Meituan 4Q25 Earnings: What the bellhop earns in an oligopoly

The subsidy war did not break Meituan’s moat. It exposed something more important: the company may no longer be a monopoly platform, but it is still becoming the default operating system for local com

TL;DR

Meituan’s 4Q25 numbers were ugly on the surface, but the underlying network held: users stayed, engagement rose, and Core Local Commerce improved sequentially even under extreme competitive pressure.

The biggest update to the thesis is that the moat survived, but the old margin structure probably did not; the key question is now steady-state earnings power in a three-player oligopoly.

This is no longer just a recovery story. It is a reclassification story: if Meituan is really the operating system for local demand, the market may still be valuing it too narrowly as a food delivery business.

From Caixin Global, February 14, 2026:

“Meituan expects a 2025 net loss of up to 24.3 billion yuan, reversing a 35.8 billion yuan profit in 2024, mainly due to fierce subsidy wars with Alibaba and JD.com.”

Then, on March 26, Meituan delivered Q4 2025 results that were simultaneously ugly and encouraging, a combination only possible when expectations have been beaten into rubble by twelve months of corporate bloodletting. Revenue grew 4.1% to RMB 92.1 billion. The net loss was RMB 15.1 billion. And the Core Local Commerce segment, the business that actually matters, posted a loss of RMB 10.0 billion, down from Q3’s record RMB 14.1 billion.

My first thought was not about the loss. It was about what survived inside it.

In September 2025, we argued that the market fundamentally misunderstood the subsidy war. We framed Meituan as the “digital bellhop”, a company whose value lay not in delivering food but in making urban complexity navigable. We predicted that Alibaba could not sustain RMB 10 billion quarterly burn rates while simultaneously funding an AI infrastructure arms race, and that Meituan’s RMB 170 billion cash pile and superior unit economics would let it simply outlast the siege. We said math was permanent; subsidies were temporary.

That was the thesis. Here is the scorecard.

What we said, what happened

Our September 2025 view rested on three pillars: the moat would hold, competitors would exhaust themselves, and Meituan’s monetization rails, membership, advertising, satellite kitchens, instant retail, would create earnings power beyond delivery commissions.

The moat held. That much is unambiguous. In a year when two of the richest companies in China threw over RMB 100 billion at Meituan’s users, platform GTV and transaction volume still grew double digits. Daily active users, monthly transacting users, transaction frequency, and ARPU all hit all-time highs. The membership program expanded, with high-value members growing steadily and purchasing across more categories. These are not the metrics of a platform losing relevance. They are the metrics of a platform under pricing stress.

The exhaustion thesis is playing out, but more slowly than we anticipated. Alibaba’s free cash flow turned negative for the first time in its public history. JD.com scaled back delivery spending in Q3 2025. The State Administration for Market Regulation intervened, summoning all three platforms in May and July, launching a formal antitrust investigation in January 2026, and reposting state media commentary titled “The Takeout War Should End” the day before Meituan’s earnings. The regulatory trajectory is real. But the war mutated rather than ended cleanly, and that is where our thesis needs updating.

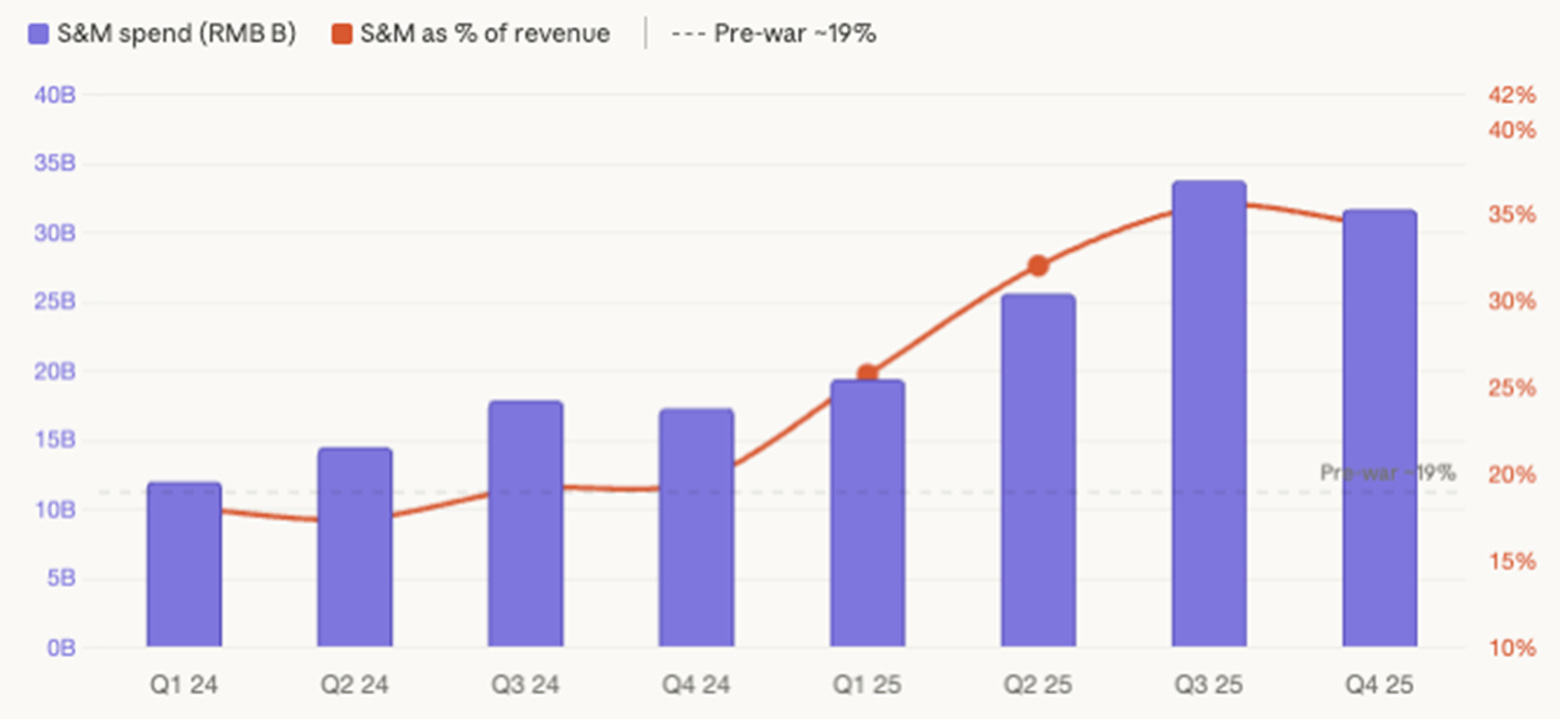

Where we were too optimistic was on the shape of the post-war market. We implied that margins would largely snap back once the math forced competitors to retreat. The Q4 data tells a different story. Core LC revenue fell 1.1% year-over-year despite healthy order and GTV growth, because incentives compressed the revenue Meituan could recognize per transaction. Selling and marketing expenses consumed 34.4% of Q4 revenue, nearly double the pre-war 18-19%. Full-year S&M spending exploded 61% to RMB 102.9 billion, eating nearly all of the gross profit.

The updated thesis in one sentence: the moat survived, but the old margin structure probably did not. Meituan remains the strongest local commerce platform in China. It will not return to being the monopolist it was in 2024.

The users stayed. The money didn’t.

The market’s debate about Meituan is still framed as “when does the subsidy war end?” I think that is the wrong question. The market is waiting for the war to end. It should be asking what the peace treaty looks like.

The better question, the one that actually determines what the stock is worth, is: what is the steady-state earning power of Core Local Commerce in a three-player oligopoly?

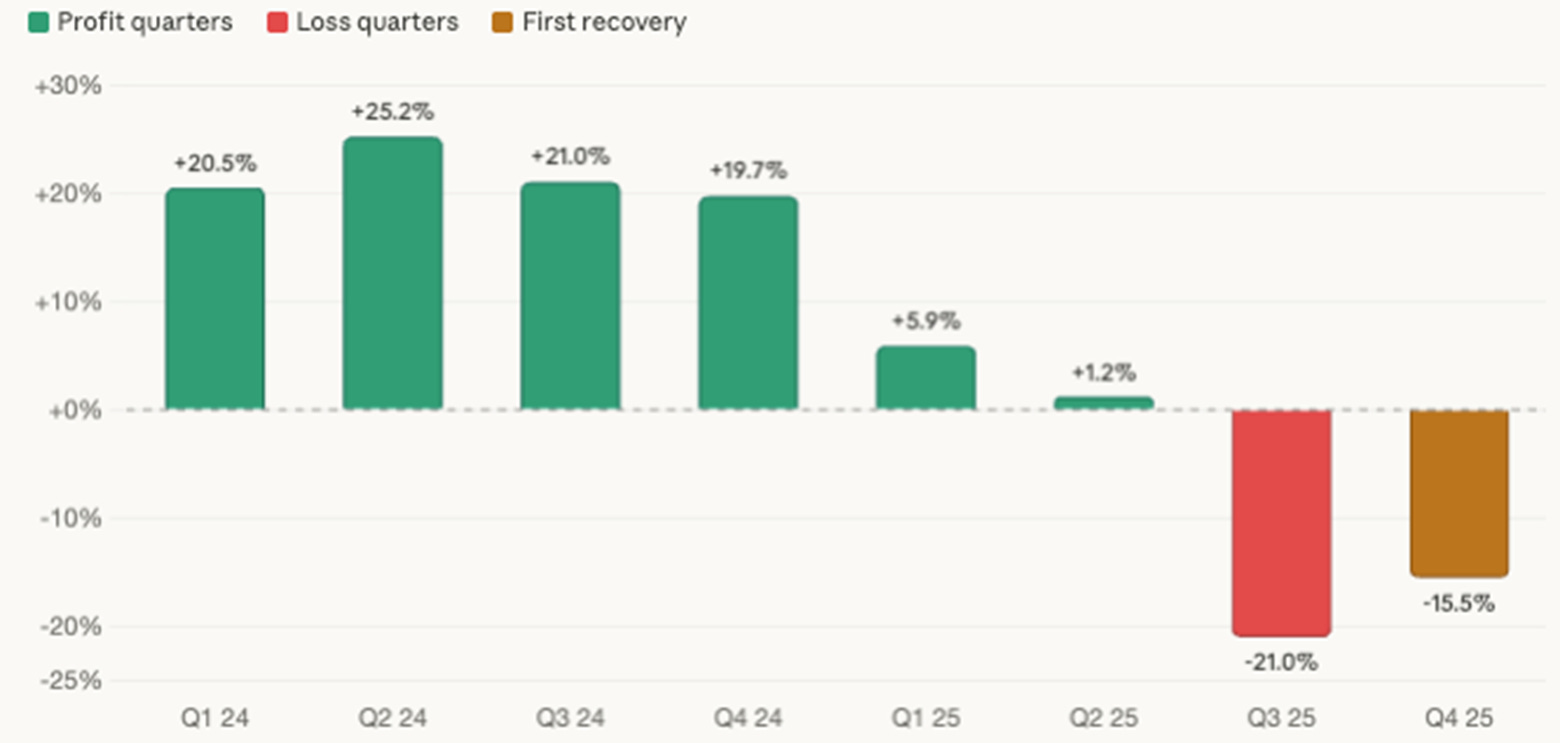

I have stared at this table for a long time, and three things stand out.

First, the margin trajectory. Core LC operating margin improved from -21.0% to -15.5% sequentially, a 29% reduction in losses and the single largest quarter-over-quarter improvement since the war began. This was driven by something specific: management said they “pulled back resources from low-AOV, low-quality orders” while S&M expenses declined from RMB 33.8 billion to RMB 31.7 billion. Meituan is voluntarily ceding the lowest-value segment of the market. That is not a company retreating. It is a company optimizing.

Second, the revenue anomaly. Core LC revenue was down 1.1% despite management saying order volume and GTV grew healthily. That arithmetic only works if the value of each transaction declined, which is exactly what happened. Commission revenue held better (+3.0%) because it is volume-driven; delivery services revenue fell 9.9% because it is AOV-driven. The subsidy war did not shrink Meituan’s network. It shrunk what Meituan could charge for running it.

Third, and this is the detail the market has not processed, management highlighted that delivery services revenue increased sequentially from Q3 to Q4. That means the AOV trough has passed. When delivery revenue is growing quarter-over-quarter while the company is simultaneously cutting subsidies, the per-order economic inflection has likely occurred. CEO Wang Xing confirmed this on the call: “We are on track to see a more meaningful sequential improvement in our food delivery per-order loss in Q1 versus Q4 last year.”

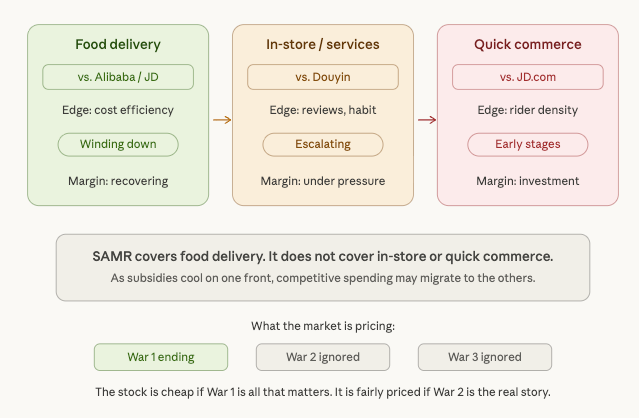

Now, the competitive update. The food delivery front against Alibaba and JD, the war everyone obsessed over, appears to be winding down. SAMR’s escalating intervention provides political cover for all players to de-escalate, and Wang Xing leaned into it with unmistakable intent: “We are firmly against involution.” In China, “involution” is not a business term, it is a political critique of destructive zero-sum competition. By adopting the government’s own vocabulary, Wang Xing is weaponizing Beijing’s policy to force a truce that Meituan could not achieve unilaterally.

But as the food delivery front cools, a different war is heating up. CFO Shaohui Chen, responding to a question about Douyin’s escalating in-store subsidies, said something remarkable in its directness: “Yes, we see the competitors’ recent ramp up in investment. This may negatively impact our short-term profitability.” That is the CFO of a RMB 550 billion company telling you, on a recorded earnings call, that his highest-margin business is under attack and it will hurt.

The operating system thesis

Here is where I step back from the quarterly noise and say what I think is actually happening.

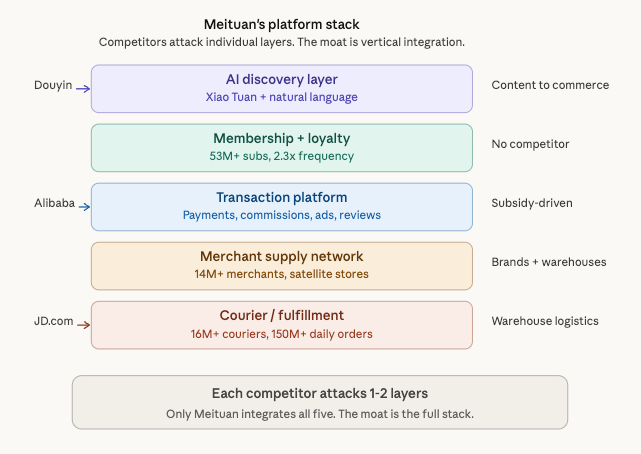

The market classifies Meituan as a food delivery company with temporarily bad margins. I think this is a classification error. I think Meituan is the operating system for local commercial life in urban China, the default interface through which consumers discover, evaluate, transact with, and receive services from the physical world around them. Delivery is the backbone, but it is not the product. The product is the relationship: the membership that ties you to the platform, the reviews that make you trust its recommendations, the AI assistant that knows what you need, and the courier network that makes everything available in 30 minutes.

The Q4 evidence supports this reading in three ways.

Membership. Management said high-value members are growing steadily, with transaction frequency and spending “rising notably” and purchases expanding “across a broader range of categories.” This is the Costco playbook, lock in your best customers with a subscription, make them economically irrational to switch. Fifty-three million paying members ordering 2.3x more than non-members create a demand floor that is impervious to competitor subsidies. These users are not leaving when the coupons disappear.

AI. Wang Xing devoted an extraordinary portion of the call to Meituan’s AI strategy, the in-house LongCat model, the Xiao Tuan assistant embedded in the Meituan app, and his vision of evolving user interaction from keyword search to natural-language requests. His argument is specific and, I think, correct: a generic AI can answer questions about restaurants, but it cannot guarantee a table at 7pm, confirm the kitchen has capacity, dispatch a rider, and track delivery in real time. That requires Meituan’s proprietary data, the API of the physical world: merchant POI, real-time operational status, authenticated reviews, rider GPS coordinates. The AI strategy is not about chatbot magic. It is about interface control. If users ask Xiao Tuan “where should I eat tonight?” instead of scrolling Douyin, Meituan keeps control of the discovery layer.

Capital allocation. The Dingdong acquisition ($717M for mainland China grocery operations) reveals management’s strategic map. Quick commerce is the one category that is structurally Douyin-proof, you do not impulse-buy Tylenol from a video feed; you buy it on-demand when you need it. By acquiring Dingdong’s East China warehouse network, Meituan is neutralizing JD’s advantage in the segment most resistant to the algorithmic content threat.

But Keeta’s international expansion is where skepticism is warranted. New Initiatives operating loss exploded from RMB 1.3 billion in Q3 to RMB 4.6 billion in Q4, almost entirely from Keeta’s four-country expansion. The Saudi data point is encouraging, when Meituan cut subsidies significantly, order volume held, suggesting real service quality moat. But Brazil, where Meituan faces an 80% market share incumbent, received conspicuously cautious language. The domestic core has earned the right to reinvest. It has not earned the right to wander.

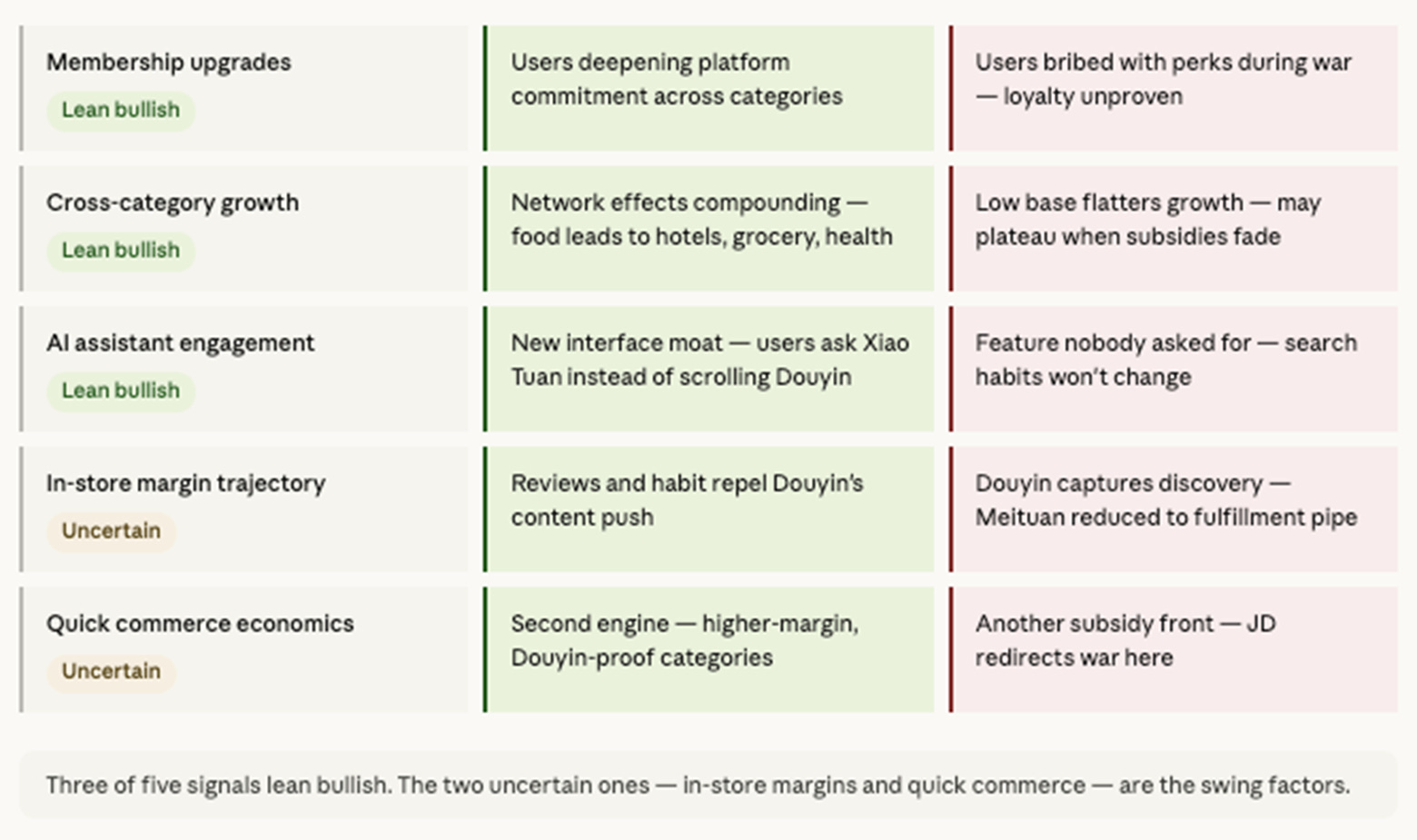

Whether the operating system thesis holds depends on five observable signals. Three lean bullish today. Two remain genuinely uncertain, and those two are the swing factors.

Variant perception

Consensus sees a battered delivery company recovering from a bad year. A repair story.

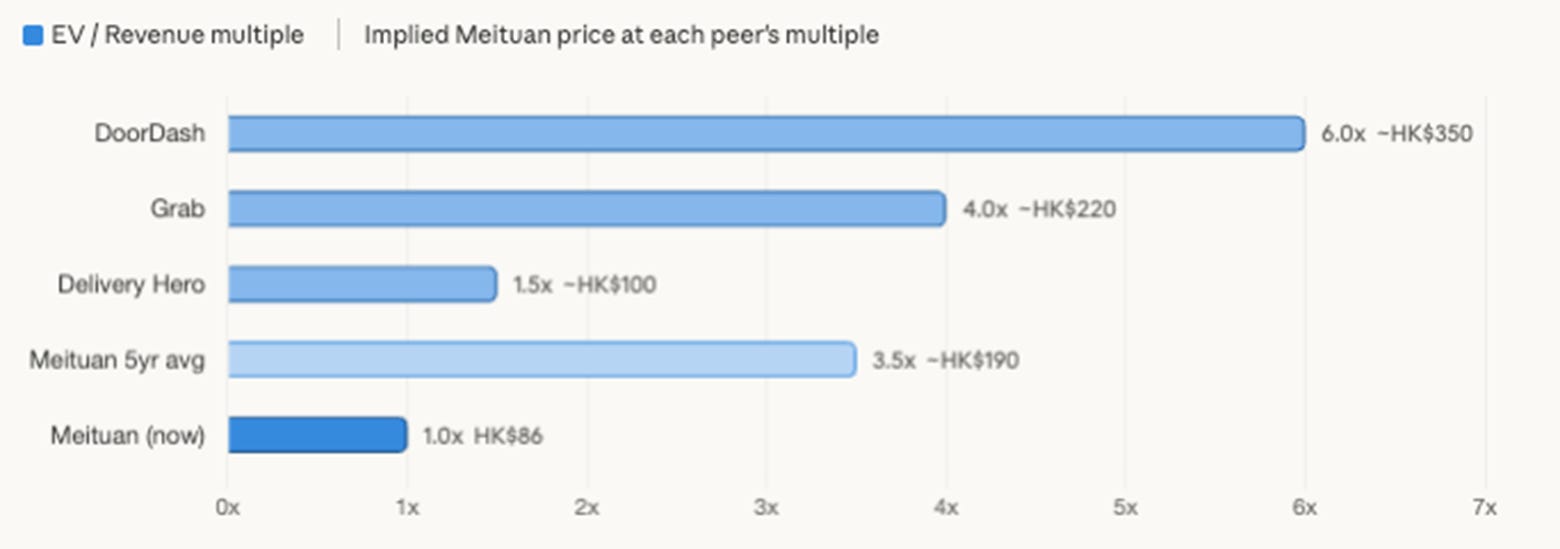

I see a reclassification story. The market values Meituan at roughly 1x EV/Revenue, versus DoorDash at 6x, Grab at 4x. Part of that gap is the China discount. But part is a classification error. If Meituan is “just” food delivery, the discount is deserved. If Meituan is the default operating system for local demand in China, with delivery as backbone, membership as retention engine, advertising as monetization layer, AI as interface, and fulfillment as infrastructure, then the stock is materially undervalued even after the margin reset.

The market is waiting for the war to end. It should be asking what the peace treaty looks like.

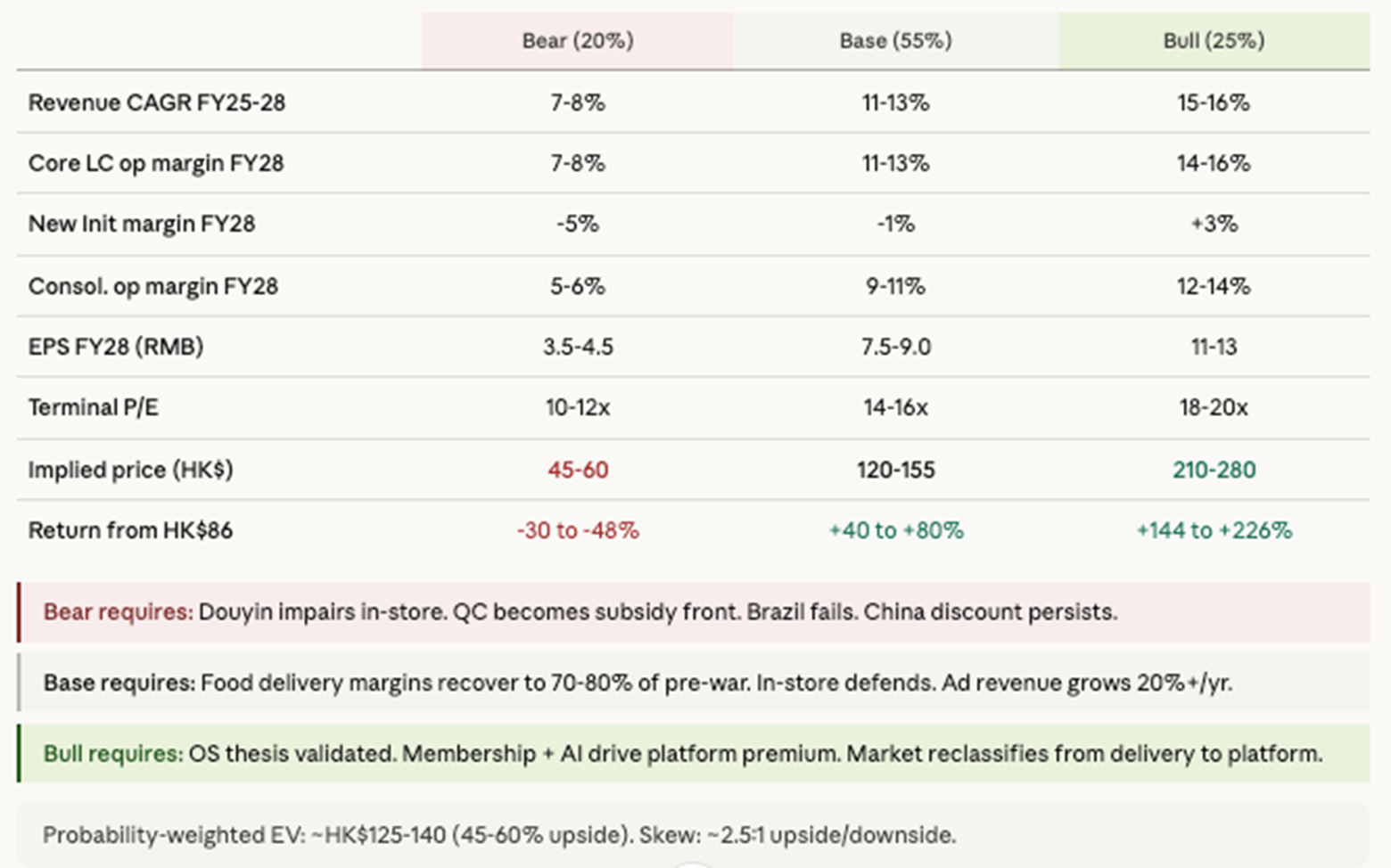

Three-year price framework

It is a framework for thinking about what the stock is worth under different assumptions about the business Meituan is becoming.

The structural insight from this table is not the specific numbers. It is the point underneath them: lower margins on a much larger base can still produce attractive absolute earnings power. But only if Meituan retains the interface and shows discipline on capital allocation. Q4 satisfied the first condition. The second remains an open question.

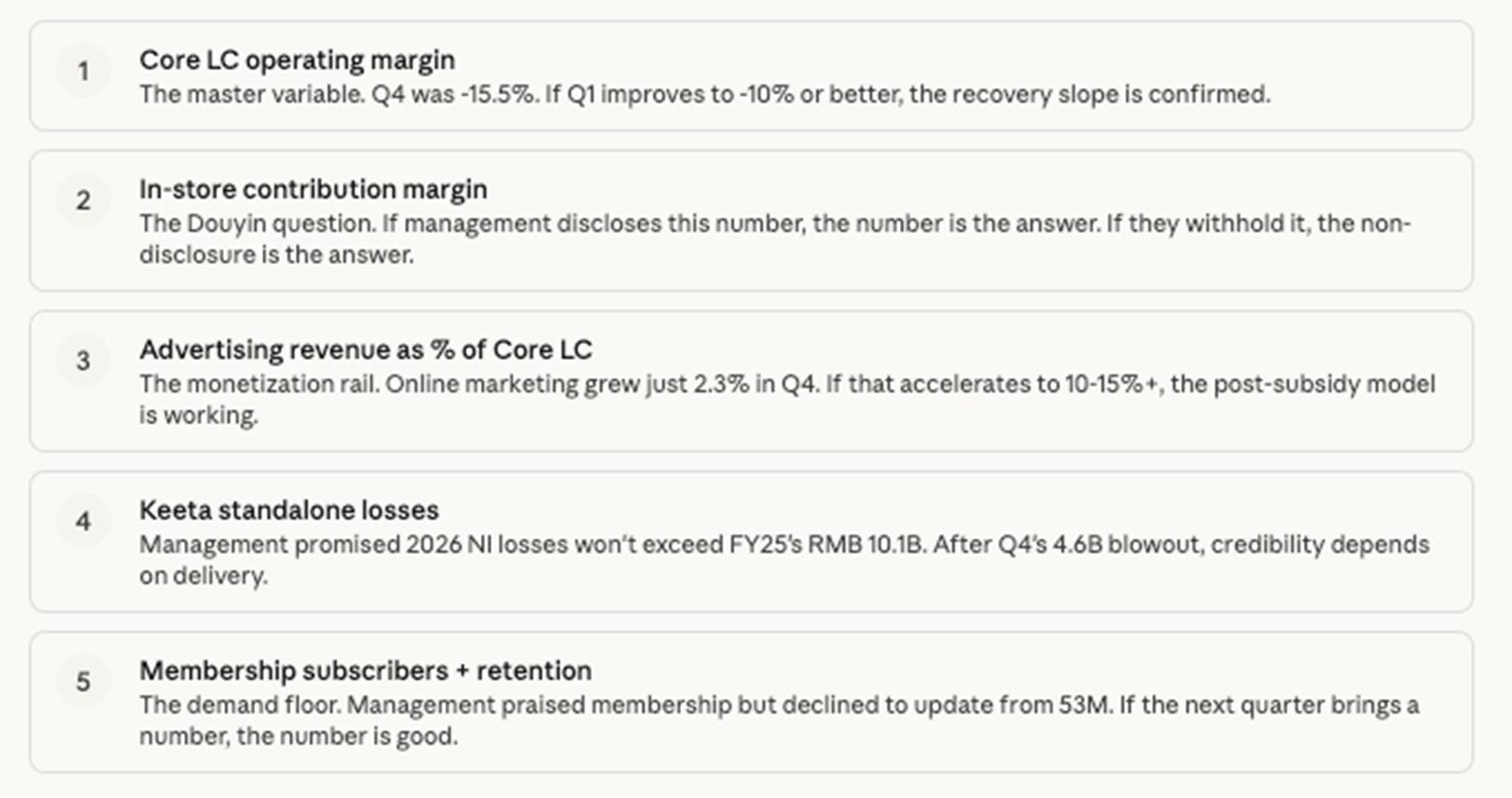

Five numbers to watch

My overall conviction: moderately bullish, but with less certainty than six months ago. The moat thesis is stronger, the stress test proved the network is durable. The margin thesis is weaker, the old economics are not coming back, and the Douyin front is a genuine new risk. At HK$86, the risk/reward still favors the patient investor. But you need to accept that you are buying a different company than the one that traded at HK$190, and that the path from here runs through 12-18 months of messy consolidated numbers before the operating system re-monetizes underneath.

The bellhop lost his monopoly on tips. But he learned every service in the building, signed you up for a membership, and built an AI that knows what you need before you ask. The question is no longer whether he survives. It is what he earns. At this price, I think the answer is more than the market expects, and less than the old monopoly bulls remember.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.