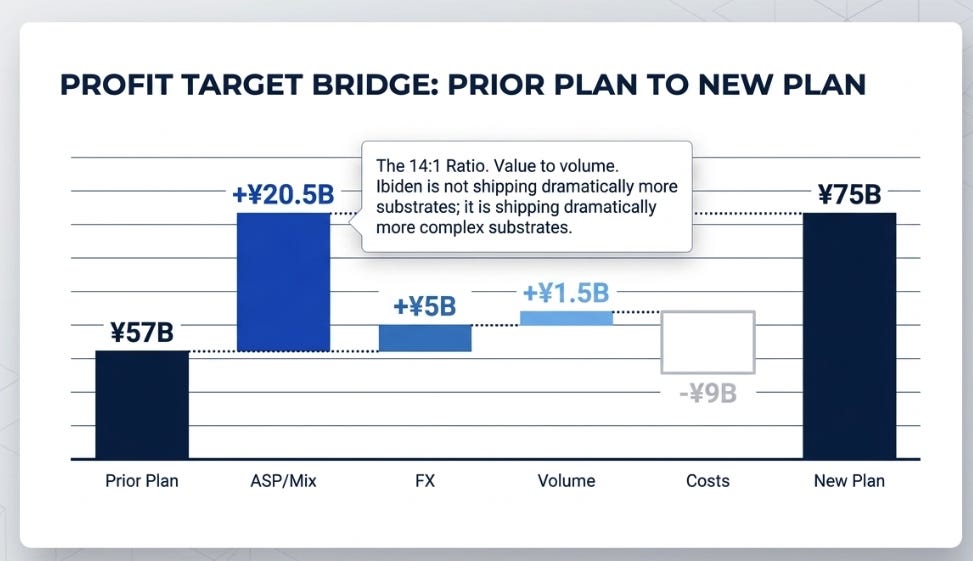

The most important data point in the earnings was not the guidance beat. It was a decomposition.

When Ibiden revised its FY2026 Electronics operating profit from the prior ¥57 billion plan to ¥75 billion, it published a bridge: ASP and product mix contributed +¥20.5 billion. Volume contributed +¥1.5 billion. FX added +¥5 billion. Costs absorbed -¥9 billion.

That 14:1 ratio, value to volume, is what “difficulty compounding into economics” looks like in the financials. Ibiden is not shipping dramatically more substrates. It is shipping dramatically more complex substrates, and the complexity commands higher prices because fewer suppliers can manufacture them at yield.

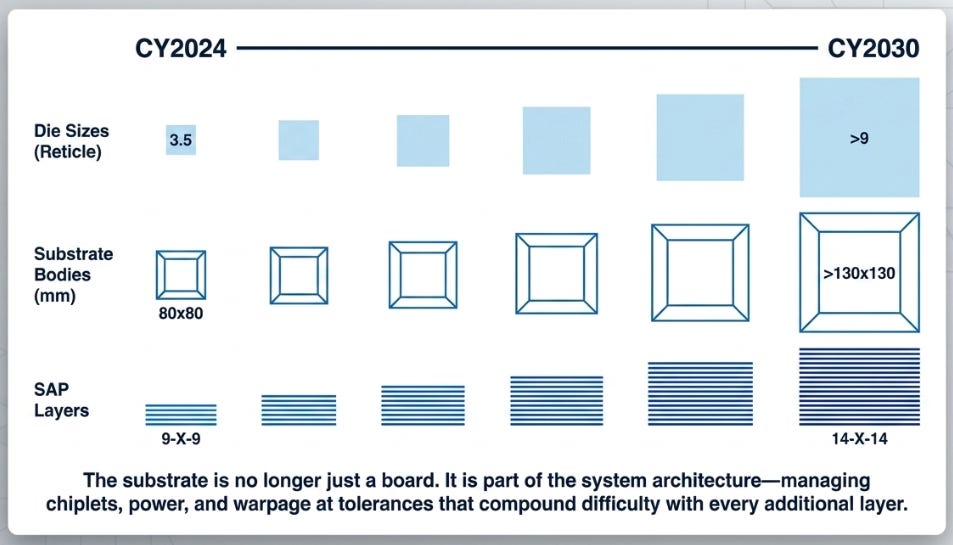

The technology roadmap quantifies why. Die sizes are headed from 3.5 reticle to above 9 by CY2030. Substrate bodies from 80×80mm to above 130×130mm. SAP layers from 9-X-9 to 14-X-14. Each step makes the manufacturing harder, pushes cumulative yields lower, and narrows the qualified supplier base. The substrate is no longer a board underneath the chip. It is part of the system architecture, connecting chiplets, routing signals, delivering power, managing warpage at tolerances that compound difficulty with every additional layer.

Electronics OPM moved from 13.6% in FY2024 to 18.6% in FY2025, guided to 22.7% in FY2026 and roughly 29% by FY2027. That is not cyclical recovery. That is value migration, and the profit bridge proves it is driven by what Ibiden ships, not how much.

The mid-term plan revision confirmed the trajectory. FY2027 operating profit was raised from ¥90 billion to ¥150 billion, a 67% increase to the anchor year. Management does not revise an anchor year by that magnitude because the cycle improved. It revises because it has concluded the structural position is more valuable than previously communicated. The long-term target: over ¥1 trillion in revenue and ¥300 billion in operating profit by FY2030, at 30% margins.

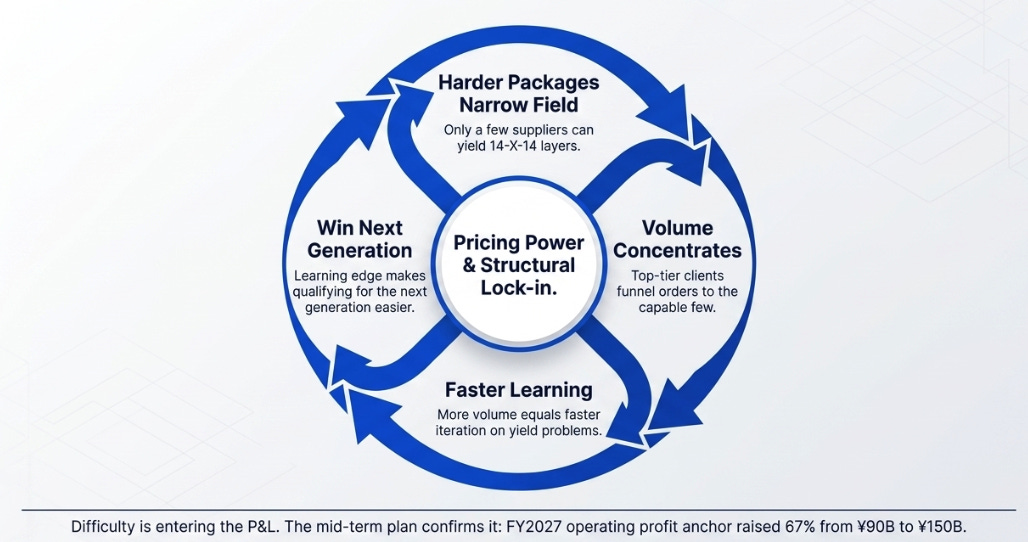

In April I wrote that the yield-learning loop, harder packages narrow the qualified field, concentrated volume accelerates learning, faster learning wins the next generation, was the mechanism to watch. This quarter, the profit bridge quantified it. Difficulty is entering the P&L.

What the Advance Payments Are Actually Saying

Which makes the one piece of contradictory evidence worth confronting honestly.

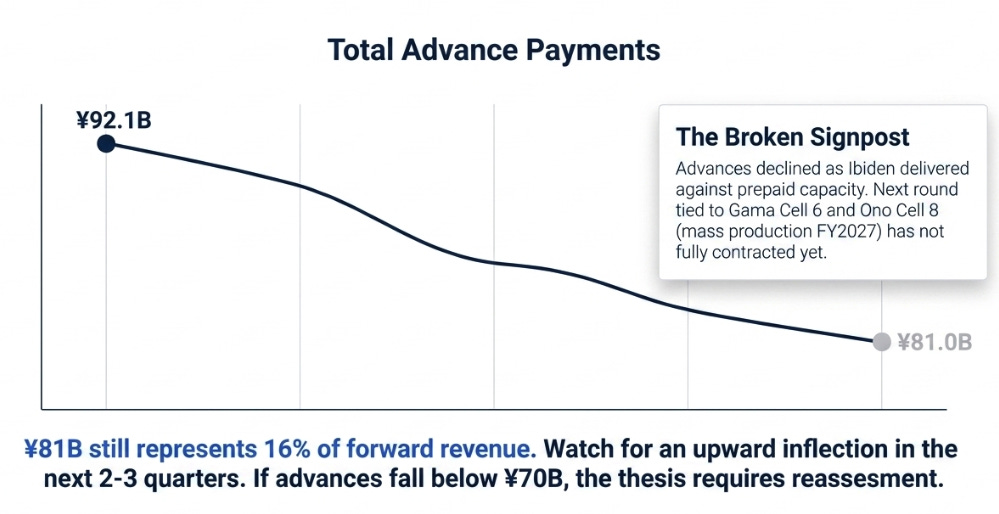

In April, I identified customer advance payments as the leading indicator. I said rising toward ¥130 billion was thesis confirmation.

They declined. From ¥92.1 billion to ¥81.0 billion.

The most likely explanation is mechanical, Ibiden delivered against previously prepaid capacity while the next round, tied to Gama Cell 6 and Ono Cell 8 mass production beginning in FY2027, has not yet been contracted in full. The ¥81 billion still represents 16% of forward revenue. Customers are simultaneously asking for capacity commitments through CY2029.

But I set the signpost. The direction was wrong. That deserves weight.

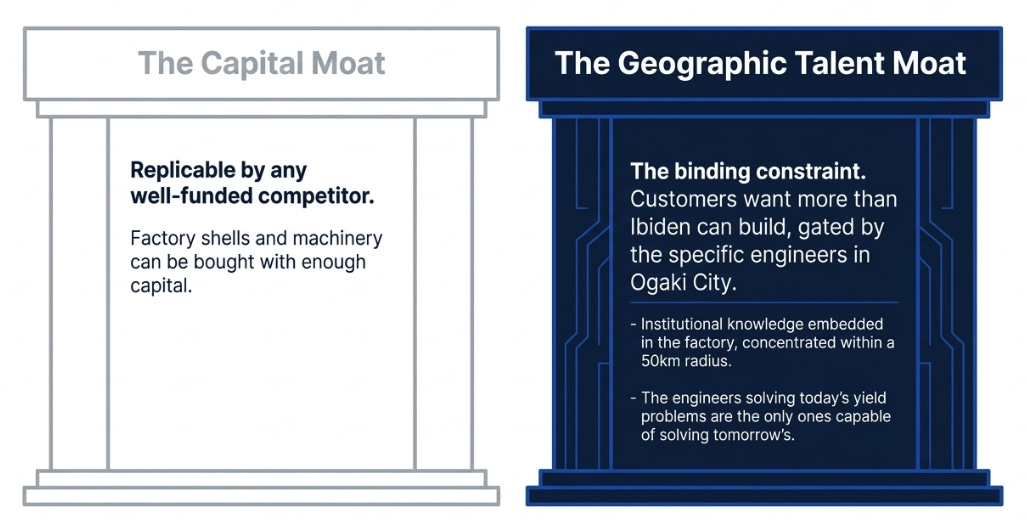

What complicates the picture is a signal I did not have in April. When Goldman asked about capacity beyond the current ¥500 billion plan, management said the binding constraint is headcount and engineering talent, not capital. Customers want more than Ibiden can build, and the bottleneck is the engineers in Ogaki City who solve next-generation yield problems, not the money to build factories.

This changes the framework in a way that is, on balance, more favorable than the advance payment decline is unfavorable. A capital constraint can be solved by any well-funded competitor. A talent constraint concentrated in a 50-kilometer radius compounds in favor of the incumbent. It is a human-capital version of the yield loop, the engineers who solved the current generation’s problems are the same ones who will solve the next generation’s, and they cannot be hired away because the institutional knowledge is embedded in the factory, not in any individual.

I expect advances to inflect upward in the next two to three quarters as Gama and Ono contracts formalize. If they fall below ¥70 billion instead, I will reassess.

The Pricing Choice

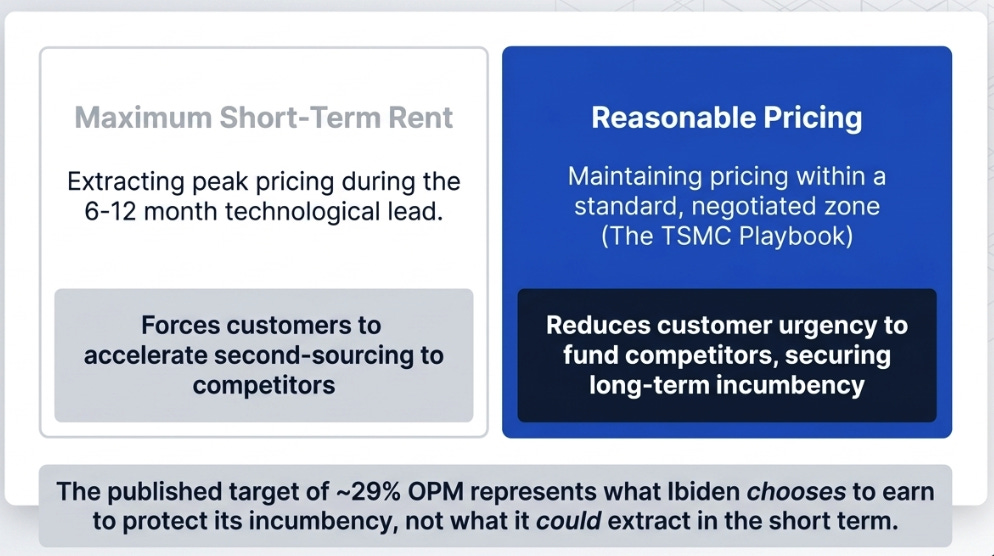

Citi’s Naito asked the natural question: with capacity tight and your position strong, why not raise prices more aggressively?

CEO Kawashima’s answer: the company does not want to increase prices “beyond the standard zone” and prefers “a reasonable price level based on the discussion with our customer.”

In April I wrote that the resolution of Ibiden’s pricing tension would come through mix rather than rate, each generation’s substrate is larger, more complex, and higher-priced, even if pricing on any given product stays disciplined. The profit bridge confirmed exactly that.

But the restraint is also strategic. Ibiden’s lead at the technology frontier lasts roughly six to twelve months before Taiwanese competitors qualify. If Ibiden extracted maximum rent during each window, customers would accelerate second-sourcing. By pricing reasonably, Ibiden reduces that urgency. This is the TSMC playbook, not the NVIDIA playbook. TSMC can price with restraint because restrained pricing keeps Intel and Samsung from investing as aggressively in catching up. Ibiden’s logic is identical: near-term margin for long-term incumbency. The published OPM targets represent what Ibiden chooses to earn, not what it could.

Three Classifications

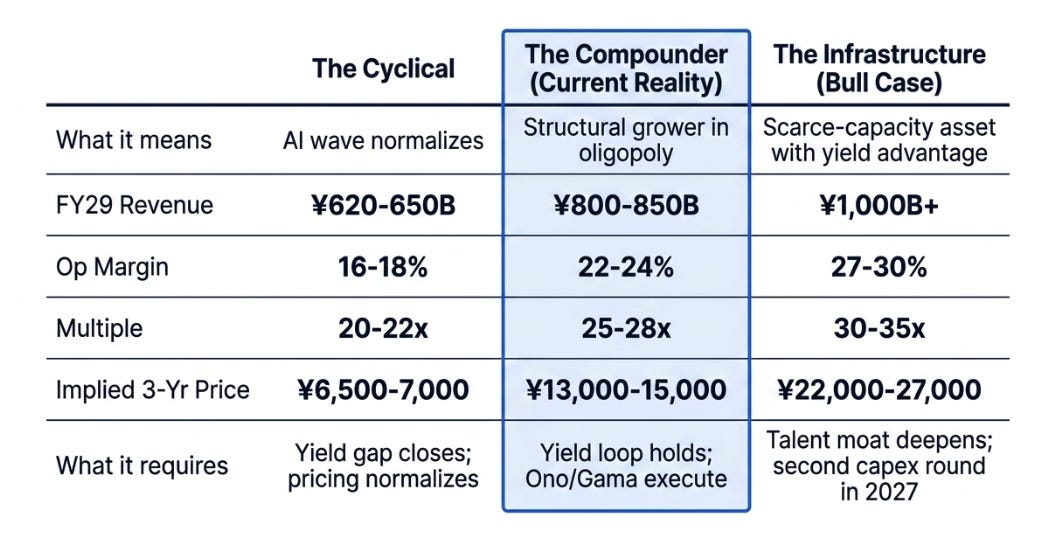

The question is not what the stock is worth under different assumptions. It is what kind of company Ibiden actually is. The classification determines the economics.

The Cyclical is Morgan Stanley’s view: Ibiden matters but the difficulty premium gets competed away. Competitors add qualified capacity, pricing normalizes, and the ¥500 billion capex absorbs the margin expansion through depreciation. The work gets harder; the returns do not scale.

The Compounder is the path Ibiden is on now. Each generation lifts mix, margins hold above 22%, ASIC diversification broadens the customer base, but competition at maturity of each generation keeps this from becoming a toll road. Difficulty pays, but doesn’t compound into monopoly economics.

The Infrastructure is the reclassification case. Complexity accelerates faster than competitors can qualify. The talent constraint deepens. A second capex decision in 2027 raises FY2030 targets. Glass core evolves as a hybrid architecture, glass beneath, ABF build-up layers on top, preserving rather than disrupting Ibiden’s process advantage. The market stops treating this as a cyclical Japanese industrial.

In April my view was Compounder with optionality toward Infrastructure. After this quarter, the evidence has shifted further, the 14:1 ratio, the mid-term plan magnitude, the talent constraint, but the stock has moved past my prior bull case, which complicates the entry even as it confirms the thesis.

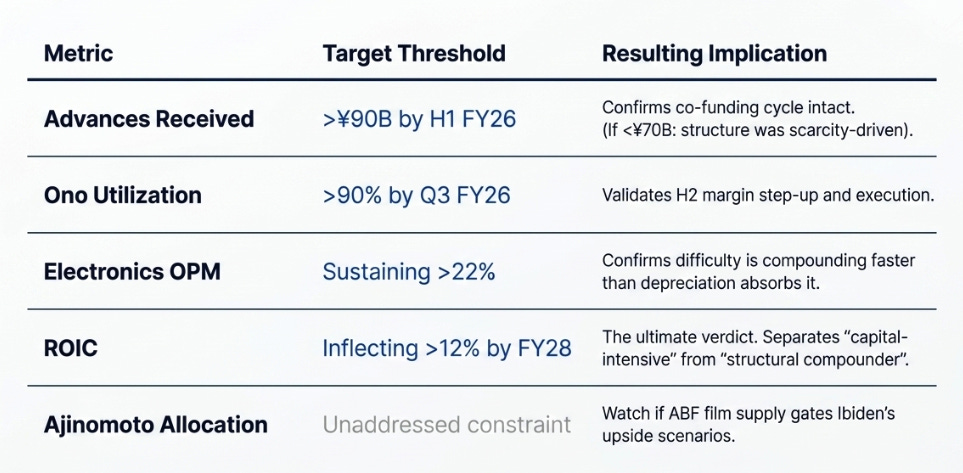

What Resolves It

Advances received. Above ¥90B by H1 FY2026 confirms the co-funding cycle is intact. Below ¥70B means the structure was scarcity-driven, not relationship-driven. Still the single most important metric.

Ono utilization. Above 90% by Q3 FY2026 confirms execution and validates the H2 margin step-up. Below 85% reopens the execution question.

Electronics OPM. Sustaining above 22% confirms difficulty is compounding faster than depreciation absorbs it. Below 18% favors the Cyclical classification.

ROIC. Inflecting above 12% by FY2028 is the ultimate verdict, it separates “strategically important but capital-intensive” from “structural compounder.” Everything else is a leading indicator.

Ajinomoto allocation. Whether ABF film supply gates Ibiden’s upside scenarios remains unaddressed. If it surfaces as a binding constraint, the market will not have priced it.

In April I asked whether difficulty compounds faster than capital consumes it. The profit bridge says yes. The margin trajectory says yes. The talent constraint says the loop may be stronger than I initially framed.

The advance payments say: not yet confirmed, check back in two quarters.

The constraint beneath AI has entered the P&L. Now it must enter returns.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.