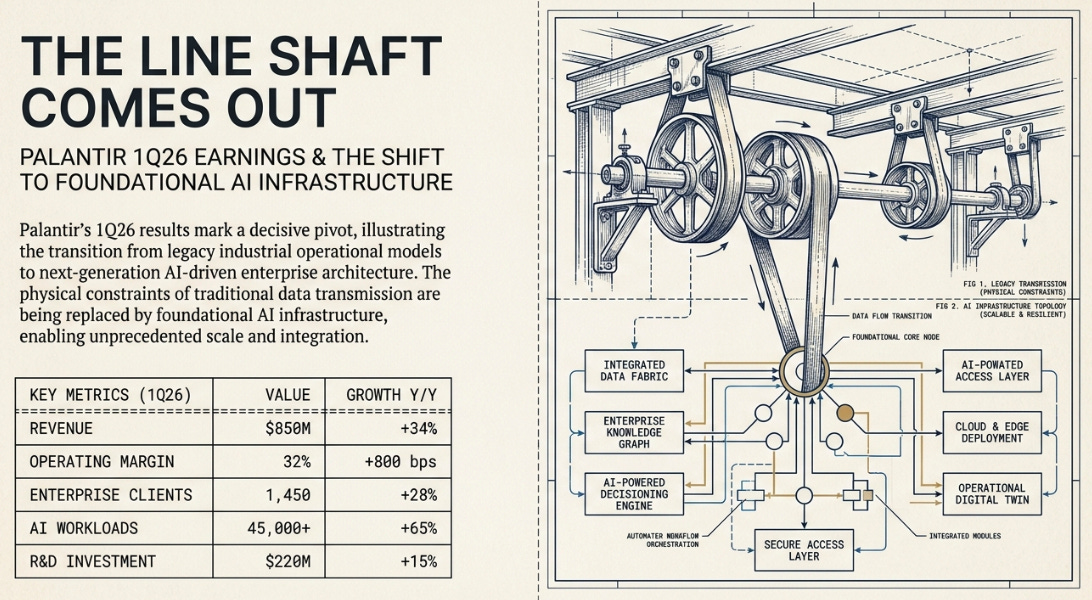

Palantir 1Q26 Earnings: The Line Shaft Comes Out

This was not just another AI beat. It was evidence that the Ontology is moving from a coordination layer between enterprise systems to the architecture around which enterprise work may be rebuilt.

TL;DR

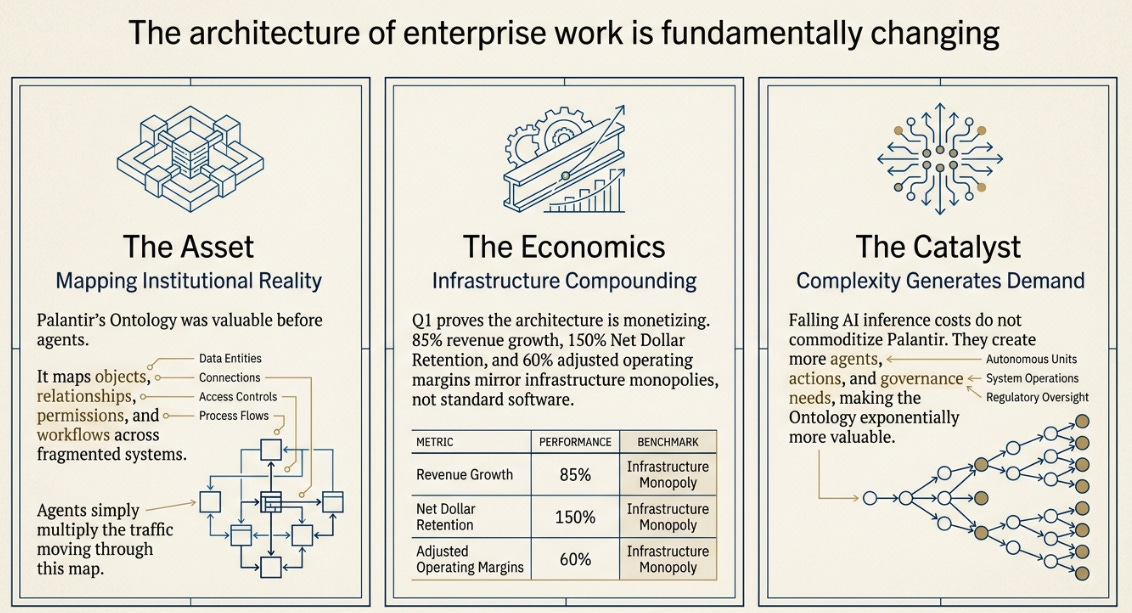

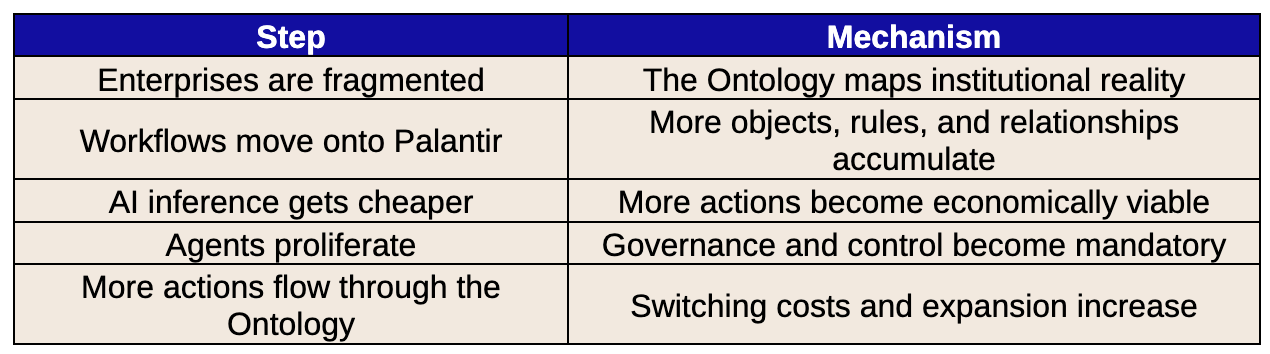

The Ontology was valuable before agents. Palantir’s core asset is its ability to map institutional reality: objects, relationships, permissions, workflows, and actions, across fragmented systems; agents simply multiply the traffic moving through that map.

Q1 showed the architecture monetizing. Revenue grew 85%, U.S. revenue grew 104%, adjusted operating margin hit 60%, net dollar retention reached 150%, and FY26 guidance moved to 71% growth, numbers that look less like normal software and more like infrastructure compounding.

The variant view is that complexity is Palantir’s demand generator. The market sees an expensive AI software winner; the more interesting possibility is that falling inference costs create more agents, more actions, and more governance needs, making the Ontology more valuable as AI spreads.

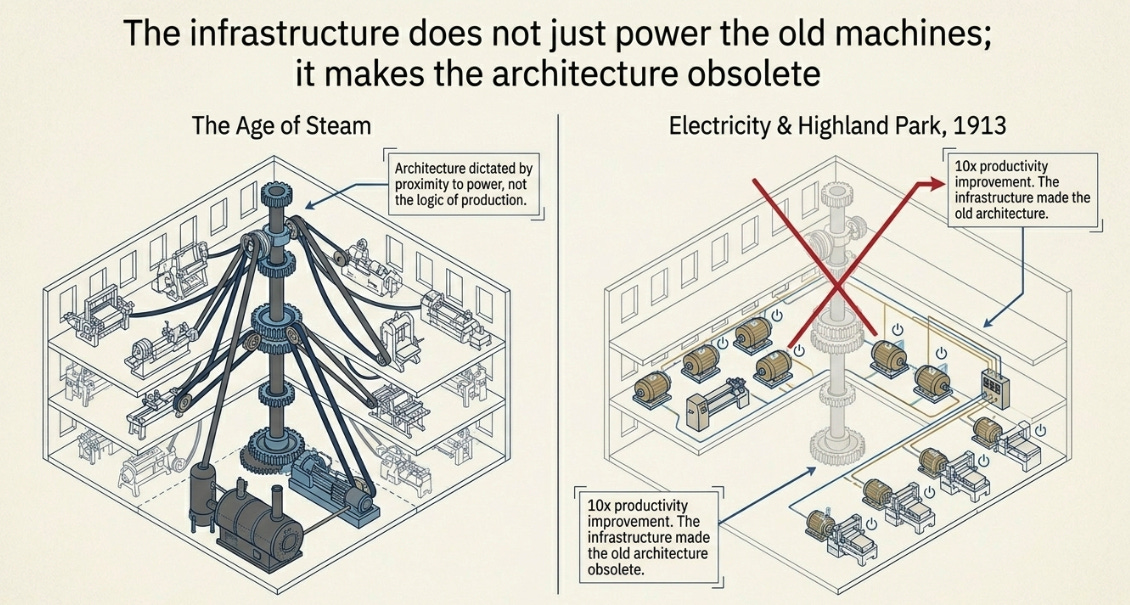

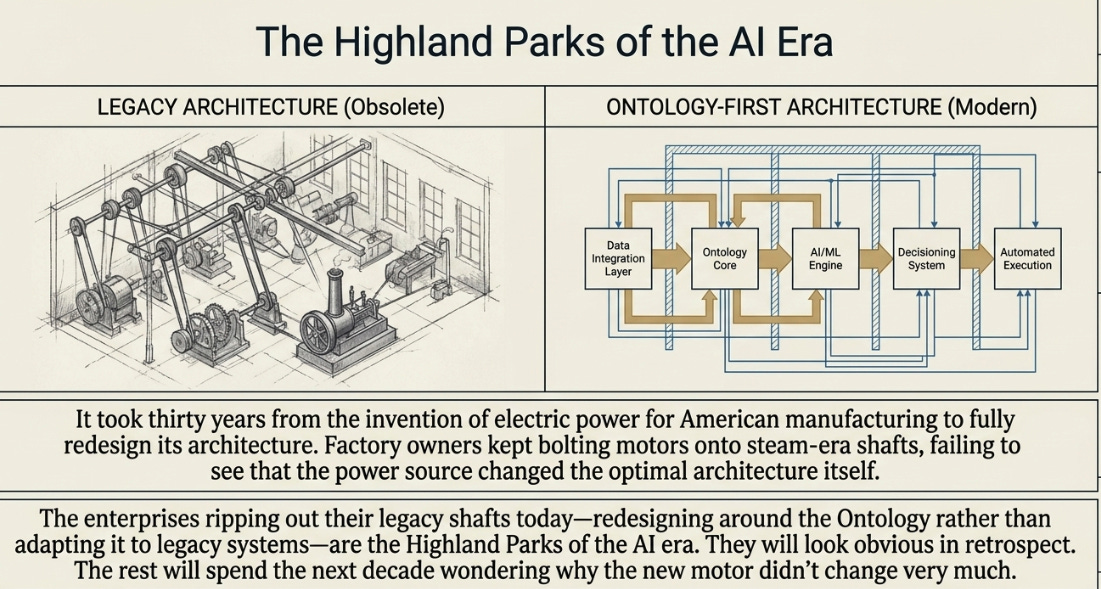

In the age of steam, factories were built around a central drive shaft. A single engine powered it, and belts and pulleys distributed force to every machine on every floor. The architecture of the building, where equipment sat, how work flowed, where bottlenecks formed, was dictated not by the logic of production but by proximity to the shaft.

When electricity arrived, factory owners did the obvious thing: they replaced the steam engine with an electric motor and kept the shaft. Productivity improved modestly. Then someone realized the real insight. If each machine has its own motor, the shaft is unnecessary. And without the shaft, the entire architectural logic of the factory dissolves. Machines can be arranged by workflow instead of proximity to power. Henry Ford’s Highland Park plant in 1913 was designed for electricity rather than adapted to it. Productivity didn’t improve five percent. It improved tenfold. The infrastructure didn’t just power the old machines. It made the architecture that housed them obsolete.

That is the right analogy for Palantir after Q1.

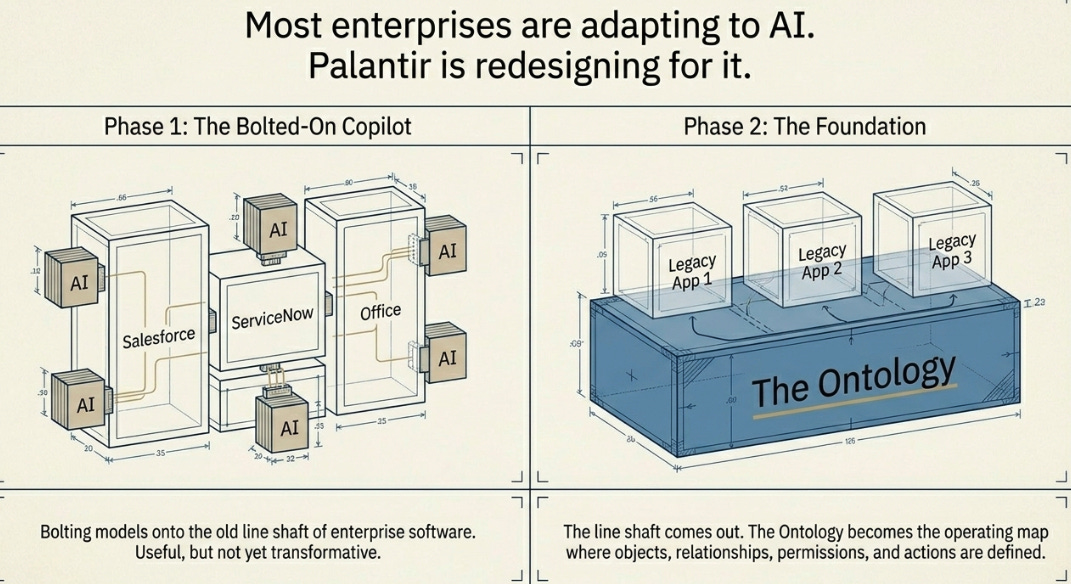

Most enterprises are in the first phase of AI adoption. They are bolting models onto the old line shaft of enterprise software, a copilot in Salesforce, an assistant in ServiceNow, a summarizer in Office. Useful, yes. Transformative, not yet. Palantir is arguing the shaft can come out. If the Ontology becomes the operating map of the enterprise, where objects, relationships, permissions, workflows, and actions are defined, then many applications stop being systems of truth and become interfaces. Some will remain important. Others will have to justify why they exist at all.

What We Said, What Happened

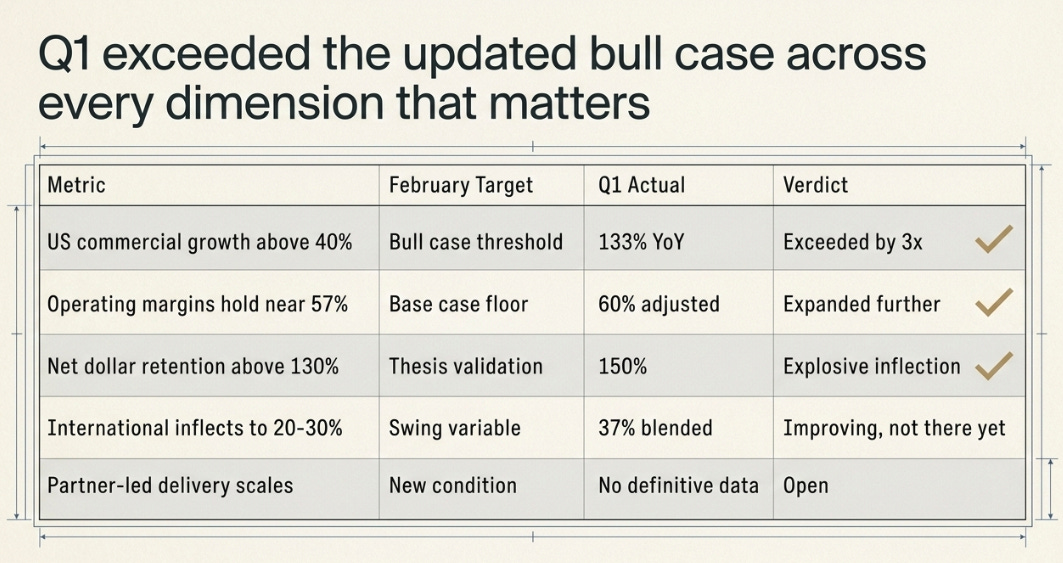

In October, I argued that Palantir had built the modern equivalent of MS-DOS, a coordination layer for incompatible enterprise systems, valuable not for any feature but for the coordination it enabled across an otherwise chaotic ecosystem. In February, after Q4 delivered 70% growth and 57% margins, I updated the thesis using the Toyota Production System: the value lived in the connections between machines, not the machines themselves. I set five conditions and scored four of five as met or exceeded. The old bull case became the new base case.

Then Q1 exceeded the updated bull case across every dimension that matters.

The mechanism we identified, coordination value appreciates with institutional complexity, now has a name from management. Shyam Sankar stood on the earnings call and articulated what is functionally the Jevons Paradox applied to enterprise AI: as inference costs collapse, token consumption explodes; as consumption explodes, the complexity of governing agent workflows grows exponentially; and as complexity grows, the Ontology becomes more essential, not less. We predicted the dynamic. The company’s CTO described it back to us using different words.

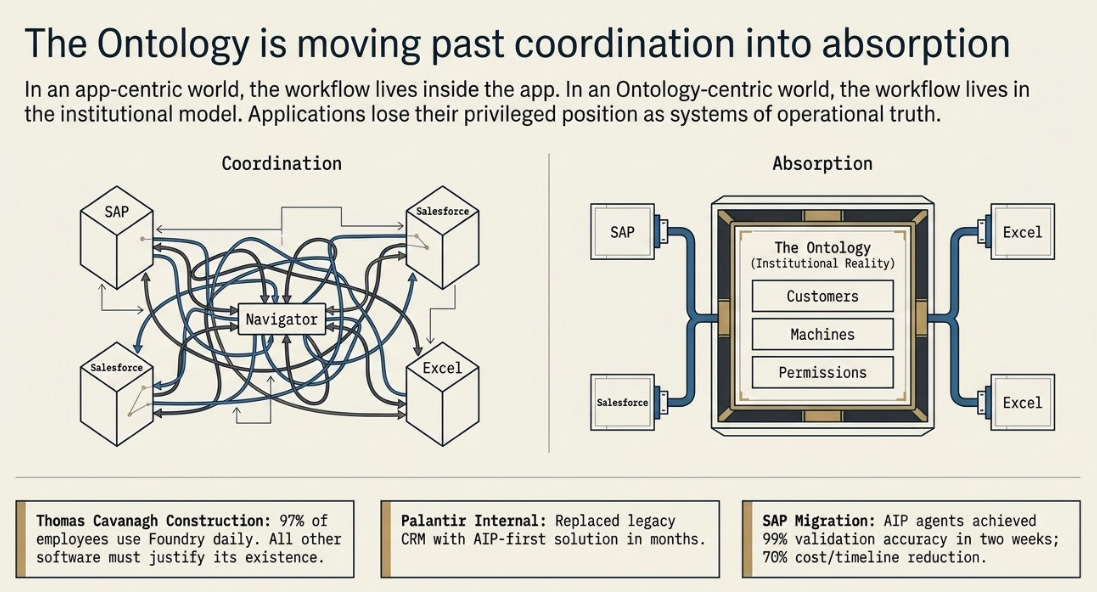

But Q1 also revealed something the framework didn’t fully anticipate. In February, I wrote that the Ontology coordinated between applications, the wiring between machines. What Q1 showed is that the Ontology has moved past coordination into absorption. That is the line shaft coming out. And it changes the thesis.

From Coordination to Absorption

The key sentence on the call was not Karp’s “N of 1” flourish. It was Sankar’s claim that AIP “replaces static workflows not by replicating the playbook, but by eliminating the need for one.” The examples that followed were specific. Thomas Cavanagh Construction, where 97% of employees use Foundry daily and every other piece of software must justify its existence. Palantir itself, which replaced its old CRM with an AI-first solution built on AIP in a few months. The SAP migration example, where AIP agents achieved 99% validation accuracy in two weeks with 70% timeline and cost reduction.

Palantir is not saying every application dies. It is saying many applications lose their privileged position as systems of operational truth. In a world organized around applications, the workflow lives inside the app. In a world organized around the Ontology, the workflow lives in the institutional model, and the app becomes replaceable. That is a subtle distinction, and it is everything.

The old view of Palantir was that it connected applications, SAP over here, Salesforce over there, manufacturing systems somewhere else, Excel everywhere, and Palantir as the integration layer that makes the mess navigable. That was already valuable. But once the Ontology encodes institutional reality, customers, claims, machines, contracts, permissions, policies, and actions, the application is no longer necessarily the owner of the process. It is one possible interface to the process. The coordination layer is becoming the operating layer. The wiring is becoming the building.

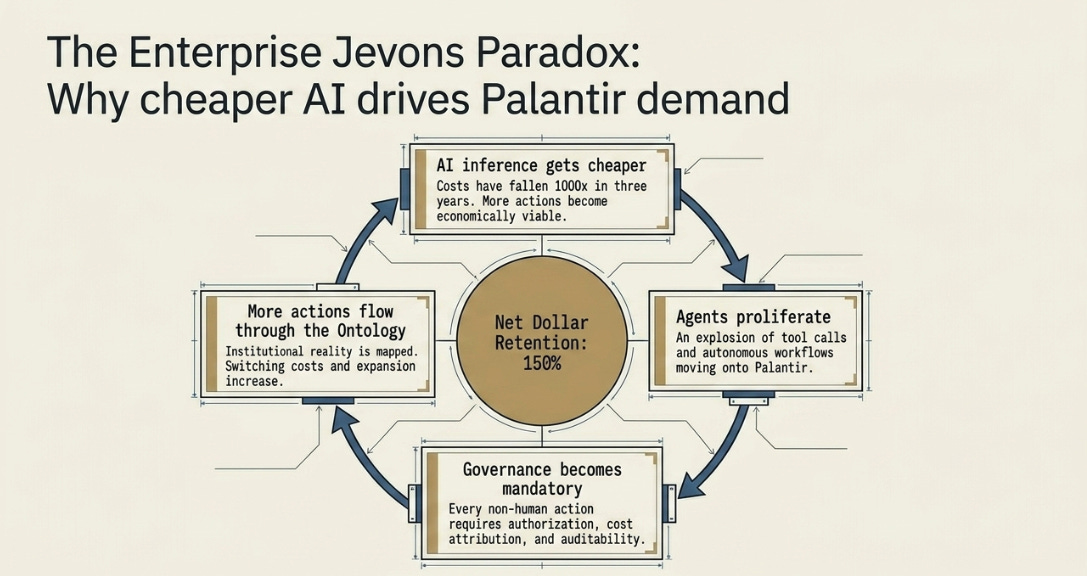

Agents Are the Accelerant

The temptation is to say agents make Palantir valuable. That is backwards. The Ontology was already valuable. Agents make it more valuable, and the mechanism explains why deceleration models keep breaking.

Sankar’s Jevons argument is the missing piece. AI inference costs have fallen roughly a thousand-fold in three years. The result is not less AI usage but an explosion of agent workflows, tool calls, and autonomous actions inside enterprises. Every one of those actions requires authorization, cost attribution, and auditability. The force that commoditizes models, falling token costs, is the same force that strengthens the governance layer. Cheap AI commoditizes intelligence but increases the value of governed action.

The flywheel is straightforward:

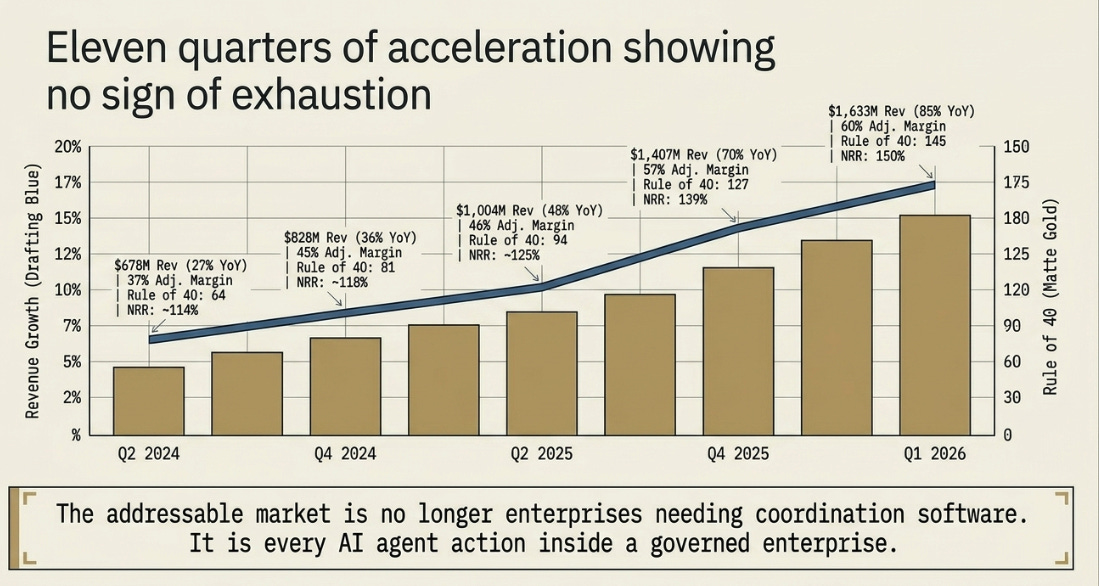

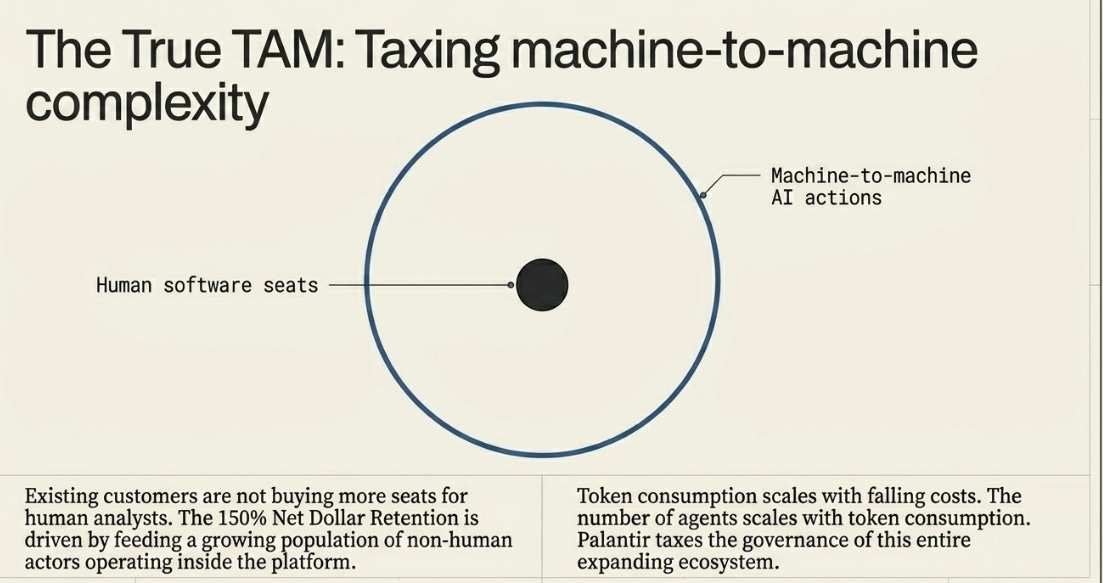

That is why net dollar retention exploded to 150%, up from roughly 118% twelve months ago. Existing customers are not buying more seats for analysts. They are feeding a growing population of non-human actors operating inside the platform. The number of agents scales with token consumption. Token consumption scales with falling costs. The addressable market is no longer “enterprises that need coordination software.” It is every AI agent action inside a governed enterprise. That is a categorically different number.

The acceleration is now eleven quarters deep and showing no sign of exhaustion:

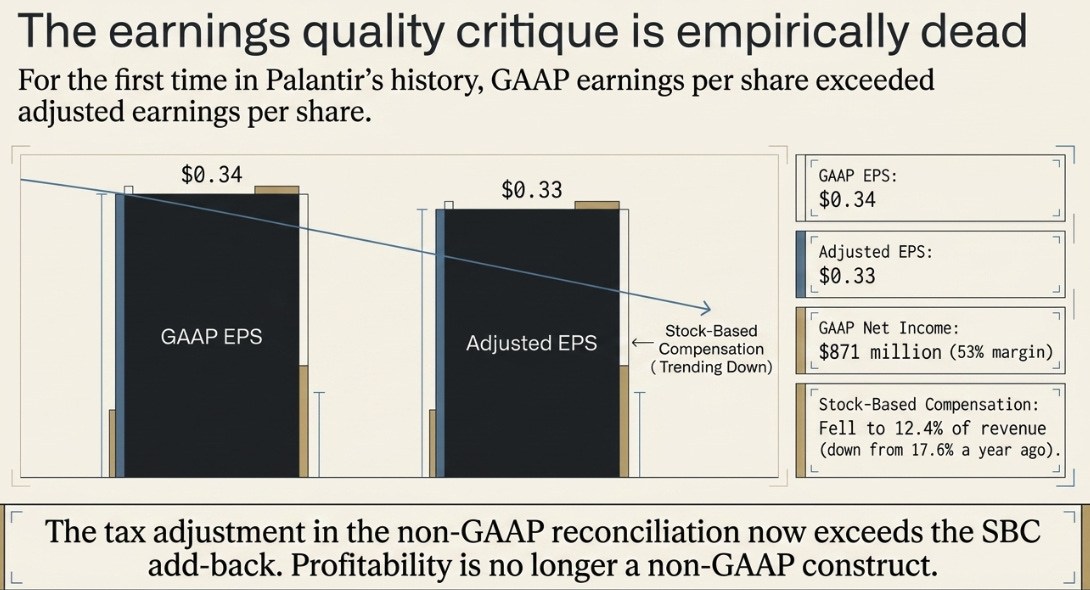

One quality signal the market has not absorbed. For the first time in Palantir’s history, GAAP earnings per share ($0.34) exceeded adjusted earnings per share ($0.33). Stock-based compensation fell to 12.4% of revenue from 17.6% a year ago, and the tax adjustment in the non-GAAP reconciliation now exceeds the SBC add-back. The profitability story is no longer a non-GAAP construct. GAAP net income was $871 million at a 53% margin. The earnings quality critique, the last structural bear argument standing, is empirically dead.

What the Market Is Getting Wrong

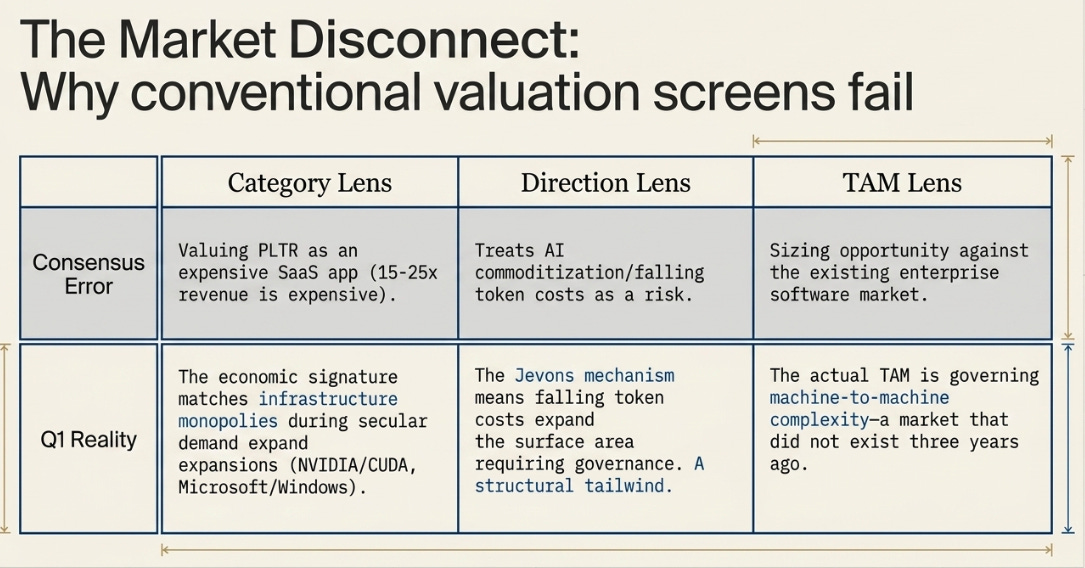

The consensus view treats Palantir as an expensive AI software stock that will eventually decelerate. I think the consensus is making three errors that compound.

The first is a category error. Palantir is being valued against SaaS companies where 15-25x revenue is expensive. But the economic signature of Q1, 85% growth, 60% margins, 150% NRR, $1.5 million revenue per employee, 70 salespeople, does not match application software. It matches infrastructure monopolies during secular demand expansions. The correct comp set is not Salesforce. It is NVIDIA during the CUDA lock-in, or Microsoft during Windows standardization.

The second error is directional. The market treats AI commoditization as a risk to Palantir. Q1 says the opposite. Growth accelerated because models commoditized, not despite it. The Jevons mechanism means every decline in token cost expands the frontier of automation, which expands the surface area requiring governance. The market is modeling a headwind that is structurally a tailwind.

The third error is about TAM. Analysts size Palantir’s opportunity against the enterprise software market. The actual opportunity is governing machine-to-machine complexity inside every institution that uses AI, a market that did not exist three years ago and grows at the rate of inference cost decline. Wrong category, wrong direction of impact, wrong TAM. Through those three lenses simultaneously, the stock looks very different than it does on a conventional screen.

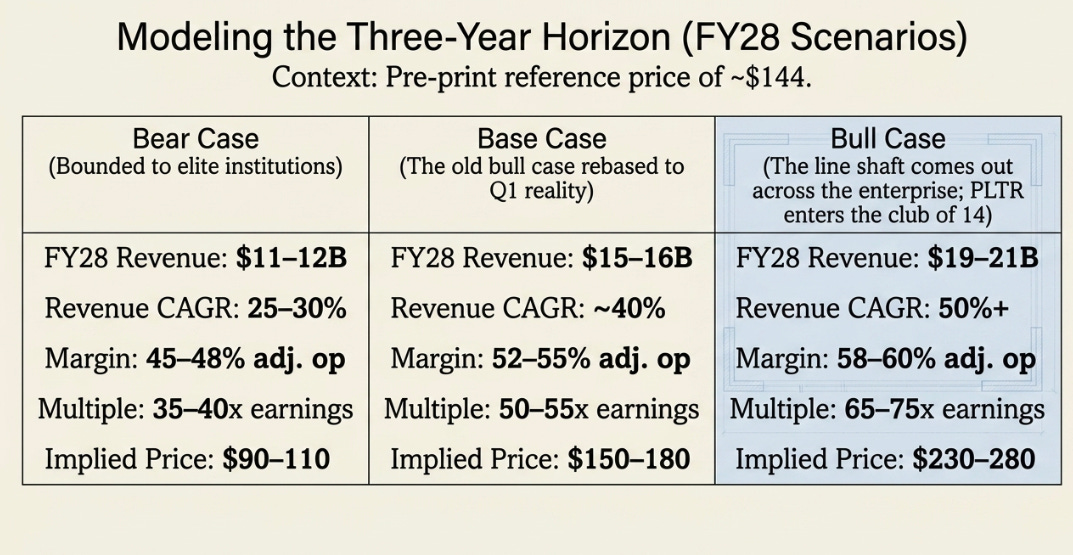

Three Years From Now

Only fourteen public companies have ever sustained 40%+ revenue CAGR for three years after crossing $10 billion in annual revenue. The list includes PDD, Meta, Alibaba, Tencent, Tesla, NVIDIA, Amazon, and Alphabet. Every one is a consumer platform or semiconductor company. Zero enterprise software companies have done it. Palantir will cross $10 billion around mid-2027. If the structural thesis holds, it becomes the first.

Here is how I would frame the next three years, using the pre-print price of approximately $144 as the reference point rather than pretending precision where none exists:

The bear case is not that Palantir is fake. That debate is settled. The bear case is that Palantir is excellent but bounded, indispensable for elite, complex institutions, but not the default architecture for enterprise AI. Growth decelerates, margins stay strong but not extraordinary, and the multiple compresses. At $144, you lose modestly.

The base case is the old bull case rebased to demonstrated reality. Palantir compounds through U.S. commercial and government, NRR stays elevated, and the company crosses $15 billion by 2028 with elite profitability. The stock works, but not spectacularly, because the quality is largely recognized.

The bull case requires the line shaft to actually come out across the enterprise. Applications become interfaces, agents multiply governed actions, and Palantir becomes the operating layer for institutional AI. That is the case where Palantir enters the club of fourteen and the current price looks cheap in retrospect.

What Would Prove Us Wrong

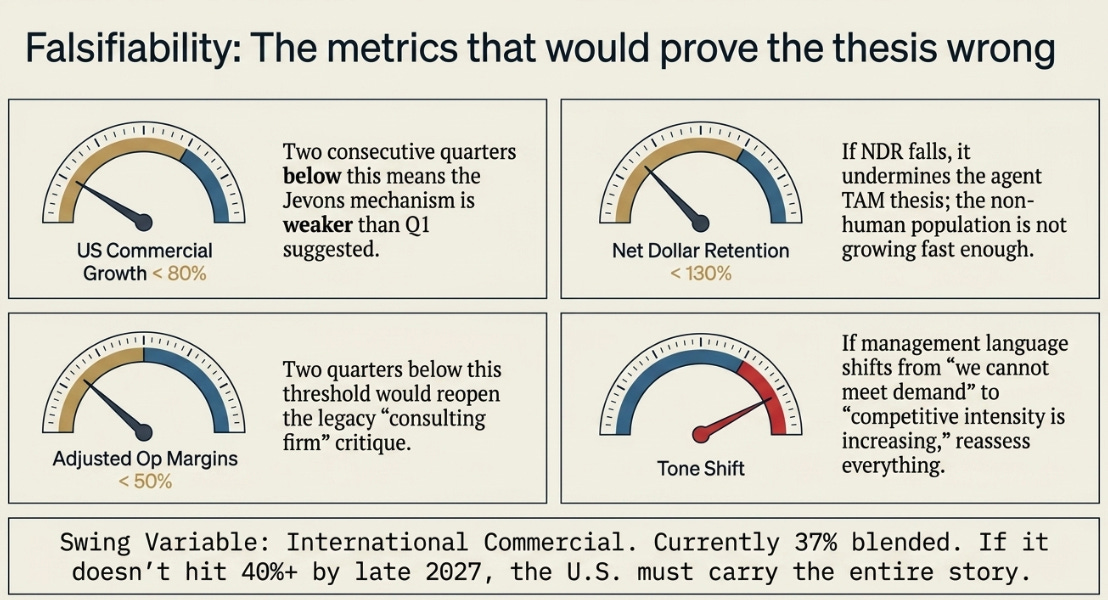

The framework requires specific things to remain true. U.S. commercial growth below 80% for two consecutive quarters without a program-transition explanation would mean the Jevons mechanism is weaker than Q1 suggested. Net dollar retention below 130% would undermine the agent TAM thesis, if existing customers are not expanding at that rate, the non-human population is not growing fast enough. Adjusted operating margins below 50% for two quarters would reopen the consulting critique. And if management language shifts from “we cannot meet demand” to “competitive intensity is increasing,” reassess everything. Tone is the leading indicator.

International remains the open condition. It grew 37% blended in Q1, up from near-zero, but it is not yet compounding at a rate that changes the three-year math. The NVIDIA Sovereign AI OS partnership is aimed at this gap. If international commercial reaches 40%+ growth by late 2027, the runway extends materially. If it does not, the U.S. has to carry the entire story.

Economic historians estimate it took roughly thirty years from the availability of electric power to the full redesign of American manufacturing. Factory owners kept bolting motors onto steam-era shafts because they could not see that the power source had changed the optimal architecture, not just the energy bill. The enterprises ripping out their shafts today, redesigning around the Ontology rather than adapting it to legacy systems, are the Highland Parks of the AI era. They will look obvious in retrospect. The rest will spend the next decade wondering why the new motor did not change very much.

Palantir is betting the world needs far more rewiring than it currently imagines. Q1 is the strongest evidence yet that the bet is right. Whether that justifies today’s price depends less on the quality of what is being built and more on how quickly the rest of the world figures out that the shaft is already obsolete.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.