NVIDIA 1QFY25 Earnings: The Architecture of Intelligence

We thought NVIDIA was selling the rack. Q1 suggests it is trying to become the default way intelligence is produced.

TL;DR

Our NVIDIA thesis has matured from demand to standardization. We already believed generated software and agentic AI make compute a revenue engine; Q1’s new ACIE disclosure gives us the first real test of whether that demand is spreading beyond hyperscalers into the broader AI factory economy.

The product is no longer the GPU, or even the rack: it is the AI factory architecture. Networking growth, Vera CPU, CUDA, NVLink/Spectrum-X, and full-stack deployment economics suggest NVIDIA is trying to become the default system for producing intelligence, not merely the leading supplier of accelerators.

The key debate is flywheel versus circle. If ACIE keeps growing, networking remains strong, and ecosystem investments moderate, NVIDIA’s platform compounds; if demand increasingly depends on NVIDIA’s own financing while ACIE slows, the “AI factory standard” thesis weakens.

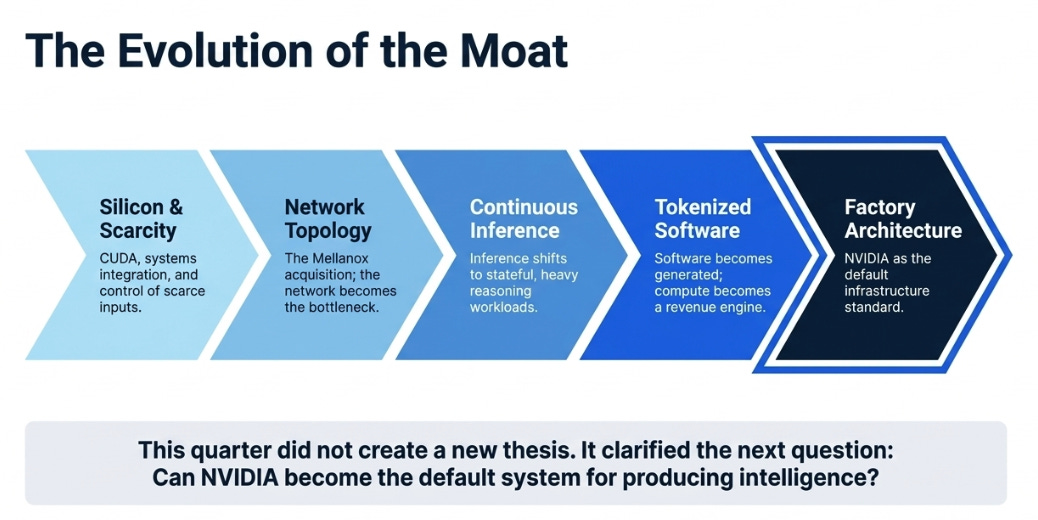

For the last year, our NVIDIA work has been organized around a simple idea: the market keeps trying to value NVIDIA as a semiconductor company, while the business keeps behaving more like infrastructure.

First, there was Silicon, Software, Scarcity: CUDA, systems integration, and control of scarce inputs were the moat. Then came The AI Networking Wars and the Mellanox lesson: the network had become the bottleneck, and NVIDIA’s real product was topology. In Industrialization of Reasoning, the key shift was that inference no longer looked like a lightweight serving workload; reasoning made inference computationally heavy, stateful, and continuous. Finally, in The Tokenization of Software, the argument moved from hardware to software itself: software was moving from pre-recorded to generated, and compute was becoming a revenue engine.

That progression matters because this quarter did not create a new thesis. It clarified the next question.

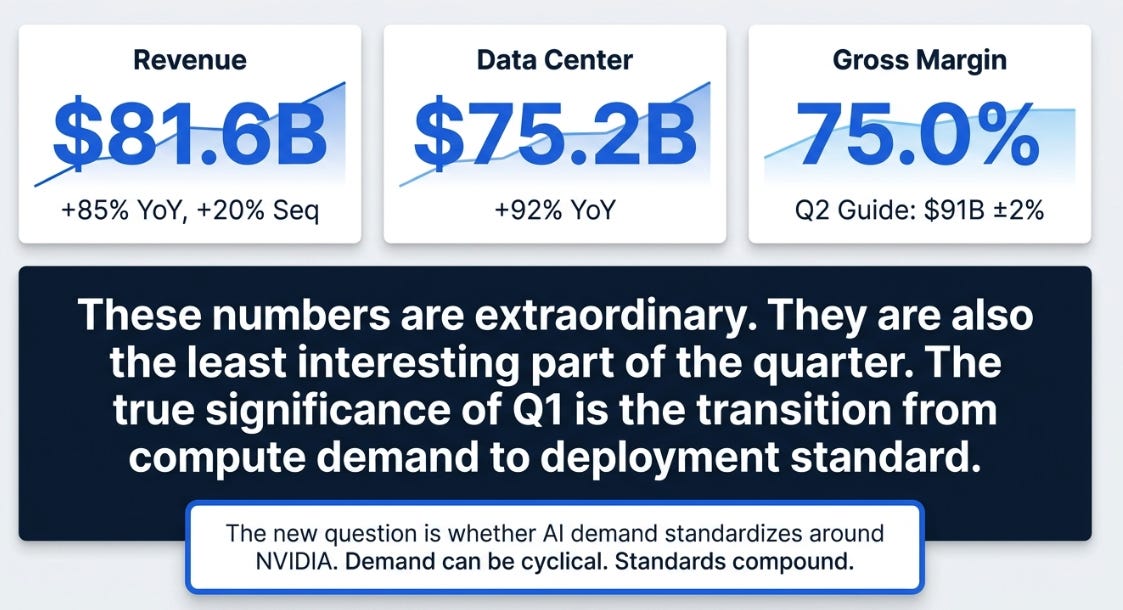

The old question was whether AI compute demand was real and durable. The new question is whether that demand standardizes around NVIDIA.

Demand can be cyclical. Standards compound.

From Compute Demand to Deployment Standard

The fundamental question is this: is agentic AI turning NVIDIA from the leading supplier of GPUs into the default architecture for AI factories, where every new deployment strengthens the software, networking, financing, and developer ecosystem that makes the next deployment more likely to choose NVIDIA?

That is a different question than whether NVIDIA beat estimates. Of course it did. Revenue was $81.6 billion, up 85% year-over-year and 20% sequentially; Data Center revenue was $75.2 billion, up 92% year-over-year; non-GAAP gross margin was 75.0%; and NVIDIA guided the next quarter to $91 billion, plus or minus 2%, while assuming no China Data Center compute revenue.

Those are extraordinary numbers. They are also, in a sense, the least interesting part of the quarter.

The more important point is that AI infrastructure is becoming a system-level market, not a chip-level market. The winning platform is not simply the fastest accelerator; it is the architecture with the best combination of GPUs, CPUs, networking, software, model support, developer ecosystem, utilization, token economics, time-to-production, and financing confidence. NVIDIA’s advantage strengthens at scale because every new deployment expands the installed base, talent pool, software optimization, and interoperability that make NVIDIA the path of least resistance for the next buyer.

This mechanism does not break because someone builds a cheaper chip. It breaks if someone builds a credible alternative ecosystem.

The Missing Metric

Until this quarter, much of the NVIDIA platform thesis had to be inferred. We could see it in networking growth. We could see it in rack-scale systems. We could see it in Jensen Huang’s language around AI factories. We could see it in CUDA, NVLink, Spectrum-X, supply commitments, and ecosystem financing. But we did not have a clean way to separate hyperscaler concentration from broader economic adoption.

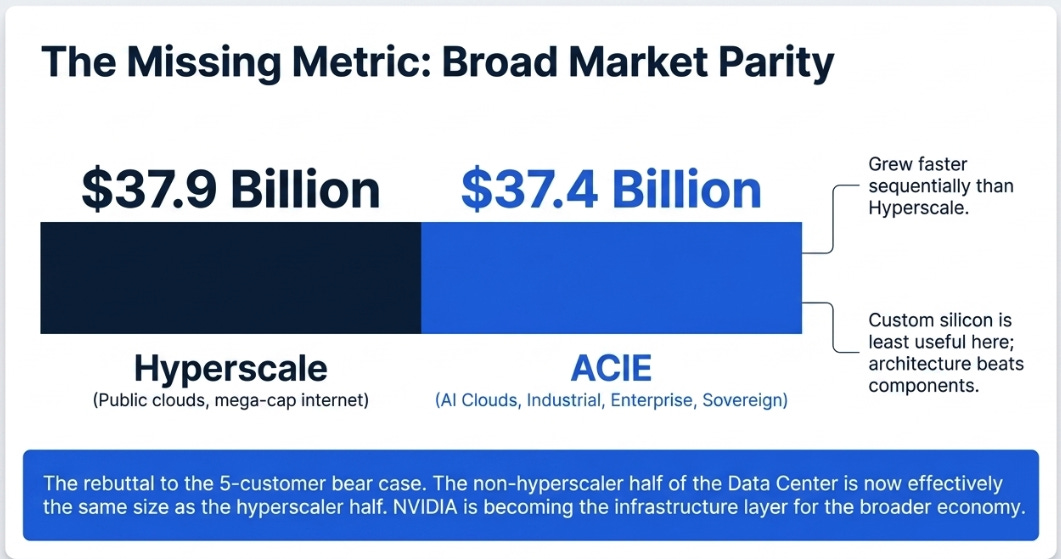

Q1 gave us that missing metric: ACIE.

NVIDIA now reports Data Center across two sub-markets: Hyperscale, which includes public clouds and the largest consumer internet companies, and ACIE, which includes AI Clouds, Industrial, and Enterprise — the broader market of AI-purpose-built data centers and AI factories across industries and countries.

That disclosure is not accounting housekeeping. It is strategic positioning.

Hyperscale revenue was $37.9 billion. ACIE was $37.4 billion. In other words, the non-hyperscaler half of Data Center is already nearly the same size as the hyperscaler half. More importantly, ACIE grew faster sequentially.

This directly addresses the most sophisticated bear case on NVIDIA. The bear case is no longer simply “AI is a bubble.” It is that NVIDIA is a derivative of five or six hyperscaler capex budgets. ACIE is the rebuttal.

If ACIE is durable, NVIDIA is not merely supplying a few mega-cloud customers. It is becoming the infrastructure layer for AI clouds, enterprises, industrial companies, sovereign projects, and eventually physical AI. That matters because this long tail is exactly where custom silicon is least useful. A hyperscaler can design chips, write compilers, tune workloads, and absorb integration complexity. A sovereign AI project, an industrial company, or an enterprise AI cloud mostly wants the thing to work.

That is where architecture beats components.

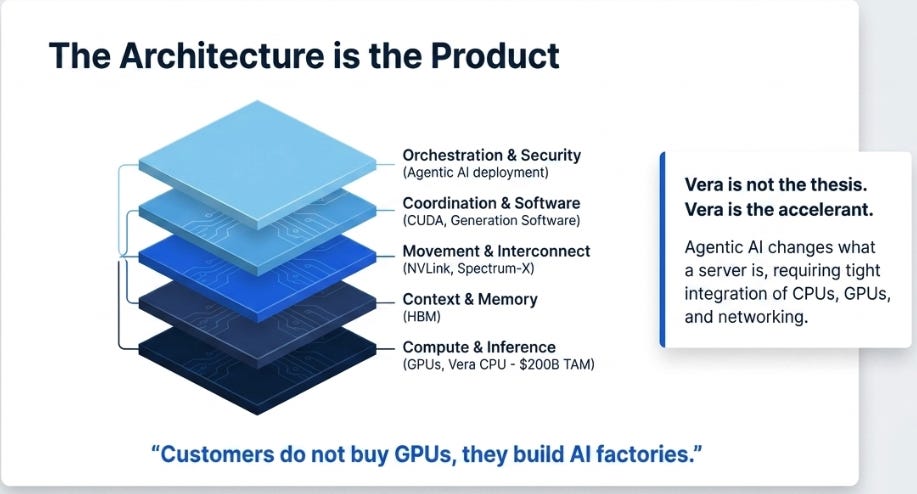

Architecture Is the Product

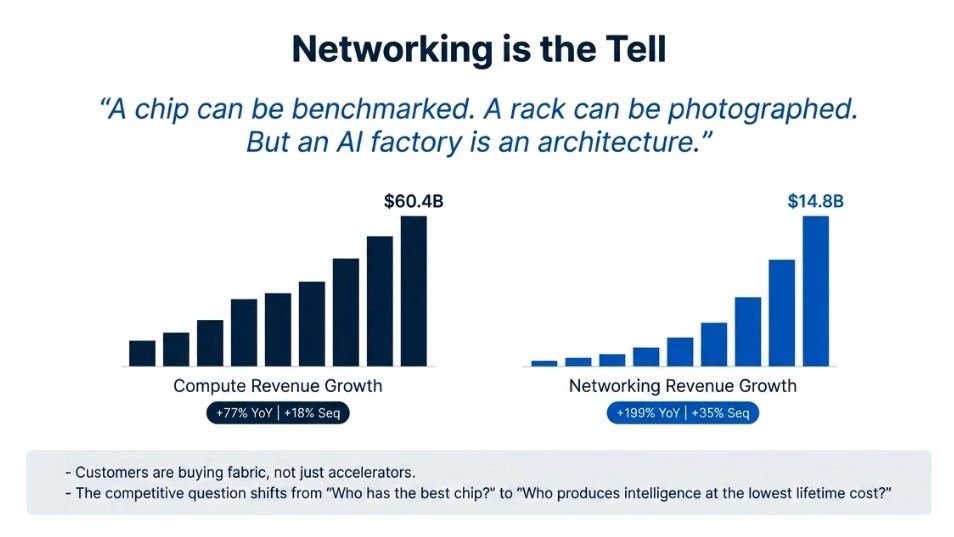

The most revealing number in NVIDIA’s release was not EPS. It was networking.

Under the previous reporting structure, Data Center compute revenue was $60.4 billion, up 77% year-over-year and 18% sequentially. Data Center networking revenue was $14.8 billion, up 199% year-over-year and 35% sequentially.

Networking is the tell. A chip can be benchmarked. A rack can be photographed. But an AI factory is an architecture. It requires compute, memory, interconnect, software, cooling, power density, model support, orchestration, and utilization. The more NVIDIA sells the architecture, the less the competitive question is “who has the best chip?” and the more it becomes “who can make the entire factory produce intelligence at the lowest lifetime cost?”

Jensen made that explicit on the call: customers do not buy GPUs, they build AI factories, and the relevant metric is not GPU purchase price but the lifetime economics of producing intelligence — tokens per watt, tokens per dollar, uptime, utilization, time to production, software durability, and asset life.

This is why Vera matters, but also why it should not be overstated. Vera is not the thesis. Vera is the accelerant.

Management framed Vera as a CPU purpose-built for agentic AI, opening a $200 billion TAM, with visibility to nearly $20 billion in total CPU revenue this year. That sounds like a new business line, and perhaps it will be. But the more important point is architectural: agentic AI changes what a server is. Agents need CPUs for orchestration, GPUs for inference, networking for movement, memory for context, software for coordination, and security for deployment. NVIDIA’s ambition is not to sell the best component. It is to define the system.

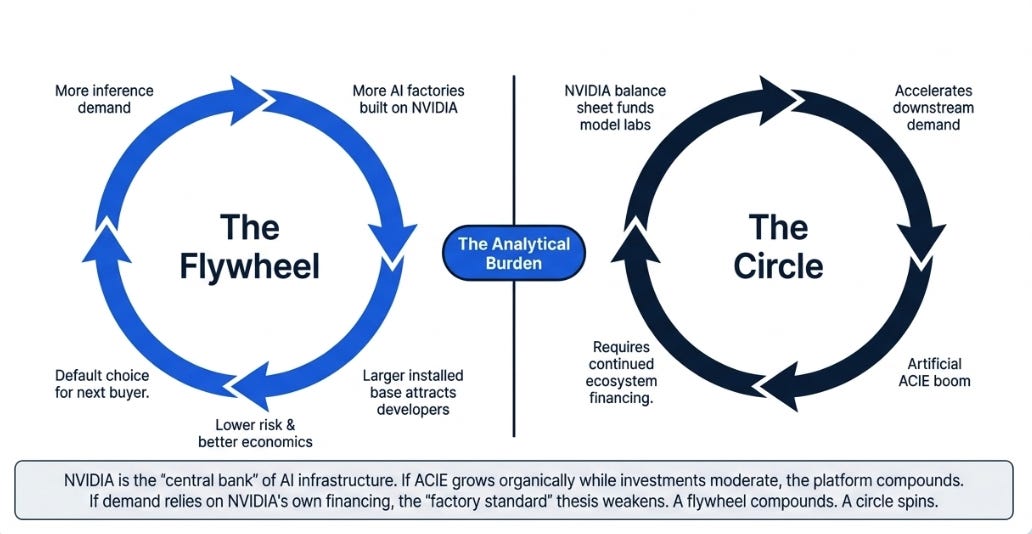

The Flywheel and the Circle

The NVIDIA flywheel is becoming clearer.

More agentic workloads create more inference demand. More inference demand requires more AI factories. More AI factories built on NVIDIA expand the installed base. A larger installed base attracts more CUDA optimization, libraries, developers, model support, and financing confidence. Better ecosystem support lowers deployment risk and token cost. Lower risk and better economics make NVIDIA the default choice for the next deployment.

Most hardware businesses weaken at scale because scale attracts competition and compresses margins. NVIDIA’s bet is that this market works differently: scale makes the architecture more useful.

That is the upside. The risk is that a flywheel can start to look like a circle.

We previously called NVIDIA the “central bank” of AI infrastructure because the company was not merely selling into the ecosystem; it was helping organize it. That was, and remains, part of the moat. NVIDIA secures supply, funds model labs, supports AI clouds, and accelerates downstream demand. But as the ecosystem gets larger, that same mechanism requires more scrutiny. The company’s Q1 private-company and infrastructure-fund investments raise the right question: how much of the ACIE boom is self-sustaining, and how much is being accelerated by NVIDIA’s own balance sheet?

This is not an accusation. It is the next analytical burden.

A flywheel compounds. A circle spins.

The distinction will be visible over the next few quarters. If ACIE continues to grow while ecosystem investments moderate, the platform thesis strengthens. If ecosystem investments keep rising while ACIE slows, the bear case becomes more serious.

What Changed in Our View

Our view has not changed directionally. It has matured.

We already believed NVIDIA was not a chip company. Q1 gives us a better way to test whether that view is right. We already believed networking was the tell. Q1 confirmed that customers are buying fabric, not just accelerators. We already believed generated software turns compute into a revenue engine. Agentic AI makes that demand more continuous. We already believed NVIDIA’s balance sheet was part of the moat. Q1 makes clear that it is also part of the risk.

The shift is subtle but important: we have moved from a demand thesis to a standardization thesis.

The demand thesis says software is becoming generated, and therefore the world needs more compute. The standardization thesis says that as the world builds that compute, it may increasingly standardize around NVIDIA’s architecture.

The first thesis makes NVIDIA larger. The second makes NVIDIA harder to replace.

The Variant Perception

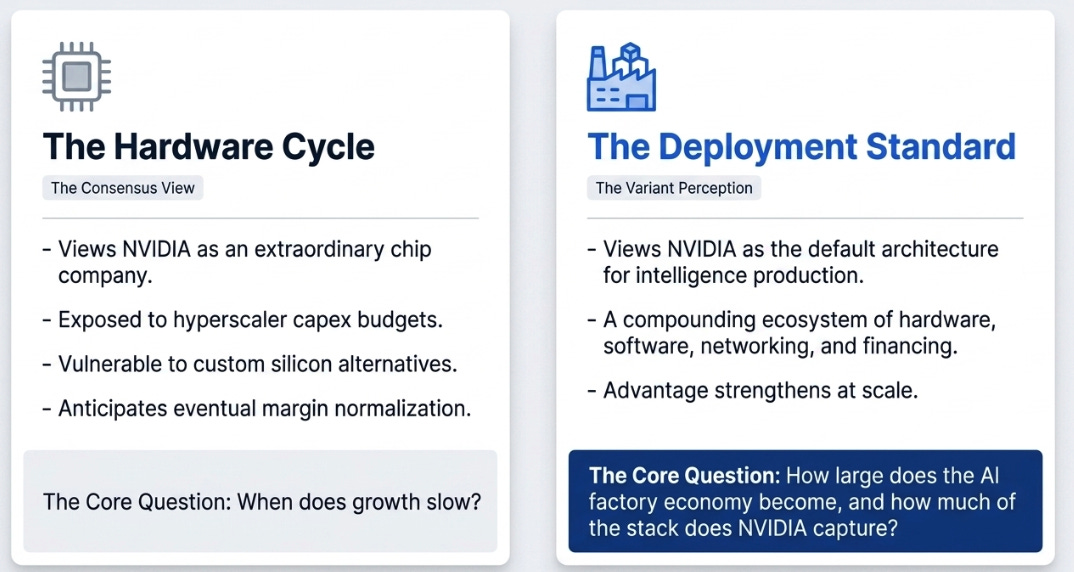

Consensus sees an extraordinary AI chip company, but one still exposed to hyperscaler capex, custom silicon, and eventual margin normalization.

Our view is different. NVIDIA is trying to become the default architecture for intelligence production. The durable advantage is not simply Blackwell, or CUDA, or Spectrum-X, or Vera. It is the compounding effect of all of them together: hardware, software, networking, model support, developer familiarity, financing, and deployment experience reinforcing one another.

If NVIDIA is a hardware-cycle company, the right question is when growth slows. If NVIDIA is becoming a deployment standard, the right question is how large the AI factory economy becomes and how much of the stack NVIDIA captures.

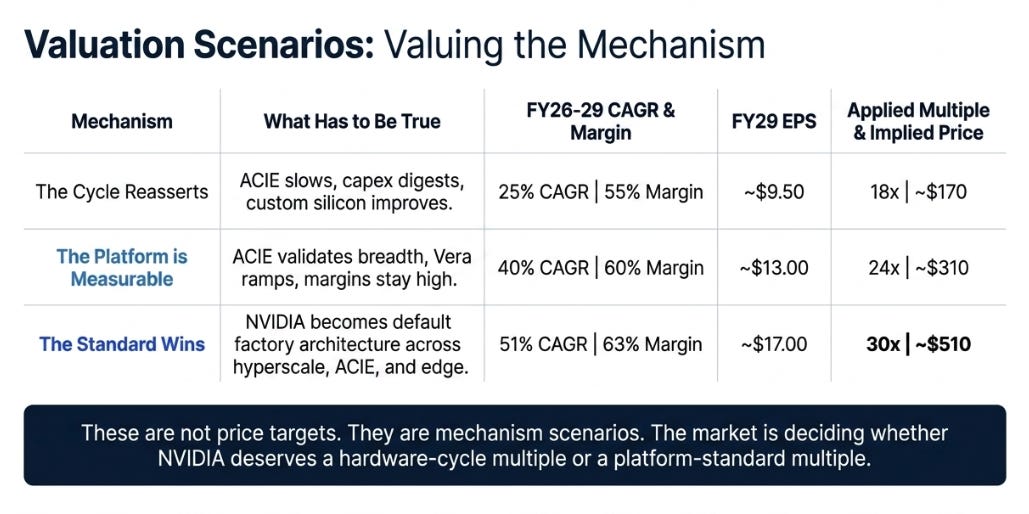

What the Mechanism Might Be Worth

The valuation range depends less on Q1 EPS and more on which mechanism wins.

These are not price targets. They are mechanism scenarios. The spread exists because the market is not deciding whether NVIDIA can beat a quarter. It is deciding whether NVIDIA deserves a hardware-cycle multiple or a platform-standard multiple.

The Next Test

The next quarter is not about whether NVIDIA beats. That bar has become almost irrelevant. The real test is whether Q1’s new disclosure gets a second data point.

ACIE needs to keep growing faster than the market expects. Networking needs to keep outgrowing compute. Rubin and Vera need to ramp without damaging the margin structure. Gross margins need to stay around the mid-70s, with a real concern if they fall below 74% and a more serious issue below 72–73%. Free cash flow needs to remain strong, and DSOs need to stay under control. Most importantly, ecosystem investments need to look like accelerants, not support beams.

NVIDIA’s Q1 was not important because the company beat estimates. It was important because it gave us a new way to test the thesis we have been building for the last year.

We thought NVIDIA was selling the infrastructure for generated software. That remains true. But the bigger possibility is that NVIDIA is becoming the default architecture for intelligence production.

That distinction matters. Demand can fade. Standards compound.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.