Netflix 2Q26: The Compounding Nobody Wants

Revenue growth is slowing. The value of each member relationship is rising. The market has decided only the first fact matters.

TL; DR

Netflix’s revenue growth is slowing as free, infinite content from YouTube and short-form platforms competes for attention, but the underlying business remains operationally strong.

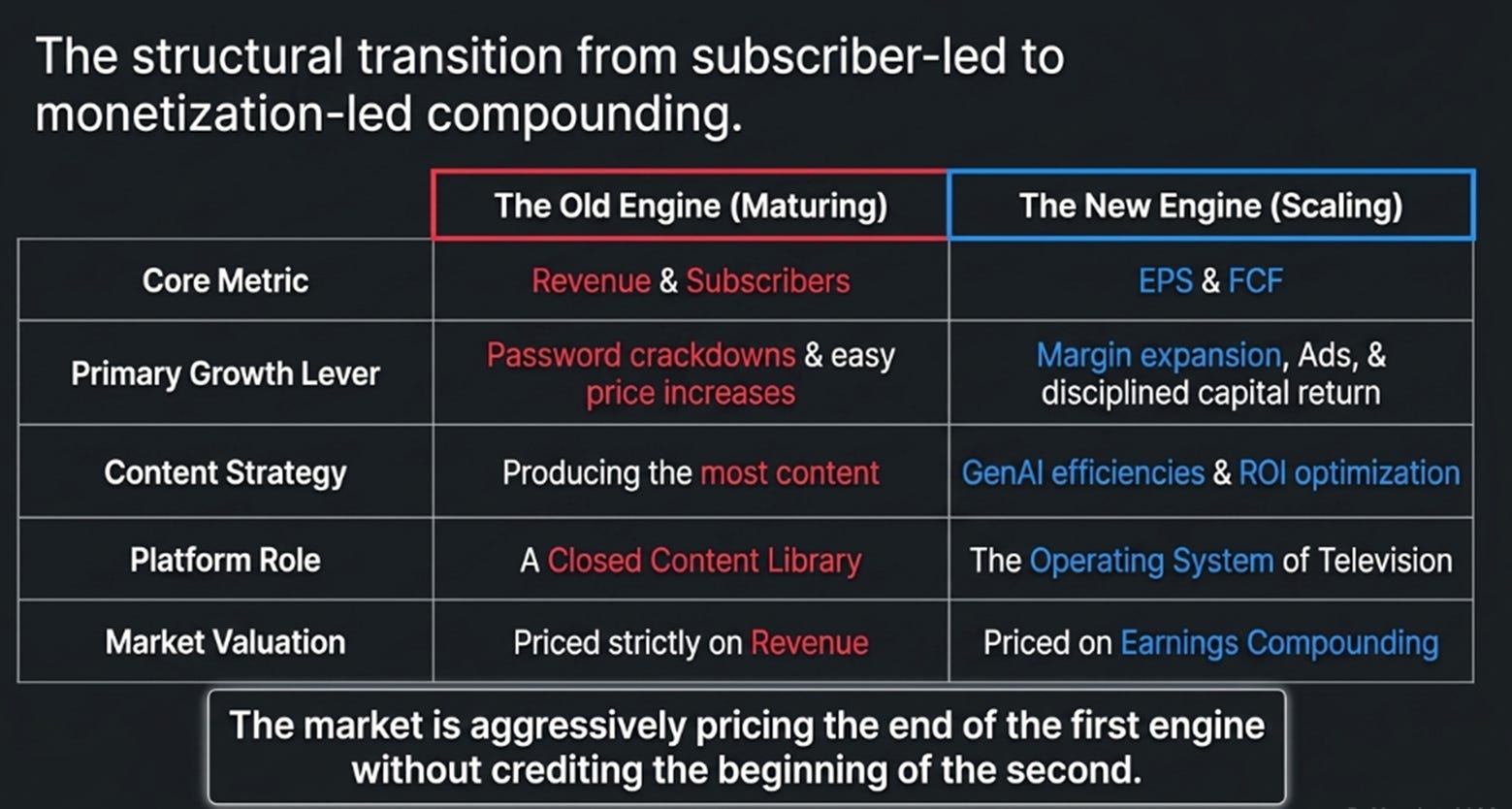

The next phase of compounding will come from higher margins, advertising, pricing and buybacks; not rapid subscriber growth with EPS capable of growing faster than revenue.

The overlooked upside is Netflix becoming the interface for television: the TF1 integration offers an early template for aggregating third-party content, broadcasters and advertisers inside Netflix itself.

What We Said, and What Happened

Before the quarter, we argued Netflix was being mispriced as a decelerating media company when it was a scaling dual-revenue platform early in its most significant business model transition since DVDs to streaming. We predicted an ambiguous print, beats on some metrics, misses on others.

We were right about the scenario and wrong about the magnitude.

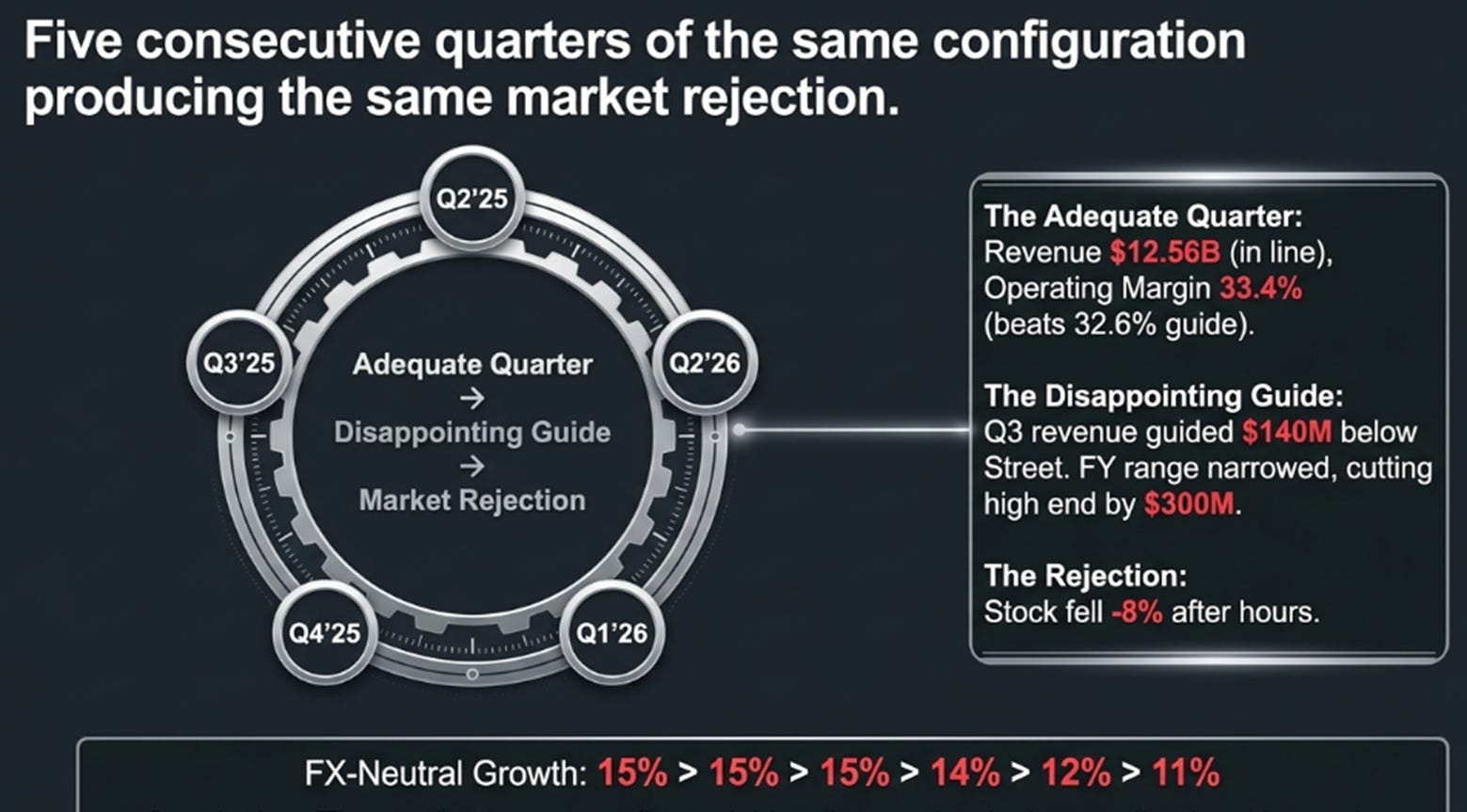

Revenue of $12.56 billion was essentially in line with guidance and consensus. Operating margin of 33.4% beat the 32.6% guide. Engagement hours grew 2% in the first half, accelerating from 1.5% in 2025. Netflix repurchased $4.7 billion of stock, its largest quarter ever. Management said they were “primarily builders, not buyers.” Every operational indicator was stable to improving.

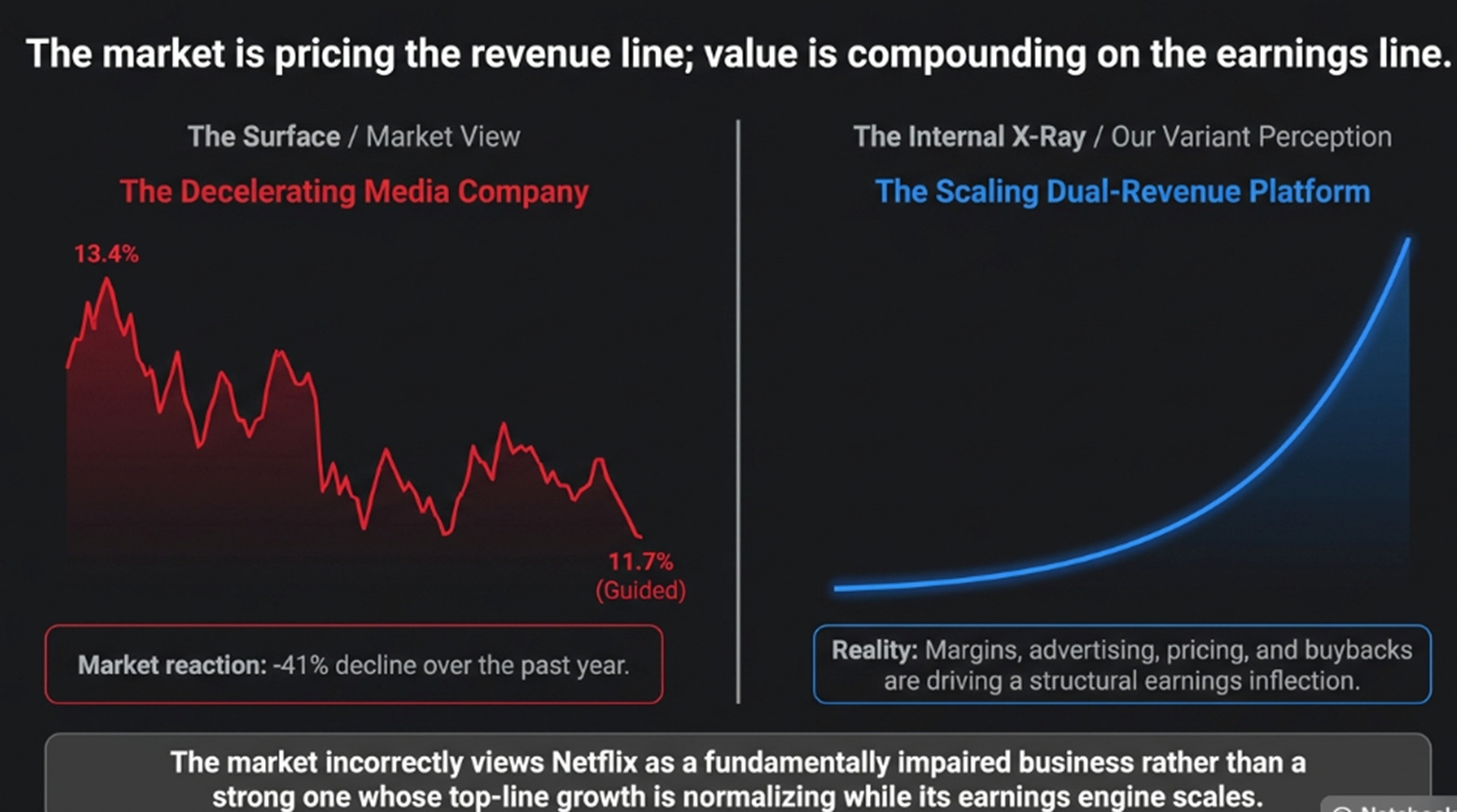

The stock fell 8% because Q3 guidance of $12.86 billion came in roughly $140 million below Street expectations, and the full-year range was narrowed from $50.7–$51.7 billion to $51.0–$51.4 billion, cutting the high end by $300 million. Growth decelerates from 13.4% to a guided 11.7%.

This is the fifth consecutive quarter in which the same configuration, adequate quarter, disappointing guide, produced a negative reaction (Q2’25, Q3’25’s -10%, Q4’25, Q1’26’s roughly -8%, now -8% after hours). Five occurrences isn’t coincidence; it’s the market repeatedly rejecting the same earnings configuration. The question is whether that rejection signals a fundamentally impaired business, or a fundamentally strong one whose growth is normalizing faster than the market will accept. We believe the second, but we owe an account of why the first keeps finding evidence.

The deceleration is worse than we projected. FX-neutral growth has declined on a nearly mechanical schedule, 15%, 15%, 15%, 14%, 12%, 11%, a point evaporating every quarter or two. Our prep assumed stabilization in Q3. It didn’t come, and our $13.05 billion Q3 bogey looks generous in hindsight.

We got the operational quality right. We got the growth trajectory wrong. The relationship between those two facts is the article.

The Tax on Attention

Netflix’s growth is not decelerating because the business is broken. It is decelerating because Netflix won a war and discovered the territory it conquered is shrinking relative to the broader battlefield.

Netflix dominates subscription streaming. Disney+ is smaller and less profitable, Prime Video is bundled, Paramount and Warner Bros. Discovery are merging to survive. Netflix won. But subscription streaming is a category within the attention economy, not the attention economy itself, and that larger market is being reorganized by platforms with fundamentally different architectures.

YouTube now commands roughly 10% of US television viewing time; Netflix has about 9%. A mobile-first, user-generated platform came to the living room screen, and suddenly infinite free content with zero marginal production cost and algorithmic personalization was competing directly for the hours Netflix built its business to own. TikTok, Reels, and Shorts capture billions of daily hours from the cohorts that represent Netflix’s growth runway, charging nothing, requiring no decision about what to watch. The friction of choosing, which Netflix spent a decade reducing, has been eliminated entirely by competitors who serve content with zero user input.

Netflix’s growth isn’t slowing because the product is getting worse. It’s slowing because the supply of competing entertainment has become functionally infinite, and most of it is free.

The engagement data reveals the tension if you do the math Netflix no longer makes easy. Total view hours grew 2% in the first half. Netflix stopped disclosing membership figures in early 2025, but if external estimates of mid-to-high single-digit subscriber growth are directionally right, the base grew meaningfully faster than viewing, implying viewing per membership is under pressure.

Netflix won’t confirm this. Instead, Co-CEO Greg Peters offered a reframing both strategically sound and strategically convenient: “There is not a linear relationship between view hours and revenue and profit, because all hours are not created equal.” He’s right, live events consume 5% of content spend and generate 1% of hours, yet produced six of the ten largest sign-up days in five years. But it is also the kind of argument a company introduces when the simple metric is moving against it. When hours per subscriber were growing, Netflix never needed to explain why some hours are worth more than others.

The Response Worth Watching

The Q2 initiatives are best understood as a coordinated response to this pressure, each addressing a specific vulnerability in how Netflix captures time. Short form deals with BuzzFeed, Condé Nast, and Hearst import the format that competes with it. Video podcasts target daytime and mobile, where Netflix under-indexes. The expanded NFL deal secures the highest-value appointment viewing on the calendar. Cloud gaming captures interactive attention. All reasonable; not transformative.

The move that deserves the most attention is getting the least.

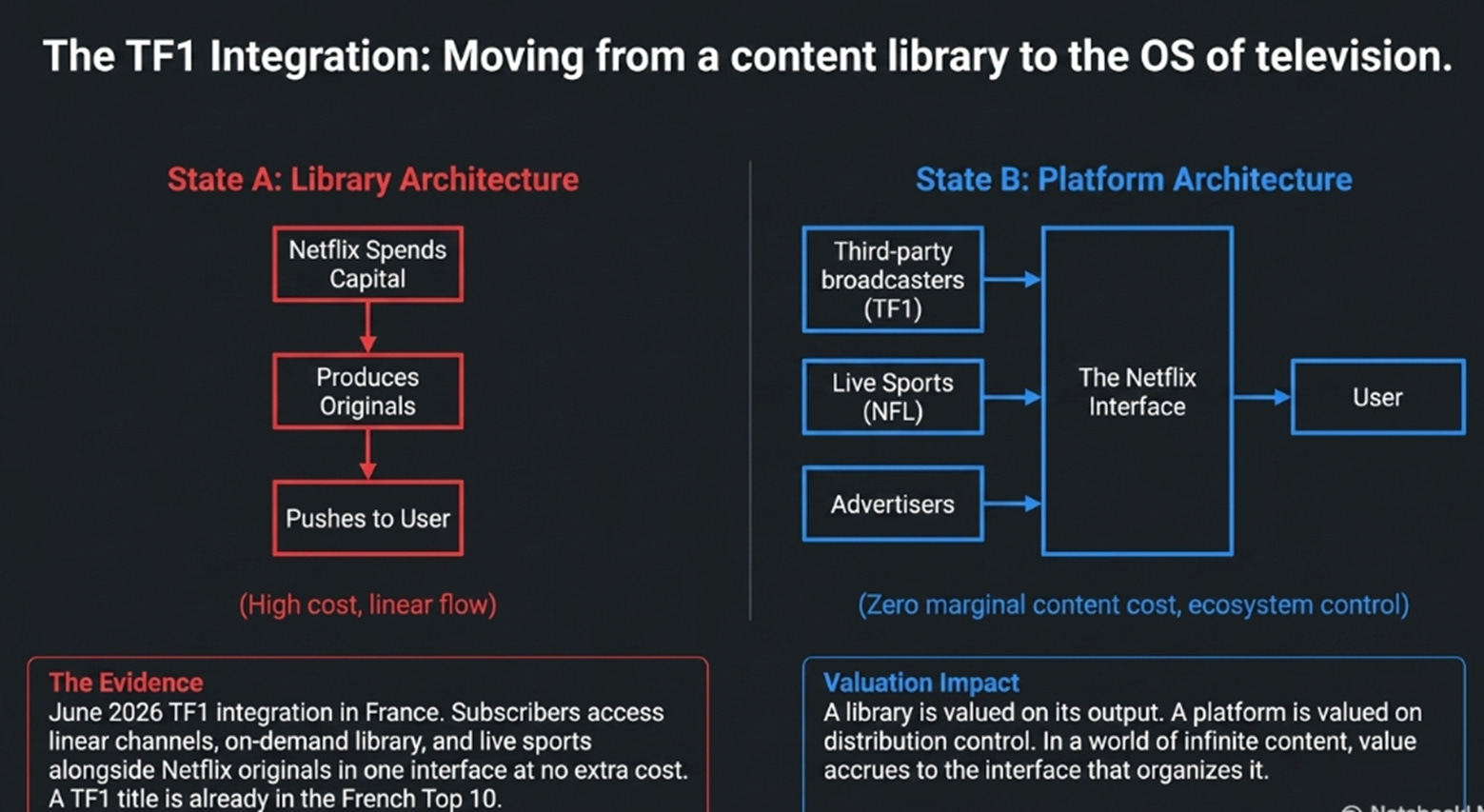

In June, Netflix integrated TF1, a major French broadcaster, directly into its app. French subscribers now access TF1’s linear channels, on-demand library, and live sports alongside Netflix originals, in one interface, at no extra cost. TF1 viewing has grown each week since launch; a TF1 title has already reached Netflix’s French Top 10.

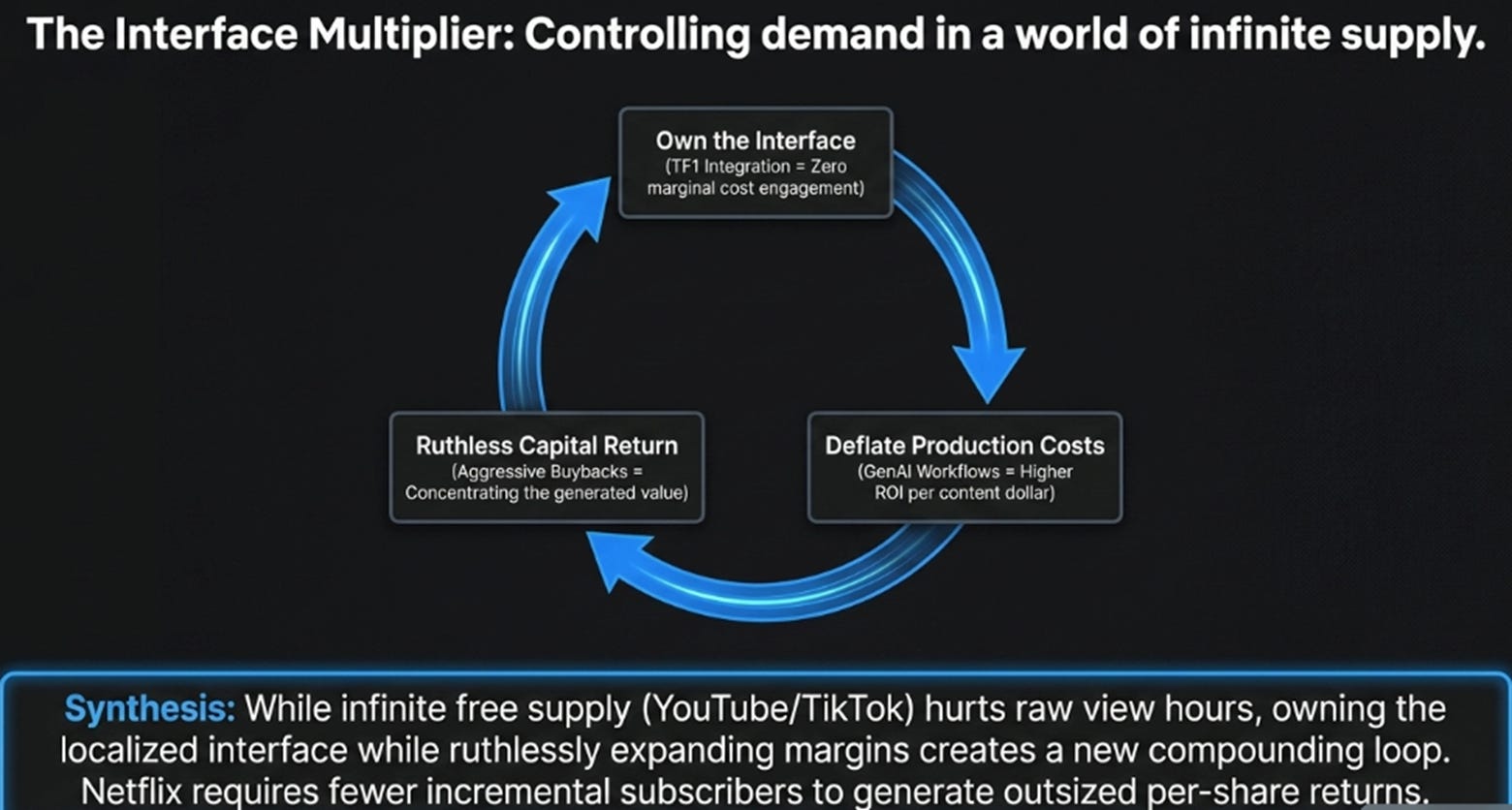

This is not a content deal. It is a platform play. Netflix supplies distribution, discovery, billing, and product; the partner supplies programming and local relevance. If the model scales, local broadcasters in each major market feeding content into the Netflix interface, the company transforms from content library into the operating system of television. That distinction matters enormously for valuation: a library is valued on its output; a platform on its distribution control and its ability to intermediate between creators, viewers, and advertisers.

Netflix is not there yet. But TF1 is the first evidence management is thinking in platform terms, and the attention economy demands it. In a world of infinite content supply, value accrues to whoever controls the interface that organizes it, not whoever produces the most of it.

The Disclosure Question

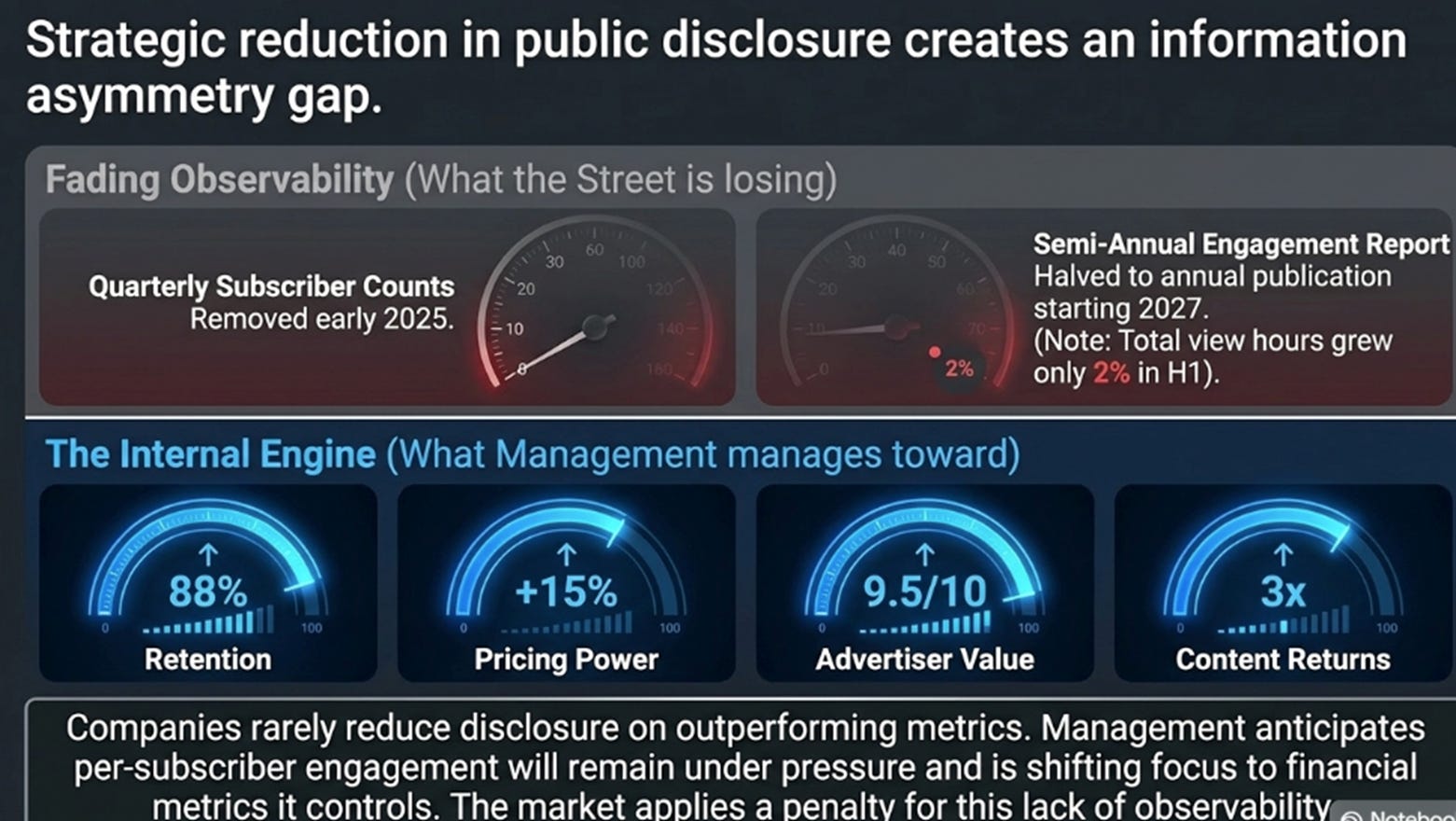

One aspect of the quarter requires direct acknowledgment. Netflix has removed two key non-financial metrics from regular reporting in eighteen months: quarterly subscriber counts (early 2025) and now the semi-annual engagement report, which shifts to annual publication from 2027, separated from earnings. Both changes were framed as refocusing on “primary financial metrics.” There are legitimate reasons, as monetization diversifies across plans, pricing, and advertising, raw subscriber and hour count genuinely become less representative of economic value.

But a pattern is worth naming: companies rarely reduce disclosure on metrics that are outperforming. Subscriber disclosure ended after subscriber growth normalized. Engagement disclosure is being halved after engagement growth slowed to 2%. Two for two. Management also declined to share the internal quality metrics that now anchor its engagement framework, citing competitive sensitivity.

The net effect: investors are asked to trust a framework they cannot verify, now it replaces observable data. We don’t think Netflix is hiding a collapse; the current data are reassuring. We think management anticipates per-subscriber engagement will stay under pressure and is preemptively shifting the conversation to metrics it controls. That’s rational. It’s also information asymmetry investors should price. The flywheel doesn’t break because hours per member decline; it breaks when declining attention weakens retention, pricing power, advertiser value, or content returns, and those are becoming harder to observe from outside.

The Compounding the Market Ignores

Here is what we think the market is not calculating.

Revenue growth is decelerating, accept that. Membership growth slows from roughly 6% to 3–4% by FY29 as acquisition matures; pricing adds a stable 3–4%; ad revenue, which needs to reach $6–7 billion by FY29, is the only force preventing a slide into single digits. The question is whether revenue growth is the right measure of value creation, or whether per-share earnings growth, margin expansion, capital return, ad mix, is the more relevant metric.

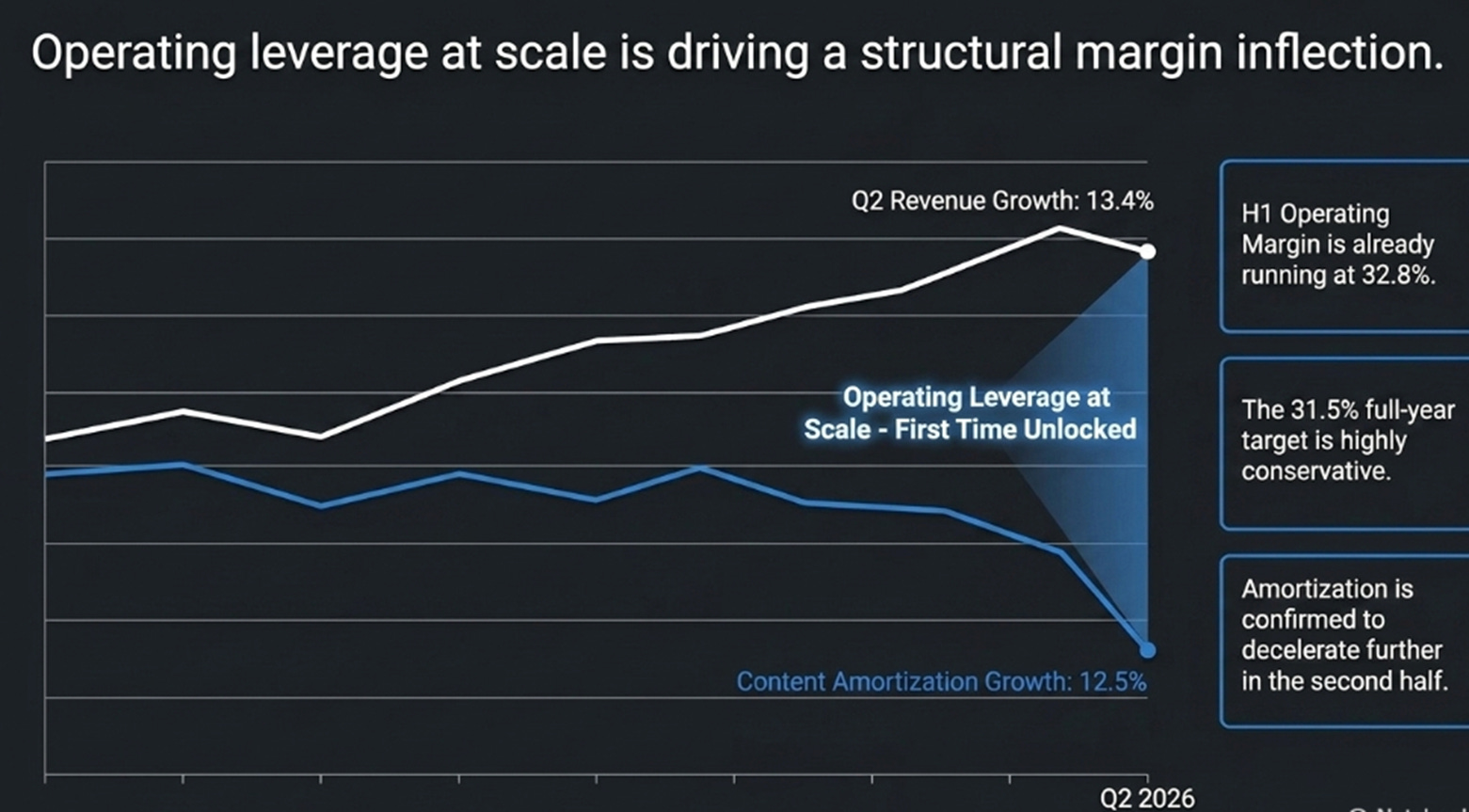

The margin inflection is real. Content amortization grew 12.5% in Q2 against revenue growth of 13.4%, a small gap with large significance: operating leverage on the biggest cost line, for the first time at scale. Management confirmed amortization decelerates further in the second half. The 31.5% full-year target is almost certainly conservative; the first half is already running at 32.8%.

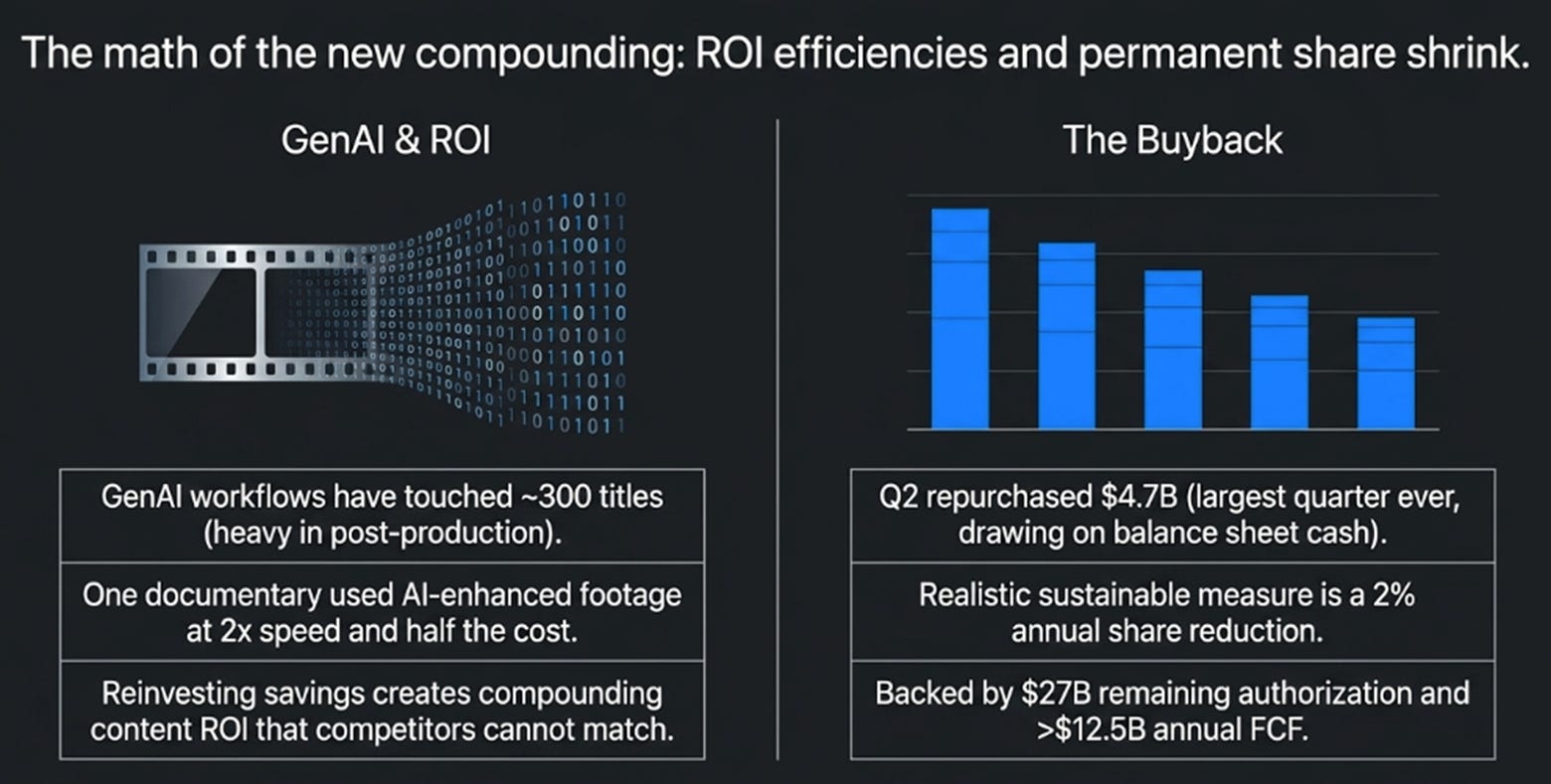

GenAI improves the return on every content dollar even if it never cuts the budget. GenAI workflows have touched roughly 300 titles, heaviest in post-production; one documentary produced AI-enhanced footage at twice the speed and half the cost. Management will reinvest the savings, not harvest them. The honest framing is not a quantifiable margin lever, the evidence is one anecdote, but improving content ROI, backed by proprietary production tools competitors can’t match.

The buyback is meaningful but should not be annualized. Q2’s $4.7 billion, the largest ever, exceeded quarterly free cash flow and drew on balance-sheet cash opportunistically. The realistic measure: diluted shares fell roughly 2% year over year, net of stock compensation. A sustainable 2% annual reduction, backed by $27 billion of remaining authorization and $12.5 billion-plus of annual free cash flow, adds roughly two points to per-share earnings growth. Permanent, compounding, unglamorous.

Together, high-single-digit revenue growth, margins moving toward the high 30s, a gradually shrinking share count, Netflix can plausibly compound EPS in the low-to-mid teens even as revenue settles near 9–10%. The market prices Netflix on the revenue line. The value compounds on the earnings line. These are different things.

Where We Stand

Our variant perception is narrower than before the quarter, but intact.

Consensus sees a maturing streamer decelerating toward single-digit growth, with engagement under structural pressure from YouTube and short-form video. The -41% decline over the past year reflects that view. We see structurally inflecting margins, improving content economics, disciplined capital return, and a nascent platform strategy the market credits at zero. At roughly 18x pre-revision FY27 earnings, the market has already assigned Netflix a materially lower growth classification. What the price doesn’t reflect, in our view, is the durability of the earnings compounding, whose sources are more within management’s control than the revenue line the market is fixated on.

Stated precisely: Netflix is transitioning from subscriber-led compounding to monetization-led compounding, and the market is pricing the end of the first without crediting the beginning of the second.

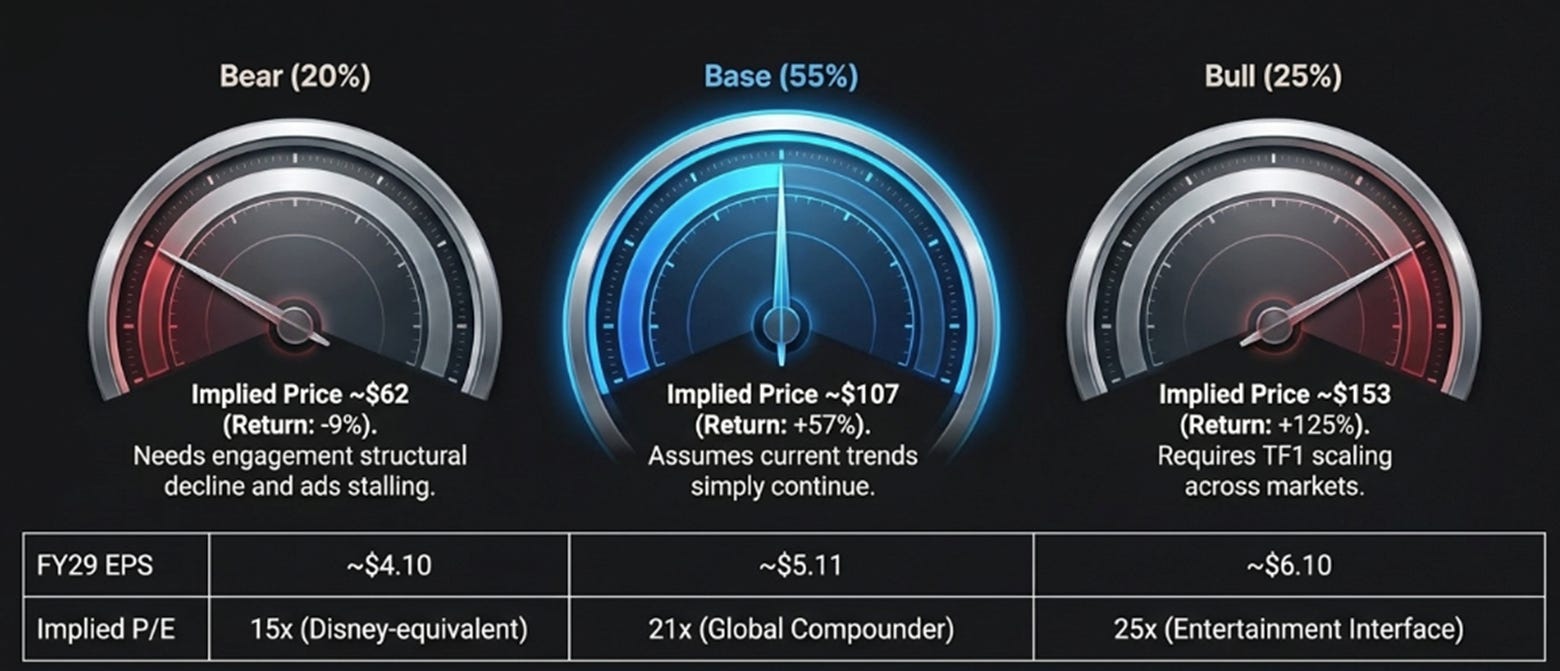

Three-year view, valued on FY29 earnings:

The multiples are applied to FY29 earnings and correspond to three identities: 15x is a mature premium content company, comparable to Disney; 21x is a high-quality global compounder, between media and the scaled platforms at 20–22x; 25x requires reclassification as an entertainment interface, which happens only if TF1 scales across markets and advertising becomes a much larger pool. The bear case needs engagement to structurally decline, ads to stall near $4 billion, and margins to plateau. The base case needs only current trends to continue. Reacceleration is not the thesis; it is the bull case.

Probability-weighted value: roughly $109, about 60% cumulative upside from $68, or 17% annualized over three years.

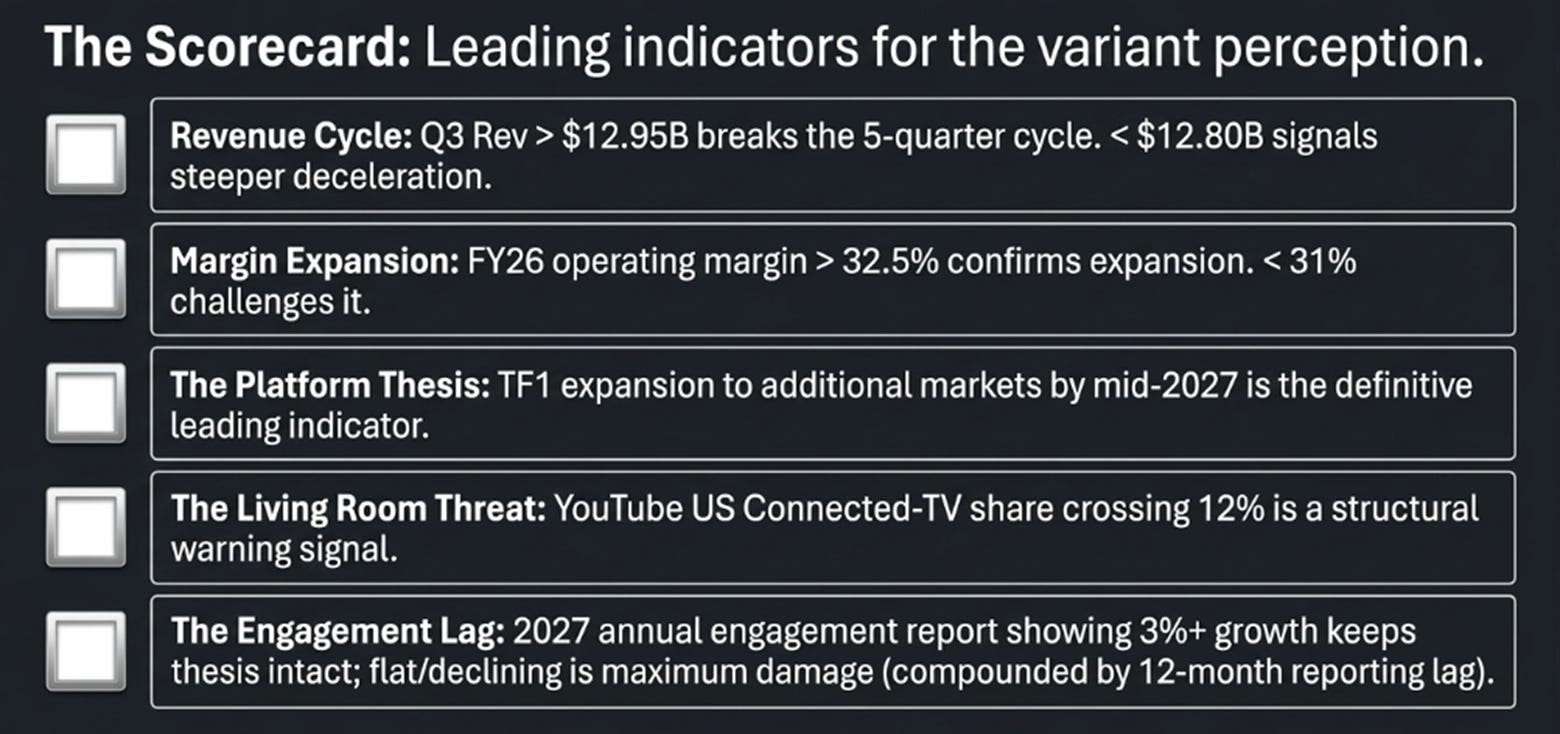

What we’re tracking: Q3 revenue above $12.95 billion breaks the five-quarter cycle; below $12.80 billion means the deceleration is steeper than the lowered guide. FY26 operating margin above 32.5% confirms the expansion; below 31% challenges it. YouTube’s US connected-TV share past 12% is a structural signal Netflix is losing the living room. Any hint at Q3 that $3 billion of ad revenue is conservative shifts the narrative. TF1 expansion to additional markets by mid-2027 is the leading indicator of the platform thesis. And the 2027 annual engagement report, hours growth of 3%+ keeps the thesis intact; flat or declining is the most damaging data point possible, and the shift to annual disclosure means it now arrives with a twelve-month lag, which is itself a risk.

Netflix’s flywheel is slowing. We said so before the quarter; Q2 confirmed it. What Q2 also confirmed is that each revolution now produces more margin, more free cash flow, and more per-share value than the one before. The old growth engine, subscribers, password crackdowns, easy price increases, is not coming back. The new engine, monetization depth, operating leverage, capital return, perhaps eventually the entertainment interface itself, is still being built, partly in public and partly behind disclosure that is getting harder to see through.

The market doubts the new engine can outlast the deceleration of the old one.

At this price, we think we’re being paid well to find out.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.