Micron 3QFY26 Earnings: The Cycle Gets a Contract

Micron is no longer just selling into a memory upcycle. It is trying to turn the cycle into a contract before China and new supply catch up.

TL; DR

The key shift is buyer behavior: memory sellers once tried and failed to fix prices; now customers are voluntarily signing five-year take-or-pay contracts with deposits because AI memory shortages can strand far larger infrastructure investments.

HBM and data-center products are weakening the old commodity framework: frontier memory is becoming less swappable as qualification, packaging, thermals, base dies, controllers, and firmware matter more than JEDEC-style interchangeability.

The race is against supply: Micron’s upside depends on moving enough revenue into contracted, differentiated products before CXMT and incumbent greenfield fabs bring the industry back toward ordinary memory-cycle economics.

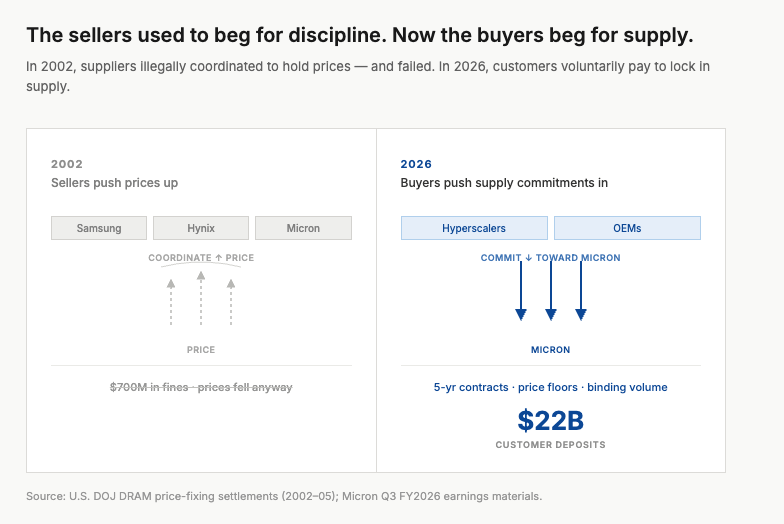

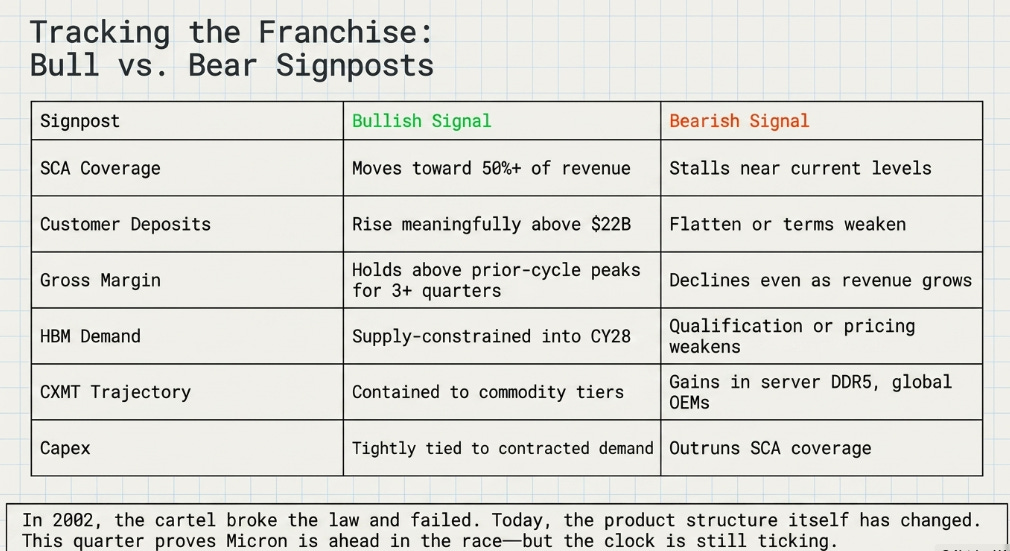

In 2002, executives from Samsung, Hynix, Infineon, and Micron met in hotel bars to fix DRAM prices. They had no choice, or so they believed. Memory was the purest commodity in technology, every chip interchangeable with every rival’s, every margin competed to zero, and the only way to hold a price was illegally. They got caught. The United States levied criminal fines exceeding $700 million. Executives went to prison. And prices fell anyway, because a cartel cannot hold together in a commodity where any member can defect by adding a wafer line.

That episode is the most useful fact about the memory industry, and not for the reason people usually cite. The cartel is typically offered as evidence of bad behavior. It is evidence of structural helplessness. These companies tried the most extreme measure available to escape the commodity curse, and it did not work. The standard was too open, the product too swappable, the entrants too numerous. No amount of coordination could override the structure.

What happened twenty-four years later is the opposite in every respect, not illegal coordination among sellers, but voluntary commitment from buyers. Micron reported $41.5 billion in quarterly revenue, 84.9% gross margins, and $18.3 billion in free cash flow, and then announced that sixteen of its customers had voluntarily signed five-year contracts with price floors, volume commitments, and $22 billion in cash deposits to guarantee access to a product that used to be available from anyone, at any time, at whatever the spot market offered.

The sellers used to beg for discipline. Now the buyers beg for supply. That inversion is the story.

The Quarter Was Evidence, Not the Thesis

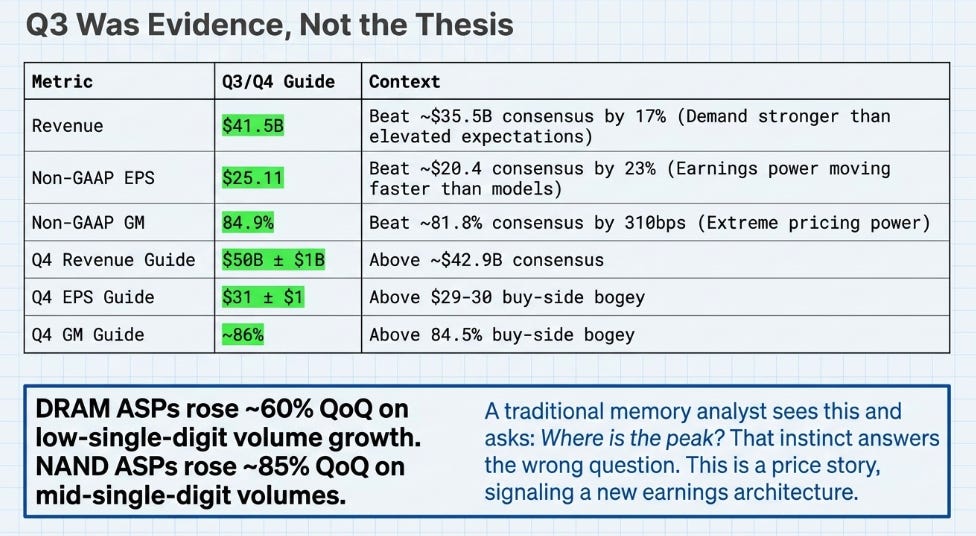

The numbers deserve acknowledgment, not extended discussion. They are the evidence. They are not the thesis.

A traditional memory analyst sees this table and immediately asks: where is peak? DRAM ASPs rose roughly 60% sequentially on low-single-digit volume growth. NAND ASPs rose roughly 85% on mid-single-digit volumes. This was a price story, not a volume story. In old memory, that is exactly when you sell.

That instinct is not wrong. It is simply answering the wrong question. The question is not whether Q3 was great. It was. The question is whether Q3 belongs to the old memory cycle or to a new earnings architecture. The difference is the contracts, and the reason the contracts exist is that something deeper has changed about the product itself.

The Death of Swappability

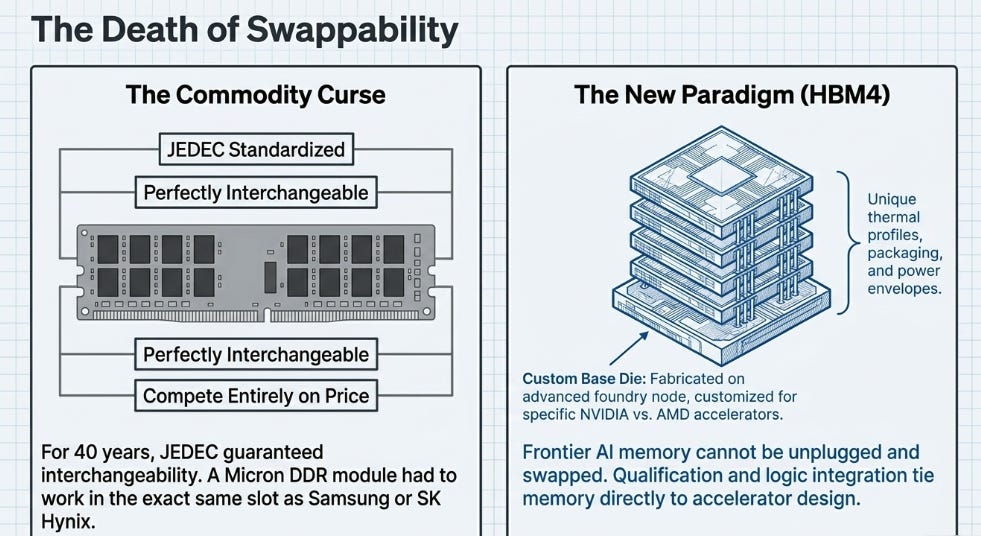

For forty years, memory’s commodity-ness was enforced by JEDEC, a standards body whose entire purpose was to guarantee interchangeability. A DDR module from Micron had to work in the same slot as one from Samsung or SK Hynix. When a component is perfectly swappable, buyers compete vendors entirely on price. That was the commodity curse, and it was the system working as designed.

What is happening at the AI frontier is that the most valuable memory is becoming less swappable. HBM nominally adheres to a standard, but the practical reality of HBM4 is that the base die, the logic layer at the bottom of the stack, is fabricated on an advanced foundry node and increasingly customized for specific accelerators. A stack qualified for NVIDIA’s platform is not the same product as one built for AMD. The thermal profile, packaging, power envelope, and qualification are all different. You cannot unplug one and plug in the other.

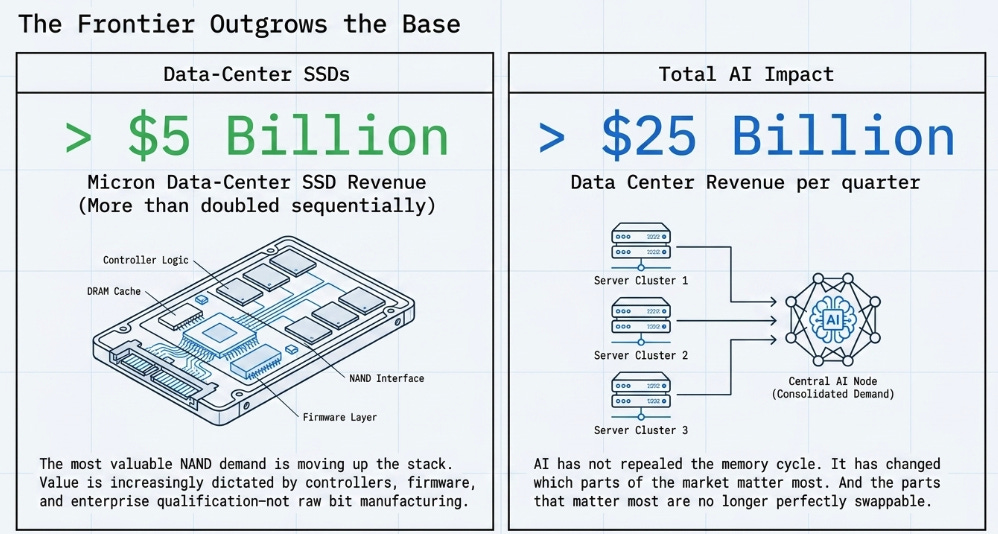

This matters because it changes the economics. The more memory becomes tied to accelerator design and customer qualification, the less it behaves like a spot commodity. The same logic extends to data-center SSDs: Micron’s data-center SSD revenue exceeded $5 billion and more than doubled sequentially. That is not proof NAND has become a franchise, but it is evidence that the most valuable NAND demand is also moving up the stack, toward controllers, firmware, and enterprise qualification.

AI has not repealed the memory cycle. It has changed which parts of the market matter most. And the parts that matter most are, for the first time, not perfectly swappable.

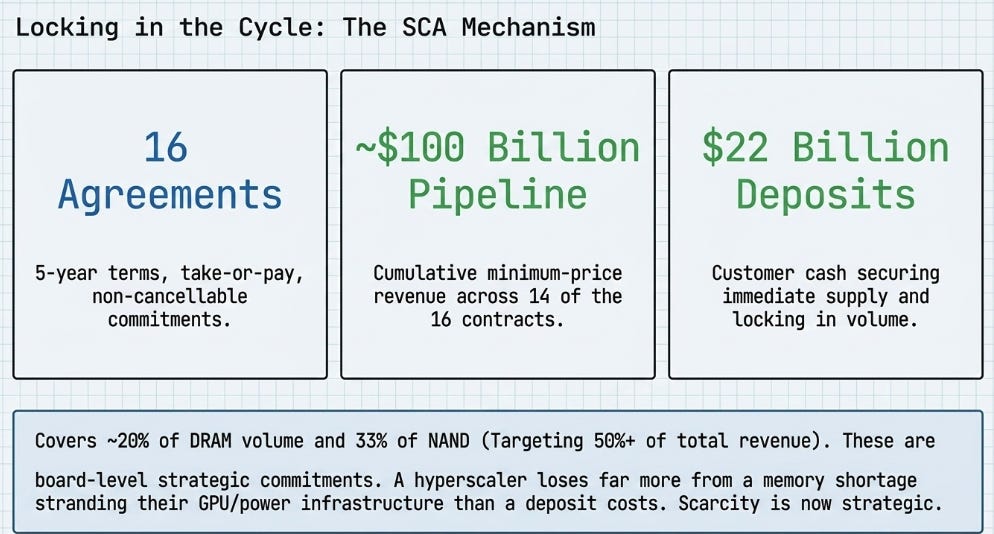

Sixteen Agreements

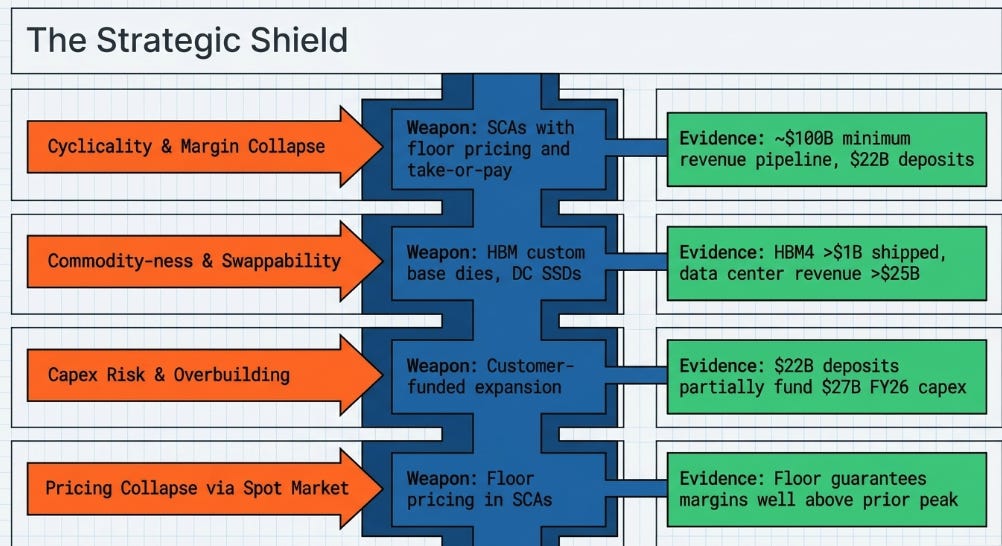

If swappability is weakening at the frontier, the SCAs are Micron’s attempt to address the other half of the problem: cyclicality.

Sixteen signed agreements. Five-year terms, take-or-pay, non-cancellable. Covering roughly 20% of DRAM volume and a third of NAND, with a target of half or more of total revenue. Fourteen of the sixteen carry cumulative minimum-price revenue of approximately $100 billion, supported by $22 billion of customer deposits and financial commitments. Management says the price floor enables margins “well above our peak quarterly margins in any past cycle.”

The coverage is incomplete. Twenty percent of DRAM volume is not transformation; it is the beginning of one. But the direction is unmistakable, and the most important evidence for the direction is not the contracts themselves, it is why the customers signed them.

Take-or-pay contracts with billions in deposits are not procurement decisions. They are board-level strategic commitments. A hyperscaler with GPUs, power infrastructure, and cloud demand lined up loses far more from a memory shortage than a deposit costs. The $22 billion is insurance against stranded infrastructure, a revealed preference about how these companies expect AI spending to evolve through 2030. When the largest technology companies in the world voluntarily lock into five-year purchase commitments at current pricing, that is a stronger demand signal than any analyst TAM forecast, because it has money behind it.

A contract is only useful if both sides have a reason to honor it. Micron wants earnings visibility. Customers want supply certainty. The agreements exist because scarcity has become strategic for both parties.

China Is The Clock

Here is where the story gets complicated, and where the market’s instinct is probably directionally right.

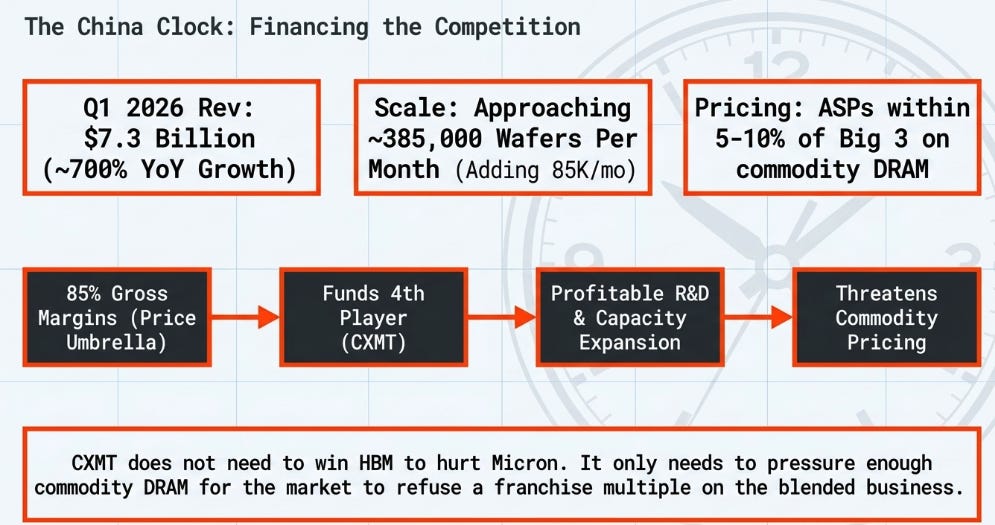

SemiAnalysis published a detailed analysis of CXMT the day before Micron’s earnings. The numbers were striking: Q1 2026 revenue of $7.3 billion with roughly 700% year-over-year growth, operating margins of approximately 70%, wafer capacity approaching Micron’s ~385,000 wafers per month, and ASPs within 5–10% of the big three on commodity DRAM. CXMT is adding roughly 85,000 wafers per month this year, the largest single-player ramp in the industry. HP is reportedly in discussions about sourcing CXMT chips for Asia-bound PCs.

I wrote about the strategic logic the same day. The big three’s discipline created a price umbrella: pricing so elevated that a fourth player can shelter underneath it profitably, funding its own R&D and capacity expansion from the rents the incumbents enabled. Maximum rent in hardware does not just attract competition, it finances competition. That is the unintended consequence of 85% margins.

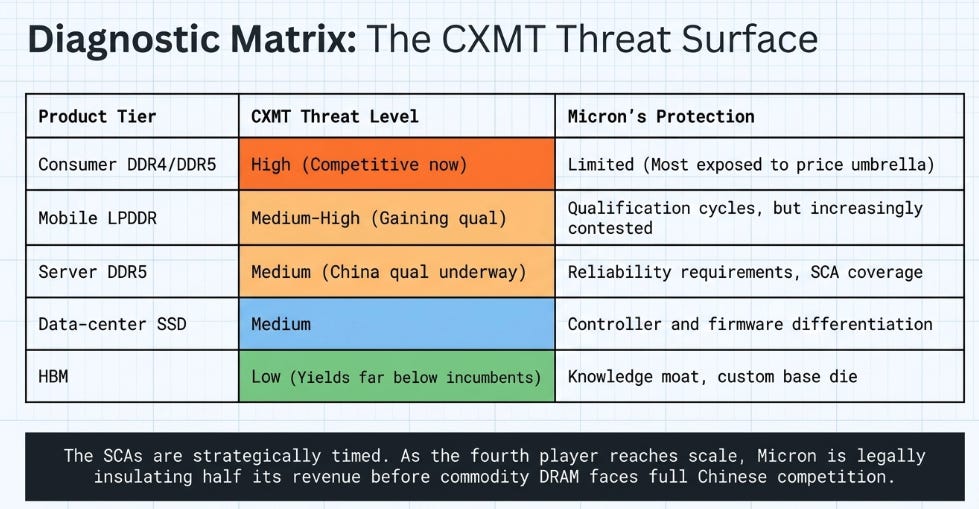

CXMT does not need to win HBM to hurt Micron. It only needs to pressure enough commodity DRAM for investors to refuse a franchise multiple on the blended business. The frontier is protected by a knowledge moat that took decades to build. But if 30–40% of Micron’s revenue faces real competition from a state-subsidized entrant, the market will cap the blended multiple regardless.

This is where the SCA timing reveals its real purpose. Micron disclosed sixteen agreements at the exact moment the fourth player is reaching competitive scale. The SCAs concede, implicitly, that commodity DRAM will face Chinese competition, and they ensure that when it does, half of revenue is contractually insulated. It is the legal solution to the problem that a criminal cartel could not solve in 2002, not because the law changed, but because scarcity flipped the leverage.

Notice what CFO Mark Murphy deflected on the call. When pressed for a hard FY27 capex number, he refused, conceding only that it would be above the mid-$40 billion range, then immediately pivoted to emphasize that more than half the increase would be construction, spending that takes years to produce bits. Management is acutely aware the market fears oversupply. The construction framing is their way of saying: this capex will not flood the market in FY27. Whether it floods the market in FY28 is the question they are not yet answering.

The Right Framework

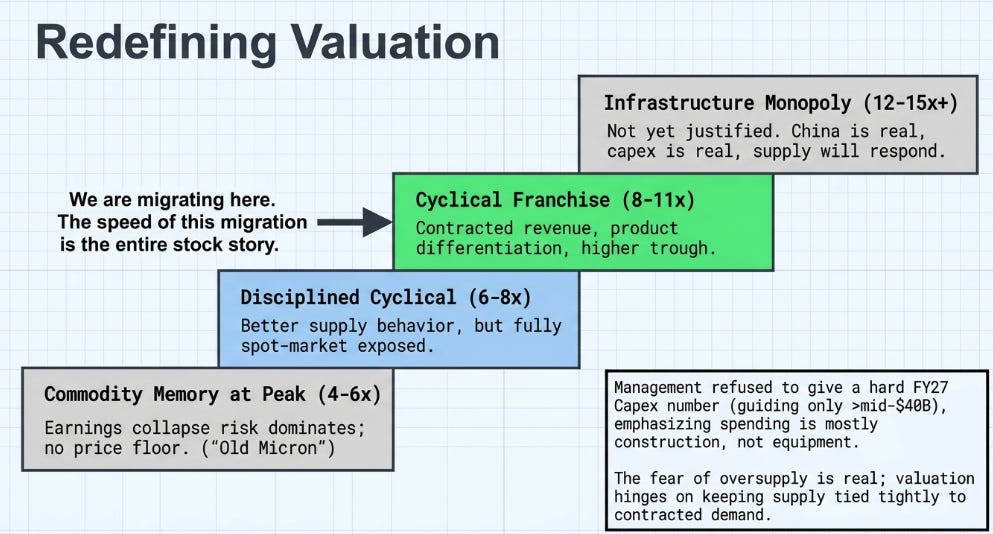

The valuation debate is not about whether Micron’s earnings are going up. That has already happened. The debate is about what kind of earnings they are, and how that determines the multiple.

Old Micron was the first row. If 85% margins are purely cyclical, then peak EPS of $175–200 at 4–6x gives you one range. If those same earnings are partially contracted, partially differentiated, and partially protected by floor pricing, then 8–11x on that earnings power gives you a very different one. The gap between those two frameworks is the entire stock.

The honest answer is that Micron is migrating from the first row toward the third, and the speed of that migration is what matters. The more revenue under SCAs, the more mix in HBM and data-center products, the more the trough rises and the more the multiple deserves to expand. The more revenue remains in spot-priced commodity DRAM, the more the old framework applies.

This is why “cyclical franchise” is the right category. Not an infrastructure monopoly, China is real, capex is real, memory supply will eventually respond. But also not the old book-value memory stock, if a meaningful and growing portion of earnings is contracted, prepaid, and tied to products customers cannot easily swap.

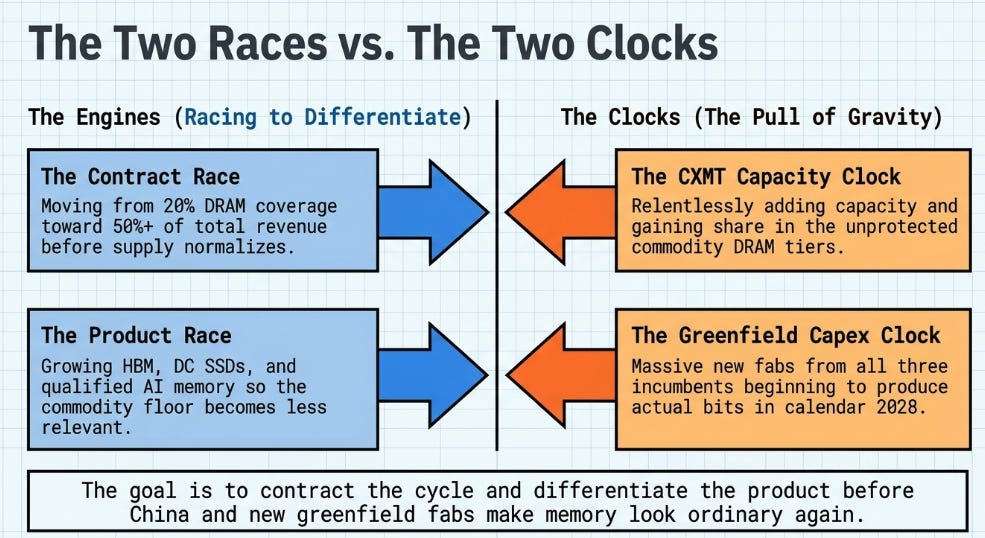

The Race

Micron is running two races against two clocks.

The contract race: from 20% DRAM coverage toward 50%+ of revenue before supply normalizes. Each SCA signed removes supply from the spot market and pushes remaining customers toward their own commitments. The mechanism is self-reinforcing, but at 20% it is a thesis, not a fact.

The product race: HBM, data-center SSDs, and qualified AI memory growing as a share of the business so the commodity floor becomes less relevant. Data center revenue already exceeds $25 billion per quarter. The frontier is growing faster than the base.

The clocks: CXMT adding capacity and gaining share in commodity DRAM. Greenfield fabs from all three incumbents beginning to produce bits in calendar 2028. The supply response is coming. It always does.

In 2002, memory executives broke the law to hold a price, and it did not work. In 2026, their customers are voluntarily locking in prices, depositing billions, and signing contracts they cannot exit. The structure that made the cartel necessary, perfect swappability, open standards, commodity economics, is fraying at the frontier, even as it persists at the floor.

Micron’s opportunity is to contract enough of the cycle, and differentiate enough of the product, before China and its own new fabs make memory look ordinary again. That is the race. This quarter’s evidence says Micron is ahead. The clock says the race is not over.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.