Lam Research 3QFY26: More Than a Cycle, More Than a Toll Booth

Lam is no longer just benefiting from a strong equipment cycle, AI is increasing Lam’s content per wafer, accelerating NAND and memory complexity, and revealing a more durable 50%+ gross margin model.

TL;DR

AI is changing chip architecture in Lam’s favor. The quarter showed that AI demand is not just boosting compute, but also increasing the etch and deposition intensity needed for NAND, DRAM, and advanced packaging.

Margins look structural, not cyclical. With gross margin at 49.9% and guidance to 50.5%, Lam appears to be benefiting from a real operational flywheel, not just a temporary China mix tailwind.

The story is shifting from cycle to compounding. Higher content per wafer, faster installed-base monetization, and better customer mix make Lam look less like a traditional WFE trade and more like a structural winner in semiconductor complexity.

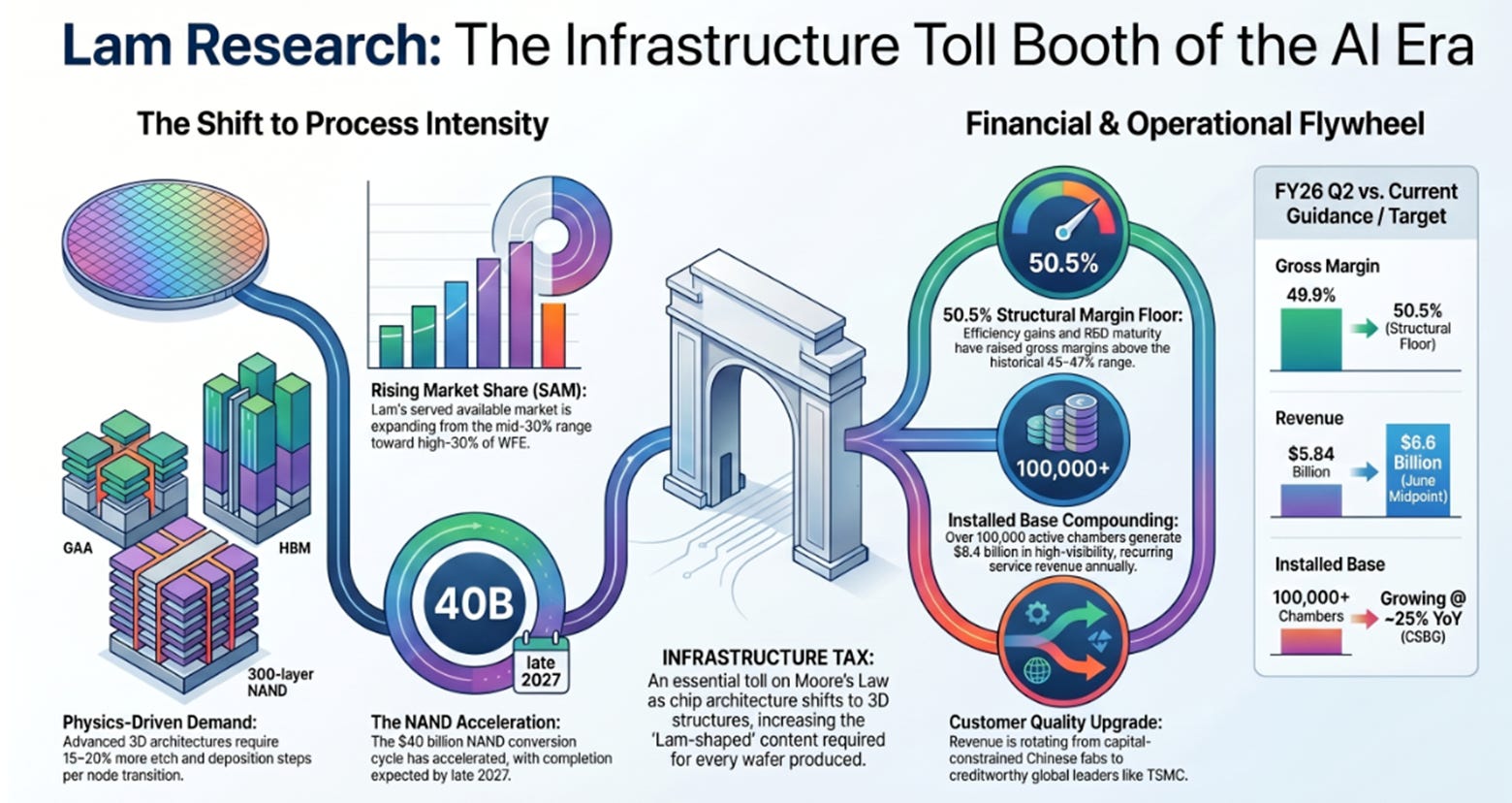

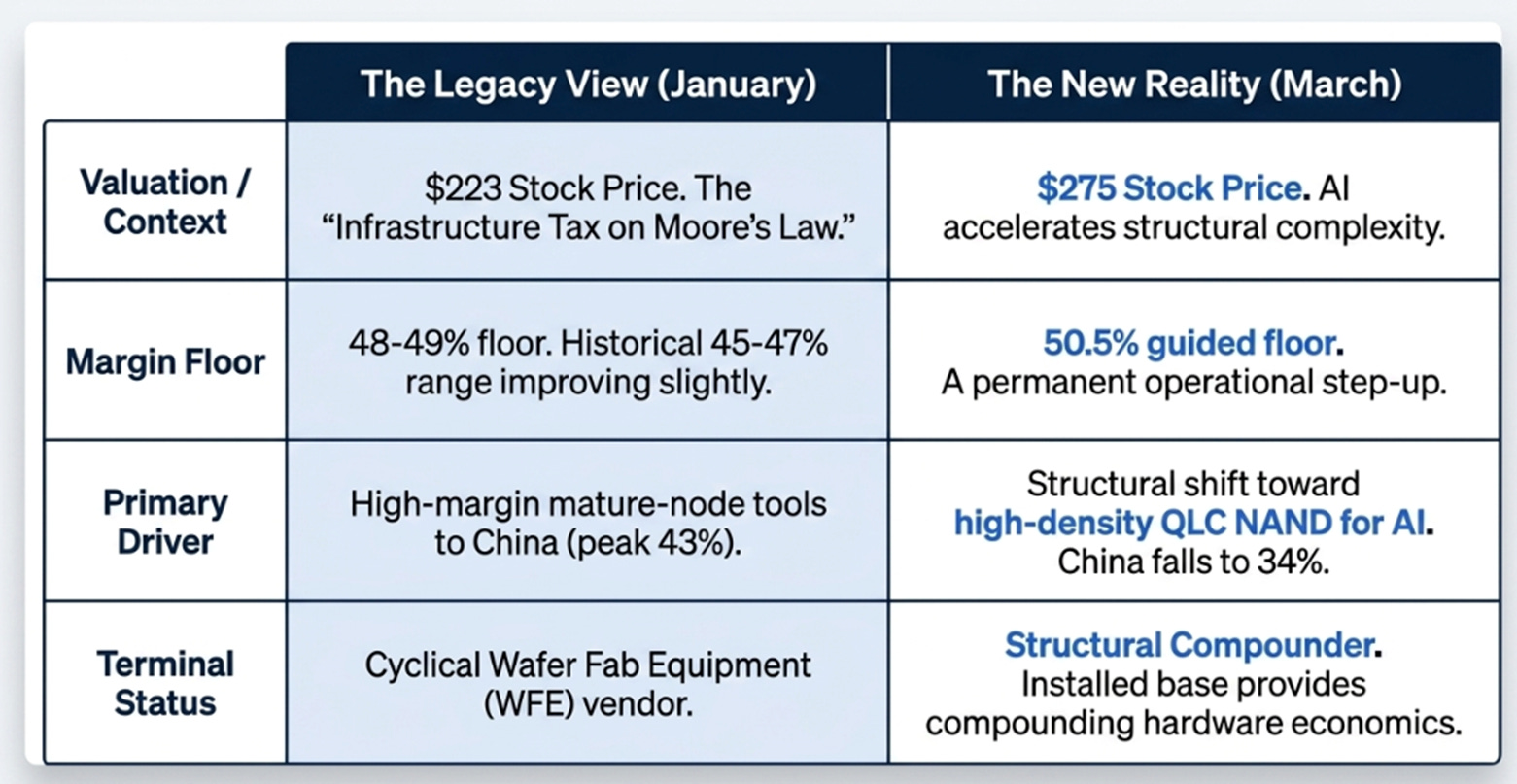

In January, at $223, the case for Lam Research was that the bottleneck in semiconductors had shifted. The important companies were no longer simply the ones that could draw smaller transistors but the ones that could physically build ever more vertical, fragile, and difficult structures at production scale. That was the logic behind calling Lam the “infrastructure tax on Moore’s Law”: advanced nodes, stacked memory, and 300-layer NAND all required more of the specific construction work Lam does best. The market, meanwhile, still mostly treated Lam as a cyclical equipment vendor.

That thesis was directionally right. But it now feels incomplete.

The March quarter did not merely show that semiconductor spending is strong. It suggested that AI is changing the shape of semiconductor manufacturing in a way that makes Lam more valuable per wafer, not merely more exposed to wafer-fab-equipment growth. That is a different claim. It is also, to my mind, the real significance of the quarter. Lam reported $5.84 billion of revenue, $1.47 of non-GAAP EPS, 49.9% gross margin, and guided June to $6.6 billion of revenue at the midpoint with 50.5% gross margin. Those are excellent numbers. More importantly, they are evidence.

The question, then, is not whether Lam beat. The question is: did this quarter prove that AI is making semiconductor manufacturing more Lam-shaped?

The architecture is shifting

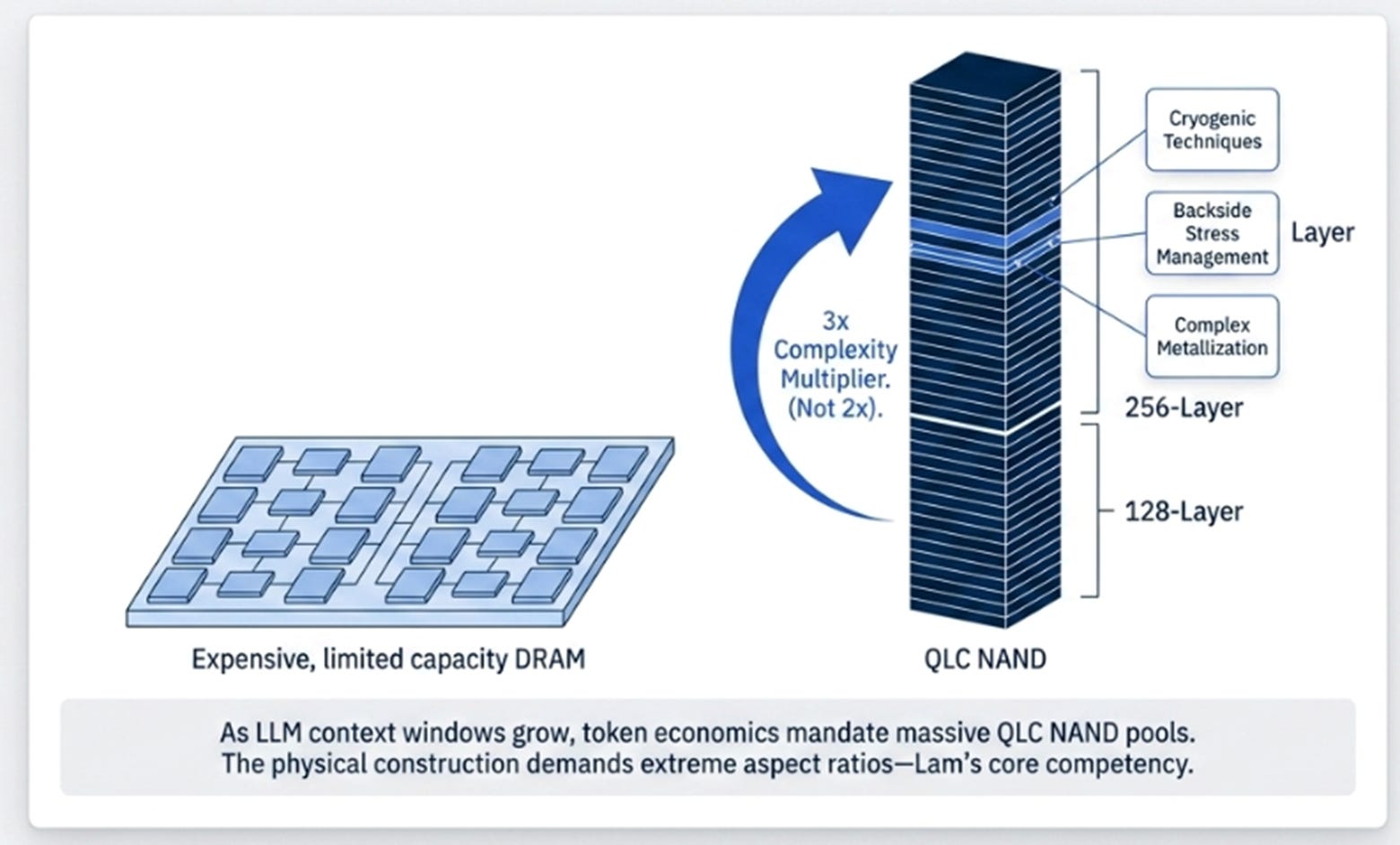

The easiest way to misunderstand the AI buildout is to think of it only as a compute story. That is where most attention goes: GPUs, networking, CoWoS, power, cooling. But what CEO Tim Archer argued on this call is that AI is also changing the memory and storage architecture of the data center, and he used a phrase that connects the software layer directly to Lam’s hardware: “token economics.”

As LLM context windows and vector databases grow, it becomes economically and physically impossible to rely solely on expensive DRAM. AI data centers are being forced to architect themselves around massive pools of high-density QLC NAND. Building this next-generation storage requires etching perfectly uniform holes through hundreds of layers of material, and doing so at aspect ratios extreme enough to demand cryogenic techniques, backside stress management films, and metallization steps that simpler devices never required. A 256-layer NAND chip is not twice as hard to build as a 128-layer chip. It is closer to three times as hard. That is Lam’s core competency, and the demand for it is accelerating.

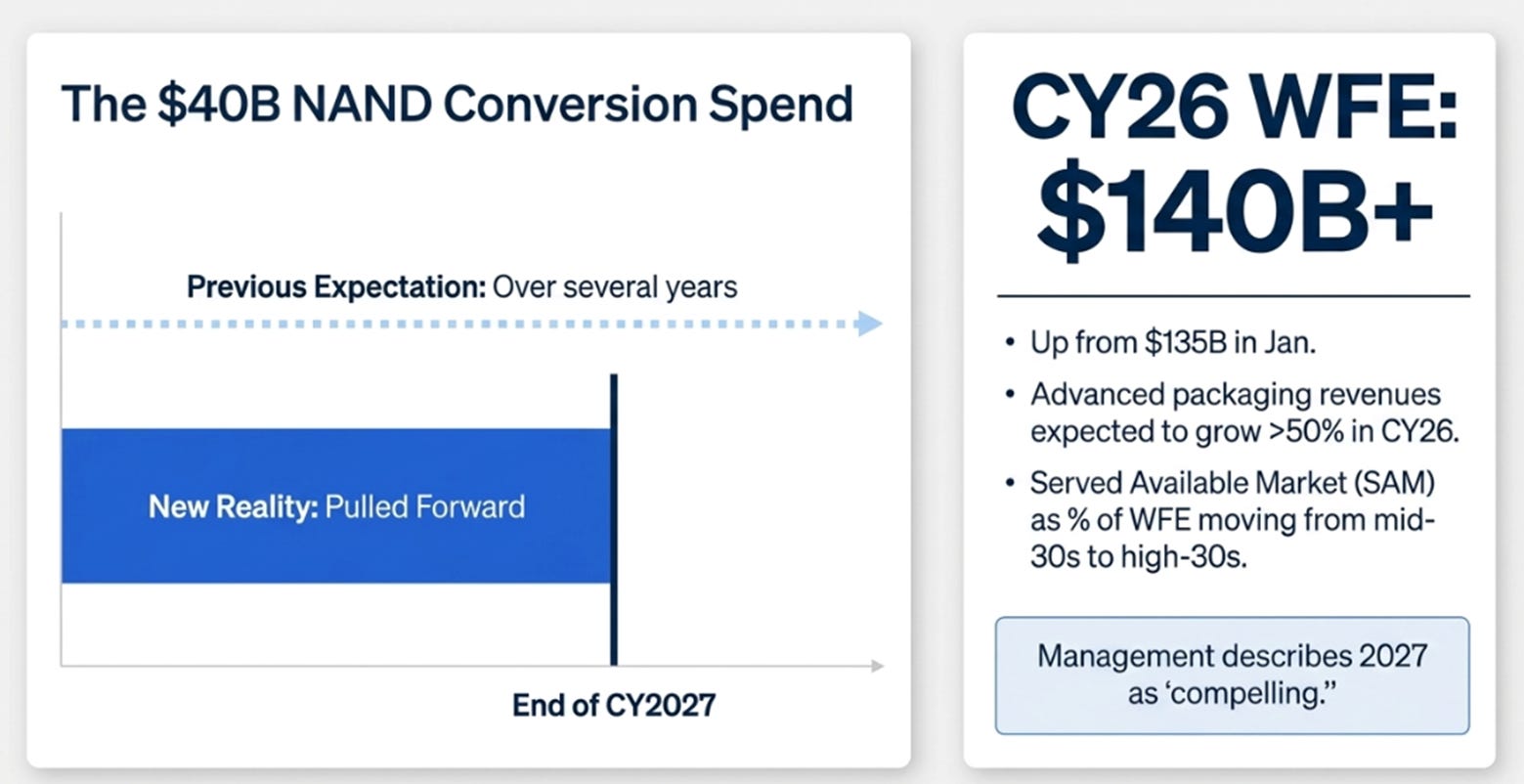

The $40 billion in NAND conversion spending that the January article identified as the “coiled spring” catalyst has been pulled forward. Management previously described this spending as occurring over several years. On the March call, Archer said the majority would complete before the end of calendar 2027. That is a meaningful acceleration, driven not by cyclical restocking but by the physical requirements of AI inference at scale.

The same dynamic is playing out across every segment simultaneously. In DRAM, the transition to 1c nodes is creating entirely new deposition applications, Lam’s Striker ALD solution is the tool of record at every major memory maker, and management estimates the dielectric deposition opportunity grows more than 20% at the 1c node. In foundry logic, Lam achieved its first dielectric etch wins at a key manufacturer, a share gain in a segment where it has historically been underweight. Advanced packaging revenues are expected to grow more than 50% in calendar 2026.

This is what management means when they say served available market as a percentage of WFE is moving from the mid-30s% toward the high-30s%. The industry is not just spending more. Each dollar of spending is becoming more etch- and deposition-intensive. The infrastructure tax rate on Moore’s Law is rising. And Lam now expects CY26 WFE of $140 billion with upside bias, up from $135 billion in January, with management describing 2027 as “compelling.”

The margin surprise and what it reveals

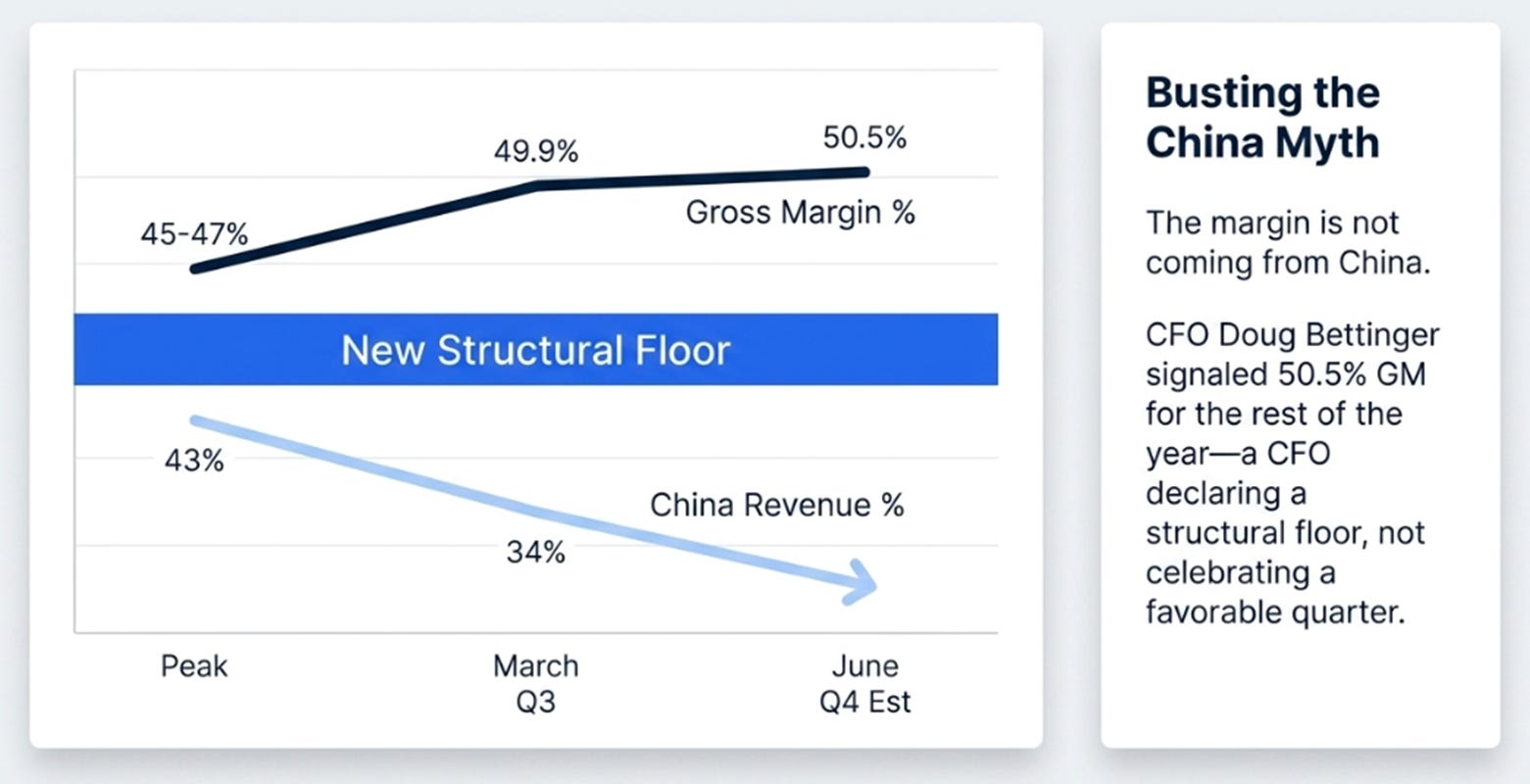

The January article made a specific claim about margins: as China revenue declined from its 43% peak, gross margins would normalize to a structural 48-49% floor, higher than Lam’s historical 45-47% range, reflecting genuine operational improvements, but below the 50%+ levels that included an outsized China premium. The logic was that China’s mature-node tools carried higher margins because customers had fewer alternatives, and as that revenue was replaced by advanced-node sales to concentrated, powerful buyers like TSMC and Samsung, pricing pressure would compress margins.

The logic was right. The number was wrong. Margins didn’t settle at 48-49%. They printed 49.9% in March, with China at 34%, and management guided 50.5% for June with China expected to decline further. The margin is not coming from China. It is coming from somewhere else.

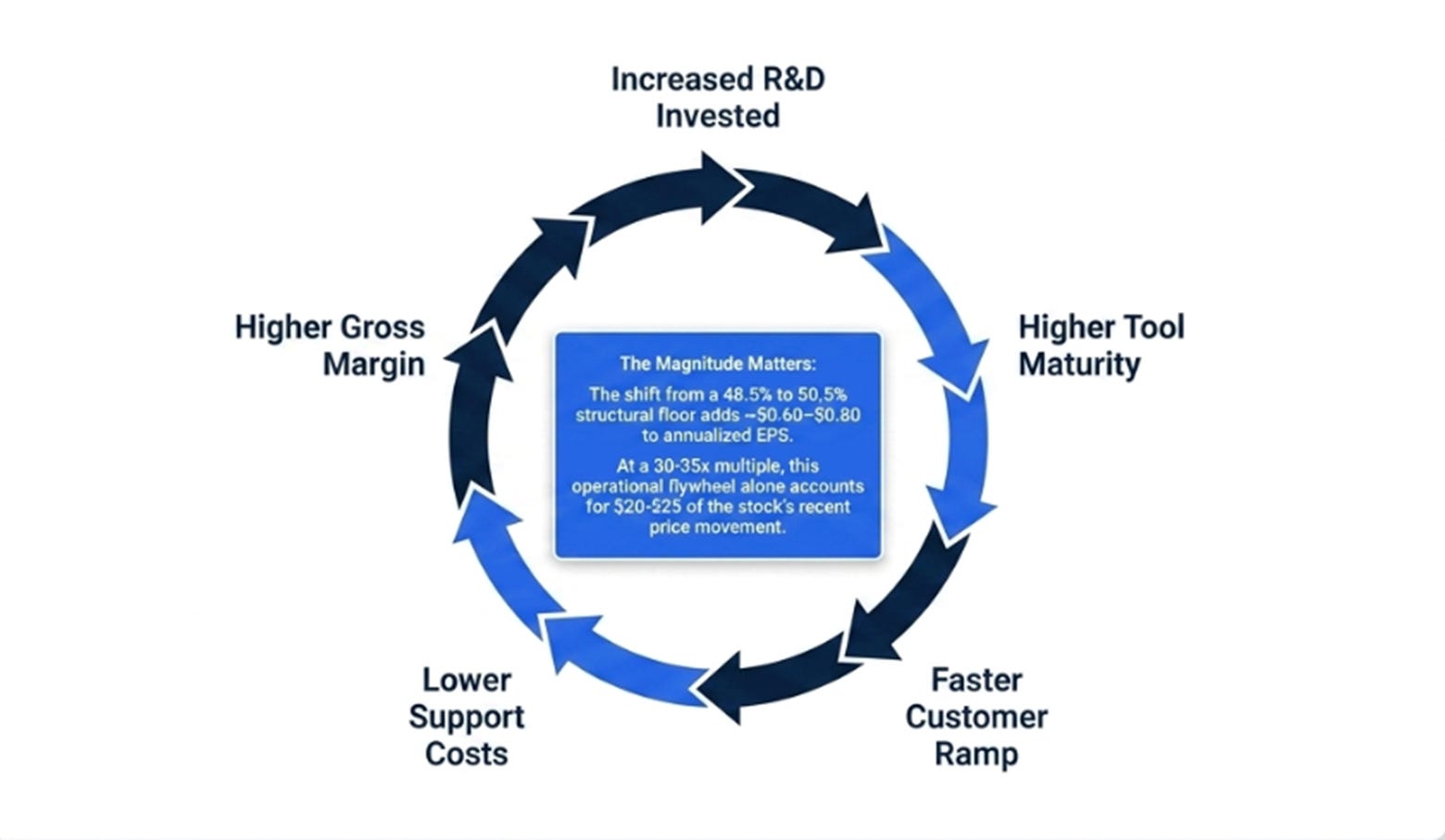

CFO Doug Bettinger was unusually specific about where. He cited factory proximity from the Malaysia manufacturing expansion, shorter freight lanes, a better supply chain setup. Those were the improvements the January article anticipated, worth roughly 100 basis points of structural gain. But CEO Tim Archer added something we underestimated: Lam has been investing in R&D specifically to ensure that new tools enter the field with greater maturity than in the past. When a tool works correctly on first installation, two things happen. The customer ramps faster, which strengthens the commercial relationship. And Lam spends less on installation support and warranty service, which flows directly to gross margin.

This is a flywheel that the January article did not describe. R&D produces more mature tools. More mature tools reduce field service costs. Lower costs improve margins. Better margins fund more R&D. Each turn makes the next turn cheaper. And because the installed base grows with every tool shipped, now over 100,000 chambers, the efficiency gains compound on a larger revenue base each quarter.

The magnitude matters. The difference between the 48-49% floor I modeled in January and the 50.5% that management is now guiding adds approximately $0.60-0.80 to annualized EPS. At a 30-35x forward multiple, that margin mechanism alone accounts for roughly $20-25 of the stock’s move from $223 to $275. The toll booth doesn’t just collect more revenue per wafer because 3D scaling demands more process steps. It collects that revenue more efficiently because the operational flywheel compounds alongside the demand flywheel. That combination, rising toll rate and falling collection cost, is what makes Lam look more like a compounder than a cyclical beneficiary.

Bettinger told analysts to model roughly 50.5% gross margin for the rest of the year. That is not the language of a company celebrating a favorable quarter. It is a CFO declaring a new structural floor.

The installed base as compounding layer

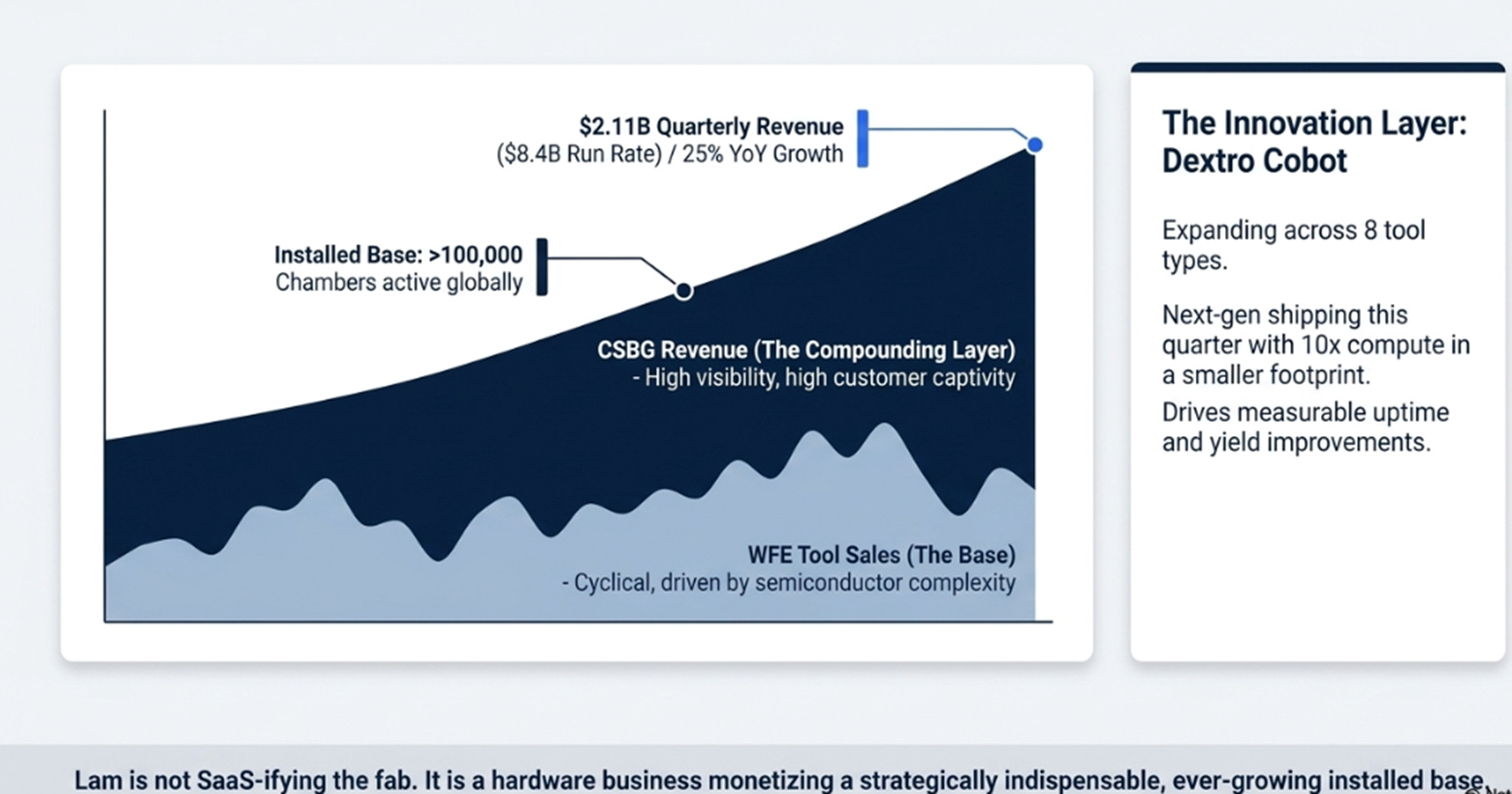

One temptation after this quarter is to overstate what Lam is becoming. The company reported its first $2.11 billion quarter for Customer Support Business Group revenue, driven by strong spares, upgrades, and services. Archer highlighted new Equipment Intelligence deployments and broader Dextro cobot coverage, now spanning 8 tool types, with a next-gen version shipping this quarter that packs 10x the compute into a smaller footprint. Customers using Dextro are seeing measurable improvements in uptime and, in some cases, yield.

It is tempting to jump from there to “Lam is becoming a platform company” or “Lam is SaaS-ifying the fab.” That goes too far. The installed base is not the thesis. It is the compounding layer.

The root mechanism is still the one described above: semiconductor complexity is increasing Lam’s content per wafer. That gets Lam the tool sale. But once the tool is installed, Lam gets a second, increasingly important way to participate: spares, upgrades, diagnostics, automation, and service attached to a base that only grows. CSBG at $2.1 billion quarterly annualizes to $8.4 billion, growing 25% year-over-year. That is not software economics. It depends on fab utilization, which is very high right now. But it has characteristics that pure cyclical revenue does not: high customer captivity, high visibility, and a new innovation layer that creates monetization opportunities that didn’t exist two years ago.

That distinction matters. It is the difference between a clever metaphor and an accurate one. Lam is not a platform. It is a hardware business whose economics improve because the hardware is becoming more strategically indispensable and more deeply monetized after installation.

The signal hiding in the down payments

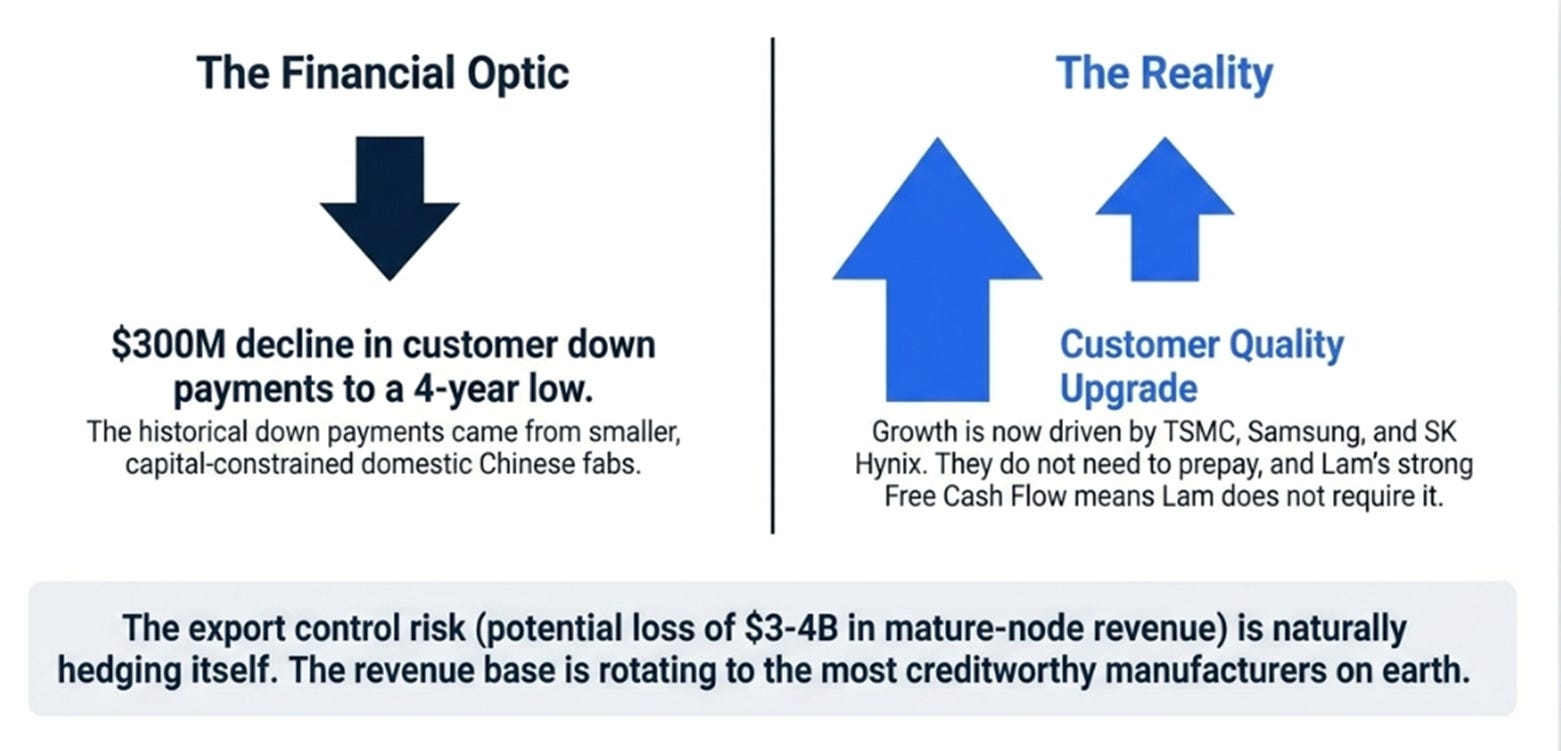

There is a data point in this quarter that I think is the single most strategically revealing moment of the call, and it appeared bearish on the surface. Customer down payments within the deferred revenue balance fell by roughly $300 million to their lowest level in four years.

Bettinger’s explanation was precise: the customers who historically provided down payments were smaller, often Chinese domestic fabs. The customers driving growth now, TSMC, Samsung, SK Hynix, don’t prepay because they don’t need to. And Lam doesn’t require it because it generates ample free cash flow to fund its own capacity expansion.

This is a customer quality upgrade disguised as a financial deterioration. Lam’s revenue base is rotating from smaller, capital-constrained buyers concentrated in a geopolitically risky geography toward the largest, most creditworthy semiconductor manufacturers on earth. The export control risk we identified in January, the potential loss of $3-4 billion in mature-node revenue, is being naturally hedged by the very demand acceleration that makes Lam valuable. The down payment decline is not a warning. It is evidence that the quality of the revenue stream is improving.

What the quarter did not prove

The old bear case, margin compression from China decline, is dead. But a new risk needs to be named, and this is the right time to name it because nobody is doing so while the numbers are this strong.

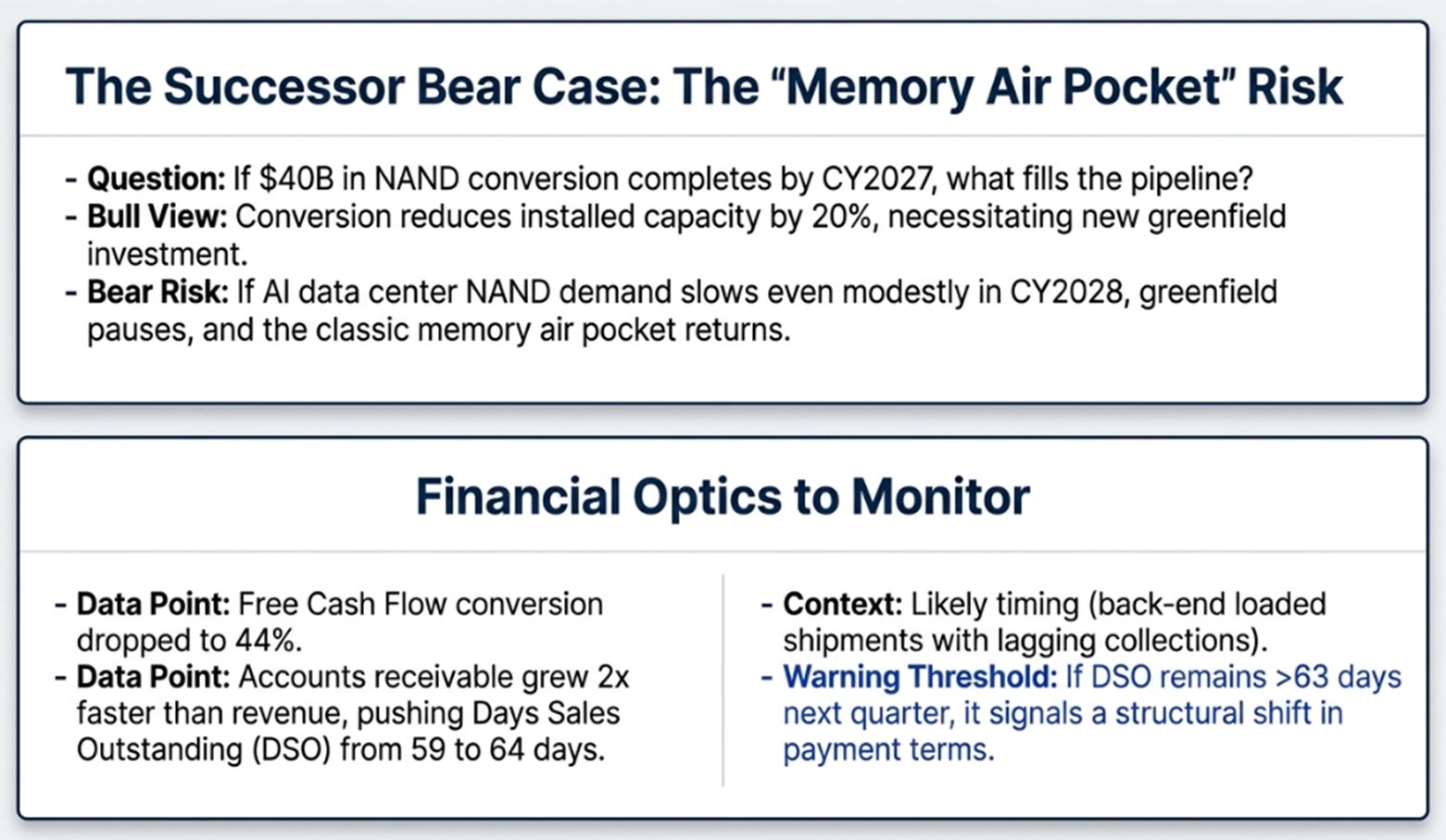

If the majority of $40 billion in NAND conversion spending completes by end of CY2027, what fills the NAND revenue stream afterward? Management’s answer is that the conversion itself reduces installed wafer capacity by more than 20%, necessitating greenfield investment. The logic is sound. But NAND has a long history of conversion cycles followed by investment pauses. If AI data center NAND demand growth slows even modestly in CY2028, the greenfield case weakens, and the classic memory air pocket returns.

This is the successor bear case to margin compression, and the seeds are being planted in the very acceleration that bulls are celebrating.

There is also a quality flag worth monitoring. Free cash flow conversion dropped to 44% this quarter as accounts receivable grew at twice the rate of revenue, pushing DSO from 59 to 64 days. This is likely timing, back-end-loaded shipments with collections lagging, but if DSO remains above 63 next quarter, it suggests something more structural about payment terms.

Variant perception

The market’s default framing still seems to be that Lam is a very good semiconductor equipment company enjoying a very good part of the cycle. That is not wrong. It is merely incomplete.

The thing I would most want to avoid saying is that Lam has become non-cyclical. It has not. The thing I would most want to say is that the market still mostly sees a great cycle, while the more interesting possibility is that semiconductor complexity is quietly making Lam structurally better: more process-intensity exposure, more installed-base monetization, more operational leverage from the maturity flywheel, and more evidence that its share of the most important parts of WFE is rising.

Three years from now

The right way to think about Lam’s three-year valuation is not as a price target but as a test of the mechanism.

The bull case is not “AI stays hot.” It is “AI keeps increasing Lam’s content per wafer, the NAND conversion bridges into greenfield, and the installed-base layer makes the gains stick.” The bear case is no longer about China or margin compression. It is about the possibility that intensity proves real but temporary, and that the NAND cycle ends without a successor catalyst.

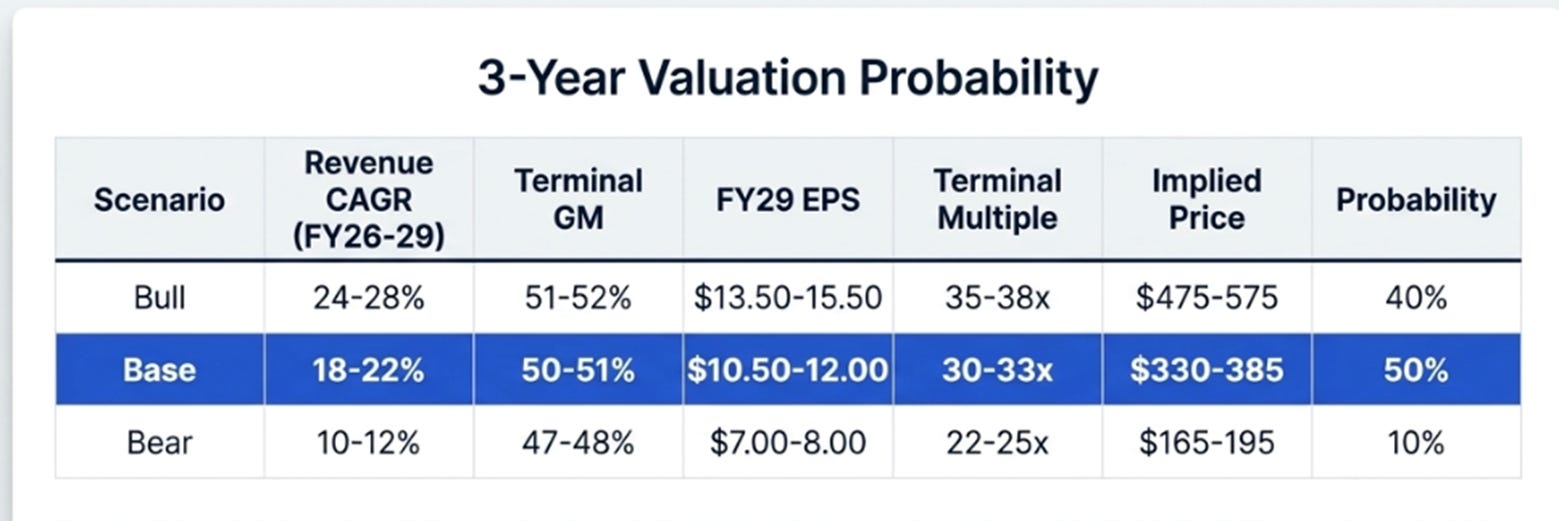

The most important change from January: the old supercycle scenario at $320-380 is now essentially the base case. Margins at 50%+ rather than 48-49% add roughly $1.50 to annual EPS at any revenue level, worth $45-50 of stock price at a 30x multiple. That single revision accounts for most of the upward shift in every scenario.

What to watch

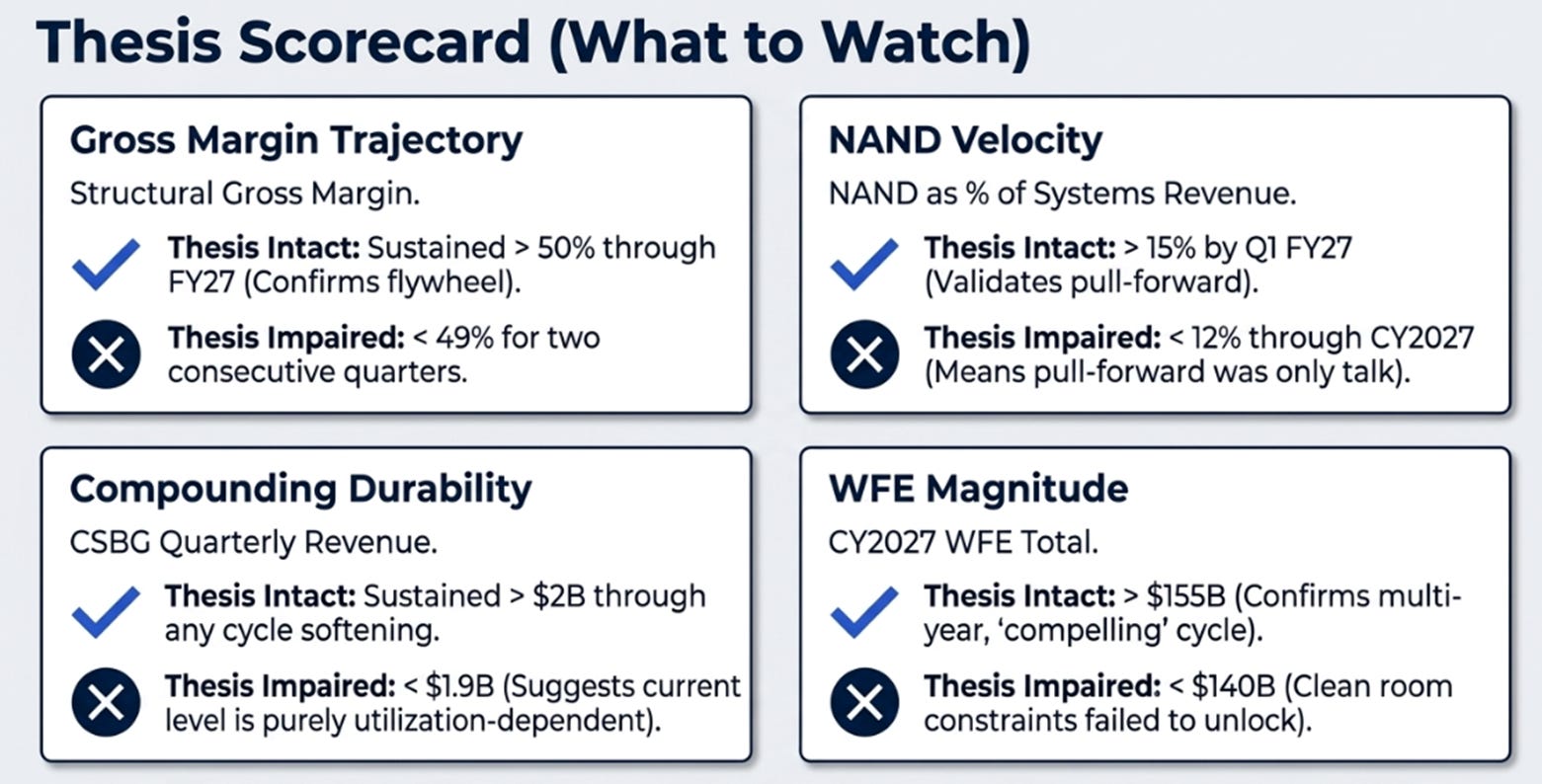

Gross margin trajectory. The thesis now rests on 50%+ as structural. Sustained above 50% through FY27 confirms the operational flywheel. Below 49% for two consecutive quarters impairs the thesis.

NAND as % of systems revenue. Above 15% by Q1 FY27 validates the conversion pull-forward. Below 12% through CY2027 means the pull-forward is talk, not shipments.

CSBG durability. Sustained above $2 billion quarterly through any softening proves the installed-base floor. A decline below $1.9 billion suggests the current level is utilization-dependent, not structural.

CY2027 WFE magnitude. Management called it “compelling.” Above $155 billion confirms the multi-year cycle. Below $140 billion means clean room constraints didn’t unlock as expected.

The January thesis was that Lam had become the infrastructure tax on Moore’s Law. The March quarter suggests the more precise version: AI is not simply driving more semiconductor spending; it is making semiconductor manufacturing more Lam-shaped. If that continues to be true, then Lam is not just a company in a good cycle. It is a company whose business gets better as the underlying technology gets harder.

At $275, you are paying for the base case. You are not paying for the compounding. The asymmetry is narrower than at $223, but the thesis is stronger because the evidence is deeper. The toll booth is real, the toll rate is rising, and the operator is getting more efficient with every wafer that passes through.

$LCRX

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.