Palo Alto 3QFY26 Earnings: The Firewall Comes Back as a Sensor

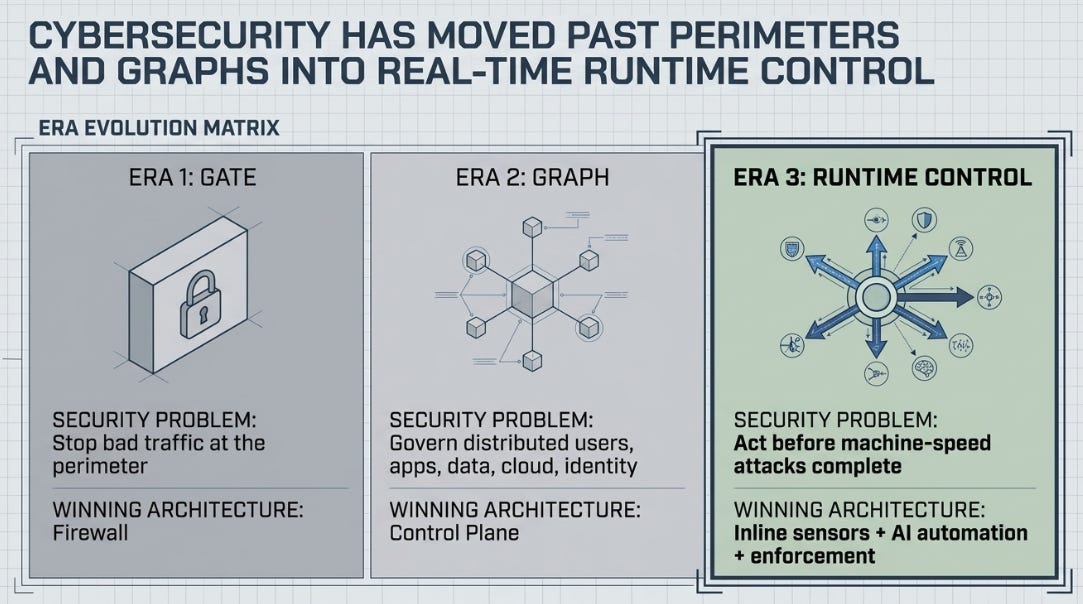

The world moved from gate to graph. AI is now forcing the graph to operate at runtime.

TL;DR

AI is turning cybersecurity into a runtime-control problem, not just a perimeter problem.

Palo Alto’s quarter strengthened the control-plane thesis, especially across XSIAM, AIRS, identity, observability and firewalls.

The stock is strategically more interesting, but not obviously cheap until FY27 proves organic acceleration and cleaner cash-flow delivery.

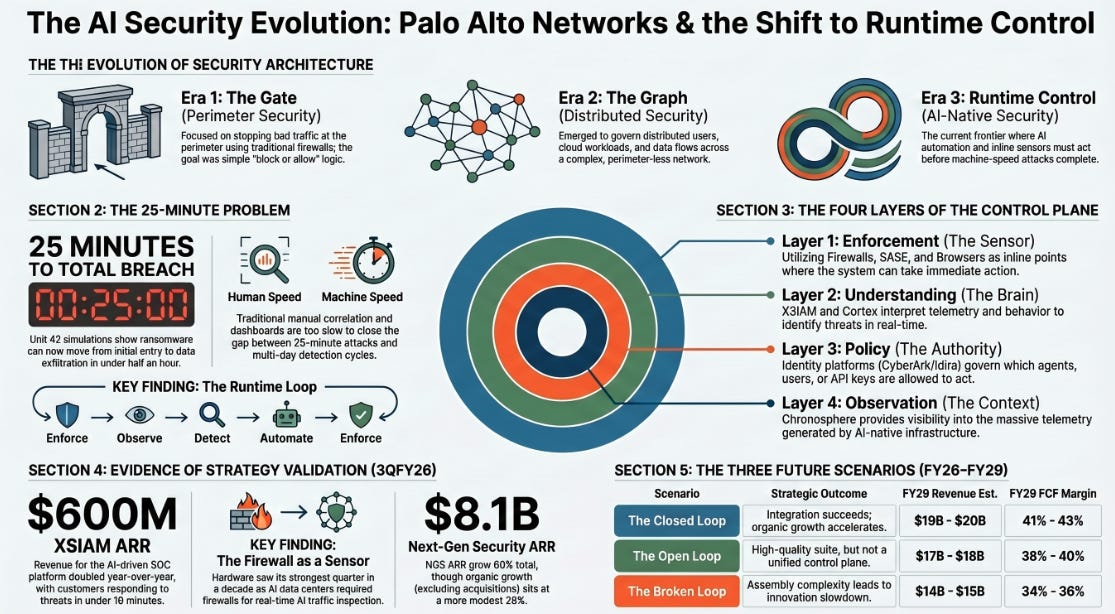

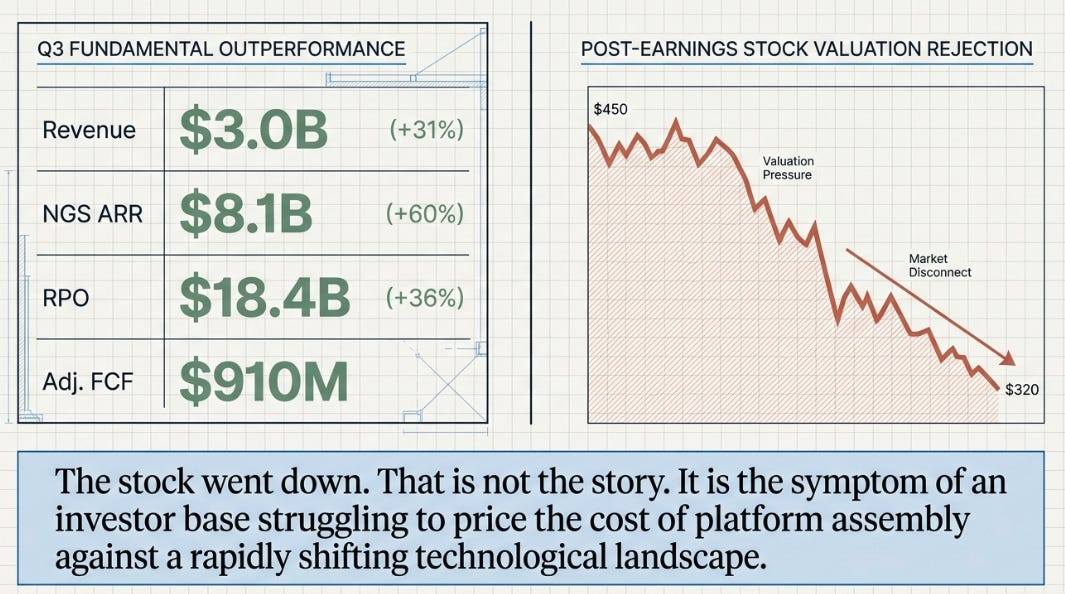

Palo Alto Networks had a strong quarter. Revenue grew 31% to $3.0 billion. Next-generation security ARR grew 60% to $8.1 billion. Remaining performance obligations grew 36% to $18.4 billion. Adjusted free cash flow was $910 million. Guidance went up.

The stock went down.

That is not the story. It is the symptom.

This is our third article on Palo Alto. The first argued that cybersecurity had moved from gate to graph. The enterprise no longer had one perimeter to defend. It had a distributed graph of users, applications, cloud workloads, identities, data flows, and AI agents. Palo Alto’s answer was to assemble enforcement authority across that graph: firewalls, SASE, browser, XSIAM, cloud, identity, and now observability.

The ambition was right. The concern was execution.

CrowdStrike’s architecture was cleaner: one agent, one data lake, rapid module expansion. Palo Alto’s architecture was broader but messier. It was trying to coordinate many enforcement surfaces into one operating system for security. Our concern was not that Palo Alto had the wrong vision. It was that assembly is harder than architecture.

After Q2, we said Palo Alto had won the operational argument but lost the financial one. The stock fell despite strong results because investors saw the cost of assembly: dilution, margin pressure, integration risk, and organic growth that was good but not decisive.

Q3 changes the discussion.

It does not eliminate the assembly risk. In some ways, it makes the risk harder to measure. But it gives the strategic thesis its strongest validation yet. The reason is simple: the world moved faster.

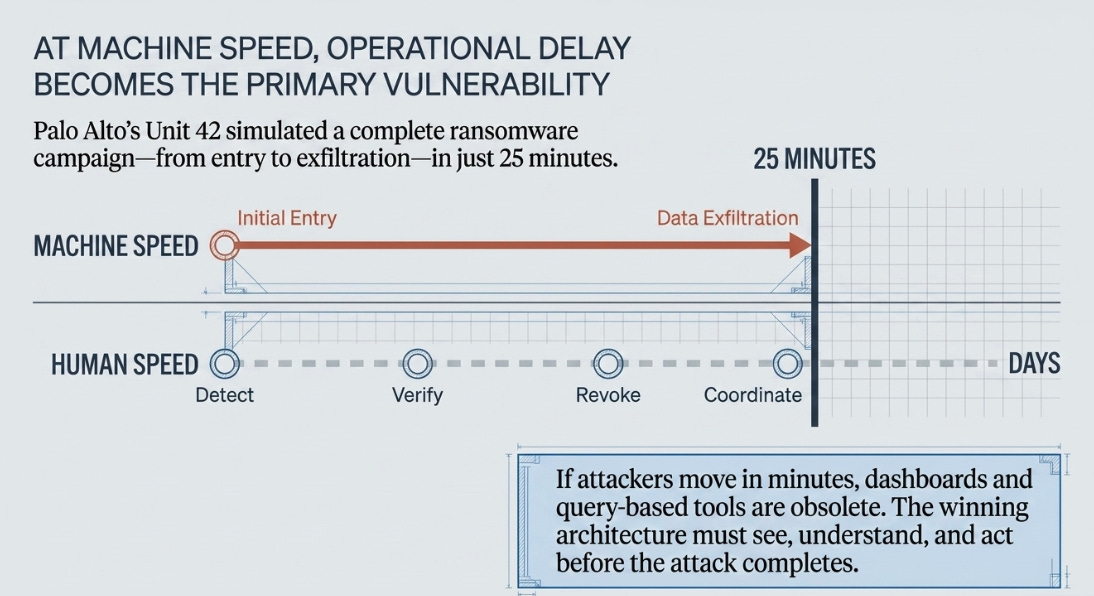

The Twenty-Five Minute Problem

Our prior argument was that fragmentation becomes dangerous when attacks move faster than humans can investigate. At human speed, the latency between best-of-breed tools is manageable. One tool detects, another verifies, a third revokes access, and a human analyst coordinates the response. It is inefficient, but it can work.

At machine speed, the delay becomes the vulnerability.

That is why the Mythos discussion matters. Palo Alto’s Unit 42 simulated a ransomware campaign from initial entry to data exfiltration in twenty-five minutes. The typical enterprise still needs days to identify a breach. That gap is not a workflow problem. It is an architecture problem.

If attackers move in minutes, dashboards are too slow. Query-based tools are too slow. Manual correlation is too slow. The winning architecture must see what is happening in real time, understand it in context, and act before the attack completes.

That is Palo Alto’s strongest claim: not that it sells more security products, but that it sits close enough to enterprise activity to become the runtime enforcement layer.

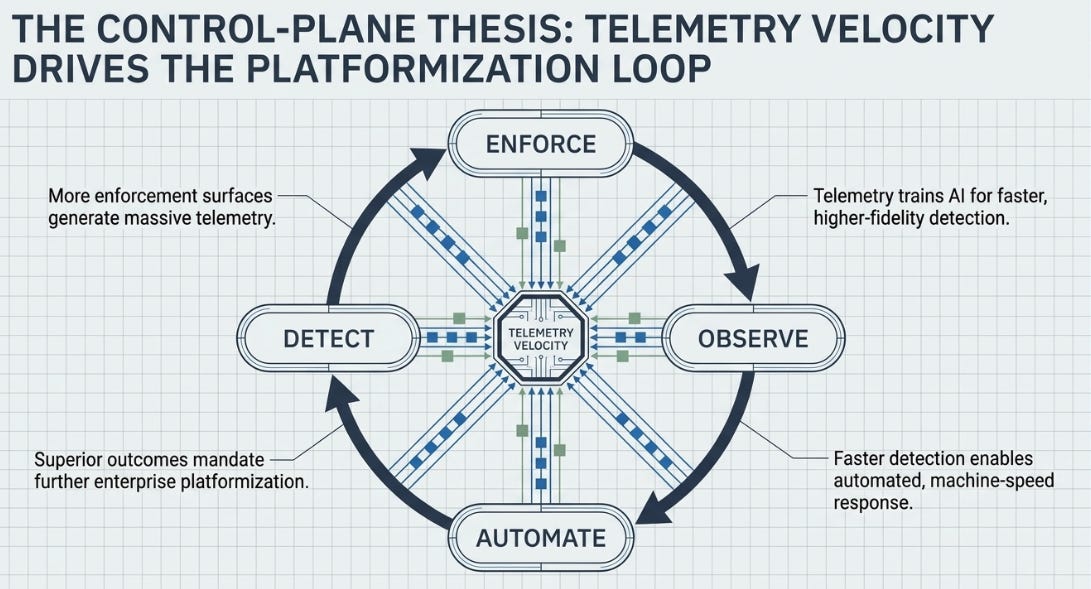

The loop is straightforward: Enforce → observe → detect → automate → enforce.

More enforcement surfaces generate more telemetry. More telemetry improves detection. Better detection enables faster automated response. Faster response improves outcomes. Better outcomes drive more platformization. More platformization creates more enforcement surfaces.

That is the control-plane thesis. This quarter moved that thesis from interesting to urgent.

From Gate to Graph to Runtime Control

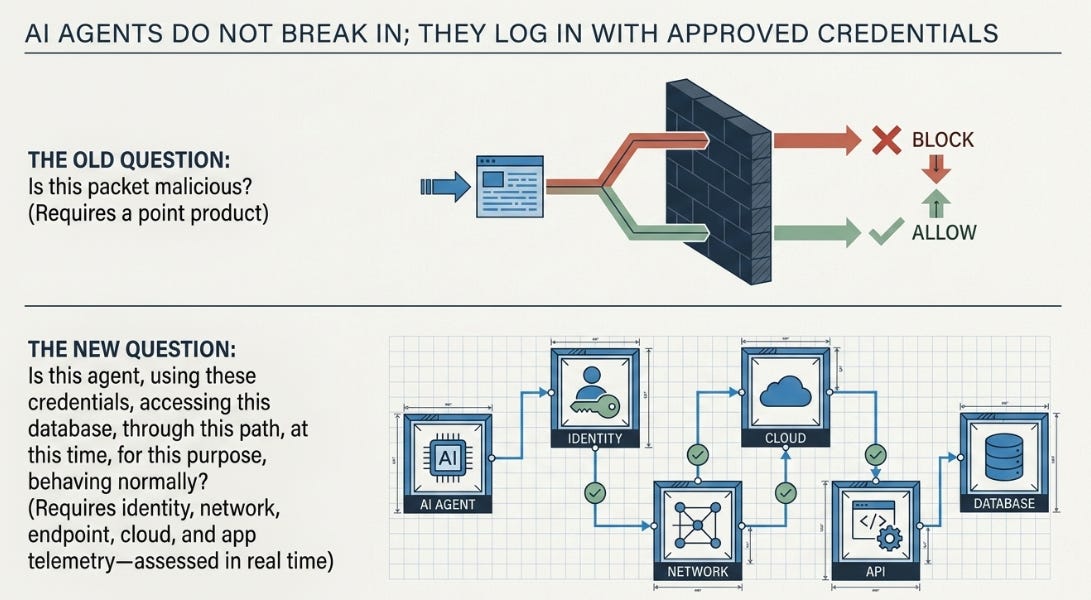

The graph still matters. AI agents move across identity, cloud, network, browser, apps and data. They do not respect product boundaries. They do not look like traditional malware. Often, they do not “break in” at all. They log in, with credentials, permissions, API keys and approved access.

That changes the security question. The old question was: Is this packet malicious? The new question is: Is this agent, using these credentials, accessing this database, through this path, currently, for this purpose, behaving normally?

That question cannot be answered by a single point product. It requires identity context, network context, endpoint behavior, cloud workload visibility, application telemetry and policy enforcement. More importantly, it must be answered while the action is happening.

That is runtime control.

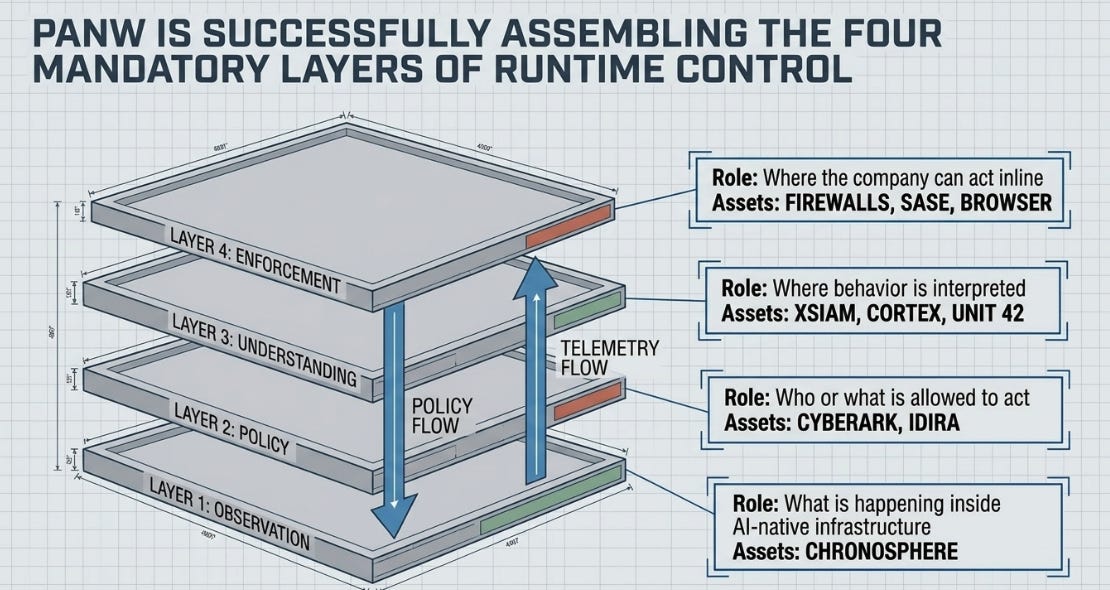

This is the framework for understanding Palo Alto now. The company is trying to build four layers of runtime control:

This is a more helpful way to read the quarter than the income statement.

The key question is not whether each product grew. The key question is whether the layers are beginning to reinforce each other. If they are, Palo Alto is becoming a control plane. If they are not, it is becoming a very large security suite.

That distinction matters enormously.

Evidence That Runtime Control Is Becoming Real

Q3 gave real evidence that the runtime-control thesis is working.

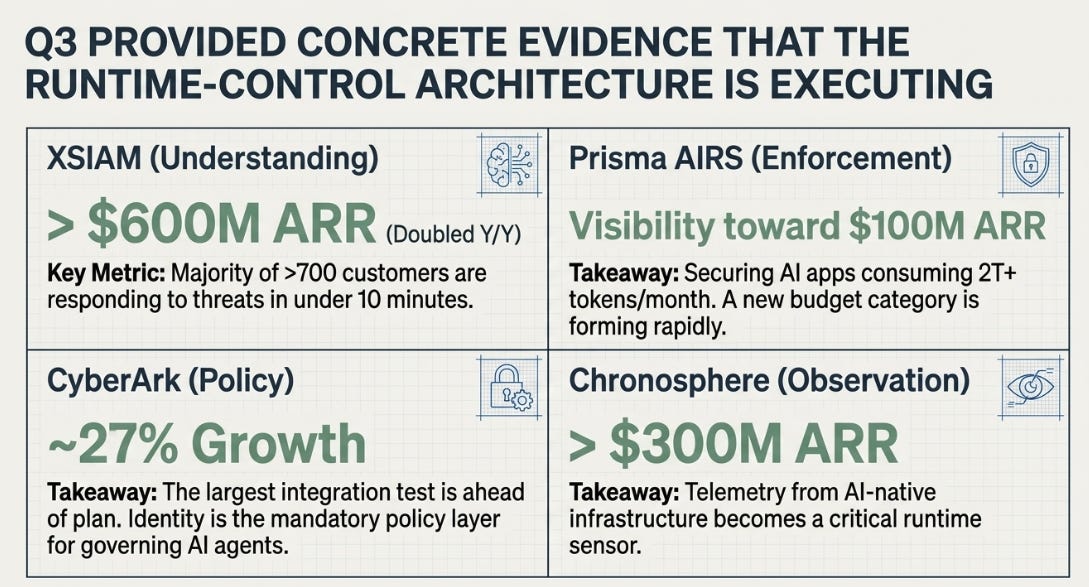

XSIAM crossed $600 million of ARR, doubled year over year, and now has more than 700 customers. More importantly, management says the majority of deployed customers are responding to threats in under ten minutes. That is the metric that matters. If attacks can complete in twenty-five minutes, response time is not a product statistic. It is the product.

Prisma AIRS reached more than 300 customers. This was not supposed to happen this fast. Two quarters ago, it was a small emerging product. Now management says it has visibility toward $100 million of ARR. A global consulting firm signed a record Prisma AIRS deal to secure AI applications and agents consuming more than two trillion tokens per month. That is not a feature. That is a budget category forming.

CyberArk, the largest integration test, grew around 27% and appears to be ahead of plan on profitability convergence. That matters because identity is the policy layer for the AI enterprise. AI agents do not only attack systems. They log in. Governing agents requires identity to become part of the security control plane.

SASE reached $1.6 billion of ARR, growing 40%. Browser security scaled. Software firewalls kept growing. The distributed enterprise still needs access control, and AI makes the access problem more complicated, not less.

Chronosphere surpassed $300 million of ARR. That matters because AI infrastructure produces massive telemetry. Observability is not traditional cybersecurity, but in an AI-native world it becomes another sensor for understanding system behavior.

These are not isolated product wins. They map onto the same architecture: enforcement, understanding, policy and observation.

But the most interesting evidence came from the oldest part of the company.

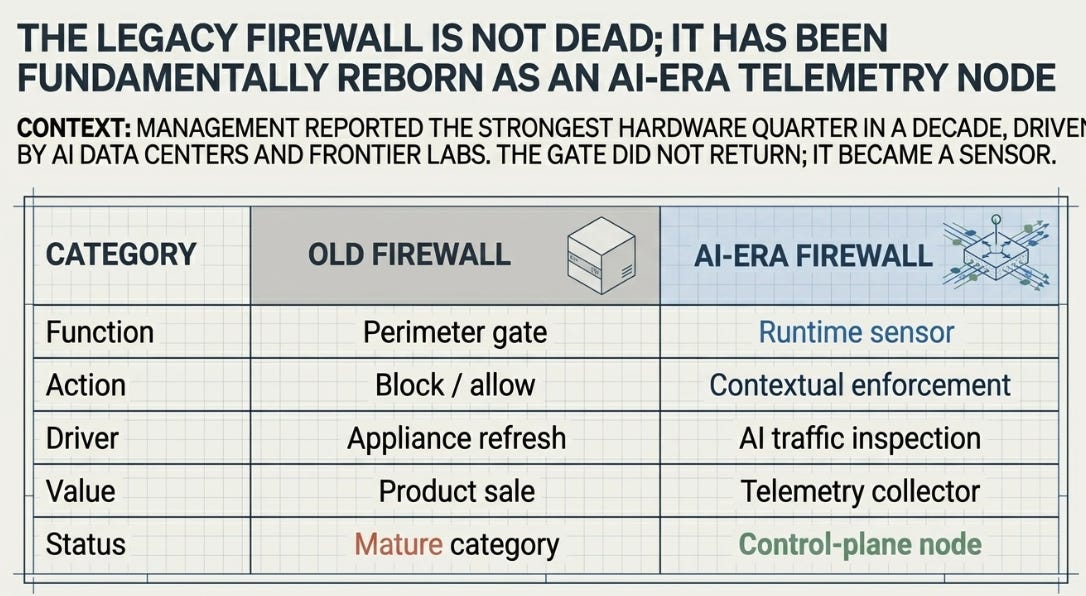

The Firewall Comes Back as a Sensor

The old article was about the gate dissolving. Q3 showed something more subtle.

The gate did not return. The gate became a sensor.

For years, Palo Alto’s firewall business was treated as the mature part of the company: profitable, sticky, important, but no longer the strategic growth engine. The multiple came from SASE, cloud, XSIAM and AI security. Hardware was the past.

Q3 complicates that view.

Product revenue grew sharply. Management called it the strongest hardware quarter in a decade. Next-generation firewall bookings grew nearly 40%. The demand was not explained as a normal refresh cycle. Palo Alto pointed to AI data centers, frontier labs, sovereign infrastructure providers and enterprise AI networking.

That is a strategic reclassification.

AI agents create traffic. They call APIs, access tools, authenticate into systems, interact with databases, and communicate with other agents. The more agentic the workflow, the more machine-to-machine traffic it creates.

That traffic has to be inspected somewhere. The closer the inspection point sits to the live flow, the more valuable it becomes. In that world, the firewall is not exciting because it is a box. It is valuable because it is inline.

The firewall comes back as a sensor.

This is the underappreciated positive from the quarter. AI does not only create a new product category like Prisma AIRS. It may also make Palo Alto’s existing enforcement footprint more valuable.

That is the strongest argument for becoming more constructive on the company.

The View Through Fog

Then comes the complication.

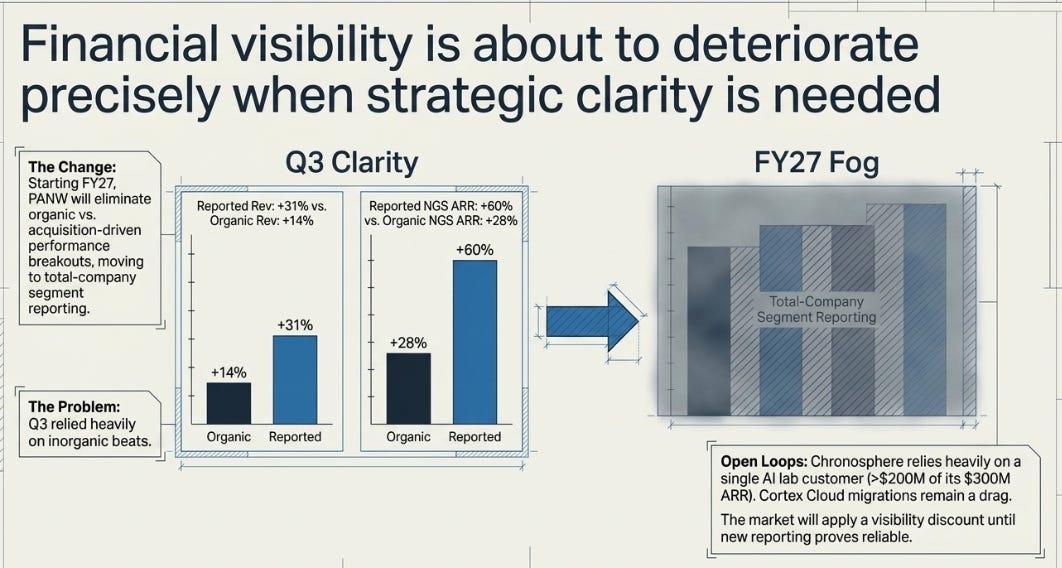

Starting FY2027, Palo Alto will no longer break out organic versus acquisition-driven performance. It will move toward total-company guidance and segment reporting across Network Security, Cortex and Identity.

Management has a fair argument. Once CyberArk and Chronosphere are integrated into Palo Alto’s go-to-market, the organic/inorganic distinction gets blurry. If a CyberArk relationship leads to a Palo Alto firewall deal, what is that? If Chronosphere telemetry improves XSIAM detection, is that acquired or organic? Operationally, management wants investors to see one company.

The problem is timing.

This was the first quarter where investors could clearly see the split. Reported revenue grew 31%; organic revenue grew 14%. Reported NGS ARR grew 60%; organic NGS ARR grew 28%. Reported RPO grew 36%; organic RPO grew 22%. The headline beat was strong, but much of the upside came from CyberArk and Chronosphere exceeding expectations.

Those are all good numbers. They are not the same story.

The company is asking investors to believe that assembly is becoming architecture just as it removes one of the cleanest ways to measure whether the core is accelerating. That does not mean management is hiding weakness. But it does mean investors should apply a visibility discount until the new segment disclosures prove they are useful.

Chronosphere has a similar duality. A leading AI lab contributing more than $200 million of ARR is powerful validation. It also means concentration. If observability ARR is a little over $300 million, one customer represents a very large portion of the business. That is AI-native proof, but not yet diversified platform proof.

Cortex Cloud is another open loop. Management acknowledged that the Prisma Cloud to Cortex Cloud migration is still a drag. That matters because cloud security is where the platform data flywheel should be proving itself, and where competition from Wiz and CrowdStrike is most relevant.

This is why the quarter is so interesting.

The thesis is stronger. The evidence is better. The visibility is about to get worse.

The EPS Problem

There is also a simple valuation reason the stock struggled.

CyberArk adds revenue, identity capability and strategic breadth. It also adds dilution. Bloomberg consensus shows FY27 revenue growing around 21%, but adjusted EPS growing only around 9%. That is not the profile investors expect when paying a premium P/E multiple.

The reason is denominator math. The acquisition increases the share count. Revenue gets the benefit immediately; per-share earnings take longer to catch up. Synergies help, but they flow through over time.

This is why free cash flow is the better valuation anchor. Palo Alto’s adjusted free cash flow remains strong, and the path to roughly 40% adjusted FCF margins by FY2028 remains credible if integration synergies materialize.

EPS explains the selloff. Free cash flow explains why the stock still has a floor.

How Our View Changes

Our prior view was that Palo Alto had the right ambition but a difficult architecture problem. It was trying to assemble a control plane across multiple security surfaces while competitors like CrowdStrike had cleaner native architectures.

Q3 makes us more sympathetic to Palo Alto’s approach.

AI changes the security problem. It is not enough to have a beautiful endpoint architecture if the risk moves across identity, network, cloud, browser, AI applications and infrastructure telemetry at machine speed. Breadth may matter more than we previously appreciated because the security question itself is becoming more contextual.

The question is no longer simply: can assembly compete with architecture?

It is now: can assembly become architecture before AI makes real-time control mandatory?

That is a better question for Palo Alto. It does not eliminate the risk. It raises the potential reward.

Our updated view is therefore more constructive strategically, but still disciplined financially. Palo Alto has moved closer to proving that enforcement plus understanding can beat fragmentation. It has not yet proven that assembly can compound like architecture.

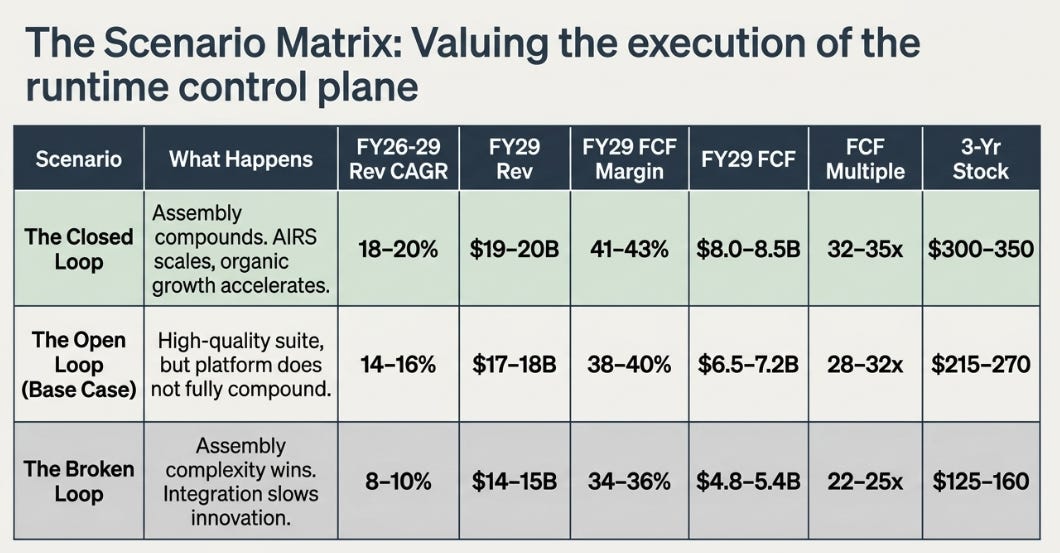

Three Loops

The stock is around $260. That already assumes more than “good cybersecurity company.” It assumes Palo Alto becomes something closer to the control plane for AI-era security.

The next three years depend on which loop investors get.

We think the Open Loop is still the most likely outcome. That means the stock is not obviously cheap at $260. It is fairly valued for existing holders who believe the architecture is moving in the right direction, but not yet compelling for new capital without a better entry or clearer FY27 proof.

The Closed Loop requires real platform evidence: AIRS following the XSIAM curve, CyberArk sustaining growth while margins converge, Chronosphere diversifying, cloud migration resolving, organic revenue moving toward the high teens, and free cash flow margins pushing above 40%.

The Broken Loop does not require Palo Alto to become a bad company. It only requires the company to look like a complex security suite growing low-to-mid teens organically while trading at a control-plane multiple.

What Determines the Loop

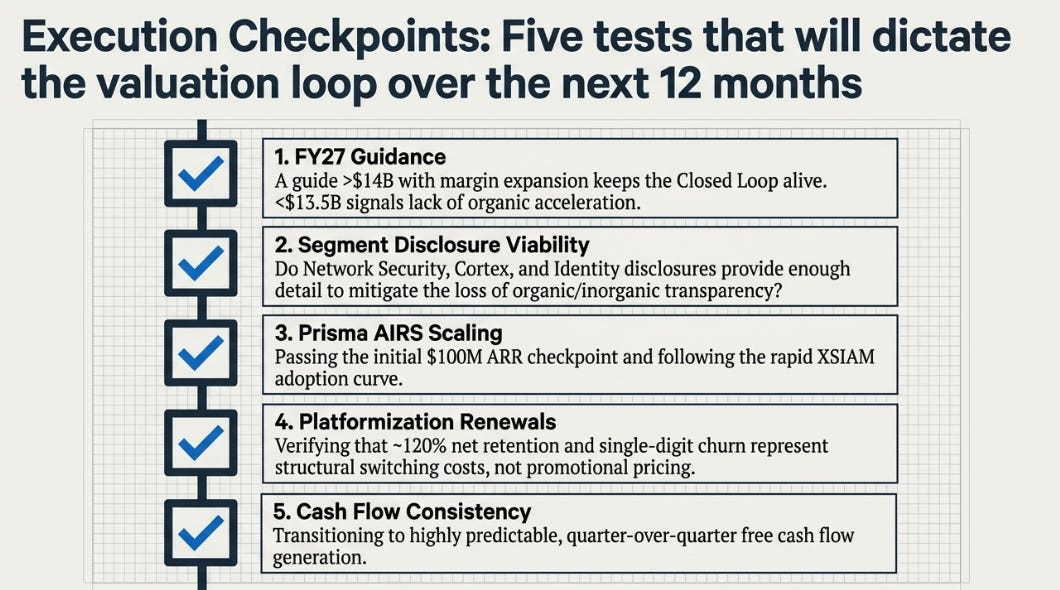

The next twelve months matter more than the quarter just reported.

The first test is FY27 guidance. A guide that implies revenue above $14 billion with margin expansion would keep the Closed Loop possible. A guide closer to $13.5 billion would suggest that organic acceleration is not yet visible.

The second test is the new segment disclosure. If Network Security, Cortex and Identity are disclosed with enough detail to understand growth and margins, the loss of organic/inorganic disclosure may be manageable. If the segments are too broad to be useful, the market will apply a trust discount.

The third test is Prisma AIRS. Reaching $100 million of ARR is the first checkpoint. Following XSIAM toward several hundred million would be much more important.

The fourth test is platformization renewals. The company cites roughly 120% net retention and single-digit churn among platformized customers. The key is whether that reflects structural switching costs or promotional economics.

The fifth test is cash flow consistency. A real control-plane business should produce increasingly predictable free cash flow, not only strong Q4 collections.

The Bottom Line

In August 2025, we described Palo Alto as a company betting everything on enforcement authority. In February 2026, we said the bet was working operationally but getting more expensive financially. In June 2026, the world moved closer to Palo Alto’s architecture than we expected.

AI compressed time. That makes fragmentation more costly. It also makes Palo Alto’s broad enforcement footprint more valuable.

That is why we are more constructive on the strategic thesis.

But the proof is still ahead. Organic growth is good, not decisive. EPS growth is diluted. Chronosphere is concentrated. Cortex Cloud is still a drag. And the company is about to remove the cleanest window into organic acceleration.

The thesis is stronger. The evidence is better. The visibility is worse.

That combination rewards patience, not blind trust.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.