Netflix's 1Q26 Earnings: Second Flywheel

Walking away from Warner didn't change the problem; it clarified the answer

Q1’26 was better strategically than the stock reaction suggests: the quarter was strong, but guidance was only “good,” which is not enough when investors already price Netflix as a premium compounder.

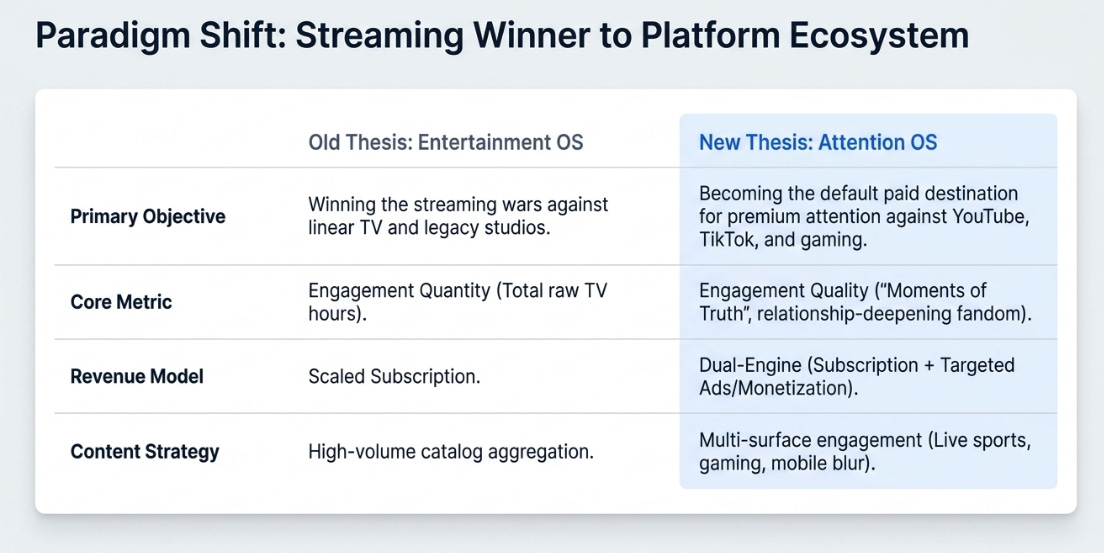

The key shift is from “Entertainment OS” to “Attention OS”: Netflix no longer looks dependent on a big library deal to deepen engagement, with live, games, podcasts, discovery, and pricing now forming the organic answer.

The real debate is no longer just subscriber growth: it is whether Netflix can turn engagement into a meaningful second monetization layer through ads, and earn a platform-style valuation rather than a media multiple.

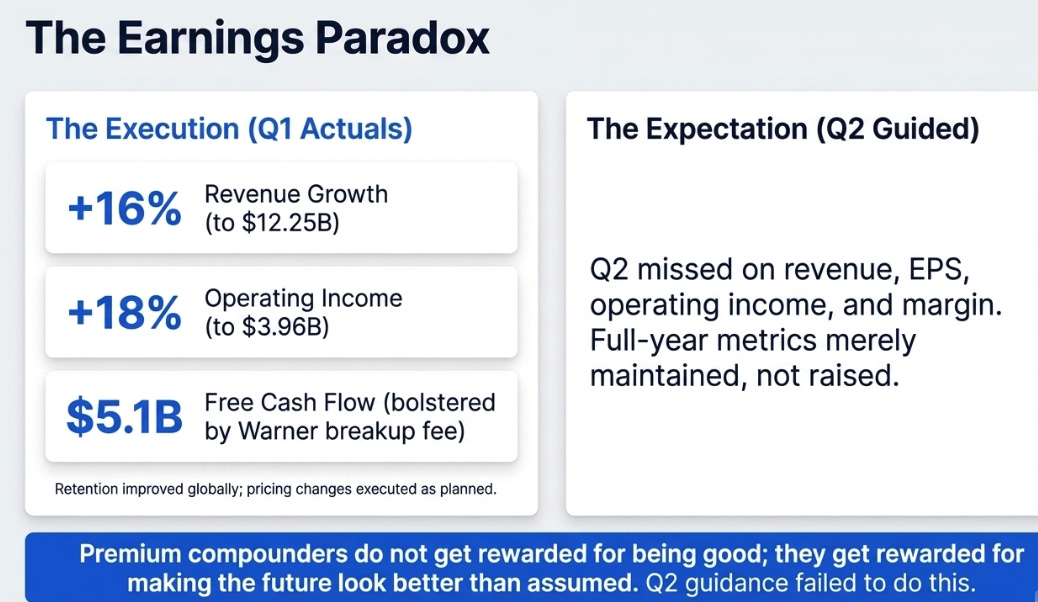

“These are great numbers. What people wanted was even better.” That was Ross Gerber’s line to Bloomberg after Netflix reported Q1. It is also the cleanest explanation for why a quarter with 16% revenue growth, 18% operating income growth, and a big free-cash-flow beat still led to a post-earnings selloff.

My view is that this was a strategically strong quarter disguised as a slightly disappointing one. The disappointment was real: Q2 guidance missed on revenue, EPS, operating income, and margin, while full-year revenue and operating margin were merely maintained. But the strategy got clearer, not weaker.

The thesis we had right, and the part we had wrong

Our prior articles argued that Netflix was becoming an “Entertainment OS”: a product with multiple entry points, shared infrastructure, and multiple “cancellation objectors” inside the household. We also argued, especially in January’s Warner piece, that Netflix’s real problem was not growth in the narrow sense but engagement durability, how do you become more essential between hit releases in a world where YouTube and TikTok compete for far more of users’ time?

That diagnosis was right. What changed is the proposed solution. The Warner bid suggested Netflix might need to buy a library to solve the engagement gap. Q1’26 suggests management thinks it can solve the same problem organically: through live events, podcasts, games, better discovery, pricing sophistication, and a scaled ad business layered on top of the subscription base. Warner, in that framing, was an accelerant, not a necessity. That is exactly how management described it.

Our updated view is not that the problem disappeared. It is that the answer is broader, and more interesting, than a library deal.

From Entertainment OS to Attention OS

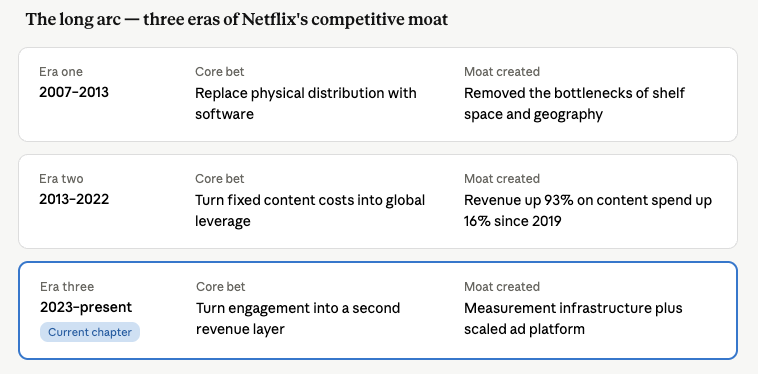

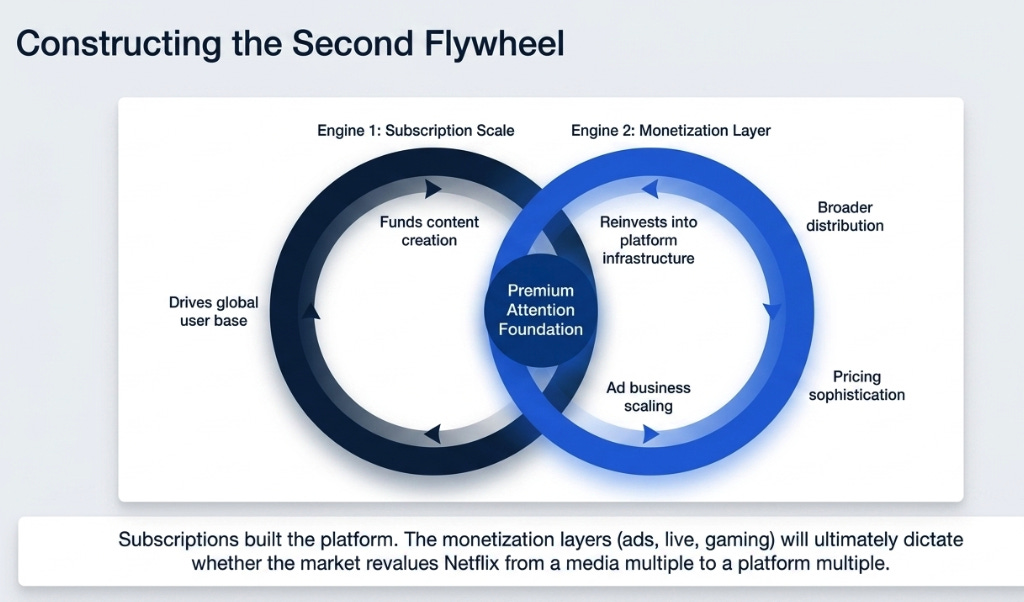

It helps to place this quarter in the longer arc. Netflix first won by replacing distribution scarcity with software: DVDs by mail, then streaming, dismantling the physical bottlenecks that made Blockbuster and cable valuable. It won again by turning fixed content costs into operating leverage: a show costs the same to produce whether 10 million or 300 million people watch it, and global scale made every content dollar more productive than any competitor’s. The next stage, the one this quarter points toward, is turning engagement into a second revenue layer.

The most important line in the shareholder letter is not a financial metric. It is Netflix saying the landscape is changing because streaming continues to take share from linear, technology is massively expanding the supply of video, more entertainment now lives on open platforms and gaming services, and the line between TV and mobile is blurring. That is a description of an attention market, not just a streaming market.

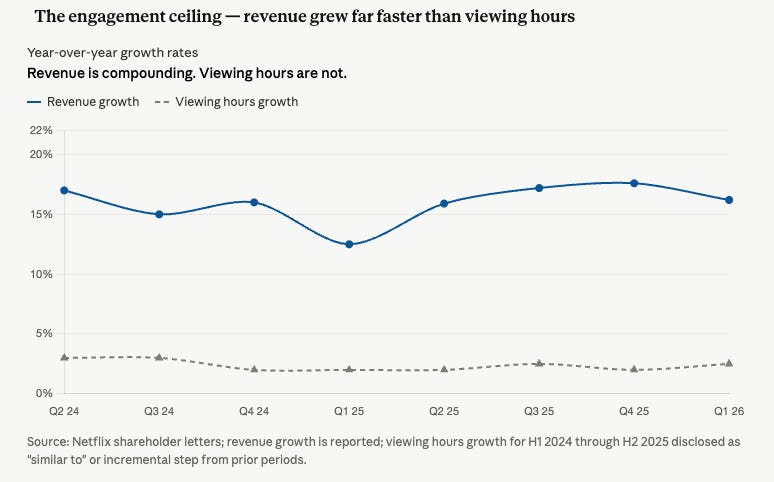

This is why management is increasingly talking about “moments of truth” and engagement quality rather than engagement quantity. The company said its primary internal quality metric hit an all-time high in Q1, the second straight quarter at a record. It emphasized that not all hours are equal, because some content does more than fill time: it drives acquisition, retention, fandom, and word of mouth. The World Baseball Classic in Japan is the proof point: 31.4 million viewers, the biggest sign-up day ever in Japan, and Japan as the single largest contributor to member growth in the quarter.

The old thesis was that Netflix was winning streaming. The new thesis is that Netflix is trying to become the default paid destination for premium attention. That reframes the YouTube problem from last year’s “Great Convergence” piece: YouTube may win more raw TV hours (12.8% share to Netflix’s ~9%), but Netflix is trying to own the most monetizable and relationship-deepening attention. Both businesses can grow. The question is which captures more of the linear TV ad dollars as they migrate, and on that question, premium inventory matters more than total reach.

The monetization layer

This is the second flywheel. Subscriptions built the platform; monetization layers may revalue it.

Netflix’s letter is unusually explicit here. The company’s three priorities are delivering more entertainment value, leveraging technology, and improving monetization. That last point is not code for “raise prices a bit.” It means broader distribution, more pricing sophistication, and a bigger ad business.

The ad business is the key. Management reiterated ad revenue on track for ~$3 billion in 2026, roughly 2x year-over-year. The ad-supported tier represented over 60% of Q1 sign-ups in ad markets, up from 55% entering the year and 40% a year ago. Netflix now works with 4,000+ advertisers, up 70% YoY. Programmatic is becoming more than 50% of non-live ads. These are not side-project metrics; they are platform metrics.

What Netflix still will not disclose is revealing. No quarterly ad revenue in dollars. No ad ARPU. Every adjacent input got volunteered; the output figure did not. Management is anchoring the narrative on adoption trajectory, not dollar run-rate, which likely means the ad business is real but still early enough that the dollar figure would raise as many questions as it answers.

The core economic question for the next three years is simple: does Netflix become a business where engagement produces two revenue streams instead of one? If yes, Netflix stops being a scaled subscription company and starts looking like a platform company. The market today is still pricing the first engine; the second engine is visibly scaling but not yet credited.

Capital return tells you how confident management is. Netflix deployed $1.3 billion on buybacks in the five weeks between the Warner walkaway and quarter-end, retiring 13.5 million shares. FY26 free cash flow guidance rose to $12.5 billion from $11 billion. Management is buying aggressively at prices they clearly consider discounted.

A good quarter, a harder stock

The paradox of Q1 is that the business looked better than the stock.

The numbers were good. Revenue grew 16% to $12.25 billion. Operating income grew 18% to $3.96 billion. Operating margin was 32.3%. Free cash flow was $5.1 billion, helped by the after-tax Warner breakup fee. Retention improved in every region. Price changes went as expected. Today Netflix announced another hike in Spain.

The problem is that Netflix is no longer a turnaround. It is a premium compounder. Premium compounders do not get rewarded for being good; they get rewarded for making the future look even better than investors already assumed. Netflix did not do that. Q2 guidance missed across the board, and full-year revenue and margin were maintained rather than raised.

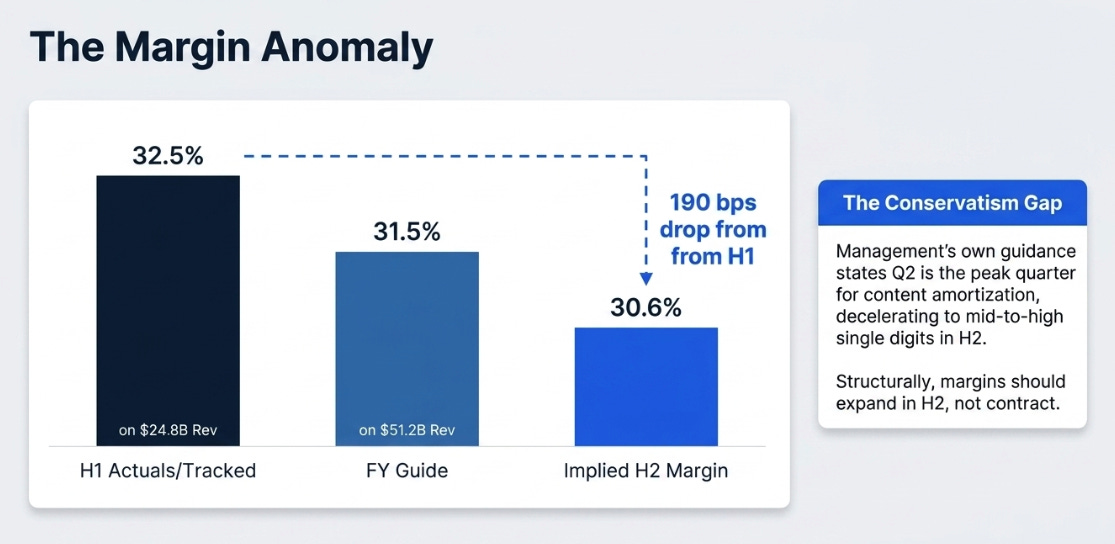

There is a subtler issue embedded in the guide. Q1 delivered 32.3% margin. Q2 is guided to 32.6%. First half tracks to 32.5% on ~$24.8 billion of revenue. The FY 31.5% guide on $51.2 billion implies second-half margin of 30.6%, 190 basis points below the first half. Management’s own amortization trajectory says the opposite should happen: Q2 is the peak content amortization quarter, decelerating to “mid-to-high single digit growth” in H2. The math suggests the FY guide has real room, whether through conservatism, unstated live-content investment, or timing noise. Every Netflix FY margin guide for three consecutive years has been raised mid-year. FY25 went from an initial 25% guide to 29.5% actual through three revisions.

Trust is not as valuable as proof. The market wanted the margin raise today; it will likely get it on the Q2 call in July.

Variant perception

Consensus sees Netflix as a very strong but increasingly mature streamer: low-teens revenue growth, some pricing power, a promising ad business, steady margin expansion. A good company, but still basically a media company.

The better framing is that Netflix is evolving from a content company with a subscription business into a global attention platform with multiple monetization layers. Live events, podcasts, kids gaming, mobile discovery, and ads are not adjacent experiments; they are all attempts to capture more surfaces of engagement and then monetize that engagement more effectively.

What has to be true for that view to work? Ads need to become economically meaningful, not just strategically promising. New formats need to deepen retention more than they dilute margins. And Netflix needs to show it is winning not just TV share, but valuable attention share against YouTube, TikTok, and gaming platforms.

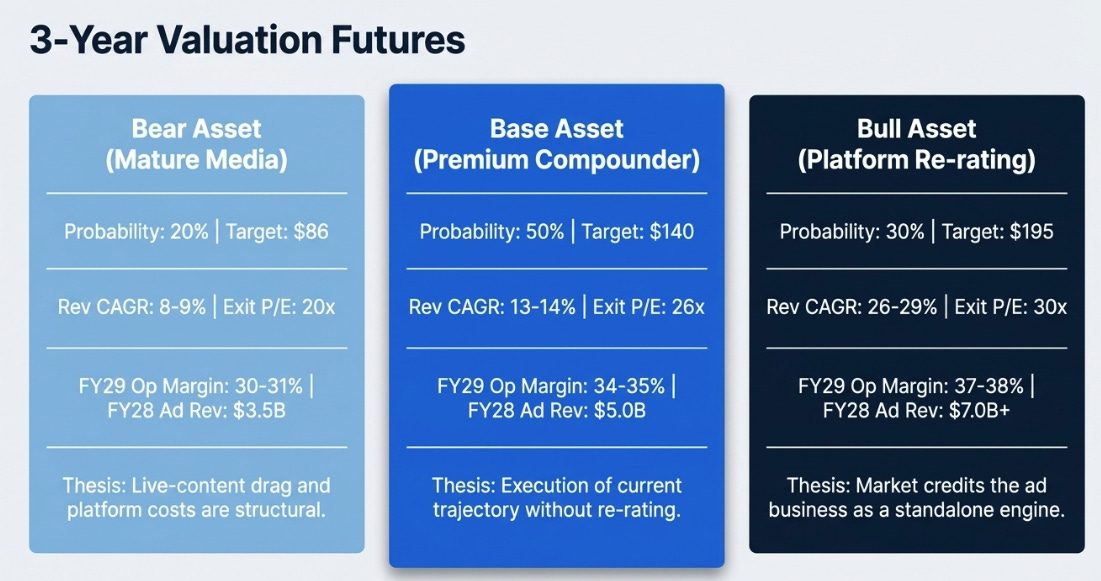

What the stock could be worth in three years

Stock is trading around $94–100 after the 8.7% after-hours drop.

The point is not the exact numbers. It is that the debate is no longer just about revenue growth. It is about whether Netflix deserves to be valued as a better media company or as a new kind of platform company. The bull case requires the market to reclassify Netflix, crediting the ad business as a standalone engine. The bear case requires the market to conclude live-content margin drag and platform-expansion costs are structural. The base case requires neither, just execution of the current trajectory.

What I’m watching now

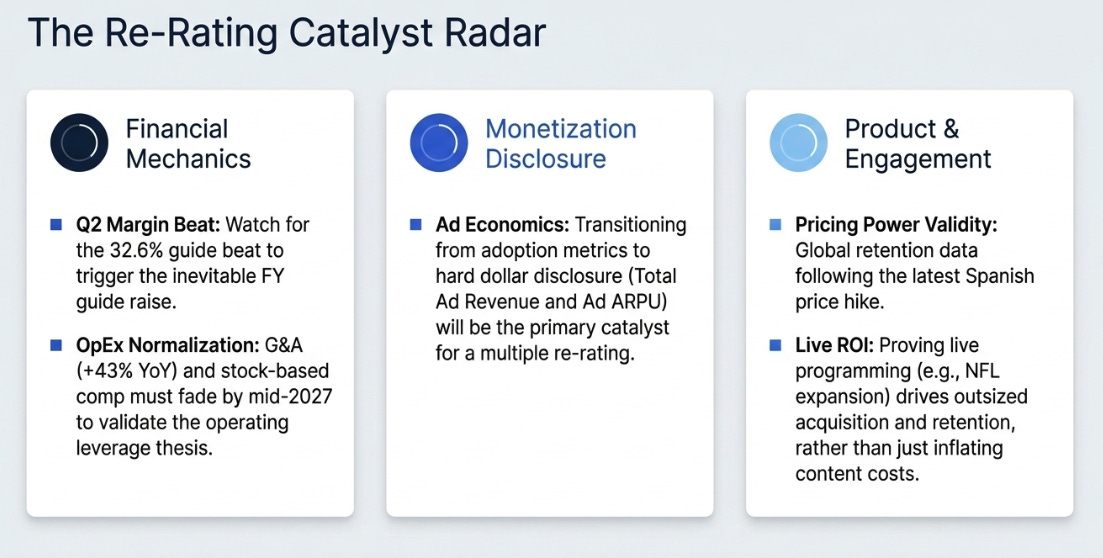

First, ad disclosure: not just sign-up share and advertiser count, but eventually ad revenue dollars and ad ARPU. That disclosure is the re-rating catalyst.

Second, Q2 margin versus the 32.6% guide. A clean beat should trigger an FY guide raise.

Third, retention after the latest round of price increases. Management sounds confident; the market wants evidence.

Fourth, whether live programming continues to show outsized acquisition and retention value, or just raises content costs. The NFL expansion discussions Sarandos telegraphed are the first test.

Fifth, whether operating expense growth normalizes. G&A grew 43% YoY in Q1 and stock-based comp nearly doubled. Some is InterPositive and Warner wind-down; the rest is platform-expansion cost that needs to fade by mid-2027 for the operating leverage thesis to work.

Sixth, whether Netflix can keep making itself the “must-have service” management described: the first place people go for entertainment, and the last thing they cancel. That line is more important than it looks. It is not a slogan. It is the entire strategy.

Walking away from Warner did not change Netflix’s problem. The company still needs to become more essential between hit releases, and it still needs to prove that more engagement can turn into better economics. What changed is that the answer now looks less like buying a library and more like building a broader platform.

The question is no longer whether Netflix can grow. It is whether Netflix can turn breadth into economics.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.