Nu Holdings Q4'25: The Compounding Machine

The market sold higher provisions. Nu reported monetization density, AI-scaled underwriting, and a deliberate bid for platform valuation.

TL;DR:

The real beat was ARPAC, not revenue. Monetization density jumped from $11 to $15, confirming Nu’s flywheel has shifted from customer growth to profit compounding.

Provision growth was mechanical, not necessarily deterioration. A 60% increase in unused credit limits front-loaded IFRS 9 losses, while actual NPLs improved. The revenue from that expansion hasn’t shown up yet.

Nu is trying to change its multiple. A new managerial P&L, platform framing, and U.S. charter progress signal a transition from “high-growth LatAm bank” to “global digital banking platform.”

“Higher costs and provisions overshadow profit.”

— Bloomberg, February 26, 2026

The Quarter the Optics Won

That line explained the stock move, not the quarter.

In my Q3 piece, Building the Moat While Breaking Records, I argued that nuFormer’s reveal marked the shift from UX dominance to decision-quality dominance, and that the 27.7% efficiency ratio reflected deliberate investment, not cost slippage. I closed by writing that the validation quarter was complete and the acceleration quarter had begun.

Q4 proved that right, but in a way the market couldn’t parse cleanly. Revenue beat consensus by 6%. ROE hit a record 33%. Early-stage NPLs improved for the fourth consecutive quarter. ARPAC reached $15. And the stock dropped 5%, because provisions went up.

I think the market traded the optics correctly and the substance backwards. But more importantly, Q4 was the quarter Nu stopped merely reporting results and started arguing for a fundamentally different way of being valued. Management introduced a new Managerial P&L, reframed 2026 as an “inflection year,” and described the company as transitioning from a Latin American leader into a “global digital banking platform.” That is not routine earnings-call language. That is a company trying to change the lens through which investors price it.

Whether it deserves that new lens is the question this quarter is really asking.

Monetization Density Is the Real Story

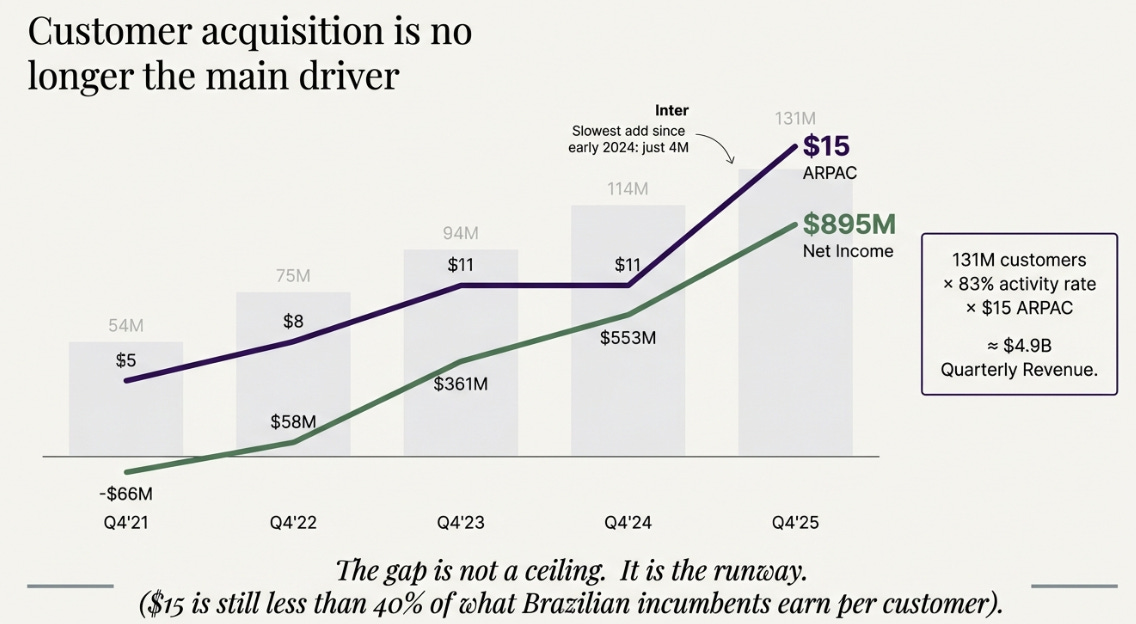

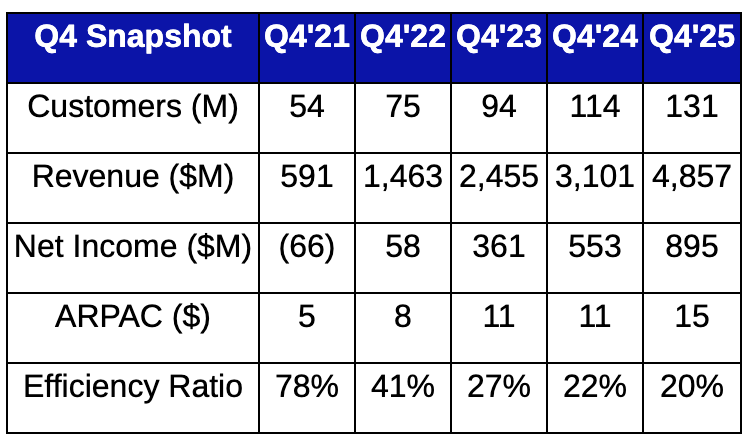

The headline beat was revenue. The more important beat was monetization density.

For years, the Nu narrative was about customer acquisition, the purple card as rebellion against Brazilian banking’s indignities, the explosive sign-up curves, the crossing of 100 million customers. That chapter is effectively over. Nu added just 4 million customers in Q4, the lowest quarterly add since early 2024.

But look at what is accelerating instead.

That table is the whole story. ARPAC stalled at $11 through 2024, the period when the market was most nervous about the stock. The re-acceleration to $15, a 35% increase on a full-year basis, is the signal that the monetization engine has found a new gear.

Do the simple math: 131 million customers, 83% activity rate, $15 ARPAC. That gets you to roughly $4.9 billion of quarterly revenue, almost exactly what Nu reported. The entire revenue line is now explained by monetization density times installed base. And $15 is still less than 40% of what Brazilian incumbents earn per customer. The gap is not a ceiling. It is the runway.

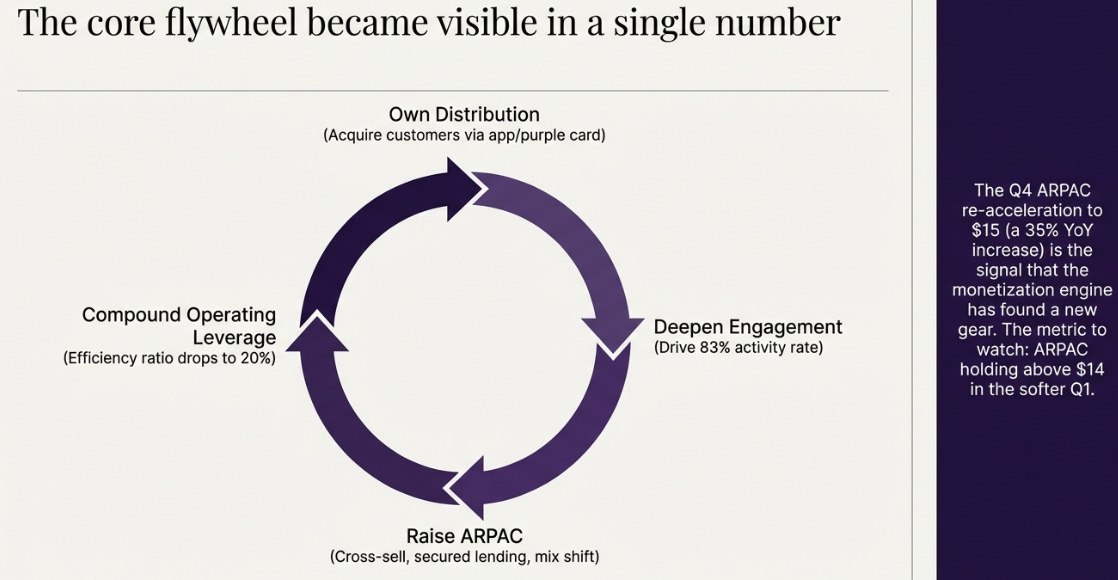

In The Purple Way, I framed this as the core flywheel: own distribution, deepen engagement, raise ARPAC, let operating leverage compound. Q4 was the quarter that flywheel became visible in a single number.

Of course, ARPAC acceleration from $11 to $15 partly reflects mix shift, more credit products, higher-yielding secured lending, seasonal Q4 effects from Brazil’s thirteenth salary. Whether this pace sustains into Q1, when seasonality works against it, is genuinely uncertain. The number to watch is whether ARPAC holds above $14 in the softer quarter. If it does, the re-acceleration is structural. If it slips back toward $12, the Q4 print was flattered.

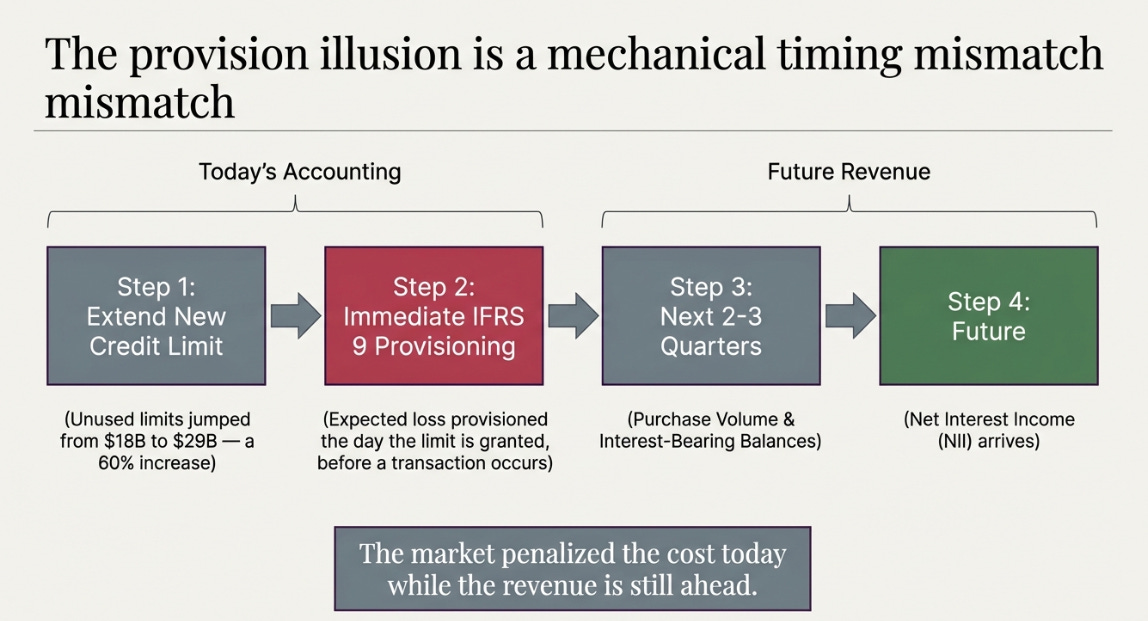

The Provision Illusion

Which brings me to what the market actually reacted to, and to a mechanism worth understanding on its own terms before deciding what it means.

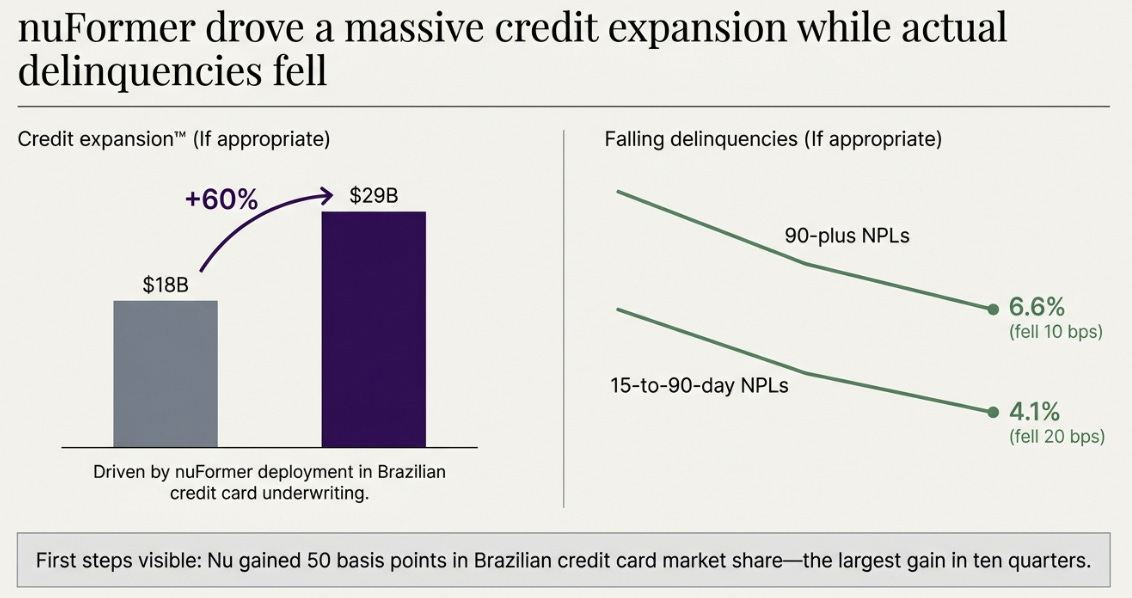

When a bank extends a new credit limit to a customer, it does not wait for the customer to use that limit before accounting for the risk. Under IFRS 9, the expected loss on unused credit must be provisioned immediately, the day the limit is granted, before a single transaction occurs. This is front-loaded accounting: the cost appears now, the revenue appears later.

In Q4, Nu’s unused credit limits went from $18 billion to $29 billion, a 60% increase, driven by nuFormer’s deployment in Brazilian credit card underwriting. That $11 billion expansion mechanically required higher provisions. Meanwhile, actual delinquencies moved in the opposite direction: 15-to-90-day NPLs fell 20 basis points to 4.1%, and 90-plus NPLs fell 10 basis points to 6.6%.

On the call, Lago pointed analysts to explanatory note 32 of the financial statements to see the unused limit data. Whether that was deliberate signaling to sophisticated investors or simply a CFO being thorough, the number is worth finding. He then laid out the conversion sequence: limits first, then purchase volume, then interest-bearing balances. “We are starting to see the first step,” he said, referring to a 50-basis-point gain in Brazilian credit card market share, the largest in ten quarters. The NII has not shown up yet. That is two to three quarters away.

My read is that this is a timing mismatch: the market penalized the cost today while the revenue is still ahead. But I want to be honest about the alternative reading, because it is not trivial.

The Risk to the AI Thesis

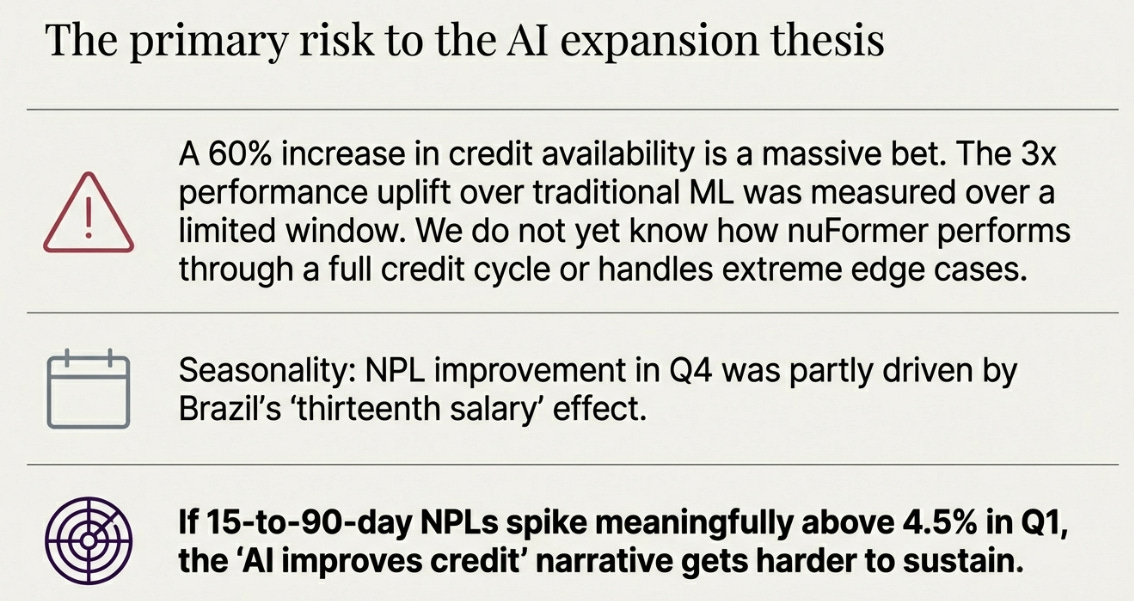

The alternative is that nuFormer’s limit expansion is too aggressive. A 60% increase in credit availability, even from a sophisticated model, is a large bet. The 3x performance uplift over traditional ML that management cited in Q3 was measured over a limited deployment window; we do not yet know how the model performs through a full credit cycle, or whether the uplift degrades as it encounters edge cases further from its training distribution. The NPL improvement in Q4 was partly seasonal, Brazil’s thirteenth salary helps borrowers catch up on payments every Q4, and management explicitly guided for a seasonal uptick in Q1. If 15-to-90-day NPLs spike meaningfully above 4.5% in Q1, the “AI improves credit” narrative gets harder to sustain.

I still think the provision increase was mechanical, not pathological. But I hold that view with less certainty than the rest of the thesis, because the magnitude of the credit limit expansion is large enough that even a small deterioration in model accuracy would matter.

A New Scoreboard Is Never Neutral

There was something else happening in Q4 that I think matters more than the provision debate. Nu introduced an entirely new reporting framework and restated results back to Q1 2021.

Lago framed it as housekeeping: “This evolution does not change economic reality, it only clarifies it.” That may be true, but companies do not reframe disclosure unless they believe the old framing is obscuring the business they are becoming. Nu also changed its efficiency ratio methodology and began presenting consolidated NPL metrics. The subtext is not subtle: Nu wants to be evaluated as a platform, not as a bank.

From Bank to Proprietary Data Loop

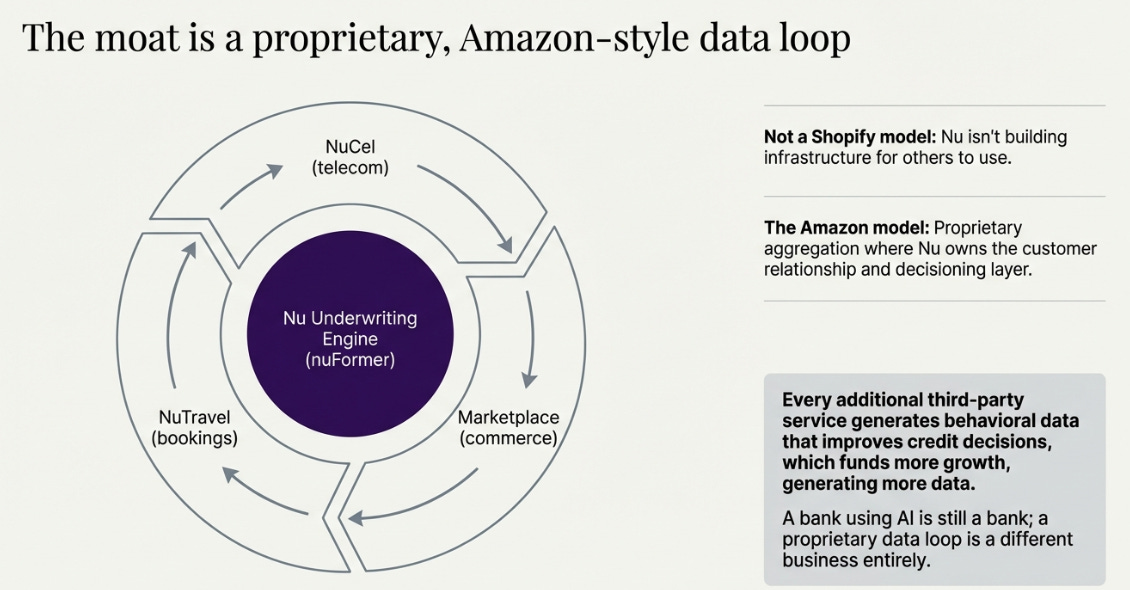

But what kind of platform? This matters for the multiple expansion thesis, and I think it deserves specificity. Nu is not building a Shopify-style infrastructure layer that others build on. It is building something closer to the Amazon model: proprietary aggregation where the company owns the customer relationship, the data loop, and the decisioning layer, while selectively integrating third-party services, NuCel for telecom, NuTravel for bookings, marketplace for commerce, as engagement extensions that feed back into the core underwriting engine. The moat is not that others can plug into Nu. The moat is that every additional service generates behavioral data that makes the credit decisions better, which funds more growth, which generates more data.

That architecture is what justifies a different multiple, if it works. A bank that uses AI is still a bank. A proprietary data loop that uses banking as its first application is a different kind of business. Q4 was the quarter Nu started explicitly making that argument.

Capital as Launchpad

Lago also guided for “four to six quarters” of efficiency pressure from three investment buckets: return-to-office (quantified at 80 to 100 basis points), AI and GPU spending (unquantified), and global expansion (”substantial” and “not capitalized”). After four quarters of accelerating ROE, 27%, 29%, 31%, 33%, I think Lago is setting a floor, not a ceiling. But the guidance serves a practical purpose regardless: it gives management room to invest without every tick in the efficiency ratio triggering a sell-off.

The most important thing he said was not about efficiency. It was this: “Our capital and liquidity positions are not simply a reflection of our past performance. They are, in fact, the foundation of what comes next.” Three billion in unrestricted cash. Two point two billion of excess capital. Available funding at twice the net credit portfolio. That is a company telling you: the investment phase is coming, the capital is in place, and we do not need external financing to execute.

The Zero-Priced Option

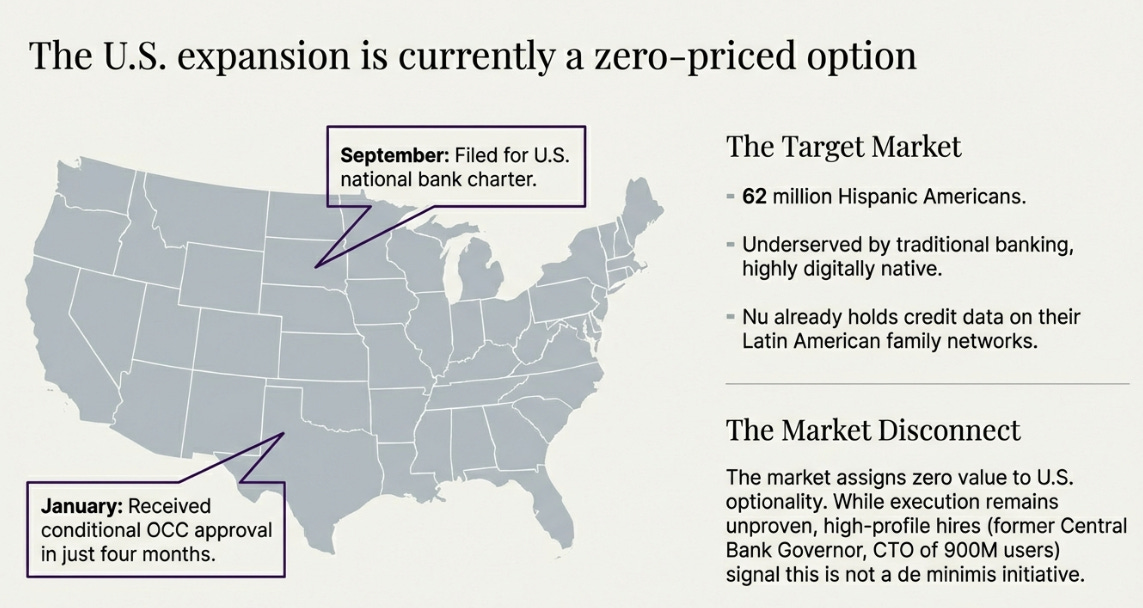

In The Purple Way, I described Act 3 as Nu’s emergence as a global financial platform, theoretical at the time. It is no longer theoretical. Nu filed for a U.S. national bank charter in September and received conditional OCC approval in January.

I want to be precise about what “conditional” means. It is not final approval. It means the OCC has determined the application has merit and is imposing conditions, typically around capital, compliance infrastructure, and business plan, that must be satisfied before a full charter is granted. Foreign fintechs have a mixed record navigating this process, and the conditions themselves have not been disclosed. This could take another six to twelve months, or longer.

That said, reaching conditional approval in four months is fast, and it signals regulatory seriousness on both sides. Velez was carefully vague on the call but revealing in his framing: “When you dig in into sub-segments, in certain niches, that, by the way, happen to be the size of Brazil, we actually find opportunity to solve a number of consumer problems.”

Sub-segments the size of Brazil. There are 62 million Hispanic Americans, younger, more digitally native, and more underserved by traditional banking than the broader population. Many have family members in Nu’s existing markets. Nu already has credit data on those family networks. It has nuFormer. It has a brand that carries trust across the Latin American diaspora. And it has a cost structure that makes U.S. neobanks look expensive.

The executive hires, a former Central Bank Governor, a CTO who has scaled to 900 million users, a Chief Design Officer with massive-scale experience, are not consistent with a “de minimis” initiative. But they are also not proof that the U.S. will work. The American market has humbled many sophisticated entrants, including well-funded fintechs with seemingly compelling wedges. I give Nu credit for the approach but not for the outcome. That has to be earned.

The market assigns zero value to U.S. optionality. That is probably wrong, but by how much depends entirely on execution that has not yet occurred.

Scenario Weights: Subtle but Important Shifts

Q4 shifts my probability weights modestly. The bull case, global platform recognition, market re-rating to 25-30x earnings by 2028, moves from 45% to 50%, on the strength of nuFormer’s proven deployment and the U.S. charter progression. Assumptions: revenue CAGR around 30%, ARPAC toward $25-plus, net margins of 18-20%.

The base case, Latin American dominance, 18-22x earnings, moves from 40% to 35%. Assumptions: revenue CAGR around 22%, ARPAC reaches $20-22, Mexico profitable but slower.

The bear case stays at 15%. Assumptions: revenue CAGR around 12%, ARPAC stalls, macro deterioration, multiple compresses to 12-15x.

From roughly $15.50, the probability-weighted outcome implies approximately $32 by 2028. The improvement reflects nuFormer moving from hypothetical to proven, and U.S. optionality moving from aspirational to regulatory.

Five things would change my mind: ARPAC stagnation below $18 for two consecutive quarters. Risk-adjusted NIM compressing below 9% without strategic explanation. Mexico ARPAC failing to reach $18-20 within eighteen months. Efficiency above 26% through 2026 without revenue acceleration. Any U.S. regulatory retreat.

Signal and Noise

The market read Q4 as a noisy bank print. It was. But it was also something else, the quarter the compounding machine revealed itself, briefly, before the noise closed back over it. Whether the reveal sticks depends on whether ARPAC keeps compounding, whether nuFormer’s credit expansion converts to NII without a credit-quality surprise, and whether the platform thesis Nu is now explicitly selling proves to be more than valuation architecture.

The cheapest capital in Latin America is still habitual trust inside an app. And that trust is now compounding with an intelligence layer that traditional banks cannot replicate. I think the thesis strengthened this quarter. I also think it has never been more important to watch the variables that could prove it wrong.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.