Oracle’s 3QFY26 Earnings: The Monetization Bridge

Q2 exposed the capital problem. Q3 offered the first believable answer: a way to monetize AI demand without funding every mile of the buildout alone.

TL;DR

OCI growth confirmed the demand story: cloud infrastructure accelerated to 84% growth, while AI and multi-cloud database adoption continued scaling rapidly.

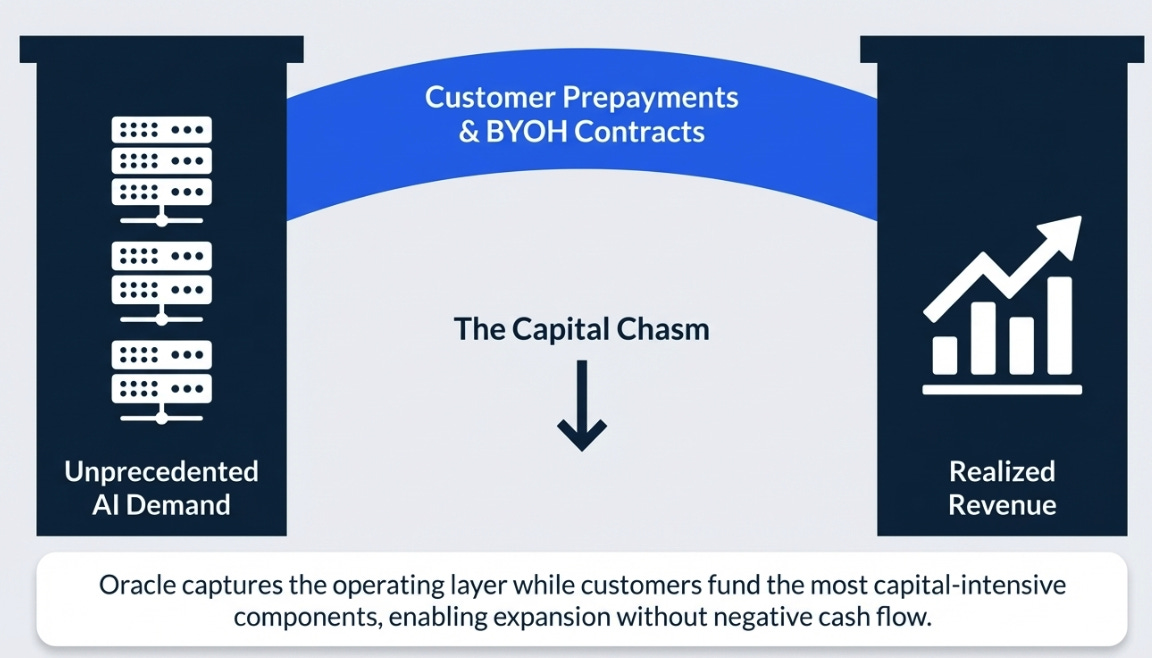

The real change was structural: large AI contracts increasingly use customer-funded GPUs or upfront prepayments, shifting capital intensity away from Oracle.

If BYOH scales: Oracle evolves from capital-constrained builder to AI infrastructure orchestrator, with backlog converting into revenue without the same balance-sheet strain.

Q2 was the quarter where Oracle’s AI story became impossible to dismiss and impossible to own comfortably. The demand was real; the balance-sheet burden suddenly was too. Q3 matters because Oracle finally showed what the bridge across that gap might look like.

That is the real update to the view.

What We Said Going In

Our prior thesis had three chapters. The AI Tollbooth: Oracle sat at the control point between decades of mission-critical enterprise data and the AI models that needed it. Strategic Vindication: the architecture Oracle built between 2016 and 2020, optimized for high-performance, data-intensive workloads, turned out to be precisely what the AI era demanded. And the Capital Chasm: the demand was unmistakably real, but Oracle had begun to look like a company that found the future and might strain its balance sheet building it.

Our variant going in was specific: the market was pricing a funding crisis, but the $553 billion RPO was effectively collateral for financing not yet announced. We expected a specific Stargate joint venture or sovereign wealth fund disclosure to be the binary catalyst.

We got the financing. The $30 billion raise was oversubscribed before the quarter even closed, at investment grade, with bond investors, who are smarter than equity markets about credit risk, effectively voting on that backlog’s collateral value. The cleanest version of the bear thesis weakened sharply. On that, we were right.

What we got wrong was the structure of the answer. We expected a one-time JV announcement. What Oracle revealed was a recurring business model shift: customers prepaying for capacity, or supplying their own GPUs, with Oracle providing the operating layer on top. That is more durable than a single financing event. A JV solves one capital problem. A structural model change means the capital problem recurs less often. We will take being wrong in that direction.

The Numbers

The subtitle above is the quarter. What follows is the evidence.

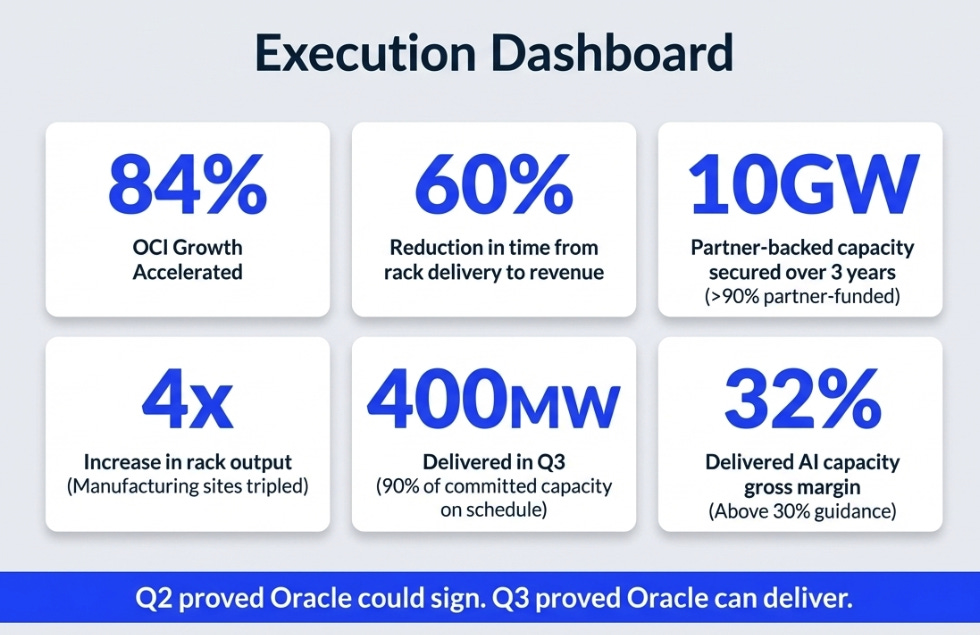

OCI growth accelerated to 84%. Free cash flow deteriorated to negative $24.7 billion trailing. Both numbers matter. Only one was surprising.

Oracle kept FY26 revenue guidance at $67 billion, kept FY26 capex at $50 billion, and raised FY27 revenue guidance to $90 billion. This was the first quarter in more than 15 years where both organic revenue and non-GAAP EPS grew 20% or more in USD. The growth story is no longer in question. What this quarter needed to answer was whether the model underneath that growth was becoming more or less sustainable. That is a different question, and it got a different kind of answer.

The Problem Was Never Demand

Our previous arc was right on strategy and too optimistic on economics. Oracle clearly found a privileged place in the AI stack: close to enterprise data, useful to the model layer, more relevant in the age of agents than the market appreciated when it was still grading the company as a late cloud entrant. Q2 proved that. The problem was that Oracle then looked like a company that had discovered the future and might strain the balance sheet building it.

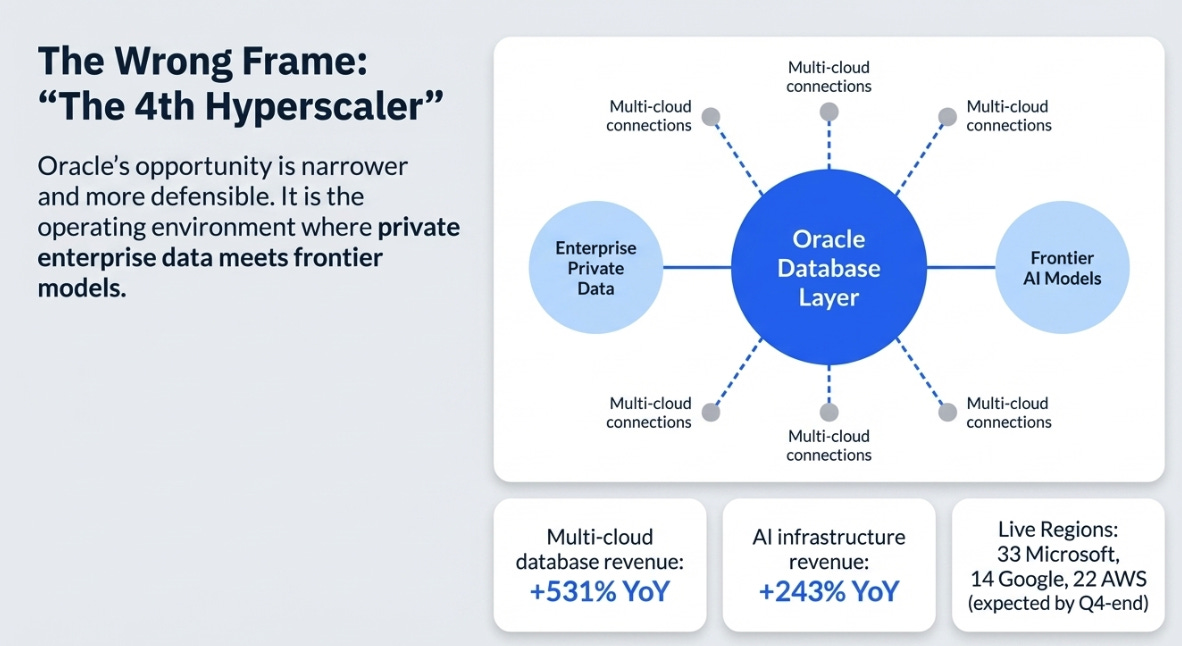

Q3 did not answer “is demand real?” That debate is over. Multi-cloud database revenue grew 531% year over year. AI infrastructure revenue grew 243%. Oracle now has 33 Microsoft regions live, 14 Google regions live, and AWS went from 2 live regions at the start of Q3 to 8 by quarter-end, with 22 expected by Q4-end.

The market still frames Oracle as if the relevant question is whether it can become the fourth hyperscaler. That is the wrong frame. Oracle’s real opportunity is narrower, more strategic, and more defensible: the multi-cloud database layer, the enterprise data control point, and the operating environment where private data meets frontier models. Oracle is not building another AWS. It is building the place enterprises go when they want to use the best models without surrendering control of their most valuable data, where vector embeddings, MCP access, advanced security controls, and data co-located with agents are the requirements, not the differentiators. That is a use case Oracle’s architecture is unusually well aligned to serve, which is different from saying competitors cannot address it, but does suggest Oracle holds structural advantages that most coverage has underpriced.

A Better Kind of Backlog

A $553 billion backlog is no longer interesting because it is huge. It is interesting if it is becoming better.

That is what changed this quarter. The most important sentence in the press release was not about OCI growth. It was this: most of the increase in Q3 RPO came from large-scale AI contracts where Oracle does not expect to raise incremental funds, because the equipment is either funded upfront through customer prepayments or bought directly by customers and supplied to Oracle.

That sentence is the quarter.

Since the last call, Oracle signed more than $29 billion in contracts under this structure, bring-your-own-hardware and upfront customer payments, enabling expansion, in Magouyrk’s words, “without any negative cash flow from Oracle.”

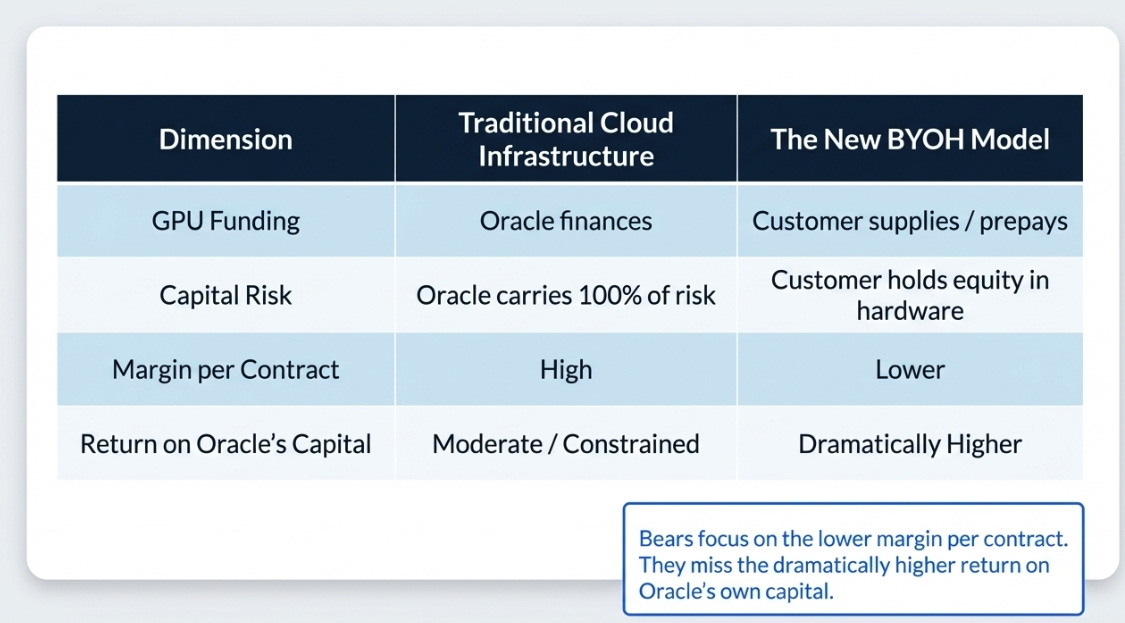

Think about what this means structurally. In the old model, Oracle finances the GPUs, builds the data center, sells cloud capacity, carries all the capital risk. In the new model, the customer supplies the GPUs, Oracle provides the facility, network, database, and software stack. The customer has equity in the hardware sitting inside Oracle’s building. Oracle captures the operating and software layer without deploying the most capital-intensive component. Lower margin per contract, but dramatically higher return on Oracle’s own capital. That distinction has not made it into consensus models, and it is the intellectual center of why Q3 represents an inflection rather than just an acceleration.

The bears were right that this affects margins. What they missed is that it changes Oracle’s return on its own capital entirely. Those are not the same thing, and treating them as equivalent is where the bear case has been analytically imprecise.

The Delivery Quarter

The smartest thing Oracle did on this call was not claim demand exceeds supply. Everyone knew that. It gave the market an actual operating bridge from demand to revenue.

More than 10 gigawatts of partner-backed capacity secured over three years. More than 90% of that capacity funded through partners. Manufacturing sites tripled. Rack output up 4x. Time from rack delivery to revenue down 60%. More than 400 MW delivered in Q3. 90% of committed capacity on or ahead of schedule. Delivered AI capacity at 32% gross margin, above the prior 30% guidance.

Q2 proved Oracle could sign. Q3 is the first quarter that suggests Oracle can deliver. The stock no longer needs promotion. It needs sequencing. Oracle finally provided it.

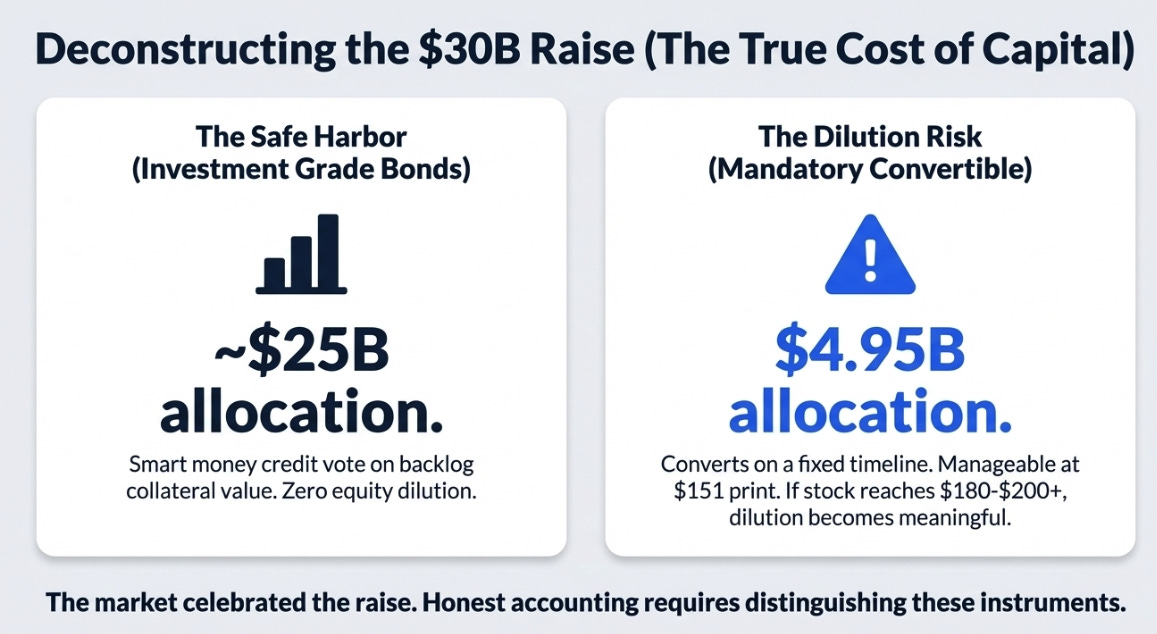

One financing detail deserves more attention than it has received. The $30 billion raise comprised two instruments that are not equivalent. The investment-grade bonds carry no dilution. The $4.95 billion mandatory convertible preferred stock will convert to common equity on a fixed timeline, regardless of stock price. At $151 heading into this print, the conversion terms are manageable. At $180-200+, the dilution becomes more meaningful. The market celebrated the oversubscribed raise without distinguishing between the two instruments. That distinction matters, and it belongs in any honest accounting of what the financing actually cost.

The Hidden Second Leg

The easiest mistake after this quarter is thinking it was all OCI. It was not.

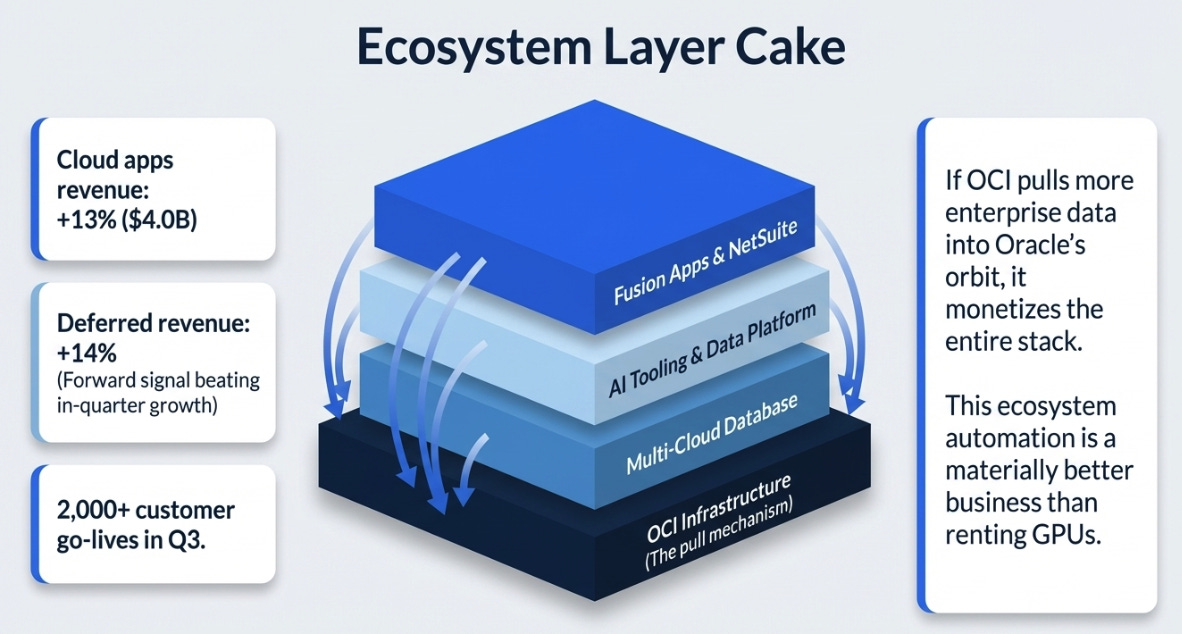

Cloud applications revenue grew 13% to $4.0 billion. Fusion ERP grew 17%. NetSuite grew 14%. More tellingly, cloud applications deferred revenue grew 14% in constant currency, faster than in-quarter revenue growth of 11%, which is the forward signal most coverage skipped. More than 2,000 customer go-lives in the quarter. Management repeatedly framed these not as single-app wins but as “ecosystem automation” conversations combining OCI, AI Data Platform, Fusion Applications, industry suites, database, and AI tooling together.

If OCI pulls more enterprise data into Oracle’s orbit, Oracle doesn’t just monetize the compute. It monetizes the database, the tooling, the applications, and the workflows around them. That is a materially better business than renting GPUs, and the applications trajectory suggests it is beginning to compound.

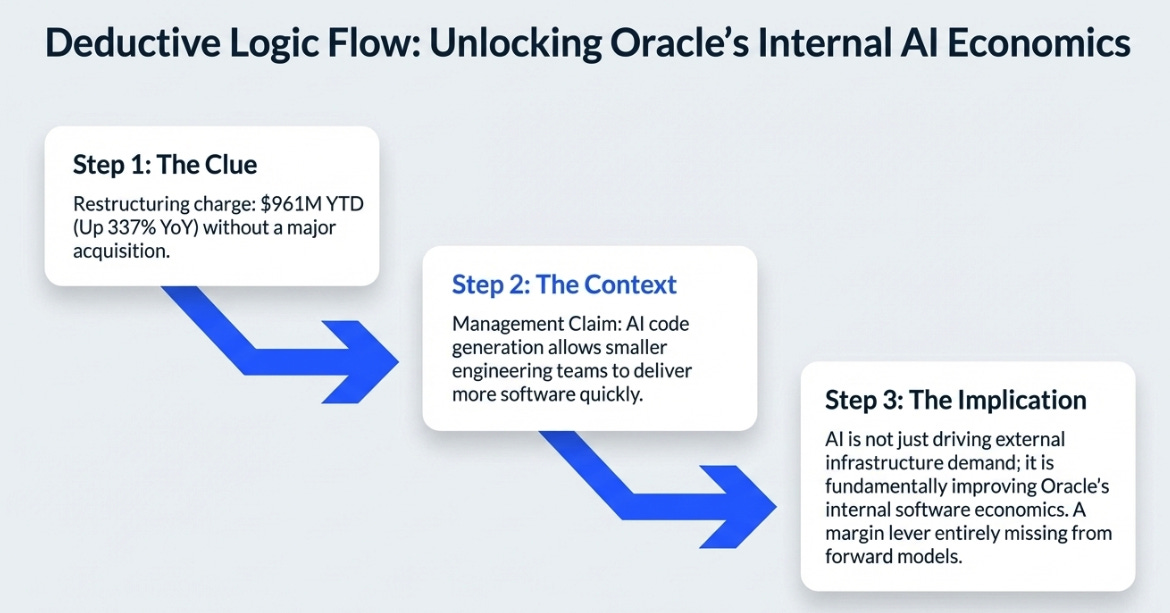

There is a second margin lever that one plausible reading of the numbers supports: Oracle’s restructuring charge is $961 million year-to-date, up 337% YoY, without a major acquisition to explain it. Management said AI code generation is allowing smaller engineering teams to deliver more software more quickly. If that is what is happening at scale, and the new product output this quarter is at least consistent with the claim, then AI may not just be driving Oracle’s infrastructure demand. It may also be improving Oracle’s own software economics in ways that don’t yet appear in any forward model. That is inference, not proof. But it is the kind of inference worth tracking.

Variant Perception

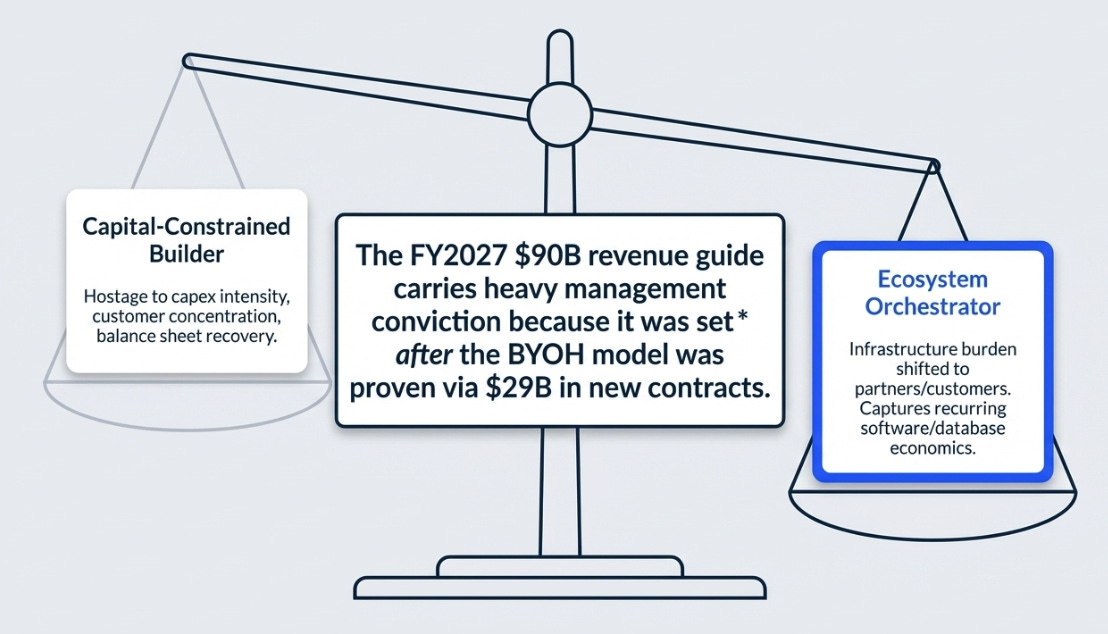

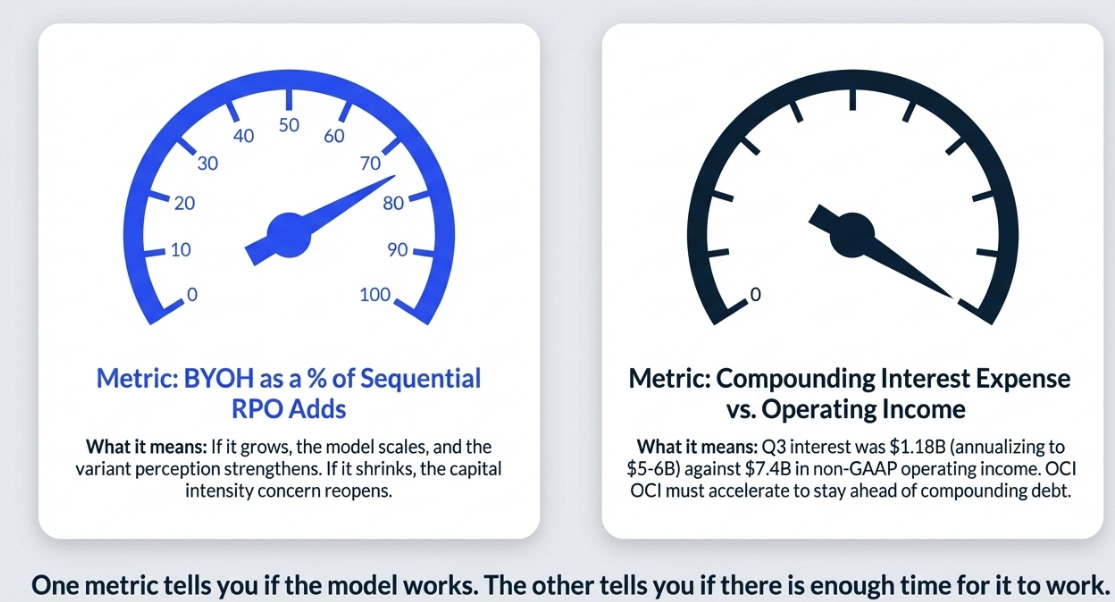

Consensus sees Oracle as a cloud infrastructure winner with a recovering balance sheet, still hostage to capex intensity, customer concentration, and backlog-conversion uncertainty. The more interesting framing is that the market remains anchored to Oracle-as-capital-constrained-builder and has not fully updated to Oracle-as-orchestrator, a company where more of the infrastructure burden may increasingly sit with customers and partners while Oracle captures the recurring cloud, database, and software economics on top. If that is right, the FY2027 $90 billion guide carries more management conviction than the market realizes, because it was set after the BYOH model was already in place for $29 billion of new contracts. The silent risk to that framing is interest expense: $1.18 billion in Q3, annualizing toward $5-6 billion against $7.4 billion in non-GAAP operating income, growing with every quarter the existing debt load compounds. The BYOH model helps on new contracts. It does not reduce the cost of servicing what is already on the balance sheet.

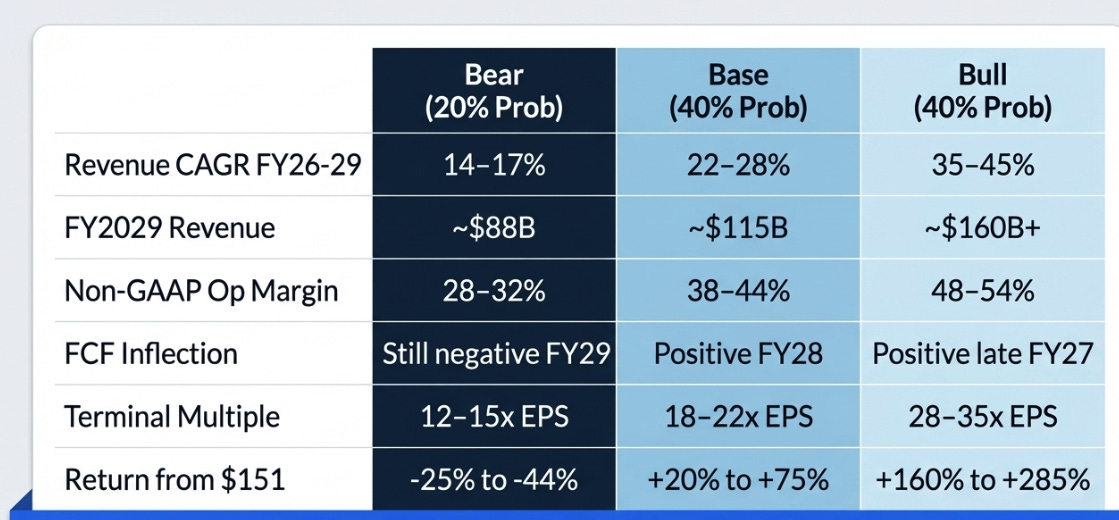

Three-Year Scenarios

The bear doesn’t require Oracle to fail outright. It requires the BYOH model to prove narrower than management suggests, effective for a handful of mega-deals but not scalable as a standard contract structure, forcing Oracle back to self-funded capex just as $134 billion in debt demands full servicing. Add AI inference efficiency gains eroding compute demand faster than new use cases emerge, and the equity story compresses toward a leveraged utility multiple. The bear case is narrower than it was six months ago. It is not gone.

The base assumes BYOH becomes roughly 40% of new RPO, OCI sustains above 60% growth through FY2027 then moderates, multi-cloud database reaches $8-10 billion annualized by FY2029, and software margins expand 300-400 basis points from AI-driven R&D efficiency. This is a good business with a complicated balance sheet that slowly resolves. The re-rating is real but partial.

The bull requires OpenAI to remain the dominant AI model company, begin its $300 billion commitment on schedule, and the BYOH structure to become the standard contract form for large AI deals, not the exception. If those three things happen simultaneously, Oracle re-rates from legacy software toward a full-stack enterprise AI platform multiple. The probability-weighted expected return across all three scenarios is approximately +85% over three years, or ~23% annualized, with upside/downside skew of roughly 3x.

What We Think Now

The single number that will tell us whether this thesis is holding is BYOH as a percentage of sequential RPO adds. If it grows quarter over quarter, the model is scaling and the variant is strengthening. If it shrinks, if Oracle reverts to self-funding incremental growth in Q4 or Q1 FY27, the capital intensity concern reopens immediately and the base case becomes the ceiling rather than the midpoint. The number that could quietly undermine everything else, regardless of BYOH trajectory, is interest expense. It doesn’t announce itself. It just compounds, quarter after quarter, against an operating income line that needs OCI to keep accelerating to stay ahead of it. Watch both numbers. One tells you whether the model is working. The other tells you whether there is enough time for the model to work before the balance sheet demands its answer.

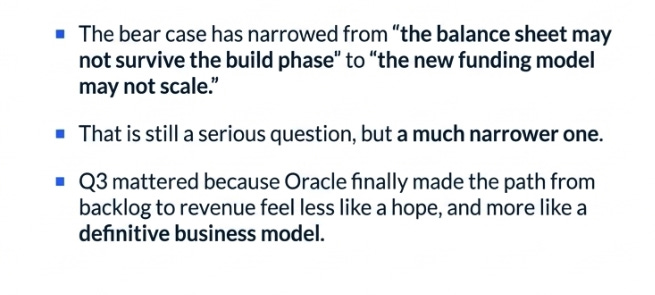

What we thought before was that Oracle had discovered a strategically privileged position in AI but risked letting capital intensity overwhelm the equity story. What we think now is that risk is still present, but Q3 is the first quarter where Oracle showed a believable way around it. The story is no longer simply “Oracle has huge demand.” It is now “Oracle may have found a way to keep the upside while outsourcing more of the funding burden.” That is a real change. The bear case has narrowed from “the balance sheet may not survive the build phase cleanly” to “the new funding model may not scale as broadly as management suggests.” That is still a serious question. But it is a much narrower one.

And that is why Q3 mattered. Not because Oracle beat. Because Oracle finally made the path from backlog to revenue feel more like a business model and less like a hope.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.