Ping An 4Q25 Earnings: The Number Nobody Watched

The RMB 8 billion buyback made the headlines, but the real story was CSM stabilization: the first sign in years that Ping An’s service-led model may be sustaining its backbook and lifting the ceiling

TL;DR

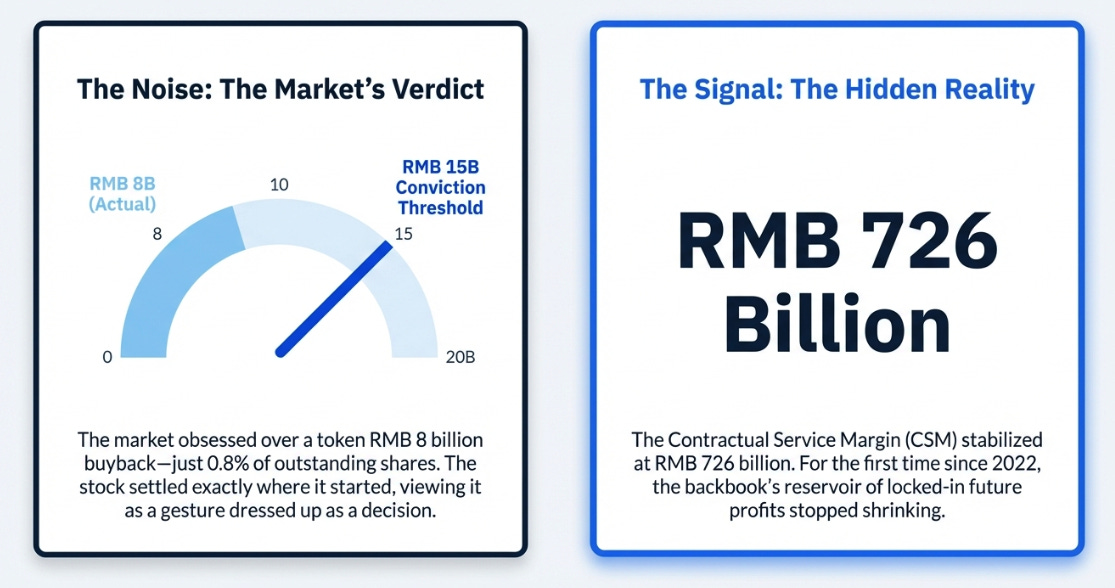

The market focused on Ping An’s RMB 8 billion buyback, but it was too small to signal real capital allocation conviction.

The more important development was CSM holding at roughly RMB 726 billion, the first time the backbook has stopped shrinking since 2022.

That shifts the thesis: Ping An no longer needs just a management catalyst, because the underlying operating model may have crossed into self-sustaining earnings growth.

Everyone was waiting for the buyback. The real story was hiding in the backbook.

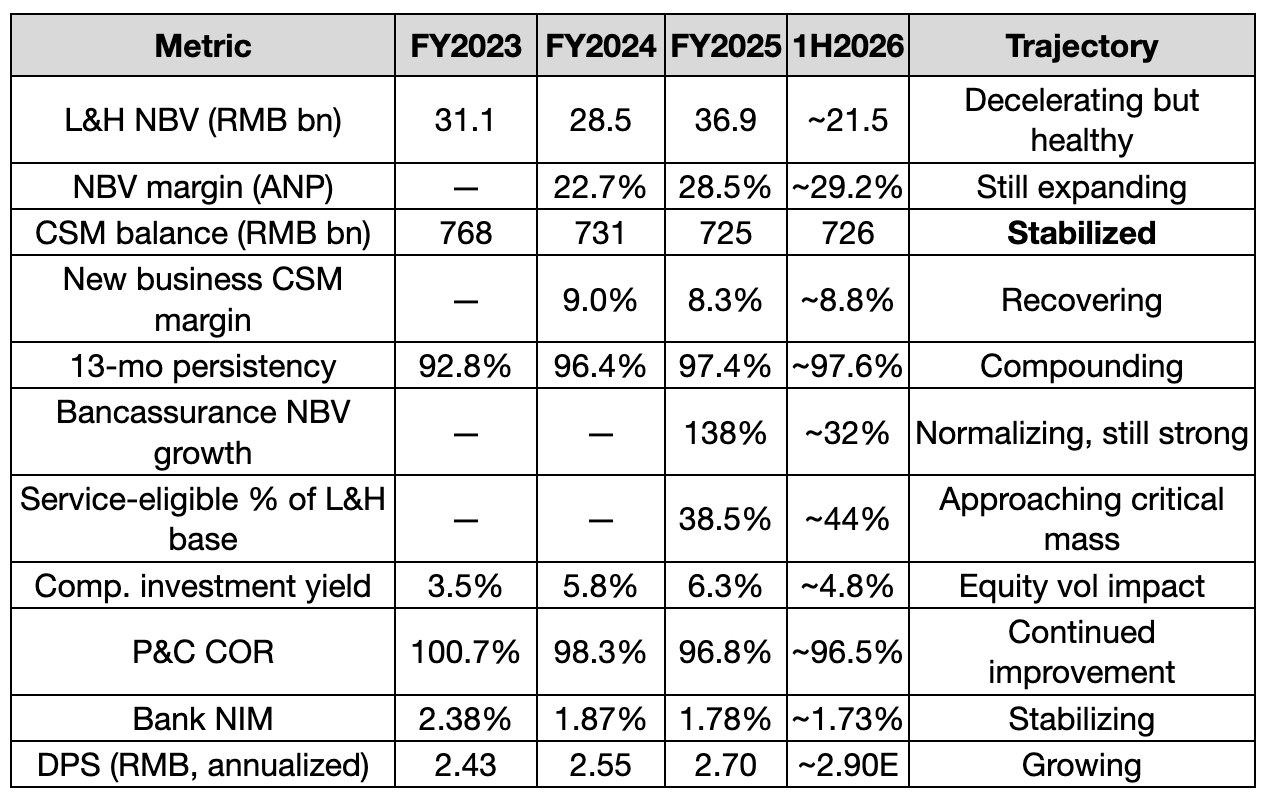

Ping An Insurance Group reported first-half 2026 new business value growth of 17.8%, a deceleration from the 29.3% pace of full-year 2025. The company announced an RMB 8 billion share repurchase program and disclosed that its contractual service margin stabilized at RMB 726 billion, the first period without decline in three years.

— Bloomberg News, August 2026

My first thought was: eight billion. That’s it.

For eighteen months I’ve argued that the single most important catalyst for Ping An’s stock was a buyback large enough to signal management conviction, RMB 15 billion or more, enough to tell the market that the people with the best information think the stock is cheap. Instead, management announced RMB 8 billion: not nothing, but not conviction either. A gesture dressed up as a decision.

The stock rose 3% on the day, gave it back within a week, and settled roughly where it started. The market’s verdict was clear: token. And I was ready to write that piece, the one about how Ping An keeps passing the test on operations and failing it on capital allocation.

Then I looked at the CSM line.

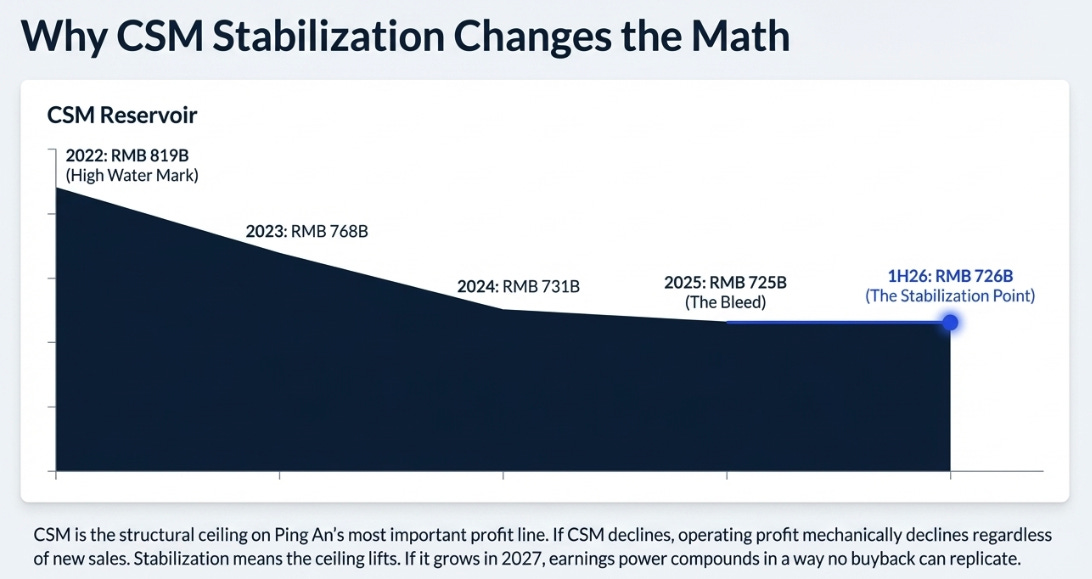

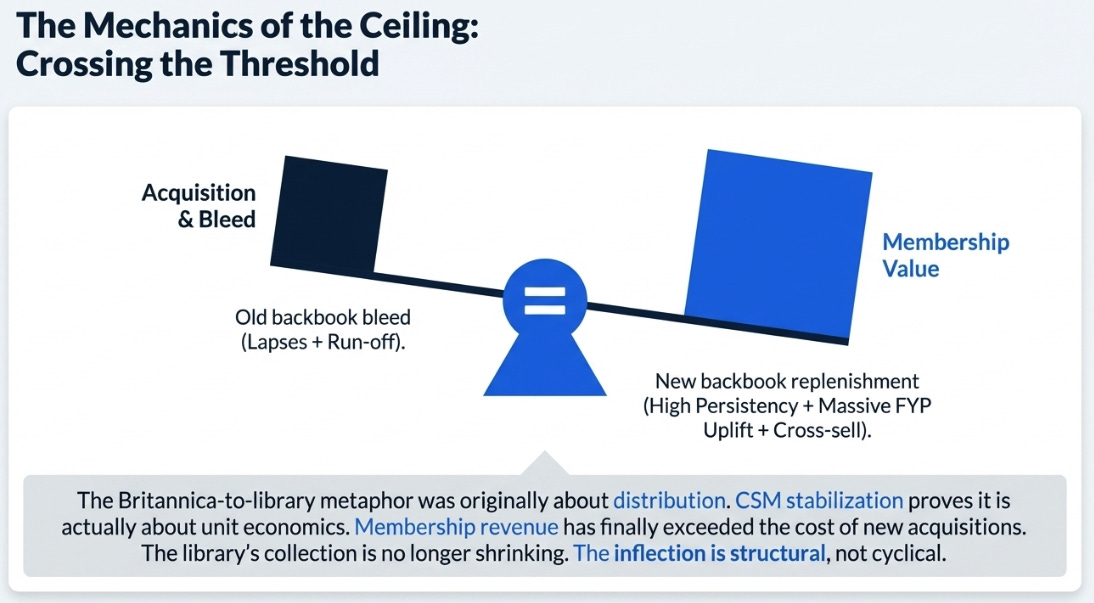

The contractual service margin, the backbook’s reservoir of locked-in future profits, came in at RMB 726 billion. That’s essentially flat versus the RMB 725 billion at year-end 2025. This sounds unremarkable. It is, in fact, the most important number Ping An has reported since the agent restructuring began, because it means the backbook has stopped shrinking for the first time since 2022.

The reason this matters more than the buyback is that CSM is the structural ceiling on Ping An’s most important profit line. The insurance service result, RMB 84 billion in FY2025, the single largest component of Life & Health operating profit, is mechanically driven by CSM releases. If the CSM keeps declining, that profit line declines with it, regardless of how fast NBV grows. If CSM stabilizes, the ceiling lifts. And if CSM starts growing again, Ping An’s earnings power compounds in a way that no buyback can replicate.

Everyone was watching the buyback. The real story was the backbook.

What We Said, and What Changed

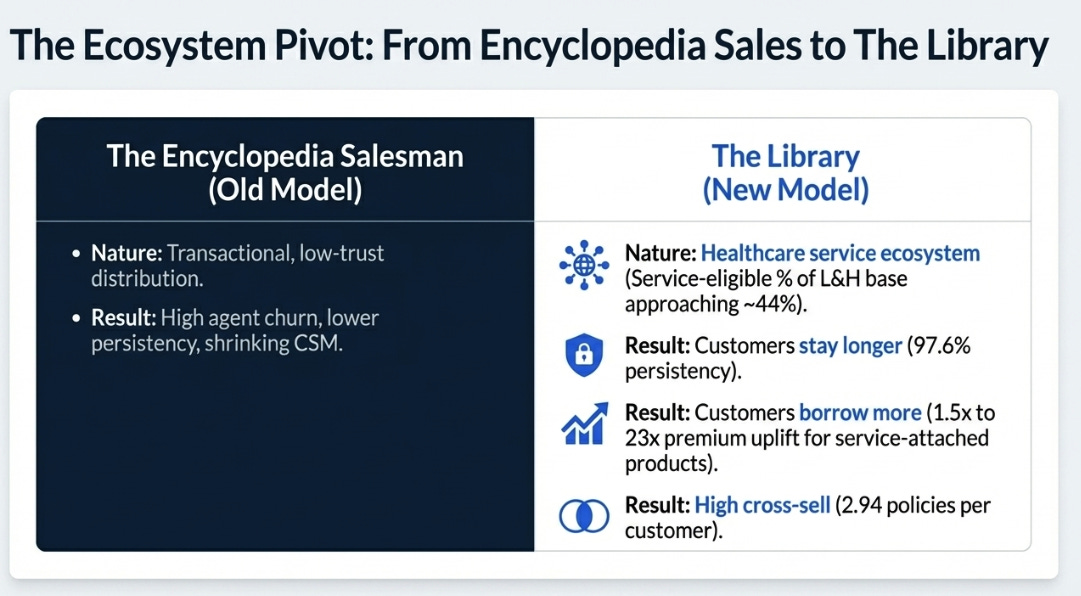

In January 2026, I wrote “The Trust Bundler,” arguing that Ping An’s collapsing agent force wasn’t a crisis but a strategy, the company was replacing expensive, low-trust distribution with a healthcare service ecosystem that created stickier, higher-value customer relationships. In March, after FY2025 results, I updated that thesis in “The Convertible Bond Test”: the operating model was proven (NBV +29.3%, persistency at 97.4%), but two new risks had emerged that I’d underweighted, the aggressive doubling of equity allocation to 19% of the portfolio, and management’s refusal to signal capital return conviction.

My framework was clear: the stock needed a catalyst, and that catalyst was capital allocation, not operations. I was half right. The operating improvement was necessary but insufficient for the stock. But I was wrong about what would make the operating improvement sufficient. I assumed it was a management decision, a buyback. What actually happened was more interesting: the operating improvement itself crossed a structural threshold. The service-attached products, which command 1.5x to 23x the premium of standard policies, finally reached enough scale to replenish the CSM backbook at roughly the rate it was being released.

Source: Company filings, author estimates for 1H2026.

The 17.8% NBV growth is a deceleration from 29.3%, and bears will seize on it. They’re missing the point. The NBV rate was always going to normalize, you can’t grow bancassurance 138% forever, and the agency channel’s productivity gains from culling weak agents are largely complete. What matters now is whether the quality of new business is good enough to sustain the backbook. For the first time, the answer appears to be yes.

Why CSM Stabilization Changes the Math

I need to explain why this matters mechanically, because it’s the kind of accounting detail that gets ignored in favor of flashier metrics.

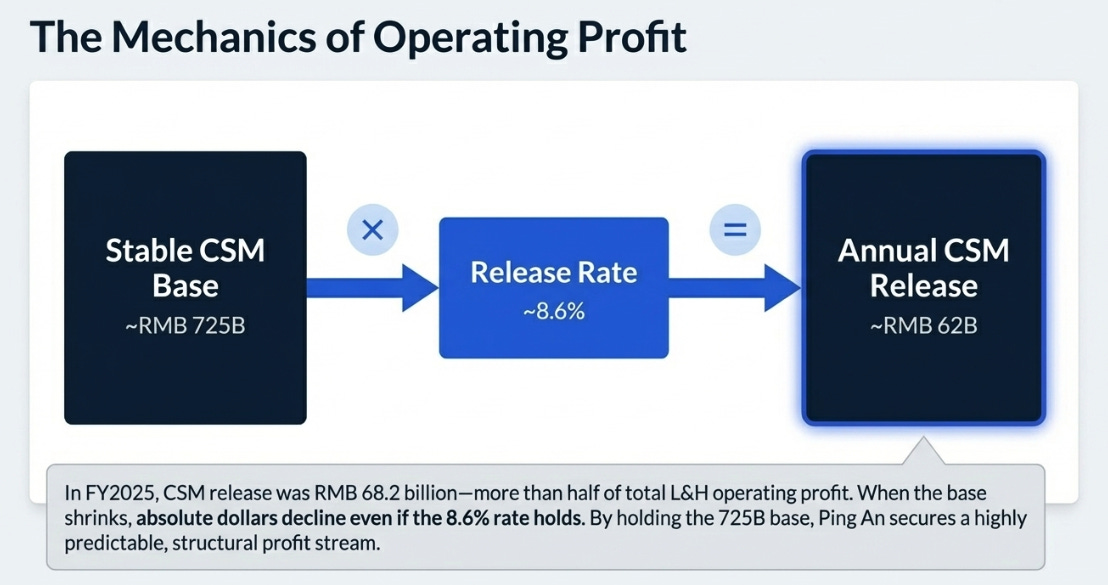

Ping An’s Life & Health operating profit comes from three sources: CSM release (the biggest), risk adjustment release, and investment service result. In FY2025, CSM release was RMB 68.2 billion, more than half of L&H operating profit. But the CSM balance had been declining for three straight years (RMB 819B → 768B → 731B → 725B), which meant the release base was shrinking. Even if the release rate held steady at ~8.6%, the absolute dollar amount would decline because the pool was getting smaller.

CSM stabilization reverses that dynamic. If the balance holds at ~RMB 725B and the release rate stays at 8.6%, annual CSM release is ~RMB 62B, a stable, predictable profit stream. If new business CSM margin recovers (8.8% in 1H26 vs. 8.3% in FY25, driven by higher-margin service-attached products), the balance could start growing again in 2027. That would mean the insurance service result, which declined 2.3% in FY2025, inflects to growth. And that inflection would be structural, not cyclical.

This is the connection to our original thesis that I didn’t fully articulate before. The Britannica-to-library metaphor was about distribution: replacing agents with services. But the CSM stabilization shows that the service model isn’t just changing how Ping An sells insurance, it’s changing the economics of what it sells. Service-attached products have higher persistency (97.6%), which means fewer lapses eating into the CSM. They have higher FYP (1.5x to 23x uplift), which means more CSM generated per policy. And they attract customers who buy more contracts (2.94 per customer, with 5-year customers holding 1.7x more), which means the cross-sell feeds back into backbook stability.

The library metaphor extends: the library isn’t just attracting more visitors. The visitors are staying longer, borrowing more books, and renewing their memberships at 97% rates. At some point, membership revenue exceeds the cost of new acquisitions. That point, I think, is now.

The Token and the Ceiling

So what about the buyback?

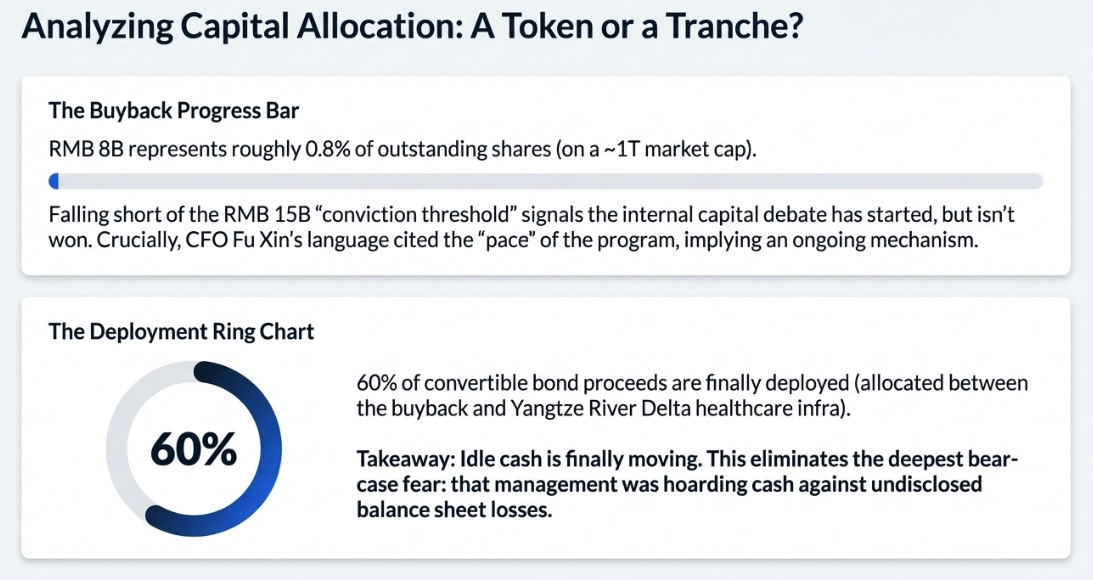

RMB 8 billion on a market cap of roughly RMB 1 trillion is 0.8% of shares outstanding. It’s better than nothing and worse than meaningful. For context, the threshold I set in March was RMB 15 billion, the amount that would signal genuine conviction rather than board-level box-checking. Eight billion signals that the capital return debate has started inside the company, but hasn’t been won.

The most important thing CFO Fu Xin said during the briefing was this: “We will evaluate the pace and scale of the repurchase program based on market conditions and regulatory considerations.” That’s boilerplate, but the word “pace” matters. It tells you management is framing this as an ongoing program, not a one-time event. The question is whether RMB 8 billion is the first tranche of something larger, or the entire commitment.

I lean toward the former, for one reason: the convertible bond proceeds are finally being deployed. Management disclosed that approximately 60% of the proceeds have been allocated, partly to the buyback, partly to a healthcare infrastructure investment in the Yangtze River Delta region. This isn’t the transformative hospital acquisition that would change the narrative overnight, but it’s directionally correct. Cash that was sitting idle for two years is moving. That’s new.

The stock’s muted reaction makes sense through this lens. The market wanted RMB 20 billion and got eight. But the market also got CSM stabilization and partial convertible deployment, two things that weren’t in anyone’s model. The net effect is that the base case got more probable and the bear case got less probable, without the bull case being triggered. That’s worth a modest re-rating over time, not a single-day pop.

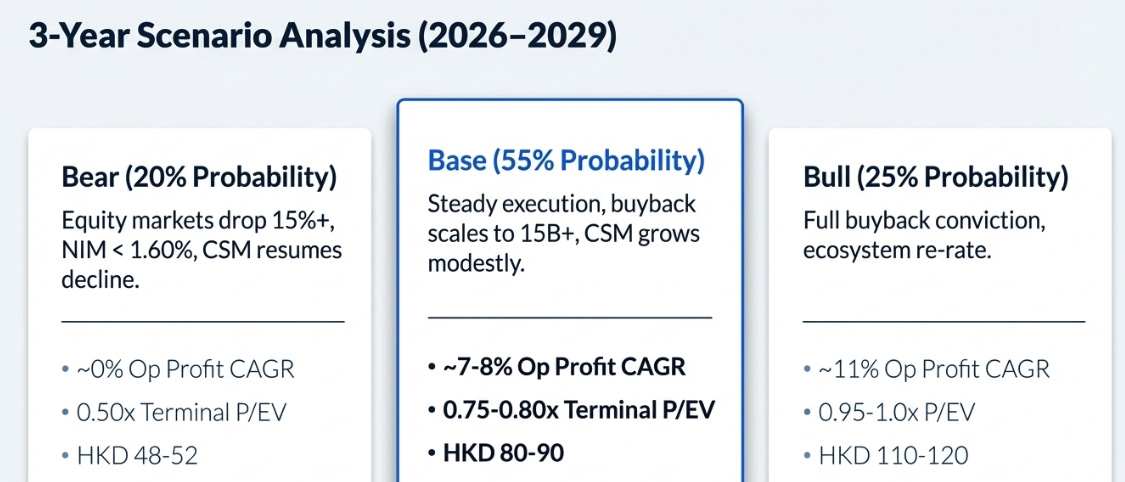

Three Years From Here

The value of scenario analysis is clarifying what you’re betting on, not pretending you can predict China’s equity market. Here’s how I think about Ping An from mid-2026 through mid-2029:

What changed since March: I’ve shifted roughly 5 percentage points from bear to base. The CSM stabilization removes the structural headwind I was most worried about. The partial convertible deployment, while underwhelming, eliminates the worst interpretation (that management was hoarding cash against undisclosed losses). The equity portfolio survived a volatile first half without forced de-risking.

The variant perception hasn’t changed in kind, but it’s sharpened in degree. Consensus still sees a cheap insurer with conglomerate complexity. I think the better frame is a service utility under construction, now showing its first evidence of self-sustaining economics in the backbook. The gap between these views is still the stock, but the evidence pile supporting the service-utility frame just got meaningfully heavier.

Probability-weighted, the expected three-year target is roughly HKD 85-90, or about 55-65% total return including dividends, approximately 16-18% annualized. That’s attractive for an income-generating position with improving fundamentals.

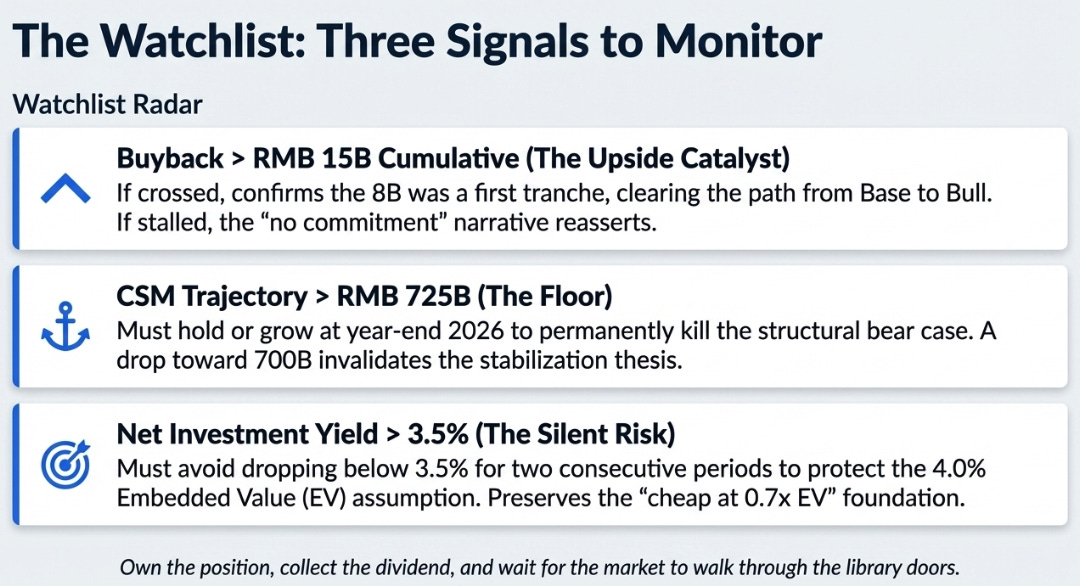

What I’m Watching

Three signals, in order of what they’d make me do:

Buyback scaling above RMB 15B cumulative, confirms that the RMB 8B was a first tranche, not a gesture. This is the clearest path from base to bull. If the buyback stalls at 8B through year-end 2026, the “management will never fully commit” narrative reasserts itself.

CSM trajectory at year-end 2026, if the balance holds above RMB 725B or grows, the structural bear case is dead. If it resumes declining toward RMB 700B, the 1H stabilization was a one-off, and the operating profit ceiling is still falling.

Net investment yield versus the 4.0% EV assumption, this remains the silent risk nobody has incentive to flag. If net yield stays below 3.5% for two consecutive reporting periods, the embedded value anchor needs to be rebuilt on a lower base, and every “cheap at 0.7x EV” argument loses its foundation.

The Library, Revisited

In January I wrote that Ping An was building a library to replace the encyclopedia salesman. In March I wrote that the library was open but management wouldn’t let shareholders use it. After this quarter, I’d put it differently.

The library is working. People are coming in, staying longer, and renewing their memberships at rates that would make any subscription business envious. The lending desk is finally staffed, if modestly. And for the first time, the rate of new book acquisitions is keeping pace with the rate of borrowing, the collection is no longer shrinking.

The stock still trades like a building with a “For Sale” sign on it. I think it’s becoming a franchise. The single thing that would make me more confident is a second buyback tranche by March 2027. The single thing that would make me less confident is the CSM resuming its decline. Until one of those happens, I own the position, collect the dividend, and wait for the market to walk through the door.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.