KLA 3QFY26 Earnings: The Complexity Tax Gets More Real

KLA 3QFY26 Earnings: The Complexity Tax Gets More Real

TL;DR

The business got better: KLA’s moat widened through higher process-control intensity, advanced packaging momentum, services growth, and sustained share leadership.

The selloff was rational: KLA is priced like the best AI equipment story, but for now it is growing slower than etch/deposition peers because the AI fab cycle is still in the capacity-building phase.

The key question is conversion: Gross margin recovery, memory mix rebound, free-cash-flow conversion, and FY2027 EPS revisions will determine whether the complexity tax becomes near-term shareholder returns.

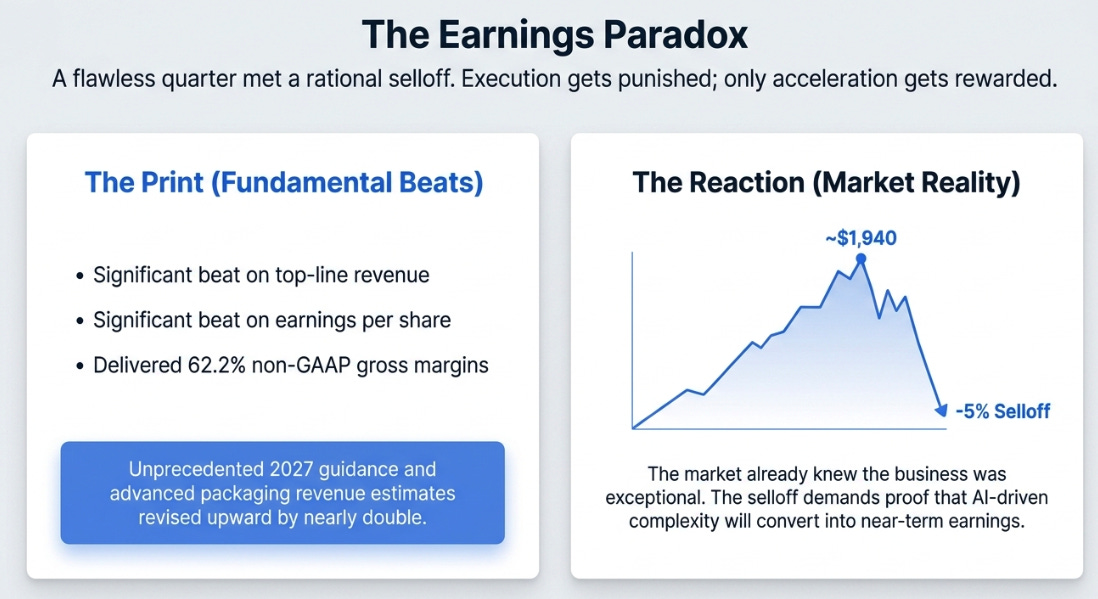

KLA beat on revenue. It beat on earnings. It beat on gross margins. Management gave the most bullish forward commentary in the company’s history, explicitly breaking their own precedent to discuss 2027 growth expectations in April of 2026. Advanced packaging revenue estimates were revised upward by nearly double. The stock fell 5%+.

This is not irrational. It is informative. And it is where I want to start this update, because the gap between a nearly flawless quarter and a meaningful selloff tells you something important about where KLA sits in the market’s mental model of the AI infrastructure buildout.

The Complexity Tax

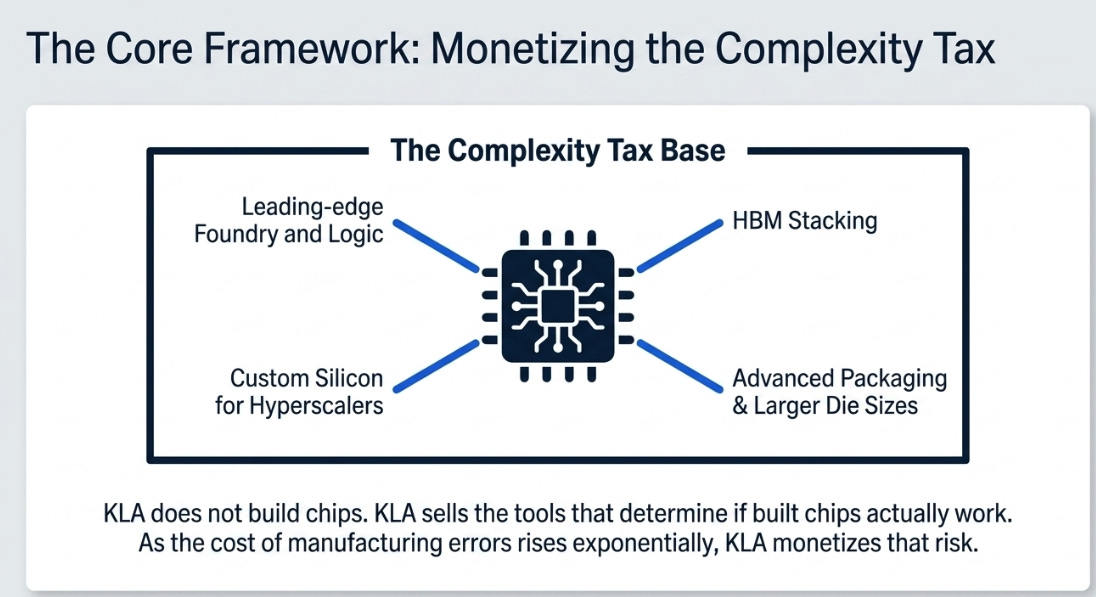

Two weeks ago, in A Perfect Business at an Imperfect Price, I argued that KLA is best understood not as a semiconductor equipment company but as a tax on semiconductor complexity. The company does not sell the tools that build chips. ASML, Applied Materials, and Lam Research do that. KLA sells the tools that determine whether the chips you built actually work. As chips become larger, more customized, more vertically stacked, and more packaging-intensive, the cost of not knowing what went wrong in the manufacturing process rises exponentially. KLA monetizes that rising cost.

That framing still holds. In fact, this quarter strengthened it. Management tied demand not to a generic “AI is good for semiconductors” narrative but to a specific, multi-dimensional complexity story: leading-edge foundry and logic, HBM stacking, custom silicon for hyperscalers, advanced packaging, larger die sizes, faster product cycles, rising design variability, and higher-value wafers. Each of these independently increases the amount of inspection and metrology a fab requires. Together, they represent a structural expansion of KLA’s tax base.

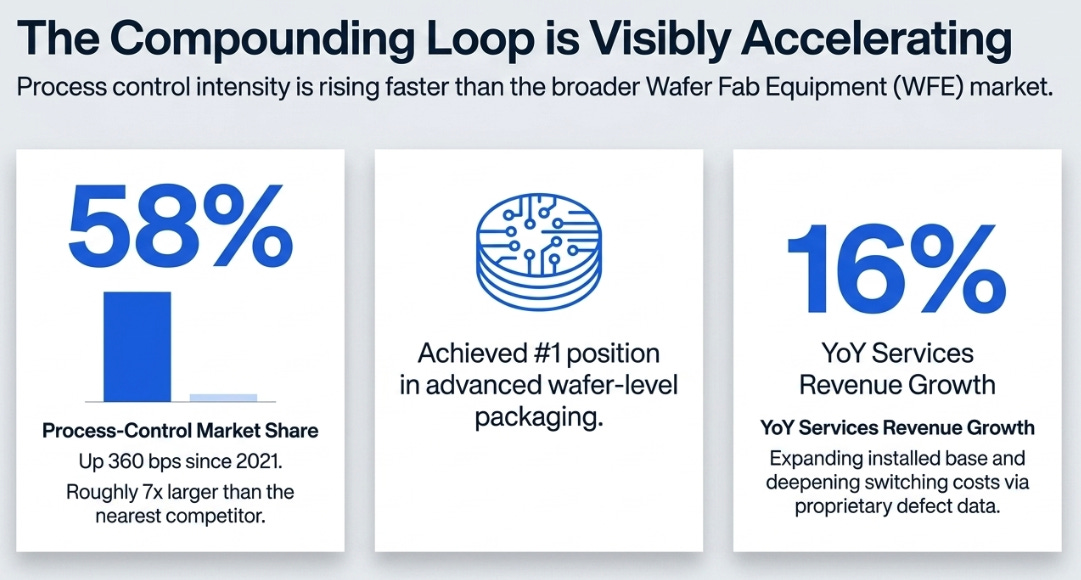

The compounding loop I described in the prior article is visibly at work. KLA reported 58% process-control market share, up 360 basis points since 2021 and roughly seven times larger than the nearest competitor. It achieved the number-one position in advanced wafer-level packaging. Services revenue grew 16% year-over-year. The installed base is expanding, the switching costs are deepening, and the proprietary defect data that trains KLA’s detection algorithms is accumulating across every advanced fab on earth.

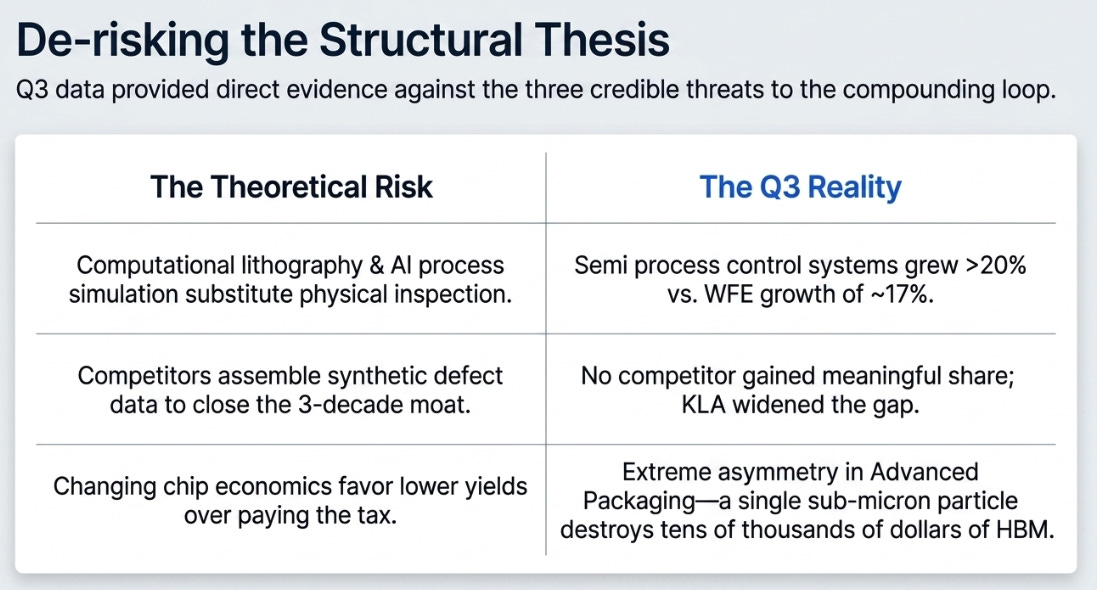

But the question this quarter needed to answer was not whether the loop exists. We established that in the prior article. The question was whether it is accelerating, stable, or at risk. Three things could slow it. First, computational lithography and AI-driven process simulation could begin substituting software for physical inspection, reducing the number of tools customers need per wafer. Second, a competitor could assemble enough defect data through synthetic generation or customer collaboration to close KLA’s three-decade data advantage. Third, chip economics could shift such that customers preferred accepting lower yields to paying the rising complexity tax, which would only happen if the devices being manufactured became less valuable, not more.

This quarter provided evidence against all three. Process control intensity rose, with the semiconductor process control systems business growing over 20% against a wafer equipment market growing roughly 17%. No competitor gained meaningful share; KLA widened the gap. And the economics moved further in KLA’s favor. Advanced packaging, where a single sub-micron particle trapped during hybrid bonding can destroy an entire HBM stack worth tens of thousands of dollars, is the most extreme expression yet of the asymmetry between what inspection costs and what its absence costs. The loop is not just intact. It is compounding into new domains faster than alternatives are emerging.

That is the structural answer. The stock, however, fell because the market already knew the business was exceptional. What it wanted to know was whether that exceptionalism would show up in near-term earnings and free cash flow fast enough to justify a price that had run to nearly $1,940 in the days before the print. On that question, the quarter was good but not sufficient.

That is the tension this update tries to resolve: the business improved more than the stock reflected. Understanding why requires looking at what we got right, what we missed, and what the quarter revealed about KLA’s position in the AI cycle that our prior framework did not fully capture.

Scoring Our Own Homework

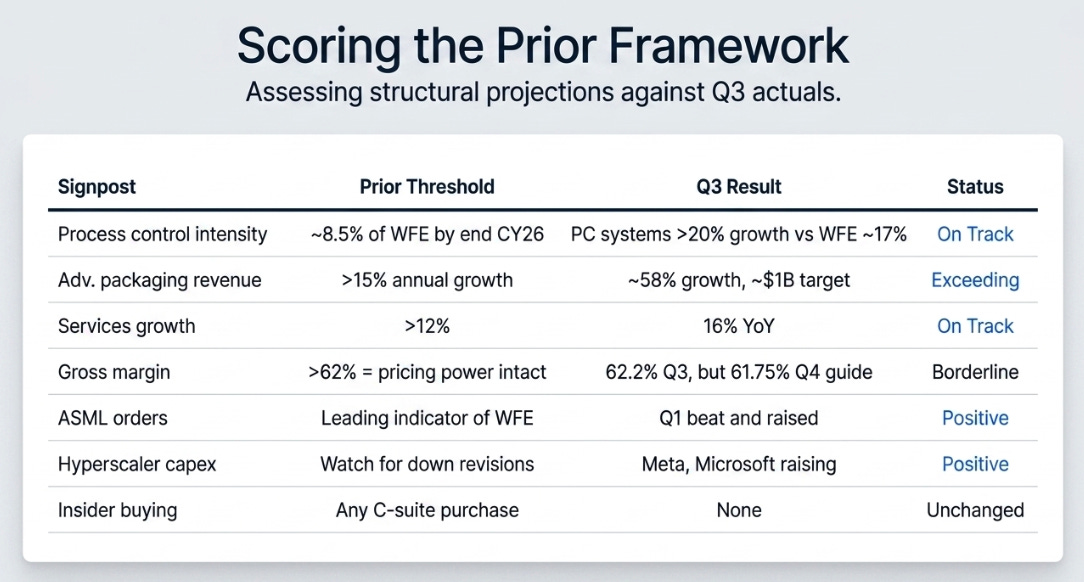

The prior article made several specific claims. Most held up. Three did not, and the three that did not are more interesting than the ones that did.

The central thesis was confirmed cleanly. The valuation warning played out precisely, the stock ran past $1,900 and sold off after a clean beat, exactly the “execution gets punished, only acceleration gets rewarded” dynamic we flagged. Services compounded within the target range. Advanced packaging exceeded even our estimates.

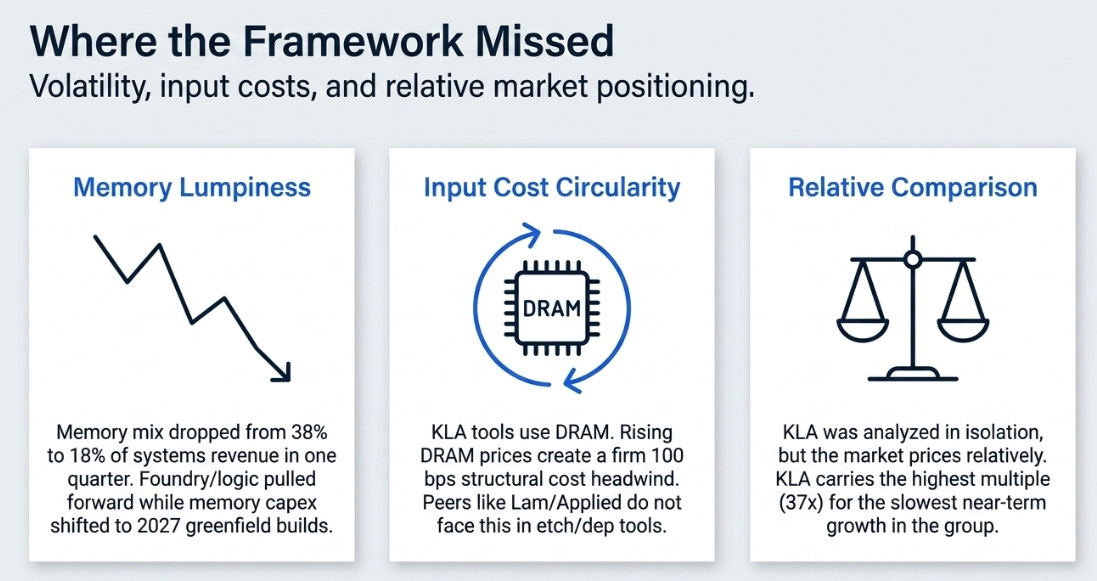

Where we were wrong matters more. First, the memory mix is far lumpier than our framework implied. We modeled HBM as a smooth, compounding tailwind. The yield math on 16-high stacks is correct structurally, but in the June quarter guidance, memory dropped from 38% to 18% of semiconductor process control systems revenue, a halving in one quarter. The explanation is that foundry and logic pulled forward while memory capex shifted to 2027 greenfield builds. Our steady-state model did not capture this volatility.

Second, we failed to name a structural vulnerability precisely enough. KLA’s inspection tools contain image-processing computers built with DRAM chips. When DRAM prices rise, which is broadly positive for the semiconductor industry, KLA’s own input costs rise with them. Management confirmed the headwind worsened from 75-100 basis points to a firm 100 basis points. No peer faces this circular cost exposure. Lam and Applied Materials do not have DRAM chips inside their etch and deposition tools.

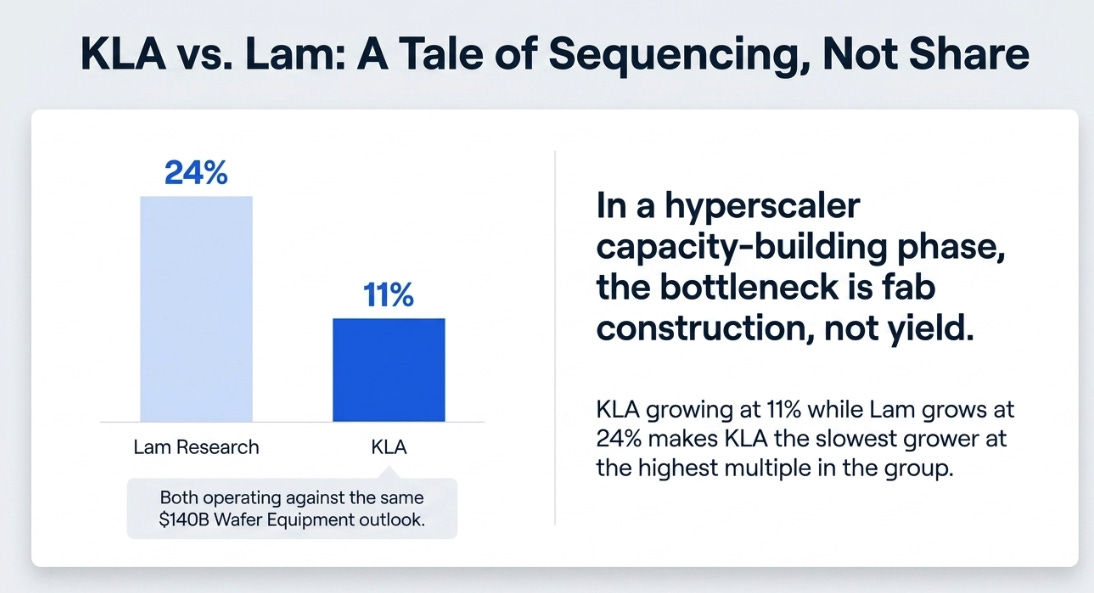

Third, and most importantly, we analyzed KLA in isolation when the market prices it in comparison. In a quarter where Lam Research grew revenue 24% on the same $140 billion wafer equipment outlook, KLA growing 11% makes it the slowest grower at the highest multiple in the semiconductor equipment group. That relative gap is the single biggest reason the stock sold off, and our prior article did not frame it.

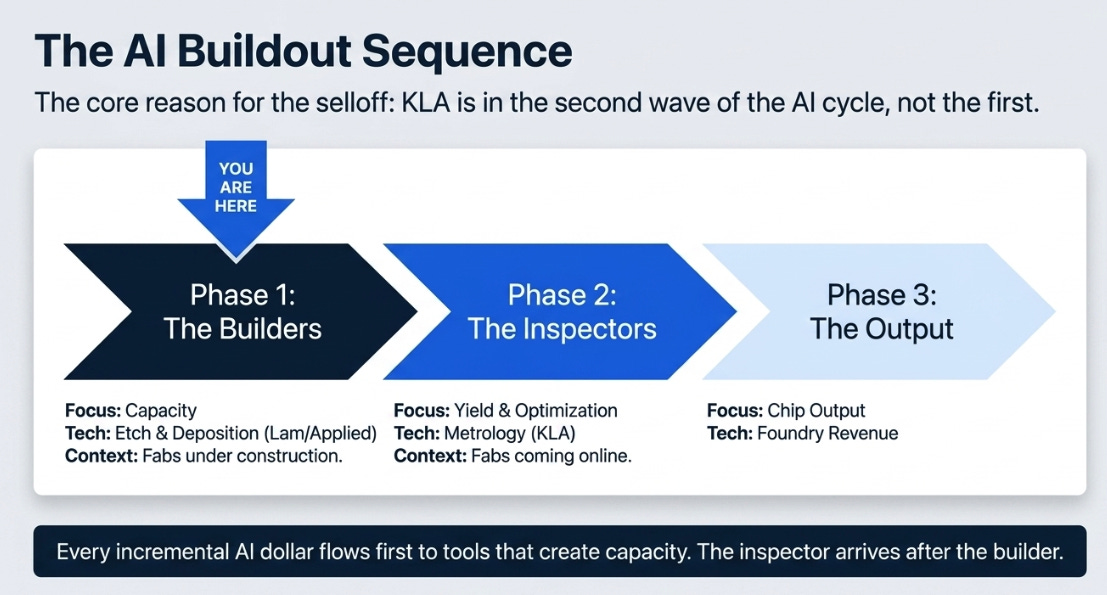

The Inspector Arrives After the Builder

This is the insight the prior article lacked, and I think it explains most of the stock’s behavior.

When a semiconductor fab gets built, there is a sequence. You install deposition chambers and etch tools first, because without them there is nothing to inspect. The tools that create capacity ship before the tools that optimize it. KLA is present throughout the manufacturing lifecycle, R&D, ramp, and high-volume production, so it is too simple to say it only matters later. But its relative growth advantage becomes most visible when the industry’s bottleneck shifts from building fabs to making those fabs yield.

The AI infrastructure buildout is in the building phase. Hyperscalers are committing historic capital, Meta raised its 2026 capex outlook to $125-145 billion. Dozens of fabs are under construction. Every incremental dollar flows first to the tools that create capacity. That is Lam territory. That is why Lam grows 24% while KLA grows 11%. It is not a share story. It is a sequencing story.

The analogy I keep returning to is cloud computing. The hardware vendors, Dell, Arista, benefited first. Then the platforms, AWS, Azure. Then the application layer, SaaS. Each wave created enormous value. The timing was staggered. AI semiconductors are following the same pattern: etch and deposition first, then inspection and metrology, then chip output and foundry revenue. KLA is in the second wave, not the first.

Management sees the second wave approaching. Rick Wallace described customer urgency around securing capacity as unlike anything in his career. Bren Higgins broke company protocol to say 2027 wafer equipment growth would exceed 2026. The backlog is building for fabs that do not yet exist. When those fabs come online and yield becomes the constraint, every deposition tool and etch chamber already installed will need KLA systems to become economically productive.

The tax collector does not arrive first. The tax collector always arrives.

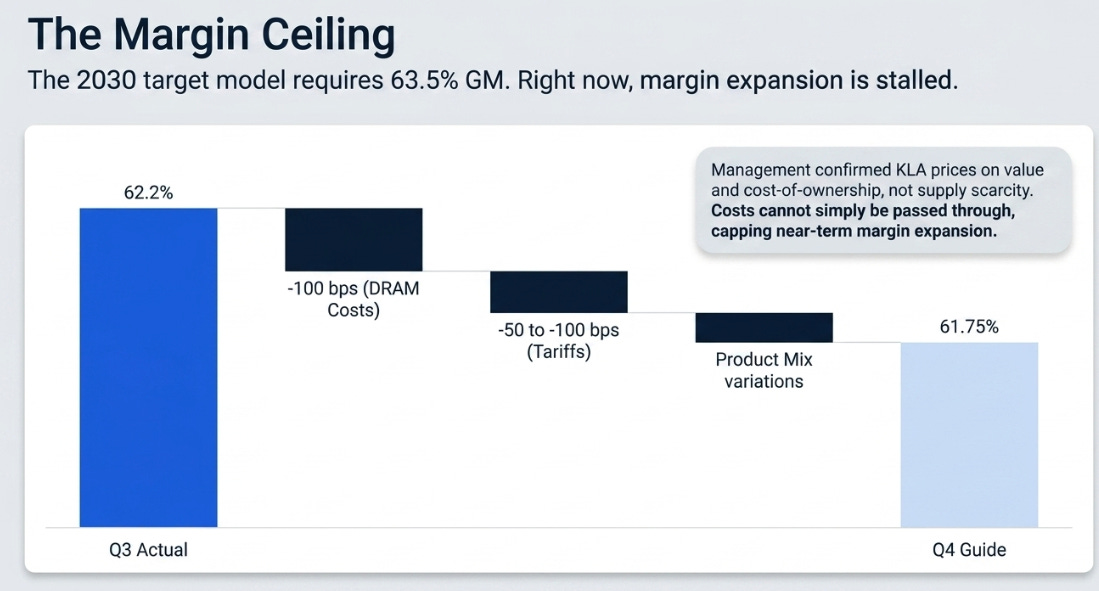

The Margin That Won’t Move

If the sequencing thesis is the reason for patience, gross margin is the reason for caution.

KLA delivered 62.2% non-GAAP gross margin in the March quarter, 45 basis points above the guided midpoint. But the June quarter guides to 61.75%, a sequential decline despite higher revenue. Three headwinds are stacking: DRAM component costs at 100 basis points, tariffs at 50-100 basis points, and product mix. Management was asked directly whether KLA could pass costs through given the strong demand environment and said no, the company prices on value and cost-of-ownership improvement, not on supply scarcity. That protects the franchise. It also caps near-term margin expansion.

The 2030 target model requires gross margins expanding from roughly 62% to 63.5%. Every year of delay costs approximately a dollar of earnings per share relative to the path. This is the swing variable between the base case and the bull case. Right now, it is not swinging.

What the Market Sees vs. What’s Actually Happening

Consensus sees KLA as a best-in-class semiconductor equipment compounder levered to AI. Correct, but incomplete.

What consensus misses is that KLA is a lagged AI beneficiary whose growth inflection arrives after etch and deposition peers, not alongside them. The market is pricing KLA at 37 times forward earnings, the highest multiple in the group, while it delivers the lowest growth rate. That combination only holds if the growth gap narrows, which requires the second phase of the buildout cycle to arrive in reported numbers. That is a late-2027 to 2028 event.

What consensus is right to question is whether duration alone justifies the premium. KLA can be strategically essential and still not be the best stock to own in the earliest phase of a capacity buildout.

Our view is that the structural thesis, complexity compounds KLA’s value, is stronger after this quarter than before it. The compounding loop is widening into advanced packaging, deepening through services, and facing no credible competitive challenge. But the stock needs four to six quarters for the growth inflection to show up in the income statement. At current prices, you are paying full freight for that future.

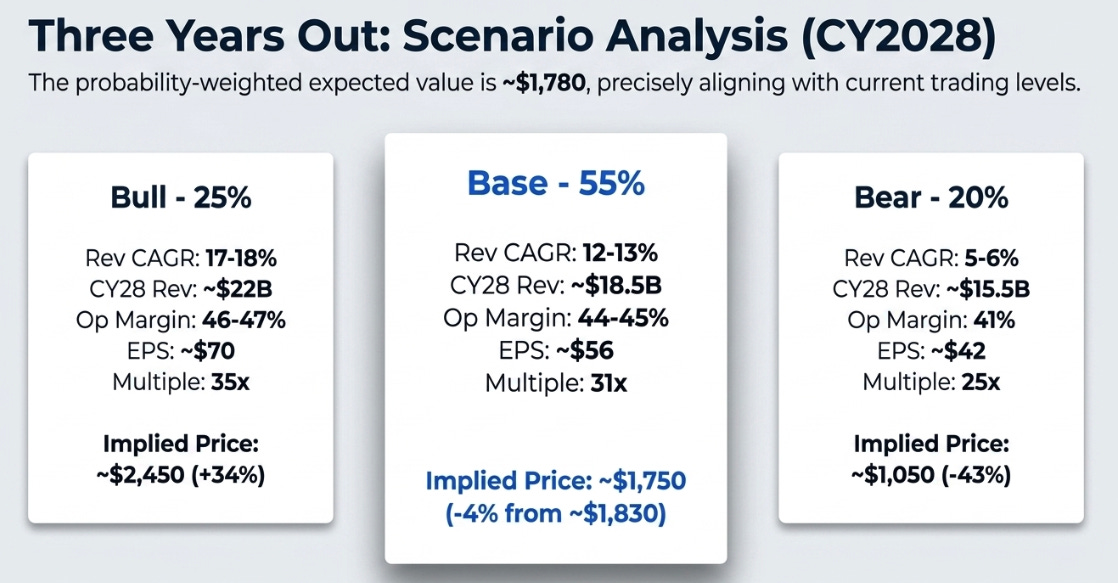

Three Years From Here

The probability-weighted expected value is approximately $1,780. That is roughly where the stock trades. The market is pricing KLA correctly for the base case. You make money only if the bull case is more likely than the 25% the market implies.

What changed from the prior article: the probability-weighted value moved from roughly $1,600 to $1,780, reflecting the improvement in forward visibility and the advanced packaging acceleration. But the stock moved too. The conclusion has not changed. KLA is fairly priced for the base case and not cheap enough to compensate for the timing lag between the structural thesis and its financial expression.

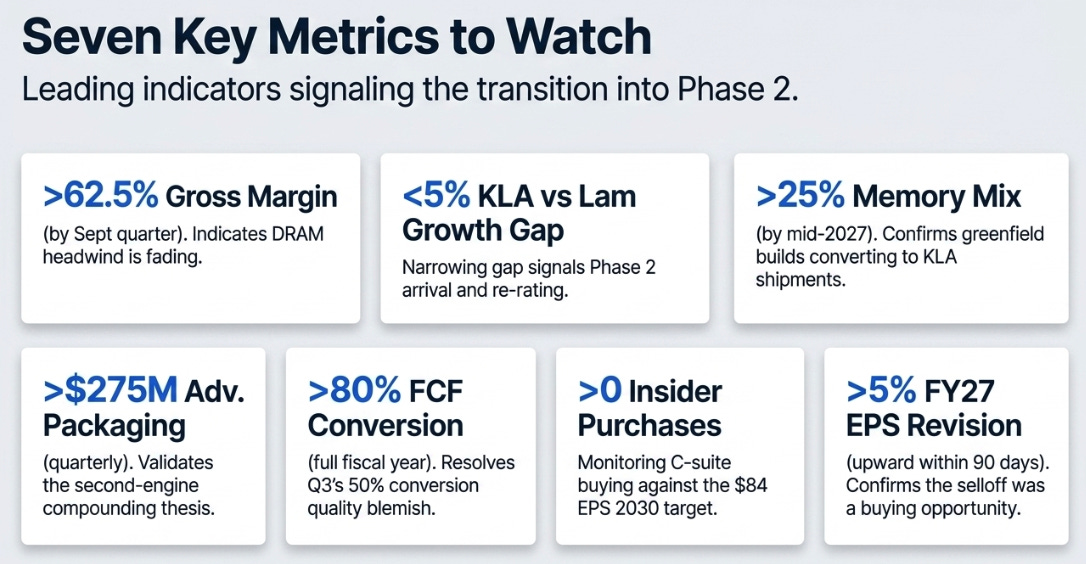

What to Watch

Seven numbers will tell us which scenario is unfolding.

Gross margin is the most important. Above 62.5% by the September quarter means the DRAM headwind is fading and the 2030 path is intact. Below 61.5% means the margin ceiling is real. KLA versus Lam relative revenue growth is the new addition, if the gap narrows below five percentage points, Phase 2 is arriving and KLA re-rates; if it widens above fifteen, the multiple compresses regardless of absolute results. Memory mix recovery above 25% by mid-2027 would confirm the greenfield builds are converting into KLA shipments. Advanced packaging must sustain above $275 million per quarter to validate the second-engine thesis. Free cash flow conversion needs to exceed 80% for the full fiscal year; Q3’s 50% conversion was the single biggest quality blemish, and a repeat would be a genuine concern. Insider purchases remain at zero from a management team guiding to $84 in earnings per share by 2030. And consensus FY2027 EPS revisions moving up more than 5% within ninety days of the print would confirm that the selloff was a buying opportunity.

The complexity tax is permanent. The compounding loop behind it is widening. The conversion question is the only one still open, and the numbers, one quarter at a time, will close it.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.