Rheinmetall 4Q25 Earnings: The Moat Got Deeper While We Weren't Looking

Customer prepayments solved the free cash flow debate and revealed a deeper advantage: governments are financing the industrial capacity they cannot replace.

TL;DR

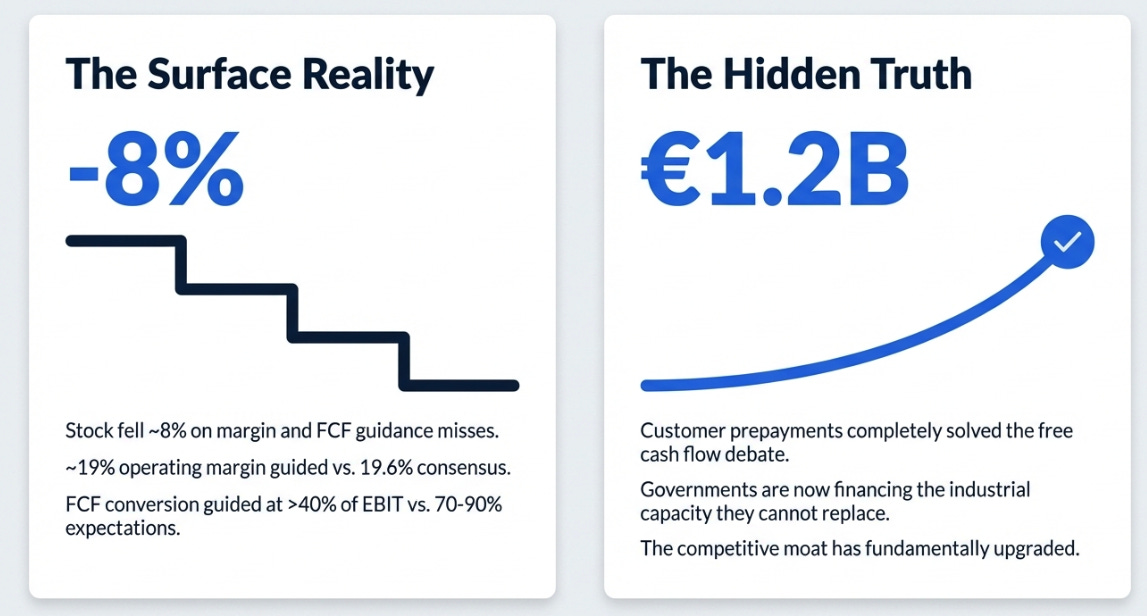

The FCF debate is closed. €1.2B of sovereign prepayments funded Rheinmetall’s working capital and flipped the balance sheet from €1.3B net debt to €369M net cash.

The moat upgraded. This is no longer just regulatory entrenchment, governments are pre-funding Rheinmetall’s expansion because the alternative is a capability gap.

The business improved, the valuation didn’t. The ceiling for the thesis rose, but at €1,542 (~40× FY26e EPS) the probability-weighted return is still ~8% annually.

Rheinmetall’s shares fell nearly 8% after the company’s 2026 outlook on profit margin and free cash flow came in below elevated expectations, with the ~19% operating margin guide below analyst consensus of 19.6% and free cash flow conversion guidance of more than 40% of EBIT well below the 70-90% some investors were looking for.,

Reuters, March 11, 2026

The Frame We Brought In

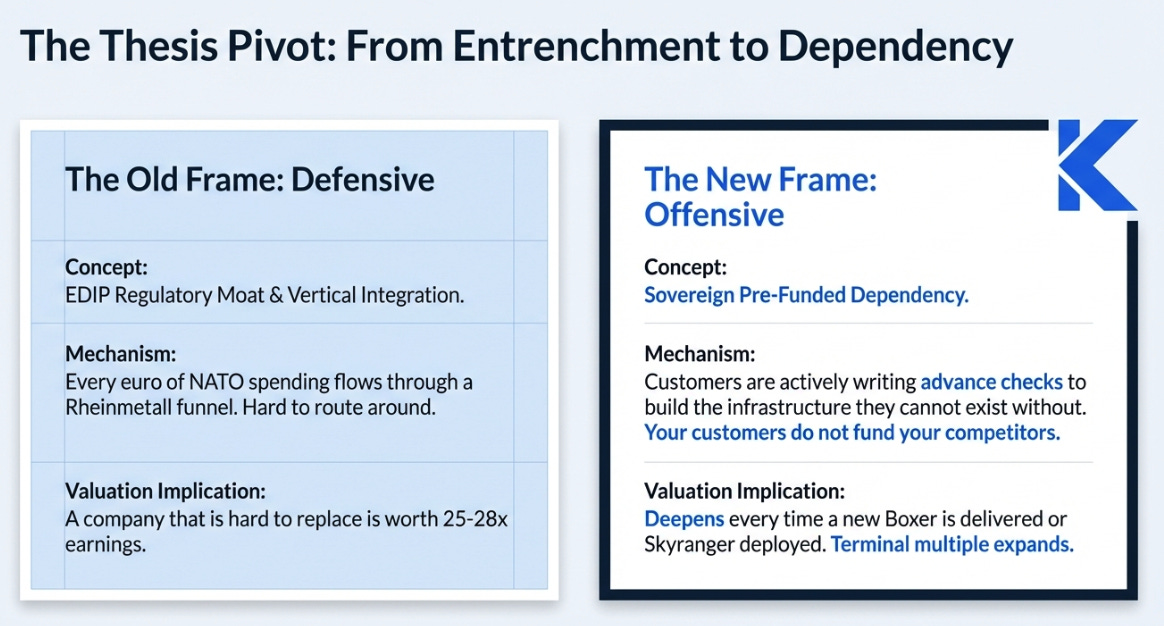

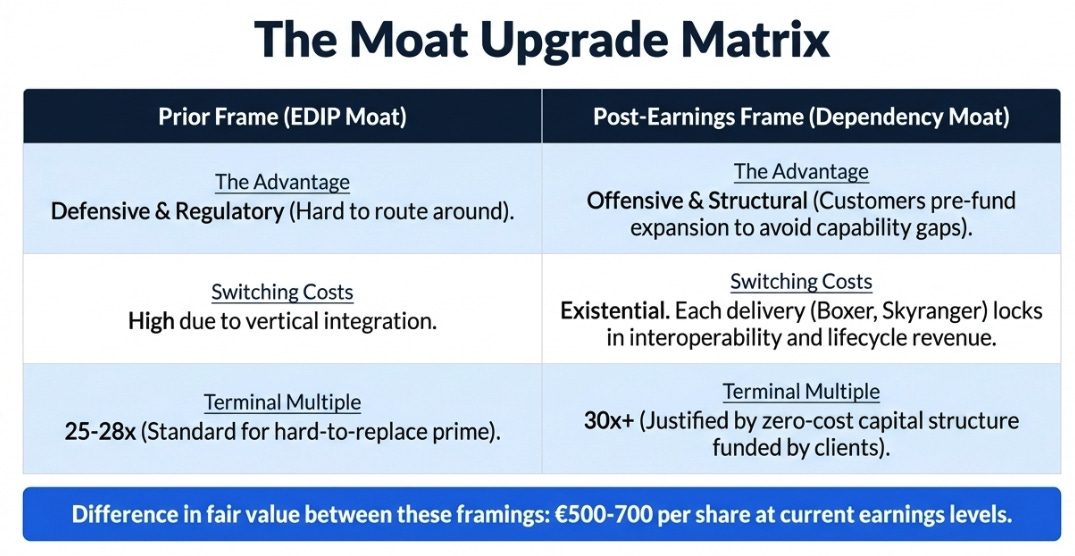

Coming into this print, the thesis rested on three pillars. First, Rheinmetall owned the only fully vertically integrated European defense production stack, from propellant through complete weapons systems, vehicles, electronics, and now naval, meaning every euro of NATO defense spending that had to be sourced in Europe flowed through a funnel where Rheinmetall was either prime contractor or mandatory subsystem supplier with no credible continental substitute. The EDIP regulatory framework and European sovereign-sourcing pressure made this entrenchment progressively harder to route around. Call it a regulatory moat with vertical integration on top.

Second, FCF was the unresolved question that could break the story. Through the first nine months of 2025, Rheinmetall had burned through €813M in operating free cash flow while posting record operating results. A company that converts 29% revenue growth and 18%+ operating margins into negative cash generation is either building something genuinely large or papering over structural weaknesses with accounting. We didn’t know which.

Third, €1,542 was full price for even a strong business. Our 5-year compounding analysis was blunt: at current prices, you needed the bull case for 15% CAGR. The high-certainty entry for that return on conservative assumptions was €700-870. We called it a strong business at full price, the kind of situation where you respect the quality and wait for the market to give you a better entry.

The central tension was this: a structurally compelling business case sitting inside a valuation that left no room for error. The question this quarter had to answer wasn’t whether demand was real. That debate was already won. The question was whether the mechanism, the actual source of Rheinmetall’s advantage, was as strong as we thought. It turned out to be stronger. And differently strong, which matters more.

What the Quarter Actually Resolved

The FCF question closes here, but the how matters more than the that.

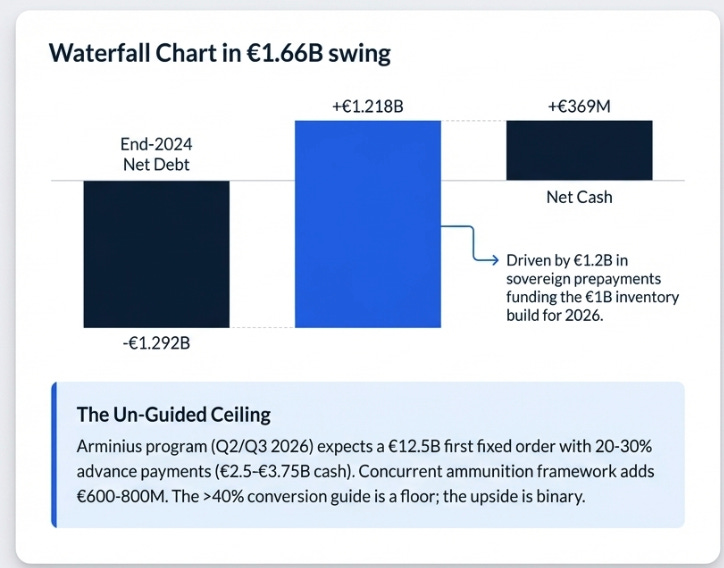

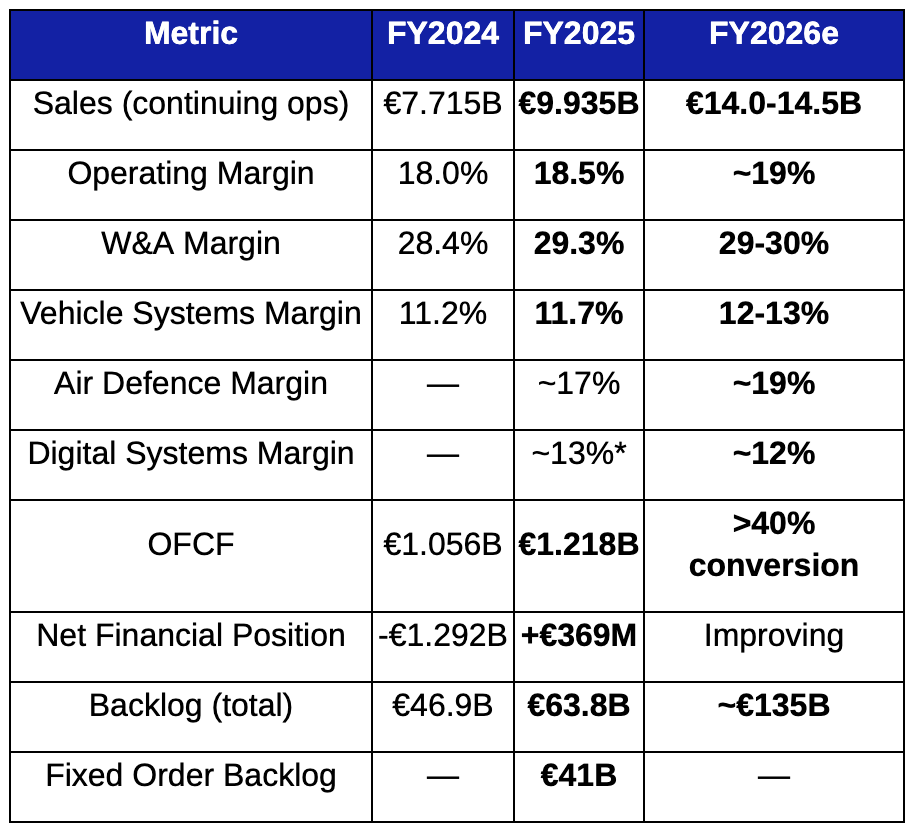

Full-year 2025 operating free cash flow came in at €1.218B. The net financial position, net debt of -€1.292B at end-2024, flipped to +€369M net cash. That’s a €1.66B swing in twelve months. The bear thesis needed a new argument before Q&A started.

But here is what the press release buried and the transcript revealed: €1.2B of customer prepayments essentially funded the entire €1B inventory build needed to execute 2026 orders. CFO Klaus Neumann was explicit: “the customer contributed €1.2 billion to our cash flow working capital improvement.” Rheinmetall didn’t generate cash by becoming more operationally efficient. It generated cash because sovereign governments with urgent capability gaps agreed to finance the factory expansion in advance.

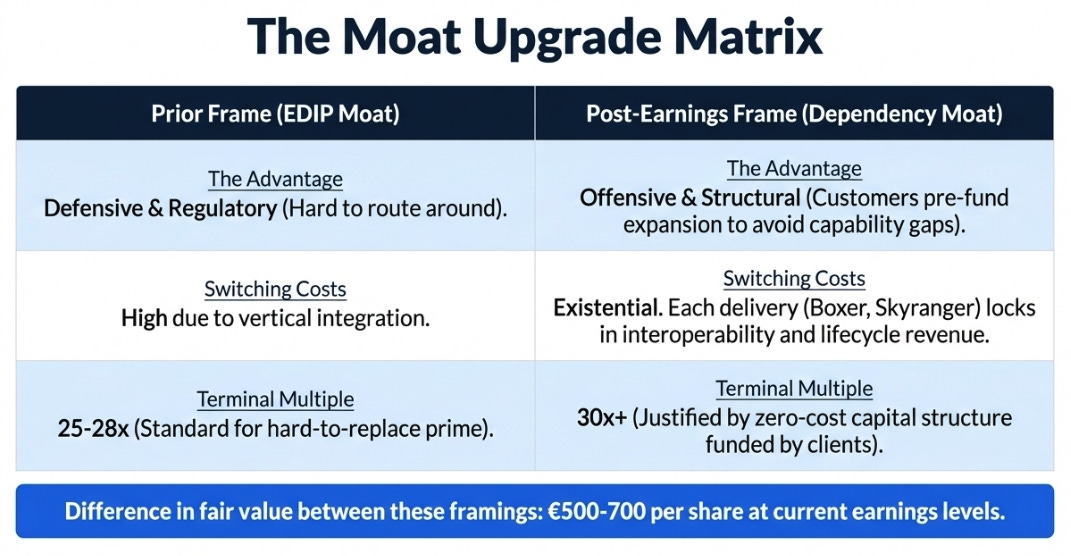

That is a qualitatively different mechanism from what the EDIP moat framing implied. A regulatory moat says: you can’t easily route around us. What this quarter revealed is something more offensive: our customers are writing advance checks to build the infrastructure they cannot exist without. The distinction matters because it changes the terminal multiple conversation. A company that is hard to replace is worth 25-28x earnings. A company whose customers pre-fund its own competitive moat, because the alternative is a capability gap they cannot accept, is worth more. Exactly how much more is the central question of the three-year scenario work below.

CEO Armin Papperger made the subtext explicit in Q&A. Pushed on cash conversion guidance of “>40% of EBIT”, well below the 70-90% some investors wanted, he said: if Arminius and the large ammunition contracts arrive with expected advance payments, “we must not longer speak about cash conversion rates.” That line deserves arithmetic, not just quotation. The Arminius program carries a first fixed order of approximately €12.5B expected in Q2/Q3 2026, with 20-30% advance payment terms under negotiation. That’s €2.5-3.75B in cash before Rheinmetall produces a single vehicle. The concurrent ammunition framework, 600-700K artillery rounds, another multi-billion contract, carries similar terms, another €600-800M. Combined: north of €4B in sovereign advance payments in a single quarter, against full-year 2025 OFCF of €1.218B. The “>40% guide” is a floor. The ceiling is deliberately unguided because the upside is binary and management knows it.

The prior frame, EDIP moat, was defensive. The correct frame after this quarter is offensive: your customers don’t fund your competitors.

The Weekend Nobody Had in Their Model

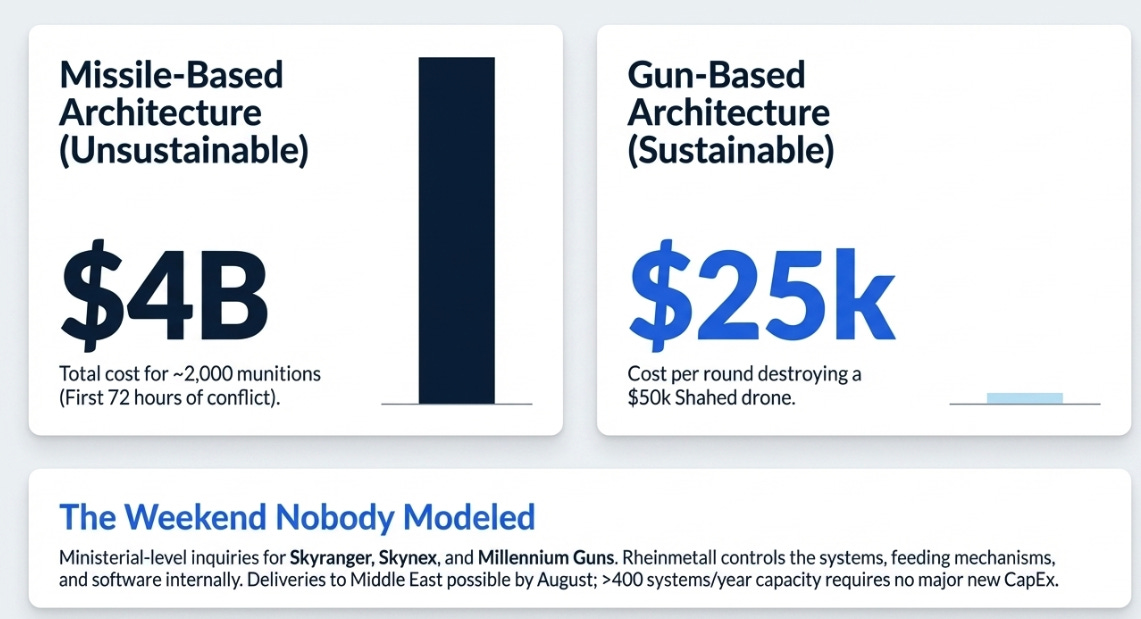

On the morning of this earnings call, Papperger had already spent his weekend taking ministerial-level phone calls from governments across Europe and the Middle East. Iranian attacks had triggered urgent inquiries about Skyranger, Skynex, and Millennium Gun platforms, gun-based air defense systems already deployed across Gulf states, proven effective against drone swarms at a fraction of the cost of missile-based alternatives.

The economics Papperger cited are not marginal. In the first 72 hours of the conflict, the US and its allies expended roughly 2,000 munitions at approximately $4B total cost. Against that, a gun-based system shooting down a $50,000 Shahed drone with a $25,000 round isn’t just arithmetic, it’s a doctrine change. The Western world built its air defense architecture around missiles. The cost curve of drone warfare has made that architecture financially unsustainable at scale. Rheinmetall, which has been producing gun-based air defense systems for 25 years, is the primary industrial beneficiary of that realization.

And because Rheinmetall controls the weapons systems, the feeding mechanisms, and increasingly the fire control software internally, it can scale faster than any competitor relying on external subcomponents. Papperger confirmed that deliveries to the Middle East are possible by August, systems already in production, without signed contracts. He also stated that expanding beyond 400 systems per year doesn’t require significant additional investment given the level of internal integration. “There is more in,” he said of the Air Defence guidance, and he said it twice.

The Air Defence segment was guided at €0.9-1.0B for 2026 at approximately 19% margin. I think that number is the most deliberately understated line in the entire guidance package, and it’s understated for the right reason, Rheinmetall doesn’t yet have signed contracts from the weekend’s conversations. When those contracts arrive, they will be incremental to a guidance figure already set as a floor.

This matters for the prior thesis in a specific way. Every scenario we built before this quarter was anchored to European rearmament as the demand driver. The Middle East development isn’t a replacement for that thesis, European sovereign urgency is still the structural base. It’s an additional demand vector that operates on its own logic, its own timeline, and its own contract structure. Our prior TAM assumption was too narrow, and the Air Defence segment is where that error shows up most directly in the numbers.

What the Segment Restructuring Is Really Saying

Rheinmetall introduced a five-segment reporting structure effective January 1, 2026: Vehicle Systems, Weapon and Ammunition, Digital Systems, Air Defence, and Naval Systems. This is not cosmetic.

Under the old Electronic Solutions umbrella, it was structurally impossible to evaluate whether Rheinmetall’s digitization narrative, TaWAN, Battlesuite, D-LBO, the tactical core, was generating real economics or just large one-time project revenue dressed in platform language. Now Digital Systems and Air Defence have standalone P&Ls that management must defend every quarter. The platform narrative now has accountability attached to it, which is exactly what a sophisticated investor should want and exactly what management should be willing to provide if the economics are real.

One important nuance that Reuters and most initial sell-side coverage missed entirely: a €48M one-time divestment gain was embedded in the 2025 Electronic Solutions numbers, surfaced only because Warburg Research pushed on it in Q&A. Strip that out and the 2026 Digital Systems margin guide of ~12% represents essentially flat underlying performance rather than the compression the headline implies. Papperger was direct about the why: F-35 integration, satellite programs, and drone capacity are running costs ahead of their associated revenues. Digital Systems in 2026 is absorbing setup costs for programs that should generate revenue at materially higher margins from 2027-2028. The segment margin guide isn’t deterioration. It’s the income statement signature of deliberate investment front-loading.

*Includes €48M one-time divestment gain; underlying ~12%

The margin line deserving the most attention is Weapon and Ammunition at 29.3% for the full year. The Q3 2025 result of 23.2% had rattled bulls, it was the first genuine evidence that the ammunition scarcity premium might be normalizing as new European capacity came online. The full-year recovery to 29.3%, with 29-30% guided for 2026 knowing that capacity is expanding, closes that debate definitively. Management is guiding the same range for 2026 with full visibility into competitor capacity additions. That is not what margin normalization looks like.

One additional item that deserves mention precisely because it was asked about directly and explained clearly: Vehicle Systems Q4 margin came in light. The reason, per Papperger, was specific and structural, approximately twelve heavy weapon carriers completed and sitting in the yard because the German MoD lacked capacity to perform final acceptance checks. Software issue on one vehicle variant, now resolved. Neither is a manufacturing problem. Both represent deferred Q1 2026 revenue rather than lost revenue. Without that explanation, a reader of the press release would see a soft Q4 Vehicle Systems result and have no framework for interpreting it. The transcript is where this became clear.

What the Upgraded Moat Is Worth, and What We Still Can’t See

Let me be precise about what changed and what didn’t, because conflating the two leads to the wrong investment conclusion.

What changed: The moat framing. The prior thesis described EDIP regulatory entrenchment as the primary competitive advantage, a defensive position that made Rheinmetall hard to route around. The correct post-earnings framing is more aggressive: Rheinmetall’s sovereign customers are pre-funding its expansion because the alternative, a capability gap they cannot remedy on any acceptable timeline, is worse than writing the check. That shifts the quality of the advantage from regulatory to structural dependency. It also shifts the terminal multiple conversation. A regulatory moat erodes when regulations change. A dependency moat deepens every time a new Boxer is delivered, a new Skyranger deployed, a new D-LBO software integration completed, because each event increases switching costs, extends lifecycle revenue, and makes the operational interoperability argument for the next procurement cycle. The difference between these two framings is approximately €500-700 in fair value at current earnings levels, which is material when you’re deciding whether €1,542 is full price or merely full price for the old frame.

What didn’t change: The valuation concern. The stock is at €1,542 against the same earnings base we were analyzing before the print. The multiple absorbed most of the good news in real time, which is what a market-cap-weighted momentum vehicle at 40x forward earnings does when a strong print confirms but doesn’t dramatically exceed consensus. The probability-weighted expected return from here is approximately 8% annually. Unexciting for the complexity and binary risk carried. The high-certainty entry for 15% annual compounding remains €900-1,100. The upgraded thesis raises the ceiling. It does not lower the entry.

What we still can’t see: The platform narrative remains unverified by financials. Management talks convincingly about TaWAN, Battlesuite, and the tactical core. But the reporting still provides no software or services revenue split, no attach rate, no lifecycle revenue per platform, and no recurring-economics bridge for Digital Systems. The segment structure improvement is genuine. The accountability gap is real. If by Q3 2026 Digital Systems is still reporting only project revenue with no platform-specific KPIs, the narrative is running materially ahead of the economics, and the 38x terminal multiple in the bull case needs revisiting.

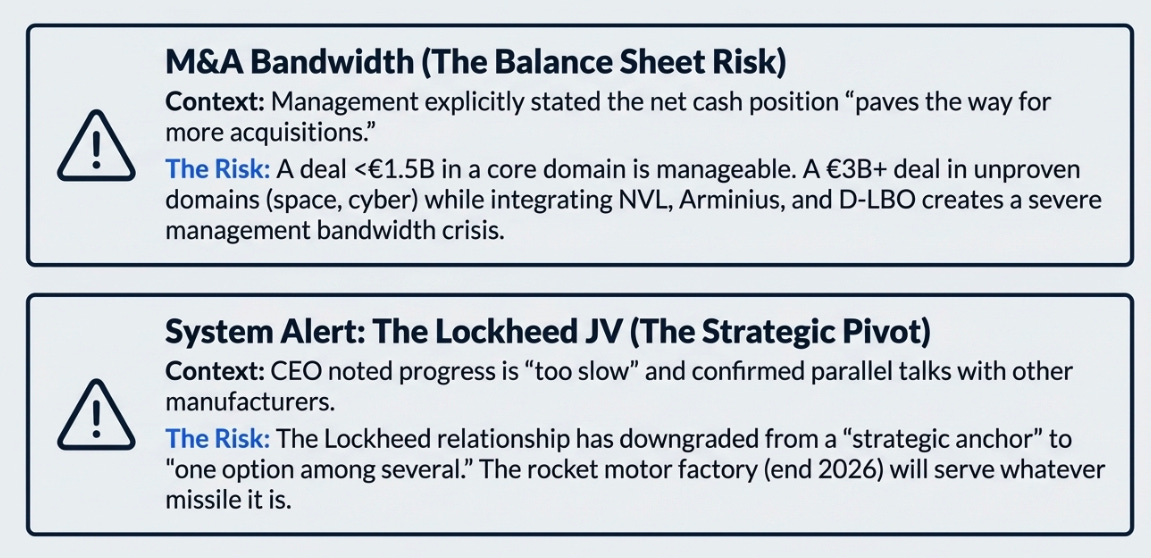

Two additional risks became louder this quarter rather than quieter. First, M&A: the net cash position and Papperger’s explicit statement that the balance sheet “paves the way for more acquisitions” means this is an active risk, not a theoretical one. One manageable deal under €1.5B in a core domain is fine. A €3B+ deal in an unproven domain, space, cyber, commercial logistics, while simultaneously integrating NVL, executing Arminius, and ramping D-LBO is a management bandwidth problem that sits at the center of the bear case. Second, the Lockheed JV: Papperger was unusually candid, “I must say it’s too slow”, and confirmed parallel conversations with other missile manufacturers. The rocket motor factory, qualifying end of 2026, will serve “whatever missile it is.” The Lockheed relationship has moved from strategic anchor to one option among several. That’s a disclosure change worth tracking.

Three Years, Three Scenarios

The thesis upgrade has a price tag, and the question is whether you’re paying for the old thesis or the new one. Three years gets us to end-2028, when major capacity investments are substantially complete, D-LBO and TaWAN are either generating recurring revenue or they aren’t, NVL is integrated, and the Arminius first tranche is in full delivery. By then you know which thesis was right.

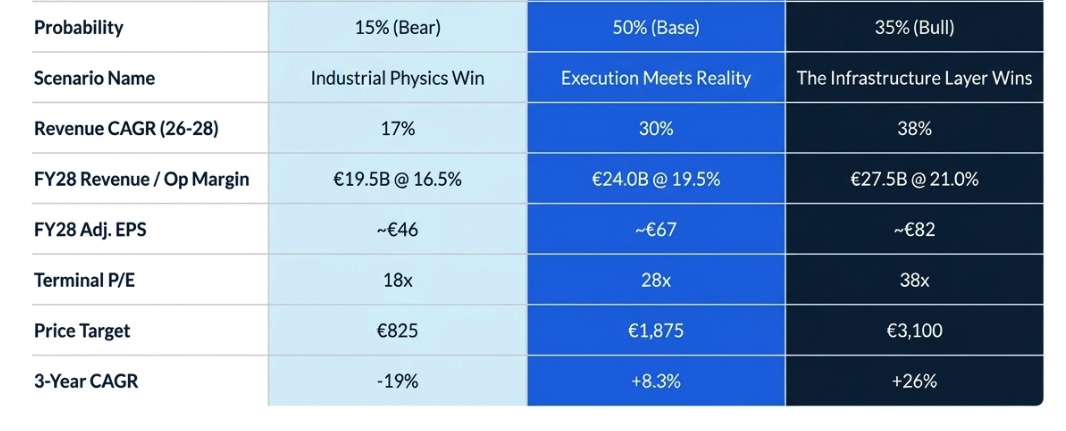

Bull case, 35% probability: “The Infrastructure Layer Wins”

Arminius closes Q2 2026 with full prepayments. Middle East air defence orders add €500M+ incrementally to guidance. W&A margin holds 29-30%, new capacity absorbed by growing demand, not normalization. Digital Systems scales to €3.5B+ at 15%+ margin as D-LBO and TaWAN convert to recurring economics; management begins disclosing platform-specific metrics that justify a re-rating. NVL frigate orders arrive. US optionality, XM30, howitzer, Navy, converts partially, none of it currently in the business case. One manageable M&A deal. No dilution.

FY2028 revenue reaches €27.5B at 21% operating margin. Adjusted EPS approximately €82. At 38x, justified if Digital Systems recurring revenue is visible, US exposure has partially converted, and the sovereign prepayment model is proven durable, the stock is worth €3,100. Adding approximately €110 in cumulative dividends over three years, total return is roughly 107%, or 26% annually from today’s price.

Base case, 50% probability: “Execution Meets Reality”

Arminius slips to Q3 on German procurement timing. W&A margin drifts modestly to 27-28% as European capacity expands, the scarcity premium partially but not fully normalizes. Middle East adds incrementally, not transformatively. Digital Systems stays in investment mode; recurring revenue visible but below 10% of segment by 2028. NVL integrates successfully but synergies remain a 2030 story. One manageable M&A deal, €1-2B range. FCF conversion of 55-65%, prepayments real but lumpy.

FY2028 revenue reaches €24B at 19.5% operating margin. Adjusted EPS approximately €67. At 28x, appropriate for a high-quality defense prime with growth decelerating toward 20-25% annually and no proven platform re-rating, the stock reaches €1,875. Total return including dividends approximately 27%, or 8.3% annually. Serviceable, but at this valuation you are not being paid for the complexity or the binary risks you’re carrying.

Bear case, 15% probability: “Industrial Physics Win”

Arminius slips into 2027 on German parliamentary budget disputes. W&A margin normalizes to 22-24% as KNDS, Hanwha, and BAE capacity erodes the scarcity premium faster than demand grows. Digital Systems disappoints, integration costs persistent, D-LBO delayed past contract milestones. A large dilutive acquisition in 2026-2027 spreads management thin across too many simultaneous programs. Ukraine ceasefire in 2027 triggers a 20-25% sector-wide de-rating as European governments reprioritize. Net cash position consumed by M&A, FCF normalization delayed.

FY2028 revenue reaches €19.5B at 16.5% operating margin. Adjusted EPS approximately €46. At 18x, full normalization to mature European industrial multiple, the range where BAE Systems and Leonardo trade in a normalized cycle, the stock reaches €825. Total return including dividends approximately -40%, or -19% annually.

Upside/downside ratio: approximately 2.5:1. The asymmetry is real. But at €1,542, 40x FY2026e EPS, you are already paying for base-to-bull execution. The probability-weighted expected return of ~8% annually is unexciting for a stock carrying geopolitical binary risk at a growth multiple. The high-certainty entry for 15% CAGR is €900-1,100, unchanged from before the print. What changed is the ceiling. The bull case got higher because the mechanism got stronger. The entry requirement did not.

What to Watch

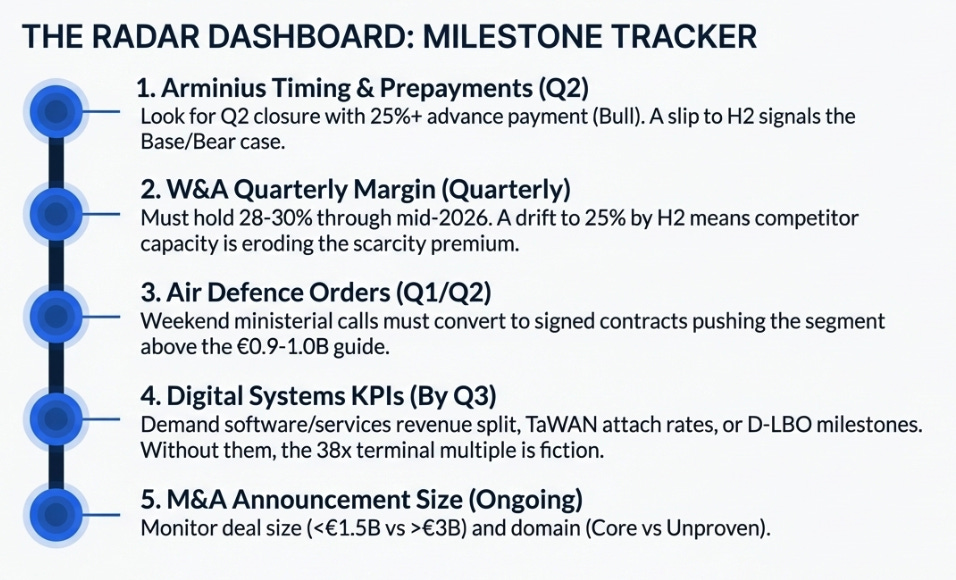

Five signals, each observable before annual results confirm them.

Arminius timing and prepayment rate. The single most important event of 2026. Q2 closure with 25%+ advance payment is the bull signal, and the arithmetic is dramatic enough that it will be visible in the Q2 OFCF number before management formally announces anything. A slip to “H2” in management language is the tell that the base case is becoming the bear case. Watch specifically for any change from “Q2/Q3” to vaguer calendar framing in Q1 results commentary.

W&A quarterly margin. The most important operational number in the entire portfolio. If it holds 28-30% through mid-2026 as new capacity comes online, the scarcity premium is structural and the bear case on margin normalization is losing. A drift toward 25% by H2 2026 means competing European capacity is arriving faster than demand is absorbing it. This one number, tracked quarterly, separates the bull from the base case more reliably than any other metric.

Air Defence order announcements. The weekend’s ministerial conversations should convert to signed contracts in Q1/Q2 2026 if the demand is real. If the segment is tracking above the €0.9-1.0B full-year guide by Q2 earnings, the Middle East vector has confirmed. If not, the phone calls were exploration. Papperger’s credibility on this specific claim is high, he was specific about August delivery timelines on systems already in production, which makes non-confirmation a meaningful signal rather than routine guidance conservatism.

Digital Systems KPI disclosure. The segment exists as a standalone entity starting January 1, 2026. This is its first full year of accountable reporting. By Q3 2026, any sophisticated investor should expect at least a directional disclosure of software or services as a percentage of segment revenue, or a first TaWAN attach rate, or a D-LBO vehicle completion milestone number. If by year-end 2026 the Digital Systems disclosure still contains only revenue and margin with no platform-specific metrics, the narrative is running ahead of the economics and the 38x terminal multiple assumption in the bull case requires a significant haircut.

M&A announcement size and domain. Papperger said explicitly the balance sheet “paves the way for more acquisitions.” The question is not whether another deal comes, it almost certainly will. The question is whether it is additive or dilutive to the thesis. Under €1.5B in a core domain with clear integration rationale: manageable, track the integration execution. Above €3B, or in an unproven domain while simultaneously integrating NVL and executing Arminius: the bear case just got more probable, and the position sizing conversation changes.

What Changed

The prior thesis was: Rheinmetall has a regulatory moat, FCF is the unresolved question, and the stock is full price for a strong business.

The current thesis is: the FCF question is closed, and what it revealed underneath is more durable than a regulatory moat. Rheinmetall’s sovereign customers are pre-funding their own dependency on its industrial capacity. The Middle East development extends that dependency globally before the European thesis has even fully converted. The company is becoming mandatory infrastructure for rearmament, not because it lobbied for the right regulations, but because no alternative exists at the scale and breadth required, and the cost of a capability gap has become politically unacceptable.

That thesis has a higher ceiling than the prior one. The bull case at €3,100, 26% annual compounding, was not available under the EDIP moat framing. It is available under the sovereign dependency framing, but only if Digital Systems converts its narrative to recurring economics, W&A margins prove structural rather than cyclical, and Arminius arrives with the prepayments management has effectively promised.

The entry price has not changed. The high-certainty entry remains €900-1,100. At €1,542 the market has already partially priced the thesis upgrade. What you’re deciding today is whether the remaining upside, the difference between the base case at €1,875 and the bull case at €3,100, is worth the binary risks you’re carrying at a 40x multiple.

Papperger closed the call with a line that was either corporate modesty or strategic confidence: “We are responsible for the performance. You are responsible for the share price.” My read is that he believes the business has already made the harder argument, that the mechanism is proven, the demand is funded, and the industrial capacity is being built on the sovereign customer’s advance payment. The question for investors is whether you are paying for the argument or waiting for the proof.

At €1,542, you are paying for most of the argument. The proof arrives quarterly. The first test is Q2 2026, when Arminius either closes or it doesn’t. Everything else follows from that.

Disclaimer:

The content does not constitute any kind of investment or financial advice. Kindly reach out to your advisor for any investment-related advice. Please refer to the tab “Legal | Disclaimer” to read the complete disclaimer.