Meituan 1Q26: The Bellhop’s New Lobby

Meituan is becoming a different company than the one the market is selling

TL;DR:

Q1 vindicated Meituan’s network, not its old margin structure. The subsidy war did not break the platform: users stayed, losses narrowed sharply, and Core Local Commerce began to repair. But the old monopoly-like economics are unlikely to return unchanged.

The war did not end; it moved. Food-delivery subsidies are being regulated down, but competitors are now attacking other layers of Meituan’s local-commerce stack: Alibaba in grocery supply, JD in fulfilment, Douyin in discovery, and AI agents at the consumer interface.

The investment question is no longer whether Meituan survives, but what it earns as the local-commerce operating system. If Meituan keeps control of intent, trust, supply and fulfilment, the stock looks mispriced. If those layers fragment, Meituan becomes infrastructure, still large, but worth much less.

In September, we wrote that Meituan was the digital bellhop.

The point was not food delivery. It was urban complexity. The old hotel bellhop was valuable because he knew which doctor made house calls, which restaurant stayed open late, which shortcut avoided the rain. Meituan’s version of that knowledge was reviews, merchants, riders, routes, membership, payments and habit. Our argument was simple: subsidies are temporary; the local operating system is permanent.

In March, after Q4, we updated the thesis. The moat had survived, but the old margin structure probably had not. Users stayed. Engagement held. The platform did not lose relevance. But the economics of running it had changed. The right question was no longer “when does the subsidy war end?” It was “what does the peace treaty look like?”

After Q1, the next update is clearer.

The peace treaty did not arrive. The war moved.

That is not a reversal of the thesis. It is the thesis becoming more precise. We have not changed our mind about what Meituan is. We have changed our mind about what it can earn, and where the next attack will come from.

Q1 vindicated the network thesis. It did not vindicate the old margin thesis.

What the Bellhop Bought

The most important thing Meituan did this quarter was not only in the income statement. It changed how it reports revenue.

Starting in Q1, Meituan separately disclosed “product sales.” This is gross-basis revenue, mainly from grocery retail businesses such as Xiaoxiang Supermarket and Kuailv. The number was RMB21 billion, or 23% of revenue, growing 46.6% year over year.

Meanwhile, delivery services revenue declined 2.9%. Merchant services, the higher-margin platform line, grew only 3.5%.

Companies do not reorganize disclosure for no reason. They do it when they want investors to see the business the way management sees it. What Meituan is saying is uncomfortable but important: the fastest-growing part of the company is not a pure platform line. It is retail, supply chain and inventory.

The market sees this and says: margin dilution.

That is correct, but incomplete.

Wang Xing made the strategic argument on the call. Consumers do not care whether supply is 1P or 3P. They care whether the product is available, good quality, fairly priced and reliably delivered. That is the argument for why an operating system sometimes needs hardware.

A platform can stay asset-light when supply is abundant, standardized and reliable. Fresh grocery is none of those things. Availability matters. Cold chain matters. Private label matters. Returns matter. Trust matters. If the platform’s promise is “everything now,” Meituan cannot rely only on someone else’s shelf.

That is why Xiaoxiang matters. That is why Dingdong matters. And that is why Alibaba’s reported bid for Pupu matters.

Grocery may lower reported gross margin, but it increases strategic control. It gives Meituan the pantry.

That trade is not automatically good. Grocery has humbled many confident technology companies. It is operationally heavy, low-margin and unforgiving. But calling it accidental dilution misses the point. Meituan is accepting lower accounting purity in exchange for more control of the daily-consumption layer.

The question is whether that control compounds or merely consumes cash.

Kiosks in the Lobby

While Meituan was remaking itself from the inside, competitors were attacking from the outside, but not exactly where our original framework expected.

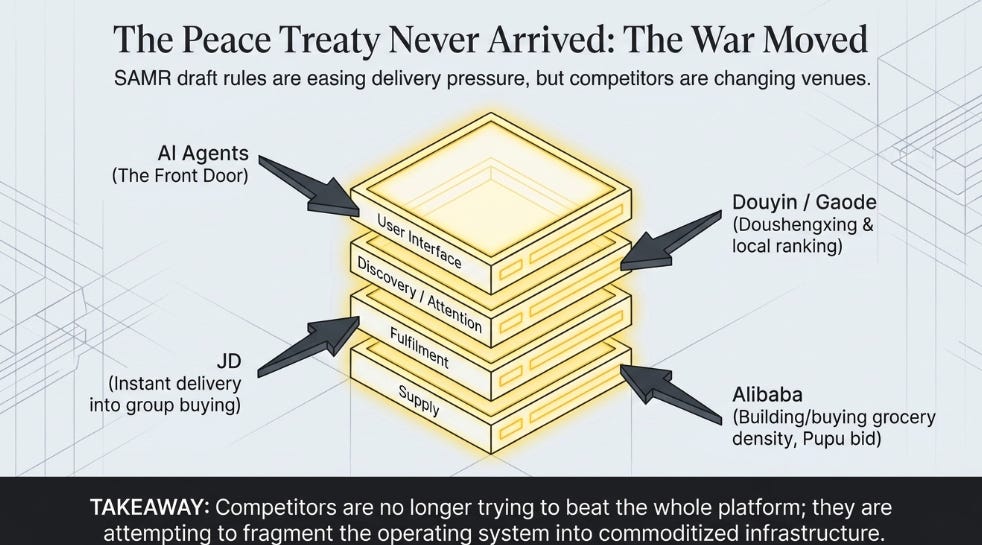

The food-delivery subsidy war appears to be moving toward regulation. SAMR’s draft rules target practices such as forcing merchants into subsidies, selling below cost, and using financial strength for unfair competition. That matters because it gives all players political cover to step back from economically destructive behavior.

This is good for Meituan. It makes Q1’s sequential repair more credible.

But competitors are not leaving local commerce. They are changing the venue.

Alibaba is trying to build or buy grocery density. JD is extending instant delivery into group buying. Taobao Flash Sale is piloting local group buying. Gaode is pushing local ranking. Douyin has Doushengxing, a dedicated group-buying app that reportedly reached meaningful daily usage and a high coupon verification rate within months.

This challenges one part of our September framework.

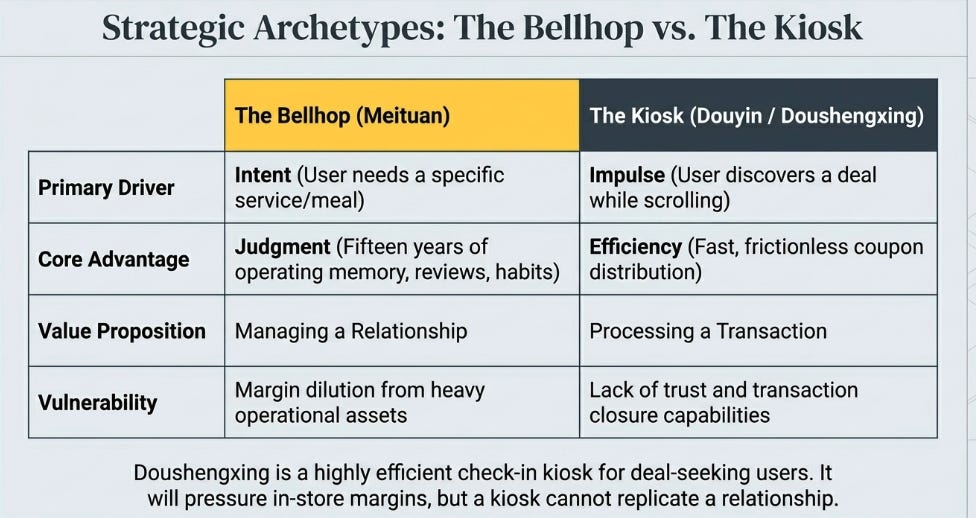

We distinguished between intent and impulse. Meituan was intent: users opened the app because they needed lunch, groceries or a service. Douyin was impulse: users discovered a deal while scrolling. Intent had better economics because demand already existed.

Doushengxing is ByteDance trying to build an intent product. No videos, no livestreams, no entertainment. Just local deals.

That is not trivial. It is the right attack.

But it still helps to return to the bellhop.

A hotel kiosk can solve one problem extremely well: check-in. It is fast, available and efficient. For the guest who knows exactly what he wants, the kiosk may beat the bellhop.

But the guest who arrives in an unfamiliar city, has dietary restrictions, wants to avoid tourist traps, needs a reliable dentist, or has a delayed flight still wants the bellhop.

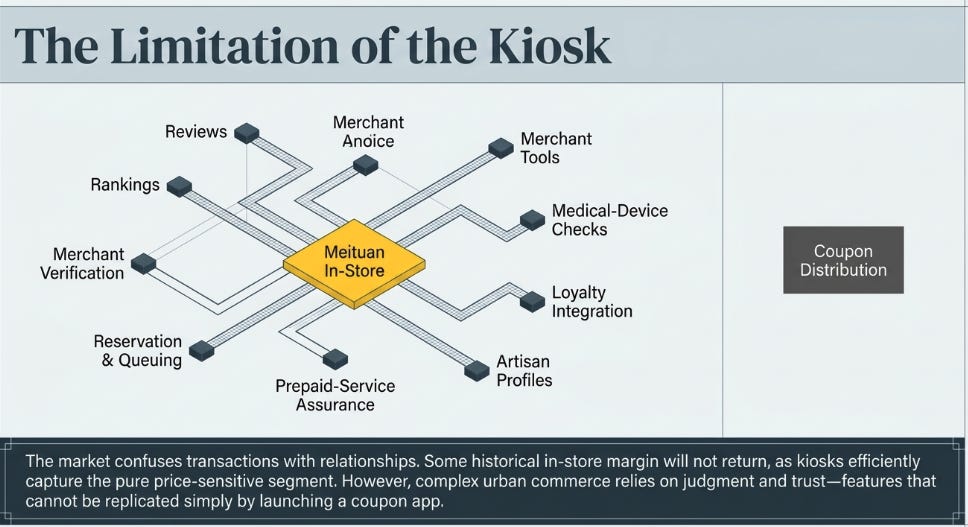

Doushengxing is a kiosk. It can distribute coupons efficiently to deal-seeking users. That will pressure Meituan in the price-sensitive in-store segment. Some of Meituan’s historical in-store margin was earned because there was no serious alternative. That margin will not fully return.

But Meituan’s in-store business is more than a coupon book. It is reviews, rankings, merchant verification, reservation, queuing, prepaid-service assurance, medical-device checks, artisan profiles, loyalty integration and merchant tools. Those are not features you replicate by launching a coupon app.

The question is not whether kiosks work. They do.

The question is how much of local commerce is check-in, and how much is judgment.

If Douyin owns discovery, Meituan becomes infrastructure. If Meituan keeps trust, reviews and transaction closure, Douyin becomes another demand channel. That distinction will decide the margin pool.

What Q1 Actually Confirmed

The numbers matter because they tell us whether the operating inflection is real or aspirational.

It is real, but not complete.

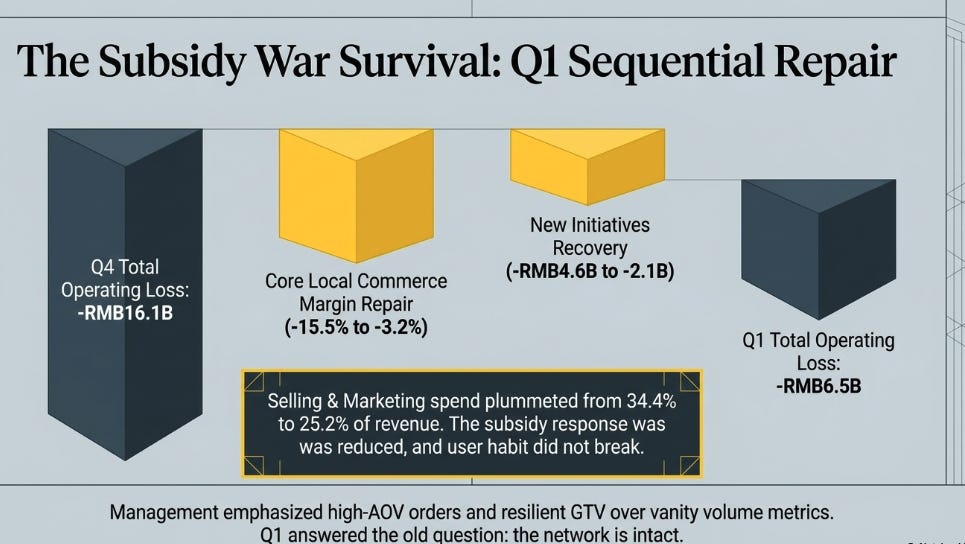

Revenue rose 5.6% year over year to RMB91 billion. That is not impressive by itself. The company still lost RMB6.8 billion, compared with a RMB10.1 billion profit a year ago. Core Local Commerce, the segment that matters most, moved from RMB13.5 billion profit last year to RMB2.0 billion loss.

That is the damage.

But sequentially, the repair was significant. Total operating loss narrowed from RMB16.1 billion in Q4 to RMB6.5 billion in Q1. Selling and marketing fell from 34.4% of revenue to 25.2%. Core Local Commerce operating margin improved from negative 15.5% to negative 3.2%. New Initiatives loss narrowed from RMB4.6 billion to RMB2.1 billion.

This is why Q1 matters. Meituan reduced the intensity of the subsidy response and the system did not collapse.

Management’s language was also revealing. It was not chasing all volume. It emphasized high-AOV orders, core users, better user structure, resilient GTV, and supply quality. It even warned that order volume growth may turn negative year over year in the second half because the company is prioritizing healthier mix.

That is not a company trying to win a vanity metric. It is a company trying to repair unit economics without breaking habit.

So the quarter answered the old question: can Meituan survive the subsidy war?

Yes.

But the post-Q1 developments ask a better question: can it still control the local-commerce loop when competitors attack each layer separately?

The Operating System Test

The market sees a battered delivery company recovering from a bad year.

I think that framing is too narrow.

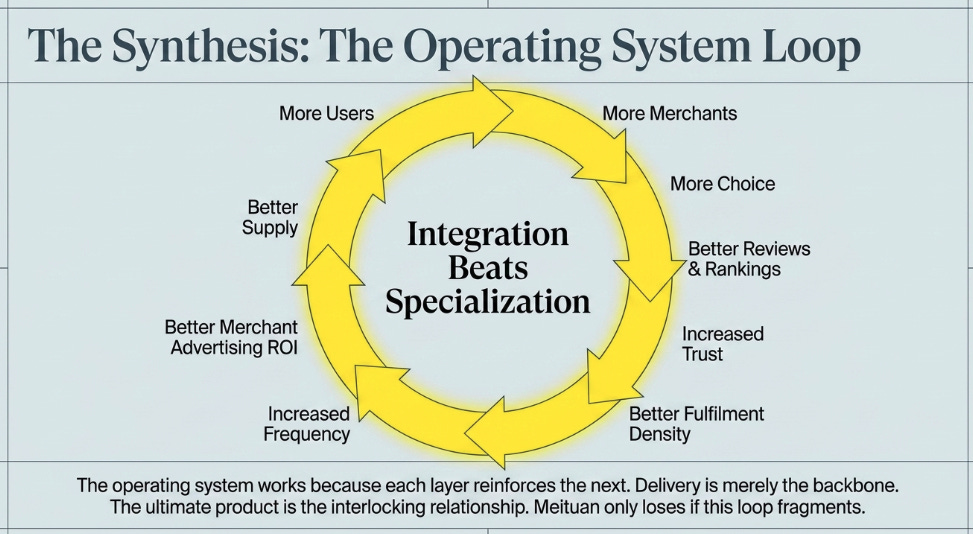

Meituan is a local-commerce operating system. Delivery is the backbone, but it is not the whole product. The product is the relationship: the user who starts with Meituan, the merchant who depends on Meituan, the rider who fulfils the order, the review that reduces uncertainty, the membership that increases habit, the grocery supply that guarantees availability, and the AI assistant that may become the new interface.

The operating system works because each layer reinforces the next.

More users bring more merchants. More merchants create more choice. More choice creates better reviews and rankings. Better reviews increase trust. More transactions improve fulfilment density. Better fulfilment increases frequency. More frequency improves merchant advertising ROI. Better merchant ROI improves supply. Better supply brings more users.

That is the loop.

Competitors are not trying to beat the whole loop at once. They are attacking pieces of it.

Alibaba attacks supply and commerce. JD attacks fulfilment credibility. Douyin attacks attention and discovery. Gaode attacks local search. AI agents may attack the front door.

Meituan wins if integration beats specialization.

It loses if the loop fragments.

Variant Perception

Consensus sees a repair story: food-delivery subsidies fade, losses narrow, margins recover.

The correct framing is a reclassification story. Meituan is becoming a lower-margin but more deeply embedded local-commerce infrastructure company. The old margin percentage may not come back. But lower margins on a larger, more controlled base can still create attractive absolute earnings power.

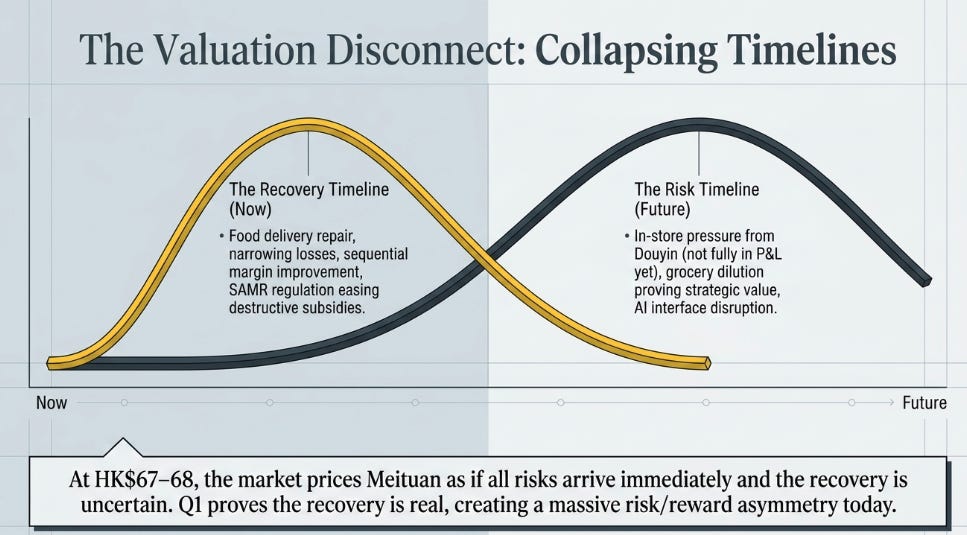

The market is also collapsing two timelines into one.

Food delivery repair is happening now. In-store pressure is emerging but has not yet fully appeared in the P&L. Grocery dilution is visible, but its strategic value will take longer to prove. AI is noisy today, but the interface question may matter later.

At today’s price, the market is pricing Meituan as if all the bad timelines arrive together and the good timeline is uncertain.

Q1 suggests the recovery timeline is real. The competitive developments suggest the risk timeline is also real.

That is why the stock is interesting, not easy.

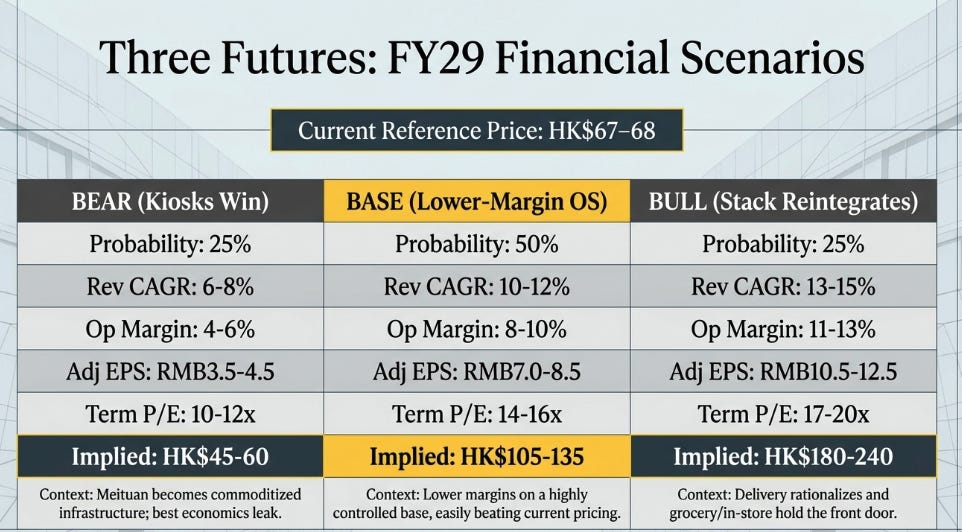

Three Futures

Using roughly HK$67–68 as the reference price, I would frame the next three years this way:

The bear case is not that Meituan disappears. It is that the best economics leak. Douyin captures more in-store discovery. Alibaba and JD make instant retail more competitive. Grocery becomes necessary but low-return. Meituan remains large, but more like infrastructure than operating system.

The base case is that food delivery rationalizes, Core Local Commerce returns to profitability, and in-store margins settle lower but remain attractive. Xiaoxiang and Dingdong improve supply control without becoming uncontrolled cash drains. KeeTa narrows losses but does not drive the valuation. Meituan earns less than old bulls remember, but more than the current price implies.

The bull case requires reclassification. Food delivery becomes rational. In-store withstands Douyin. Grocery density strengthens instant retail. Merchant advertising recovers. Membership deepens habit. Xiaotuan and agent integrations protect the front door. The market stops valuing Meituan as delivery and starts valuing it as local-commerce infrastructure.

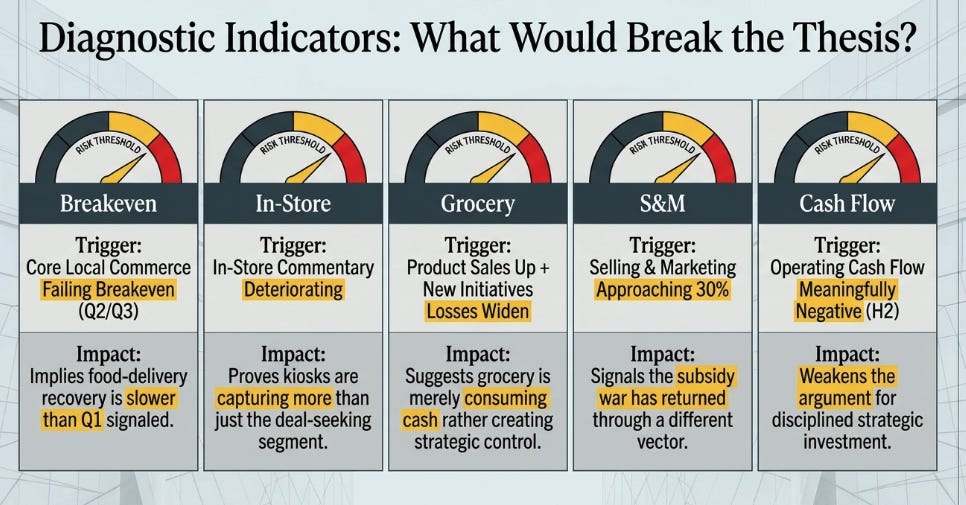

What Would Change My Mind

First, Core Local Commerce failing to reach breakeven in Q2 or Q3 would mean the food-delivery recovery is slower than Q1 implied.

Second, in-store commentary deteriorating sharply would mean the kiosks are taking more than the deal-seeking segment.

Third, product sales growing while New Initiatives losses widen would suggest grocery is consuming control rather than creating it.

Fourth, S&M returning toward 30% of revenue would mean the subsidy war has reappeared through another door.

Fifth, operating cash flow staying meaningfully negative into the second half would weaken the argument that this is disciplined strategic investment.

The Building and the Bellhop

In September, the bellhop’s problem looked simple: two wealthy guests were throwing money around the lobby to prove they did not need him. We said the money would eventually run out. Directionally, that was right. But it was too simple.

In March, the problem became subtler: the bellhop survived, but at lower wages. We said the question was no longer whether he survived, but what he earned.

Now the building has kiosks in the lobby, a rival management company pitching the landlord, and a grocery store in the basement the bellhop just bought.

His advantage is no longer monopoly. It is judgment.

The kiosk tells you which restaurant is cheapest. The bellhop tells you which one is good. The kiosk processes your coupon. The bellhop remembers that you do not eat shellfish. The kiosk can complete a transaction. The bellhop manages a relationship.

The market is watching the kiosks multiply and concluding the bellhop is obsolete.

I think the market is confusing transactions with relationships.

Transactions can be automated. Relationships compound.

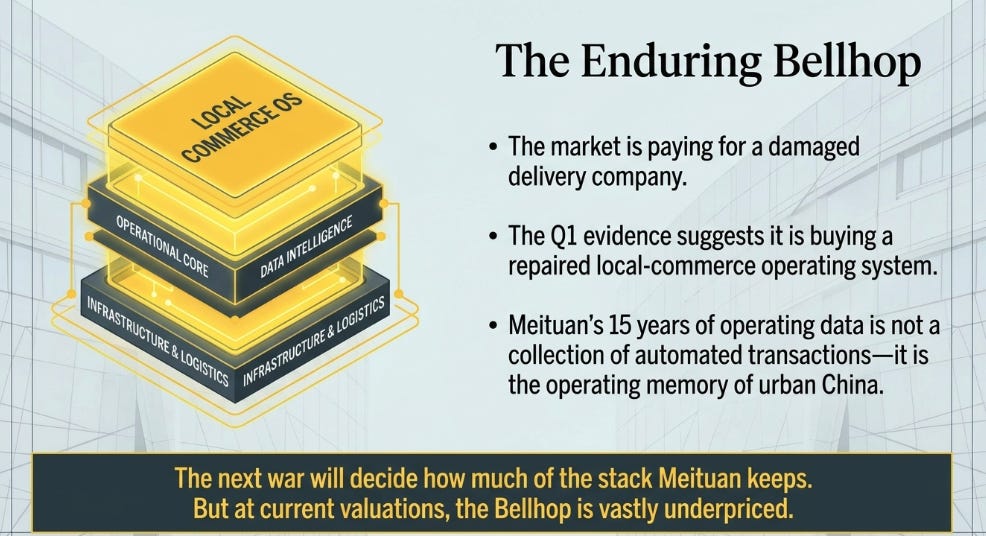

Meituan’s fifteen years of reviews, merchants, riders, memberships, fulfilment infrastructure and operating data are not just transactions. They are the operating memory of local commerce in urban China.

At HK$67–68, the market is paying for a damaged delivery company.

The Q1 evidence suggests it may be buying a repaired local-commerce operating system.

That difference is the opportunity.

The next war will decide how much of it Meituan keeps.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.