Microsoft 3QFY26 Earnings: Is AI a CIO Cycle or a User Cycle?

Microsoft's bull case is that enterprise context becomes the new OS. Microsoft's bear case is that the agent becomes the new OS.

TL;DR

Microsoft’s Q3 FY26 was strong, but the real debate is not capex or Azure growth; it is whether AI is a CIO-led cycle or a user-led cycle.

If Agent 365, Work IQ, Entra, and Purview become the default governance layer for enterprise agents, Microsoft can capture durable AI value even without owning every frontier model.

The risk is that Claude, ChatGPT, Cursor, or another AI-native agent owns the user intent layer, leaving Microsoft as essential middleware rather than the operating system of AI-era work.

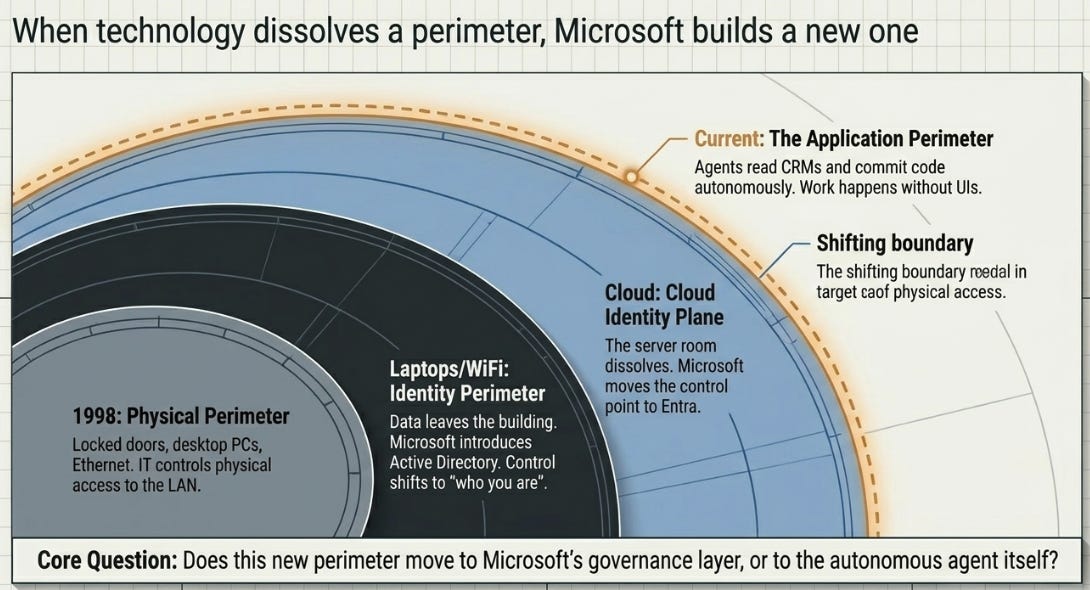

When the Perimeter Moves

In 1998, corporate security meant a locked door. Data lived on servers inside buildings, accessed through desktops connected by Ethernet cables. The IT department controlled security by controlling physical access to the local area network. Then laptops arrived with WiFi cards, and data started leaving the building every night in thousands of laptop bags. The physical perimeter dissolved.

Microsoft’s answer was not to fight the laptop. It was to move the perimeter. Active Directory shifted the control point from the building to the user’s identity. It no longer mattered where you were; what mattered was who you were. If you wanted to access the file server, you authenticated through Microsoft. The principle was elegant: when technology dissolves an old perimeter, don’t rebuild it. Build a new one at a different layer.

Cloud computing dissolved the next perimeter, the server room. Microsoft moved the control point again, to Entra and the enterprise cloud identity plane. And now agents are dissolving the application perimeter itself. When an autonomous agent reads your Salesforce database, updates your CRM, and commits code to GitHub without a human ever opening a UI, the application interface is no longer the control point. Work happens without anyone touching the software. The perimeter must move again.

The question, and it is the most important strategic question facing Microsoft, is whether the perimeter moves to Microsoft’s governance layer, or to the agent itself.

What We Got Right, and What We Missed

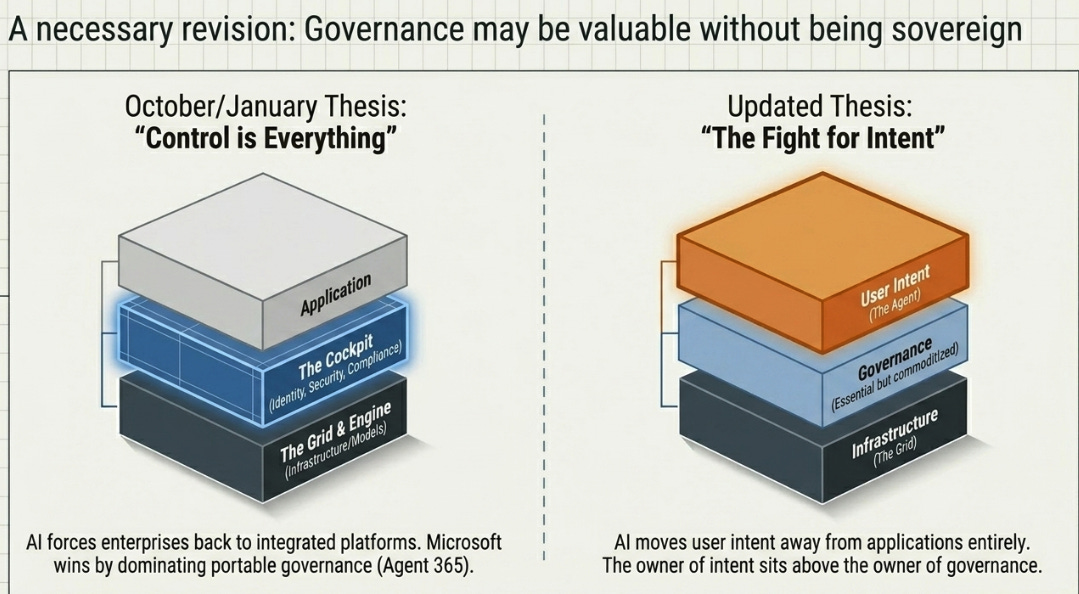

I have spent the past three quarters building a thesis about Microsoft and AI control. In October, I argued that AI’s “jagged intelligence” would force enterprises back toward integrated platforms. I introduced a three-layer framework, the Grid (infrastructure), the Engine (models), and the Cockpit (identity, security, compliance), and concluded that Microsoft would win by dominating the Cockpit. I titled the section “Control is Everything.”

In January, I extended the thesis. Agent 365 was not just integrated governance; it was portable governance. Microsoft’s bet was not that AI always runs on Azure, but that every enterprise agent must authenticate through Microsoft’s control plane. I compared it to Active Directory and concluded that the perimeter always moves but never disappears.

Those frameworks were not wrong. But they were incomplete. My prior thesis was that AI would move control from applications to governance. That still looks right. What I underweighted is that AI may also move user intent away from applications entirely, and if the agent owns intent, governance may be valuable without being sovereign.

What changed my mind was not an earnings print. It was watching Microsoft bring a competitor’s agentic technology into its own flagship product, and call it progress.

The Quarter: Strong Metrics, Wrong Debate

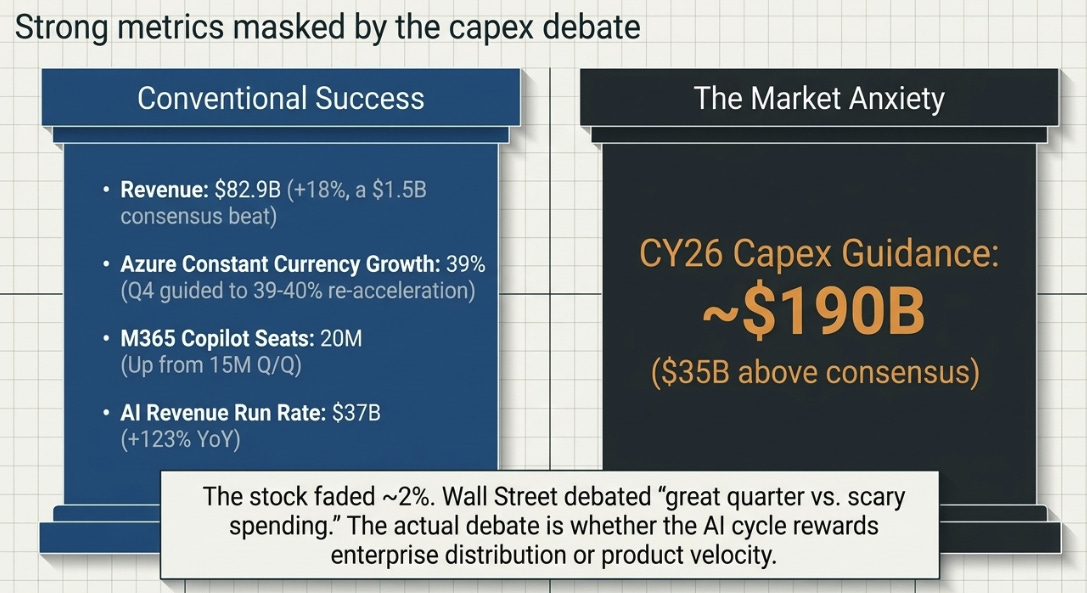

Microsoft’s Q3 FY26 results were excellent by any conventional measure. Revenue was $82.9 billion, up 18%, beating consensus by $1.5 billion. Azure grew 39% in constant currency, above the 37-38% guide, with Q4 guided to 39-40%, the first signal of re-acceleration. M365 Copilot paid seats crossed 20 million, up from 15 million the prior quarter. For the first time, Microsoft disclosed an AI revenue run rate: $37 billion, growing 123% year over year. Satya Nadella said Copilot’s weekly engagement has reached the same level as Outlook.

The stock faded roughly 2% because Microsoft guided calendar-year 2026 capex to approximately $190 billion, $35 billion above consensus. Wall Street’s debate became: great quarter versus scary spending. That is the stock analyst’s debate. The strategic debate is about something the earnings call surfaced but the market has not fully processed: whether the AI cycle rewards enterprise distribution or product velocity, and which one Microsoft actually has.

The Copilot Cowork Moment

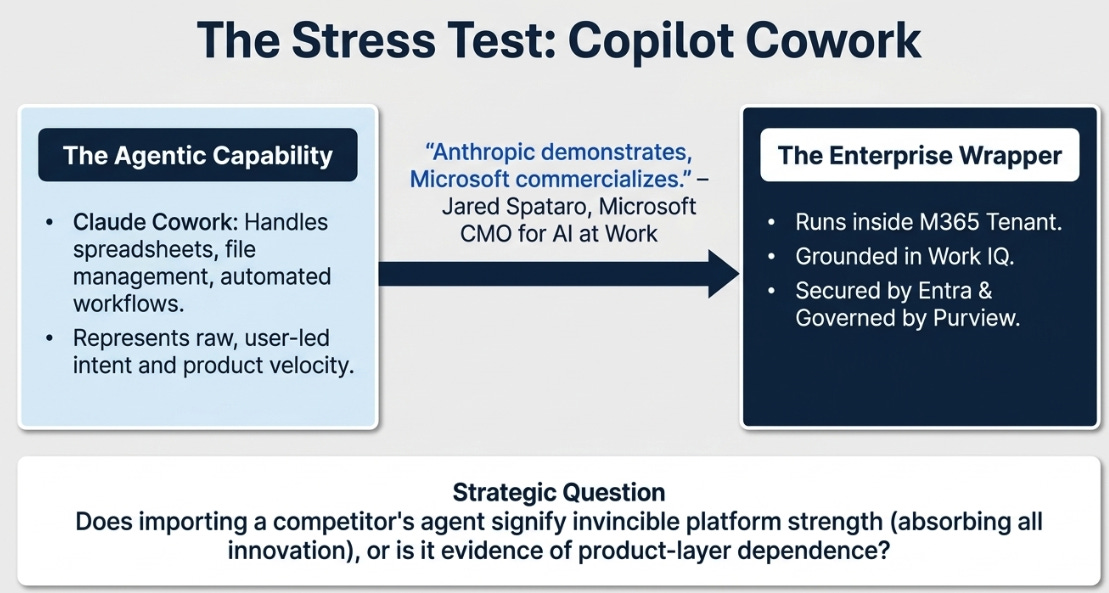

In January 2026, Anthropic launched Claude Cowork, an agentic tool for non-developers that handles spreadsheets, file management, reports, and automated workflows. The launch coincided with a sharp selloff in enterprise software stocks as investors recognized that Anthropic’s products looked a lot like traditional software and could replace much of the sector.

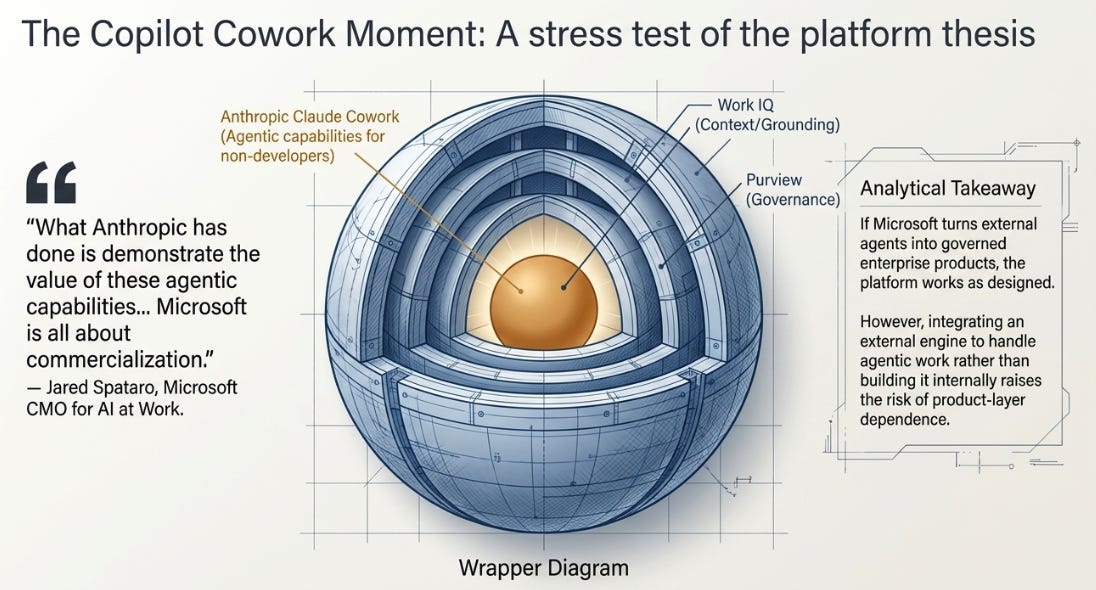

Seven weeks later, on March 9, Microsoft launched Copilot Cowork. Microsoft’s own blog described it as integrating “the technology platform that powers Claude Cowork” into Microsoft 365 Copilot. The enterprise version runs inside a customer’s Microsoft 365 tenant, grounded in Work IQ, secured by Entra, governed by Purview. According to Fortune’s reporting, Microsoft’s CMO for AI at Work, Jared Spataro, called Anthropic’s offering “a fantastic tool” and said: “What Anthropic has done is demonstrate the value of these agentic capabilities and show us practically what it could look like. Microsoft is all about commercialization.”

This is not a disproof of Microsoft’s platform thesis. It is the cleanest possible stress test of it.

If Microsoft can turn every external agent innovation into a Microsoft-governed enterprise product, then importing Anthropic is not weakness, it is the platform working as designed. Microsoft adds identity, compliance, Work IQ context, and enterprise data protection. The agentic capability becomes safe for the Fortune 500. That is a powerful value proposition.

But the implication of Spataro’s framing, Anthropic demonstrates, Microsoft commercializes, captures a division of labor that should make long-term investors uncomfortable. Microsoft, with exclusive OpenAI access since 2019, $190 billion in annual AI capex, and 450 million M365 users, did not build the agentic work product first. It integrated someone else’s. The question is whether that pattern reflects platform strength or product-layer dependence.

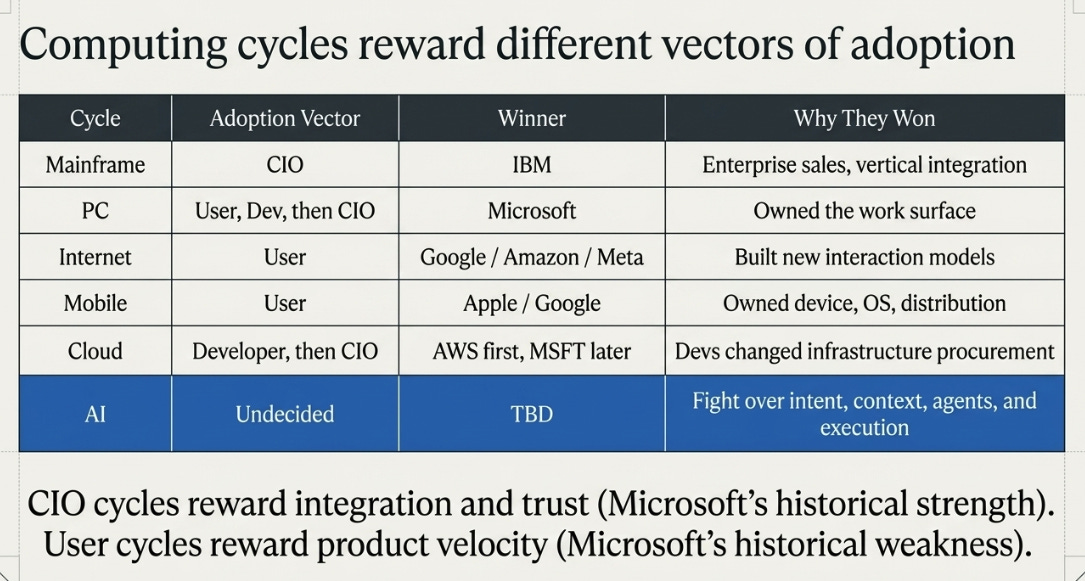

Is AI a CIO Cycle or a User Cycle?

Every major computing cycle is ultimately a fight over the default interface, the surface where users express intent.

CIO cycles reward integration, distribution, and enterprise trust. User cycles reward product velocity and new interaction models. Microsoft wins the first kind. It historically loses the second.

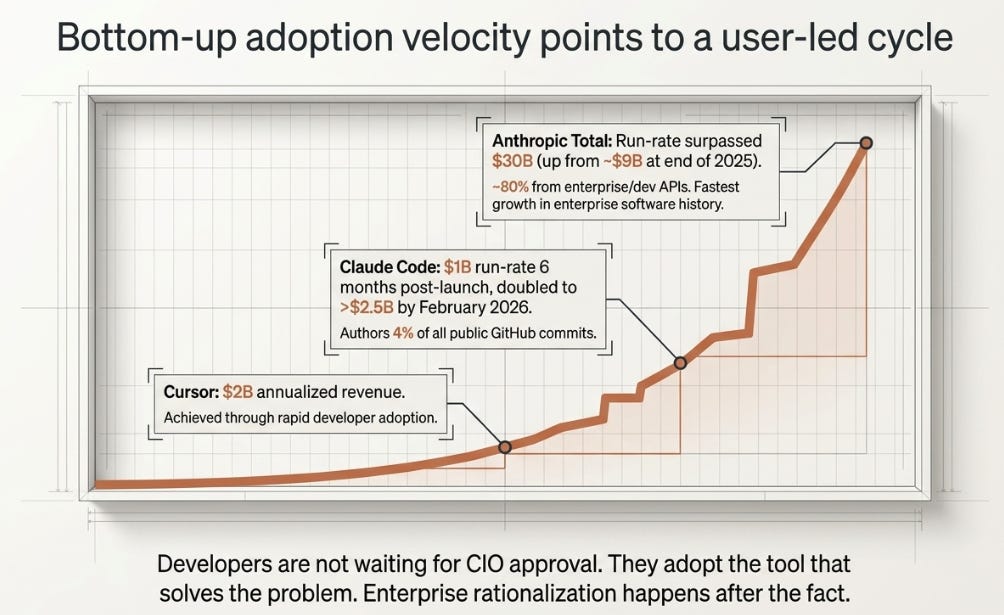

The evidence from the past eight months suggests AI is behaving like a user cycle at the product layer. Anthropic reported that its run-rate revenue has surpassed $30 billion, up from approximately $9 billion at the end of 2025, the fastest growth trajectory in enterprise software history, with roughly 80% coming from enterprise and developer API usage. Claude Code, which Anthropic said reached $1 billion in run-rate revenue just six months after public launch, had more than doubled to over $2.5 billion by February 2026. Developer surveys suggest Claude Code has overtaken GitHub Copilot in professional usage, with substantially higher satisfaction scores. One analysis estimated that 4% of all public GitHub commits are now authored by Claude Code. Cursor, another AI-native coding tool, reportedly reached $2 billion in annualized revenue.

Developers did not wait for CIO approval. They adopted the tool that solved the problem. Enterprise followed. This is what a user cycle looks like: bottom-up adoption, product quality as the selection criterion, enterprise rationalization after the fact.

If Context Is the OS, Microsoft Wins

Microsoft’s strongest argument is not about Copilot-the-chatbot or Azure-the-infrastructure. It is about enterprise context as a structural moat.

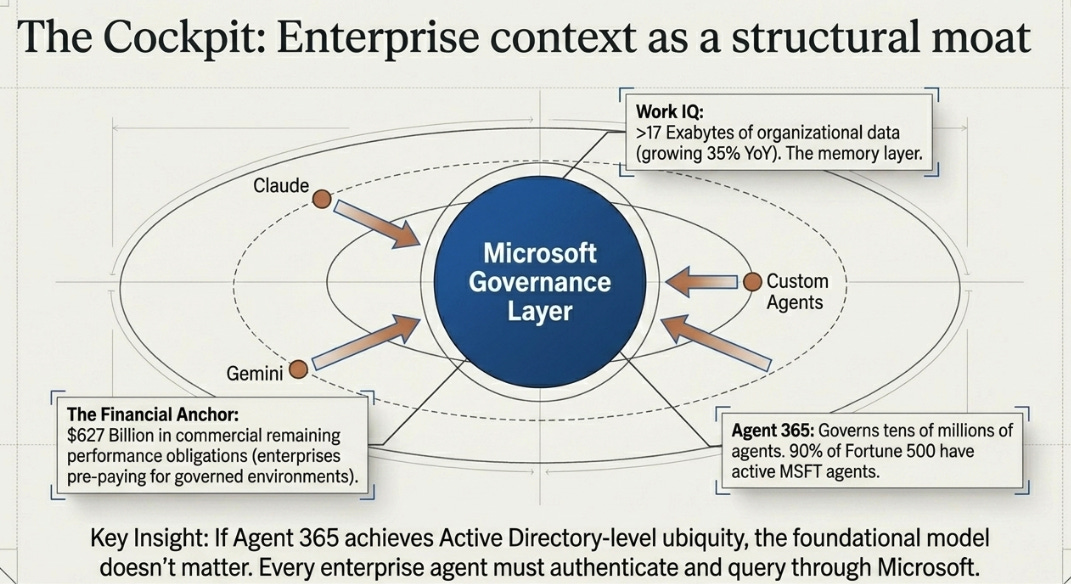

AI agents need organizational context to be useful in enterprise settings. They need permissions, identity, organizational memory, audit trails, and policy enforcement. Microsoft owns that context layer. Work IQ spans more than 17 exabytes of organizational data, growing 35% year over year. Agent 365 governs tens of millions of agents across tens of thousands of companies. Ninety percent of the Fortune 500 have active agents built with Microsoft’s tools. The $627 billion in commercial remaining performance obligations represents enterprises pre-paying for governed AI environments.

If Agent 365 achieves Active Directory-level ubiquity, then it does not matter whether developers prefer Claude Code or whether ChatGPT has a better consumer experience. Every agent that operates inside an enterprise must still authenticate through Microsoft, query Microsoft’s context layer, and comply with Microsoft’s governance. The Copilot Cowork launch demonstrates exactly this: Anthropic provides the agentic capability, but the enterprise version runs inside Microsoft 365’s tenant, wrapped in Work IQ and enterprise data protection.

The strongest bull reading is that Microsoft can absorb the best agents. The model doesn’t matter. The agent doesn’t matter. The context and governance layer, the new Cockpit, is what matters.

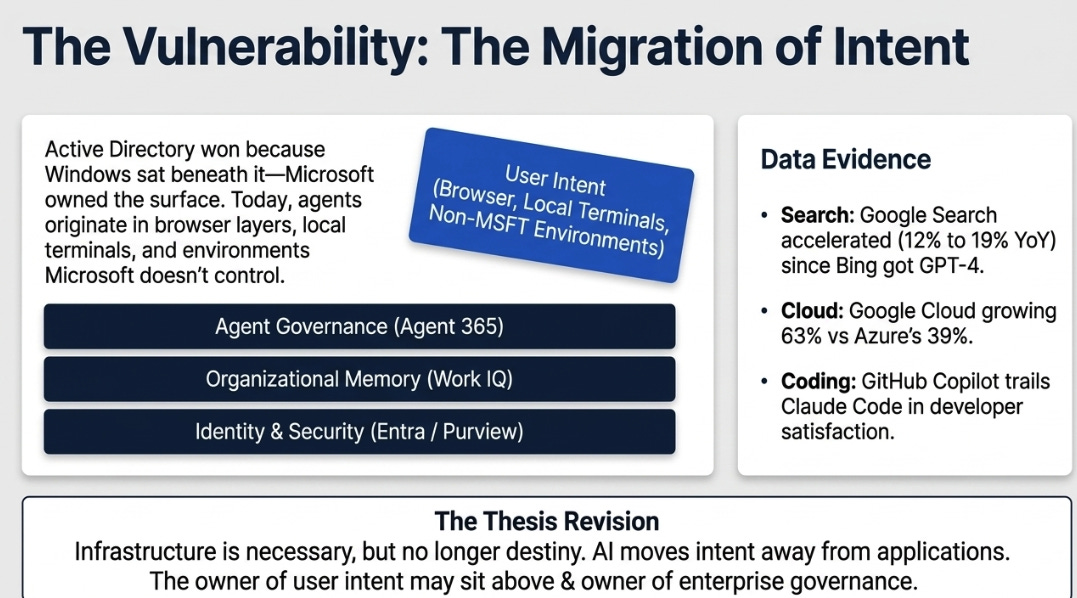

But there is a historical echo worth noting. Active Directory had Windows beneath it. Microsoft controlled the desktop operating system, which meant it controlled the surface that applications ran on. Agent 365 may not have the equivalent advantage. Agents can originate in Claude, ChatGPT, Gemini, Cursor, local terminals, browser layers, or future environments Microsoft does not control. Can governance achieve ubiquity without owning the surface beneath it? That is the open question.

The Product Layer Problem, A Thesis Revision

This is where I need to revise my own framework. In January, I wrote that “the Cockpit can win even if other layers face pressure.” I still think that is directionally right. But the evidence since January has accumulated in a pattern I can no longer dismiss as noise.

In every product category where Microsoft had an AI first-mover advantage, search, coding, enterprise productivity, consumer AI assistant, it has either lost the product lead or failed to convert the head start into dominance. Google Search revenue has accelerated from 12% to 19% year-over-year growth since Bing got GPT-4, based on Fiscal.ai data from SEC filings, Google Cloud is growing 63% versus Azure’s 39%, with Google Cloud margins expanding while Microsoft’s compress. GitHub Copilot, with a four-year head start, now trails Claude Code in developer satisfaction surveys. And when the defining agentic work product appeared, Microsoft’s response was to integrate it rather than build it.

Fifteen months ago, I titled an article “Infrastructure as Destiny.” I am no longer sure that is right. Infrastructure is necessary. Whether it is destiny depends on whether the user surface forms inside Microsoft’s products or outside them. Microsoft is not at risk of missing AI revenue. It is at risk of missing AI sovereignty, the ability to set the terms of how AI-era work gets done rather than merely facilitating it.

We were right that AI dissolves the application perimeter and makes governance more valuable. What we may have missed is that AI also moves intent away from applications, and the owner of intent may sit above the owner of governance.

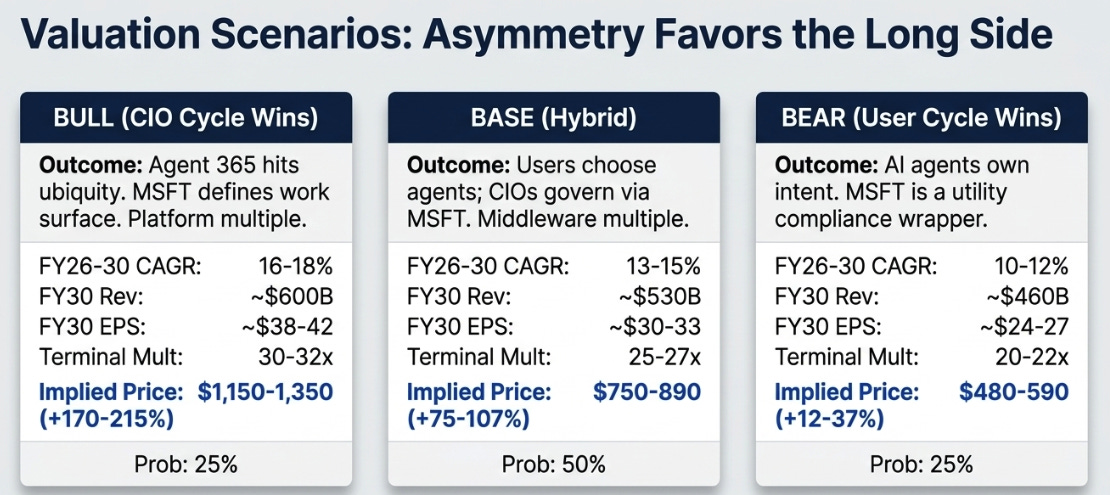

Three Scenarios for Microsoft’s AI Future

The strategic question maps to three distinct outcomes, each with different implications for what Microsoft is worth.

The observation that matters: even the bear case has meaningful upside from $430. At 24x forward earnings, the stock is priced closer to the bear scenario than the base. The market has already discounted the capex risk and competitive pressure. What it has not priced is the possibility, still the most likely outcome, that Microsoft’s governance layer captures durable value even if it does not define the era. The asymmetry favors the long side. But the type of return differs across scenarios: the bull is a platform compounder that re-rates to 30x; the base is a steady mid-teens grower that normalizes to 26x; the bear is a utility generating excellent cash flow at a compressed multiple.

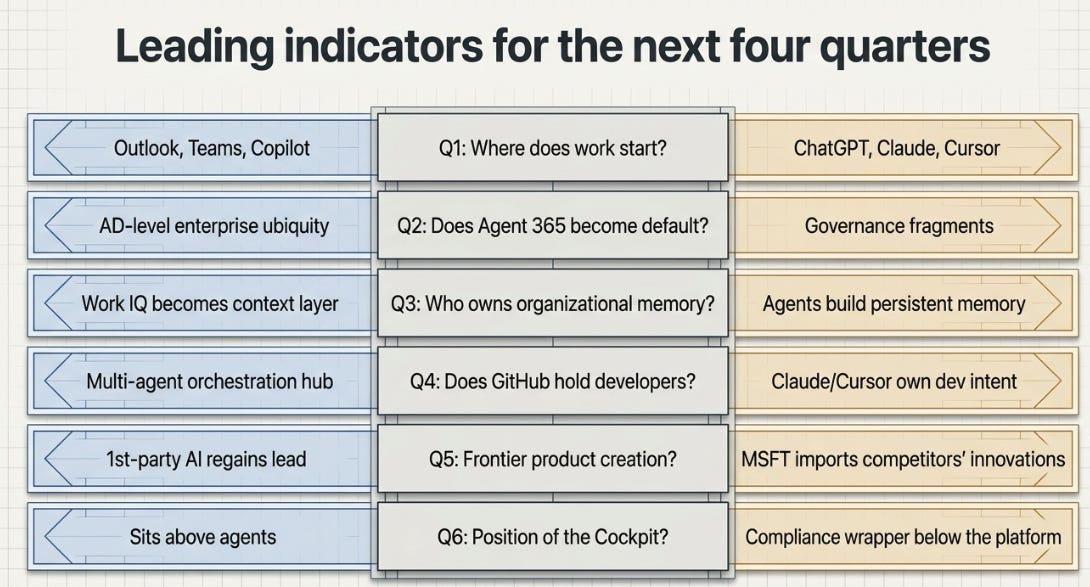

The Perimeter Always Moves

Six things will determine which scenario unfolds, not Azure growth in isolation, not quarterly EPS, but the questions that separate platform ownership from profitable participation.

The perimeter always moves. It never disappears. For the past year, I have been confident that the next perimeter is Microsoft’s governance layer, that control would migrate from applications to identity, compliance, and context, and that Microsoft would own it the way it owned Active Directory.

I still believe governance is a massive and durable business. Microsoft’s enterprise distribution, identity infrastructure, and organizational context layer are assets no competitor can replicate quickly. The most likely outcome is that Microsoft captures enormous value from the AI cycle through this control layer.

But I now take seriously the possibility that governance is not the operating system of the AI era, it is the middleware. The operating system may be the agent itself: the AI that users form a relationship with, that remembers their work, that executes on their behalf, that improves over time. If that agent is Claude, or ChatGPT, or something that has not been built yet, then Microsoft’s governance layer becomes essential infrastructure wrapped around someone else’s platform, the way IBM wrapped enterprise relationships around an operating system it did not own.

The distinction between governance as the operating system and governance as middleware is the difference between Microsoft setting the terms of the AI era and Microsoft merely participating in it. Copilot Cowork, integrating Anthropic’s agentic technology inside Microsoft 365’s governance boundary, is what that distinction looks like in practice. It may be exactly how Microsoft wins. It may also be evidence that the agent layer is being invented somewhere else.

The next four quarters will tell us which one it is.

$MSFT

General Disclaimer: The information presented in this communication reflects the views of the author and does not necessarily represent the views of any other individual or organization. It is provided for informational purposes only and should not be construed as investment advice, a recommendation, an offer to sell, or a solicitation to buy any securities or financial products.

While the information is believed to be obtained from reliable sources, its accuracy, completeness, or timeliness cannot be guaranteed. No representation or warranty, express or implied, is made regarding the fairness or reliability of the information presented. Any opinions or estimates are subject to change without notice.

Past performance is not a reliable indicator of future performance. All investments carry risk, including the potential loss of principal. This communication does not consider the specific investment objectives, financial situation, or particular needs of any individual.

The author and any associated parties disclaim any liability for any direct or consequential loss arising from the use of this material and undertake no obligation to update or revise it.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.