MercadoLibre's 4Q25 Earnings: $12.5 Billion Identity Crisis

The logistics flywheel is compounding. The credit engine now decides the multiple.

TL;DR

Commerce won. Credit changed the story. Revenue +45%, unit shipping costs -11%, Mexico +56%. The logistics density thesis played out exactly as expected. But a $12.5B credit book now dominates the P&L, with provisions nearly equal to operating income.

This is a re-categorization, not a slowdown. MELI isn’t being repriced as weaker e-commerce. It’s being repriced as a capital-intensive LatAm lender. The market doesn’t know how to value a 45%-growth tech platform that also runs a rapidly scaling balance sheet.

The next 4–6 quarters decide the multiple. If NIMAL stabilizes and the book seasons cleanly, ads, deposit funding, and selective margin harvesting could add 3–5pp of operating margin. If Brazil turns before the portfolio matures, the stock trades like a bank.

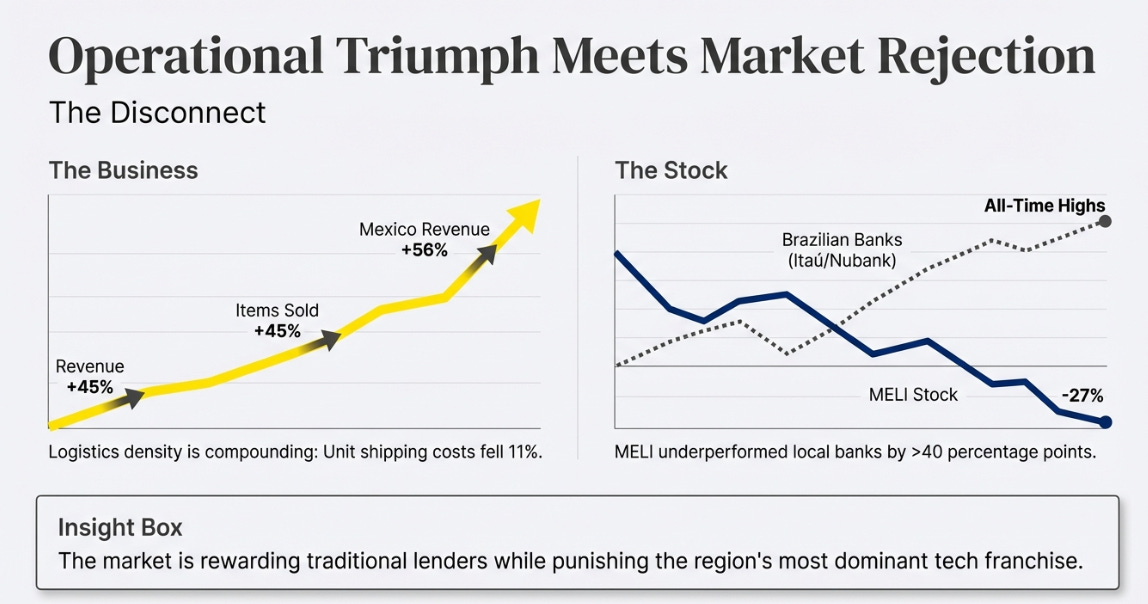

Brazilian Banks Are at All-Time Highs. MELI Is Down 27%.

Brazil’s Bovespa hit record highs in late 2025. Itaú is paying 8% dividend yields. Nubank trades at 9x book. Local banks, the institutions MELI was supposed to be disrupting, are the market’s darlings. Growing loans, managing risk, printing earnings in a high-rate environment that was built for them.

Meanwhile, MercadoLibre, the most dominant technology franchise in Latin America, growing revenue 45% with leading market share across every geography and product vertical, peaked at $2,700 last April and now trades at $1,923. The stock underperformed Brazilian banks by over 40 percentage points in the past year. A company growing revenue three to four times faster than the index is being treated as the worst-performing asset class in the region.

The surface-level explanation is margin compression: operating margins fell from 13% to 9%. But that’s the symptom, not the cause. Our prior four articles explained at length why margins were falling, deliberate investment in shipping subsidies, 1P, cross-border trade, credit card scaling, and why that compression was strategic offense, not weakness. Q4 validated every one of those calls.

Items sold in Brazil grew 45%, accelerating from 42% in Q3 and 26% in Q2. Unit shipping costs fell 11% in local currency. Mexico revenue surged 56%, crushing the 45% threshold we set. Management voluntarily disclosed for the first time that strategic investments represent 5-6 percentage points of operating margin drag, implying a “normalized” margin of 14-15%. The logistics war is won, and the density flywheel is compounding exactly as we described.

The commerce thesis isn’t the problem. The problem is that while we were watching the logistics war, MELI became something else entirely.

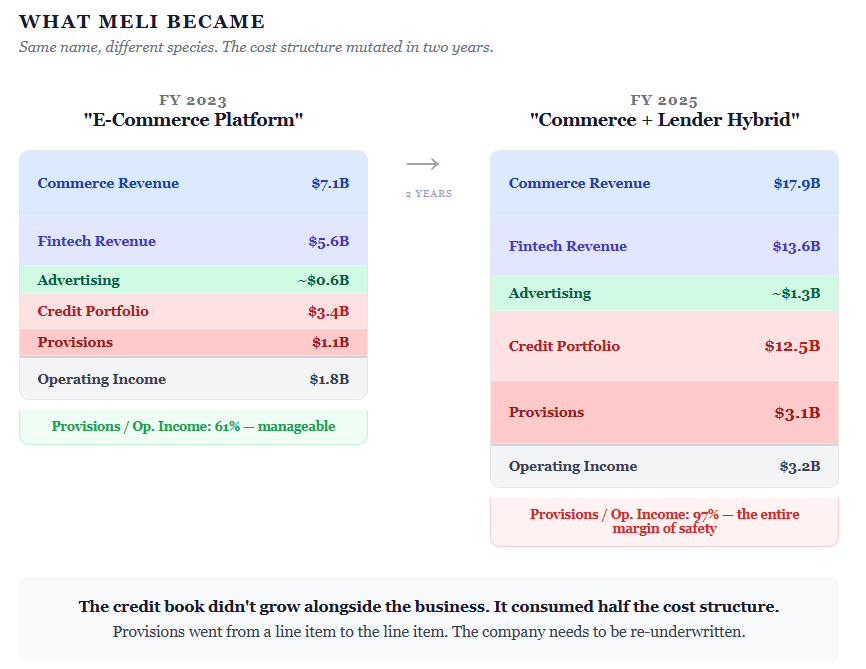

The $12.5 Billion Transformation

Two years ago, MercadoLibre’s credit portfolio was roughly $3 billion, meaningful but not defining. Today it is $12.5 billion. It quadrupled.

Full-year provisions for doubtful accounts hit $3.1 billion in 2025, nearly matching the $3.2 billion in total operating income. In Q4 specifically, provisions of $983M exceeded clean operating income of $790M after stripping out a one-time $99M tax credit. The company’s credit losses now generate more expense than the entire cost of running the marketplace, logistics network, and payments platform after overhead.

This isn’t a feature bolted onto a commerce platform. This is a structural transformation. Net debt doubled from $2.2B to $4.7B. Fintech revenue is 43% of the total and growing faster than commerce. NIMAL, the net interest margin after losses that measures whether lending actually makes money, compressed 580 basis points in two years, from 28.2% to 22.4%.

Our prior articles framed the margin debate as “commerce investment versus short-term profit.” That lens was correct through Q3. It is no longer sufficient. The margin story is no longer primarily about shipping subsidies. It’s about a $12.5B credit book with a 34% annual gross provision rate, operating in a region with volatile currencies and 14.25% policy rates, under a new CEO who stated plainly that 2026 will be “consistent with this bold approach.”

The market used to price MELI as a capital-light e-commerce compounder, a 35x earnings business with software-like margin expansion ahead. It now has to price a capital-intensive Latin American lender. Those are different businesses deserving different multiples. That recategorization, not the commerce margin compression we spent a year writing about, is why the stock fell from $2,700 to $1,900 while the Bovespa rallied and revenue accelerated.

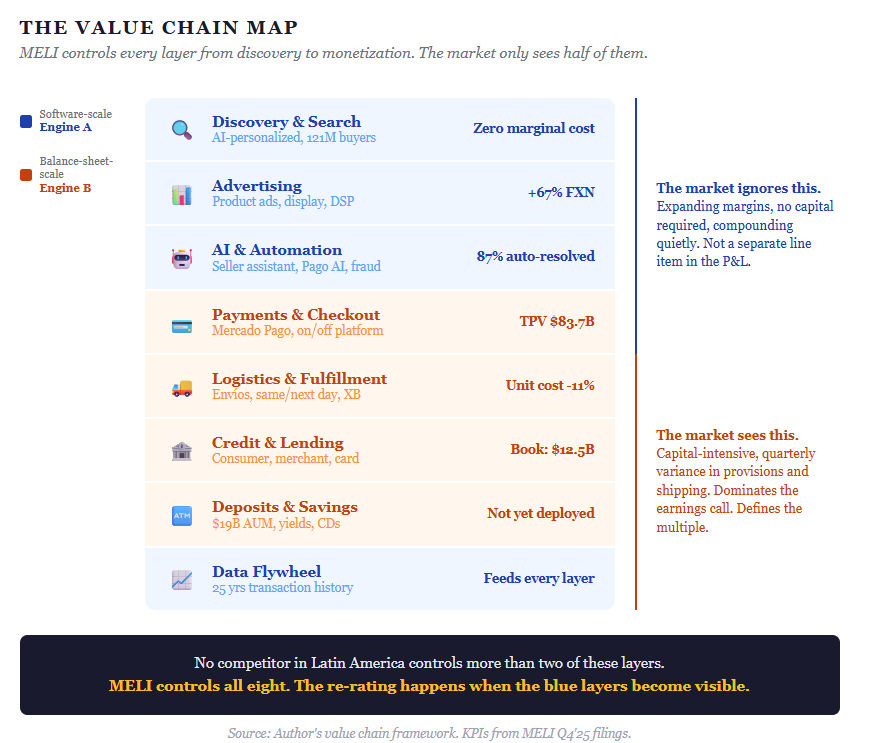

A Company Running Two Businesses on One Stock Price

The clearest way to understand MELI’s predicament is that two fundamentally different businesses share one ticker.

Engine A is software-scale. Marketplace take rates, advertising growing 67% FXN on near-zero marginal cost, AI tools, the seller assistant now touches 20% of GMV, the Pago AI assistant resolved 87% of 9M+ conversations in Q4 without a human, and the data flywheel that improves with every transaction across 121 million buyers. Engine A has expanding margins, no capital consumption, and no macro sensitivity. It compounds quietly.

Engine B is balance-sheet-scale. Credit origination, shipping infrastructure, deposit gathering, and the $3.1B annual provision expense that comes with lending $12.5B to underbanked consumers across four countries. Engine B consumes capital, carries credit cycle risk, and depends on Brazilian macro cooperation. It dominates the P&L.

The stock trades on Engine B because that is where the quarterly variance lives. Every earnings print, the conversation starts and ends with provisions and shipping costs. Engine A’s contribution, the ad revenue growing 67%, the AI assistant eliminating headcount growth, the data moat deepening with each cohort, doesn’t show up as a separate line item. It’s buried in the blended result.

This is the analytical key to the stock. The re-rating doesn’t require Engine B to disappear. It requires Engine A to become visible enough, through advertising scale, AI-driven operating leverage, and credit card maturation, to change the market’s perception of which engine defines the company.

The Credit Book: Both Sides of the Ledger

The honest assessment starts with acknowledging that both the bull and bear cases find support in the same quarter.

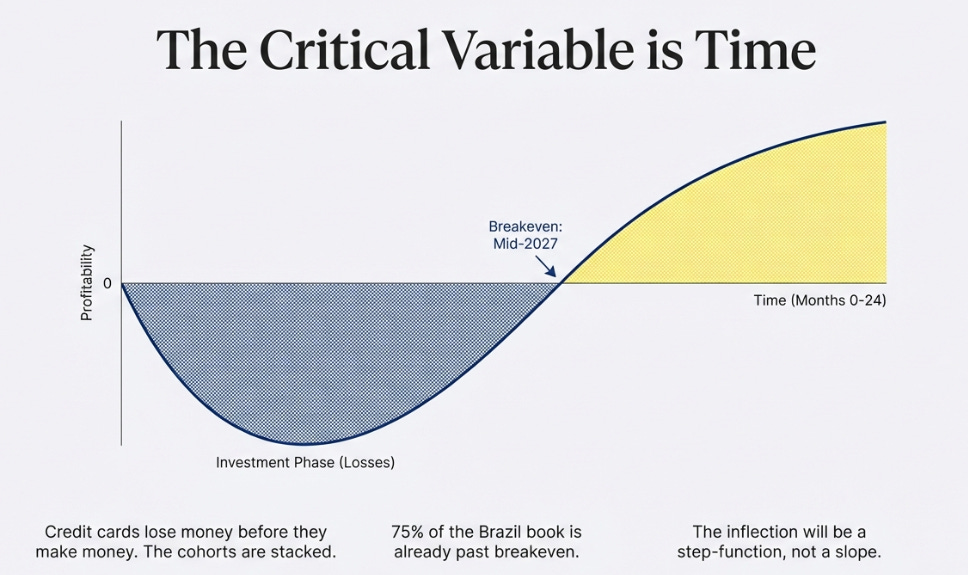

What’s improving: Credit card 15-90 day NPL hit 4.4% in Q4, a historic low, improving for the fifth consecutive quarter. Brazilian card cohorts older than two years are profitable on a net interest margin basis, with roughly 75% of the Brazil book past breakeven. MELI issued 3 million credit cards in Q4, up from 1.5M in Q2, with improving unit economics at each step. The underwriting models, built on 25 years of first-party transaction data, are producing better results as they scale. Mercado Pago achieved the leading Net Promoter Score among all financial institutions in Brazil, Mexico, Argentina, and Chile simultaneously, a trust advantage that took years to build and cannot be replicated by partnership.

What’s getting worse: Consumer and merchant book NPLs ticked higher in Q4 despite favorable seasonality. Management attributed this to intentional expansion into riskier segments at higher yields, which is what every lender says in the 12 months before a cycle turns. NIMAL compressed to 23.3% from 27.6% a year ago, meaning the spread between what MELI earns and what it loses on each dollar lent is narrowing. The $3.1B provision bill on a 34% gross rate leaves razor-thin margin for underwriting error. And the book has never been tested at this scale in a downturn. A 200 basis point NPL increase adds ~$250M in annual provisions. A severe scenario, Brazilian unemployment up 300bps, Selic spiking, BRL down 20%, could compress EPS by 40-50%.

The variable that resolves this tension is time. The credit card maturation curve suggests the full portfolio crosses NIMAL breakeven by mid-2027 at current rates. When it does, 2-3 percentage points of operating margin appear as a step-function, not gradual improvement, but a visible inflection that changes the earnings profile of the entire company. The credit card doesn’t get 5% better each quarter. It loses money for 18-24 months, then it makes money. The cohorts are stacked. The crossover, when it comes, will be sudden.

The question is whether the macro cooperates long enough for the book to get there. MELI’s underwriting advantage, 25 years of transaction data, behavioral signals from 121M buyers that no traditional bank possesses, is real. But underwriting advantages don’t eliminate credit cycles. They reduce severity. The $12.5B question isn’t whether MELI is a better lender than Itaú. It’s whether being a better lender is enough when you’re lending four times more than you were two years ago in a region where currencies can move 20% in a quarter.

$MELI

Three Levers Nobody Is Modeling

If the credit book seasons cleanly, three additional catalysts could accelerate the transition from Engine B dominance to Engine A visibility.

Deposit-funded lending. Mercado Pago sits on $19B in assets under management that are not being used for credit funding. CFO Osvaldo Giménez confirmed on the call they are “not doing fractional banking.” When MELI eventually funds 20-30% of the credit book from deposits rather than wholesale markets, borrowing costs drop by $200-400M annually. No sell-side model includes this optionality.

Advertising scale. Ads run at under 2% of GMV versus 3-5% for mature US e-commerce platforms. On $65B of annual GMV, closing half the gap represents ~$1B in incremental revenue with near-pure margins, no credit risk, no capital, no macro dependency. This is the highest-quality earnings lever in the entire model, and it grew 67% this quarter.

The quiet harvest signal. In January 2026, MELI restructured merchant shipping charges in Brazil to a weight-and-dimension-based model. Management refused to quantify the margin impact when asked directly. The timing, weeks after disclosing the 5-6pp investment drag, is not coincidental. This is the first indication that selective margin harvesting has begun, even as the headline investment posture remains aggressive.

Combined, these three levers represent 3-5 percentage points of incremental operating margin over 2-3 years. None require heroic assumptions. All require the credit book to remain stable.

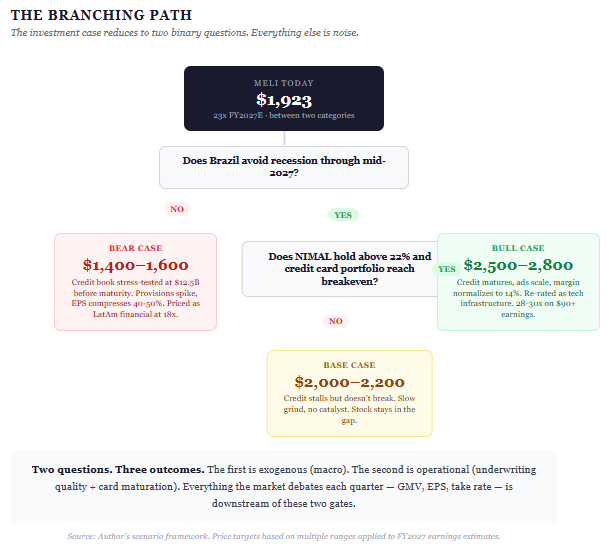

The Conditions, the Scenarios, and Where We Stand

We have been bullish for a year. Every commerce call validated. The stock didn’t move. We owe specific conditions under which this thesis either works or breaks.

Four signposts that determine which scenario plays out:

NIMAL must hold above 22% and trend toward 24% by mid-2026, this is the single most important number in the model. Provisions as a percentage of revenue must trend from 11.2% toward 10%, if it stays above 12% through H1, credit growth is permanently dilutive. Management’s 5-6pp investment drag must narrow to 4-5pp within two quarters, flat or wider means no margin inflection is coming. And Brazil cannot enter recession before the credit card portfolio matures, the exogenous variable nobody controls.

If conditions hold: Bull case, $2,500-2,800. Credit matures, ads scale, margins normalize toward 14%, the market re-rates MELI from “hybrid bank” back toward “tech infrastructure.” At 28-30x on $90+ FY2027 earnings, you get $2,700.

If credit stalls but doesn’t break: Base case, $2,000-2,200. Current trajectory continues. Slow improvement, quarterly noise, no catalyst. The stock grinds.

If macro turns before the book seasons: Bear case, $1,400-1,600. Brazilian recession stress-tests $12.5B in consumer credit before the card portfolio reaches breakeven. Provisions spike, EPS compresses 40-50%, the market prices MELI as a LatAm financial at 18x depressed earnings.

At $1,923 and 23x FY2027 consensus, the stock is stuck between two investor bases that don’t overlap. The tech growth investors who owned MELI at $2,700 fled when margins fell from 13% to 9%, they wanted operating leverage, got operating deleverage, and moved capital to companies where AI is expanding margins rather than compressing them. The structural utility investors who should own MELI at $1,900, pricing it as a 45%-growth integrated commerce-fintech platform with 78 million financial users and leading NPS in four countries, haven’t arrived because they need to see the credit book survive a full cycle before they’ll underwrite a financial institution at this scale.

That gap is the stock. Not the quarter. Not the EPS miss. Not the margin compression. The gap between who left and who hasn’t yet shown up.

What closes it is time, and specifically the passage of time without a credit event. Every quarter where the card book matures, where NIMAL stabilizes, where provisions-to-revenue ticks down rather than up, that’s a quarter that pulls structural capital off the sidelines. The bull case doesn’t require a single new initiative. It requires the existing portfolio to season.

A year ago we wrote that margin compression was the strategy, not the problem. That was right about commerce. What we didn’t appreciate was that the same company was simultaneously building a $12.5B lending operation that would change how the market categorizes the entire business. We were watching the logistics war. The credit transformation happened in peripheral vision.

The logistics war is won. The credit war is just beginning. The commerce moat was earned over 25 years of compounding density and trust. The credit moat has to be proven, and the next four to six quarters will tell us whether it will be.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.