Ibiden: The Hidden Bottleneck Beneath AI

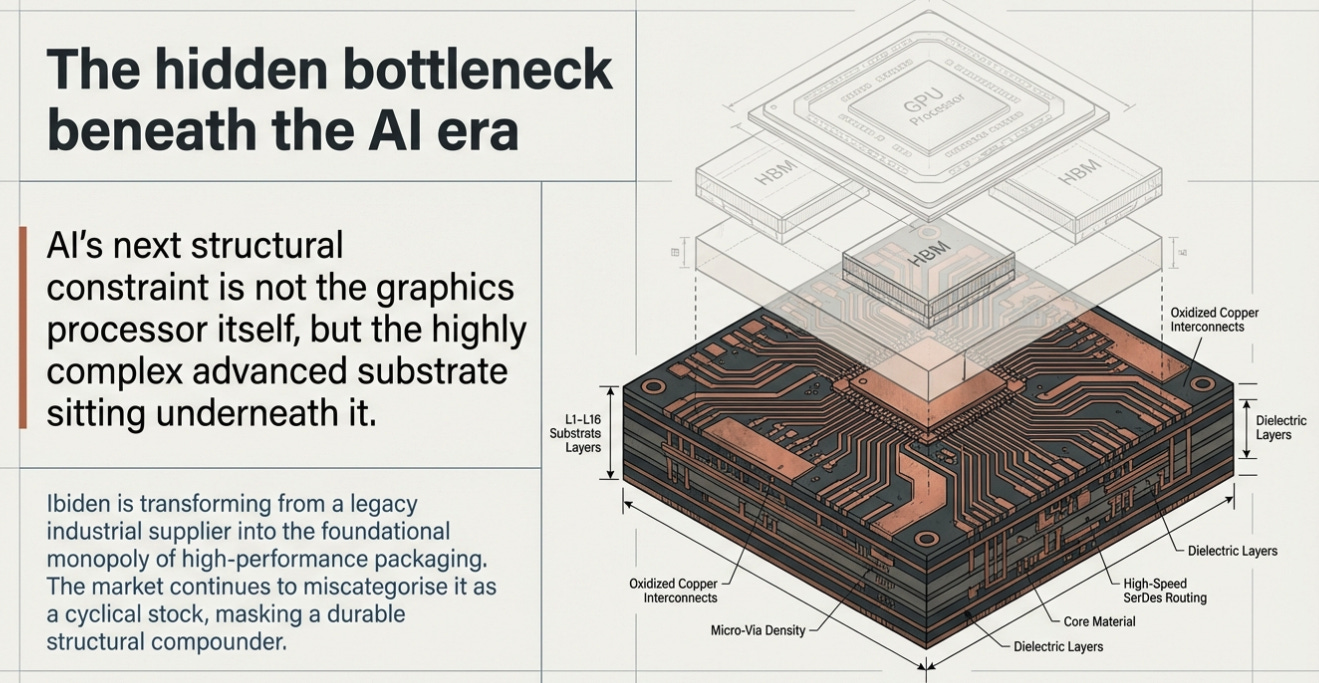

AI’s next constraint is not the GPU itself, but the advanced substrate underneath it, and Ibiden may be one of the few companies positioned to turn that manufacturing difficulty into durable economic

TL;DR

AI has shifted the bottleneck from chip design to packaging. As GPUs get larger, hotter, and more complex, the substrate underneath them has become one of the hardest and most valuable parts of the stack.

Ibiden’s edge is yield, not glamour. Its accumulated manufacturing know-how, customer prepayments, and position in the highest-complexity substrate segment suggest it may be more than just another cyclical semiconductor supplier.

The core investment question is who captures the economics. Ibiden is clearly strategically important, but the stock will depend on whether rising complexity translates into lasting returns rather than just higher capital intensity.

In 1912, a company was founded on the banks of the Ibi River in Gifu Prefecture, Japan, to do something that sounds unremarkable until you think about it for a moment: turn moving water into electricity. The river ran fast, Japan needed power, and Ibiden was the kind of enterprise that exists because a natural force needs to be converted into something usable. For the next eighty years, the company stayed close to that logic. It generated electricity. It made ceramics. It built housing materials. Always the same pattern: take something difficult and make it work for someone else.

In the 1990s, Intel needed a supplier for the small circuit boards underneath its processors. Ibiden took the contract. For twenty-five years, it made substrates for Intel, and Intel accounted for 70–80% of Ibiden’s substrate revenue. It was a comfortable arrangement. Intel set the specifications. Ibiden built to them. The substrate, the multilayered organic board that connects a chip to the outside world, was necessary but unglamorous. Nobody thought much about it, because the chip above it was where the value sat.

Then, within the span of about eighteen months, two things happened. Intel stumbled. And AI made the substrate the hardest part of the chip to build.

The World Where Substrates Did Not Matter

To understand why the situation changed, you first must understand why it stayed the same for so long.

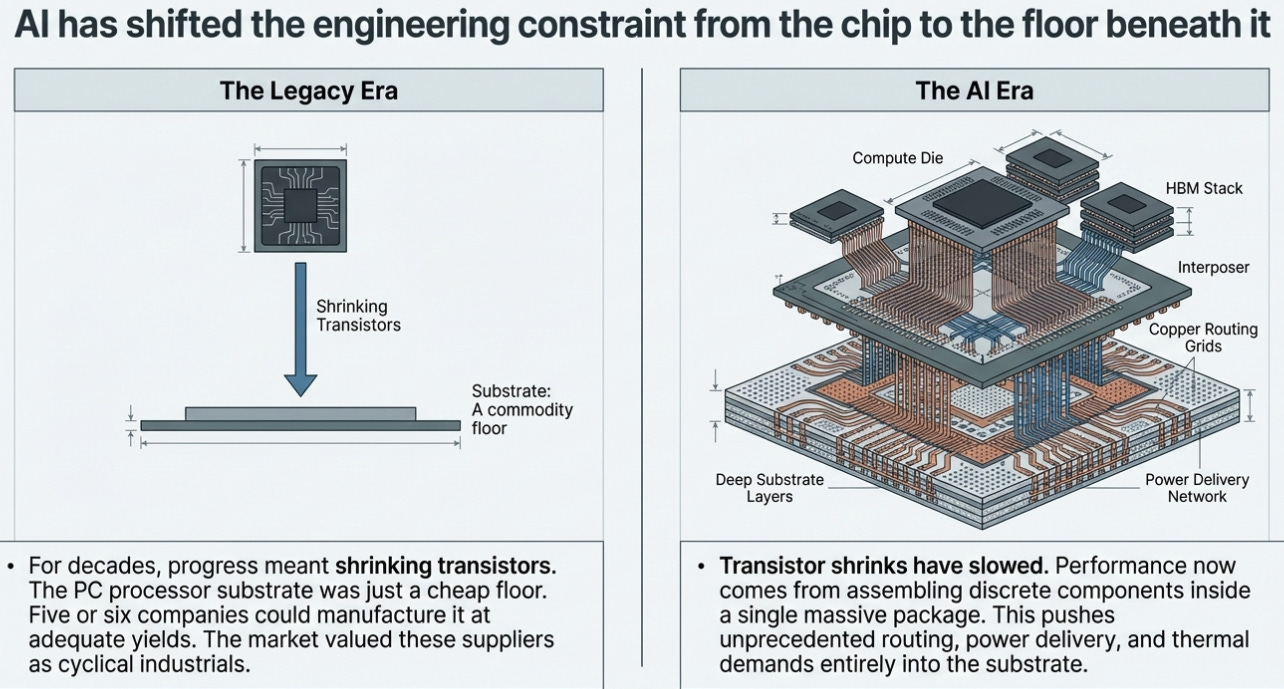

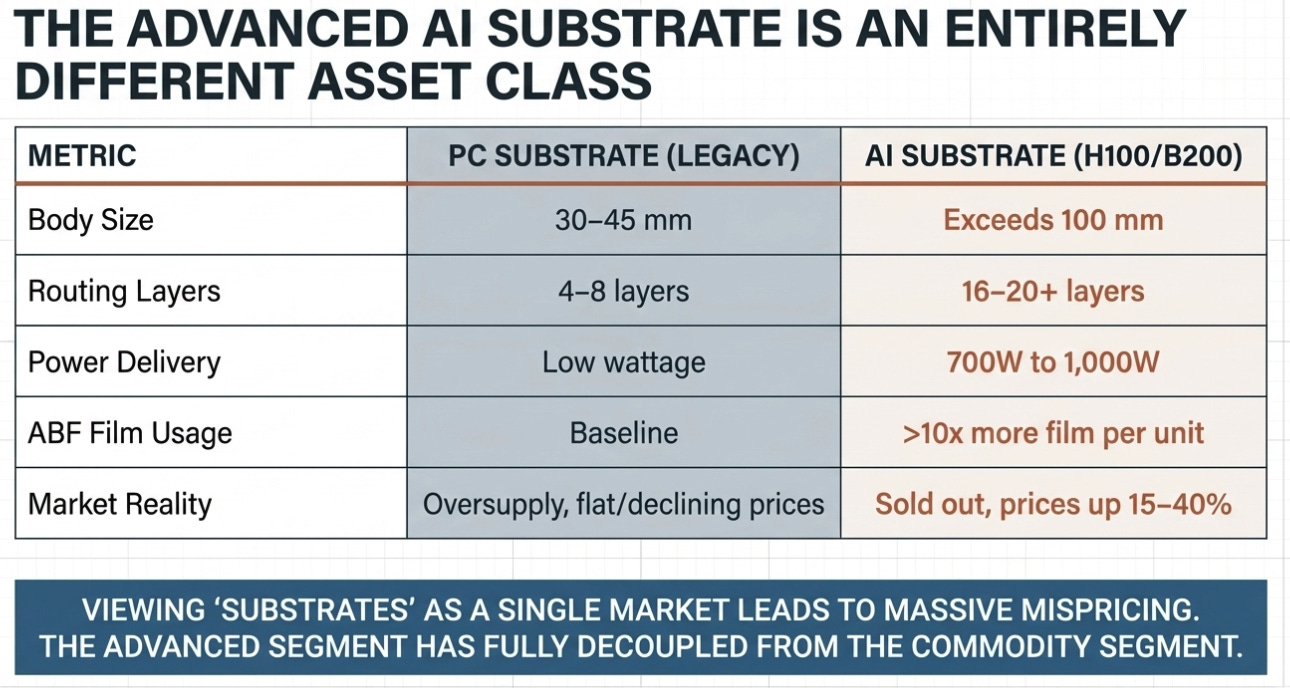

For most of the history of modern computing, progress meant shrinking transistors. Smaller transistors meant faster chips. Faster chips meant better computers. The package underneath, the substrate, was just the floor. A PC processor substrate had four to eight layers of electrical routing, measured 30–45 millimeters across, and cost under a dollar. Making one was not trivial, but it was not the constraint on anything. Five or six companies could do it at adequate yields.

Ibiden built a solid business in this world. The moat was not glamorous, it was a yield-learning curve. Ibiden did not have a patent wall or a proprietary standard. What it had was thirty years of accumulated knowledge about how to manufacture multilayer organic substrates at high yield. That knowledge translated into lower cost per good unit, which translated into Intel coming back every generation. Other companies could make substrates. They could not learn as fast at the same scale.

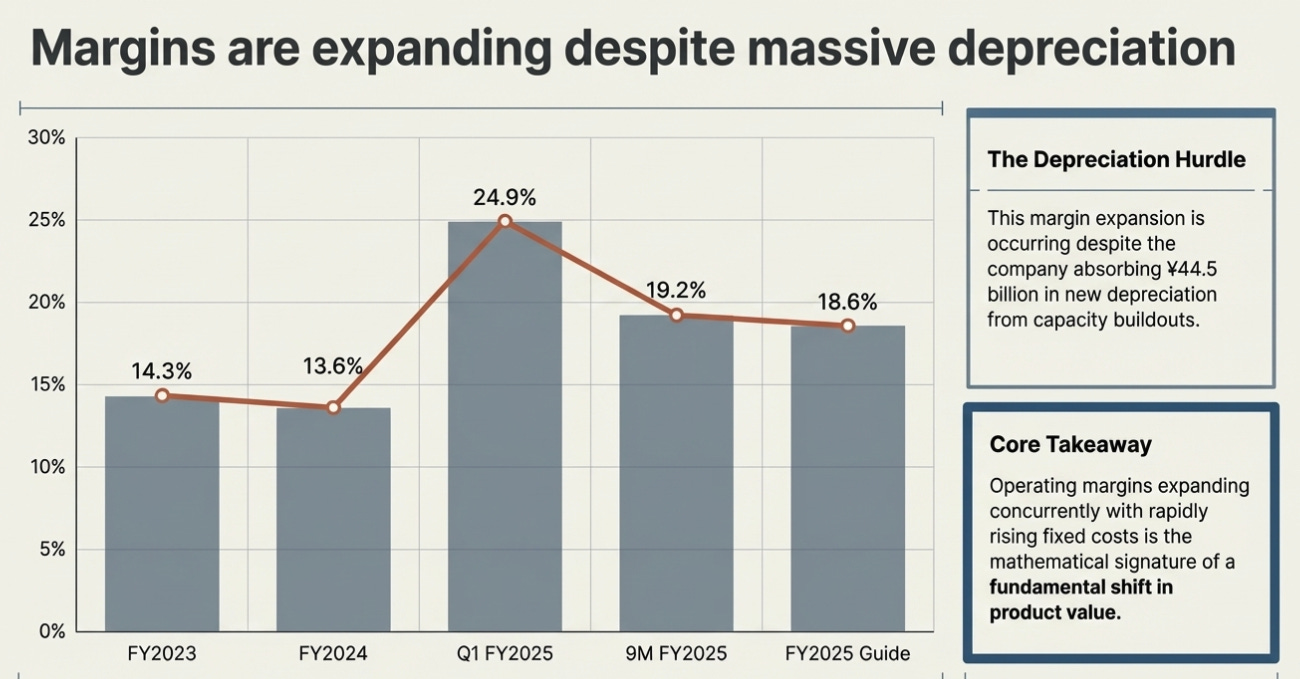

The market understood this and valued Ibiden accordingly. Cyclical Japanese industrial. Goes up when the PC cycle is strong, goes down when it weakens. When Intel lost share to AMD and struggled with its foundry strategy through 2023 and 2024, Ibiden’s numbers deteriorated. Revenue was flat at ¥369 billion in FY2024. Operating margins: 12.9%. The sell-side consensus: wait for the server cycle to recover, check back later.

That assessment was not irrational. It was also about to become obsolete.

When the Floor Became the Constraint

What changed was not that AI created more demand for chips. What changed was where the engineering difficulty went.

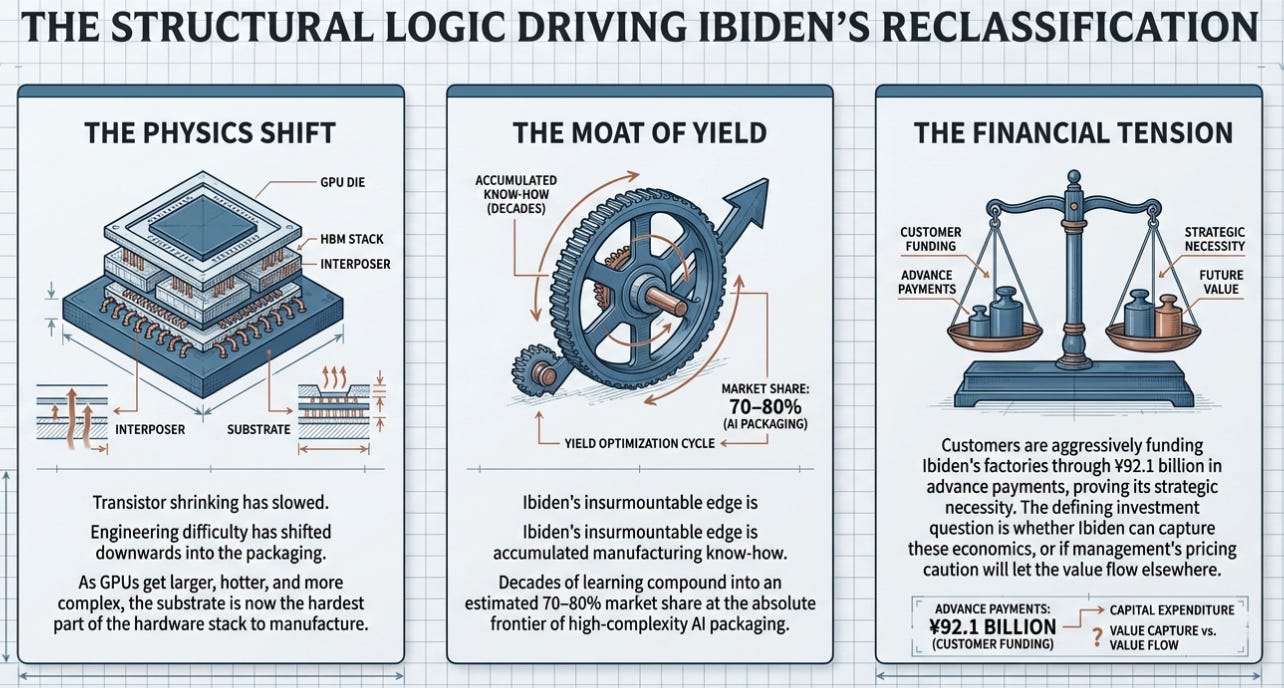

Transistor shrinks started slowing down. The industry’s response was not to give up on performance; it was to find a different way to get it. Instead of making one chip smaller, engineers started connecting multiple chips together inside a single package: compute chiplets, memory stacks, interposer layers, power delivery networks. The performance that used to come from transistor scaling now comes from how those pieces are assembled. And all of them sit on the substrate.

An Nvidia H100 GPU substrate has sixteen to twenty routing layers, exceeds 100 millimeters in body size, and must deliver 700 watts of power through dedicated planes while routing thousands of high-speed signals. The next generation, the B200, pushes to 1,000 watts, eight stacks of high-bandwidth memory, and a dual-die design that was physically impossible on the previous packaging architecture. Each generation demands a larger, more complex, more difficult substrate.

Ajinomoto, the Japanese food company whose subsidiary produces the dielectric insulating film used in virtually all high-performance substrates, has published the math: a high-performance computing substrate uses over ten times more ABF film than a PC substrate. Not ten percent more. Ten times. Both the body size and the layer count rise together, and the manufacturing difficulty compounds with each additional layer.

This is the first thing the market can get wrong about Ibiden. If you think “substrates” is one market, the company looks cyclical, dependent on total chip volumes, subject to the usual semiconductor swings. If you recognize that the advanced segment has separated from the commodity segment, AI substrates sold out with prices up 15–40%, PC substrates in oversupply with flat or declining prices, the business starts to look like something else.

The proof is in the segment data. Ibiden’s electronics operating margin expanded from 13.6% in FY2024 to 19.2% through the first nine months of FY2025, despite absorbing ¥44.5 billion in new depreciation from capacity buildouts. Margins rising while fixed costs rise. That only happens when the product mix is shifting toward something substantially more valuable.

Manufacturing Difficulty as a Compounding Advantage

This is where the strategic logic gets interesting, and where I think most analysis of Ibiden stops too early.

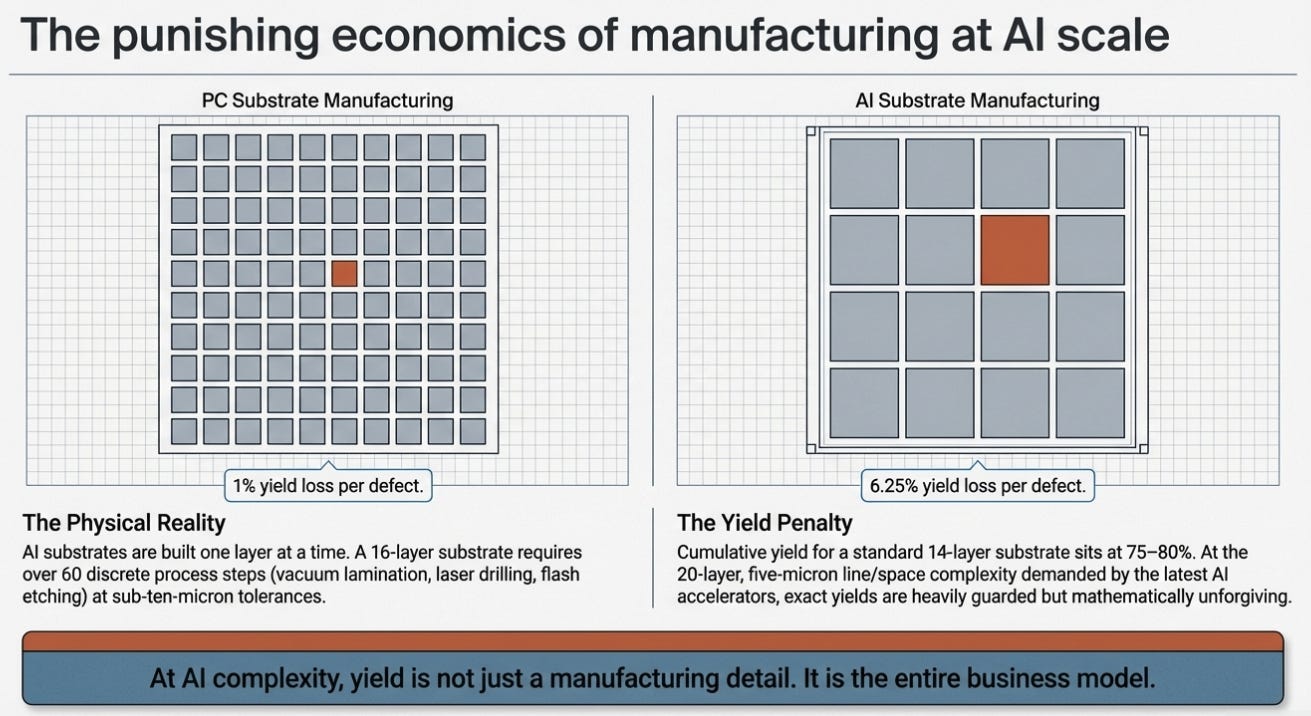

An ABF substrate is built one layer at a time. Each layer requires vacuum lamination of the insulating film, thermal curing, laser drilling of microvias, chemical cleaning, electroless copper seeding, photoresist patterning, electrolytic plating, resist stripping, and flash etching, all at sub-ten-micron tolerances. A sixteen-layer substrate requires this sequence six to eight times per side. Over sixty discrete process steps. Cumulative yield for a fourteen-layer substrate is estimated at 75–80%. For a twenty-layer substrate at five-micron line and space, what the latest AI accelerators require, yields are substantially lower, and the exact numbers are closely guarded.

The economics of yield at AI scale are punishing. A modern manufacturing panel holds only about sixteen AI-grade packages at 120-millimeter body size. One defective package causes a 6.25% yield loss. Compare that to a PC substrate panel, which holds roughly one hundred packages, where one defect costs about 1%. At AI complexity, yield is not a manufacturing detail. It is the entire business.

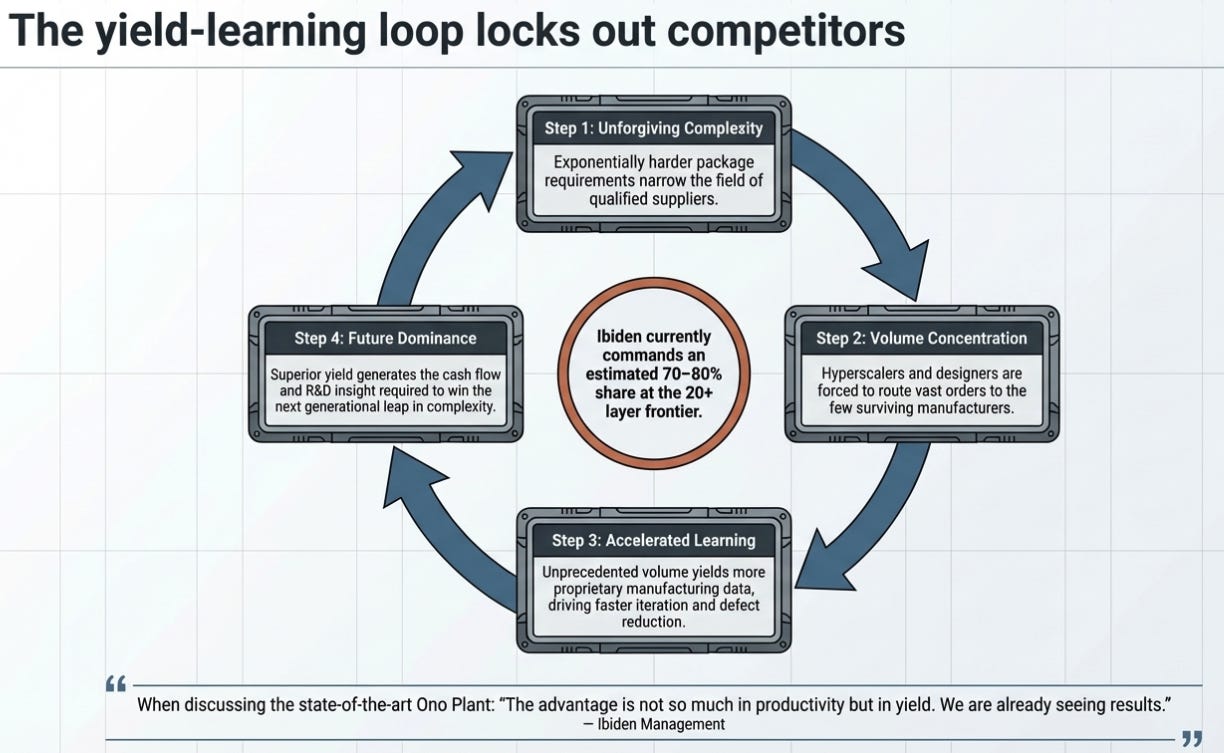

Now consider what happens over time. Each generation of AI chip demands a more complex substrate. More layers. Larger body. Finer features. Embedded components for power delivery. The number of suppliers that can manufacture these substrates at commercially viable yields shrinks with each step up in difficulty. Customers concentrate orders at the survivors. The survivors accumulate more yield-learning data from higher volumes. Their yields improve. They become better positioned to win the next generation.

This is the loop: harder packages narrow the qualified field. A narrower field concentrates volume. Concentrated volume accelerates learning. Faster learning makes the leader better equipped for the next leap in difficulty.

Ibiden’s management confirmed the mechanism in the most direct way possible. When asked about the Ono Plant, the company’s newest and most advanced facility, management said the advantage was “not so much in productivity but in yield. We are already seeing results.”

The parallel to TSMC’s position in leading-edge logic fabrication is obvious, and it clarifies the limits of the comparison. TSMC has no credible competitor at the most advanced node. Ibiden has four or five credible competitors, Unimicron, AT&S, Shinko Electric, Samsung Electro-Mechanics, Kinsus, at one generation behind. They can make substrates. Some of them are very good. But at the highest complexity, twenty-plus layers, embedded components, body sizes exceeding 100 millimeters, the field narrows sharply, and Ibiden claims 70–80% share. That is not a monopoly. But it is a frontier position in a concentrated manufacturing layer, and it appears to strengthen rather than weaken as complexity increases.

The Food Company That Controls the Supply Chain

If you want to understand why the advanced substrate market is as concentrated as it is, you must look one level up, to the most unlikely bottleneck in the entire AI hardware ecosystem.

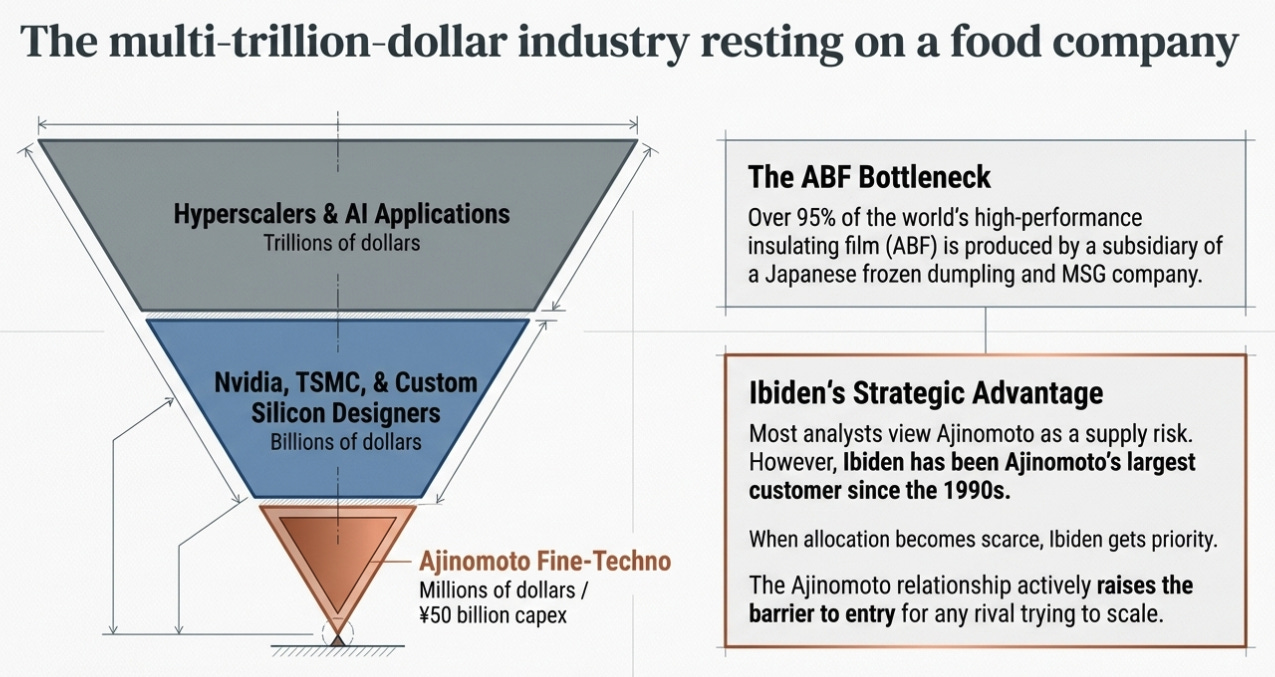

Every high-performance substrate in the world, every one made by Ibiden, Unimicron, AT&S, Shinko, Samsung Electro-Mechanics, or anyone else, requires an insulating dielectric film called ABF, Ajinomoto Build-up Film. It is produced almost exclusively by Ajinomoto Fine-Techno, a subsidiary of the Japanese company best known for MSG seasoning and frozen dumplings. Ajinomoto holds over 95% of the global market for this material. It operates two manufacturing plants, both in Japan.

The capital asymmetry between Ajinomoto and its downstream customers is one of the most striking features of the entire semiconductor supply chain. Ajinomoto’s planned capacity expansion, roughly ¥50 billion through 2030, will increase output by about 50%. That investment is less than what Ibiden will spend on a single new substrate fab. The cheapest monopoly in the chain gates the most capital-intensive oligopoly beneath it.

Most analysts’ frame Ajinomoto’s dominance as a supply risk for substrate makers. I think this framing is backwards, at least for the incumbents.

Every substrate maker depends on the same material. But Ibiden has been Ajinomoto’s largest customer since the late 1990s. When Ajinomoto allocates scarce film during shortages, which it did during the 2020–2022 crisis, when lead times stretched to five months and prices rose 30–50%, Ibiden gets priority. A company trying to enter the advanced substrate market does not just need to build a billion-dollar fab and survive thirty-six months of customer qualification. It also needs to secure ABF film allocation from a monopolist that prioritizes its existing high-volume customers.

The Ajinomoto relationship does not just protect Ibiden from competition. It actively raises the barrier to entry for everyone else.

The genuine constraint is different, and management has been direct about it. Ibiden has secured enough ABF film for current guidance, but “not yet secured materials to accommodate potential upside.” Even if customer demand and factory capacity are available, film supply may cap how fast the company can grow. That is a real limitation. But it constrains every competitor equally, and Ibiden is best positioned within it.

If I were looking for a single leading indicator that almost nobody tracks, it would be Ajinomoto’s capacity expansion decisions and allocation priorities. Not Nvidia’s quarterly shipments. Not hyperscaler capex guidance. The food company’s factory plans.

Who Gets Paid for This?

Here is where the story becomes an investment question, and where I think the tension is genuinely unresolved.

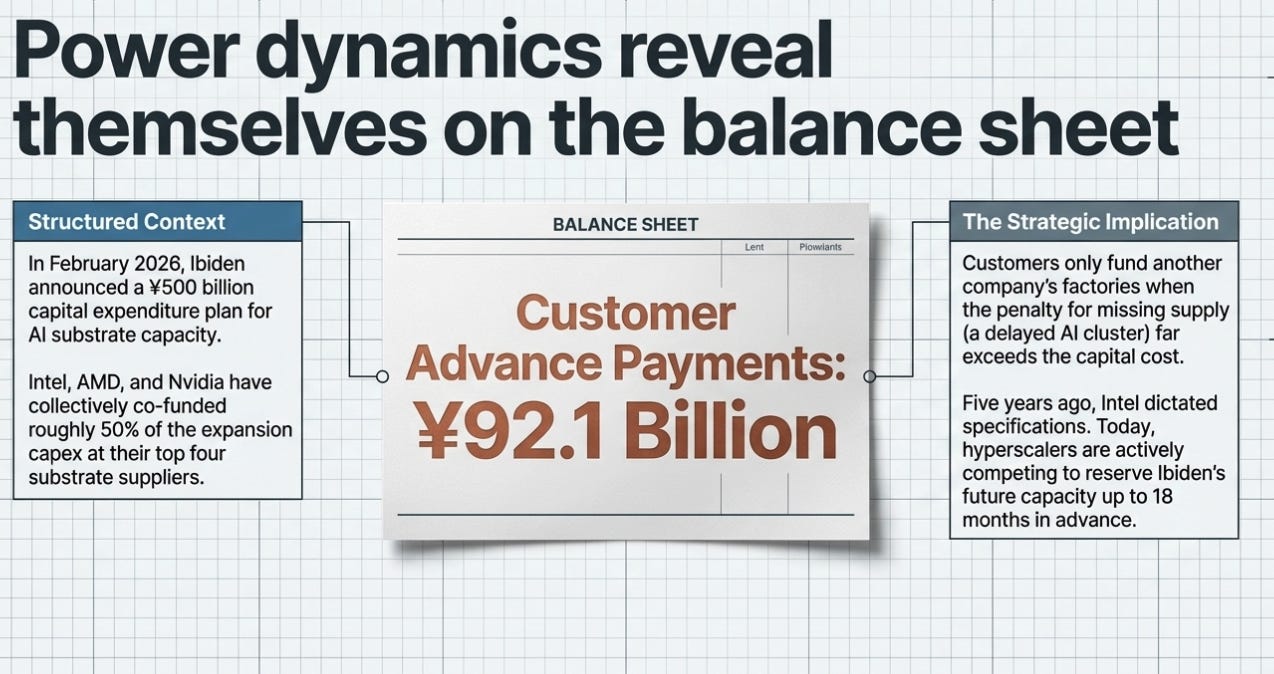

In February 2026, Ibiden announced a ¥500 billion capital expenditure plan for AI substrate capacity. The critical detail came in the Q&A:

“Our basic policy is to conclude contracts with customers and then receive an amount equivalent to the investment as an advance payment.”

Ibiden’s balance sheet already carries ¥92.1 billion in customer advance payments. Nvidia, Intel, and hyperscalers building custom AI chips are paying for the factories. Not investing in Ibiden’s equity. Paying for the physical capacity. Intel, AMD, and Nvidia have collectively co-funded roughly 50% of the expansion capex at their top four substrate suppliers.

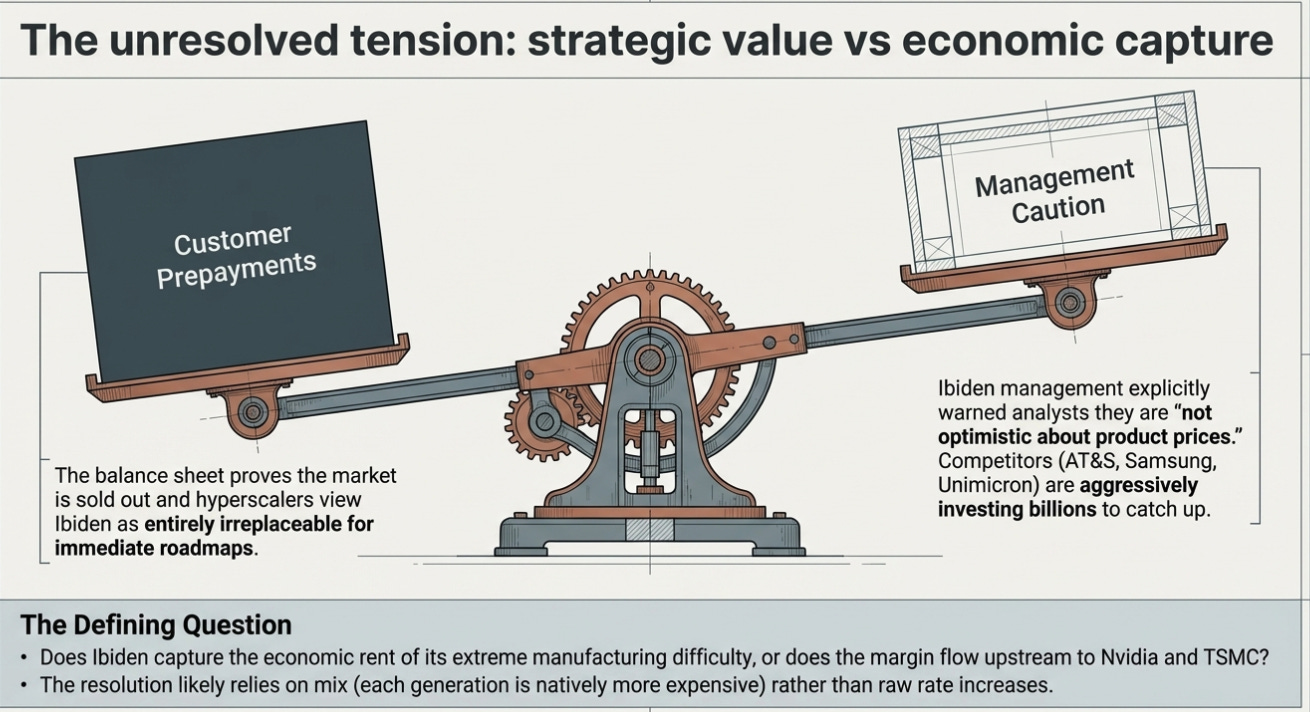

Customers behave this way when they believe they have no practical alternative. When the penalty for not having supply, a delayed GPU launch, a missed data center deployment, a slipped AI training cluster, exceeds the cost of funding someone else’s factory. That is what the advance payments tell you about power dynamics. Five years ago, Intel dictated specifications and Ibiden built to them. Now customers are competing to reserve Ibiden’s future capacity.

But here is the part that makes this more complicated than a simple dominance story. Despite holding 70–80% share in a sold-out market, Ibiden told analysts in October 2025 that the company was “not optimistic about product prices.” Competitors are expanding. AT&S is building in Malaysia and Austria. Samsung Electro-Mechanics is investing over a trillion won per year. Unimicron has raised annual capex to a record.

Management’s candor about pricing reveals the real question. The market does not need to be convinced that the work is hard. It does not need to be convinced that AI packaging is getting more complex or that Ibiden has a strong position. What the market needs to decide is whether Ibiden captures the economics of that difficulty, or whether it ends up doing increasingly important, increasingly expensive work while the returns flow elsewhere in the value chain.

The advance payments suggest customers think Ibiden matters. Management’s pricing caution suggests Ibiden may not be able to fully charge for how much it matters. The resolution probably comes through mix rather than rate: each generation’s substrate is larger, more complex, and higher-priced than the last, even if the pricing on any given product stays disciplined. That is a durable growth model. But it is not the same as pricing power, and the distinction matters for how much the stock is worth.

Two Companies in One Earnings Report

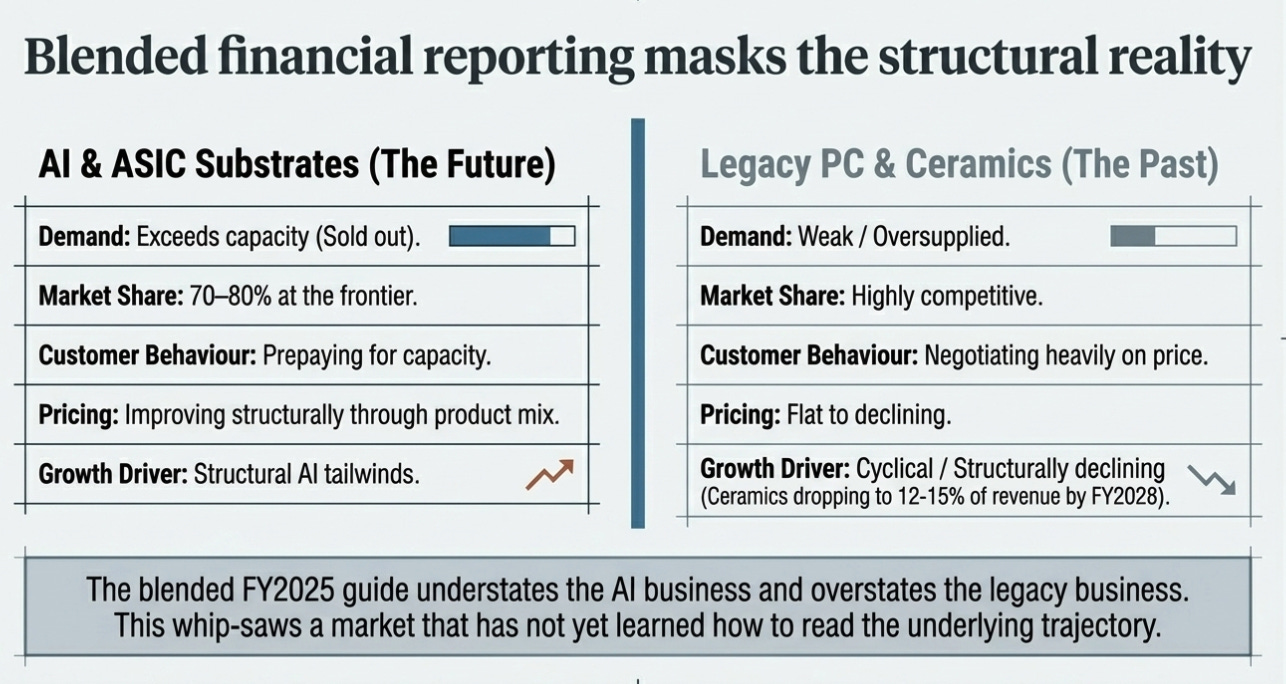

One reason this investment question is so hard to answer from reported results is that Ibiden still presents itself as one company when it is economically closer to two.

The AI and ASIC substrate business is growing into a tighter, higher-value market. Demand exceeds capacity. Customers fund expansion. Margins are expanding through mix.

The legacy PC, general-purpose server, and ceramics businesses are competitive, price-pressured, and in the case of ceramics, silicon carbide diesel particulate filters for European cars, structurally declining.

The blended FY2025 operating margin guide of 14.5% understates the first business and overstates the second. The Q3 FY2025 quarter “missed” expectations not because AI demand weakened, management said explicitly it did not, but because PC, server, and networking orders disappointed. The AI business delivered. The old business did not. The blended result looked mediocre. The trajectory underneath was unchanged.

By FY2028, ceramics will likely be 12–15% of revenue, a slowly shrinking business that the electronics segment is outgrowing. The risk is not that ceramics drags down the thesis. It is that blended reporting keeps making good quarters look mediocre and mediocre quarters look bad, whipsawing a stock that the market has not yet learned to read properly.

What the Stock Needs to Prove

On consensus estimates, Ibiden trades at roughly 50 times FY2026 earnings, 40 times FY2027, and 30 times FY2028. The market is already pricing significant improvement. The question is not whether the company is better than it was in 2023, obviously it is. The question is whether the earnings path from here justifies the entry point.

The variant view, and this is my view, is that the market is using the wrong time horizon and partly the wrong classification. If Ibiden’s reported return on capital understates the economic return to shareholders because customer prepayments fund a portion of the asset base, and if the Gama Plant represents a step-function increase in earnings power that is not yet in any forecast (management confirmed this explicitly in October 2025), then the forward multiples are less demanding than they appear. JPM raised its FY2028–2029 estimates in March 2026 specifically to capture Gama and new 2.5D packaging products. Consensus has not fully followed.

The market wants to treat this as a cyclical semiconductor company with AI exposure. The better frame may be a scarce, customer-reserved producer of something harder to replace than the market realizes. The gap between those two classifications is where the stock either works or doesn’t.

Three Futures

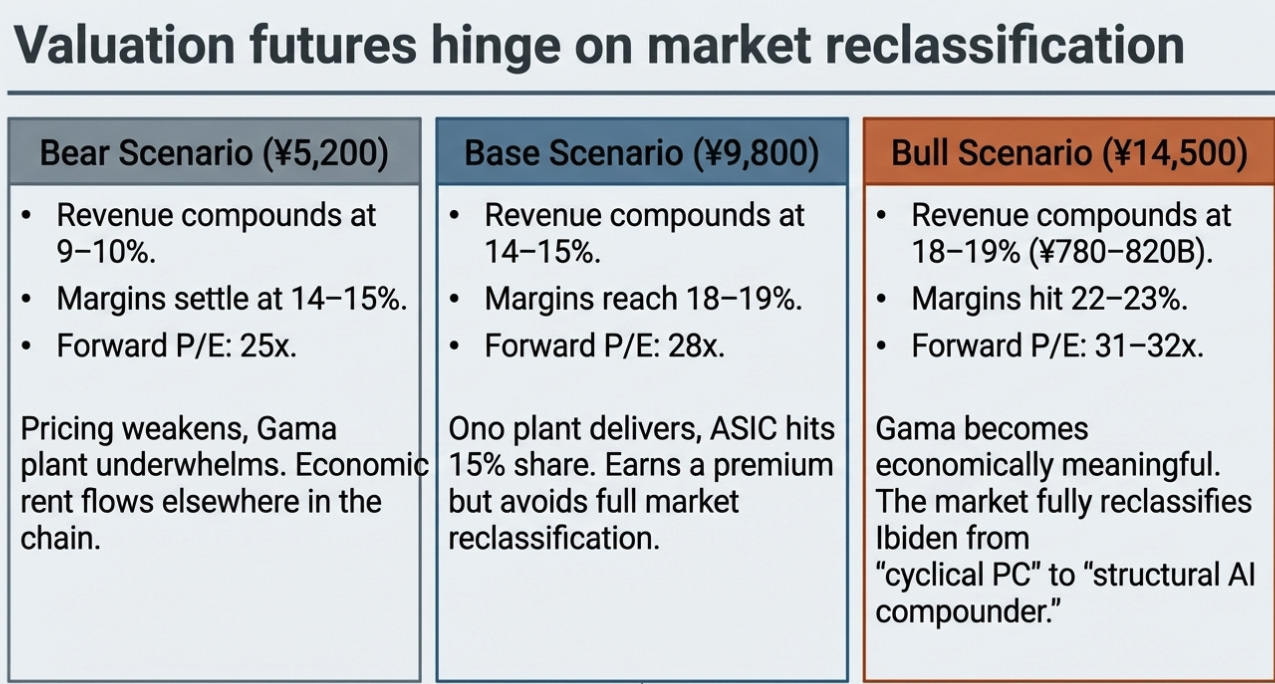

Bear, ¥5,200. Revenue compounds at 9–10% to ¥540–560 billion by FY2029. Margins settle at 14–15%. EPS: ¥200–210. At 25 times. Pricing weakens, Gama underwhelms, and Ibiden proves good but not great, difficulty keeps increasing, but the economic rent sits elsewhere.

Base, ¥9,800. Revenue compounds at 14–15% to ¥650–680 billion. Margins reach 18–19%. EPS: ¥340–350. At 28 times. Ono delivers, Gama contributes, ASIC diversification hits 15%. A very good business that earns its premium without transforming its classification.

Bull, ¥14,500. Revenue compounds at 18–19% to ¥780–820 billion. Margins hit 22–23%. EPS: ¥450–470. At 31–32 times. Gama becomes economically meaningful, the market reclassifies the business, and the old frame gives way.

What Would Prove This Right

The thesis does not need another quarter of noisy results. It needs evidence that the economics are catching up to the strategic importance.

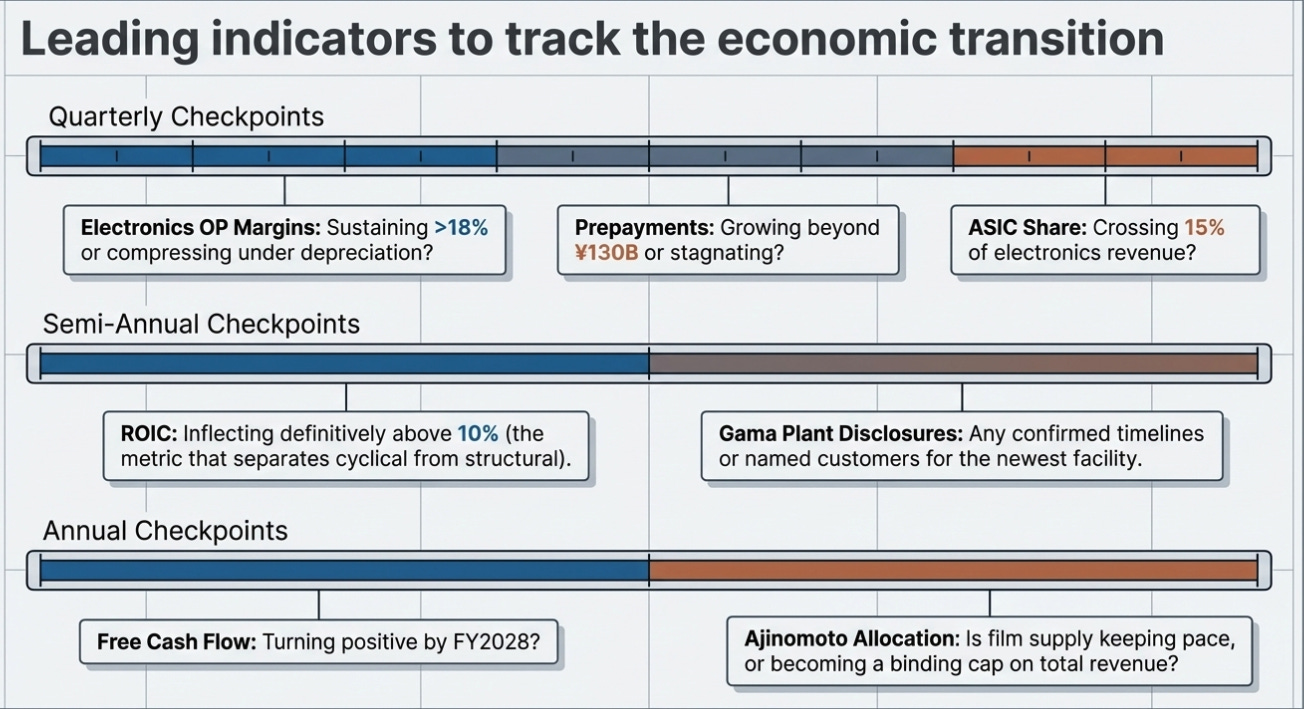

Watch quarterly. Electronics operating margin, sustaining above 18%, or compressing under depreciation? Customer advance payments, growing toward ¥130 billion or more, or stagnating? ASIC revenue as a share of electronics, crossing 15%?

Watch semi-annually. Return on invested capital, inflecting above 10%? That single metric is the most important test. It separates “well-positioned cyclical” from “business the market has misclassified.” Gama Plant disclosures, any named customer, confirmed timeline, or financial projection? Competitor yields at twenty-plus layers, is the gap narrowing or holding?

Watch annually. Free cash flow, positive by FY2028? Glass substrate milestones, commercial production for AI applications before 2029? Ajinomoto allocation decisions, is film supply keeping pace, or becoming the binding constraint nobody planned for?

The Constraint Beneath

Ibiden is either the most expensive cyclical stock in Japan or a structural compounder the market has not yet properly valued. Those are not close to the same thing.

I think the evidence tilts toward something the market has not fully absorbed. The customers closest to the problem, the chip designers whose products cannot exist without what Ibiden builds, are behaving as if this is not temporary scarcity. They are paying for factories. They are reserving future capacity. They are co-designing substrates eighteen months before tape-out. That is not how you treat a replaceable supplier.

But management is guiding as if the advantage might not last. Pricing caution despite a sold-out market. Conservative revenue targets that exclude the most strategically important factory. Language calibrated to keep expectations in check while the balance sheet fills with customer cash.

One of them, the customers or the management, is wrong about how durable this position is. The customer advance payments will tell you which. If they keep rising, the market has underestimated what Ibiden is becoming. If they stall, the old classification was right, and the stock is expensive.

The Ibi River still runs through Gifu. The hydroelectric plants still generate a modest current, 147,340 megawatt-hours last year. The company that started by converting a river’s force into usable power is now converting manufacturing difficulty into the physical foundation of AI. Whether difficulty compounds faster than capital consumes it is the question that will determine what Ibiden is worth.

The river has not stopped flowing in 113 years. But rivers do not care about earnings multiples. The advance payments do.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.