Nu Holdings 1Q26: The Decision Engine Meets the Credit Cycle

Revenue, ARPAC, Mexico, and AI all advanced. The stock still wants one thing: proof that Nubank’s decision engine works when credit gets noisy.

TL;DR

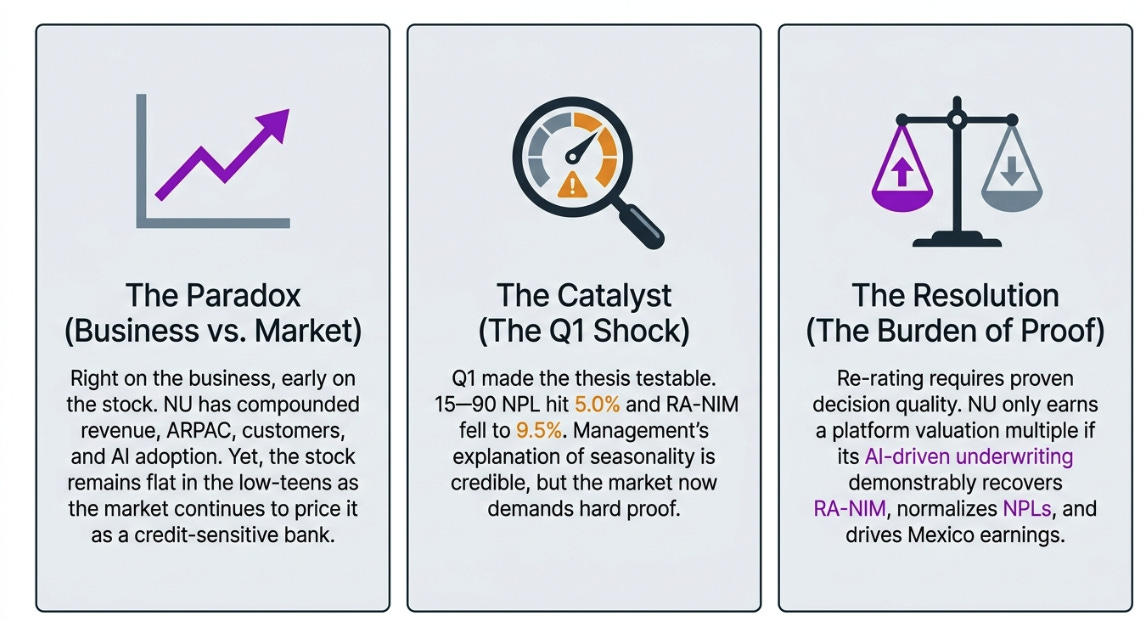

Right on the business, early on the stock: NU has compounded revenue, ARPAC, customers, Mexico, and AI; but the stock is flat because the market still prices it as a credit-sensitive bank.

Q1 made the thesis testable: 15–90 NPL hit 5.0% and RA-NIM fell to 9.5%; management’s explanation is credible but now needs proof.

Re-rating requires decision quality: NU gets a platform multiple only if AI/data-driven underwriting shows up in RA-NIM recovery, NPL normalization, and Mexico earnings.

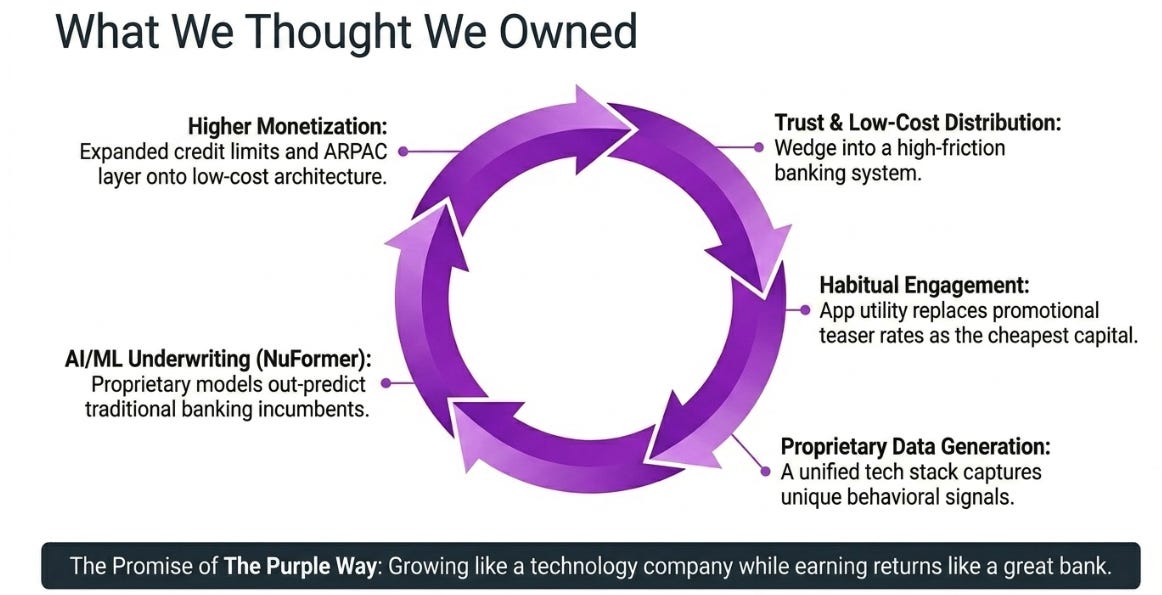

A year ago, the Nubank thesis was elegant. Trust would compound into engagement; engagement would compound into data; data would improve underwriting; better underwriting would expand monetization; and higher monetization, layered on a low-cost digital architecture, would create one of the rare financial platforms that could grow like a technology company while earning returns like a great bank.

A year later, the business has largely followed that script. The stock has not.

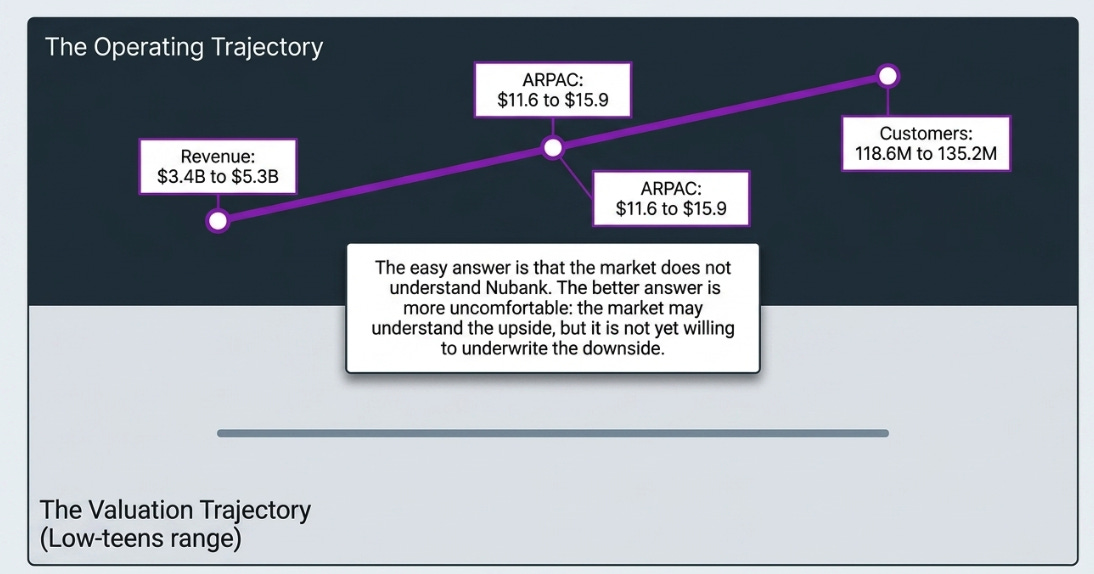

That is the uncomfortable starting point for any honest Q1’26 update. Nubank’s quarterly revenue has moved from roughly $3.4 billion in Q1’25 to $5.3 billion in Q1’26. ARPAC has risen from $11.6 to $15.9. Customers have increased from 118.6 million to 135.2 million. Mexico has gone from promising expansion market to break-even business. AI has moved from a strategic claim to a production tool inside credit decisioning. Net income is up sharply year-over-year.

And yet the stock remains near the same low-teens range that framed much of our earlier work.

The easy answer is that the market does not understand Nubank. The better answer is more uncomfortable: the market may understand the upside, but it is not yet willing to underwrite the downside.

That is the tension Q1 brought back to the surface. We have been broadly right about the operating trajectory. We were too early — perhaps too optimistic — about when the market would pay for it.

What We Thought We Owned

Our view of Nubank has evolved over the past year.

In The Purple Way, the thesis was that Nubank was not simply a digital bank. It was a new financial institution built around customer trust, low-cost distribution, and a culture of product simplicity in markets where incumbents had trained customers to expect friction. The purple card was not just a product; it was a wedge into a banking system that had grown fat on fees, branches, and inertia.

By Q2’25, Mexico became the key proof point. The question was whether Nubank’s international growth was being bought with promotional deposit rates or earned through product utility. When Mexico customers largely stayed after yields were cut, the conclusion was powerful: trust had become a funding advantage. The cheapest capital was not a teaser rate; it was habitual use inside an app.

By Q3, the thesis moved from distribution to decision quality. NuFormer made the argument more ambitious: Nubank was not only acquiring customers more cheaply; it was potentially making better financial decisions because it had proprietary data, a unified technology stack, and machine-learning models trained on behavioral signals incumbents could not replicate.

Q4 sharpened the debate. The market sold higher provisions. We argued that the provision increase was largely mechanical: NuFormer-driven credit limit expansion front-loaded IFRS 9 expected losses before the associated revenue appeared. But we also said the important question was whether that limit expansion would convert into NII without credit deterioration.

Q1 did not ask a new question. It asked the same question again, with less room for elegance.

The Question Q1 Forces

The fundamental question is simple:

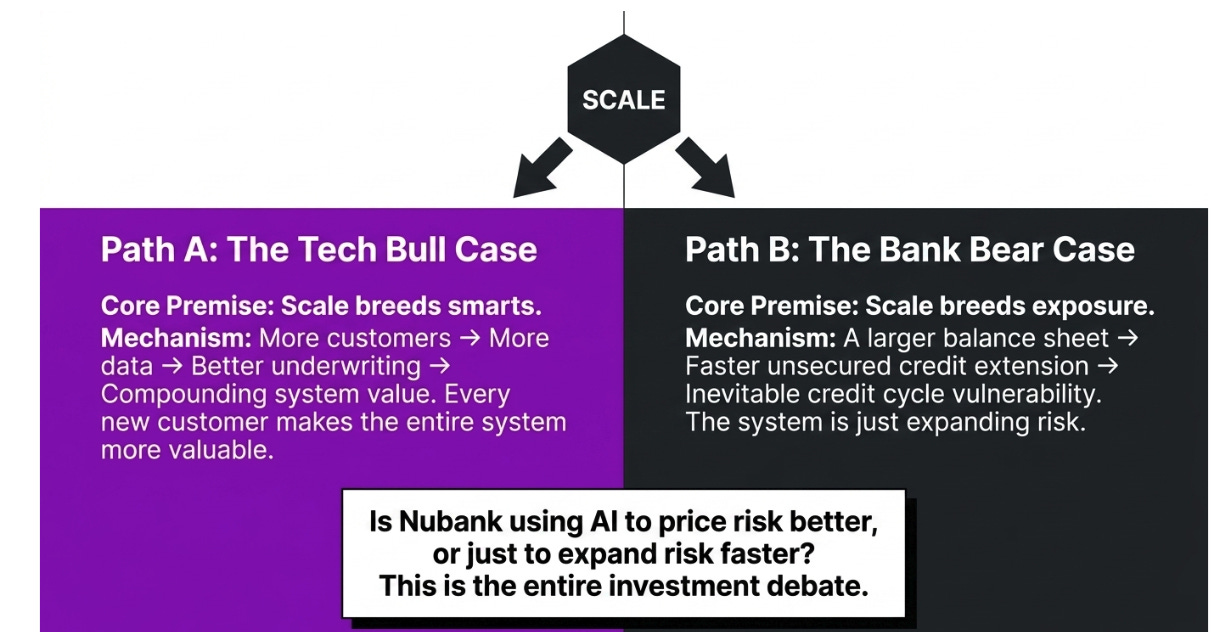

Is Nubank’s scale making its underwriting engine smarter, or merely making its credit book larger?

This is the entire investment debate.

If Nubank’s scale improves underwriting, then every new customer makes the system more valuable. More customers create more data; more data improves credit decisions, personalization, fraud detection, collections, and cross-sell; better decisions raise ARPAC and reduce losses; higher profitability funds more product development and market expansion. That is the compounding loop.

If, however, scale simply allows Nubank to extend more unsecured credit faster, then the story is less special. The company may still be an excellent digital bank, but it deserves to be valued as a bank: profitable, growing, but exposed to credit cycles and capital constraints.

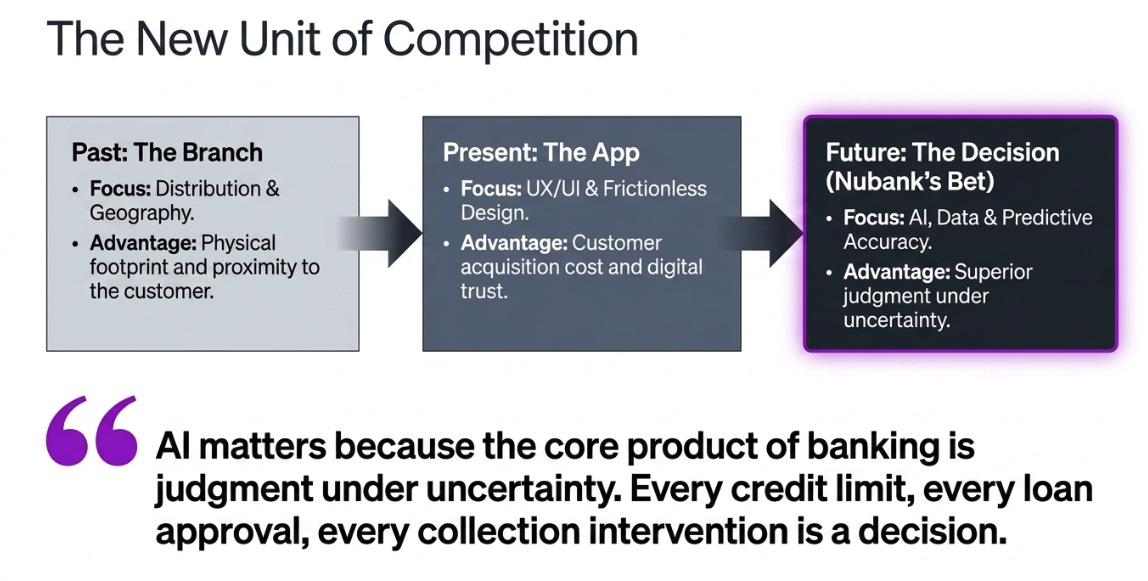

This is why AI matters. Not because it makes customer service cheaper, although it may. Not because it makes the app better, although it may. AI matters because the core product of banking is judgment under uncertainty. Every credit limit, every loan approval, every collection intervention, every deposit rate, every product offer is a decision.

The old unit of competition in banking was the branch. Then it was the app. Nubank is arguing that the new unit of competition is the decision.

Q1 made that argument measurable.

Why the Market Sold First

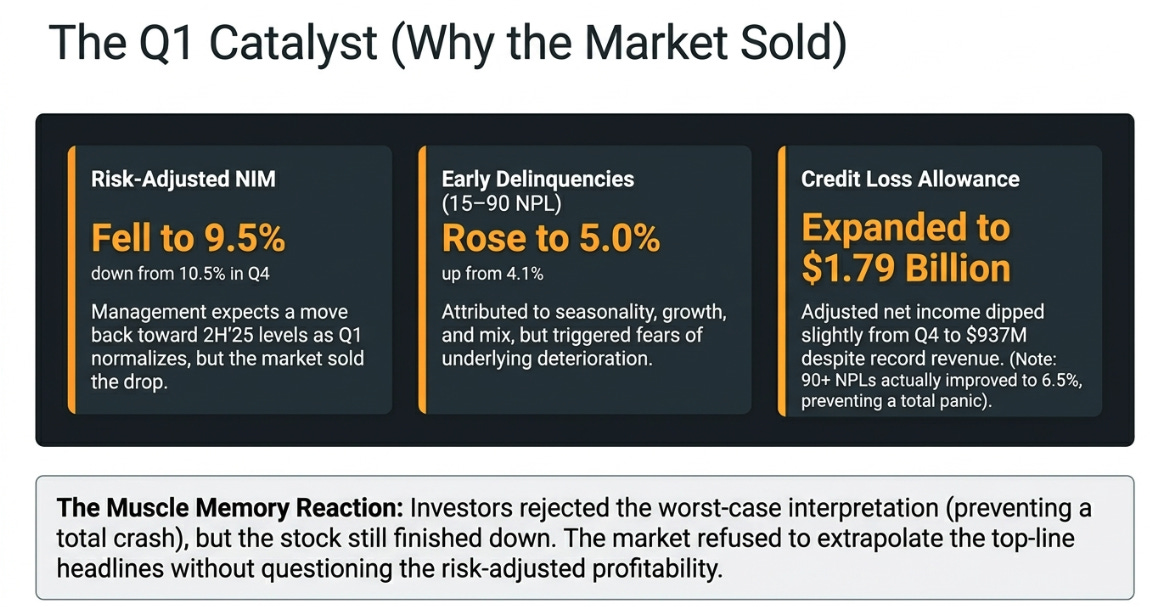

The initial selloff after the Q1 print was not irrational. Revenue was strong, but the first-pass market reaction was not about revenue. It was about risk-adjusted profitability.

Risk-adjusted NIM fell to 9.5% from 10.5% in Q4. The 15–90 NPL ratio rose to 5.0% from 4.1%. Credit Loss Allowance rose to $1.79 billion. Adjusted net income was $937 million, down slightly from Q4 despite record revenue.

Those numbers trigger bank-investor muscle memory. The concern is straightforward: perhaps Nubank is not using AI to price risk better; perhaps it is using AI to expand risk faster.

Management’s response was credible. The company argued that the 15–90 NPL move was mostly seasonal, that growth and mix drove provisioning, and that 90+ NPLs actually improved to 6.5%. On the call, management said risk-adjusted NIM should move back toward second-half 2025 levels as Q1 dynamics normalize.

That explanation matters. It is also not enough.

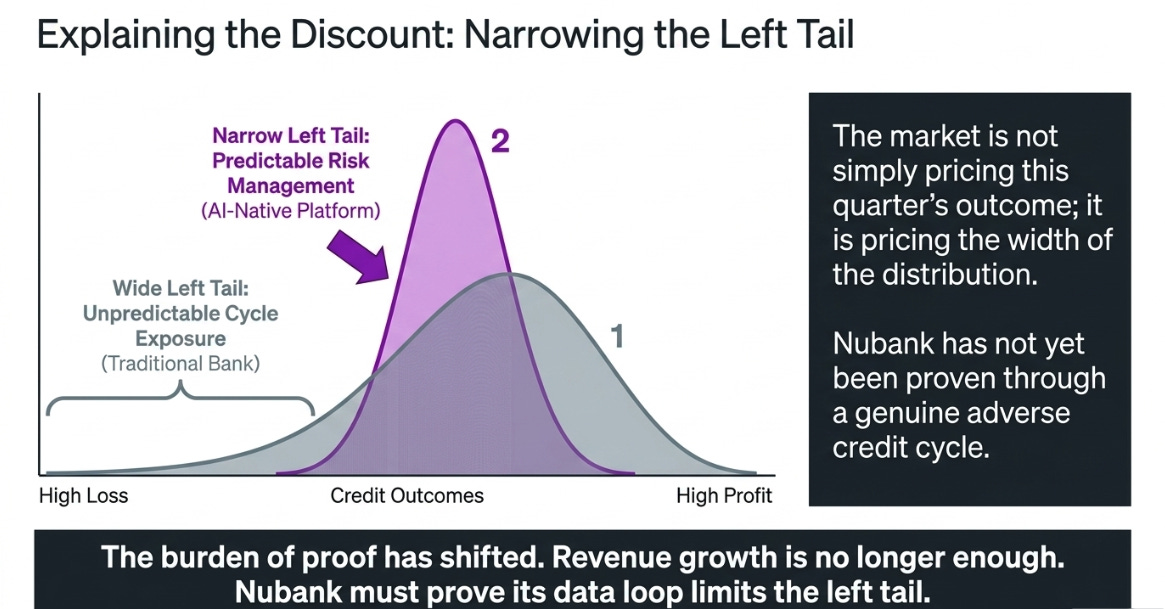

The market is not simply pricing this quarter’s outcome. It is pricing the width of the distribution. Nubank’s AI underwriting may be superior. Cohort economics may be healthy. Coverage may be strong. But the market has not yet seen this model through a genuine adverse credit cycle.

That is the discount.

Why the Stock Came Back

The recovery from the lows should not be interpreted as the market accepting the platform thesis. It was more modest than that. Investors rejected the worst-case interpretation.

They had reasons. The credit bridge was detailed. Late-stage delinquencies improved. The seasonal pattern in early delinquencies had precedent. Mexico reached break-even. AI disclosures were more tangible than in prior quarters. And the broader market backdrop was supportive enough that buyers were willing to underwrite an explanation rather than extrapolate the first headline.

Still, the stock finished down. That matters too.

Q1 did not resolve the debate. It made the debate measurable.

What Changed in Our View

The long-term thesis is not broken. It is more conditional.

Before Q1, it was reasonable to argue that the market was over-penalizing provision optics. After Q1, that may still be true, but it now requires proof. The burden of proof has shifted from demonstrating the flywheel to narrowing the left tail.

That is a subtle but important change.

Revenue growth is no longer enough. ARPAC growth is no longer enough. Mexico reaching break-even is not enough. AI adoption metrics are not enough.

The next phase of the thesis depends on whether decision quality shows up in risk-adjusted returns. The market does not need Nubank to eliminate credit risk; that would be impossible. It needs evidence that Nubank’s data, underwriting, and cost structure make credit outcomes more predictable than they would be at a traditional lender.

That is also where our own framework needs humility. We have been right about the business direction. We were early on the re-rating. The market has not refused to see Nubank’s progress; it has refused to capitalize that progress at a platform multiple before the credit engine is proven through stress.

The variant perception, therefore, is not that Nubank deserves no credit discount. It is that the discount may be too large if the company can demonstrate that its data loop narrows the left tail.

Mexico Is the Counterweight

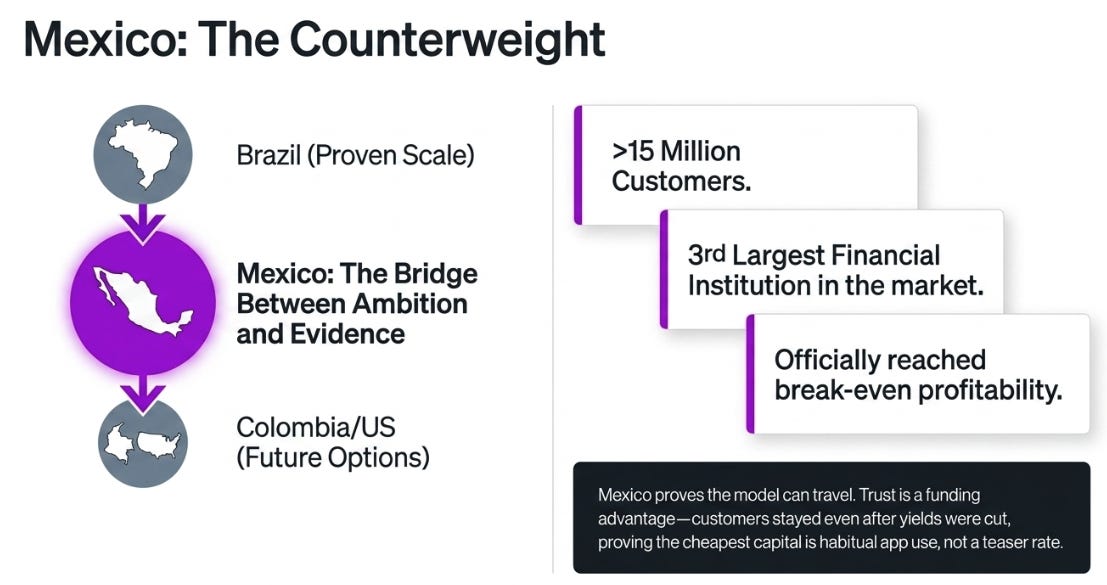

The reason Q1 is not simply a credit-risk story is Mexico.

Brazil proved that Nubank’s model can scale. Mexico is testing whether it can travel. Q1 was a real milestone: Mexico crossed 15 million customers, became the third-largest financial institution in the market, and reached break-even.

That does not yet force a re-rating. Break-even is validation, not materiality. But it changes the probability distribution. A year ago, Mexico was mostly evidence of transferability. Now it is beginning to look like the second earnings engine.

That matters because the bull case for Nubank has never been only Brazil. It has been that the company’s core capability — trust, data, underwriting, low-cost product manufacturing — can travel across markets. Mexico is the first serious test of that claim. The U.S. is still an option. Colombia is still early. Mexico is the bridge between ambition and evidence.

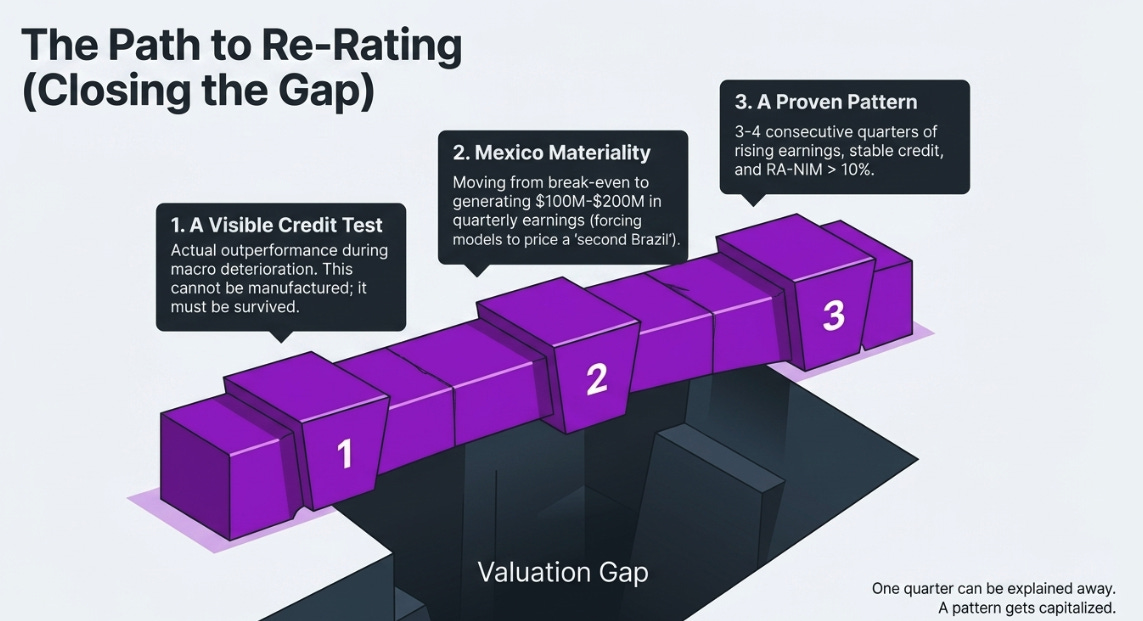

What Would Close the Gap

There are only three credible ways for the valuation gap to close.

First, Nubank needs a visible credit test. Not seasonal Q1 noise, but an actual period of macro deterioration where industry NPLs rise and Nubank’s outcomes prove structurally better. That would be the definitive evidence, but it cannot be manufactured.

Second, Mexico must become material. Break-even validates the playbook. A business generating $100–200 million of quarterly earnings would force investors to model a second Brazil.

Third, the company needs a pattern: three or four consecutive quarters of rising earnings, stable or improving credit metrics, and risk-adjusted NIM back above 10%. One quarter can be explained. A pattern gets capitalized.

This means the re-rating is probably not immediate. Nubank may be mispriced, but the catalyst is evidence accumulation, not one earnings call.

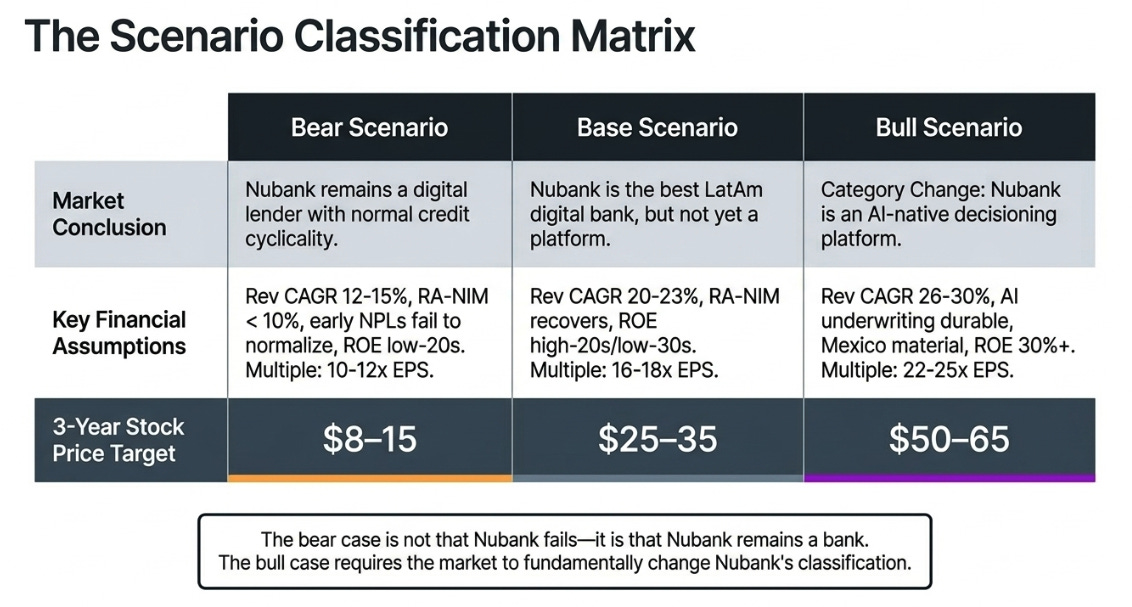

Scenarios

The scenarios are not just financial. They are classification outcomes.

The bear case is not that Nubank fails. It is that Nubank remains a bank. The bull case is not simply that revenue grows. It is that the market changes the category.

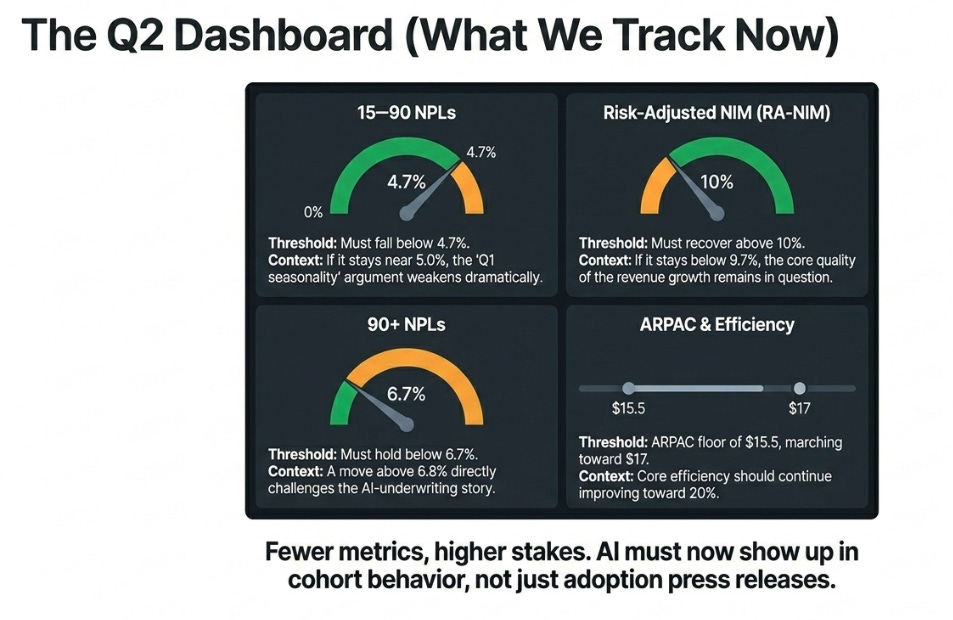

What We Track Now

The next few quarters need fewer metrics, not more.

The 15–90 NPL ratio needs to fall below 4.7% in Q2; if it stays near or above 5.0%, the seasonality argument weakens. Risk-adjusted NIM needs to move back above 10%; if it stays below 9.7%, growth quality remains in question. 90+ NPLs need to stay below 6.7%; a move above 6.8% would challenge the underwriting story.

ARPAC should hold above $15.5 and move toward $17 over time. Mexico needs to remain profitable. The efficiency ratio can normalize toward 20%, but core efficiency should continue improving. And AI needs to show up in cohort behavior, not just adoption metrics.

Early, Not Exonerated

The best theses are not the ones that never get challenged. They are the ones where the challenge clarifies what must be true.

Nubank’s Q1 did not break the thesis. It made it more honest. The company has executed like a platform, but the market is still valuing the unknowns like a bank. That is frustrating, but it is not irrational.

I still think we are early, not wrong. But early no longer means waiting for investors to notice revenue growth, ARPAC, Mexico, or AI. It means waiting for enough credit evidence to narrow the left tail.

If that evidence arrives, the platform multiple becomes available. If it does not, the market will have been right to keep Nubank in the bank bucket all along.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.