Oracle's 4QFY26 Earnings: The Price of the Moat

Oracle found a bridge across the capital chasm. Q4 asked whether shareholders get across too.

TL;DR

Q4 validated Oracle’s AI “bridge,” but not for free: customer-funded / customer-supplied GPU contracts are now real enough to support the $638B RPO story, but Oracle still needs heavy financing, including more debt and equity issuance.

The core debate is identity: Oracle is part sticky enterprise-data compounder, part capital-intensive AI infrastructure builder. The stock depends on whether infrastructure spending deepens the high-margin data moat or simply turns Oracle into a leveraged GPU landlord.

Watch cash-flow mechanics, not headline beats: the key tells are BYOH share of new RPO, RPO conversion, net CapEx discipline, ATM dilution, multi-cloud DB disclosure, and whether interest expense compounds faster than operating income.

Oracle beat on revenue, EPS, and operating income, and posted a backlog, $638 billion of remaining performance obligations, that would have been unimaginable for a legacy software company a few years ago. The stock fell anyway.

The easy explanation is “good quarter, scary CapEx.” True, but not enough. The better read is that this is the next answer in a sequence. Over the past year Oracle has retired its risks one by one: first whether the AI demand was real, then whether it could deliver against it, now whether it can finance the delivery without giving away too much of the upside. The answer after Q4 is yes, with asterisks. Financeability is possible, not yet cheap, not yet self-funded, not yet fully equity friendly. Those asterisks are the entire debate.

What We Have Been Updating

We owe a word on our own arc first. In Q2 we argued Oracle had found the future but might strain its balance sheet building it, the Capital Chasm. In Q3 the company gave the first believable answer: large AI contracts could use customer-funded or customer-supplied GPUs, with Oracle providing the operating layer on top. That was the Monetization Bridge, and it changed the question from whether Oracle could sign AI demand to whether it could monetize it without funding every mile of the buildout alone.

Q4 validates that mechanism and raises the bar. We were right about the bridge; we underestimated the weight. A fair reader should ask whether this is refinement or rationalization, and the honest answer is that each quarter has not moved the goalposts so much as revealed the next layer beneath them. Demand was real. Delivery improved. BYOH scaled. But a better funding model is not a self-funding business, and we should also admit we have drifted steadily more bullish across these four quarters. Hold that drift in view; it is why the conclusion must be handed to you rather than asserted.

The Data Business and the Infrastructure Bill

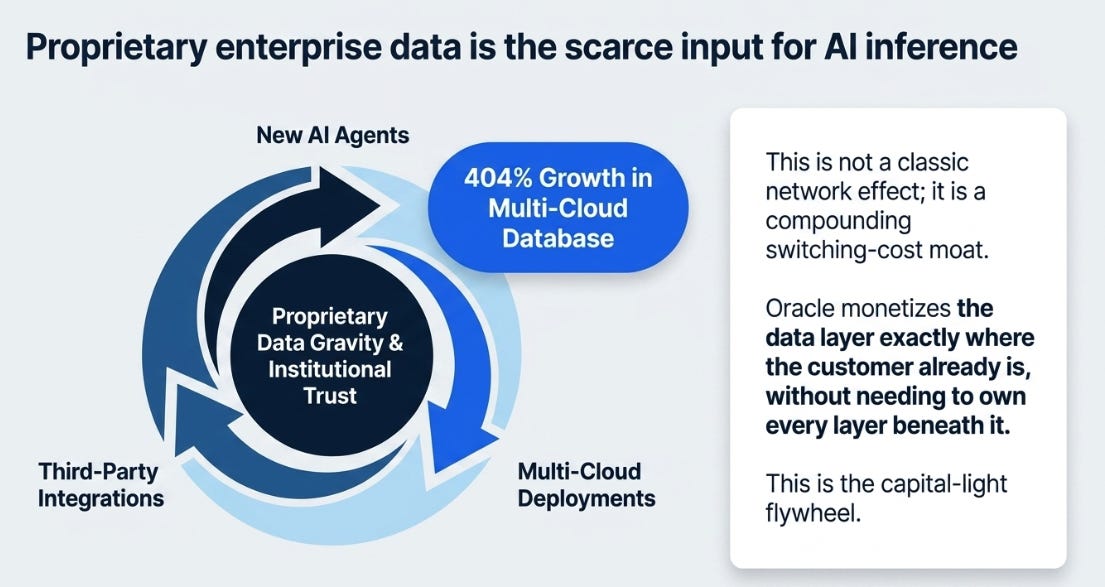

Oracle becomes more valuable as AI grows if proprietary enterprise data becomes the scarce input for useful inference, and much of that data already sits in Oracle databases, applications, and workflows. Every new agent, integration, and multi-cloud deployment raises the cost of leaving. This is not a classic network effect; it is a compounding switching-cost moat built on data gravity and institutional trust. The strongest evidence this quarter was not OCI growth but multi-cloud database growing 404%, Oracle’s database running where the customer already is, monetizing the data layer without owning every layer beneath it. That is the capital-light flywheel.

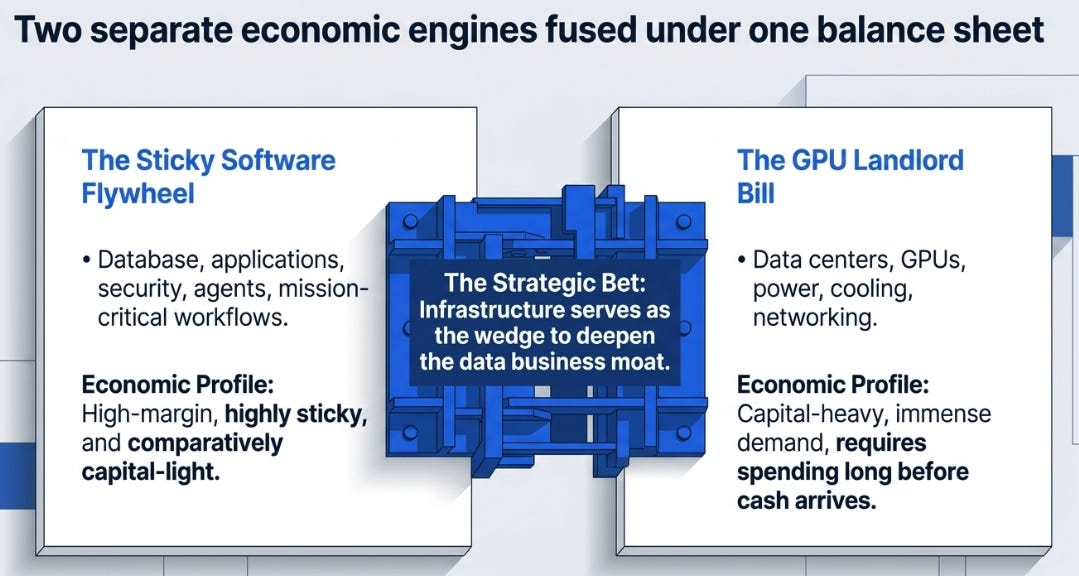

The discomfort is that Oracle has chosen to protect that flywheel with a capital-heavy buildout. There are two companies inside Oracle, with opposite economics. One deserves the premium, database, multi-cloud database, applications, agents, security, mission-critical workflows: sticky, high-margin, comparatively capital-light. The other consumes the capital, data centers, GPUs, power, cooling, networking: enormous demand, but closer to infrastructure than software, and requiring the spend before the cash arrives. Oracle has fused them by choice. That is the strategic bet: the infrastructure business is the wedge that deepens the data business, win the AI deal, anchor the database, application, and security relationship around it. This is why “GPU landlord” is too simple a slur; it misses the power, networking, identity, operations, and database adjacency wrapped around the chips. But the market is right to press the harder question: if the build is the moat around the data business, how much must Oracle spend before shareholders enjoy the moat? The logic is sound. The financing window is the whole game.

A Better Backlog, not a Free One

The most important confirmation in Q4 is that Q3’s bridge was not a one-quarter artifact. Most of the RPO increase in both quarters came from contracts where customers prepaid for or supplied the GPUs, and the cumulative prepaid-and-customer-supplied pool now stands at $75 billion. We still don’t have the full forward mix, but that is enough to validate the bridge: customer-funded hardware is no longer a theoretical answer to the chasm.

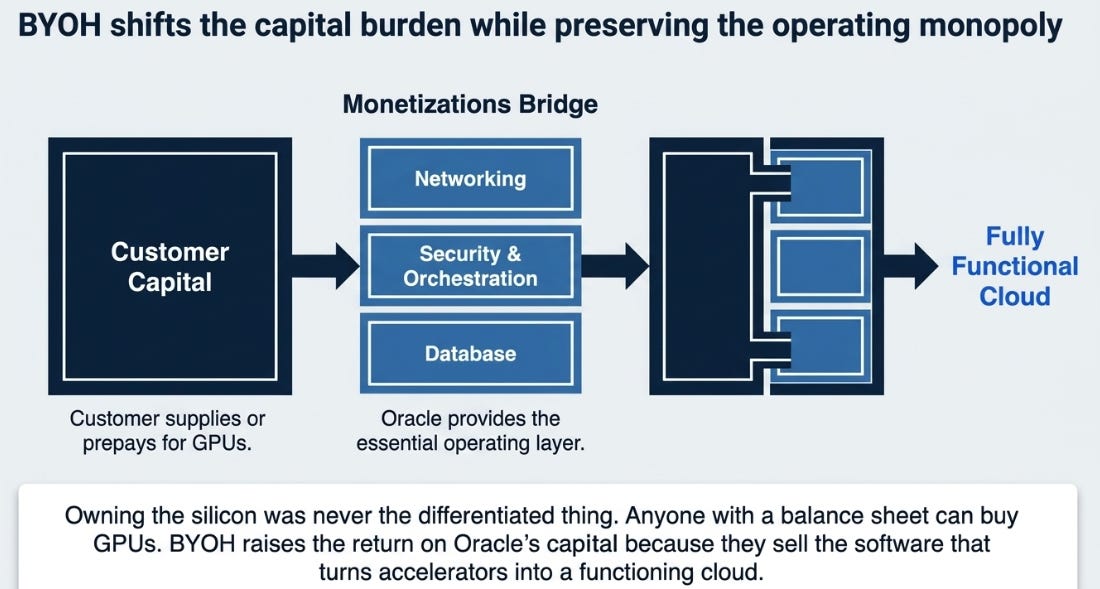

Read what it means, not just what it measures. When Oracle shifts GPU capital to the customer, it concedes, through contract structure, where concessions are most honest, that owning the silicon was never the differentiated thing. Anyone with a balance sheet can buy GPUs. What Oracle sells is the operating layer: networking, security, orchestration, database, the software that turns accelerators into a functioning cloud. Bears focus on lower margin per contract; the better question is return on Oracle’s own capital. If customers fund the most expensive component and Oracle earns attractive economics on the operating layer, BYOH raises the return on Oracle’s capital even as the income statement looks less software-like. That inverts the landlord fear we ourselves carried: the risk is not that BYOH makes Oracle too capital-heavy, but that the market may still be pricing a capital-light operator as if it were buying every GPU itself.

Q4 also drew the limit. BYOH changes the return on Oracle’s capital; it does not make Oracle capital-light. If the model solved the problem outright, Oracle wouldn’t still need another large financing year, $43 billion of debt and $5 billion of equity raised in FY26, roughly $40 billion more planned for FY27 including a $20 billion at-the-market equity program. The bridge is real. It is not free. And this is how to read the new “net cash outlay for CapEx” metric: useful, because it separates what Oracle must fund from what customers prepay, but free cash flow remains the shareholder’s lens. Net CapEx explains funding; free cash flow explains ownership. That Oracle needs the former does not make the latter irrelevant, and the latter was negative $23.7 billion.

So RPO has changed meaning. It is collateral, obligation, and temptation at once, collateral because it supports financing, obligation because Oracle must deliver against it, temptation because the larger it grows, the more seductive it becomes to build ahead of cash conversion. That is the Capital Chasm in a more sophisticated form.

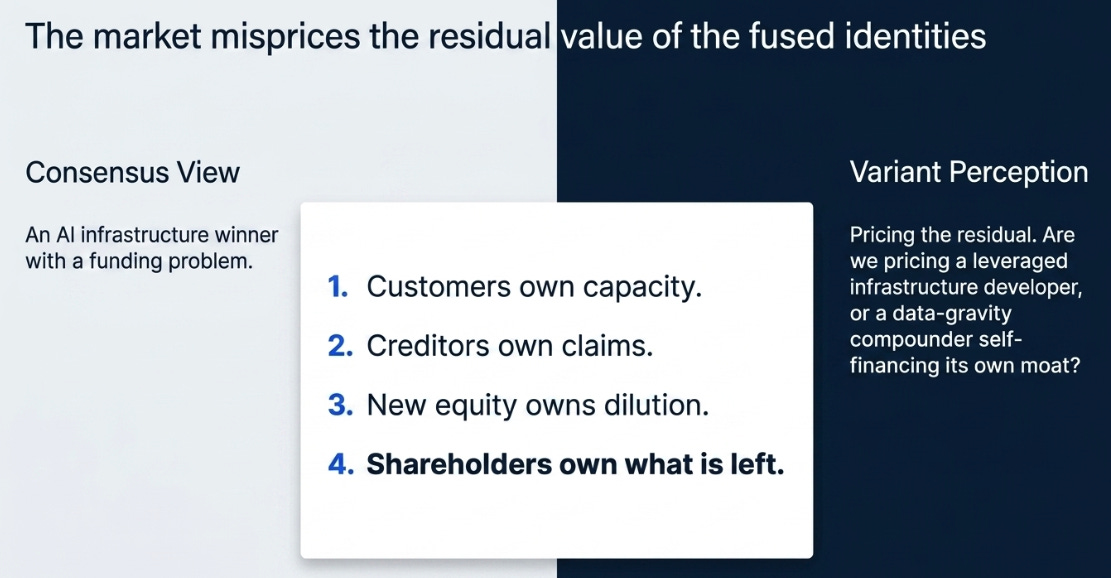

Variant Perception

Consensus sees an AI infrastructure winner with a funding problem. Not wrong; incomplete. The funding problem is real, and the market is right to put Oracle in the penalty box. The variant question is what that box is. Customers own capacity. Creditors own claims. New equity owns dilution. Shareholders own what is left. The whole debate is whether that residual is correctly priced as the leftover of a leveraged infrastructure developer, or wrongly discounted because the market cannot see the data-gravity compounder underneath, the one self-financing its own moat. If Oracle is renting GPUs, the multiple should compress. If it is using infrastructure as the wedge to deepen its grip on enterprise data, the CapEx is not spending, it is the price of the moat. Both readings are plausible on today’s evidence. That is why Q4 mattered: it did not settle the debate. It made it investable.

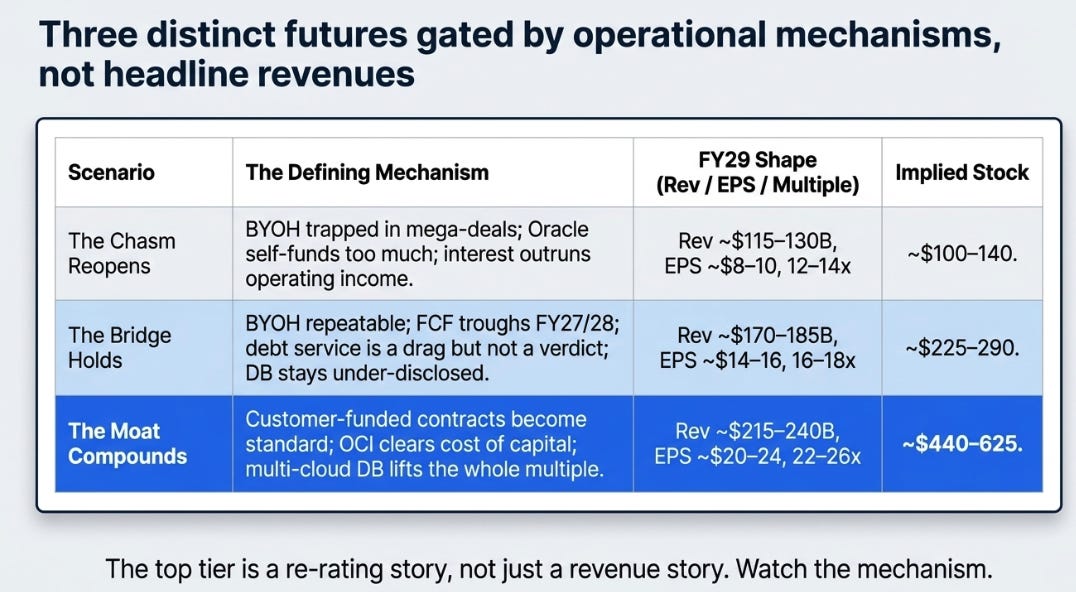

Three Futures

The honest scenarios aren’t bull, base, and bear, that’s too mechanical. Oracle’s future turns on which identity wins, and each below is gated by a mechanism, not a revenue line.

The point isn’t precision; it’s that each world is gated by a different mechanism, the share of BYOH, the direction of margin, the pace of conversion, the execution of the ATM, the race between interest and operating income. The top tier is mostly a re-rating story, not a revenue story; know that when you weigh it. Watch the mechanism, not the revenue.

What We Think Now

After Q3 we thought Oracle had found a believable way across the chasm. After Q4 we still think so, but the bridge must carry more weight than we appreciated.

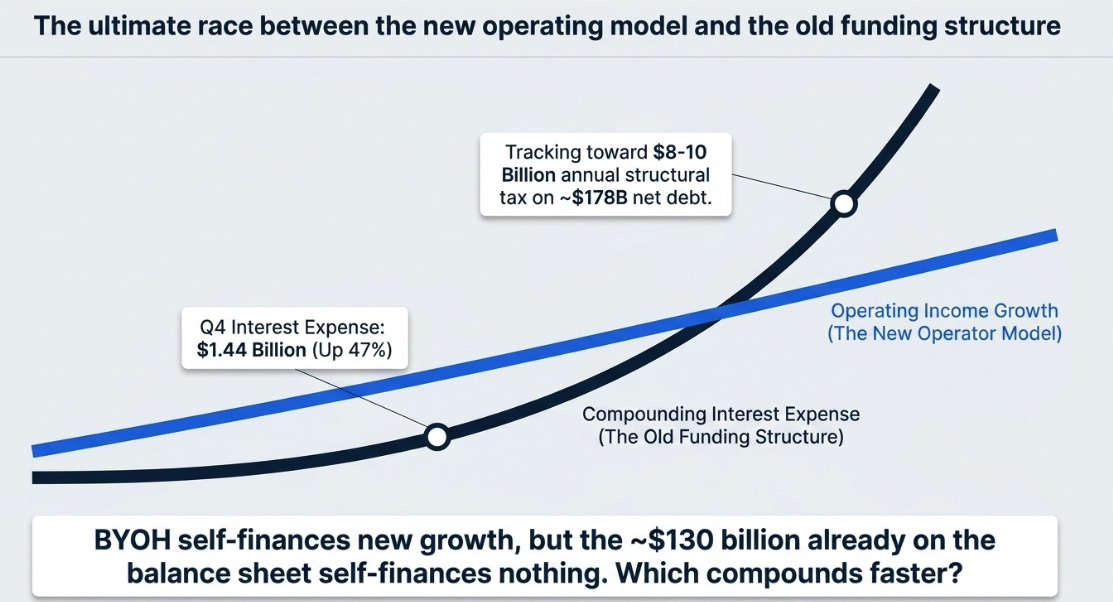

The bear has evolved and deserves its strongest form. It is no longer “BYOH may not scale”; Q4 showed it is scaling. The sharper risk: BYOH self-finances new growth, but the roughly $130 billion already on the balance sheet self-finances nothing. Interest expense was $1.44 billion this quarter, up 47%, and on the path toward ~$178 billion of net debt it climbs toward eight-to-ten billion a year, a structural tax that compounds whether the new model works. The real contest is between two identities: a new operator model getting lighter, and an old funding structure getting heavier. Which compounds faster is the whole question.

So, we’ll be opinionated about the parts and silent overall. We believe the bridge is real, the data-gravity flywheel is real, and the landlord fear partly inverts. We will not tell you which identity wins, not from cowardice, but because the one risk that could break this is the one we’re now least equipped to judge, having spent a year talking ourselves toward the other side.

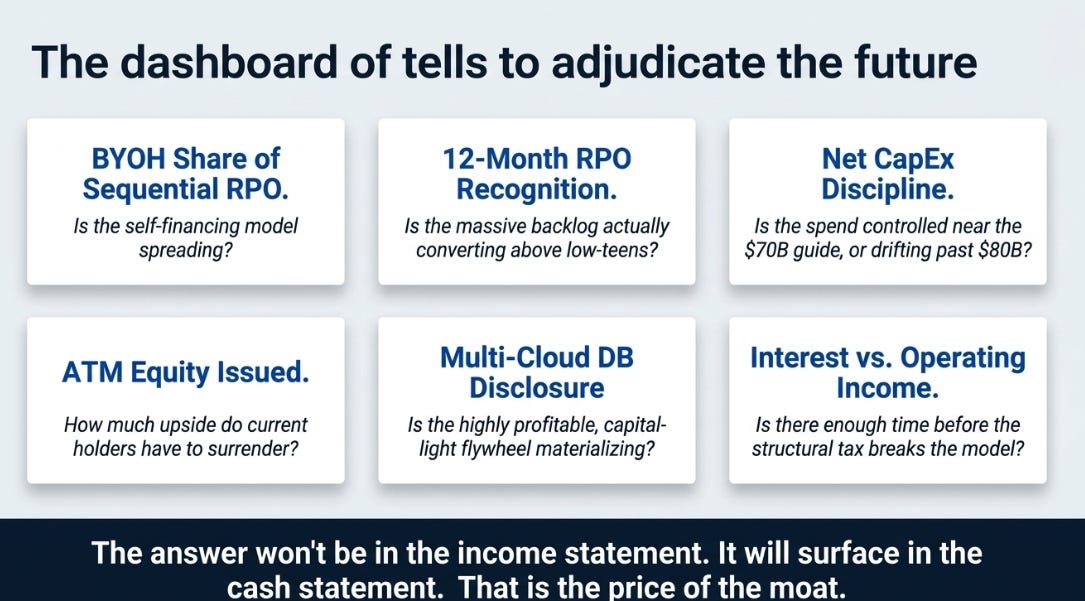

The metrics that adjudicate it aren’t generic beats: BYOH as a share of sequential RPO adds (is the model spreading?); twelve-month RPO recognition above the low-teens (is it converting?); net CapEx near the $70 billion guide, not drifting past $80 billion (is the spend controlled?); equity issued under the ATM (how much do holders surrender?); multi-cloud DB disclosure (is the light flywheel material?); interest expense against operating income (is there time?).

Oracle is no longer simply a software company, nor simply an AI infrastructure company. It is a premium enterprise-data business fused to a capital-intensive buildout designed to defend that data moat. If the fusion works, Q4 will read as the moment the market fixated on the price of admission and missed what the admission bought. If it fails, it will read as the moment Oracle handed investors the future and the bill on the same page. Either way, the answer won’t be in the income statement, where the beats live and everyone is looking. It will surface, quarter by quarter, in the cash statement, in whether the self-financing model spreads faster than the interest compounds.

That is the price of the moat.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.