Meta's 1Q26 Earnings: AI Tax

The ad business is already proving the value of AI. The problem is that the price of admission keeps going up.

TL;DR

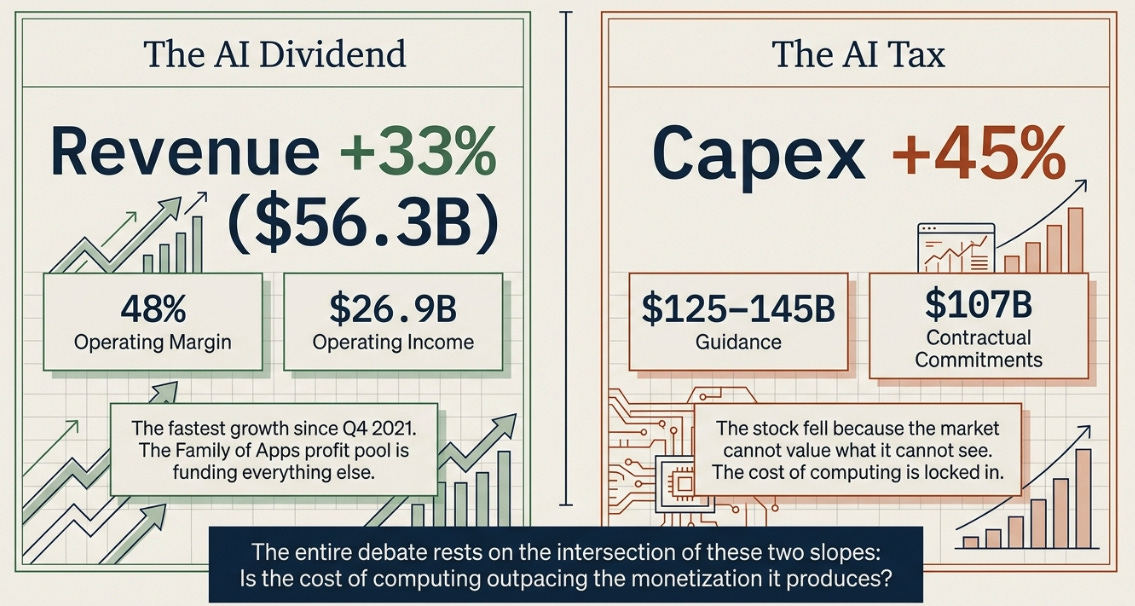

The AI dividend is real and accelerating. Revenue grew 33%, driven by 19% more ad impressions at 12% higher prices, the rare combination that only happens when AI is making the product genuinely better. The Family of Apps generated $26.9B in operating income at a 48% segment margin.

The AI tax is rising and locked in. Capex guidance rose to $125–145B, but the spending isn’t just for better ads, it’s building a consumer agent platform that doesn’t have revenue yet. Revenue grew 33%; capex grew 45%. Those two slopes are the entire debate.

The stock fell because the market can’t value what it can’t see. Meta has a history of making massive bets on attention shifts before the business model is clear, mobile, Instagram, Stories, Reels. The AI agent bet follows the same pattern at 100x the cost. The market is not rejecting the strategy. It is struggling to price a future it cannot yet measure.

What Is Meta?

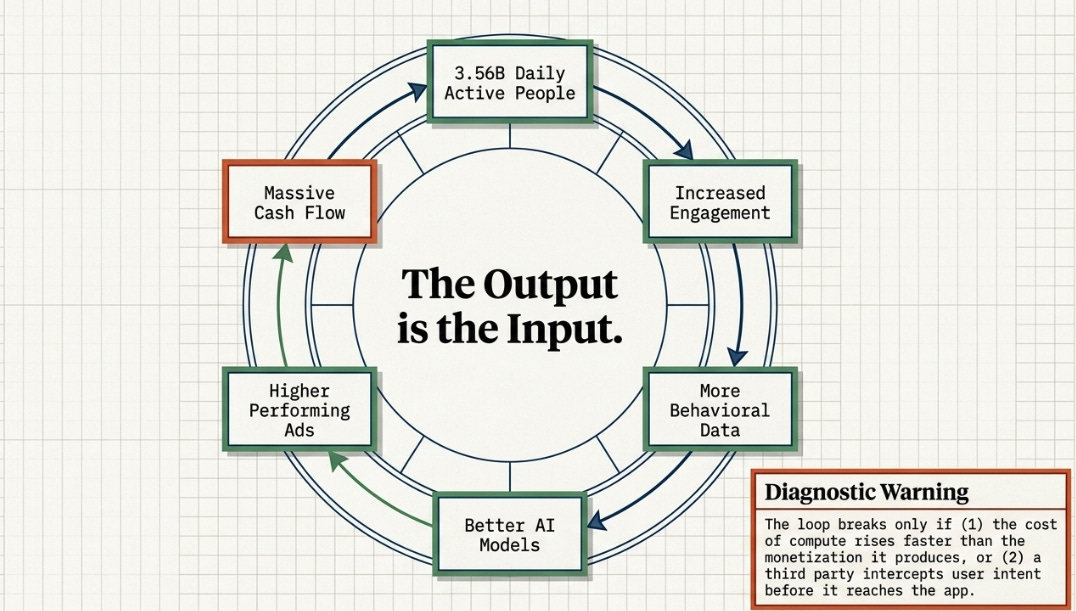

Before the quarter: Meta becomes more valuable as its market grows because every unit of human attention flowing through its apps generates behavioral data that improves AI models, which makes the next unit of attention more valuable, to the user, to the advertiser, and to Meta. More engagement creates more data; better data creates better models; better models create more engagement and higher-performing ads; higher ad performance generates the cash to fund more compute; more compute improves the models.

The output of the system is also the input. That is what makes it compound.

This mechanism strengthens at scale because Meta has 3.56 billion daily active people, massive advertiser liquidity, real-time conversion feedback, and enough cash flow to fund the infrastructure required to keep the loop spinning. It breaks if the cost of compute rises faster than the monetization it produces, or if something intercepts user intent before it reaches Meta’s apps.

That is the fundamental question this quarter needed to answer: is the loop still compounding, or is the cost of running it starting to outpace the returns?

AI and the Attention Business

The answer, on the operating side, was unambiguous.

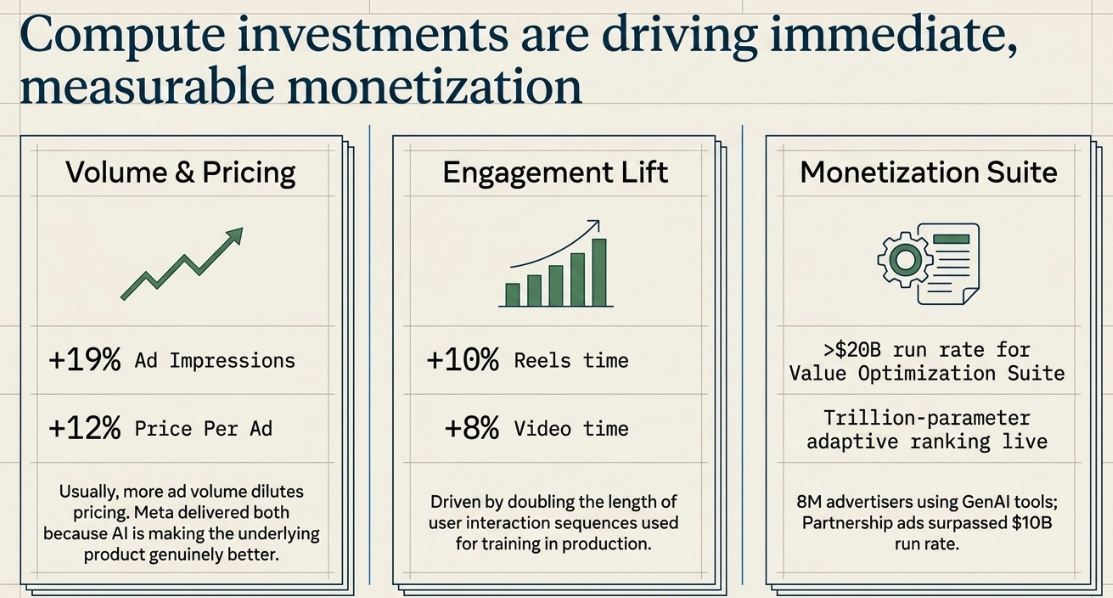

Revenue grew 33% year-over-year to $56.3 billion, the fastest growth since Q4 2021, on a revenue base nearly twice as large. More importantly, ad impressions grew 19% and price per ad grew 12%. That combination is rare. Usually more ad volume dilutes pricing. Meta delivered both because the underlying product is getting better.

Susan Li explained the mechanism:

On Instagram, the ranking improvements that we made in Q1 drove a 10% lift in Reels time spent. On Facebook, total video time increased more than 8% globally in Q1, the largest quarter-over-quarter gain in four years... We doubled the length of user interaction sequences we use for training on Instagram and increased the richness of how each user interaction is described, enabling our systems to develop a deeper understanding of user interests.

These are not plans. They are engineering changes running in production, generating measurable engagement gains right now. The ad improvements are not separate from the AI investment. They are the first return on it.

The monetization evidence goes further. The value optimization suite, which helps advertisers find the highest-value conversions, not just the most conversions, has surpassed $20 billion in annual revenue run rate, more than doubling year-over-year. The adaptive ranking model, a trillion-parameter LLM-scale inference system, drove measurable conversion rate gains across major ad surfaces. Eight million advertisers are using generative AI creative tools. Partnerships ads surpassed $10 billion in run rate.

The Family of Apps generated $26.9 billion in operating income at a 48% segment margin. That is the profit pool funding everything else. No other consumer internet company generates cash at this rate.

The AI dividend is real, measurable, and accelerating. Price per ad re-accelerated from just 6% in Q4 to 12% in Q1. The flywheel is working.

The Capex, and What It’s Actually Building

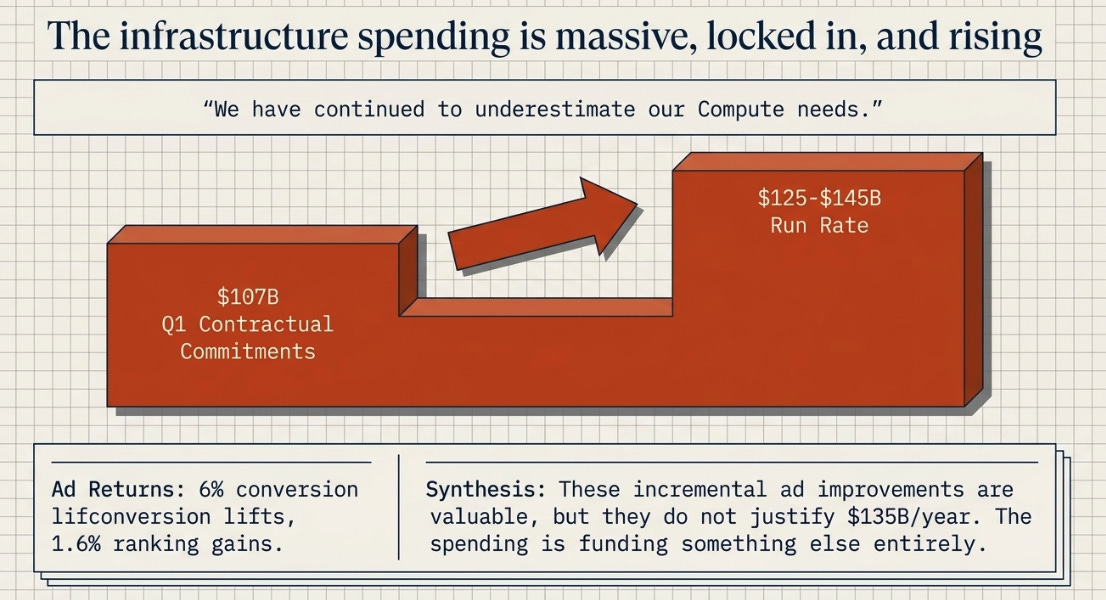

That brings us to the number the market cared about. Meta raised its 2026 capex guidance from $115–135 billion to $125–145 billion, and disclosed a $107 billion step-up in contractual commitments in Q1 alone, multi-year cloud deals and infrastructure agreements that lock in the spending trajectory for years. Li was candid:

Our experience so far has been that we have continued to underestimate our Compute needs, even as we have been ramping capacity significantly.

If this spending were only about making ads better, the market would have a point. The ad stack improvements are valuable but incremental, 6% conversion lifts, 1.6% ranking gains, better creative tools. Important, but probably not $135-billion-a-year important.

The spending makes sense only if you understand what Meta is actually building: not just a better ad machine, but a consumer agent platform.

Zuckerberg was explicit about this on the call:

My view of AI is very different from many others in the industry. I hear a lot of people out there talk about how AI is going to replace people. Instead, I think that AI is going to amplify people’s ability to do what you want... We are building a personal agent focused on helping people achieve the diverse goals in their lives. We’re also building a business agent focused on helping entrepreneurs and businesses across the world.

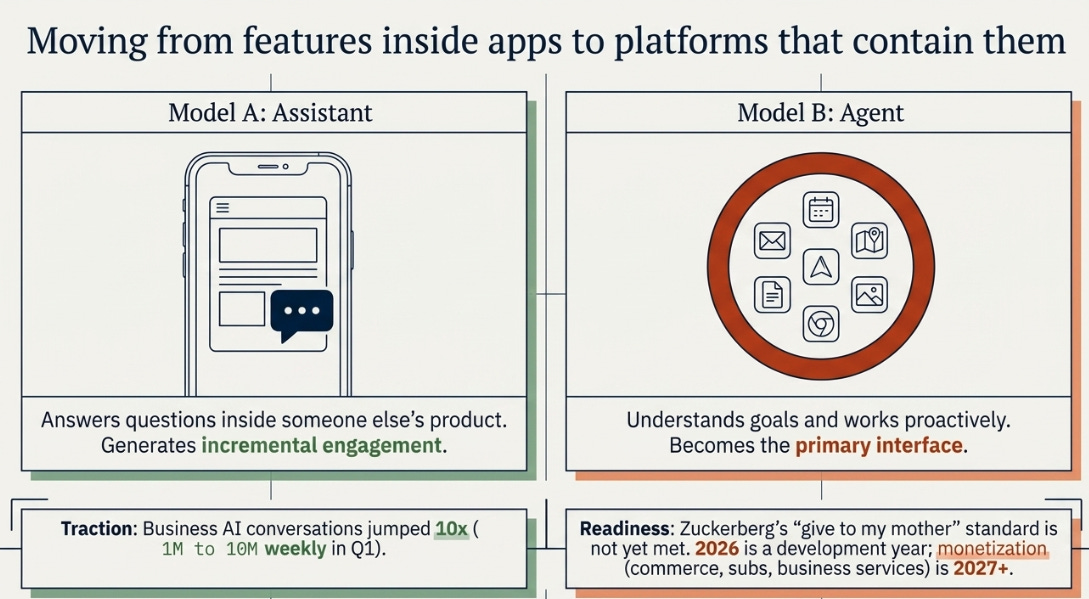

The distinction between an assistant and an agent is the distinction between a feature and a platform. An assistant answers questions inside someone else’s product. An agent understands your goals and works proactively to achieve them, it becomes the interface. If successful, it opens monetization beyond advertising: commerce commissions, premium subscriptions, business services.

The earliest evidence is already visible. Business AI conversations on WhatsApp and Messenger grew from 1 million weekly at the start of the year to 10 million, a 10x increase in one quarter. Li noted these are “currently free for most businesses,” with plans to establish a longer-term monetization model.

But Zuckerberg was also honest about readiness. Asked about timing, he said the quality bar is building something he would “want to give to my mother.” That tells you the consumer agent is not ready for mass-market deployment. 2026 is a development year. Monetization is 2027+.

So the capex funds two things: the ad stack improvements generating returns today, and the agent platform that is supposed to generate returns tomorrow. The first justifies some of the spending. The second is supposed to justify the rest. And the second does not have revenue yet.

The Risk Under the Risk

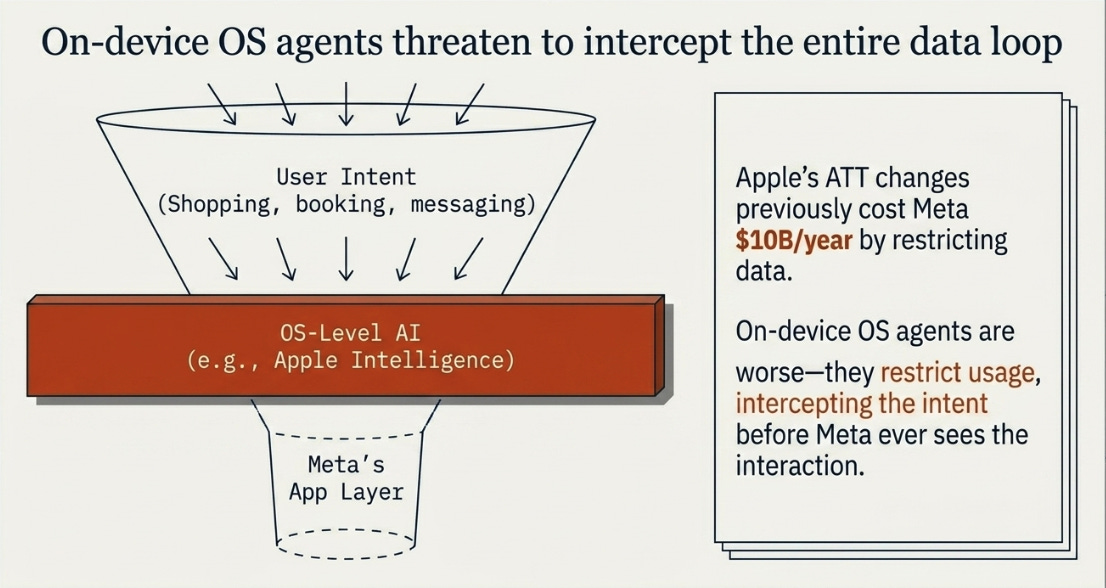

Most of the market’s debate is about cost. I think the deeper risk is disintermediation.

Meta’s flywheel depends on attention and intent flowing through its apps. If an on-device AI agent, Apple Intelligence, most obviously, handles shopping, recommendations, and messaging at the operating system layer before the user opens Instagram or WhatsApp, Meta never sees the interaction. The data loop breaks at its source. Apple’s ATT changes already cost Meta an estimated $10 billion in annual revenue by restricting data. On-device agents could do worse, not by restricting Meta’s data, but by making Meta’s apps unnecessary.

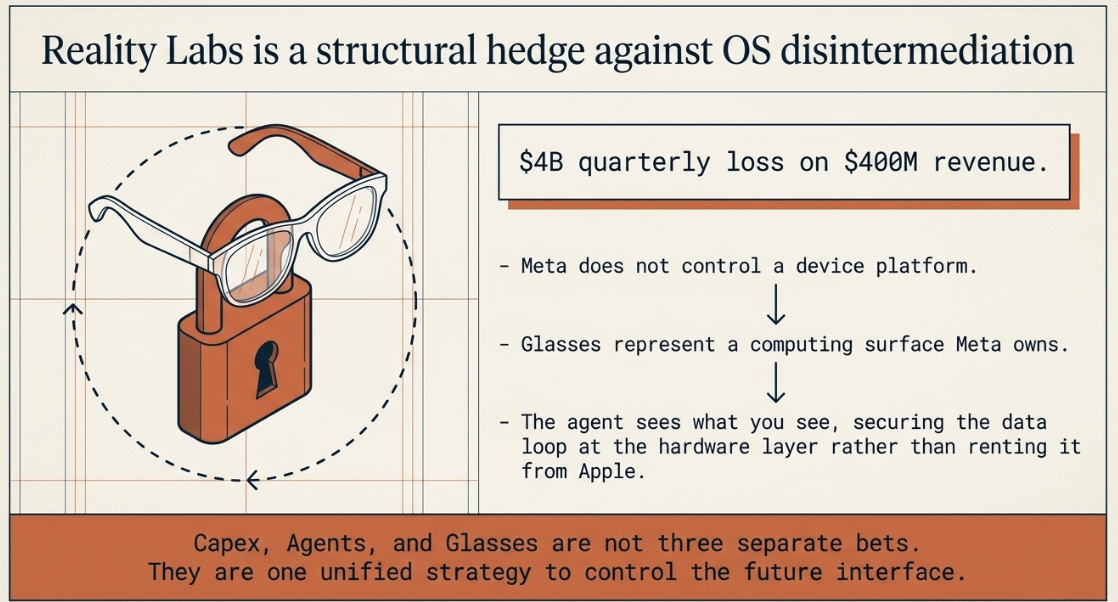

This is why Reality Labs matters despite $4 billion in quarterly losses on $400 million in revenue. Meta does not control a device platform. Glasses are not strategically interesting because of hardware revenue. They are interesting because they could become a computing surface Meta owns, one where the agent sees what you see and the data loop is secured at the hardware layer rather than rented from Apple at the app layer.

Capex, agents, and glasses are not three separate bets. They are one bet.

Why the Market Is Confused

The stock fell because the market cannot value what it cannot see.

Meta told investors two things simultaneously.

First: AI is already making the core business better, here are the metrics.

Second: we are spending $135 billion a year building something new that does not have revenue yet, and we cannot tell you when the spending peaks.

The first story had numbers. The second had vision. The market priced the second.

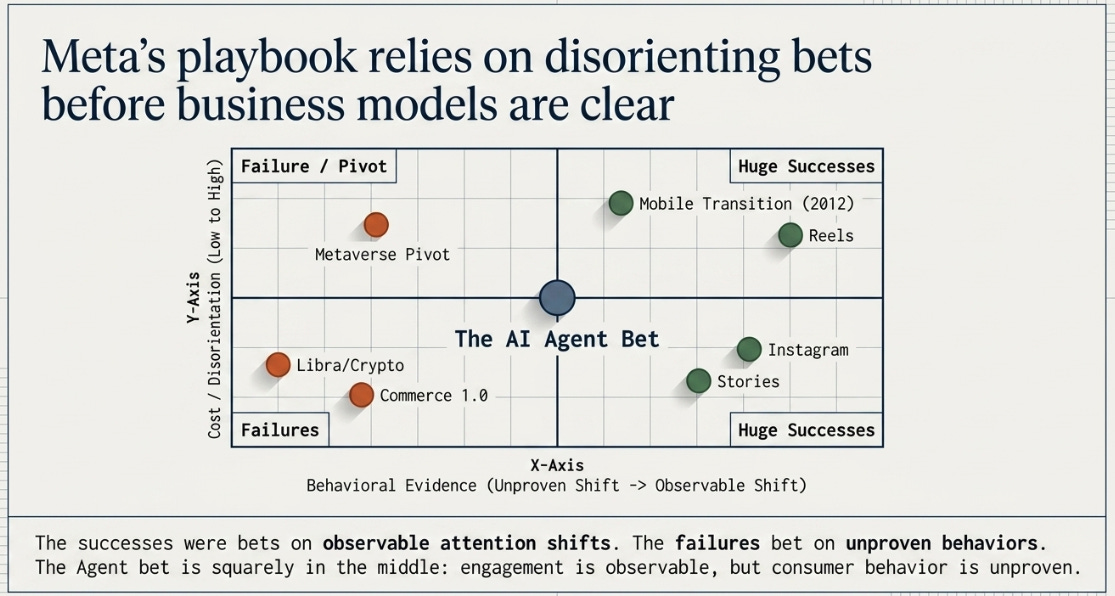

This is a familiar pattern for Meta, though not always a comfortable one. The company has a history of making large, disorienting bets on where attention is moving, often before the business model is clear, and often at a cost that alarms investors.

The mobile transition in 2012–2013 is the closest parallel. Meta saw usage migrating to phones, invested heavily in mobile ad formats while desktop revenue slowed, and watched the stock trade below its IPO price for over a year. The market could see the cost of the transition but not the revenue. Then mobile ads worked, and the stock went from $18 to $300 over the next eight years.

Instagram looked reckless, $1 billion for thirteen employees and no revenue. Stories looked self-destructive, cannibalizing News Feed. Reels looked derivative, copying TikTok. In each case, Zuckerberg bet on where attention was heading and absorbed near-term pain.

But not every bet has worked. The metaverse pivot was the most expensive strategic miscalculation in Meta’s history, costing tens of billions before the company course-corrected toward AI. The Libra/Diem cryptocurrency initiative collapsed under regulatory pressure. Meta’s commerce push on Instagram and Facebook in 2021–2022 was quietly wound down.

The difference between the successes and failures is instructive. The successes, mobile, Instagram, Stories, Reels, were bets on observable shifts in user attention. The failures, metaverse, crypto, commerce 1.0, were bets on behavior changes that had not yet occurred.

Which category does the AI agent bet fall into? The engagement data says users are already spending more time on AI-improved content. The business AI data says businesses are already adopting AI-mediated conversations. The agent quality, by Zuckerberg’s own admission, is not yet at the “give to my mother” standard. The spending is locked in. The product is still catching up.

The Whole Quarter

Revenue grew 33%. Capex grew 45%. The ad flywheel is compounding. The cost of building the agent platform is rising. The stock reflects uncertainty about which curve is steeper.

The near-term test is price per ad. Q1’s 12% growth re-accelerated from 6% in Q4, the strongest evidence that AI compute is improving the value of Meta’s inventory. If that holds above 10% through the second half while capex stays within $145 billion, the dividend is outgrowing the tax. If price per ad falls back toward mid-single digits despite the spending, the marginal return on compute is compressing.

Meta is not becoming a worse business. It is becoming a more expensive business to run, in service of a platform that does not yet exist in finished form. The market has seen Meta make this kind of bet before. Sometimes it worked spectacularly. Sometimes it didn’t.

That uncertainty is reasonable. I think it is too pessimistic. But I understand why no one wants to say that out loud with $107 billion in contractual commitments on the table.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.