Intel's 1Q26 Earnings: The CPU Thesis Arrived; The Foundry Thesis Didn't

Q1 2026 showed that AI inference is reviving Intel’s server CPU franchise, but the harder question remains whether that product momentum can fund a foundry turnaround before the cycle turns.

TL;DR

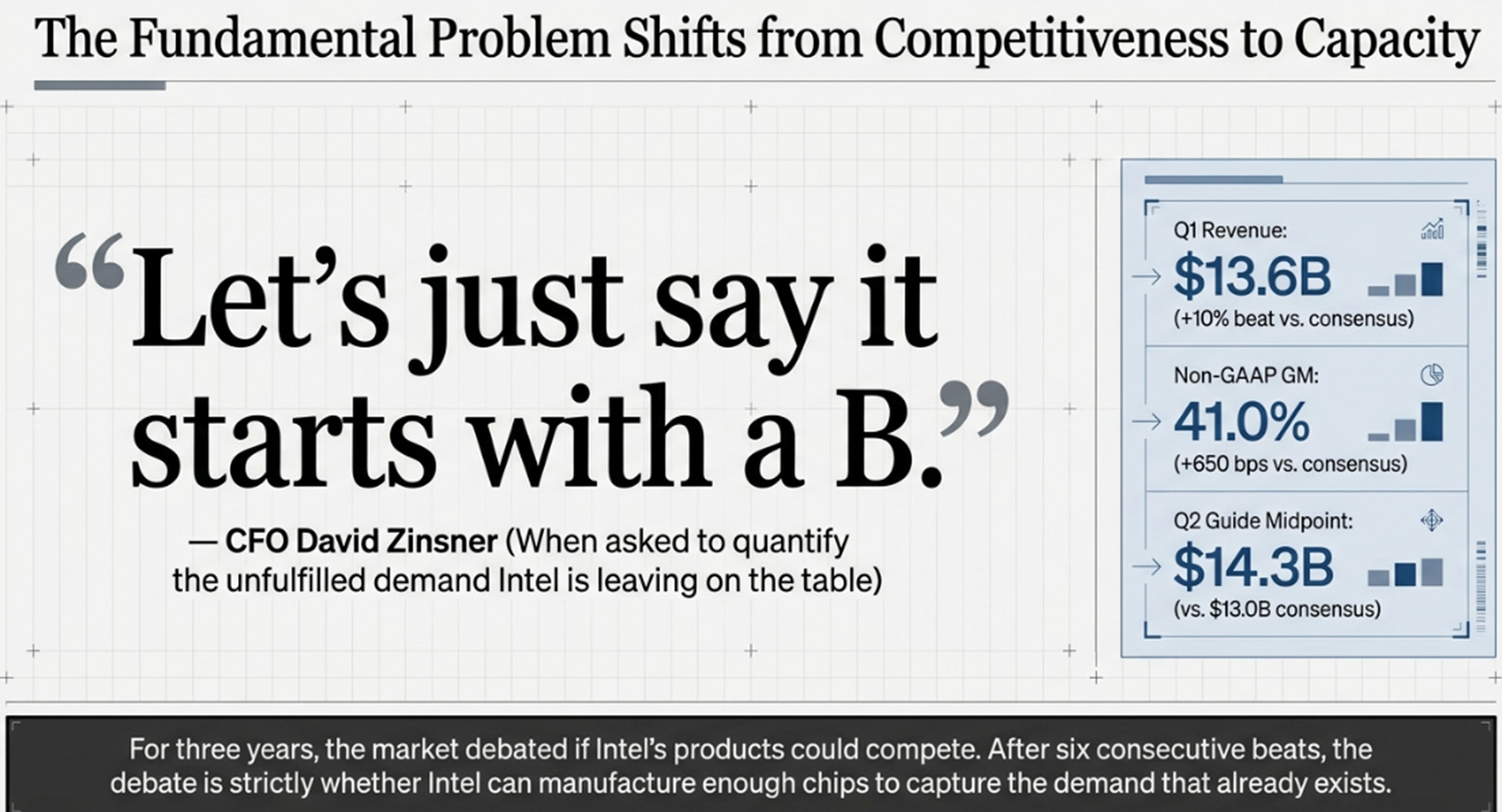

The quarter reframed Intel’s problem from demand to supply. Server CPU demand is strong enough that management suggested unfilled demand “starts with a B,” while DCAI margins expanded sharply to 30.5%.

The CPU thesis is finally visible, but the foundry thesis is still mostly prospective. Google LTAs, Nvidia DGX Rubin NVL8, and custom ASIC growth validate Intel’s AI infrastructure role, while external foundry revenue remains small and losses remain large.

Intel is now a race between two clocks. The product flywheel is accelerating, but the foundry still consumes cash; the bull case depends on CPU-led cash generation arriving before AI demand slows.

From Bloomberg’s Ian King:

Intel Corp. delivered a blockbuster sales forecast that shattered Wall Street expectations, signaling that the long-struggling chipmaker is benefiting from the giant build-out of artificial intelligence computing. Revenue will be $13.8 billion to $14.8 billion in the June quarter. Analysts estimated $13 billion on average.

I’ll admit it: I did not expect Intel to report a quarter where the most important number was the one management didn’t report, the revenue they couldn’t ship. When CFO David Zinsner was asked on the call to quantify how much demand Intel is leaving on the table, his answer was five words: “Let’s just say it starts with a B.”

That single sentence reframes the entire Intel debate. For the past three years, the question has been whether Intel’s products are competitive enough to sustain the company while it tries to become a foundry. After this quarter, the question is whether Intel can manufacture enough chips to capture the demand that already exists. That’s a fundamentally different problem, and a much better one to have.

Here are the numbers:

Sixth consecutive beat. Every line above the high end of guidance. Stock up 15–20% after hours toward $76–82.

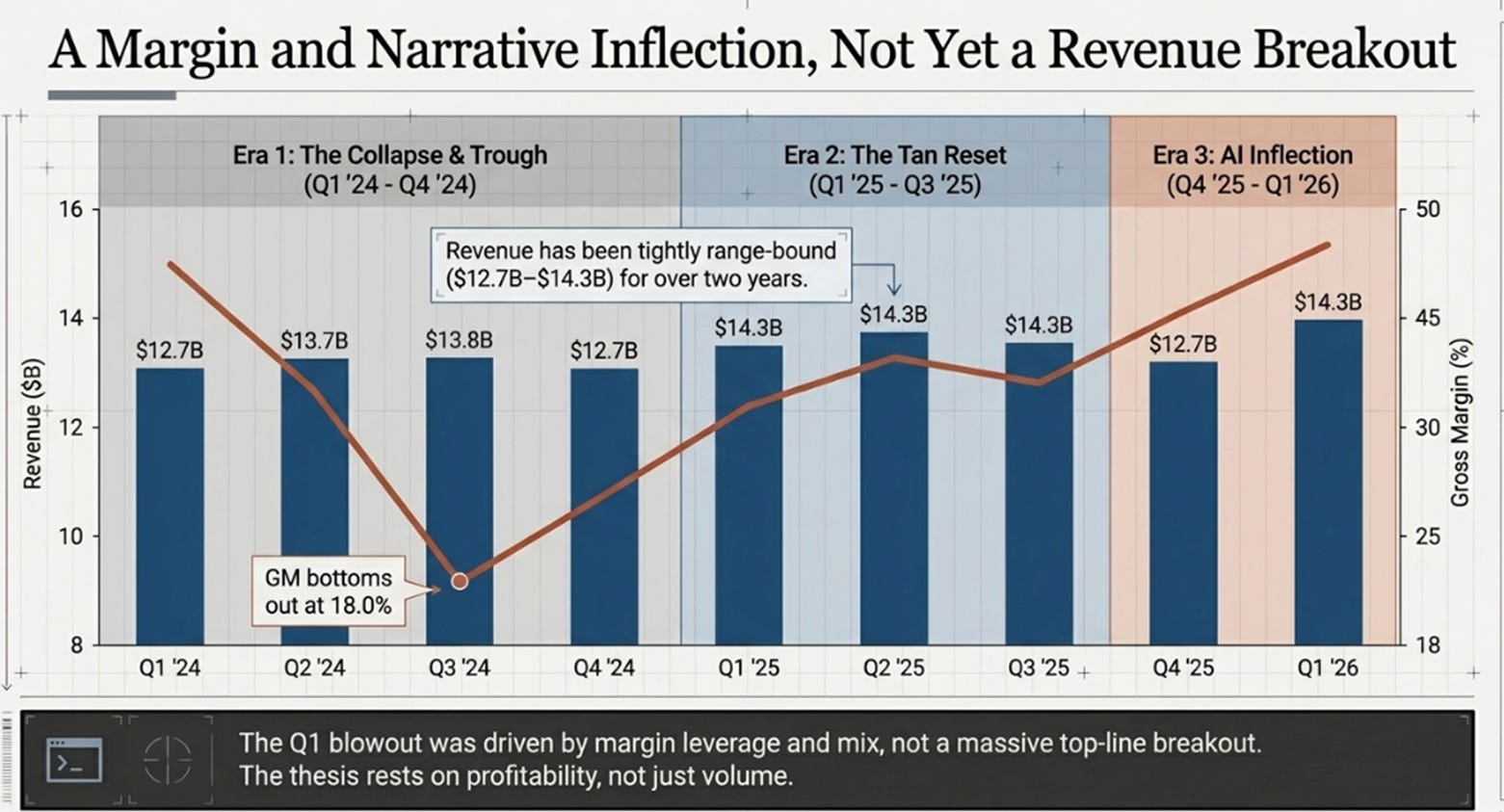

But a single quarter, even a blowout, only matters if it reveals something about the company’s trajectory. Nine quarters of context tell the story:

Revenue has been range-bound between $12.7B and $14.3B for two years. This is not yet a revenue inflection. It is a margin and narrative inflection, and the distinction matters for everything that follows.

Why the CPU-to-GPU Ratio Is the Quarter’s Most Important Number

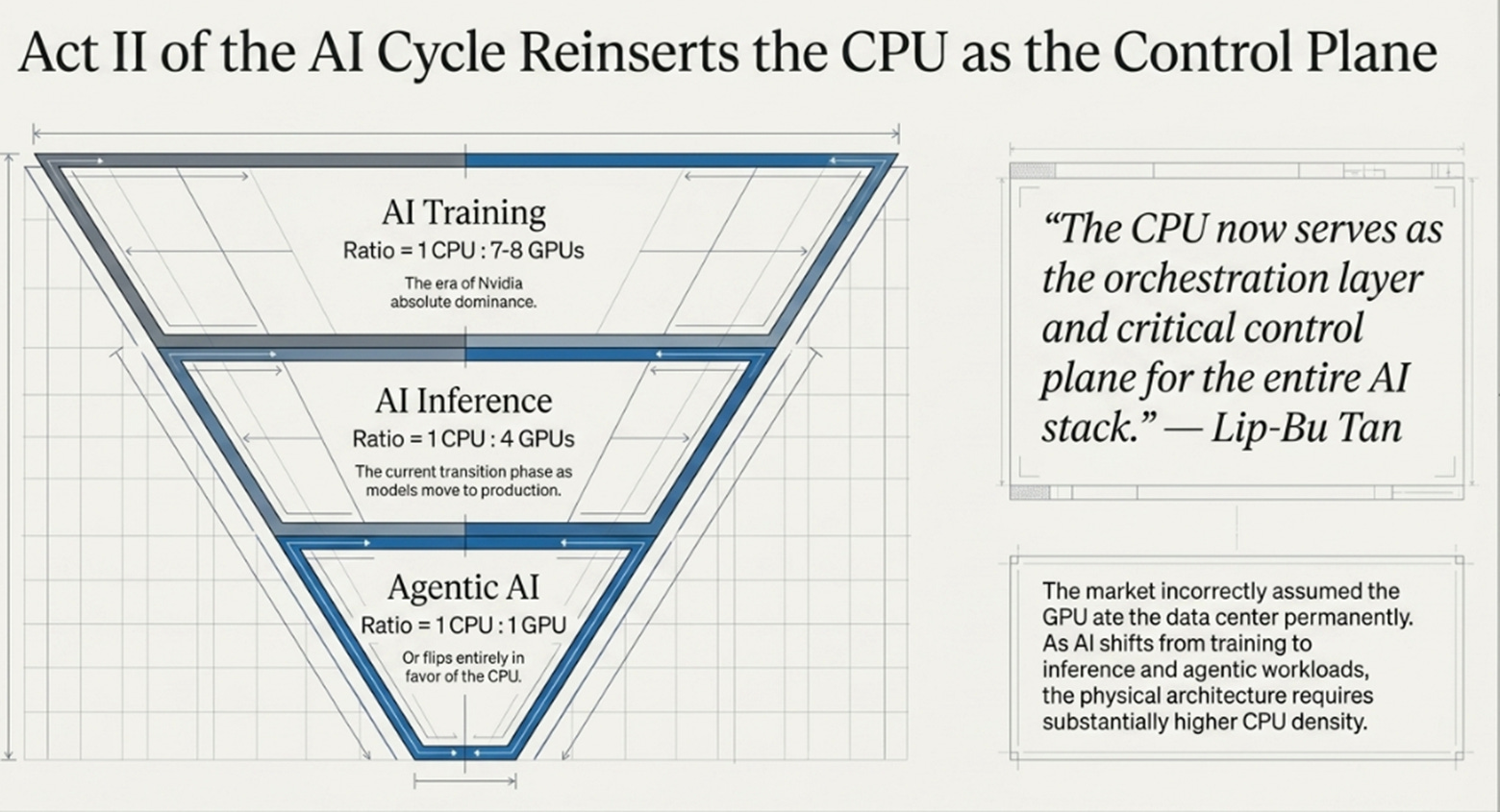

There is a narrative that has dominated the semiconductor conversation since late 2022: the GPU is eating the data center. Nvidia’s ascent from a $300 billion company to a $3+ trillion company was built on a simple and largely correct observation, AI training requires massive parallel compute, and GPUs deliver that better than anything else.

What this narrative missed, and what Intel’s Q1 results illuminate, is that training was only the first act. The industry is now moving into inference, agentic AI, and production deployment, and each of these stages reinserts the CPU as a critical component of the stack. Here’s how Lip-Bu Tan described it:

“The CPU now serves as the orchestration layer and critical control plane for the entire AI stack. This is not just our wishful thinking. It is what we hear from our customers, and it is evident in the demand profile for our products.”

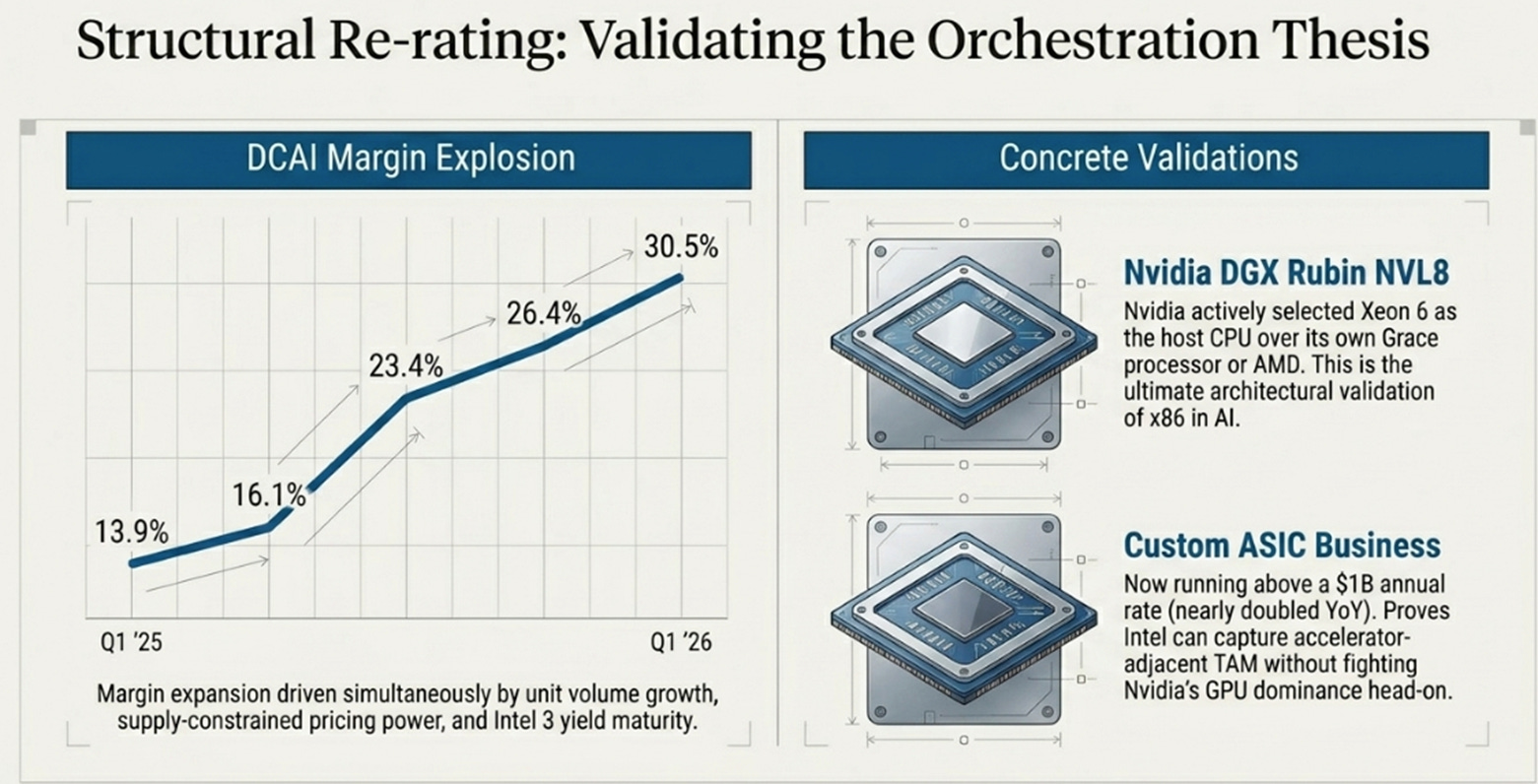

The numbers back him up. DCAI revenue hit $5.05 billion, up 22% year-over-year, with operating margins expanding from 13.9% a year ago to 30.5%, a trajectory that looks less like cyclical recovery and more like structural re-rating:

That margin expansion, from 14% to 31% in four quarters, is remarkable. It’s driven by three forces operating simultaneously: volume growth (more units), pricing power (supply constraints letting Intel raise ASPs), and cost improvement (Intel 3 yields maturing). When all three move in the same direction at once, the operating leverage is enormous.

But the number that really matters is the CPU-to-GPU ratio. Zinsner laid out the math: training runs at 1 CPU for every 7–8 GPUs. Inference drops to 1:4. Agentic workloads approach 1:1 or potentially flip in the CPU’s favor. If you believe, as I do, that inference and agentic are going to be substantially larger markets than training, then the total addressable market for server CPUs is expanding, not shrinking.

Two data points from the quarter make the CPU-demand thesis concrete rather than theoretical. First, Xeon 6 was selected as the host CPU for Nvidia’s DGX Rubin NVL8, the most important AI server platform on earth. Nvidia could design its own CPU; it has Grace. It could use AMD. It chose Intel. That is not a legacy relationship being maintained out of inertia; it is an active architectural decision by the company with the deepest understanding of AI data center requirements. When Nvidia puts Intel inside its flagship rack, it validates the x86 orchestration thesis in a way no amount of management commentary can.

Second, Intel’s custom ASIC business, purpose-built silicon for specific customer workloads, nearly doubled year-over-year and is now running above a $1 billion annual rate. Zinsner said on the call that “people have been surprised about how big the business is already,” and Tan described it as a fast-growing opportunity over the next five years. This matters because it shows Intel can participate in the accelerator-adjacent TAM without competing head-on with Nvidia’s GPU franchise. Intel brings x86 CPU IP, advanced packaging, and captive manufacturing to the table; the customer brings the workload-specific design. It’s a business model that didn’t exist two years ago.

These customer commitments sit underneath the structural argument that HSBC’s Frank Lee is building his $95 price target around: 20% server CPU shipment growth in both 2026 and 2027, with 20% ASP increases in 2026 and 10% in 2027. His DCAI revenue estimates of $22.8B (2026) and $29.1B (2027) sit 16% and 33% above Street consensus. Those are aggressive numbers. After this print, they look more plausible than they did a week ago.

What Intel Wants You to See, and What It Buried

I find it instructive to examine what Intel’s earnings presentation highlighted and what got buried. The slide deck’s executive summary had four bullet points:

Tangible Progress Building the New Intel

6th Consecutive Quarter Exceeding Expectations

Intel CPUs Foundational to Inference and Agentic

AI Driving Demand for Silicon and Advanced Packaging

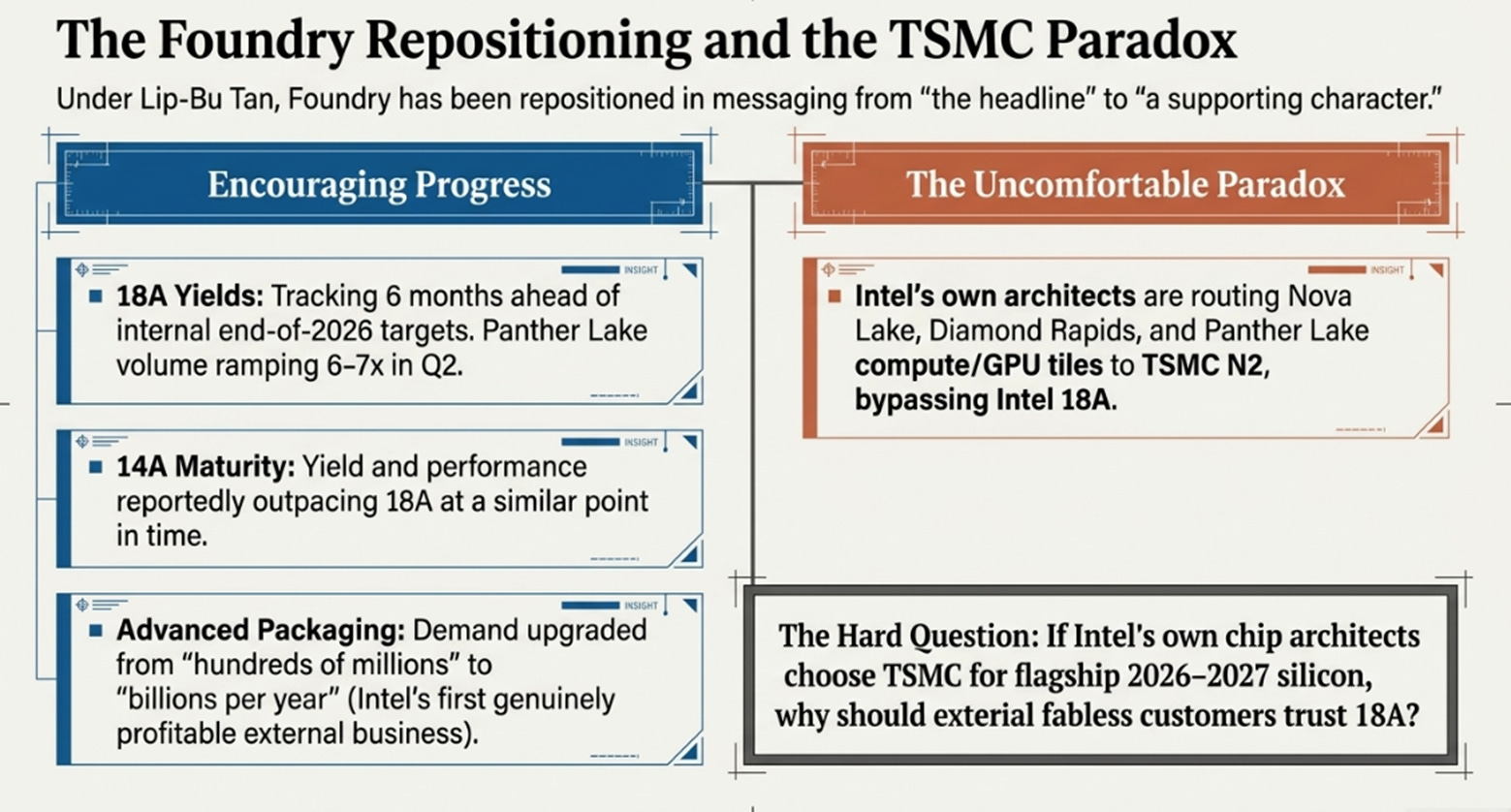

Notice what’s missing: the foundry. External foundry revenue. 14A customer names. Foundry breakeven timeline. These were the centerpieces of Intel’s narrative under Pat Gelsinger. Under Lip-Bu Tan, the foundry is repositioned as a supporting character, important, progressing, but not the headline.

This is smart messaging management. Tan understands that the market will pay for what’s measurable today (server CPU demand, margin expansion, supply constraints) and discount what’s prospective (external foundry revenue, 14A customer conversion). By leading with the product franchise and making foundry progress a secondary talking point, he lets the numbers speak first and the narrative follow.

That said, when you dig into the foundry details, the news is more encouraging than the understated presentation suggests:

18A yields: Zinsner revealed that Tan’s end-of-2026 yield target will likely be hit by mid-year. That’s a six-month pull-in on the company’s own internal plan. He also noted that Panther Lake volume is ramping 6–7x from Q1 to Q2, a genuine production ramp, not a token volume.

14A progress: Tan said 14A “maturity, yield, and performance are outpacing Intel 18A at a similar point in time.” If true, this is significant, it suggests Intel’s learning curve is compressing, which is exactly what you’d expect from an organization that has gotten its manufacturing discipline back.

Advanced packaging: This is where Zinsner’s tone shifted from measured to almost excited. His prior guidance was “hundreds of millions” of external packaging revenue. On this call, he upgraded that to demand “in the billions of dollars per year kind of level,” with margins at or above foundry average. Packaging may end up being Intel Foundry’s first genuinely profitable external business, arriving before the wafer revenue that gets all the attention.

But here’s what Intel didn’t mention, and what bulls need to sit with: Intel’s own product designers are routing Nova Lake desktop compute tiles and Diamond Rapids server compute tiles to TSMC’s N2 process, not Intel 18A. The GPU and I/O tiles for Panther Lake also go to TSMC. In other words, Intel’s highest-performance 2026–2027 silicon, the chips that will determine whether Intel stabilizes server CPU share, will be manufactured by Intel’s foundry competitor.

Management can explain this as rational chiplet-era engineering: use TSMC N2 where density matters most, use 18A where PowerVia delivers a power-delivery advantage. That’s technically defensible. But it creates an uncomfortable credibility problem for the external foundry pitch. If Intel’s own chip architects, who have the most intimate knowledge of 18A’s capabilities and limitations, choose to send their flagship compute tiles elsewhere, why should an external fabless customer trust 18A with their flagship silicon? This is the single hardest question in the Intel bull case, and nobody on the earnings call asked it.

The GAAP Problem Nobody Wants to Talk About

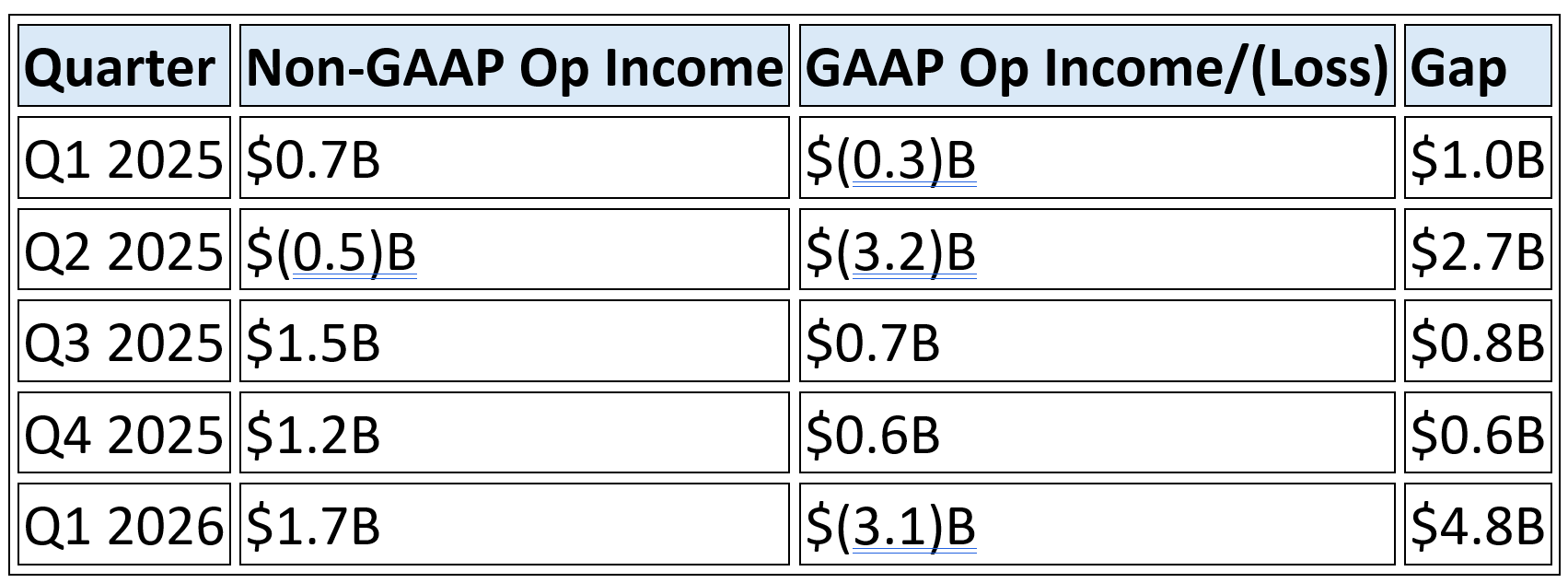

Here’s where I need to push back on the euphoria. Intel reported non-GAAP EPS of $0.29. It reported GAAP EPS of $(0.73). The gap, over a dollar per share, is explained by $4.1 billion of restructuring and other charges (primarily a Mobileye goodwill impairment), $621 million of stock-based compensation, and $1.1 billion of mark-to-market losses on the government’s escrowed shares.

You can argue that any one of these is non-recurring or non-operational. But when the adjustments consistently dwarf the “real” earnings, when non-GAAP operating income is $1.7 billion but GAAP operating loss is $3.1 billion, it’s worth asking what the actual economic earnings of this business are.

Here’s the five-quarter trend:

The Q1 2026 gap is the widest in a year, driven almost entirely by the Mobileye impairment. Fair enough, goodwill impairments are non-cash and backward-looking. But the pattern of chronic GAAP losses alongside improving non-GAAP earnings is a feature of Intel’s financials that bulls need to at least acknowledge.

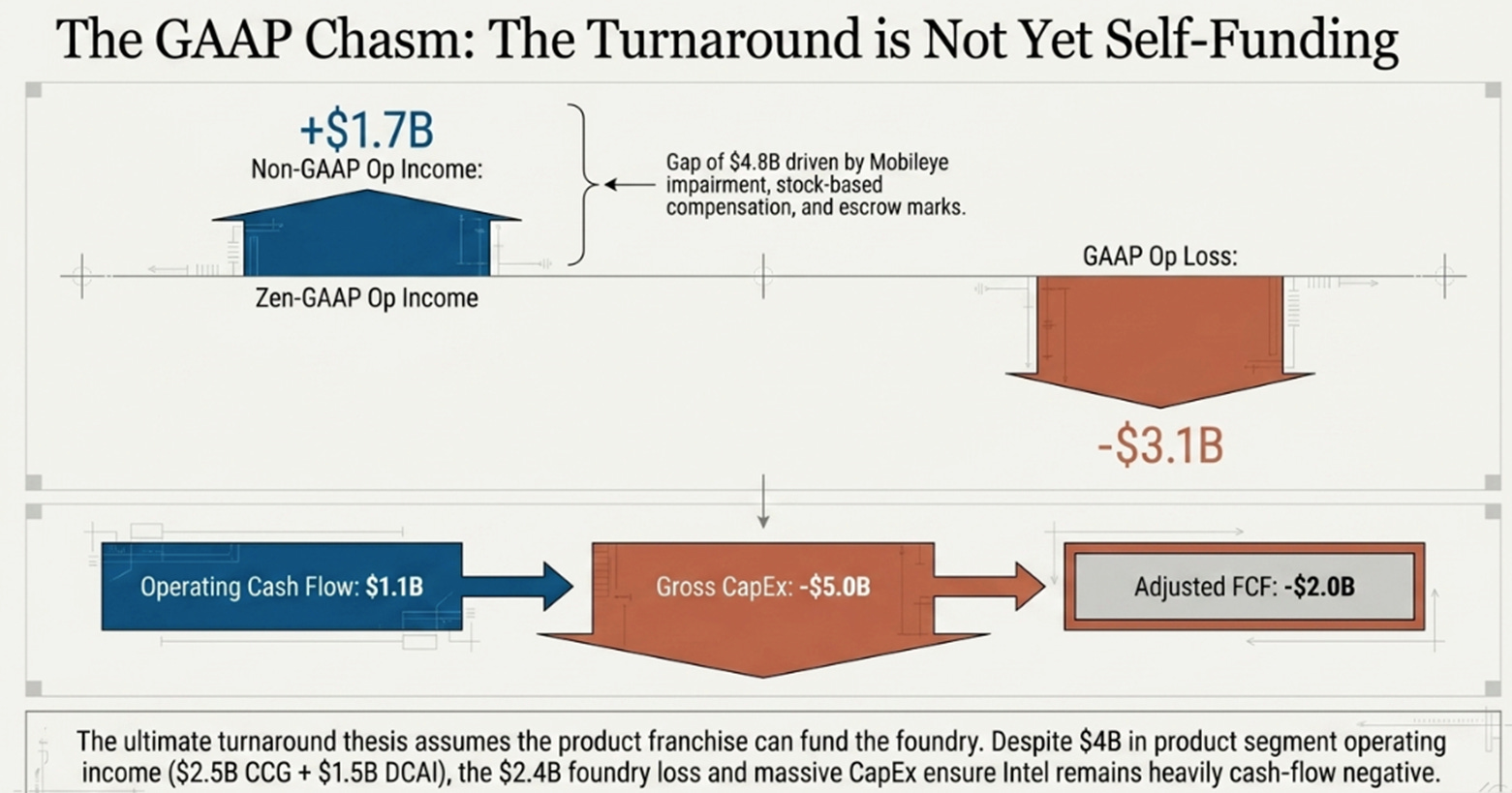

The other number that deserves scrutiny: adjusted free cash flow of negative $2.0 billion. Intel is still spending more on capital investment than it generates from operations, even in a blowout revenue quarter. Operating cash flow was $1.1 billion; gross capex was $5.0 billion. Government incentives ($107M) and partner contributions ($2.0B) close part of the gap, but the business is not self-funding its investment program. Zinsner reiterated positive adjusted FCF for the full year excluding the Fab 34 buyback, but that “excluding” is doing a lot of work given that the buyback was $14.2 billion.

This matters because the entire turnaround thesis assumes Intel’s product franchise can fund the foundry transition. Right now, the product franchise is generating $4B of segment operating income per quarter ($2.5B CCG + $1.5B DCAI), but after corporate overhead, foundry losses ($2.4B), and capex, the company is still cash-flow negative. The trajectory is improving, but it’s not there yet.

Using Scarcity to Lock In Customers

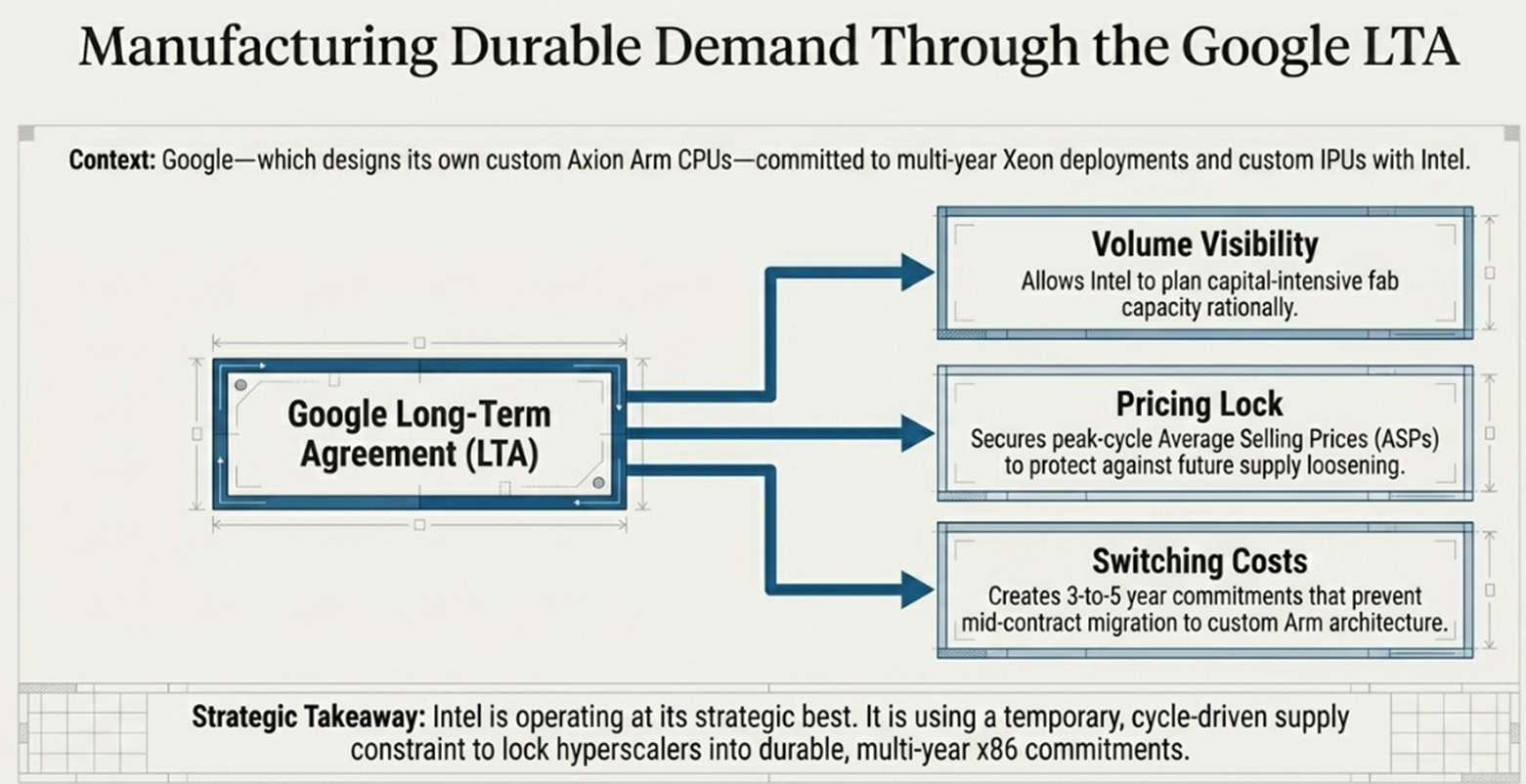

The most strategically important disclosure in the quarter wasn’t a financial metric, it was the Google long-term agreement. Google committed to deploying multiple generations of Intel Xeon processors across its data centers and co-developing custom IPUs with Intel.

Why does this matter? Because Google is one of three hyperscalers (along with AWS and Microsoft) that has invested heavily in custom Arm CPUs for its data centers. Google has Axion. If Google, a company that designs its own TPUs, its own CPUs, and its own networking chips, is signing multi-year Xeon commitments, it tells you something about the indispensability of x86 in production AI infrastructure.

Zinsner described the LTA structure: “Most of these agreements are structured with volume and pricing. They’re usually somewhere between three and five years.” He also noted that some customers prefer confidentiality, implying there are additional agreements beyond Google that Intel hasn’t announced.

The LTA strategy serves three purposes simultaneously. First, it gives Intel volume visibility, which lets the company plan capacity more rationally. Second, it locks in pricing in a supply-constrained market, protecting Intel from future price competition if supply loosens. Third, it creates switching costs, once a hyperscaler commits to three-to-five years of Xeon volume at negotiated prices, they’re not migrating that workload to Arm mid-contract.

This is Intel at its strategic best: using a temporary supply advantage to create durable demand commitments. The question is whether the commitments survive the end of the supply constraint.

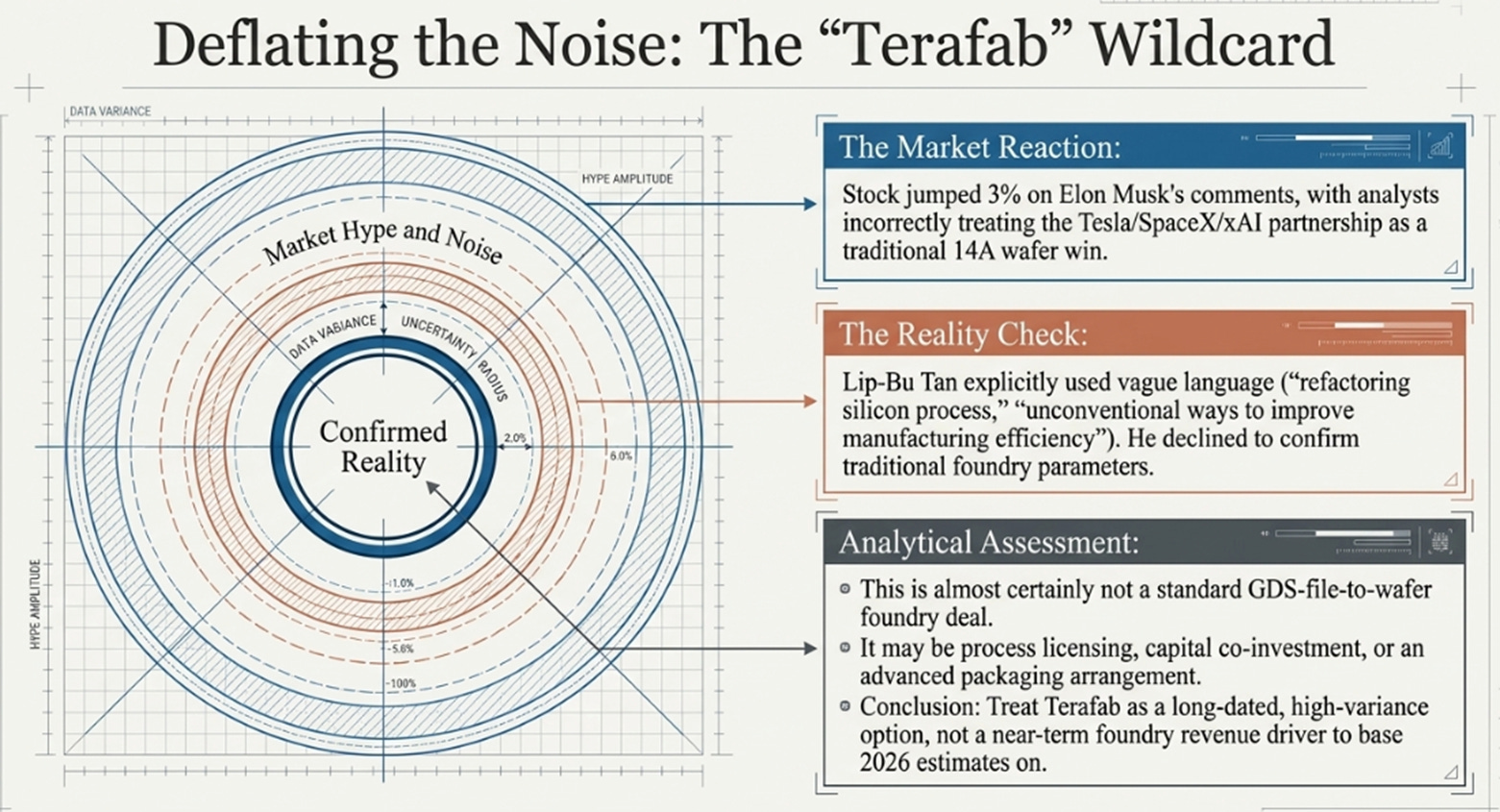

The Terafab Question

I want to address the Terafab partnership separately because I think the market is conflating two different things.

The Tesla/SpaceX/xAI Terafab project is being treated as a 14A foundry customer win. The stock jumped 3% on Musk’s comments, and it was cited as a catalyst in virtually every post-earnings note. But listen carefully to what Tan actually said on the call:

“Elon and I, we believe that global supply chain is not keeping pace with the rapid acceleration in demand. We both share the vision that we’re going to learn a lot together, exploring the innovative way... in the process of the manufacturing.”

And when pressed by Tim Arcuri on whether this is a traditional foundry arrangement or something different, possibly a process licensing deal or even turning over an entire fab, Tan said: “Clearly it’s a very broad relationship and then, we would update you as we go.”

This is deliberately vague. “Very broad relationship” could mean many things. It could be a multi-billion-dollar 14A wafer commitment. It could be a co-investment in a new fab where Intel provides the process technology and Tesla provides the capital. It could be an advanced packaging deal for chips designed by Tesla and fabbed elsewhere.

What it almost certainly is not is a typical foundry engagement where Intel takes a GDS file and produces wafers. The language about “refactoring silicon process technology” and “unconventional ways to improve manufacturing efficiency” suggests Musk wants to rethink how fabs operate, which is interesting intellectually but commercially uncertain.

I’d treat Terafab as a long-dated option with high variance, not as a near-term revenue driver. The fact that Tan declined to provide further details, even after Musk publicly named Intel on Tesla’s earnings call, suggests the commercial terms are either not finalized or structured in a way that doesn’t map cleanly to traditional foundry revenue.

Intel’s Three Different Competitive Problems

It’s tempting to ask “who is Intel competing against?” as if the answer is one company. It’s not. Intel faces three structurally different competitive contests, and this quarter changed Intel’s position in each of them differently.

Against AMD, the fight is x86 versus x86: core count, performance-per-watt, roadmap cadence, pricing. AMD took 41.3% server revenue share in Q4 2025 and nothing in this quarter’s data shows that trend reversing. Tan acknowledged the gap, noting that Coral Rapids will restore multithreading to compete more effectively, which is an implicit admission that current products are disadvantaged. The supply constraint masks the share loss: Intel can sell everything it makes regardless of competitive position. When supply normalizes, the AMD question returns.

Against Arm and hyperscaler custom silicon, the fight is architectural control. Amazon, Google, and Microsoft are building their own CPUs not primarily for performance but to reduce dependency on merchant suppliers and capture margin internally. Intel’s response here isn’t just x86 compatibility, it’s the bundle: ASIC co-design, custom IPUs, advanced packaging, and captive manufacturing capacity. The Google LTA is evidence this response is working. Google signed a multi-year Xeon commitment despite having Axion. That means x86 offers something Arm doesn’t for those specific workloads, probably software ecosystem depth and orchestration maturity.

Against TSMC, Intel is simultaneously a customer and an aspiring competitor. Tan explicitly called TSMC “a very important partner” and described a multi-foundry approach. This is rational, Intel Products needs the best manufacturing, even if Intel Foundry wants external customers. But it creates the credibility tension described above: every tile Intel sends to TSMC is a tile that didn’t go to its own fabs.

The strategic implication is that Intel’s moat, if it rebuilds one, won’t be a single-product advantage. It will be a bundle: x86 installed base, server CPU orchestration, customer-specific IP, advanced packaging, domestic leading-edge manufacturing, and long-term supply commitments. No single element is defensible alone. Together, they might be.

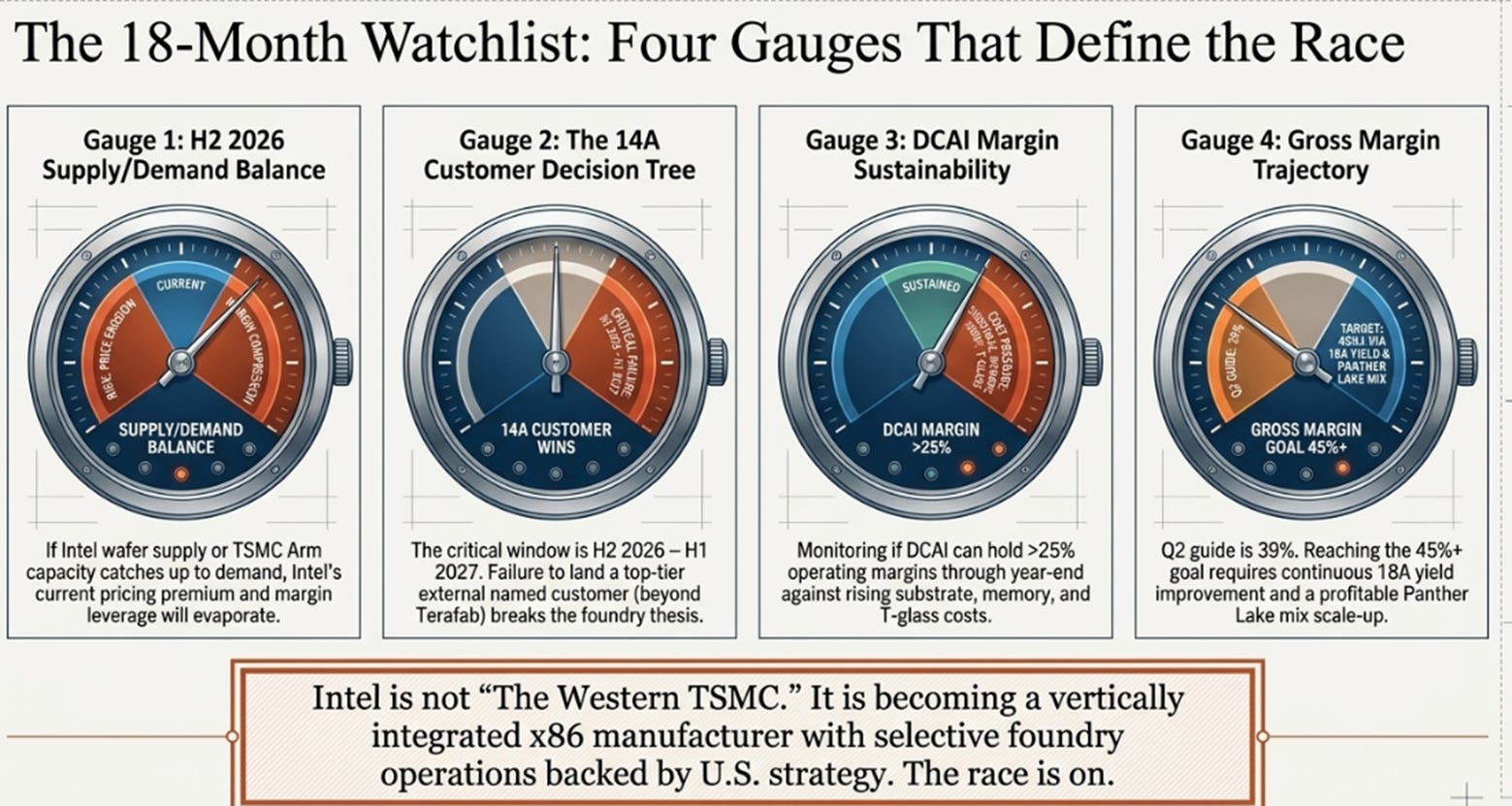

What I’m Watching

The supply-demand balance through H2 2026. Intel’s pricing power exists because of supply constraints, not because of product superiority (though Granite Rapids early traction is positive). If supply catches up to demand, either through Intel’s own wafer start increases, TSMC expanding Arm CPU capacity, or a hyperscaler capex slowdown, the pricing premium evaporates. Zinsner said supply will increase every quarter going forward, but demand outlook has also improved. The sequencing matters enormously.

The 14A customer decision tree. Tan said he expects “earlier design commitments emerging beginning in the second half of 2026 and expanding into the first half of 2027.” This is the window. If H2 2026 passes without a named top-tier 14A customer (beyond the ambiguous Terafab arrangement), the foundry thesis weakens materially.

DCAI operating margin sustainability. The 30.5% margin in Q1 was flattered by pricing actions, improving Intel 3 yields, and volume leverage. Memory cost increases in H2 (”substrates are going up, T-glass, memory” per Zinsner) could compress margins even as revenue grows. If DCAI margins hold above 25% through year-end while revenue grows 20%+, the earnings power of the product franchise is genuinely transformed.

Gross margin trajectory. The 41% non-GAAP GM in Q1 included inventory reserve releases that won’t repeat. Q2 is guided at 39% due to heavier 18A mix (Panther Lake at 6–7x volume but below corporate-average margins). The path from 39% toward 45%+ requires 18A yields to keep improving and input cost inflation to moderate. Both are plausible but neither is guaranteed.

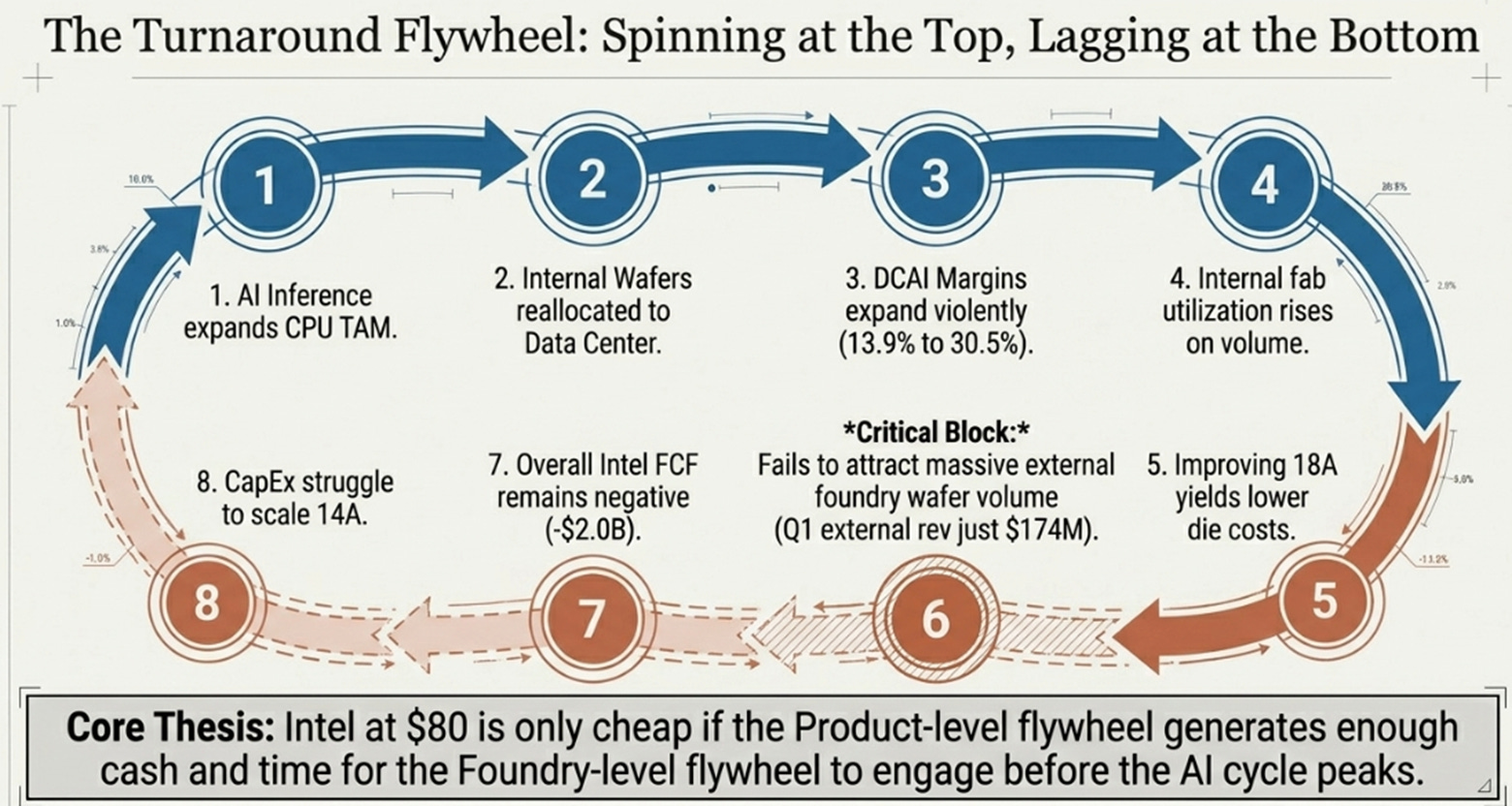

The Loop That Matters

Before addressing valuation, it’s worth making explicit the self-reinforcing mechanism that the bull case depends on, because if it’s real, it changes what Intel is worth, and if it’s not, nothing else in this quarter matters.

The loop works like this: AI-driven server CPU demand rises → Intel reallocates wafer starts from client to data center → DCAI revenue and margins expand (13.9% → 30.5% in four quarters) → higher internal wafer volume improves fab utilization → foundry losses narrow as fixed costs are spread across more units → improving 18A yields lower cost-per-good-die → better yields attract external foundry and packaging customers → packaging backlog converts to high-margin revenue → Intel generates more cash to invest in 14A and capacity → better process technology attracts more customers. Each turn of the loop makes the next turn easier.

This is the mechanism that distinguishes “Intel is having a good quarter” from “Intel is structurally more valuable.” The evidence from Q1 that the loop is engaging: DCAI margin expansion is real and accelerating; Zinsner confirmed 18A yields are ahead of plan; packaging demand upgraded from hundreds of millions to billions per year; Google, Nvidia, and undisclosed others signed multi-year LTAs. The evidence that the loop has not yet fully engaged: external foundry revenue was $174M; the foundry lost $2.4B; adjusted free cash flow was -$2.0B; and Intel still sends its own best silicon to TSMC.

The loop is spinning at the product level. It has not yet reached the foundry level. The question that determines whether Intel at $76–82 is cheap or expensive over the next 18 months is simple: Does the product-level flywheel generate enough cash and enough time for the foundry-level flywheel to engage before the AI infrastructure cycle peaks?

The Strategic Position

Intel is not a foundry company. It may never be a foundry company in the way TSMC is a foundry company, with dozens of fabless customers across the design ecosystem. What Intel is becoming, under Tan, is something different: a vertically integrated manufacturer of x86 server processors with a packaging services business and a selective external foundry operation funded by the U.S. government’s strategic interest in domestic leading-edge capacity.

That’s a less exciting pitch than “the Western TSMC.” But it may be a more honest and more achievable one. The product franchise is generating real cash, $4B of quarterly segment operating income, and the demand environment for server CPUs is the strongest it’s been in a decade. If Intel can convert that demand into sustainable earnings while gradually shrinking foundry losses through higher internal utilization and selective external wins (packaging first, wafers later), the financial model starts working without requiring Intel to become something it has never been.

The risk, as always with Intel, is that the current strength is cyclical, not structural. Server CPU demand is booming because AI infrastructure is being built out at unprecedented scale. That build-out will slow at some point. When it does, Intel’s supply constraints will vanish, its pricing power will erode, and the bears will re-emerge with the same arguments they’ve always had: AMD is eating x86 share, Arm is eating x86 TAM, and the foundry burns $10 billion a year.

The difference between this moment and 2024 is that Intel now has 18 months of demonstrated execution under a credible CEO, a balance sheet that can absorb another cycle, strategic investors who are economically aligned with the turnaround, and, for the first time, a demand environment where the product franchise and the manufacturing base reinforce each other rather than competing for capital. Those are real assets.

Whether they’re worth $400 billion depends on a race between two clocks: the product flywheel generating cash, and the foundry flywheel consuming it. This quarter showed the product clock accelerating. The foundry clock hasn’t slowed yet. The bull case is that the gap between them is closing. The bear case is that the AI cycle will peak before it does.

I don’t know which clock wins. But after Q1 2026, I know this is a race worth watching, and that’s a sentence nobody would have written about Intel eighteen months ago.

$INTC

General Disclaimer: The information presented in this communication reflects the views of the author and does not necessarily represent the views of any other individual or organization. It is provided for informational purposes only and should not be construed as investment advice, a recommendation, an offer to sell, or a solicitation to buy any securities or financial products.

While the information is believed to be obtained from reliable sources, its accuracy, completeness, or timeliness cannot be guaranteed. No representation or warranty, express or implied, is made regarding the fairness or reliability of the information presented. Any opinions or estimates are subject to change without notice.

Past performance is not a reliable indicator of future performance. All investments carry risk, including the potential loss of principal. This communication does not consider the specific investment objectives, financial situation, or particular needs of any individual.

The author and any associated parties disclaim any liability for any direct or consequential loss arising from the use of this material and undertake no obligation to update or revise it.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.